Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 27.84 Billion |

| Market Size (2026) | USD 28.78 Billion |

| Market Size (2031) | USD 33.97 Billion |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Washing Machine Market Analysis by Mordor Intelligence

The Asia-Pacific washing machine market size is expected to grow from USD 27.84 billion in 2025 to USD 28.78 billion in 2026 and is forecast to reach USD 33.97 billion by 2031 at a 3.37% CAGR. Policy tightening on energy and water use is shifting replacement decisions toward high-efficiency, feature-rich models that reduce utility costs and meet stricter labeling norms in China, India, Japan, Hong Kong, and Australia. E-commerce continues to compress purchase cycles through quick delivery, bundled installation, and real-time promotions, with large retail events elevating conversion for appliances across China and key Southeast Asian markets. At the same time, urban premiumization favors AI-enabled washer-dryers, auto-dosing, and larger capacities for fewer weekly cycles, while microfiber emission rules and wastewater thresholds are starting to reshape design choices and bill of materials. Online and social commerce now set the pace on value-added services, while subscription and lease-to-own pilots in advanced Asia-Pacific markets signal a gradual transition from one-time ownership to managed service models. Across categories and price bands, brands that orchestrate ecosystems with detergent partners and smart home platforms are positioned to capture repeat engagement beyond the initial sale in the Asia-Pacific washing machine market.

Key Report Takeaways

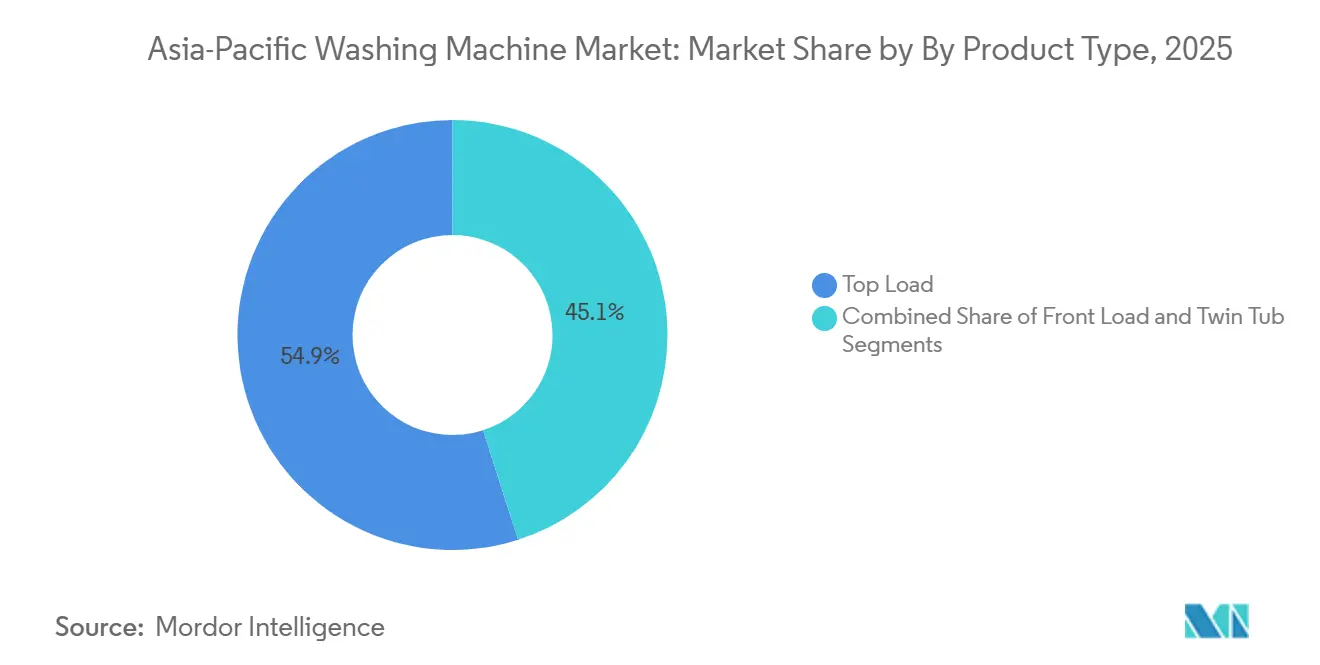

- By product type, top load held 54.94% of the Asia-Pacific washing machine market share in 2025, while front load is projected to expand at a 3.75% CAGR through 2031.

- By capacity, the 5–8 kg segment accounted for a 48.21% share of the Asia-Pacific washing machine market size in 2025, and above 8 kg is advancing at a 5.34% CAGR through 2031.

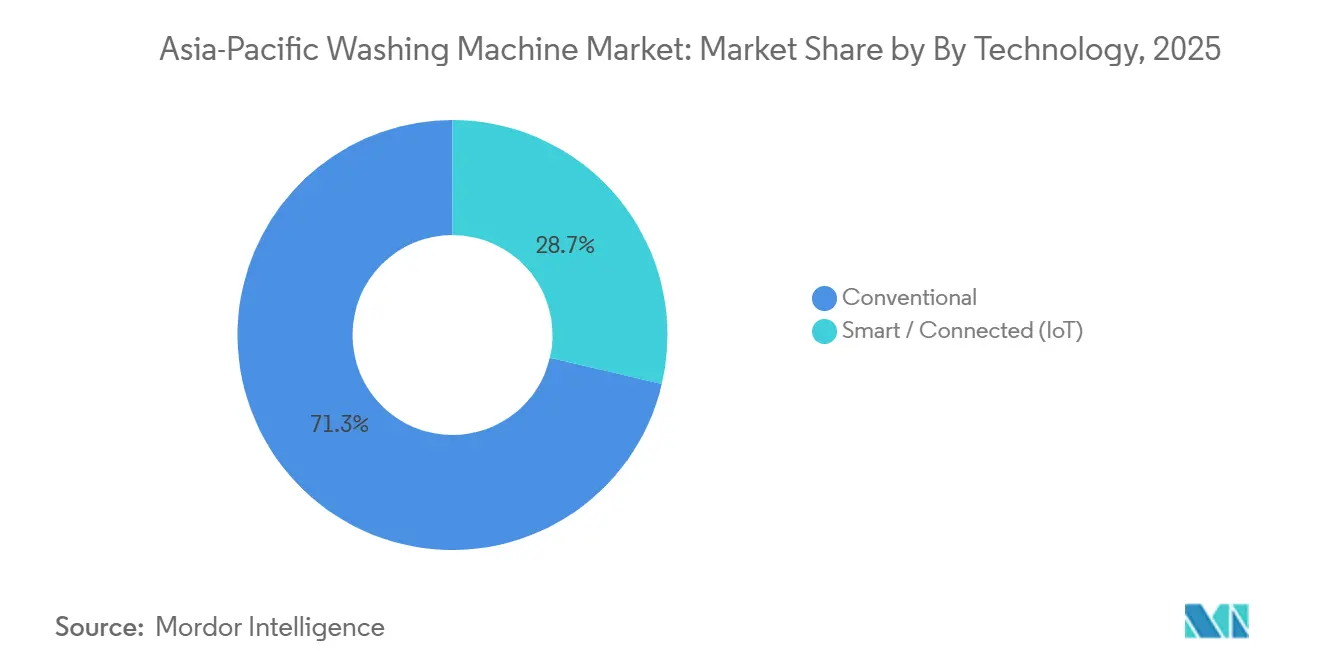

- By technology, conventional models commanded a 71.34% share in 2025, and smart/connected (IoT) is forecast to grow at a 4.76% CAGR to 2031.

- By end user, residential accounted for 88.02% of the 2025 volume, while commercial is recording the fastest incremental growth at a 5.34% CAGR through 2031.

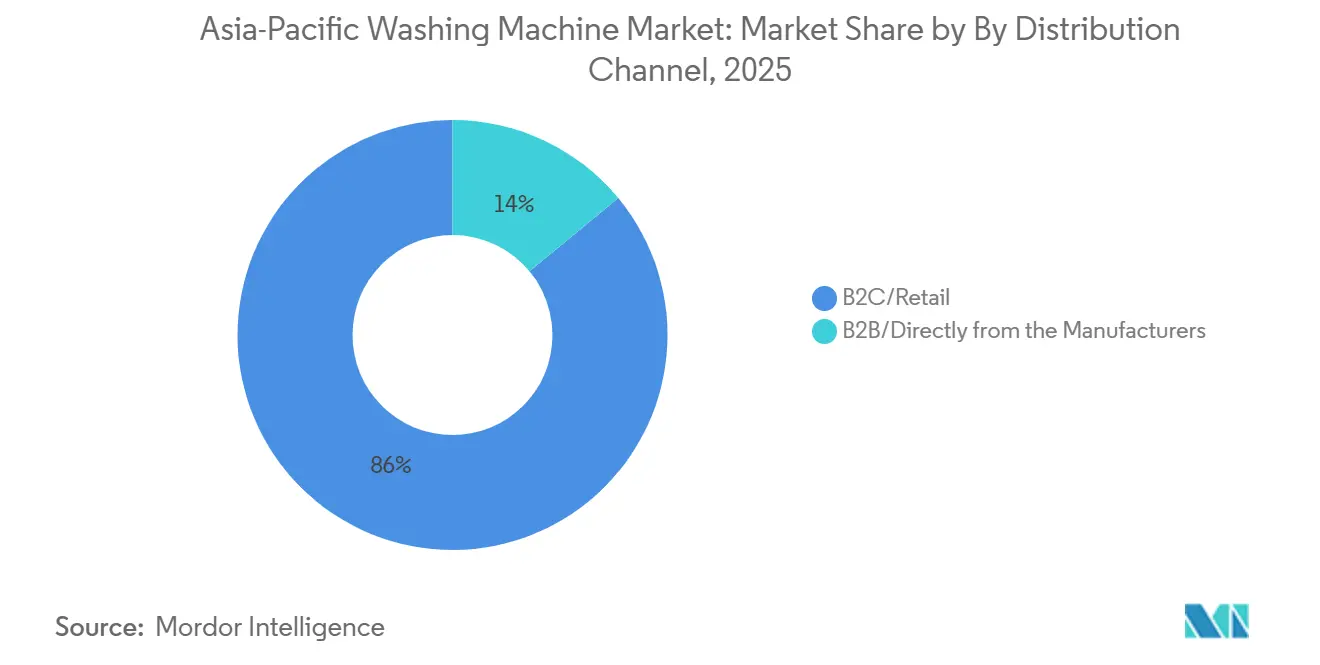

- By distribution channel, B2C/ retail captured 86.00% of 2025 transactions, and online (within B2C) is forecast to grow at a 7.60% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Washing Machine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Energy- and water-efficiency policy tightening triggers replacement demand | +0.8% | China, India, Japan, Australia, SEA core markets | Medium term (2-4 years) |

| Rapid e-commerce and omnichannel adoption for Major Domestic Appliances | +1.2% | Global, strongest in China, India, SEA; accelerating in developed Asia-Pacific | Short term (≤ 2 years) |

| Premiumization and AI-enabled feature adoption lift ASPs in urban segments | +0.6% | China Tier-1, Japan, South Korea, Singapore, Australia | Medium term (2-4 years) |

| Capacity upshifts to ≥8 kg in family households | +0.4% | India, Indonesia, Philippines, China Tier-2/3 | Long term (≥ 4 years) |

| Subscription/lease-to-own models expand access in Korea and are spreading in SEA | +0.2% | South Korea, Malaysia, Thailand, Taiwan; pilot in Vietnam | Long term (≥ 4 years) |

| OEM–detergent ecosystem integrations accelerate smart uptake | +0.3% | Global, led by China, India, SEA, and Europe partnerships spilling into the Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Energy and Water Efficiency Policy Tightening Triggers Replacement Demand

China’s 2026 home appliance trade-in scheme narrows subsidy eligibility to top-class efficiency models and streamlines the number of eligible categories, prompting portfolio refreshes and accelerating upgrades in the Asia-Pacific washing machine market. Complementary labeling frameworks at national and city levels are strengthening in Asia, with Hong Kong’s updated Mandatory Energy Efficiency Labelling Scheme effective September 30, 2025, lifting grading thresholds and projecting meaningful energy savings across participating product classes [1]Electrical and Mechanical Services Department, “Mandatory Energy Efficiency Labelling Scheme,” HKSAR Government, emsd.gov.hk. India made Bureau of Energy Efficiency labeling mandatory for washing machines starting January 1, 2024, which is steering product development toward inverter motors and efficient wash programs that reduce running costs for households [2]Bureau of Energy Efficiency, “Star Labeling for Washing Machines,” BEE India, beeindia.gov.in. In Japan, METI’s Top Runner program continues to refine targets that raise the performance floor, while local subsidies such as zero-emission point schemes support the replacement of older stock with high-efficiency configurations. Independent analyses suggest that stronger minimum performance standards can deliver significant reductions in carbon and water intensity, reinforcing policy momentum across the region. Australia’s drought preparedness and water efficiency orientation further tilt the mix toward front loaders, which aligns with federal climate commitments and state-level conservation goals within the Asia-Pacific washing machine market.

Rapid E Commerce and Omnichannel Adoption for Major Domestic Appliances in Asia-Pacific

Digital events are catalyzing appliance sell through integrated delivery and installation, compressing the purchase journey, with Singles’ Day 2025 on major Chinese platforms highlighting strong year-over-year surges in traffic and orders for large appliances. Leading OEMs report a rising share of revenue from e-commerce marketplaces and brand-managed digital stores, supported by improved product pages, enriched media, and interactive formats that shorten discovery. Social commerce formats and live video shopping are advancing awareness and intent among younger cohorts, while unified fulfillment links pre-sale content with post-sale service in the Asia-Pacific washing machine market. OEM software features now complement channel strategies; barcode scan and smart home integration direct consumers to efficient wash cycles and reinforce repeat use after the initial hardware sale. As online share expands, offline showrooms compete on experience, demonstrations, and same-day setup to keep pace with the convenience advantages established by digital channels across Asia-Pacific.

Premiumization and AI-Enabled Feature Adoption Lift ASPs in Urban Segments

AI-driven washer-dryer combos are a visible catalyst for premium adoption, with flagship launches posting six-figure unit milestones and adding features that reduce energy consumption without compromising cycle outcomes. Cycle optimization, multi-fabric detection, and real-time soil sensing now converge with auto-dosing to improve cleaning performance and lower resource use in the Asia-Pacific washing machine market. Large brands are also scaling smart home connectivity through mobile apps for remote control, alerts, and predictive maintenance that keeps machines running efficiently over longer lifecycles. At the very top of the price ladder in China, premium lines secured a dominant early share within segments priced above RMB 20,000 as AI-assisted wash-dry care platforms expanded choice for affluent replacement buyers. In Japan and South Korea, replacement cycles increasingly favor heat pump configurations and advanced fabric care features, adding value to mature but technologically advanced segments in the Asia-Pacific washing machine market.

Capacity Upshift to ≥8 kg in Family Households

Households are moving toward larger drums to consolidate weekly loads, with 8–10 kg machines emerging as a new baseline for families seeking to reduce cycle count and time expenditure. Retail guidance across Asia-Pacific directs multi-person households to 8–9 kg options as the best balance between load size and efficiency, while highlighting leading models from global brands. Premium entrants are also expanding capacity with stacked or triple drum architectures that eliminate manual transfer and shorten end-to-end cycle time for urban households in tier one cities [3]Haier Corporate Affairs, “Casarte and AI Vision Launches,” Haier Smart Home, haier.com. Regulatory and labeling programs are pushing water and energy efficiency alongside capacity, reinforcing demand for front loaders where water scarcity is a priority. In turn, OEMs deploy smart sensors and dosing to decouple bigger drums from proportional increases in energy and water use, strengthening the case for a capacity upshift in the Asia-Pacific washing machine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity and long replacement cycles reduce velocity | -0.7% | India, Indonesia, Philippines, Vietnam, China Tier-3/rural | Long term (≥ 4 years) |

| Water and power infrastructure constraints in emerging Asia-Pacific markets | -0.5% | India, Indonesia, Myanmar, rural China, Pakistan | Medium term (2-4 years) |

| Microfiber emission and wastewater compliance raising design/BoM costs | -0.3% | Global with early enforcement in Australia, potential China/India adoption | Long term (≥ 4 years) |

| Margin compression from event-led promotions and social commerce in China/SEA | -0.4% | China, SEA (TikTok Shop, Shopee, Lazada markets) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity and Long Replacement Cycles Reduce Velocity

Long household ownership slows down unit turnover in the Asia-Pacific washing machine market, especially when durable inverter platforms and heat pump systems extend useful life without loss of performance. Household replacement decisions also remain sensitive to up-front pricing and availability of financing, which affects the pace of shift from semi-automatic to fully automatic models in value-conscious segments. Policy supports help, but do not fully offset price resistance, as China’s 2026 trade-in scheme restricts eligibility to top-class models and trims the number of subsidized categories. In Southeast Asia, interest in smart features is high, yet many shoppers abandon carts when AI add-ons lift prices beyond accepted thresholds compared with basic equivalents. High return rates linked to impulse purchases during large promotional events can also amplify cost pressure on sellers, encouraging a cautious approach to pricing and inventory. As OEMs rebalance portfolios toward mid-price configurations that deliver visible efficiency gains, demand elasticity improves but does not erase the drag from extended replacement cycles in price-sensitive cohorts within the Asia-Pacific washing machine market.

Water and Power Infrastructure Constraints in Emerging Asia-Pacific Markets

Limited access to safe water and reliable electricity constrains the serviceable base in several Asia-Pacific economies, slowing adoption of fully automatic models where utility infrastructure is weak. Water quality and scarcity concerns in parts of India and Southeast Asia amplify the need for low-pressure, low-water designs and adaptive cycles that can deliver results under variable conditions [4]Stockholm International Water Institute, “Water Access and Quality in South Asia,” SIWI, siwi.org. A significant population across developing Asia still lacks affordable access to grid electricity and essential appliances, with off-grid and decentralized solutions advancing but not yet at scale. Standards and certification schemes under ASEAN energy labeling improve transparency and raise the floor on performance, but enforcement gaps and uneven wastewater treatment capacity persist outside primary urban centers. In markets with voltage fluctuations, buyers and brands favor surge-tolerant machines and protective features that prevent damage, a consideration that shapes product choice and speeds in the Asia-Pacific washing machine market. As infrastructure improves and awareness grows, these headwinds should be eased, yet they remain a structural factor in near-term addressability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Front Load Drums Gain on Efficiency, Top Load Retains Volume Lead

Top load washing machines accounted for 54.94% of the Asia-Pacific washing machine market size in 2025, while front load models are set to expand at a 3.75% CAGR through 2031 as resource efficiency requirements tighten in water-stressed regions. Urban buyers gravitate to compact or built-in drum designs and advanced washer-dryers that reduce space needs and remove manual transfer steps. Premium front loaders also align with evolving labeling regimes that emphasize lower water and energy per kilogram of laundry. Meanwhile, top load remains favored for shorter cycles, ease of loading, and affordability in several emerging sub-markets of the Asia-Pacific washing machine market.

OEMs are closing the convenience gap with features that let users optimize cycles and dosing through mobile apps and on-device intelligence, making front-load adoption smoother for first-time buyers. Comparative narratives around fabric care, gentler tumble, and reduced microfiber shedding provide an additional rationale for premium drums, reinforced by ongoing work to standardize fiber shedding measurement. As labeling thresholds rise and drought preparedness stays in focus, front-load penetration is likely to climb while top-load defends its footprint in mid-price and rural segments within the Asia-Pacific washing machine market.

By Capacity: 5–8 kg Anchors Family Demand, above 8 kg Logs Fastest Expansion

The 5–8 kg segment commanded 48.21% share of the Asia-Pacific washing machine market size in 2025, and above 8 kg is projected to grow at a 5.34% CAGR through 2031, reflecting the core needs of three to six-member households. Regional retail guidance places 8–10 kg machines as the preferred fit for family loads where users want to reduce weekly cycle count without sacrificing results. Capacity upshift also aligns with premium offerings that combine high-efficiency wash with heat pump drying and AI cycle guidance in the Asia-Pacific washing machine market.

At the upper end, extra-large or multi-drum solutions create time savings for dual-income households and streamline care for bulky items. For compact homes, retailers in Australia highlight 8–9 kg options as a balance point on space, load size, and efficiency, especially when coupled with modern labeling and water-saving features. As star rating tables and test protocols index energy use to capacity, OEMs rely on load sensing and accurate auto dosing to preserve ratings in larger drums across the Asia-Pacific washing machine market.

By Technology: Conventional Machines Sustain Dominance Amid Infrastructure Realities

In 2025, conventional washing machines held 71.34% of the Asia-Pacific market, and smart/connected (IoT) is projected to grow at a 4.76% CAGR through 2031. This reflects a preference for efficient, reliable machines over fully connected ones, driven by infrastructure gaps and budget constraints. Policies reward energy and water efficiency but do not mandate IoT features. China's 2026 trade-in plan narrows subsidies to top-tier efficiency models, excluding incentives for connected features. Limited access to safe water and inconsistent power in parts of Asia further reduce the appeal of always-connected machines. Conventional semi-automatic models remain relevant with features like zero-pressure filling and hard-water treatment. Even in major Chinese cities, premium conventional models emphasizing inverter efficiency and reliability, such as multi-drum configurations, are gaining traction among users prioritizing performance over app controls.

Smart and connected washing machines remain a niche in the region, with adoption concentrated in developed markets like Japan, South Korea, Singapore, and Australia, where smart-home integrations and after-sales connectivity are strong. Regulatory measures, such as India's mandatory star labeling, treat efficient inverters and IoT-equipped models equally, limiting any policy advantage for connectivity. To address affordability, leading brands are introducing hybrid models with features like fabric sensing and auto-dosing at mid-tier prices, offering convenience without full IoT integration. As ASEAN harmonizes energy labelling, cost-efficient conventional platforms are expected to retain an edge until utility programs provide clearer incentives for connected features.

By End User: Residential Anchors Volume, Commercial Segment Sprints Ahead

Residential comprised 88.02% of the 2025 volume, while commercial deployments across hospitality, multi-family, factory dormitories, and healthcare are growing faster at a 5.34% CAGR through 2031. Residential buyers focus on aesthetics, connected convenience, and star ratings, whereas commercial procurement prioritizes durability, uptime, and total cost of ownership in the Asia-Pacific washing machine market.

Subscription and rental pilots blur boundaries between residential and commercial, offering managed services that bundle installation, maintenance, and consumables under one price. These models fit co-living and service department use cases and may spread into broader residential channels as consumers trade up for convenience and predictable monthly costs in the Asia-Pacific washing machine market.

By Distribution Channel: B2C/Retail Channels Surge, Offline Defends Through Experience

B2C/retail channels captured 86.00% of 2025 transactions, and online (within B2C) is projected to grow at a 7.60% CAGR, reflecting event-driven spikes and the appeal of bundled installation, trade-in logistics, and financing. Major sales festivals continue to elevate appliance revenue and order volume, while same-day or next-day services raise expectations for convenience in the Asia-Pacific washing machine industry.

Offline retailers adapt with immersive displays, in-store demos, and white-glove setup that mirrors online service bundles to preserve share. As omnichannel paths become standard, shoppers research across touchpoints and finalize purchases where the perceived value and support are strongest in the Asia-Pacific washing machine market.

Geography Analysis

China accounted for 49.08% of the Asia-Pacific washing machine market share in 2025, supported by strong brand portfolios and increasingly digital routes to purchase. Trade-in incentives in 2026 narrowed eligibility to first-class efficiency models and trimmed the number of subsidized categories, which shifts value toward premium and compliant configurations. Leading domestic players reported substantial contributions from e-commerce channels in 2025 as platform investments and short video engagement improved discovery and conversion. Over the forecast period, replacement-led demand and stricter labeling norms are expected to reinforce front-load and all-in-one washer-dryer adoption in humid coastal cities and water-stressed northern provinces in the Asia-Pacific washing machine market.

India is set to be the fastest-expanding major demand pool as penetration climbs from a low base and mandatory energy labeling guides product choices toward efficient, fully automatic machines. Access to safe water and consistent power varies by region, making low-pressure-tolerant and surge-resistant features important differentiators for first-time buyers. As households trade up from semi-automatic to fully automatic formats, capacity preferences are rising, helped by the availability of EMI options and bundled installation that reduce frictions in the Asia-Pacific washing machine market.

Japan, South Korea, Australia, and Southeast Asia present a mix of replacement-driven and first-time buyer dynamics shaped by local policies and channel structures. In Japan and South Korea, Top Runner aligned and heat pump platforms anchor the premium tier, with connected features and service packages adding value to mature segments. Australia’s water efficiency emphasis keeps front loaders in focus, supported by labeling practices that guide consumers to lower water per kg outcomes. In Southeast Asia, demand for smart features is rising in parallel with high cart abandonment when AI premiums exceed acceptable thresholds, which drives interest in mid-tier models that preserve essentials at palatable prices. As RCEP rules encourage regionalized sourcing and tariff reductions phase in, ASEAN procurement and assembly footprints are adjusting to meet 40% regional value content goals, supporting long-term availability in the Asia-Pacific washing machine market. Select markets such as Vietnam have shown notable share gains for key brands, helped by efficient washer-dryer launches and targeted channel strategies.

Competitive Landscape

The Asia-Pacific washing machine market remains concentrated around global and regional leaders, reinforced by R&D intensity, localized manufacturing, and service coverage. Chinese champions leverage cost-competitive engineering and channel breadth to dominate mid to low tiers, while Korean and Japanese incumbents defend premium price points with AI-enabled care, heat pump drying, and connected ecosystems. Strategic bets center on high-efficiency washer-dryers for humid climates, capacity upshift to reduce weekly cycles, and integrated filtration to address microfiber discharge requirements in the Asia-Pacific washing machine market.

Platform alignment is now critical: OEMs are embedding app features that nudge efficient behavior and streamline detergent selection, while partnerships with detergent majors target cartridge-based refills and short-cycle performance. Subscription and lease-to-own propositions expand access and open recurring revenue streams that stabilize economics versus promotional sales, especially in advanced Asia-Pacific markets. Leading firms also engage in standards-setting bodies to shape test methodologies on energy, water, and microfiber shedding, which helps align regulatory timelines with product pipelines in the Asia-Pacific washing machine market.

Localization and supply chain design are evolving under regional trade frameworks that link tariff preferences to content thresholds, encouraging OEMs to deepen Asia-Pacific sourcing and assembly. Marketing execution continues to shift online, with marketplace and direct-to-consumer storefronts driving incremental share through content, configuration, and event participation. As competition intensifies, product roadmaps emphasize AI-assisted fabric care, accurate auto dosing, and shorter eco cycles, with flagship washer-dryers setting user experience benchmarks for the Asia-Pacific washing machine market.

Asia-Pacific Washing Machine Industry Leaders

Haier Smart Home

LG Electronics

Samsung Electronics

Midea Group

Whirlpool Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Samsung previewed expanded AI-connected laundry features ahead of CES 2026, including faster full cycle times, a Booster Heat Exchanger, and Auto Open Door+, alongside AI Wash & Dry+ with multi-sensor fabric and soil detection.

- January 2026: China unveiled a 2026 subsidy scheme for home appliance trade-ins, offering consumers up to CNY 1,500 per item at 15% of the final purchase price for top-class energy-efficient machines and requiring integrated delivery and old appliance collection.

- September 2025: Sharp launched the Plasmacluster drum washer dryer ES 12X1 with generative AI laundry advice and high energy efficiency features for Japan’s premium tier.

Asia-Pacific Washing Machine Market Report Scope

A washing machine is an electronic home appliance that is used to wash various types of clothes without applying any physical effort.

The study gives a brief description of the Asia-Pacific washing machine market and includes details on price ranges, different types of various brands, and the launch of products. The Asia-Pacific washing machine market is segmented by product type, technology, and distribution. By product, the market is segmented into front-load, top-load, and twin tub. By Capacity, the market is segmented into below 5 kg, 5 - 8 kg, and above 8 kg. By technology, the market is segmented into Conventional and Smart / Connected (IoT). By end user, the market is segmented into residential and commercial. By distribution channel, the market is segmented into B2C/Retail and B2B/Directly from the manufacturers. By geography, the market is segmented into China, India, Japan, South Korea, Australia, and the rest of Asia-Pacific. The report offers market size and forecasts for the Asia-Pacific washing machine market in value (USD) for all the above segments.

By Product Type

| Front Load | With Dryers |

| Without Dryers | |

| Top Load | With Dryers |

| Without Dryers | |

| Twin Tub |

By Capacity

| Below 5 kg |

| 5 – 8 kg |

| Above 8 kg |

By Technology

| Conventional |

| Smart / Connected (IoT) |

By End User

| Residential |

| Commercial |

By Distribution Channel

| B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | |

| Online | |

| Other Distribution Channels | |

| B2B/Directly from the Manufacturers |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South-East Asia |

| Rest of Asia-Pacific |

| By Product Type | Front Load | With Dryers |

| Without Dryers | ||

| Top Load | With Dryers | |

| Without Dryers | ||

| Twin Tub | ||

| By Capacity | Below 5 kg | |

| 5 – 8 kg | ||

| Above 8 kg | ||

| By Technology | Conventional | |

| Smart / Connected (IoT) | ||

| By End User | Residential | |

| Commercial | ||

| By Distribution Channel | B2C/Retail | Multi-brand Stores |

| Exclusive Brand Outlets | ||

| Online | ||

| Other Distribution Channels | ||

| B2B/Directly from the Manufacturers | ||

| By Geography | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the Asia-Pacific washing machine market size and growth outlook for 2031?

The Asia-Pacific washing machine market size was USD 27.84 billion in 2025 and is projected to reach USD 33.97 billion by 2031 at a 3.37% CAGR.

Which product type is growing fastest in the Asia-Pacific washing machine market?

Front-load models are the fastest-growing product type with a 3.75% CAGR through 2031, while top-load retains the largest share.

How are online channels shaping demand in the Asia-Pacific washing machine market?

Online/digital channels are on track for a 7.60% CAGR through 2031, helped by bundled installation, trade-in logistics, and event-led promotions.

What capacity sweet spot is most popular among Asia-Pacific households?

The 5–8 kg segment anchors family demand, accounting for 48.21% share in 2025 and above 8 kg projected to grow at a 5.34% CAGR through 2031 as households aim to reduce weekly cycle counts.

What policy changes most affect appliance replacement in Asia-Pacific?

Efficiency labeling and trade‑in programs in China, India’s mandatory BEE labels, Hong Kong’s tightened grading, and Australia’s water‑efficiency focus all nudge upgrades toward compliant, resource-efficient models.

Page last updated on: