Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 0.25 Billion |

| Market Size (2026) | USD 0.28 Billion |

| Market Size (2031) | USD 0.34 Billion |

| Growth Rate (2026 - 2031) | 3.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Singapore Ready-to-Eat Food Market Analysis by Mordor Intelligence

Singapore ready-to-eat food market size is valued at USD 0.28 billion in 2026, growing from the 2025 value of USD 0.25 billion, and is forecast to climb to USD 0.34 billion by 2031, advancing at a 3.12% CAGR. Demand momentum rests on time-pressed urban households that are willing to pay for convenience even while the nation’s vibrant hawker culture continues to command habitual meal occasions. Dual-income families, growing e-commerce penetration, functional product upgrades, and packaging technologies that lengthen shelf life collectively sustain incremental volume gains. Private-label expansion by leading grocery chains is squeezing branded profit pools, prompting incumbents to use health claims, ethnic flavors, and alternative proteins to justify price premiums. Meanwhile, Singapore’s clear regulatory pathway for novel foods positions it as a regional launchpad for cultivated meat and precision-fermentation ingredients, further diversifying the offer set within the Singapore ready-to-eat food market.

Key Report Takeaways

- By product type, Ready Meals led with 38.28% of the Singapore ready-to-eat food market share in 2025, and Instant Soups and Snacks are projected to expand at a 4.28% CAGR through 2031.

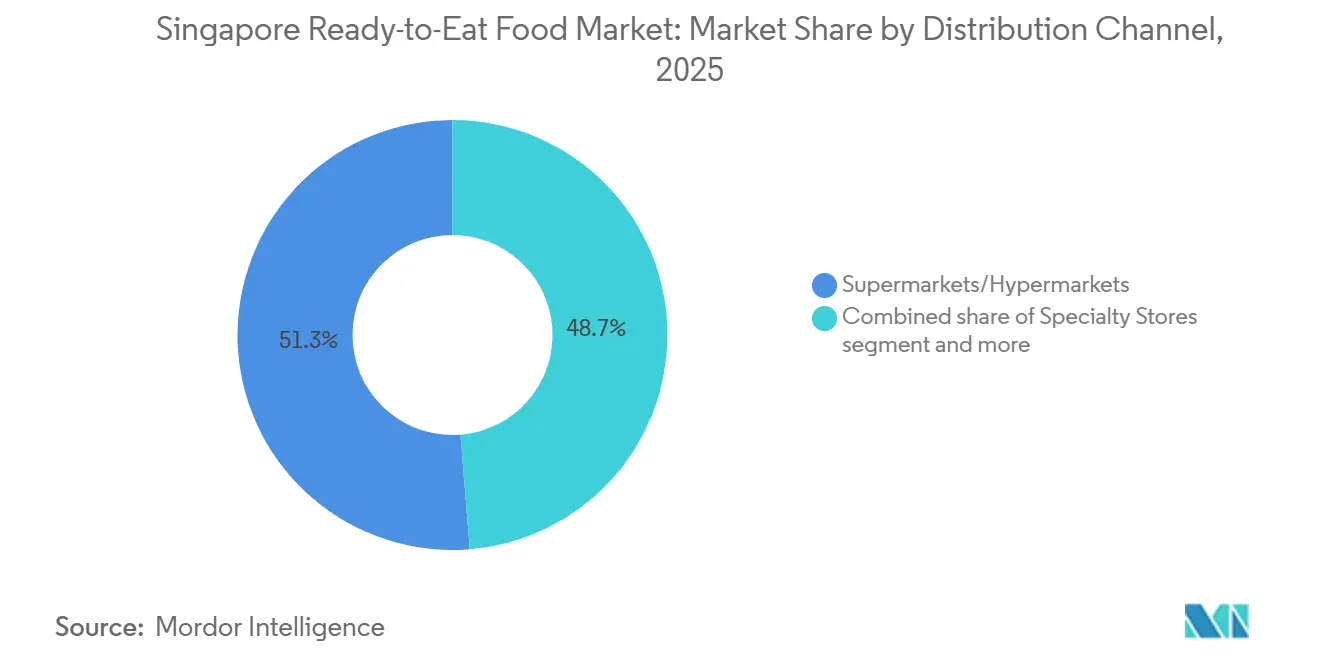

- By distribution channel, Supermarkets and Hypermarkets accounted for 51.27% share of the Singapore ready-to-eat food market size in 2025, and Online Retail is forecast to record a 5.26% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Ready-to-Eat Food Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Western Convenience Foods | +0.6% | National, with higher penetration in expatriate-dense districts (Orchard, Marina Bay) | Medium term (2-4 years) |

| Dual-income Households Seeking Time-Efficient Meals | +0.8% | National, concentrated in HDB estates and private condominiums | Long term (≥ 4 years) |

| Expansion of E-Commerce and Food Delivery Platforms | +0.7% | National, with early gains in central and eastern Singapore | Short term (≤ 2 years) |

| Health Consciousness Drives Demand for Organic, Low-Sugar, and Plant-Based RTE Products | +0.5% | National, skewed toward higher-income segments and younger demographics | Medium term (2-4 years) |

| Cultural Diversity Spurs Varied Cuisine RTE Options | +0.4% | National, reflecting Malay, Indian, Chinese, and fusion preferences | Long term (≥ 4 years) |

| Technological Advances in Packaging Extend Shelf Life | +0.3% | National, with spillover benefits to regional export markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Dual-Income Households Seeking Time-Efficient Meals

In Singapore, high labor-force participation rates and long working hours have resulted in a structural time deficit. RTE (Ready-to-Eat) suppliers are addressing this demand by offering portion-controlled, microwaveable options. Approximately 28% of Singaporean consumers report insufficient time to cook, exceeding the global average by 8 percentage points. Additionally, 49% of Singaporeans consume takeaway or ready-made meals at least once a week. Household expenditure surveys show a significant increase in spending on food-serving services, rising from SGD 404.1 (USD 299) in 1993 to SGD 965.7 (USD 715) in 2023. This 2.9% annual growth rate surpasses headline inflation, indicating a lasting shift toward convenience. Consumers in this demographic prioritize speed and minimal cleanup, often choosing RTE meals that replicate popular hawker dishes, such as chicken rice, laksa, and nasi lemak packaged in single-serve trays. The Progressive Wage Model, which raised median monthly incomes for food-services workers to SGD 5,500 (USD 4,070) in 2024, has further constrained household time budgets, according to the Ministry of Manpower[1]Source: Ministry of Manpower, “Progressive Wage Model for Food Services,” Mom.gov.sg. With higher wages enabling greater spending on convenience, the motivation to cook from scratch has declined.

Expansion of E-Commerce and Food Delivery Platforms

In 2023, online food and beverage sales reached USD 2.31 billion, contributing approximately 25% to 27% of the total food and beverages revenue. Online grocery channels generated USD 1.4 billion in 2024 and are projected to grow to USD 2.3 billion by 2033. Around 68% of Singaporeans use food-delivery services daily, spending an average of SGD 108 (USD 80) per month. The platform has maintained high order volumes by partnering with ComfortDelGro taxis for last-mile delivery, enabling fulfillment within 2 hours in densely populated residential areas. Foodpanda's Pandamart dark stores, which stock over 40,000 SKUs, offer an average delivery time of 25 minutes. This effectively positions RTE products as on-demand meal solutions that compete on speed rather than price. These infrastructure advancements allow brands to bypass traditional retail negotiations and test limited-edition flavors or functional variants with minimal inventory risk. This has reduced product-development cycles from 18 months to under 6 months for digital-first launches.

Health Consciousness Drives Demand for Organic, Low-Sugar, and Plant-Based RTE Products

In 2023, Singapore's investment in alternative proteins climbed to USD 170 million, representing a significant rise from the USD 85 million invested in 2021. This increase is driven by both government-supported initiatives and private capital seeking regulatory clarity on novel ingredients. By mid-2024, the Singapore Food Agency had approved 16 cell-based and precision-fermentation products, establishing the city as a global hub for testing next-generation ready-to-eat (RTE) formulations. For instance, GOOD Meat's cultivated chicken will be available at SGD 7.20 (USD 5.33) for 120 grams at Huber's Butchery starting May 2024, as reported by GOOD Meat and the SFA[2]Source: Singapore Food Agency, “Novel Food Approvals and Regulations,” sfa.gov.sg. Nestlé's partnership with KosmodeHealth to create high-protein, high-fiber noodles from upcycled barley grains, an initiative recognized as the "Most Transformational Collaboration" at the 2023 Singapore International Chamber of Commerce event, demonstrates the industry's shift toward circular-economy principles in mainstream RTE products. Moreover, the Health Promotion Board's Healthier Dining Programme, which mandates reduced sodium and sugar levels in participating outlets, is influencing retail RTE categories. Manufacturers are proactively reformulating their products to meet these evolving standards, reducing potential reputational risks from future regulatory actions.

Technological Advances in Packaging Extend Shelf Life

The Soup Spoon's high-pressure processing (HPP) technology has extended the shelf life of refrigerated soups from 14 days to 120 days and ready meals from 3 days to 28 days. This advancement enables nationwide distribution without the costs of a frozen supply chain and reduces retailer markdown losses by up to 40%. Active packaging, which includes oxygen scavengers and antimicrobial films, is becoming a standard feature in premium ready-to-eat (RTE) lines. Additionally, smart packaging with QR-code freshness indicators and time-temperature tags allows consumers to verify cold-chain integrity before purchasing, addressing trust concerns related to chilled convenience foods. In April 2024, the Nurasa Food Tech Centre, a 3,840-square-meter facility backed by Temasek, opened at Biopolis. This center provides co-manufacturing infrastructure for startups developing innovative barrier films and modified-atmosphere packaging, which can triple ambient shelf life without using synthetic preservatives. Singapore's position as a regional logistics hub enhances the strategic importance of these innovations. For example, extending shelf life by 30 days transforms Singapore into a viable export platform for RTE products destined for Malaysia, Indonesia, and other emerging ASEAN markets, turning a domestic technological advantage into a cross-border competitive edge.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Health Concerns Over Preservatives, Additives, and High Sodium in Processed RTE Foods | -0.5% | National, with heightened scrutiny among health-conscious millennials and Gen Z | Long term (≥ 4 years) |

| Strict Singapore Food Agency Regulations | -0.4% | National, affecting all RTE manufacturers and importers | Medium term (2-4 years) |

| Strong Hawker Culture and Preference for Fresh-Cooked Meals | -0.6% | National, particularly in mature estates with established hawker centers | Long term (≥ 4 years) |

| High Operational Costs from Premium Ingredients and Advanced Packaging | -0.3% | National, with spillover effects on export pricing competitiveness | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strong Hawker Culture and Preference for Fresh-Cooked Meals

Singapore's 114 hawker centers, managed by the National Environment Agency and comprising over 14,000 stalls, are central to the city's dining culture. Approximately 70% of residents visit these venues four or more times a week, reducing their dependence on packaged ready-to-eat (RTE) alternatives. Hawker meals, priced between SGD 3 and SGD 5 (USD 2.22 to USD 3.70) per serving, are more affordable than most chilled RTE products and are perceived as fresher. Additionally, the communal dining experience and direct vendor interactions add a social element, creating barriers to switching that extend beyond cost considerations. Government support, including subsidies for hawker-center construction and stall rentals, aligns with efforts to preserve Singapore's culinary heritage. These measures ensure fresh-cooked meals remain both accessible and affordable, effectively limiting the premium consumers are willing to pay for convenience. In response, RTE suppliers replicate hawker flavors and collaborate with celebrity hawkers to co-brand frozen versions of popular dishes. However, these products primarily target a niche audience, including consumers who are traveling, working late, or living in newer estates with fewer hawker options. The resilience of the hawker model suggests that RTE growth in Singapore will remain gradual, complementing rather than replacing existing options. Export markets with less developed fresh-food infrastructures may offer greater potential for higher returns on marketing investments.

Strict Singapore Food Agency Regulations

The Singapore Food Agency (SFA) implemented Novel Food Regulations requiring pre-market safety assessments for ingredients without a history of human consumption. This regulation has caused delays of 6 to 12 months for plant-based and cell-cultured ready-to-eat (RTE) product launches in Singapore compared to jurisdictions with less stringent rules. Moreover, the SS 672:2021 standard for RTE meal delivery in Singapore enforces compliance costs between SGD 15,000 and SGD 30,000 (approximately USD 11,100 to USD 22,200) per stock-keeping unit (SKU). These costs stem from requirements for temperature logging, traceability protocols, and microbial testing. Such financial demands discourage small-batch experimentation, giving an edge to larger players with dedicated quality-assurance teams. Additionally, strict labeling requirements, including allergens, nutritional content, and country-of-origin, reduce available packaging space. This limitation forces brands to choose between highlighting marketing claims or meeting regulatory disclosures. While these standards enhance public health and reinforce Singapore's reputation as a safe-food hub, they also create a two-tier market. Multinational corporations, capable of spreading compliance costs across regional portfolios, gain an advantage over local startups. These startups often rely on partnerships with contract manufacturers or face prolonged time-to-market challenges. By mid-2024, the SFA had approved 16 novel-food applications, indicating progress in the regulatory framework. However, the agency's non-transparent, case-by-case review process leaves applicants uncertain about approval timelines, complicating investor due diligence and product-launch planning.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Functional Claims Reshape Portfolio Mix

In 2025, Ready Meals accounted for 38.28% of the market, driven by dual-income households seeking convenience and portion control over traditional cooking. Instant Soups and Snacks, growing at a 4.28% CAGR through 2031, lead product category growth with functional benefits like high protein and plant-based broths. Instant Breakfast and Cereals gained traction with fortified oat blends and protein granolas, such as General Mills' 2024 launches targeting busy consumers. Baked Goods and Meat Products cater to niche occasions with shelf-stable croissants and vacuum-sealed sausages as bakery substitutes. Plant-Based Ready Meals, though emerging, are expanding, with Impossible Foods' products available in major retail outlets since 2020 and 2021.

Functional and Protein Snacks are reshaping indulgence by adding health benefits, such as Heal Nutrition's Protein Puffs, offering 20 grams of protein per pack in unique flavors. Other Product Types, including sauces, condiments, and meal kits, create cross-selling opportunities, like Prima Taste's sauce range and Hai's Chicken Rice Sauce Kit, enabling quick hawker-style meals. These products blur the line between ready-to-eat and home-cooked meals. The Singapore Food Agency's approval of Solar Foods' Solein protein powder and its 2024 incorporation into Fazer snack bars highlight regulatory acceptance of innovative ingredients. This development signals potential shifts in product boundaries during the forecast period.

By Distribution Channels: Private Label Pressures Branded Margins

In 2025, Supermarkets and Hypermarkets accounted for 51.27% of the distribution share, effectively utilizing promotional pricing, strategic end-cap placements, and private-label products to attract cost-conscious shoppers. In 2024, NTUC FairPrice's Own Brands portfolio generated over SGD 1 billion (USD 740 million) in revenue, contributing approximately 20% to the group's total sales. These products appeared in 70% of online grocery baskets, a penetration rate that pressures branded suppliers to innovate and justify premium pricing or risk being delisted. Convenience and Grocery Stores focus on quick top-up purchases and impulse buys. For example, 7-Eleven Singapore offers more than 300 ready-to-eat (RTE) SKUs, including plant-based burgers and ethnic meal trays, catering to late-night workers and transit hubs. Specialty Stores target affluent customers seeking organic, imported, or artisanal RTE options. A notable example is Huber's Butchery, which introduced GOOD Meat's cultivated chicken in May 2024 at SGD 7.20 (USD 5.33) per 120 grams, demonstrating how niche retailers test premium pricing before broader market adoption.

Online Retail channels are experiencing the fastest growth among distribution formats, with a 5.26% CAGR projected through 2031. This growth is driven by dark-store networks and 25-minute delivery windows, which minimize the gap between impulse purchases and order fulfillment. foodpanda's pandamart stocks over 40,000 items and ensures a 25-minute delivery time. Similarly, RedMart's collaboration with ComfortDelGro taxis enables same-day delivery slots for suburban areas that previously relied on weekly supermarket trips. Other Distribution Channels, such as vending machines, workplace canteens, and petrol-station marts, capitalize on micro-occasions where convenience outweighs price considerations. However, their combined market share remains small compared to the dominance of big-box retailers and e-commerce platforms. The shift to online ordering allows RTE brands to bypass slotting fees and achieve better margins through direct-to-consumer sales. At the same time, this transition exposes brands to algorithm-driven visibility challenges, where factors like search ranking and sponsored placements significantly impact sales performance alongside product quality.

Geography Analysis

Singapore, with its compact 734-square-kilometer footprint and a population of 5.9 million, serves as a hyper-urban laboratory where patterns of Ready-to-Eat (RTE) adoption emerge more swiftly than in the region's sprawling markets. However, this density also intensifies competition from hawker centers and restaurant deliveries. As a regional headquarters for multinational food giants like Nestlé, Unilever, and PepsiCo, Singapore often becomes a testing ground for product innovations. These innovations, once piloted locally, typically scale across Southeast Asia within a mere 12 to 18 months. This dynamic positions Singapore as a disproportionately influential test market, especially given its relatively modest revenue base. Highlighting this influence, Nestlé, in March 2025, announced an expansion of its research and development center in Singapore, with backing from the Economic Development Board. The focus is on alternative-protein formulations and sugar-reduction technologies, set to be deployed in neighboring countries like Malaysia, Indonesia, Thailand, and the Philippines.

Singapore's government, with its "30 by 30" initiative, aims to locally produce 30% of the nation's nutritional needs by 2030. This ambition is driving investments into vertical farms, aquaculture, and precision fermentation facilities. These facilities not only supply fresh inputs to RTE manufacturers but also aim to reduce the nation's dependency on imports and shorten the farm-to-fork cycle. In April 2024, the Nurasa Food Tech Centre, a 3,840-square-meter facility backed by Temasek and located at Biopolis, commenced operations. This center offers co-manufacturing infrastructure for startups experimenting with novel ingredients and packaging formats. By doing so, it effectively subsidizes early-stage research and development, which might have otherwise relocated to more cost-effective jurisdictions. Singapore's strategic position is further bolstered by its free-trade agreements and the cargo throughput of Changi Airport, which handled 7.4 million tonnes in 2019. This makes Singapore a prime re-export platform for RTE products aimed at ASEAN markets. Notably, advanced packaging techniques that extend shelf life by 30 days can facilitate distribution to tier-2 and tier-3 cities in these markets, which often lack cold-chain infrastructure, as highlighted by the CAAS[3]Source: Civil Aviation Authority of Singapore (CAAS) "Changi Airport Cargo Throughput Statistics." caas.gov.sg.

Cross-border e-commerce platforms are capitalizing on the "Made in Singapore" label, listing Singapore-manufactured RTE products in neighboring markets. This label acts as a quality signal, allowing these products to command a 10% to 15% price premium over locally produced alternatives in both Indonesia and Malaysia. In a testament to Singapore's growing influence in the RTE sector, Temasek Holdings made headlines with its March 2025 acquisition of a 10% stake in India's Haldiram's, valuing the company at USD 10 billion. Additionally, the firm's November 2024 regulatory nod to invest in Rebel Foods further underscores the appetite of Singaporean capital for scaling RTE platforms across South and Southeast Asia, with Singapore emerging as both a financial nucleus and an operational blueprint.

Regulatory Landscape

Singapore ready-to-eat (RTE) foods are regulated by the Singapore Food Agency (SFA) under the Food Regulations, with microbiological requirements for RTE foods set out in the Eleventh Schedule (for example, E. coli limits specified for relevant categories). Importers of processed foods, including certain RTE items, must register with SFA, and selected categories can require additional certification and producer registration depending on origin and risk profile.

A major change in the compliance environment is the Food Safety and Security Act 2025 (FSSA), assented to in February 2025. The FSSA replaces the Sale of Food Act 1973 and expands oversight from food sales to the wider food supply chain, including donation and free distribution. Separately, the Food (Amendment) Regulations 2025 came into operation on 30 January 2026, updating prepacked-food labelling requirements to align more closely with Codex Alimentarius guidance (including clearer parameters for gluten-free claims). This raises the bar for claims governance while easing technical alignment for multinational portfolios formulated for multiple markets.

Competitive Landscape

Singapore's ready-to-eat food market demonstrates moderate fragmentation, characterized by competition between established multinational companies like PepsiCo Inc., Nestlé S.A., Kellanova, and General Mills Inc. The fragmented market structure allows niche players to target specific consumer segments while creating opportunities for strategic consolidation. This dynamic is exemplified by the July 2024 partnership between SATS and Mitsui, which combines SATS' culinary expertise and production capabilities with Mitsui's global procurement and distribution network.

In Singapore, market leaders are capitalizing on the country's favorable regulatory environment and robust infrastructure to pilot products before rolling them out regionally. These companies benefit from Singapore's strategic position as a hub for innovation and testing, leveraging its well-established logistics network and supportive policies to refine their offerings before scaling operations across Southeast Asia. Meanwhile, smaller players are carving out a niche in premium segments, setting themselves apart through health-centric positioning, sustainability claims, and a nod to cultural authenticity, all in pursuit of fatter margins. Their focus on premiumization allows them to cater to a discerning consumer base willing to pay a premium for quality and value. Notably, the market is ripe with opportunities, especially in plant-based ready meals and functional foods, resonating with Singapore's wellness-centric trends and growing demand for healthier, convenient options.

Newer entrants are shunning traditional retail routes, opting instead for direct-to-consumer models. By harnessing the power of e-commerce platforms, these companies are tapping into the fastest-growing distribution channel in the ready-to-eat food sector. This approach enables them to connect with consumers swiftly, bypassing intermediaries and reducing costs. Additionally, it allows these businesses to gather real-time consumer insights, adapt to evolving tastes, and offer personalized experiences, further strengthening their market presence.

Singapore Ready-to-Eat Food Industry Leaders

-

Nestlé S.A.

-

General Mills Inc.

-

PepsiCo Inc.

-

Kellanova

-

Prima Limited

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Digitization and productivity programs provide RTE manufacturers and co-manufacturers with an operational pathway to shorten development cycles and tighten cold-chain compliance. In February 2026, Enterprise Singapore and IMDA launched a refreshed Food Manufacturing Industry Digital Plan to guide over 1,500 food manufacturers in adopting technology, including traceability, quality control, and production planning, which influence RTE economics and SKU agility across chilled and ambient formats.

Innovation funding and food-safety R&D also create openings for higher-value RTE propositions that combine nutrition, shelf-life extension, and new ingredients with regulatory-ready documentation. In 2025, SFA committed SGD 42 million under the Singapore Food Story (SFS) R&D Programme to 11 Future Foods and Food Safety projects, with A*STAR-linked support such as the MTC IAF-PP Food Manufacturing Grant (FMG) focused on productisation, side-stream valorisation, and sustainable packaging. Together with the existing SFA safety framework for RTE microbiological standards, these initiatives support a compliance-centric development process for reformulated and novel-ingredient RTE variants, scaling through central kitchens and co-manufacturing infrastructure.

Recent Industry Developments

- July 2026: Nestle Professional Singapore launched the KITKAT Chocolate Drink for foodservice operators, expanding distribution across cafe and dining networks such as Burger King, Nan Yang Dao, Kopitiam, and Koufu. The release targets foodservice-linked, ready-to-use beverage solutions that can be deployed with minimal back-of-house prep, reinforcing standardized convenience formats alongside retail RTE.

- March 2026: Nestle upgraded its research and development facilities in Singapore and introduced a regional R&D Accelerator aimed at helping startups and local SMEs develop and upscale new products in under six months. This expands Singapore-based formulation and scale-up capacity for convenience foods, supporting faster iteration on claims, packaging, and ingredient innovation that can feed into RTE pipelines.

- July 2024: SATS and Mitsui announced a partnership combining SATS' culinary and production capabilities with Mitsui's global procurement and distribution network. The tie-up improves access to ingredients and cross-border routes for packaged meal solutions, supporting scale economics and broader channel reach for RTE and adjacent convenience-food formats.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers packaged ready-to-eat foods sold in Singapore that are consumed directly or after brief reheating. This includes frozen, chilled, and shelf-stable formats, and it focuses on at-home purchases through retail and e-grocery.

Scope exclusions: Fresh deli counter items, catering trays, pet meals, and food-delivery platform sales are excluded from this market sizing.

Segmentation Overview

-

By Product Type

- Ready Meals

- Instant Soups and Snacks

- Instant Breakfast/Cereals

- Baked Goods

- Meat Products

- Plant-Based Ready Meals

- Functional/Protein Snacks

- Other Product Types

-

By Distribution Channels

-

Supermarkets/Hypermarkets

- Convenience/Grocery Stores

- Specialty Stores

- Online Retail Stores

- Other Distribution Channels

-

Supermarkets/Hypermarkets

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts by setting the market boundaries and collecting the series that best explain Singapore demand for packaged ready-to-eat items. We reviewed public statistics and rulebooks from sources such as Singapore Department of Statistics, Singapore Food Agency, UN Comtrade trade tables, and health or diet references from the World Health Organization to understand consumption context and import reliance.

To keep the model aligned with what shoppers can access, we also used retailer and brand websites for pack sizes and formats, company filings and investor presentations for category commentary, and credible press for pricing and distribution shifts. Where needed, a paid subscription for company financials and news, along with an import-export shipment-level database and a patent database, were used to validate supplier activity signals and innovation pipelines. The sources listed here are illustrative only, and many other public references were also checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary conversations were used to pressure-test the desk assumptions on which SKUs are treated as ready-to-eat, what pricing tiers look like by storage type, and how online retail and convenience channels are changing the mix. Interviews covered packaged food manufacturers, importers and distributors, retail category teams, and packaging or cold-chain participants. Inputs filled gaps in the SKU basket and helped align the final totals with on-the-ground market behavior in Singapore.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 13% | |

| Mid tier: 46% | Functional/Unit leaders: 37% | |

| Smaller Players: 22% | Managers: 50% |

Market-Sizing & Forecasting

Sizing is built using a top-down approach where national consumption indicators, packaged food spend patterns, and import flow signals are reconstructed into a demand pool for ready-to-eat products in Singapore. Once that pool is established, it is narrowed using market-specific filters such as the split between frozen, chilled, and ambient packs, the share of meals versus snack-style items, and the portion of sales happening through supermarkets, convenience stores, specialty outlets, and online retail.

To make sure the total is realistic, we corroborate it with selective bottom-up checks based on sampled brand and retailer assortments, observed pack size ranges, and price-per-pack logic. These are then matched to reasonable turnover rates by channel. When a category does not publish clean volume data, gaps are handled using proxy series such as import value by relevant HS codes, packaging format prevalence, and shelf-stable versus cold-chain distribution intensity. For forecasting, scenario analysis is applied around a base case, and the forward view is anchored on variables discussed with industry respondents, including price inflation pass-through, household time-scarcity trends that support convenience foods, and the pace of new product launches in ready meals and instant snacks.

Data Validation & Update Cycle

Outputs are cross-checked against independent signals, such as trade movements for key prepared-food lines, retail price changes seen across major channels, and shifts in cold-storage or ambient shelf allocations, so the model does not drift away from what is observable. Variance checks are done at multiple levels, and if a segment looks unusually large or small, assumptions are revisited and, when needed, respondents are re-contacted for clarification.

Before sign-off, the numbers go through a step-by-step analyst review so calculation errors, unit mismatches, and currency timing issues are caught early. The report is refreshed annually, and interim updates are triggered when there is a material event such as a sharp input-cost swing or a meaningful policy change affecting packaged foods. Right before delivery, a final data pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Singapore Ready to Eat Food Market Size Versus Other Published Estimates

Different published market sizes can vary because the definition of ready-to-eat is not always applied in the same way, and channel coverage and base-year pricing can also be treated differently. Some studies lean heavily on broad packaged food totals, while others start from narrower shopper behavior signals, which can create a noticeable spread even for the same country.

Food-delivery platform sales sit outside Mordor Intelligence's scope, and that single exclusion can widen the gap versus estimates that bundle delivered prepared meals with retail-ready packaged products. Differences also come from whether fresh deli counters are mixed into ready meals, how chilled versus frozen is split, and whether currency conversion uses an average-year rate or a point-in-time rate. Update timing matters too, because short-term inflation and promotion intensity can move the value number quickly in Singapore.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.25 B (2025) | |

| Industry Data Publisher A | USD 3.43 B (2024) | Uses a wider ready-to-eat definition that appears to include additional prepared-food and packaging-technology adjacencies, and it also reports an earlier base year, which can inflate the comparable total versus a retail-packaged-only view. |

| Market Advisory B | USD 0.24 B (2025) | Likely applies a narrower product basket and different channel weighting, and the value can shift if average selling prices are projected using a simple trend rather than being checked against observed pack-price tiers by storage type. |

Overall, the spread mainly comes from what is counted as ready-to-eat in practice and which sales routes are included in the demand pool. When the scope is kept tied to packaged retail and e-grocery items, and the pricing logic is checked against real pack sizes and shelf formats, the resulting market value stays easier to trace and replicate year to year.

Key Questions Answered in the Report

What is the current value of the Singapore ready-to-eat food market?

The market is valued at USD 0.28 billion in 2026 and represents a single-city consumer base with high purchasing power.

What growth rate is forecast for the Singapore ready-to-eat food market through 2031?

Revenue is projected to rise to USD 0.34 billion by 2031, translating to a 3.12% CAGR over the period.

How are health trends shaping product innovation?

Brands reformulate with lower sodium, natural preservatives and plant-based proteins to address rising health awareness and comply with Nutri-Grade labeling.

Why is Singapore considered a regional launchpad for ready-to-eat products?

A compact geography, streamlined food-safety approvals and high expatriate diversity allow companies to test new flavors locally before scaling to wider ASEAN markets.

Page last updated on: