Asia Pacific Smart Home Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

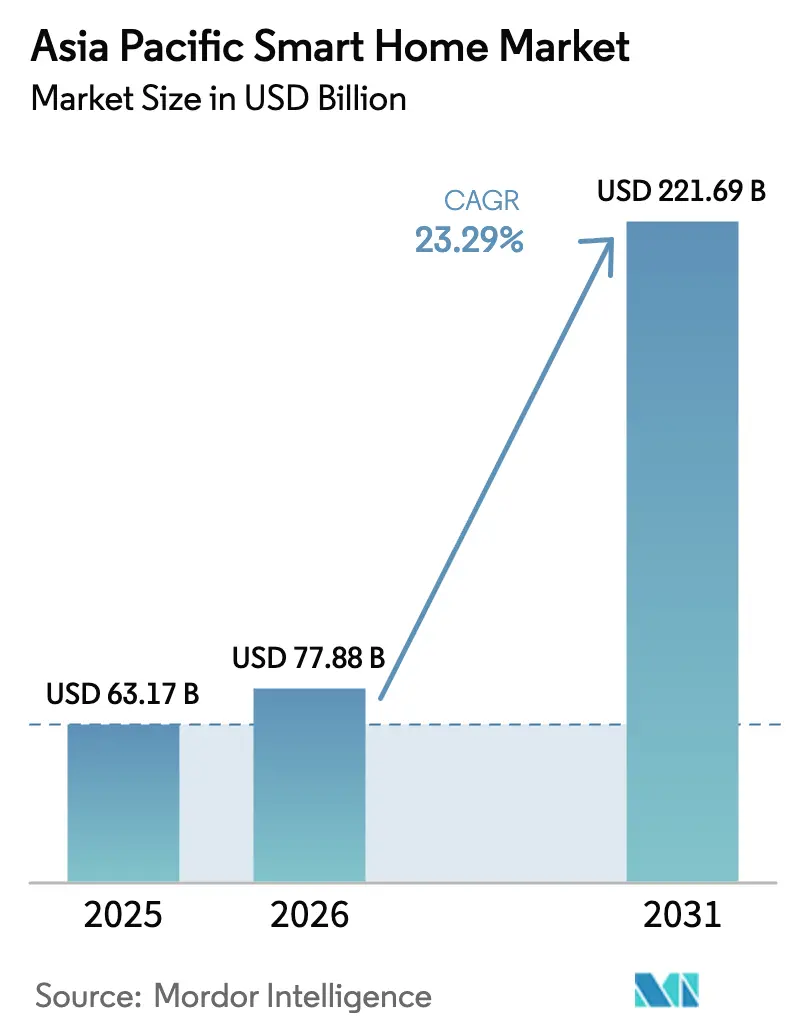

| Base Year Market Size (2025) | USD 63.17 Billion |

| Market Size (2026) | USD 77.88 Billion |

| Market Size (2031) | USD 221.69 Billion |

| Growth Rate (2026 - 2031) | 23.29% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Smart Home Market Analysis by Mordor Intelligence

The Asia-Pacific smart home market size was valued at USD 63.17 billion in 2025 and estimated to grow from USD 77.88 billion in 2026 to reach USD 221.69 billion by 2031, at a CAGR of 23.29% during the forecast period (2026-2031). Rising disposable incomes, widespread fiber-to-home roll-outs, and active government incentives for energy-efficient housing accelerate device penetration. Operators bundle 5G with home-IoT services to lift average revenue per user, while semiconductor suppliers scale Matter-compliant chips that cut integration friction. Aging societies in Japan and South Korea push demand for ambient assisted-living solutions, and post-COVID health concerns lift adoption of indoor-air-quality sensors. Competitive intensity grows as appliance makers, telcos, and platform companies converge on a unified ecosystem strategy anchored in open standards.

Key Report Takeaways

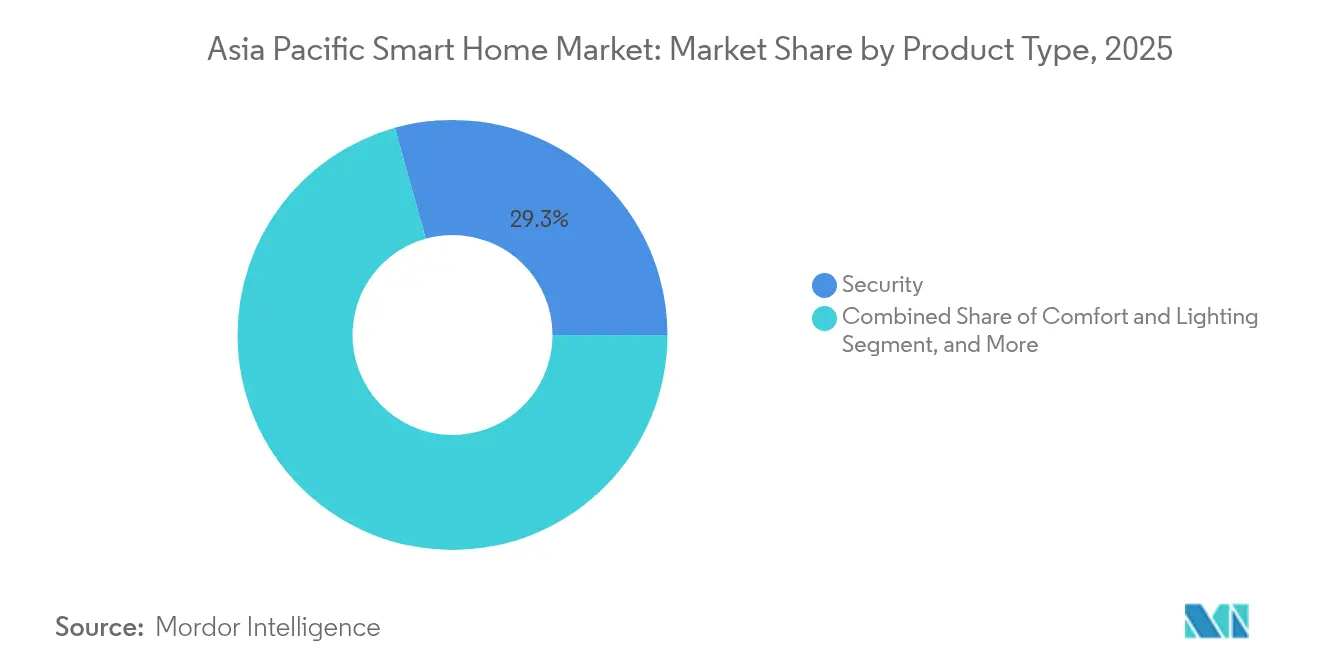

- By product type, security solutions led with 29.32% of Asia-Pacific smart home market share in 2025, whereas smart appliances are projected to expand at a 26.18% CAGR to 2031.

- By technology, Wi-Fi held 54.05% of Asia-Pacific smart home market share in 2025, while Thread is expected to grow at 24.83% CAGR through 2031.

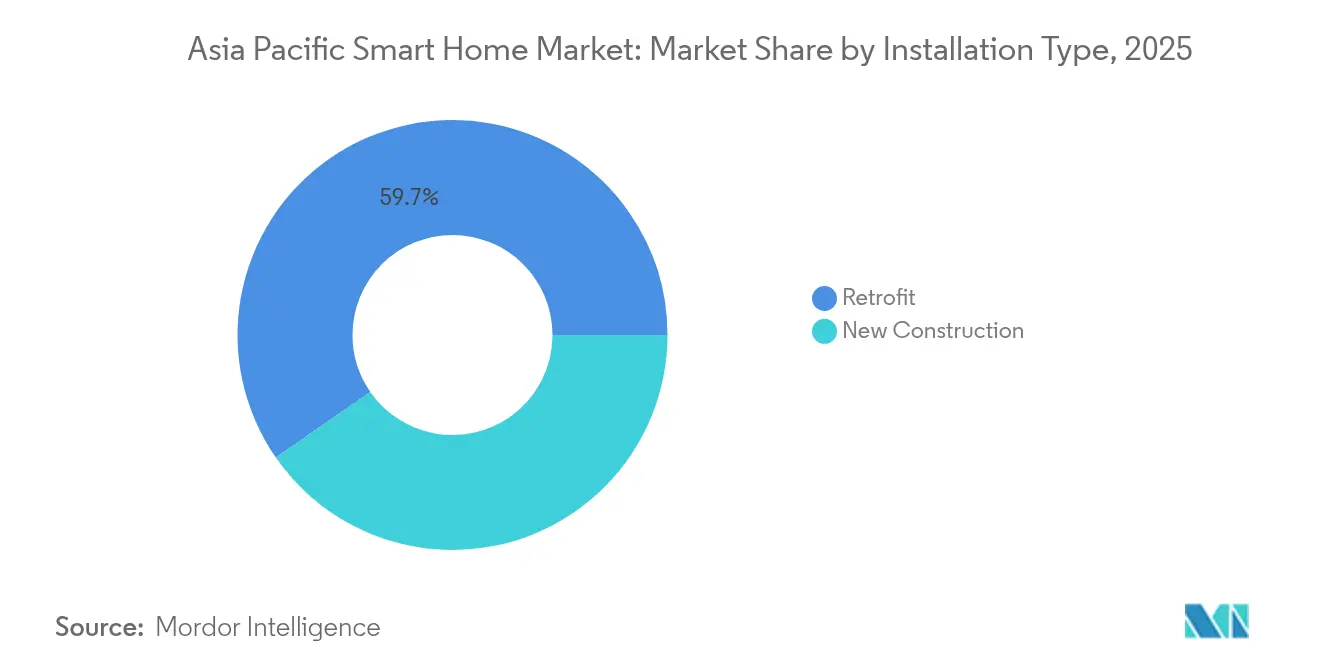

- By installation type, retrofit projects accounted for 59.65% share of the Asia-Pacific smart home market size in 2025; new construction is set to rise at a 23.85% CAGR to 2031.

- By distribution channel, online platforms captured 47.65% revenue share in 2025 and will remain the fastest route to market at a 23.12% CAGR.

- By geography, China commanded 41.10% revenue share in 2025, whereas the rest of Asia-Pacific is poised for quicker expansion at a 23.68% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Smart Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization with integrated smart-residential projects | +4.2% | China, India, Southeast Asia core markets | Medium term (2-4 years) |

| Government-backed Zero-Energy-Home incentives | +2.8% | Japan, South Korea, ASEAN spillover | Long term (≥ 4 years) |

| 5G-bundled home-IoT packages by operators | +3.5% | South Korea, Japan, China urban corridors | Short term (≤ 2 years) |

| Aging-population demand for ambient assisted living | +2.1% | Japan, South Korea, Singapore | Long term (≥ 4 years) |

| E-commerce price competition and local-language voice assistants | +3.9% | China, India, Southeast Asia | Medium term (2-4 years) |

| Post-COVID indoor-air-quality focus | +2.7% | China, India, Indonesia mega-cities | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization and Integrated Smart-Residential Projects in China and India

Large-scale housing developments embed IoT wiring, dedicated conduits, and gateway devices during construction, lowering per-unit deployment costs and assuring interoperability from day one. China Mobile’s HDICT program positions smart home infrastructure as baseline utility, and municipal guidelines aligned with GB/T 39190-2020 enforce common specifications.[1]China Government Portal, “Action Plan for Implementing the National Standardization Development Outline (2024-2025),” gov.cn In India, similar blueprints appear in metropolitan redevelopment schemes, although retrofit costs remain elevated in Tier-2 and Tier-3 cities.

Government-Backed Zero-Energy-Home Incentives in Japan

Japan’s ZEH policy framework grants subsidies and tax breaks for dwellings that cut primary energy use by at least 20%. Builders integrate HVAC, solar, storage, and EMS controllers that rely on continuous sensor feedback. Panasonic’s OASYS central air system reduces heating-cooling energy by more than 50% in airtight homes.[2]Panasonic Corporation, “OASYS Residential Central Air Conditioning System,” news.panasonic.com The incentive structure ensures a multi-year pipeline for smart energy management devices and standardizes demand for interoperable gateways.

5G-Bundled Home-IoT Packages by Asia-Pacific Telecom Operators

Telcos monetize 5G by bundling routers, cameras, voice hubs, and subscription analytics. SK Telecom recorded 19% AI revenue growth in 2024 on the back of such offerings.[3]SK Telecom, “SK Telecom Announces FY 2024 Results,” sktelecom.com Similar propositions from NTT Docomo and China Unicom compress customer-acquisition costs and raise data traffic per household, though gaps in rural coverage postpone mass adoption beyond major cities.

E-Commerce Price Wars Expanding Device Affordability

Aggressive discount campaigns on regional platforms reduce entry-level smart bulb prices below USD 5, broadening addressable segments. Fulfilment data-analytics allow sellers to target emerging Tier-3 conurbations, while local-language voice assistants remove linguistic barriers. Margin pressure intensifies for smaller OEMs, yet volume growth offsets profit dilution for scale players.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented device standards among Chinese OEMs | -2.3% | China, Southeast Asia, export markets | Medium term (2-4 years) |

| Stricter data-privacy regulations | -1.8% | India, Japan, Australia | Short term (≤ 2 years) |

| High retrofit costs outside Tier-1 cities | -2.1% | India, China, Southeast Asia suburbs | Medium term (2-4 years) |

| Semiconductor geo-political supply constraints | -1.9% | Taiwan-centric supply chains | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Device Standards Among Chinese OEMs Hindering Interoperability

Proprietary firmware and cloud stacks create “walled gardens,” complicating multi-brand deployments for integrators. Matter and Thread promise relief, yet current border-router heterogeneity implies that seamless cross-vendor pairing will remain sporadic until at least 2026. Large appliance firms weigh the trade-off between ecosystem control and cross-platform addressable market.

Stricter Data-Privacy Regulations Raising Compliance Costs

India’s Digital Personal Data Protection Act mandates explicit consent, purpose limitation, and breach notification, compelling vendors to retrofit encryption, localize servers, and appoint data fiduciaries. Comparable rules in Australia and Japan increase legal spend and delay product launches, especially for start-ups lacking compliance infrastructure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Security Keeps Top Spot while Appliances Race Ahead

Security solutions generated the largest revenue slice at 29.32% in 2025 as households prioritized cameras, video doorbells, and smart locks for deterrence and insurance compliance. The segment benefits from AI-based anomaly detection and cloud video analytics bundled into subscription models. In contrast, smart appliances post the highest 26.18% CAGR as connected washing machines, refrigerators, and cooktops move from novelty to mainstream. Midea’s AI-enabled platform spanning more than 200 countries underscores how appliance makers leverage firmware updates and cloud telemetry to deepen customer engagement. Energy management, entertainment, and HVAC controls round out the portfolio, each responding to discrete consumer pain points such as rising utility tariffs or air-quality anxiety.

The expansion of appliances catalyzes cross-category sales; for instance, a Matter-capable oven often triggers purchase of compatible sensors and hubs. Health and wellness devices, including sleep trackers and fall-detection mats, climb steadily in aging societies. Smart furniture remains nascent but gains momentum as OEMs embed wireless chargers and environmental sensors into desks and beds. Although share today is modest, falling sensor costs and modular designs position the category for later-cycle upside.

By Technology: Wi-Fi Dominant, Thread Accelerating

Wi-Fi’s 54.05% share reflects ubiquitous home routers and consumer familiarity. Upcoming Wi-Fi 7 trials demonstrate throughputs above 3 Gbps, preparing bandwidth-intensive use cases such as 8K streaming and multi-point AR experiences. Yet Thread records the fastest 24.83% CAGR due to native IPv6, mesh routing efficiency, and backing from the Connectivity Standards Alliance. Certification counts surpassed 670 devices in 2024, and chipset vendors have begun shipping multi-protocol SoCs that lower bill-of-materials.

Bluetooth retains a foothold in battery-powered tags and wearables, while Zigbee faces displacement in favor of Thread. Z-Wave persists in professional security installs demanding longer range and sub-GHz robustness. Where coverage gaps emerge, NB-IoT or PLC provide fallback connectivity, particularly in concrete high-rise blocks. The pluralistic protocol landscape will persist until routers ship with tri-band radios and universal controllers abstract underlying transport layers.

By Installation Type: Retrofit Leads, New Construction Gains Momentum

Retrofit projects contributed 59.65% revenue in 2025, anchoring the early adoption curve. Mature urban households replace legacy alarms with cloud-connected systems and add sensors room by room. However, installation complexity—rewiring, conduit drilling, and gateway placement—adds cost and prolongs payback in mass-market housing. Developers now embed smart conduits, PoE switches, and multi-sensor clusters in new builds, driving a faster 23.85% CAGR. Integrated design lowers material spend per dwelling and assures code compliance with upcoming energy and safety regulations.

Professional installers capture a growing services slice, handling advanced lighting scenes, HVAC zoning, and unified dashboards. For simpler devices, modular plug-and-play kits sustain a buoyant DIY segment. Over the forecast horizon, retrofit share will gradually erode as greenfield housing dominates incremental stock, especially in China’s satellite cities and India’s urban corridors.

By Distribution Channel: Online Platforms Democratize Access

Digital marketplaces owned nearly half of shipments in 2025 as real-time ratings, flash sales, and influencer videos shrank decision cycles. Cross-border e-commerce enables niche brands to reach Southeast Asian consumers who previously lacked retail representation. The channel benefits from algorithmic recommendations that bundle complementary devices, lifting cart values. Conversely, offline retail thrives in premium tiers where shoppers want tactile demos and turnkey installation quotes.

Professional distributors partner with builders to pre-install hubs and sensors, receiving recurring maintenance income. Hybrid click-and-collect models emerge, blending online price transparency with neighborhood service centers for last-mile support. Logistics investment in cold-chain and same-day delivery shortens lead times, further eroding barriers to trial. Fraud and counterfeit risks persist, spurring platforms to deploy QR-based authenticity programs co-developed with brand owners.

Geography Analysis

China accounted for 41.10% of 2025 revenue, underpinned by national standard GB/T 39190-2020 and industrial policy that classifies smart home infrastructure as a pillar of the digital economy. Telecom operators such as China Mobile aim for a cumulative smart living market worth CNY 3 trillion by 2025, embedding hubs in fiber modems to normalize adoption. Nevertheless, growth momentum shifts toward emerging economies where new broadband connections scale rapidly. India, Indonesia, Vietnam, and the Philippines collectively post CAGRs north of 25% as 5G launches, local-language voice assistants, and declining device prices converge.

Japan forms a mature cluster with South Korea and Singapore, characterized by high per-capita gadget density and policy-driven energy efficiency mandates. ZEH incentives, stringent appliance labelling, and demographic imperatives for elderly care sustain premium demand. Prefabricated housing brands integrate earthquake-resilient frames with AI-controlled ventilation, achieving net-zero energy status in over 80% of new detached units. South Korea’s municipal governments co-fund AI-enabled public health monitoring in senior apartments, reinforcing the ambient assisted-living narrative.

Australia and New Zealand emphasize sustainability. Net-zero building codes and rebates for rooftop solar in conjunction with smart inverters stimulate uptake of energy dashboards and automated load-shifting plugs. Regional installers leverage ABB-Samsung collaborations to unify photovoltaic, storage, and HVAC data streams. Although absolute population is modest, high ASPs translate into outsized revenue contribution.

Competitive Landscape

The vendor arena is moderately fragmented. In aggregate, the five largest suppliers control roughly 48% of shipments, leaving room for niche innovators. Chinese brands such as Xiaomi and Haier leverage vertical integration-from chipset to cloud-to price aggressively and iterate hardware every six months. Samsung applies semiconductor scale to integrate Thread, Zigbee, BLE, and Wi-Fi radios on single dies, reducing power draw and board area. Schneider Electric and ABB target the premium electrical segment, favoring open APIs and IEC-compliant controllers for builders.

Strategic direction pivots from single-device sales to platform stickiness. Panasonic Go aspires for 30% of corporate revenue from AI services by 2035, pairing wellness data with HVAC tuning. Telcos bundle monitoring subscriptions with broadband to cut churn, while SoC vendors race to certify Matter over Thread, Zigbee, and Wi-Fi HaLow. Supply-chain resilience becomes critical as geo-political tension concentrates advanced packaging in Taiwan. Firms diversify fabs across Japan, Singapore, and India to hedge risk.

Platform alliances proliferate. ABB integrates its InSite EMS with Samsung SmartThings to marry electrical switchgear telemetry with consumer dashboards. Thread Group membership surpassed 200 organizations, signaling consensus around IP-based mesh as the neutral backbone. Start-ups exploit Wi-Fi HaLow to deliver kilometer-scale coverage for perimeter sensors, reducing gateway count and installation cost. Competitive advantage now lies in user-experience orchestration, cloud analytics, and regulatory compliance rather than proprietary radios.

Asia Pacific Smart Home Industry Leaders

Schneider Electric SE

Emerson Electric Co.

ABB Ltd.

Honeywell International Inc.

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Morse Micro’s MM6108-EKH05-Light platform secured Matter certification, extending Wi-Fi HaLow range tenfold for residential and industrial IoT.

- May 2025: Mitsubishi Estate and JG Corporation formed a strategic partnership to enhance the HOMETACT smart-home platform for multi-dwelling projects.

- April 2025: Sekisui Chemical launched two Tokyo projects with ZEH-M Oriented standards and community IoT apps.

- March 2025: Panasonic introduced 61 Matter-ready residential AC models in India, rated for ambient temperatures up to 55 °C.

- March 2025: AWE2025 in Shanghai hosted over 1,000 brands showcasing AI-driven living solutions

Asia Pacific Smart Home Market Report Scope

A smart home refers to integrated and networked devices that automate different functions within a home and can communicate with each other, as well as a centralized control interface. The prominent purpose of this type of system is to enhance comfort, safety, energy efficiency, and management of household resources.

The Asia-Pacific smart home market is segmented by product type (comfort and lighting, control and connectivity, energy management, home entertainment, security, smart appliances, and HVAC control), technology (Wi-Fi, Bluetooth, and other technologies), and country (China, Japan, India, South Korea, and Rest of Asia-Pacific). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Comfort and Lighting |

| Control and Connectivity |

| Energy Management |

| Home Entertainment |

| Security |

| Smart Appliances |

| HVAC Control |

| Smart Furniture |

| Smart Health and Wellness Devices |

| Wi-Fi |

| Bluetooth |

| Zigbee |

| Z-Wave |

| Thread |

| Others (NB-IoT, RF, PLC) |

| New Construction |

| Retrofit |

| Offline (DIY and Professional) |

| Online |

| China |

| Japan |

| India |

| South Korea |

| South East Asia |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Product Type | Comfort and Lighting |

| Control and Connectivity | |

| Energy Management | |

| Home Entertainment | |

| Security | |

| Smart Appliances | |

| HVAC Control | |

| Smart Furniture | |

| Smart Health and Wellness Devices | |

| By Technology | Wi-Fi |

| Bluetooth | |

| Zigbee | |

| Z-Wave | |

| Thread | |

| Others (NB-IoT, RF, PLC) | |

| By Installation Type | New Construction |

| Retrofit | |

| By Distribution Channel | Offline (DIY and Professional) |

| Online | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| South East Asia | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size of the Asia-Pacific smart home market?

The market stands at USD 77.88 billion in 2026 and is projected to reach USD 221.69 billion by 2031, growing at a 23.29% CAGR

Which product category leads the Asia-Pacific smart home market?

Security solutions hold the top position with 29.32% revenue share in 2025, driven by rising demand for cameras and smart locks.

Why is Thread technology gaining momentum?

Thread offers low-power IPv6 mesh networking and direct alignment with the Matter protocol, yielding the fastest forecast growth at 24.83% CAGR.

How do Zero-Energy-Home incentives influence market demand?

Japan’s ZEH program mandates energy savings that require smart HVAC and energy-management systems, underpinning sustained device adoption

Which sales channel grows fastest for smart home devices?

Online platforms account for 47.65% of 2025 revenue and will continue expanding at a 23.12% CAGR due to price transparency and wide product variety.

What challenges limit penetration outside major cities?

High retrofit costs, fragmented device standards, and limited 5G coverage in rural areas restrain adoption across Tier-2 and Tier-3 regions.

Page last updated on: