Multi Vendor Support Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

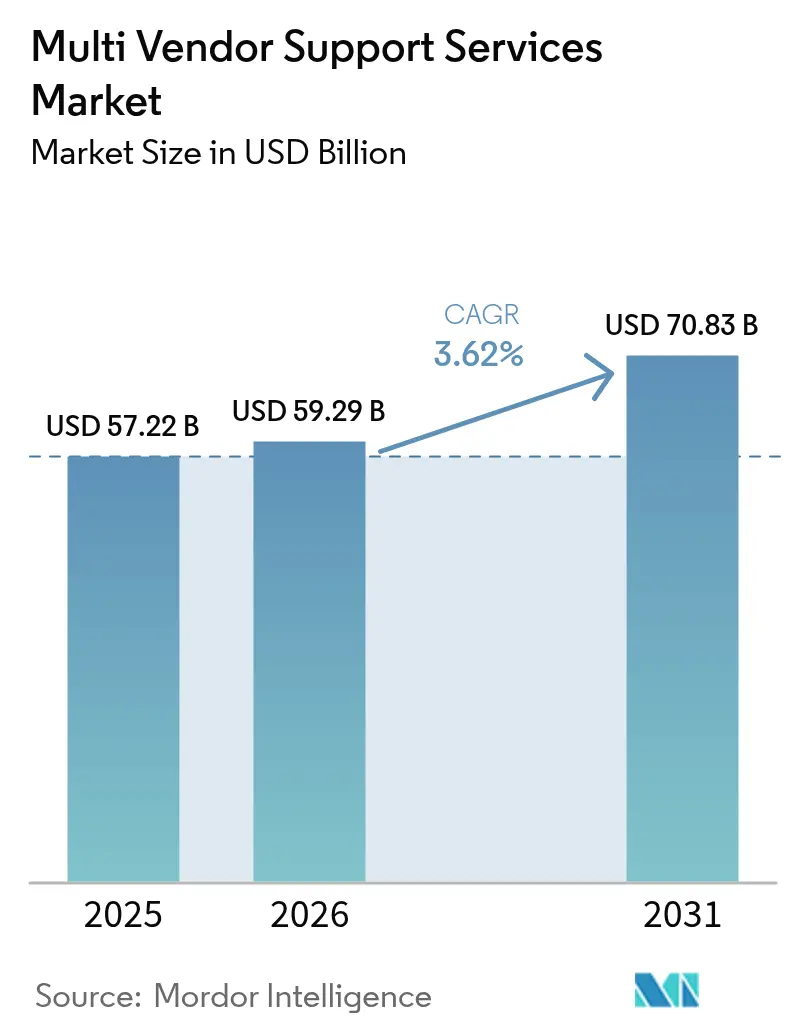

| Market Size (2026) | USD 59.29 Billion |

| Market Size (2031) | USD 70.83 Billion |

| Growth Rate (2026 - 2031) | 3.62% CAGR |

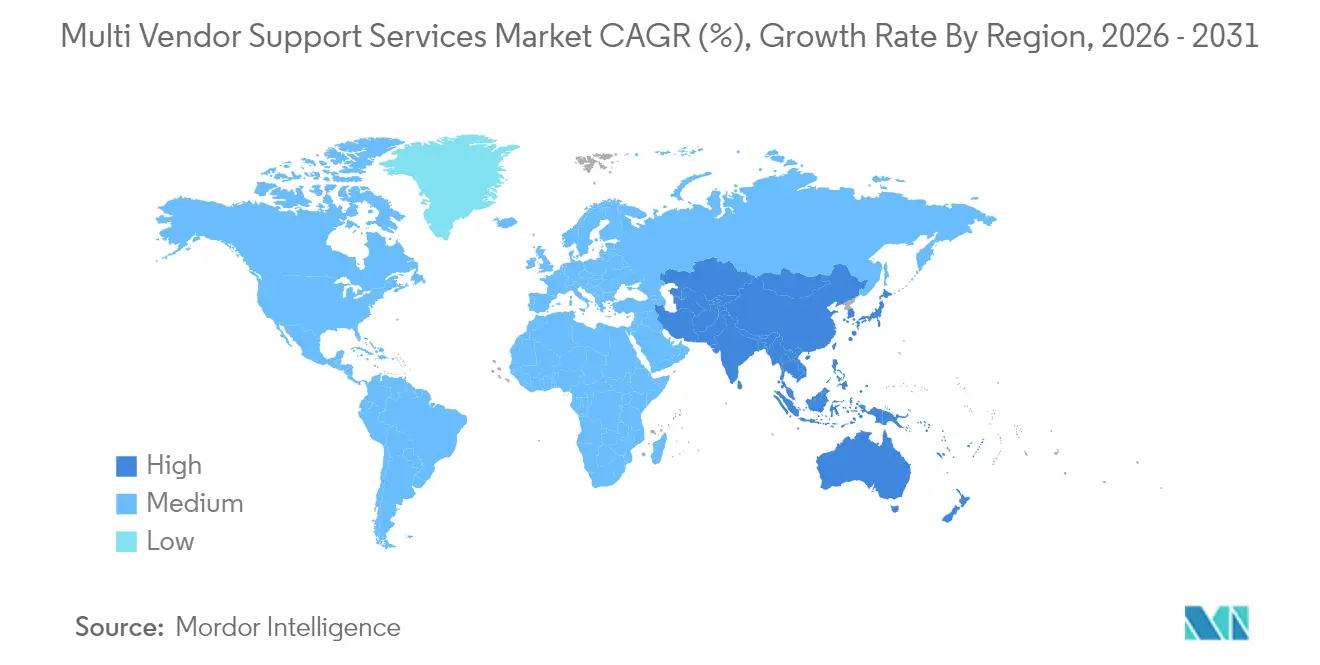

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Multi Vendor Support Services Market Analysis by Mordor Intelligence

The Multi Vendor Support Services market size is expected to grow from USD 57.22 billion in 2025 to USD 59.29 billion in 2026 and is forecast to reach USD 70.83 billion by 2031 at 3.62% CAGR over 2026-2031. Rising enterprise demand for predictable, outcome-based support contracts and the need to navigate increasingly heterogeneous hardware and software estates underpin this steady expansion. Cost-optimized purchasing policies, accelerated by macro-economic caution, are steering buyers toward vendor consolidation and life-extension strategies that lower total cost of ownership without compromising compliance. Providers with robust AI-driven diagnostics, zero-trust security frameworks, and experience in regulated sectors are gaining competitive advantage. Heightened regulatory focus on operational resilience, particularly in financial services, and on sustainability-linked product lifecycles, especially in Europe, is also reshaping service scope and value propositions.

Key Report Takeaways

- By service type, managed services captured 70.65% of the Multi Vendor Support Services market share in 2025; remote and virtual support is projected to log the fastest 4.38% CAGR to 2031.

- By enterprise size, large enterprises held 69.10% of the Multi Vendor Support Services market in 2025, while the SME segment is expanding at a 4.86% CAGR through 2031.

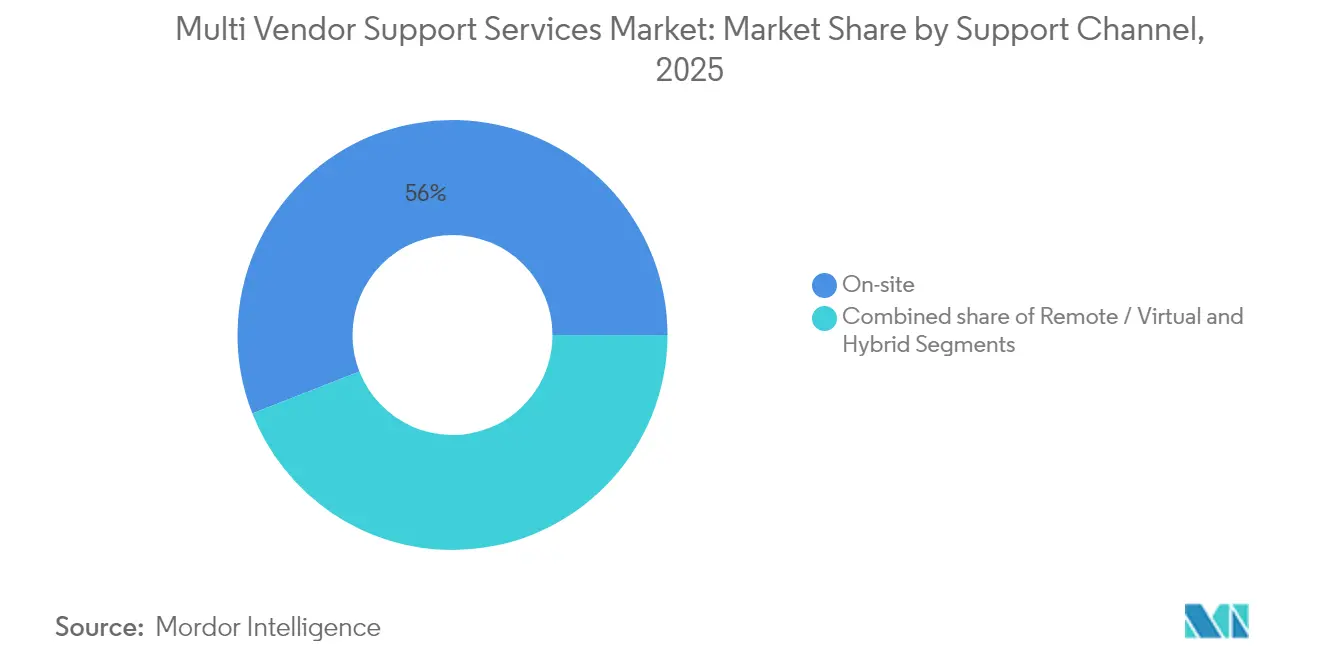

- By support channel, on-site services accounted for 55.95% of the Multi Vendor Support Services market size in 2025, but hybrid models mixing remote diagnostics with targeted field visits are scaling fastest.

- By end-user vertical, IT & telecommunications led with 22.10% revenue share in 2025; BFSI is poised to grow at a 3.78% CAGR through 2031 on the back of operational-resilience mandates.

- By geography, North America dominated with 34.60% revenue share in 2025; Asia-Pacific is forecast to clock a 4.03% CAGR to 2031 as cloud-first deployments proliferate.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Multi Vendor Support Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising maintenance cost of OEM services | +1.2% | Global (North America, Europe highest) | Medium term (2-4 years) |

| Growing complexity of multi-vendor IT estates | +0.8% | Global (APAC scaling) | Long term (≥ 4 years) |

| Cost-optimization and vendor consolidation push | +0.9% | North America and EU, expanding to APAC | Short term (≤ 2 years) |

| Shorter OEM support window / rapid obsolescence | +0.6% | Global, technology-intensive regions | Medium term (2-4 years) |

| Sustainability-linked life-extension mandates | +0.4% | EU leading | Long term (≥ 4 years) |

| AI-driven predictive maintenance capabilities | +0.7% | North America and EU early adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Maintenance Cost of OEM Services

OEMs continue to lift annual maintenance prices as hardware margins erode, widening the cost differential against independent support firms that frequently deliver equivalent SLAs at 50–80% lower expense. Procurement teams now benchmark total cost of ownership rather than headline purchase prices, spurring hybrid models that retain OEM cover for mission-critical assets while offloading legacy estates to third-party providers. CFO-led scrutiny has intensified under uncertain economic conditions, accelerating the switch to outcome-based contracts that guarantee uptime while capping spend. Even heavily regulated organizations are joining the shift, provided providers evidence compliance with sector-specific controls. The financial effect has made cost-savings a primary selection criterion in new tenders.

Growing Complexity of Multi-Vendor IT Estates

Typical enterprises now run equipment from five to seven manufacturers, a product of best-of-breed strategies and rapid cloud adoption. Heterogeneous stacks increase interoperability challenges and expose gaps in traditional OEM-centric support models. Companies therefore expect partners to own end-to-end incident resolution across servers, storage, networking, and cloud platforms. This complexity premium rewards service integrators with certified expertise on disparate technologies and centralized command centers capable of orchestrating multi-party escalations. Demand is rising for unified dashboards that provide single-pane-of-glass visibility into incident queues and SLA compliance.

Cost-Optimization and Vendor Consolidation Push

Operating-expense reduction programs prioritize supplier rationalization, with enterprises discovering that managing several dozen contracts can inflate procurement and governance overheads by 15–20%. Aggregated spending enhances bargaining leverage and simplifies SLA management, fueling migration toward providers that can support multi-vendor estates globally. Consolidation is particularly attractive to organizations facing heightened audit scrutiny, as a single master services agreement eases compliance tracking. As a result, vendors showcasing broad certification portfolios and proven governance frameworks enjoy higher win rates.

Shorter OEM Support-Window / Rapid Obsolescence

Hardware refresh cycles have compressed to approximately four years, with end-of-support notifications often arriving before capital investments are fully depreciated[1]European Commission, “Circular Economy Action Plan,” ec.europa.eu. Third-party providers are bridging this gap, offering parts availability and on-site engineering for platforms that OEMs no longer service. Customers extend asset life to redirect capital toward transformative initiatives such as edge computing and AI analytics. EU ecodesign directives are reinforcing this life-extension mindset by emphasizing repairability and circular-economy metrics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Security and privacy concerns with third-party access | -0.7% | Global, regulated industries focus | Short term (≤ 2 years) |

| OEM resistance and warranty-void threats | -0.5% | Global, risk-averse enterprises | Medium term (2-4 years) |

| Global shortage of legacy hardware skill sets | -0.4% | Developed markets acute | Long term (≥ 4 years) |

| Compliance / data-sovereignty complexities | -0.3% | Europe and APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Security and Privacy Concerns with Third-Party Access

High-profile supply-chain breaches have heightened scrutiny of extended vendor ecosystems, with frameworks such as the EU Digital Operational Resilience Act obliging banks to evidence robust third-party risk governance. Security teams fear that privileged remote tools could become attack vectors, delaying contracting cycles while due-diligence checks are completed. Leading support firms are responding with zero-trust architectures, rigorous background screening, and cyber-insurance protections that in several cases exceed OEM offerings. Adoption momentum is therefore tempered but not derailed, as risk-mitigation best practices mature.

OEM Resistance and Warranty-Void Threats

Many manufacturers threaten to void warranty coverage if unauthorized technicians work on equipment, deterring some enterprises from fully migrating to independent support[2]Repair Association, “Right to Repair Policy Updates,” repair.org. Right-to-repair legislation enjoys growing political backing in the United States and Europe, but tangible relief remains two to three years away. To navigate the risk, buyers commonly keep OEM cover on newer assets while transferring older fleets to third-party maintenance. Independents counteract OEM rhetoric by offering insurance underwriters that guarantee performance equivalent to original warranties, yet perception hurdles persist among risk-averse boards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Managed Services Drive Market Evolution

Managed services accounted for 70.65% of the Multi Vendor Support Services market share in 2025, evidencing enterprise preference for predictable, outcome-based models that offload operational risk. Providers package 24×7 monitoring, parts logistics, and compliance reporting into multi-year contracts that harmonize disparate SLAs. The Multi Vendor Support Services market size for managed services is forecast to expand at a 5.23% CAGR from 2026 to 2031 as AI-powered tools elevate automation and lower unit costs. Professional services remain vital for migrations and complex upgrades but are expected to grow more slowly, constrained by one-time project billing.

Advanced providers differentiate by embedding machine-learning engines that anticipate failures and schedule just-in-time parts delivery, raising asset uptime. Predictive analytics combined with automated runbooks shrink mean-time-to-repair, enabling service-credit models that align incentives. The managed approach also supports regulatory audits, as centralized ticket data simplifies evidence gathering. Collectively, these attributes reinforce customer loyalty and underpin higher renewal rates that elevate provider valuations.

By Enterprise Size: SME Adoption Accelerates Digital Parity

Large organizations retained 69.10% revenue share in 2025, reflecting extensive legacy estates and complex compliance demands. Yet SMEs are the fastest-growing constituency, logging a 4.86% CAGR through 2031 as cloud economics level the playing field. Consumption-based pricing plus standardized support bundles remove the need for hefty capital outlays, making enterprise-grade services accessible to smaller IT teams. Providers leverage remote monitoring and templated runbooks to deliver scale benefits irrespective of client headcount.

SME demand is strongest in manufacturing, healthcare, and professional-services niches where regulatory and uptime requirements mirror those of larger peers. Vendors respond with modular offerings that bundle security, backup, and hardware maintenance into a single invoice. This simplification resonates with mid-market CFOs eager to consolidate suppliers and streamline governance, translating into longer contract tenures once onboarded.

By Support Channel: Remote Capabilities Transform Service Delivery

On-site interventions still represented 55.95% of the Multi Vendor Support Services market in 2025, underscoring the continued need for hands-on expertise in secure facilities and heavy-industries plants. Nonetheless, the Multi Vendor Support Services market size attached to remote services is climbing rapidly, thanks to a 4.38% CAGR fueled by augmented-reality headsets, AI-assisted troubleshooting, and encrypted connectivity. Pandemic travel restrictions proved the viability of virtual resolution workflows, and many customers now make remote triage a contract prerequisite.

Hybrid models prevail: providers run initial diagnostics remotely, dispatching field engineers only when physical repair is unavoidable. This approach cuts response times, trims travel emissions, and maximizes talent utilization across regions. Leading platforms integrate automatic session recording, sentiment analysis of technician-client dialogues, and auto-generated service reports, relieving engineers of administrative overhead.

By End-User Vertical: BFSI Leads Digital Resilience Investment

IT and telecommunications firms generated the largest revenue slice at 22.10% in 2025, reflecting demanding uptime SLAs and rapid product cycles. Financial-services institutions, however, will contribute the highest incremental growth, with a 3.78% CAGR to 2031. Regulatory imperatives such as DORA place stringent resilience and third-party oversight duties on banks, spurring comprehensive support contracts that span data centers and hybrid-cloud nodes. Healthcare buyers are likewise leaning on multi-vendor support to manage connected medical devices under HIPAA and GDPR constraints.

Manufacturers adopt predictive maintenance to avert unplanned line stoppages, while retailers rely on end-to-end support for omnichannel point-of-sale platforms. Energy utilities constitute an emerging hotspot, where distributed grid assets require rapid field response and secure remote diagnostics. The depth of domain knowledge demanded in these regulated segments favors providers willing to certify engineers, invest in compliance automation, and secure sector-specific accreditations.

Geography Analysis

North America commanded 34.60% of global revenue in 2025, underpinned by early cloud adoption, sophisticated procurement teams, and stringent data-protection rules that favor specialized partners. The region’s enterprises tend to refresh hardware frequently, generating a steady pipeline for lifecycle-extension services. High labor costs also magnify the economic argument for automation-driven remote support, prompting providers to establish AI centers of excellence in the United States and Canada.

Europe maintains a solid position, buoyed by ecodesign regulations that encourage repairability and by privacy frameworks such as GDPR that elevate audit requirements. Multi-vendor contracts often incorporate green-IT metrics, rewarding providers that can document carbon savings from extended asset life. Government agencies in Germany and the Nordics are pioneering long-term partnerships that weave sustainability KPIs into performance dashboards.

Asia-Pacific is the growth engine, expected to post a 4.03% CAGR to 2031. Enterprises in India, China, and Indonesia are leapfrogging legacy architectures, adopting cloud-native workloads that require heterogeneous support from day one. Local service integrators are scaling rapidly, while global players open regional service hubs and bilingual helpdesks to tap rising demand. Regulatory maturity varies by market, but the common thread is an aggressive digital-transformation agenda that outstrips local OEM warranty provisions, reinforcing the multi-vendor proposition.

South America and the Middle East and Africa register smaller absolute spending yet demonstrate strong interest in remote-first models to overcome talent shortages and geographical dispersion. Currency volatility and fiscal constraints temper contract sizes, but low data-center density makes high uptime even more critical, enhancing the value narrative for predictive maintenance propositions.

Regulatory Landscape

Regulation affecting multi-vendor support services is tightening around third-party risk, supply-chain security, and operational resilience, lifting compliance expectations for remote access, privileged tooling, and subcontractor use. In the EU, the Digital Operational Resilience Act (DORA) is a key reference point for BFSI outsourcing governance. Broader digital-infrastructure initiatives, including European Commission proposals around the Digital Networks Act, and ongoing updates tied to the Cybersecurity Act (CSA 2.0), are reinforcing expectations for demonstrable supply-chain controls and security-by-design practices for supported telecom and IT estates.

In the United States, equipment-authorization and telecom security measures are also moving toward more stringent national-security and conformance requirements, reflected in FCC action in 2026 to strengthen telecommunications certification and measurement-facility controls. Across major markets, data-sovereignty constraints and public-sector procurement frameworks increasingly favor vendor-neutral, auditable service delivery. This is pushing multi-vendor providers to formalize governance, reporting, and control evidence (such as standardized incident logs, access recordings, and compliance-ready documentation) into contract scope rather than treating it as optional add-ons.

Value Chain Analysis

The value chain starts with OEM and third-party hardware and software ecosystems that shape parts availability, firmware access, and tooling. It then moves to the service provider layer, where multi-vendor coverage is assembled into a single operating model. Providers build capabilities across remote diagnostics, field engineering, spares logistics, and knowledge management, and frequently package these into managed services to maintain end-to-end accountability.

Enterprises, through procurement and IT governance teams, contract around outcome-based SLAs and typically require integration with ITSM and CMDB systems so they can maintain a single source of truth across heterogeneous estates. Downstream work focuses on incident triage, escalation orchestration across multiple OEMs, and lifecycle services such as life-extension, refresh planning, and compliance reporting. Key enablers include vendor-agnostic monitoring and observability, secure remote-access gateways aligned to zero-trust practices, and orchestration layers in multisourcing and service integration models that normalize inconsistent data formats and reporting structures across vendors. Bottlenecks often come from fragmented telemetry, mismatched SLA definitions, and limited legacy skills, which drives providers to invest in automation, standardized runbooks, and partner ecosystems for niche platforms and regulated-sector requirements.

Competitive Landscape

The Multi Vendor Support Services market remains moderately fragmented but is consolidating as clients favor suppliers with global reach and broad certification portfolios. Major OEMs such as IBM, Dell, and Cisco continue to operate in-house support arms yet face pricing pressure from independents promoting 50–70% cost savings. Acquisition activity is brisk: IBM agreed to purchase HashiCorp for USD 6.4 billion to fortify multi-cloud automation, while Cognizant bought Belcan for USD 1.3 billion to diversify into engineering services.

Technology investment defines competitive edge. Providers are embedding predictive-analytics engines that decode telemetry streams and trigger proactive dispatch. Field technicians receive augmented-reality overlays for guided repair, raising first-time fix ratios. Security posture is equally pivotal; zero-trust remote-access gateways and continuous compliance reporting distinguish bids in regulated verticals. Vendors unable to fund such platforms risk relegation to niche, price-led segments.

Vertical specialization deepens as players court industries with complex governance regimes. Rimini Street’s expansion into SAP cloud support strengthens its appeal to enterprises balancing hybrid ERP stacks. NWN’s acquisition of InterVision broadens its cybersecurity and public-sector footprint, underscoring a trend toward portfolio stacking to win multi-tower contracts[3]Finsmes, “NWN Corporation Acquires InterVision,” finsmes.com . Private-equity investors, exemplified by Warburg Pincus backing Service Express, target firms with recurring revenue and sticky customer bases, accelerating roll-up strategies.

Emerging disruptors include cloud-native managed-service providers leveraging infrastructure-as-code tooling to deliver elastic support at margins untenable for legacy models. However, risk-averse global enterprises still prize long operating histories and audited controls, limiting near-term share shift. Overall, the competitive dynamic is transitioning from pure cost contest to value-centric differentiation anchored in automation, vertical compliance expertise, and ESG alignment.

Multi Vendor Support Services Industry Leaders

IBM Corporation

Microsoft Corporation

Oracle Corporation

Hewlett Packard Enterprise Co

Dell Technologies Inc

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Outcome-based consolidation remains a major whitespace. Enterprises running five to seven OEM relationships want a single point of accountability for mixed estates while preserving technology choice. This supports opportunities for providers that can combine multi-vendor break-fix with compliance-ready governance, including access controls, ticket evidence, and third-party risk reporting aligned to regulated-vertical expectations, particularly BFSI resilience needs connected to DORA. A second whitespace is hybrid delivery, where remote diagnostics and AI-assisted troubleshooting reduce on-site dependence, while customers still require assured parts availability and certified field coverage for secure facilities and edge locations.

Technology-led differentiation is also expanding, creating openings for providers that productize service orchestration and observability across vendors, rather than focusing only on staff-based maintenance. Evidence of market direction includes platform and portfolio moves by large incumbents aimed at unifying support across multi-vendor, multi-cloud, and edge environments, such as HPE refocusing HPE Complete Care Service for AI-driven operations and multi-vendor coverage, and IBM expanding Technology Lifecycle Services into adjacent networking and security support domains. In telecom and IT operations, vendor consolidation initiatives and SIAM-style governance frameworks are being used to reduce contract sprawl, supporting demand for providers that can act as a neutral prime contractor while integrating OEMs and specialist subcontractors under one service model.

Recent Industry Developments

- June 2026: HPE introduced new supercomputing programming software positioned to simplify developer workflows and provide first-call support across multi-vendor environments. This strengthens HPEs support-led differentiation for complex HPC and sovereign AI deployments where customers run heterogeneous stacks and want a single escalation path.

- May 2026: HPE announced new GreenLake private cloud innovations aimed at unifying infrastructure modernization and data readiness for enterprise AI. The updates support multi-vendor operational models by reducing the need for fragmented toolsets and aligning platform operations with managed support constructs.

- October 2025: IBM expanded Technology Lifecycle Services to cover firewall and network support in partnership with Cisco. The move broadens IBM-led multi-vendor accountability beyond core infrastructure maintenance into security and networking domains that are increasingly central to enterprise support contracts.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market covers third party support services that maintain and troubleshoot mixed vendor IT environments, where a single provider supports hardware and related software across servers, storage, networks, and key enterprise systems through on-site and remote delivery.

Scope exclusions: We exclude OEM warranties bundled with original equipment sales and pure help-desk outsourcing that is not tied to multi-vendor infrastructure support.

Segmentation Overview

- By Service Type

- Professional

- Managed

- By Enterprise Size

- Large Enterprises

- Small and Medium Enterprises (SMEs)

- By Support Channel

- On-site

- Remote / Virtual

- Hybrid

- By End-user Vertical

- IT and Telecommunication

- BFSI

- Healthcare

- Energy and Power

- Manufacturing

- Retail

- Other End-user Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Egypt

- Nigeria

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Desk Research

We start with desk research to set the boundaries and build a fact base around installed IT infrastructure, typical refresh cycles, and enterprise support spending patterns. For this, we rely on public sources such as US SEC filings for revenue disclosures, the US Bureau of Labor Statistics for labor cost trends that influence support pricing, and OECD indicators that help show how each country is directing IT investment.

We also review sources such as ISO and IEC standards pages for service and quality definitions, WIPO patent databases to see where monitoring and diagnostics are moving, and ITU publications on connectivity readiness that affects remote support delivery. These inputs are complemented with press releases, investor presentations, and contract announcements, plus selective use of paid subscriptions for company financials and intelligence, news and financials, patent analytics, and global contracts and tenders to confirm deal structures and service scope. The desk research sources listed here are illustrative, and we used many other public documents for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work was used to pressure test what is counted as multi-vendor support, how contracts are priced (site coverage, SLA levels, parts logistics), and how much spend is being shifted away from OEM support. We spoke with providers, channel partners, and enterprise IT decision makers across major regions so assumptions on renewal rates, attach rates to installed base, and average contract values could be adjusted to reflect what is happening in real buying cycles.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 14% | APAC: 42% |

| Mid tier: 58% | Functional/Unit leaders: 41% | EMEA: 31% |

| Smaller Players: 16% | Managers: 45% | Americas: 27% |

Market-Sizing & Forecasting

Our sizing starts with a top-down demand build that reconstructs the addressable support spend from the active installed base of enterprise IT equipment and the share that is typically placed under third party contracts after warranty expiry. Once the demand pool is formed, it is allocated across regions using enterprise IT footprint signals, then adjusted for contract coverage intensity (for example, 24x7 versus business hours) and the mix of on-site versus remote delivery.

To keep the totals grounded, results are corroborated with selective bottom-up approximations based on sampled contract values, service provider revenue disclosures where available, and channel checks on renewal behavior. Inputs that most often move the model include post-warranty penetration rates, installed base aging and refresh cadence, average annual contract value by device class, SLA driven price uplifts, and parts logistics costs that affect pricing in remote locations. Where bottom-up inputs are missing for smaller countries, we fill gaps using proxy ratios from comparable markets and then re-check them with expert feedback.

For forecasting, we use scenario analysis because contract renewals and infrastructure refresh cycles can shift quickly when budgets tighten or when hybrid environments expand. The forward view is shaped by expected installed base growth, policy and compliance pressure that raises uptime needs, and a realistic progression of average pricing that we validate during interviews.

Data Validation & Update Cycle

We validate the outputs through triangulation across three layers, demand signals, supply side disclosures, and interview based reality checks. Variance checks are run at region and country level so sudden jumps can be traced back to a specific input, such as an unusual SLA mix or an unrealistic penetration rate.

Before sign-off, numbers are reviewed in more than one analyst pass, and outliers trigger follow-up calls or extra desk checks until the reason is clear. Reports are refreshed annually, and interim updates are made when material events change pricing, contract structures, or the addressable installed base. Right before delivery, a final refresh pass is completed so clients receive the latest view rather than an older snapshot.

Mordor Intelligence's Multi Vendor Support Services Market Sizing Compared With Other Published Estimates

Published market values for multi-vendor support services often vary because each publisher draws the line differently between OEM warranty work, third party support, and adjacent managed services. Timing also matters, since some estimates use older base years, mix currencies differently, or apply aggressive growth assumptions without re-checking contract behavior.

By tracking contract eligibility after warranty expiry and refresh cadence checks, Mordor Intelligence keeps the market total tied to paid post-warranty maintenance and break-fix contracts, rather than counting bundled warranties or unrelated help-desk outsourcing that inflates the spend pool.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 59.29 B (2026) | |

| Industry Publisher A | USD 57.60 B (2024) | Uses a different base year and a broader service map, and it appears to include more application and business-function support that can overlap with managed services budgets. |

| Industry Tracker B | USD 12.26 B (2027) | Reports incremental growth over a period instead of a full market value, which makes the number look much smaller and is not directly comparable to a single-year market size. |

The spread mainly comes from what is counted and how the number is presented, not only from real demand differences. When scope is kept to paid post-warranty multi-vendor infrastructure support and inputs are re-checked against renewal and pricing behavior, the final value becomes easier to trace and to repeat for planning.

Key Questions Answered in the Report

What is the current size of the Multi Vendor Support Services market?

The Multi Vendor Support Services market size stood at USD 59.29 billion in 2026 and is projected to reach USD 70.83 billion by 2031.

Which service type dominates the Multi Vendor Support Services market?

Managed services dominate, holding 70.65% market share in 2025 as enterprises favor outcome-based, risk-transfer contracts.

Which region is growing fastest?

Asia-Pacific is forecast to record the fastest 4.03% CAGR through 2031, driven by rapid cloud-first adoption and growing need for multi-vendor integration.

Why are financial institutions increasing spend on multi-vendor support?

Frameworks such as the EU Digital Operational Resilience Act obligate banks to strengthen third-party risk management and operational resilience, prompting 3.78% CAGR spending growth in BFSI.

How are AI technologies influencing support delivery?

Providers embed machine-learning models for predictive maintenance, improving uptime and reducing mean-time-to-repair, a key differentiator in contract bids.

What is a typical cost saving from third-party maintenance versus OEM support?

Independent providers frequently deliver equivalent SLAs at 50–80% lower cost, a gap widening as OEMs shift to subscription-driven models.

Page last updated on: