Data Quality Tools Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

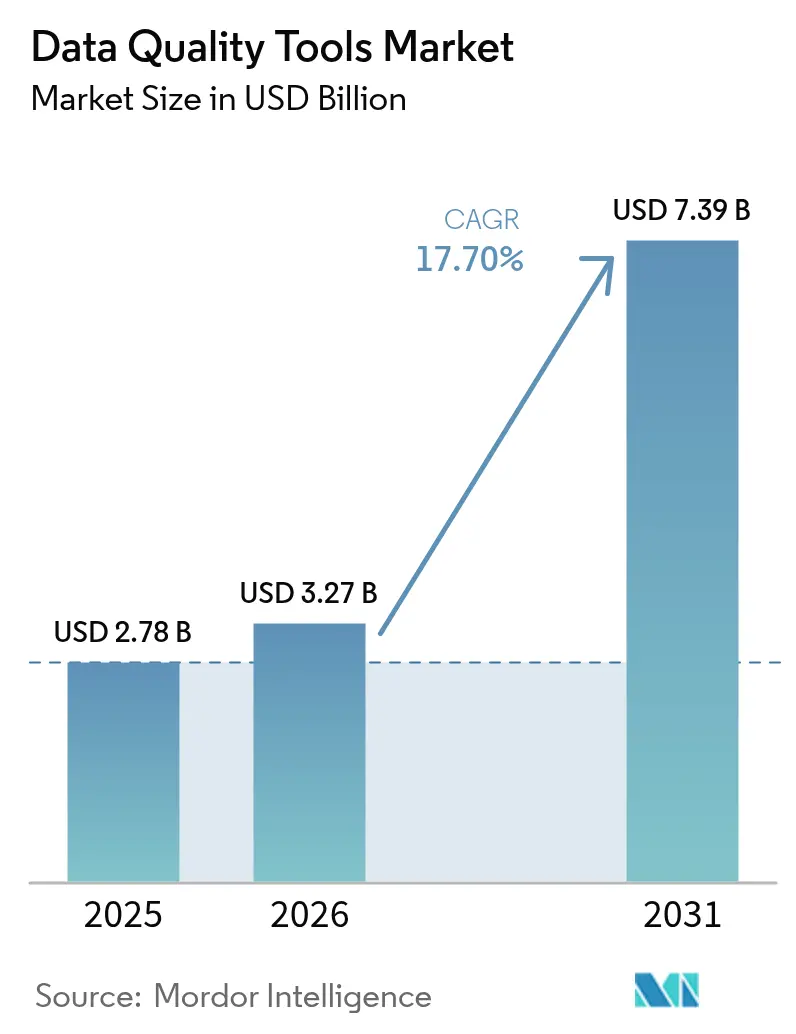

| Market Size (2026) | USD 3.27 Billion |

| Market Size (2031) | USD 7.39 Billion |

| Growth Rate (2026 - 2031) | 17.70% CAGR |

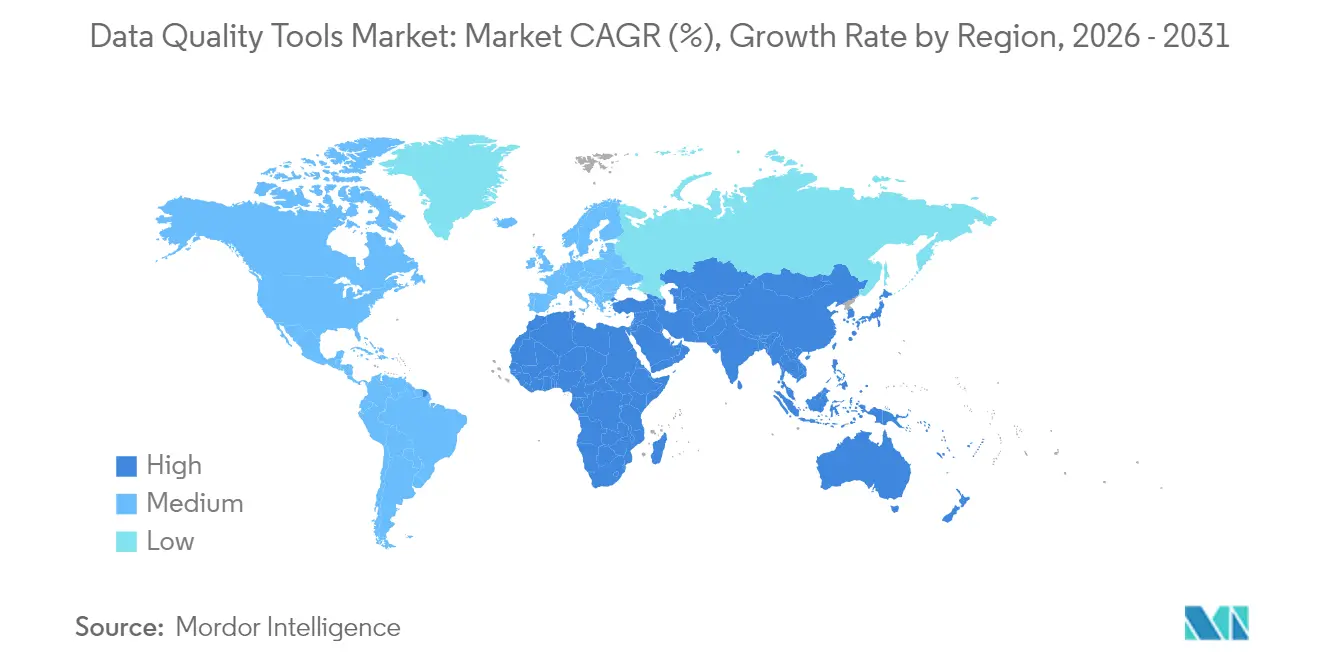

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Data Quality Tools Market Analysis by Mordor Intelligence

The data quality tools market size is expected to grow from USD 2.78 billion in 2025 to USD 3.27 billion in 2026 and is forecast to reach USD 7.39 billion by 2031 at 17.7% CAGR over 2026-2031. Escalating regulatory scrutiny, rapid cloud adoption, and the surge in real-time analytics have positioned high-quality data as a non-negotiable asset. Enterprises are pairing data quality initiatives with AI deployments because model accuracy depends on clean, reliable data. Demand is strongest for cloud-ready platforms that integrate with data lakes and low-code workflows, helping firms offset shortages of specialist talent. Vendor focus has shifted toward automated anomaly detection, predictive cleansing, and domain-specific rules that accelerate implementation in sectors such as BFSI, retail, and healthcare.

Key Report Takeaways

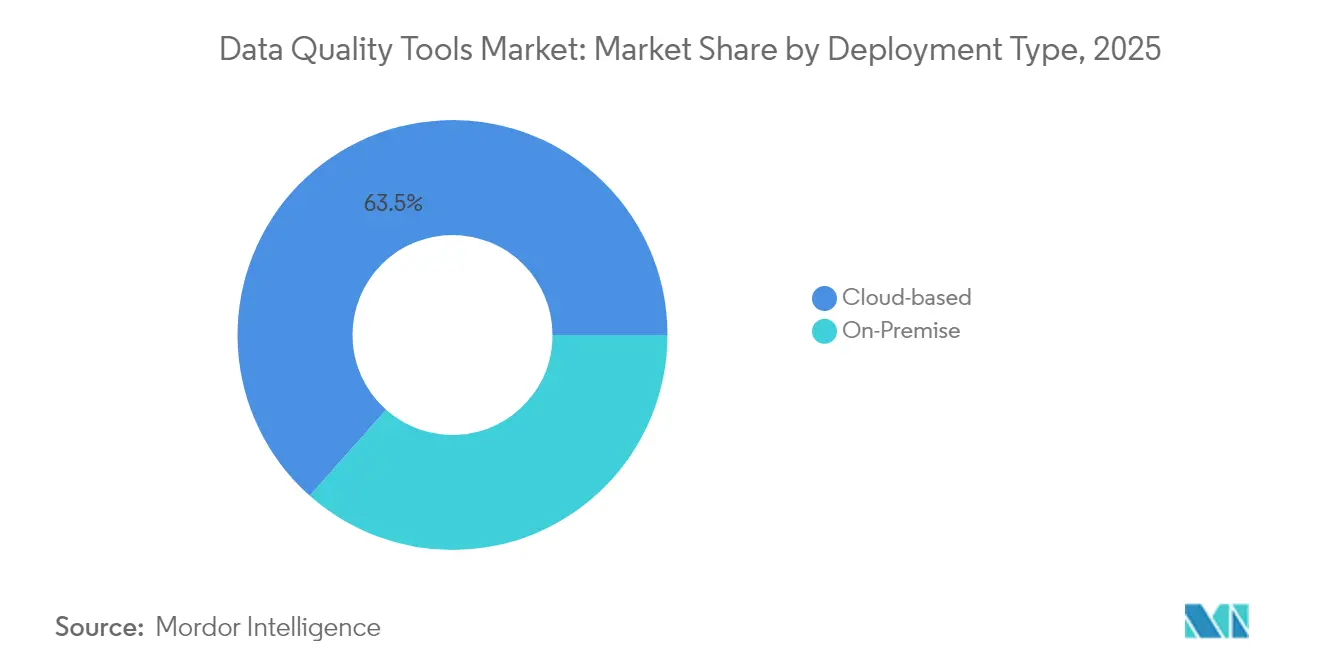

- By deployment type, cloud solutions held 63.45% of the data quality tools market share in 2025 and are expanding at a 19.8% CAGR through 2031.

- By organization size, large enterprises commanded 57.30% share of the data quality tools market size in 2025, while SMEs are growing at 18.9% CAGR to 2031.

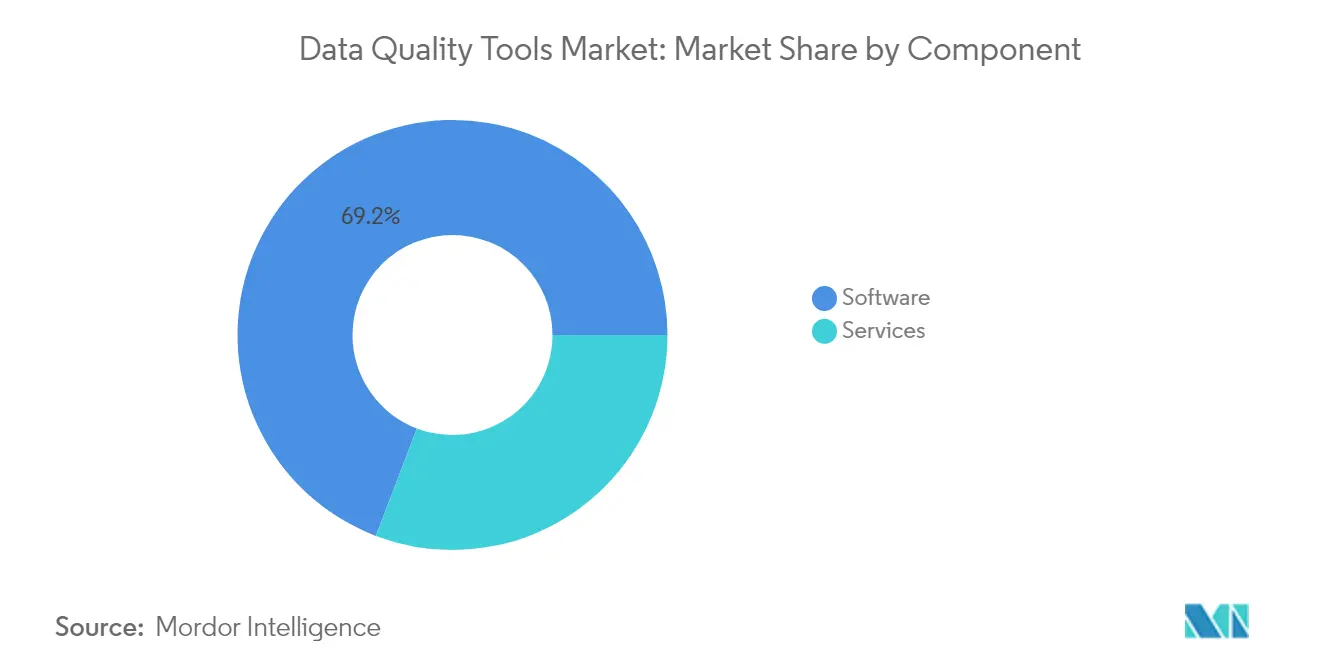

- By component, software led with 69.20% revenue share in 2025; services are advancing faster at an 18.2% CAGR through 2031.

- By data domain, customer data captured 39.40% of the data quality tools market share in 2025; product data is projected to grow at 20.9% CAGR.

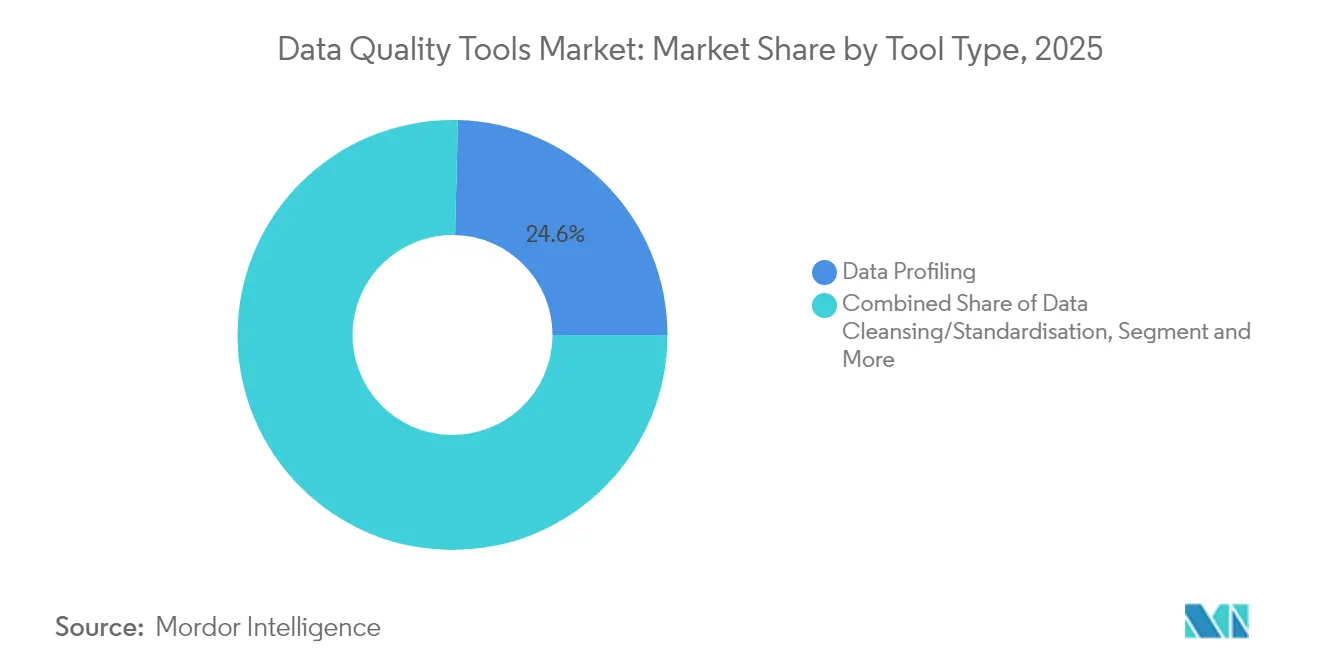

- By tool type, monitoring and alerting solutions are forecast to post the highest 22.0% CAGR, outpacing data profiling’s 24.60% share baseline.

- By end-user vertical, BFSI accounted for 22.70% share in 2025; retail and e-commerce is the fastest-growing segment at 23.1% CAGR.

- By geography, North America dominated the market with a 35.70% share in 2025, while Asia-Pacific is emerging as the fastest-growing region with a projected CAGR of 21.7% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Data Quality Tools Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerated Migration of Core Banking Platforms to Cloud Driving High-Volume Data Remediation Projects in North America | 4.5% | North America, with spillover to Europe | Medium term (2-4 years) |

| Intensifying ESG-Reporting Mandates in Europe Necessitating Enterprise-Wide Data Quality Controls | 3.2% | Europe, North America, expanding to APAC | Long term (≥ 4 years) |

| AI-Driven Customer 360 Initiatives Boosting Spend on Data Profiling and Matching Tools Across APAC Retail | 2.8% | APAC, North America, Europe | Medium term (2-4 years) |

| Real-Time Fraud-Detection Pipelines in BFSI Catalysing Demand for Streaming Data Quality Engines | 2.1% | Global, with concentration in North America and Europe | Short term (≤ 2 years) |

| Vendor-Native Automation Plug-Ins Reducing Total Cost-of-Ownership for SaaS Workloads | 1.8% | Global, with early adoption in North America | Short term (≤ 2 years) |

| Healthcare Interoperability Rules (US and EU) Accelerating FHIR-Compatible Data Cleansing Solutions | 1.4% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Accelerated Migration of Core Banking Platforms to Cloud Driving High-Volume Data Remediation Projects

Financial institutions moving legacy cores to cloud environments are prioritizing automated data remediation to keep lending and payments processes online. Mortgage approval checks that once took 4-6 hours under manual validation now run in near real time after tool deployment, improving customer experience and reducing operational risk. Cloud-native data quality engines tighten feedback loops between data ingestion, profiling and AI-driven analytics, creating a cycle in which better data increases cloud ROI, which in turn reinforces quality budgets.

Intensifying ESG-Reporting Mandates Necessitating Enterprise-Wide Data Quality Controls

SEC climate disclosures, California SB-253/SB-261, and the EU CSRD begin in January 2025 and collectively affect thousands of firms. Compliance programmes now earmark dedicated budgets for lineage, validation, and audit-readiness functionality. Boards link poor ESG data to reputational risk, pushing sustainability officers to adopt solutions that track Scope 3 emissions and verify supplier declarations [1] Informatica, “Navigating ESG Regulations with Intelligent Data Management,” informatica.com.

AI-Driven Customer 360 Initiatives Boosting Spend on Data Profiling & Matching Tools

Retailers in APAC are consolidating clickstream, loyalty, and inventory feeds to power hyper-personalised offers. AI-enabled entity resolution lifts customer-record match rates by up to 30% against rule-based baselines, ensuring recommendation engines receive accurate profiles [2]Hasura, “AI-Powered Data Agents Transform FinServ Data Quality,” hasura.io. Continuous profiling reduces time-to-campaign and underpins omnichannel growth strategies.

Real-Time Fraud-Detection Pipelines in BFSI Catalysing Demand for Streaming Data Quality Engines

Streaming validation curbs false positives that inflate investigation costs. Banks report 30% fewer erroneous alerts after integrating sub-second cleansing with transaction scoring models. Adoption is sharpest where instant-payment schemes expose institutions to higher fraud velocity, forcing a pivot from batch to event-level quality assurance.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Technical Debt in Legacy On-Prem Data Warehouses Delaying Modern Tool Adoption | -1.9% | Global, with higher impact in North America and Europe | Medium term (2-4 years) |

| Shortage of Data Engineering Talent Limiting Effective Tool Utilisation in SMEs | -1.2% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Fragmented Regional Data-Residency Statutes Complicating Global Roll-Outs | -0.8% | Global, with particular complexity in Europe and APAC | Long term (≥ 4 years) |

| High Switching Costs from Embedded ETL Rule-Sets within Tier-1 ERP Suites | -0.6% | Global, with concentration in enterprise segments | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent Technical Debt in Legacy On-Prem Data Warehouses Delaying Modern Tool Adoption

Many organisations divert budgets to maintain ageing ETL jobs and proprietary databases, spending USD 3 million yearly on upkeep. Integration gaps between old schemas and modern APIs slow rollouts, leading firms in finance and healthcare to phase upgrades over multi-year roadmaps before unlocking full cloud-native quality capabilities.

Shortage of Data Engineering Talent Limiting Effective Tool Utilisation in SMEs

Job postings for data engineers have quadrupled in five years, pushing mid-level salaries to USD 125,128–157,222 and crowding SMEs out of the recruitment market. Vendors respond with low-code rule builders and guided workflows. Although these features lower entry barriers, many smaller firms still lack the data literacy to scale adoption quickly.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Type: Cloud Solutions Accelerate Quality Initiatives

Cloud deployments generated 63.45% of data quality tools market revenue in 2025, equal to roughly USD 1.76 billion in the 2025 baseline year. Exceptional 19.8% CAGR indicates that scalability, elastic pricing, and proximity to cloud data stores outweigh security concerns for most buyers. The data quality tools market size for cloud services is set to expand rapidly as API-driven connectors simplify ingestion from SaaS sources and streaming platforms.

On-premise installations remain critical for sectors handling sensitive patient, payment, or defence data. Accounting for 36.55% of revenue in 2025, this cohort is enhancing hybrid capabilities that bridge regulated workloads with public cloud analytics. Healthcare providers illustrate the balance, retaining clinical records on site while cleansing lab feeds in HIPAA-compliant clouds.

By Size of Organization: SMEs Embrace Accessible Quality Solutions

Large enterprises produced 57.30% of total revenue in 2025, thanks to complex data estates spanning dozens of domains and regulatory mandates. Many run enterprise governance programmes that integrate data profiling, monitoring, and remediation into common control planes. The data quality tools market size among large enterprises is stable yet incremental.

SMEs deliver the strongest momentum with 18.9% CAGR to 2031. Pay-as-you-go pricing, consumption credits, and modular packaging lower entry costs. Case studies from UK manufacturers show that improved data quality increased product innovation velocity and enhanced competitive positioning, fostering broader adoption beyond early tech adopters.

By Component: Services Growth Outpaces Software Segment

Software licences remained the backbone at 69.20% revenue share in 2025, translating to USD 1.92 billion in 2025. Vendors continue to embed machine learning within rules engines to surface outliers and recommend fixes automatically. Advancements in pattern recognition and predictive scoring let teams move from reactive to proactive remediation.

Services contributed 30.80% of sales but are rising at an 18.2% CAGR, outstripping software. Managed offerings cover initial assessments, rule optimisation, and continuous observability. Organisations lacking full-time data reliability teams contract experts to maintain SLAs, ensuring sustained quality without diverting scarce internal talent.

By Data Domain: Product Data Emerges as Growth Leader

Customer records held the largest 39.40% share in 2025, equal to USD 1.09 billion in 2025, as omni-channel engagement strategies rely on accurate identities, preferences, and consent flags. High-fidelity customer data underpins AI models for churn prediction and cross-sell recommendations.

Product information is the growth standout at 20.9% CAGR. The data quality tools market size for product data is fueled by SKU expansion, marketplace syndication, and richer attribute requirements for search filters and voice commerce. Clean product data lifts conversion rates and lowers return costs, incentivising retailers and manufacturers to prioritise quality initiatives.

By Tool Type: Monitoring Tools Lead Market Growth

Data profiling accounted for 24.60% of revenue in 2025, or USD 0.68 billion in 2025. Profilers discover patterns, nulls, and anomalies, establishing baselines for subsequent cleansing. Enhanced visualisations now translate technical metrics into business-friendly dashboards.

Monitoring and alerting platforms are expanding fastest at 22.0% CAGR. Continuous rules check streaming pipelines, issuing instant alerts when drift surpasses thresholds. The data quality tools market size dedicated to monitoring benefits from AI models that predict rule violations and suggest preventive measures before downstream reports are affected.

By End-User Vertical: Retail & E-commerce Drive Adoption

BFSI remained the top buyer with a 22.70% share in 2025, worth USD 0.63 billion in 2025. Regulatory filings, risk calculations, and fraud detection all demand precise, lineage-verified data. Banks integrate quality engines with core systems to satisfy BCBS 239 traceability requirements while supporting real-time analytics.

Retail and e-commerce sector purchases rise at 23.1% CAGR. Unified product catalogues, inventory feeds, and clickstream logs power personalised merchandising and supply-chain automation. Data quality directly influences customer satisfaction, pushing merchants to embed quality checks within every storefront update.

Geography Analysis

North America generated 35.70% of global revenue in 2025, or close to USD 0.99 billion in 2025, underpinned by heavy cloud migration in financial services and advanced adoption of AI-enabled analytics. The introduction of SEC climate reporting rules strengthens the compliance rationale for enterprise-wide data controls. Vendors headquartered in the region accelerate innovation cycles, providing early exposure to new features.

Asia-Pacific is the fastest mover with a projected 21.7% CAGR from 2026 to 2031. Investments in 5G, e-commerce, and fintech generate vast data volumes that require quality assurances. China, India, and Japan emphasise data integrity as a pillar of digital public infrastructure, while APAC retailers deploy profiling engines to enhance Customer 360 rollouts and personalise offers.

Europe’s growth is steady, driven by stringent privacy and sustainability mandates. The CSRD drives demand for solutions that ensure auditable ESG disclosures. Organisations weigh cloud benefits against data sovereignty, adopting regional nodes or sovereign clouds to comply with localisation rules. Increasingly, European boards recognise clean data as foundational to digital competitiveness.

Competitive Landscape

Market concentration is moderate. Established vendors such as Informatica, SAP, IBM, and Microsoft compete with specialist providers including Collibra, Ataccama, and Precisely. Differentiation centres on AI automation depth, cloud-native architecture, and out-of-the-box industry rule packs. Partnerships with hyperscalers extend reach and reduce integration friction, while acquisitions target gap fillers such as data observability and policy enforcement engines.

Emerging players leverage large-language-model-based rule generation, proactive drift detection, and synthetic test-data creation. Patent filings surged in 2024, exemplified by Egnyte’s portfolio covering unified access control and subject-access request optimisation. White-space opportunities exist around unstructured content quality, IoT streaming validation, and distributed data fabric enforcement.

First-mover vendors embed quality checks within broader data platform stacks, bundling governance, lineage, and observability. Buyers increasingly favour integrated suites over point tools, valuing reduced vendor management overhead and consistent rule propagation across data domains.

Data Quality Tools Industry Leaders

IBM Corporation

Oracle Corporation

SAP SE

Informatica Inc.

Talend Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Acceldata introduced Agentic Data Management that automates reconciliation and pre-emptive correction across distributed data estates.

- April 2025: Collibra upgraded its Data Quality & Observability platform with auto-discovery and stakeholder notification enhancements.

- March 2025: Ataccama ONE version 14 added unstructured data quality assessment and deeper data fabric integrations.

- March 2025: Atlan raised USD 105 million in Series C funding to enhance AI-driven data discovery and quality automation.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the data quality tools market as all off-the-shelf software and cloud subscriptions whose primary function is to profile, cleanse, match, enrich, and continuously monitor enterprise data sets across operational and analytical systems. Solutions bundled inside wider data management platforms are included only when their revenues are reported separately, thereby keeping the accounting neat.

Scope exclusion: offerings limited to generic extract-load-transform (ELT) pipelines or one-time advisory projects are kept outside the numbers.

Segmentation Overview

- By Deployment Type

- Cloud-based

- On-Premise

- By Size of the Organization

- Small and Medium Enterprises

- Large Enterprises

- By Component

- Software

- Services

- By Data Domain

- Customer Data

- Product Data

- Financial Data

- Supplier and Vendor Data

- Risk and Compliance Data

- By Tool Type

- Data Profiling

- Data Cleansing / Standardisation

- Data Matching and De-Duplication

- Monitoring and Alerting

- Master Data Management-Centric Tools

- By End-User Vertical

- BFSI

- Government and Public Sector

- IT and Telecom

- Retail and E-commerce

- Healthcare and Life Sciences

- Other Industries (Manufacturing, Utilities, Media)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Chile

- Peru

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- Australia

- New Zealand

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Turkey

- South Africa

- Rest of Middle East and Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview tool vendors, implementation partners, and enterprise data-governance leads across North America, Europe, and fast-growing Asian economies. Conversations test adoption thresholds, average subscription pricing, cloud migration timelines, and regional regulation triggers, letting us reconcile desk findings and refine model assumptions.

Desk Research

We start by mapping the universe through publicly available anchors such as US Census software trade statistics, Eurostat ICT spending tables, India's MeitY cloud adoption dashboards, and filings to the US SEC that break out data-quality lines. Additional color is gained from trade associations like the EDM Council, policy papers on GDPR enforcement, and patent families accessed via Questel that flag emerging automation modules. Company investor decks, earnings calls, and reputable press coverage layer recent pricing moves and customer wins. These sources are illustrative only; many others inform data collection, cross-checks, and clarifications.

Market-Sizing & Forecasting

A top-down build begins with enterprise software spend by industry, which is then filtered through indicators such as regulated-data intensity, cloud workload penetration, and compliance audit frequency to derive an addressable pool. Select bottom-up roll-ups of vendor revenues, channel checks, and sampled annual contract value validate and adjust totals. Key variables include average price per data-quality seat, share of workloads moving to the cloud, number of regulatory audits per thousand enterprises, growth in AI model deployments needing clean data, and frequency of data breach incidents. Multivariate regression links these drivers to historical market performance and projects them through 2030 under a base, high, and low scenario. Gaps in vendor disclosures are bridged by margin back-solves and peer benchmarking.

Data Validation & Update Cycle

Outputs pass three-layer checks: variance tests against independent software indexes, anomaly flags reviewed by a senior analyst, and a peer review before sign-off. Reports refresh each year, with mid-cycle updates when material events, large acquisitions, game-changing regulation, or macro shocks shift the baseline.

Why Mordor's Data Quality Tools Baseline Commands Credibility

Published numbers often diverge because studies track different revenue streams, convert currencies on varying dates, or project growth off unmatched driver sets. Our disciplined scope choices, annual refresh cadence, and dual-path modeling tighten those seams for clients who must act on dependable figures.

These comparisons show that when scope breadth, variable selection, and refresh timing differ, valuations swing widely. By tying every figure to transparent drivers and repeating the same reproducible steps, Mordor Intelligence delivers a balanced, traceable baseline decision-makers can trust.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.78 B (2025) | Mordor Intelligence | - |

| USD 1.66 B (2024) | Global Consultancy A | Counts license fees only, excludes managed cloud services |

| USD 2.71 B (2024) | Regional Consultancy B | Relies on vendor bookings without price normalization |

| USD 2.30 B (2024) | Trade Journal C | Limits scope to profiling modules, omits monitoring tools |

These comparisons show that when scope breadth, variable selection, and refresh timing differ, valuations swing widely. By tying every figure to transparent drivers and repeating the same reproducible steps, Mordor Intelligence delivers a balanced, traceable baseline decision-makers can trust.

Key Questions Answered in the Report

What is the current value of the data quality tools market?

The data quality tools market is valued at USD 3.27 billion in 2026.

How fast is the market expected to grow?

It is projected to register a 17.7% CAGR, reaching USD 7.39 billion by 2031.

Which deployment model is growing the quickest?

Cloud-based solutions are expanding at a 19.8% CAGR and already represent 63.45% of revenue.

Why are data quality tools critical for ESG reporting?

Regulations such as the SEC climate rule and EU CSRD require auditable, high-fidelity data, pushing firms to adopt lineage and validation capabilities.

Which industry vertical is adopting data quality tools the fastest?

Retail and e-commerce lead growth with a 23.1% CAGR due to omnichannel product data requirements and personalised customer experiences.

How does talent scarcity affect tool adoption in SMEs?

Limited access to data engineers raises implementation barriers, prompting vendors to offer low-code, guided interfaces to reduce skills dependency.

Page last updated on: