Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

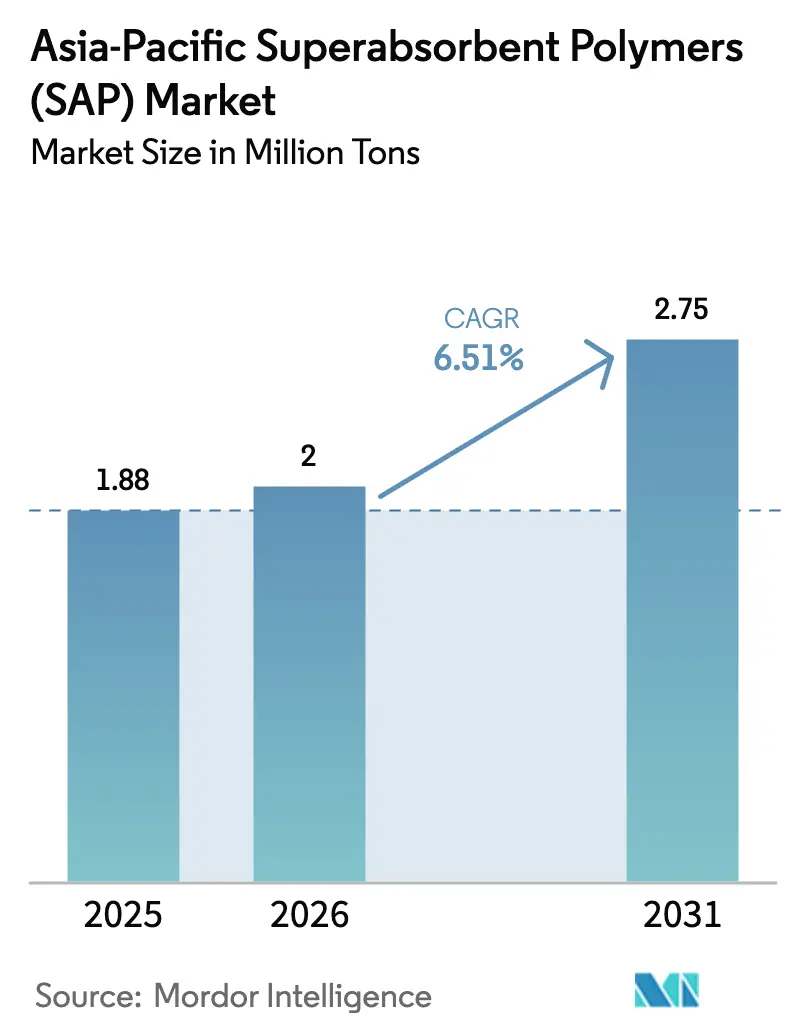

| Base Year Market Size (2025) | 1.88 Million tons |

| Market Volume (2026) | 2 Million tons |

| Market Volume (2031) | 2.75 Million tons |

| Growth Rate (2026 - 2031) | 6.51% CAGR |

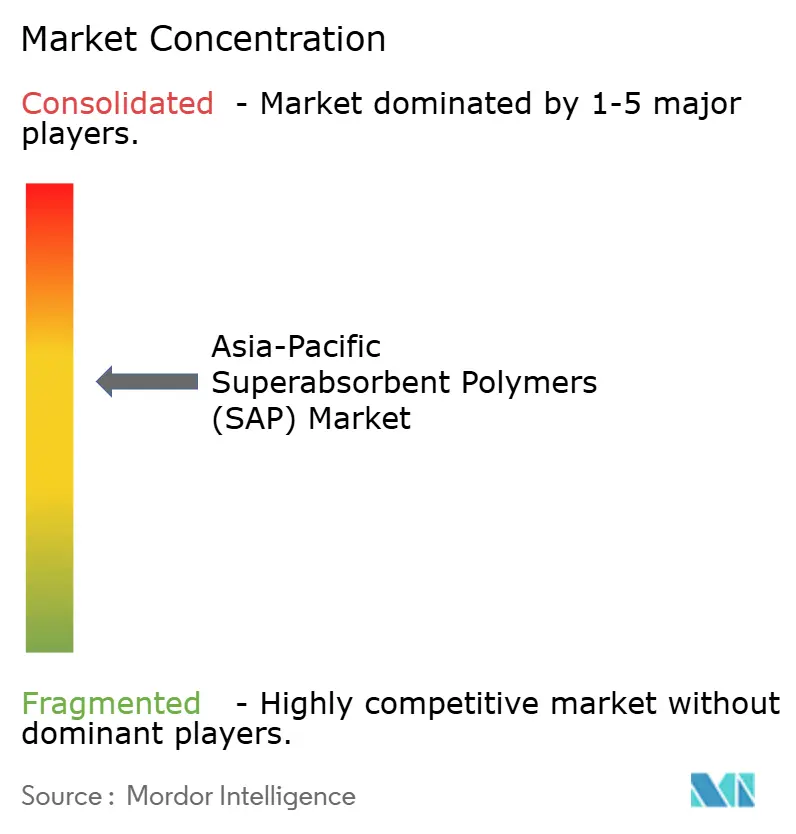

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Superabsorbent Polymers (SAP) Market Analysis by Mordor Intelligence

The Asia-Pacific Superabsorbent Polymers Market size is expected to grow from 1.88 million tons in 2025 to 2 million tons in 2026 and is forecast to reach 2.75 million tons by 2031 at a 6.51% CAGR over 2026-2031. The region’s outsized role in diaper and adult incontinence production anchors demand, while agricultural moisture-retention uses are expanding from a small base. China supplies most of the incremental capacity, yet rising per-capita income across India and Southeast Asia underpins volume growth in lower-tier cities. Regulatory attention to microplastics and feedstock volatility is prompting research and development into bio-based grades, even as conventional acrylic-acid chemistries remain cost-competitive. On the supply side, Japanese incumbents defend share through process upgrades, whereas Chinese entrants leverage feedstock integration to price aggressively in export and spot markets.

Key Report Takeaways

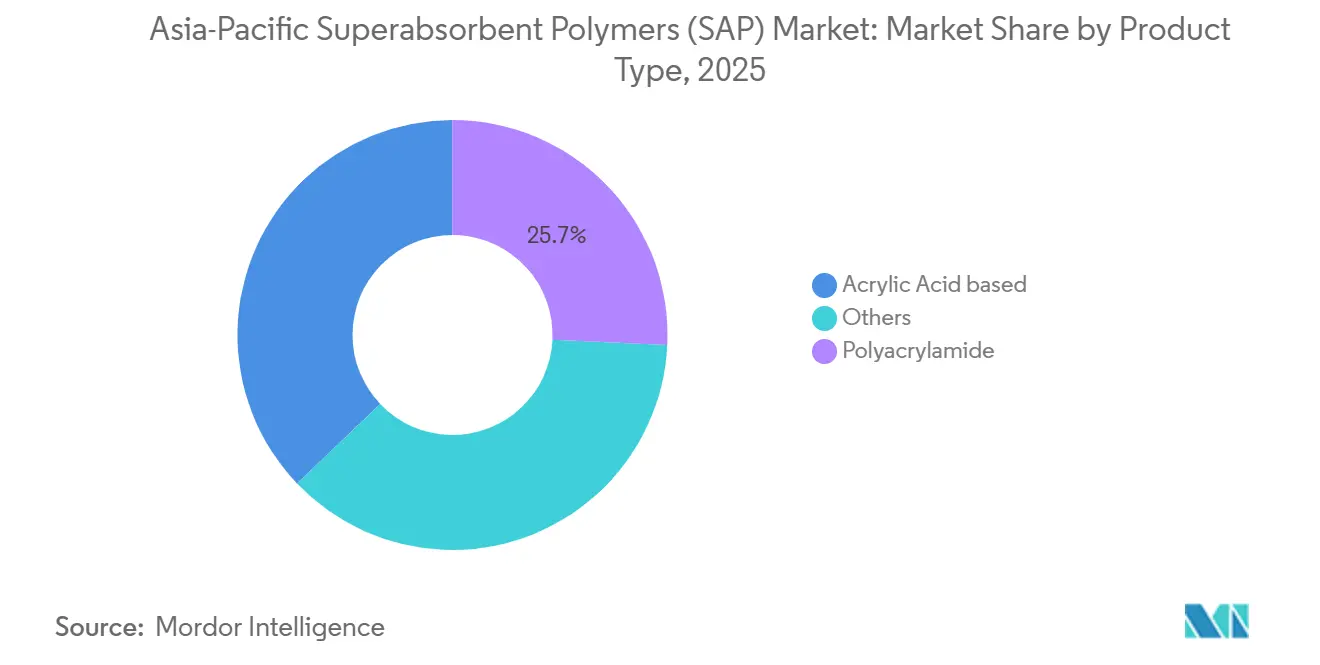

- By product type, polyacrylamide captured 25.74% of the Asia-Pacific superabsorbent polymers market share in 2025 and is forecast to expand at a 6.08% CAGR through 2031.

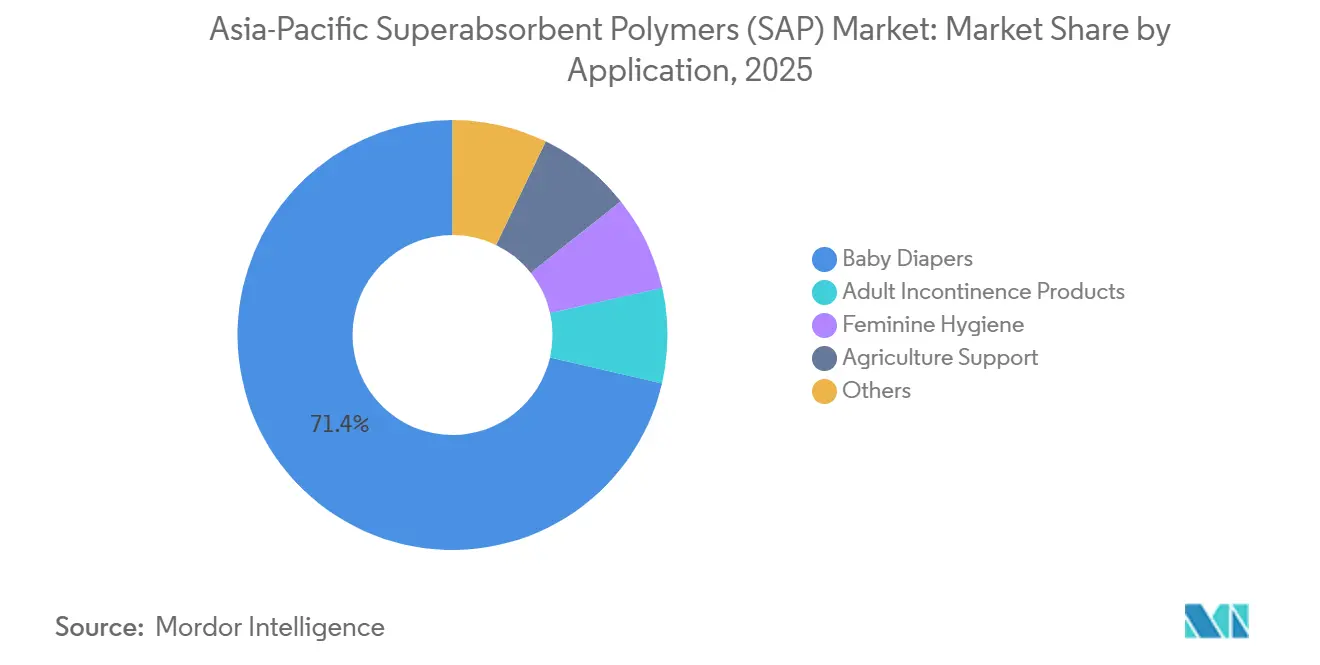

- By application, baby diapers accounted for 71.37% of the Asia-Pacific superabsorbent polymers market size in 2025 and are advancing at a 6.01% CAGR to 2031.

- By geography, China led with a 57.23% volume share in 2025, while its 7.48% CAGR to 2031 outpaces every other national market in the region.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Superabsorbent Polymers (SAP) Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising hygiene awareness and disposable incomes | +1.8% | China, India, Southeast Asia | Medium term (2-4 years) |

| Rapid aging population boosting adult incontinence demand | +1.2% | Japan, South Korea, urban China | Long term (≥4 years) |

| Expansion of diaper manufacturing capacity | +1.5% | China, India, Vietnam, Indonesia | Short term (≤2 years) |

| Government incentives for water-saving agriculture | +0.6% | India, Australia, parts of China | Medium term (2-4 years) |

| Shift toward bio-based SAP chemistries | +0.4% | Japan, South Korea, Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising Hygiene Awareness And Disposable Incomes

Lower-tier cities in China and India are switching from cloth to disposables as household incomes rise, keeping penetration below 15% in many Tier-3 districts but creating a steep catch-up path to coastal averages above 90%. Unicharm’s new Gujarat plant will lift its Indian output by 50%, while Kimberly-Clark’s USD 50 million Nanjing Phase III project, due September 2025, adds four lines aimed at inland demand. Government sanitation campaigns have normalized diaper use even in rural settings, and income elasticity estimates between 1.2 and 1.5 signal that GDP expansion translates directly into superabsorbent polymer offtake. Multinationals localize production for fiscal advantages, yet still rely on regionally sourced SAP grades customized for thinner cores. The driver’s medium-term runway remains intact despite near-term macro cycles.

Rapid Aging Population Boosting Adult Incontinence Product Demand

Japan’s mature market already sells more adult pants than baby diapers, and South Korea’s 65-plus cohort is on track to hit 46.4% by 2070. Adult briefs command unit prices 30%–50% higher than baby products, rewarding SAP suppliers capable of low-rewet, odor-control chemistries. Chinese urban centers are beginning to shift in the same direction as population aging accelerates. This demand mix change favors producers with advanced surface-treatment know-how over commodity players. Long-term visibility allows incumbents to allocate research and development toward high-margin grades even while defending baby-diaper volumes.

Expansion Of Diaper Manufacturing Capacity Within APAC

Vietnam, Indonesia, and western India continue to attract greenfield diaper investments that shorten lead times and exploit labor cost advantages[1]Indian Chemical News Staff, “Unicharm Expands India Diaper Capacity,” indianchemicalnews.com. Nippon Shokubai will add 50 kilotons per year in Indonesia by July 2027, securing local offtake from new hygiene plants. Once a diaper line is tuned to a given SAP’s absorption curve and particle-size distribution, switching costs rise, reinforcing local supply contracts. Capacity moves in upstream acrylic acid—such as BASF’s Zhanjiang complex—are set to support these downstream expansions. The result is a virtuous short-term lift in regional SAP demand.

Government Incentives For Water-Saving Agriculture Using SAP Hydrogels

Field trials in the Indo-Gangetic Plains showed yield gains of up to 19% under full irrigation and more than 50% under rain-fed regimes when biopolymeric SAP was applied at 2.5 kg per hectare[2]Nature Editorial Team, “Superabsorbent Hydrogels Improve Water Productivity,” nature.com. Subsidy programs in Gujarat and Rajasthan now reimburse part of the product cost, stimulating adoption despite farmer price sensitivity. Australia’s horticulture sector is taking a similar path as drought cycles intensify, with vineyards and golf courses using SAP to cut irrigation rounds. Scaling remains limited by current farm-grade prices, yet medium-term public funding is set to widen the addressable base.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile acrylic acid feedstock pricing | -1.1% | China, Southeast Asia, India | Short term (≤2 years) |

| Environmental and end-of-life concerns | -0.5% | Japan, South Korea, Australia | Medium term (2-4 years) |

| Looming microplastics regulations | -0.3% | Japan, South Korea (EU spillover) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Acrylic Acid Feedstock Pricing

Spot acrylic acid in China fell from CNY 15,800 per ton in February 2022 to CNY 6,550 by December 2022, squeezing margins for SAP makers tied to fixed diaper contracts. New acrylate units from BASF and Changhong Polymer will add more than 450 kilotons of capacity by 2026, potentially tempering spikes, but exposure remains acute until integration spreads. Sanyo Chemical’s March 2024 exit after a JPY 1.6 billion loss spotlights how non-integrated producers are most vulnerable. Hedging strategies and propane-based acrylic routes may mitigate the short-term drag, yet pricing volatility still subtracts 1.1 percentage points from forecast growth.

Environmental And End-Of-Life Concerns For Petro-Based SAP

Roughly 300,000 used diapers enter global waste streams every minute, drawing scrutiny to landfill persistence of polyacrylates. Japan funds chemical-recycling pilots to recover acrylic acid, while BASF released a zero-PCF grade certified under ISCC PLUS in February 2025. Consumer preference studies in South Korea show willingness to pay modest premiums for lower-footprint disposables, but scalability challenges hold back immediate volume shifts. The medium-term restraint therefore reduces the CAGR by half a point.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cost Advantages Keep Polyacrylamide At The Forefront

Polyacrylamide captured 25.74% of regional volume in 2025 and is on track for a 6.08% CAGR, giving it the fastest growth among established chemistries in the Asia-Pacific superabsorbent polymers market. Acrylic-acid grades still dominate premium baby and adult briefs thanks to superior absorption and retention, but they concede price-sensitive agricultural and feminine-care niches to polyacrylamide.

Producers enhance acrylic-acid SAP through surface-treatment upgrades that cut gel-blocking and enable thinner diaper cores, a key requirement for value brands pushing down gram-per-piece costs. Nippon Shokubai’s 2022 global retrofit that lifted plant productivity by roughly 10% underscores how incumbents lean on process gains to defend share. Bio-based or cellulose-grafted SAP posts double-digit growth, helped by pilot launches such as BAYSE. The trajectory suggests a gradual mix shift rather than a sudden displacement, so supply chains for both legacy and emerging chemistries will coexist through the decade.

By Application: Baby Diapers Provide Volume, Adult Incontinence Drives Margin

Baby diapers represented 71.37% of total volume in 2025 and will advance at 6.01% through 2031, maintaining the bulk of the Asia-Pacific superabsorbent polymers market demand. Brand expansions in China, India, and Vietnam anchor the segment's growth. The segment is bifurcating into premium and value tiers, forcing SAP suppliers to support a two-tier product line.

Adult briefs grow faster from a smaller base as Japan and South Korea age, with urban China quickly following. Unit margins are higher because formulations must cut rewet and control odor, elevating technical requirements. Feminine pads consume SAP mainly in liquid cores, and global brands are testing ultra-thin formats that need rapid-acquisition grades. Agriculture registers the highest percentage growth in public subsidies in water-stressed regions. Other industrial uses - cable-wrap, concrete curing - round out demand yet remain opportunistic in volume terms.

Geography Analysis

China held 57.23% of regional volume in 2025 and is projected to post a 7.48% CAGR through 2031, cementing its dominance in the Asia-Pacific superabsorbent polymers market. Satellite Chemical’s planned 300-kiloton complex and Changhong Polymer’s propane-route acrylic acid unit illustrate how domestic groups pair feedstock security with downstream expansion. Policy incentives for Western China’s arid zones may create a small but strategic offtake for agricultural-grade SAP, while coastal clusters keep diaper production concentrated near export hubs.

India offers the largest white-space opportunity given diaper penetration below 15% in many Tier-2 locales. Unicharm will raise domestic output by 50% via its third Gujarat plant, and local brand Nobel Hygiene is fundraising to scale rural distribution. Agricultural trials in the Indo-Gangetic Plains report yield gains above 50% under rain-fed conditions when SAP is applied, prompting state subsidies. These dynamics suggest India could deliver double-digit volume growth even if national CAGR figures are yet to be fully quantified.

Japan and South Korea display contrasting demographics: shrinking birth rates slash newborn diaper sales, yet senior-care demand lifts adult briefs. Importantly, both governments are early movers on environmental standards, channeling grants toward recycling pilots and bio-based alternatives. Australia and New Zealand remain niche in volume but lead per-capita adoption of farm-grade SAP thanks to chronic drought. Rest of Asia-Pacific - Vietnam, Indonesia, Thailand, Philippines - absorbs capacity relocations from China; Vietnam alone is adding 40% diaper capacity via multinational investments, creating a robust pipeline for regional SAP offtake.

Regulatory Landscape

Regulation affecting SAP in Asia-Pacific increasingly sits at the intersection of chemicals registration and hygiene-product quality requirements. In China, the Ministry of Ecology and Environment (MEE) issued draft revisions (June 2026) to the Measures for the Environmental Management Registration of New Chemical Substances, shifting compliance toward administrative approval-based pathways and raising the bar for how polymers and related chemistries are brought to market. National standards such as GB/T 44422-2024 (implemented December 1, 2024) for cross-linked polyacrylic acid absorbent resins used in urine absorption aids and GB/T 20405.2-2024 (implemented January 1, 2025) for residual monomer testing tighten product and quality-control expectations relevant to diaper and incontinence supply chains.

Japan continues to refine chemicals oversight under CSCL through more structured polymer assessment routes. The April 2026 guidance issued by MHLW, METI, and MOE for the Polymer Flow Scheme (effective June 1, 2026) introduces updated evaluation criteria based on chemical structure and properties, which affects testing and notification strategies for SAP and upstream polymer intermediates. Across the region, stricter registration mechanics combined with clearer test-method frameworks increases the need for documentation, traceability, and in-region compliance capabilities for SAP producers and importers.

Value Chain Analysis

The Asia-Pacific SAP value chain begins with petrochemical feedstocks, notably propylene to acrylic acid and acrylates for the dominant polyacrylate routes, followed by polymerization, cross-linking, drying, milling, and surface-treatment steps that tailor absorption, gel strength, and rewet performance for specific hygiene formats. China is a central node because it pairs acrylic acid and SAP capacity additions with downstream diaper manufacturing clusters, while Japanese incumbents compete through process upgrades and specialty grades that support thinner cores and higher-performance adult incontinence products.

Downstream demand is concentrated among disposable hygiene manufacturers (baby diapers, adult incontinence, and feminine hygiene). Qualification cycles and tuned formulations make switching costs meaningful once a SAP grade is locked into a production line. Distribution typically relies on direct contracts for large hygiene accounts and converters, with some spot trading for commodity grades, particularly when acrylic acid pricing swings. Non-hygiene outlets such as agricultural moisture retention and select industrial uses remain smaller, but they add additional channels for off-spec or differentiated products, while sustainability initiatives (recycled-content accounting and circularity programs) increasingly influence supplier selection and product development priorities.

Competitive Landscape

The Asia-Pacific superabsorbent polymers market is moderately consolidated. Leading players in the market are facing intense price competition from vertically integrated Chinese suppliers. Nippon Shokubai, the global volume leader, is investing in an Indonesian debottleneck to serve Southeastern Asian demand while shifting capital into higher-margin specialties. Innovation vectors cluster around carbon-neutral production and circularity.

Asia-Pacific Superabsorbent Polymers (SAP) Industry Leaders

NIPPON SHOKUBAI CO., LTD.

SUMITOMO SEIKA CHEMICALS CO.,LTD.

LG Chem

BASF SE

SANYO CHEMICAL, LTD.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A key near-term whitespace is local supply aligned to fast-growing hygiene manufacturing footprints in Southeast and South Asia, where logistics and lead times shape supplier choice alongside cost. Nippon Shokubai has signaled this direction through its Indonesian expansion program at PT Nippon Shokubai Indonesia in Cilegon, including a new 50,000 t/y SAP plant that leverages on-site acrylic acid integration and is tied to a documented investment program. Integrated, in-region capacity builds create opportunities for SAP suppliers that can qualify locally with diaper producers and offer more stable pricing structures despite acrylic acid volatility.

A second opportunity is performance and sustainability differentiation as scrutiny on end-of-life impacts and microplastics-linked concerns tightens. Sumitomo Seika’s SAP technology scale-up pathway, including its dedicated pilot plant at Himeji and follow-on chemical-recycling pilot activity, points to ongoing investment in circular solutions that can fit brand-owner and retailer requirements for lower-footprint hygiene products. Bio-based and biodegradable SAP development also has visible momentum through BAYSE positioning, creating room for suppliers that can provide drop-in grades (or blends) while meeting regional testing and quality standards such as residual monomer methods and application-specific resin requirements.

Recent Industry Developments

- June 2026: Sumitomo Seika Chemicals announced that its pilot facility for chemical recycling of superabsorbent polymers at the Himeji Works commenced operations. The initiative advances a circularity pathway for diaper-grade SAP and supports brand-owner discussions around end-of-life solutions and recycled-chemistry integration.

- August 2025: Nippon Shokubai, through PT Nippon Shokubai Indonesia, held a groundbreaking ceremony for a new 50,000 metric tons per year SAP plant in Cilegon, Indonesia, with commercial operation scheduled for July 2027. Adding capacity at an integrated acrylic acid site strengthens regional supply proximity to Southeast and South Asian hygiene clusters and supports tighter cost control versus imported intermediates.

- August 2024: Nippon Shokubai announced an SAP-related capacity and supply-chain initiative focused on strengthening its hygiene materials business footprint. The announcement continued capital allocation toward SAP competitiveness, supporting customer qualification efforts and product supply stability in Asia-Pacific.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as the demand and supply of superabsorbent polymers in Asia-Pacific, measured as volume sold into end uses such as hygiene absorbents and other absorbent applications within the region.

Scope exclusions: Excludes downstream finished products (like diapers themselves) and counts only SAP material volumes, not end-product retail value.

Segmentation Overview

- By Product Type

- Polyacrylamide

- Acrylic Acid based

- Others

- By Application

- Baby Diapers

- Adult Incontinence Products

- Feminine Hygiene

- Agriculture Support

- Others

- By Geography

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with mapping Asia-Pacific SAP demand pools and resin economics, then anchoring assumptions to public statistics and technical references. We relied on sources such as UN Comtrade for acrylic acid and polymer trade flows, national statistical agencies in key Asia-Pacific countries for industrial output indicators, and customs or port releases where available to understand short-term shipment direction.

To avoid building the model on one single signal, capacity and operating rate clues were also taken from company annual reports, investor presentations, and public plant announcements, then cross-checked using peer-reviewed polymer and absorbent-material journals. Patent databases were reviewed to understand where product innovation is moving (for example, bio-based and performance grades), and a paid subscription for company financials and business intelligence was used selectively to standardize regional revenue exposure and manufacturing footprint notes. The desk sources listed here are illustrative, and many other public documents were also used for data collection, validation, and research clarification.

Primary Interviews and Surveys

Primary work focused on validating how SAP volumes move into hygiene and non-hygiene uses across Asia-Pacific, and how pricing and formulation shifts affect realized demand. Interviews covered manufacturers, distributors, and downstream converters, and the discussions were used to stress-test assumptions on country-level demand, import dependence, and typical contract pricing patterns.

Coverage was kept balanced across major consuming markets and supply hubs in APAC, and follow-up checks were run when desk signals and interview feedback diverged on utilization, trade intensity, or application mix.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 15% | |

| Mid tier: 53% | Functional/Unit leaders: 25% | |

| Smaller Players: 17% | Managers: 60% |

Market-Sizing & Forecasting

Market sizing was built using a top-down, demand-pool approach, where hygiene consumption indicators are translated into SAP requirement per unit, and then rolled up across key Asia-Pacific countries before being reconciled to regional supply and trade signals. To keep the totals realistic, we corroborated the output with selective bottom-up approximations, such as sampling supplier volumes where disclosed, channel checks on typical shipment lots, and ASP x volume sense checks for major applications.

Inputs used in the model were chosen because they are observable and explain SAP usage changes in Asia-Pacific. These included diaper and adult incontinence product output trends, feminine hygiene consumption direction, agriculture water-retention adoption cues, acrylic acid feedstock availability and price direction, and net import or export movement for relevant polymer categories. Where data gaps existed for smaller countries, proxy ratios were applied using similar markets by income level and hygiene penetration, and then adjusted after interview feedback.

Forecasting was done through scenario analysis, supported by a simple multivariate regression on the most consistent drivers (hygiene output proxies, population aging signals, and feedstock price direction), with assumptions stress-tested for conservative and faster-growth cases. The final forecast was accepted only after the projected application mix and regional trade balance stayed within ranges that industry respondents considered practical.

Data Validation & Update Cycle

Validation was handled in several steps so that obvious inconsistencies were caught early. We compared modeled volumes against independent signals like announced capacity additions, trade direction by key hubs, and downstream hygiene production momentum, then reviewed any large variances at country and application level.

When an outlier appeared, the assumption was re-checked, and respondents were re-contacted if the gap could change the regional total in a meaningful way. Before sign-off, another analyst review pass is completed to confirm units, conversions, and time alignment, and the report is refreshed annually with interim updates when material events occur. Right before delivery, we run a last freshness check so clients receive the most updated view available.

Mordor Intelligence's Asia Pacific Superabsorbent Polymer Market Market Size Versus Other Published Estimates

Published estimates for Asia-Pacific SAP often do not match because they are not always sizing the same thing, even when the market name looks identical. Differences usually come from whether the metric is volume or value, how applications are grouped, and what pricing assumptions are used for the same year.

The gap also widens when one estimate uses older base-year pricing, or applies a single regional ASP without correcting for country mix and contract timing, which can matter in polymers. Some figures also blend finished hygiene product value with raw SAP material, which inflates totals if the scope is not carefully separated.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.00 M (2026) | |

| Industry Databook A | USD 3.85 B (2023) | Uses revenue sizing with a 2023 base year, and it appears to apply broad regional pricing assumptions, which can overstate totals when country mix and contract-price timing are not adjusted. |

| Market Outlook B | USD 3.85 B (2023) | Reports value for 2023 and may include a wider interpretation of SAP-related revenue across the chain, which can differ from material-only measurement and can shift totals when conversion factors are not made explicit. |

The table shows a clear split between volume-led and value-led reporting, and that alone can create a wide spread before any forecast choices are even discussed. Mordor Intelligence's approach treats the Asia-Pacific market as SAP material volume into defined applications, which keeps the estimate tied to consumption and trade signals instead of being driven mainly by ASP assumptions.

Key Questions Answered in the Report

What volume will the Asia-Pacific superabsorbent polymers market likely achieve by 2031?

Forecasts indicate the market will reach about 2.75 million tons, expanding at a 6.51% CAGR.

Which country contributes the largest demand for superabsorbent polymers in Asia-Pacific?

China leads with 57.23% of regional volume and is set to grow at 7.48% through 2031.

Which application segment generates the most SAP consumption in the region?

Baby diapers dominate, representing 71.37% of total volume in 2025 and maintaining a 6.01% CAGR outlook.

How are bio-based SAP grades impacting supplier strategies?

Pilot-scale launches such as ZymoChem’s BAYSE and Sumitomo Seika’s recycling initiative signal a shift toward circular and biodegradable options ahead of potential microplastics rules.

What is the primary risk factor dampening near-term SAP growth?

Volatile acrylic acid feedstock prices can compress producer margins, shaving an estimated 1.1 percentage points off projected CAGR.

Page last updated on: