Asia-Pacific Online Grocery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

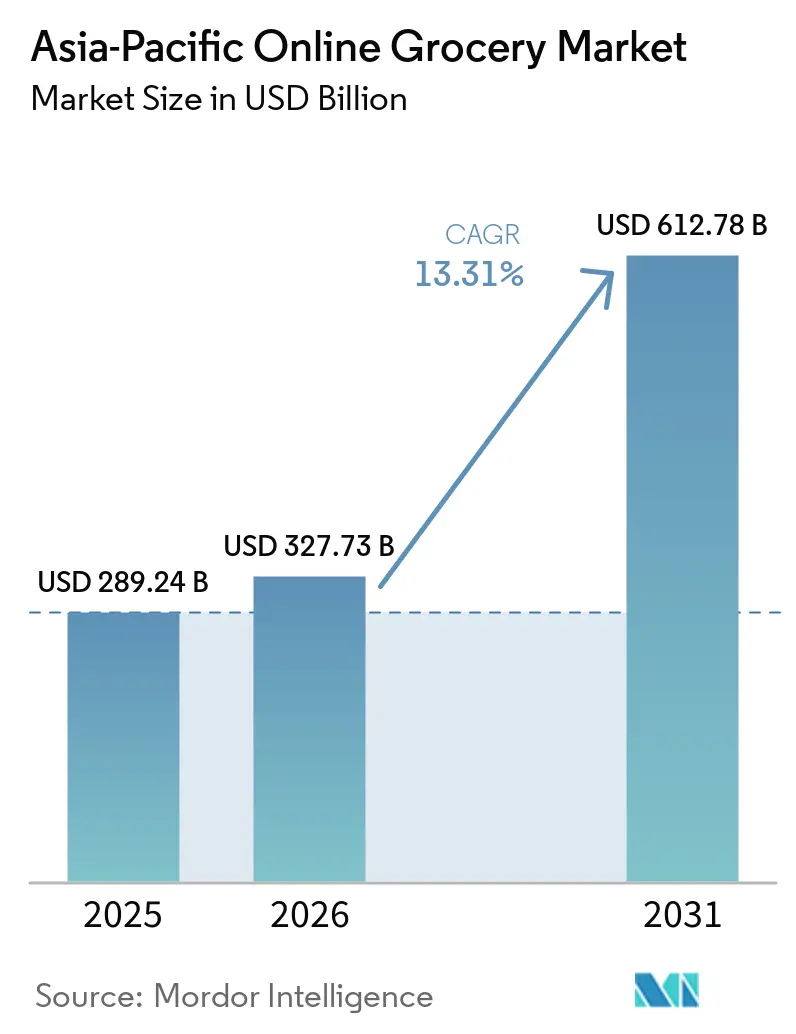

| Base Year Market Size (2025) | USD 289.24 Billion |

| Market Size (2026) | USD 327.73 Billion |

| Market Size (2031) | USD 612.78 Billion |

| Growth Rate (2026 - 2031) | 13.31% CAGR |

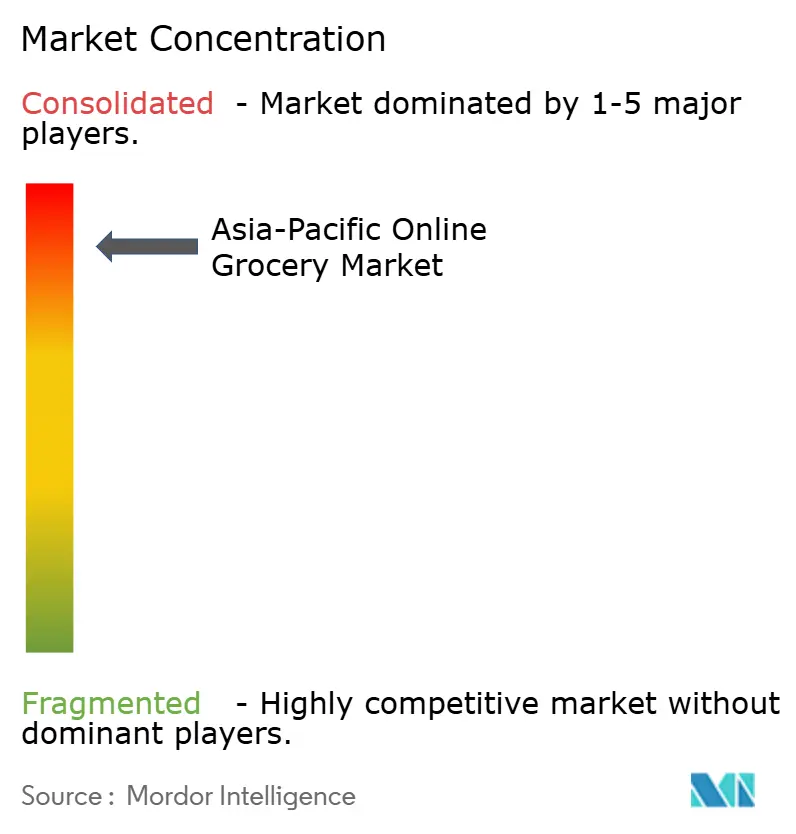

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Online Grocery Market Analysis by Mordor Intelligence

The Asia‑Pacific Online Grocery Delivery Market is expected to grow from USD 289.24 billion in 2025 to USD 327.73 billion in 2026 and is forecast to reach USD 612.78 billion by 2031 at a CAGR of 13.31% over 2026–2031. High smartphone penetration, scalable digital payments, and urban fulfillment models are driving a shift from planned stock-ups to smaller, instant purchases, emphasizing app-first shopping experiences. High-frequency digital payment systems like India’s UPI enable near-instant grocery replenishment, boosting order frequency and repeat purchases in densely populated areas[1]GSMA Intelligence Team, “Digital Societies in Asia-Pacific,” GSMA, gsma.com. Investments in cold chain infrastructure and automated fulfillment centers in Australia and Japan enhance freshness consistency and reduce cycle times for perishables, building trust in online fresh purchases. Policy frameworks in China and ASEAN promoting cross-border data flows, retail digitization, and instant retail align with platform strategies for sub-two-hour deliveries, bridging gaps with offline shopping experiences.

Key Report Takeaways

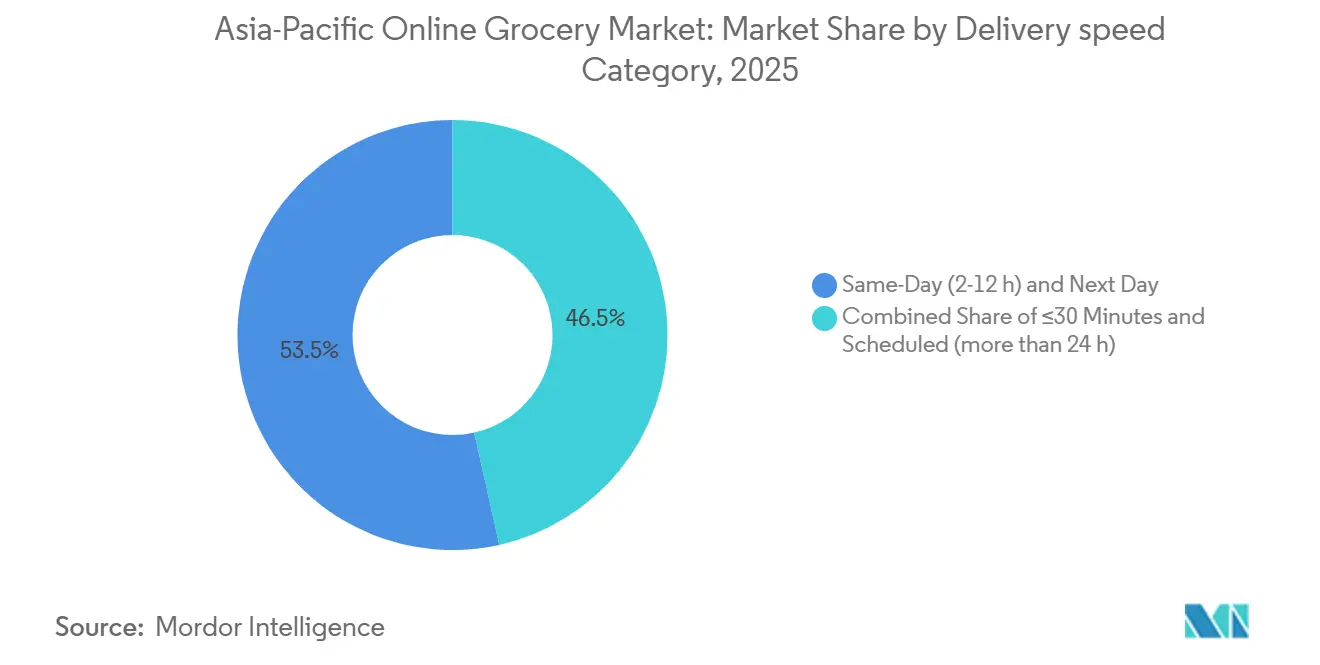

- By delivery speed, same-day and next-day services held 53.48% of the Asia-Pacific online grocery delivery market share in 2025, while the ≤30-minute category is forecast to post an 18.74% CAGR through 2031.

- By product type, staples and packaged goods led the Asia‑Pacific online grocery delivery market with a 31.78% revenue share in 2025, while fresh produce is projected to expand at a 17.35% CAGR through 2031.

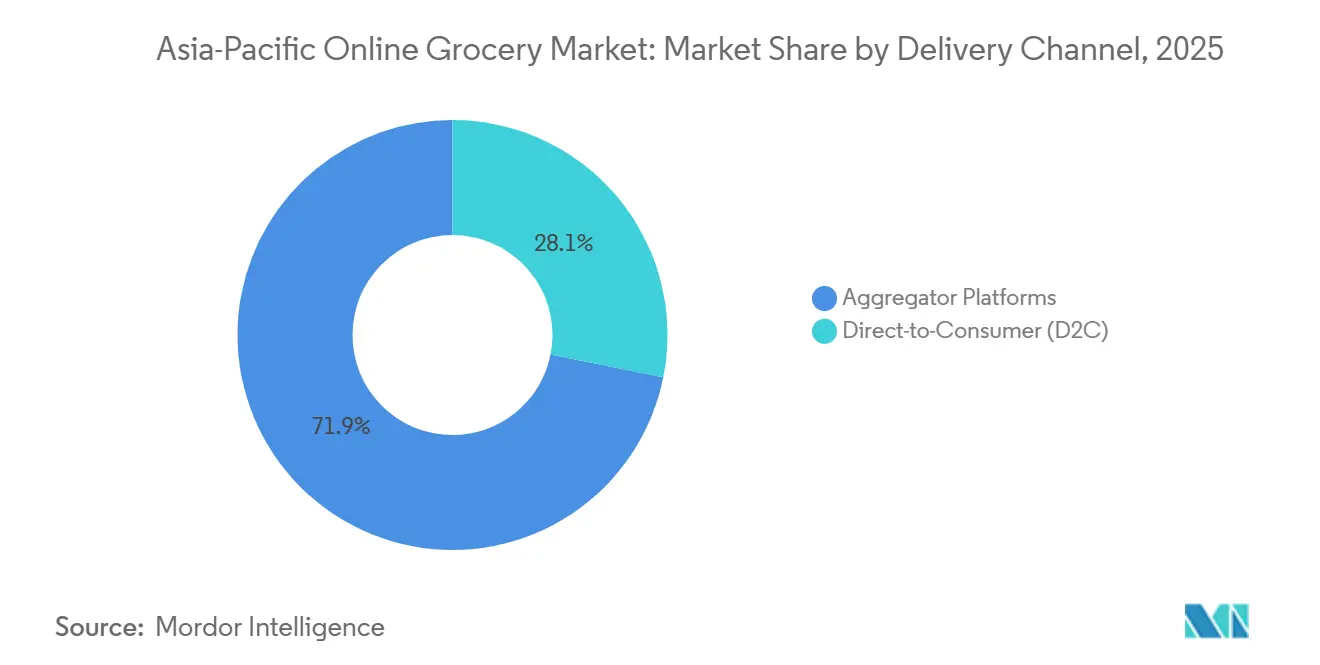

- By delivery channel, aggregator platforms commanded 71.86% share of the Asia-Pacific online grocery delivery market size in 2025, and direct-to-consumer models are advancing at a 15.92% CAGR through 2031.

- By geography, China accounted for 45.88% of the Asia-Pacific online grocery delivery market share in 2025, while India is recording the fastest CAGR of 16.55% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia contributes to a system defined not by any single geography but by the interaction of many. The global online grocery market data by Mordor Intelligence represents that combined structure.

Asia-Pacific Online Grocery Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising online adoption of fresh and perishable grocery categories | +2.8% | Global, strongest in India, Southeast Asia, Australia | Medium term (2-4 years) |

| Smartphone penetration driving mobile-first grocery shopping behavior | +3.1% | Pan-regional, particularly India, Indonesia, Philippines, Vietnam | Short term (≤ 2 years) |

| Rapid growth of quick commerce for instant delivery needs | +4.2% | Urban cores in China, India, expanding in parts of Southeast Asia | Medium term (2-4 years) |

| Government support for digital infrastructure and e-commerce adoption | +3.3% | India, China, ASEAN member states | Long term (≥ 4 years) |

| Booming On-Platform Advertising Budgets Among FMCG Brands | +1.4% | China, India, Philippines, Thailand | Medium term (2-4 years) |

| Subscription-Based Delivery Models for Daily Essentials | +1.7% | Japan, Singapore, Australia, urban China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Online Adoption of Fresh and Perishable Grocery Categories

Fresh produce has become a key growth driver for platforms, supported by advancements in temperature-controlled logistics and automated picking, which enhance order accuracy and minimize waste. Automated customer fulfillment centers in Sydney and Melbourne have increased throughput and improved freshness, enabling scalable two-hour delivery windows and strengthening consumer trust in online purchases of perishables. Cold chain gaps persist in several markets, with India experiencing post-harvest losses of 5–15% for fruits and vegetables due to inadequate farmgate infrastructure and a focus on single commodities. Regional cold chain projects and modernized logistics systems are addressing these challenges, while Southeast Asia requires further investment in storage, energy-efficient operations, and digital WMS and TMS.

Smartphone Penetration Driving Mobile-First Grocery Shopping Behavior

Mobile devices dominate digital commerce access across Asia-Pacific, with smartphone adoption shaping how consumers discover, order, and pay for groceries. Younger demographics and urban density drive frequent orders, while real-time inventory visibility and route optimization reduce delivery times. In Japan, e-commerce ecosystems integrate fulfillment centers, loyalty programs, and payment systems, enhancing engagement for routine grocery purchases. Regional policies on digital identity and cross-border data flows aim to ease checkout and compliance for mobile-first transactions across ASEAN. In India, account-to-account payments and minimal transaction costs eliminate cash-handling inefficiencies, enabling quick, low-value transactions and supporting mobile grocery adoption at scale.

Rapid Growth of Quick-Commerce for Instant Delivery Needs

Instant delivery services are becoming more professionalized, with platforms utilizing denser micro-fulfillment networks and improved demand forecasting to enable rapid delivery of groceries and ready-to-eat items. In China, major players combine online-first assortments with networked frontend warehouses and selective offline locations to support 30-minute deliveries in high-density areas[2]Woolworths Group Corporate Affairs, “Customer Fulfilment Centers and Two-hour Coverage,” Woolworths Group, woolworthsgroup.com.au. Order economics improve as platforms enhance item availability, reduce substitutions, and use merchandising algorithms to promote higher-margin categories and private labels, offsetting last-mile costs. Mature markets adopt mixed models, integrating click-and-collect for larger baskets with instant delivery for urgent needs. Operators prioritize safety and compliance amid evolving curb management and labor policies to compete with retailer-owned channels and integrated ecosystems.

Government Support for Digital Infrastructure and E-Commerce Adoption

Public policy drives digital grocery adoption through investments in digital payments, data infrastructure, and cross-border harmonization. Budgetary allocations in India support zero-MDR digital payments for small-ticket transactions, ensuring merchant acceptance and cost efficiency for mobile grocery purchases. China’s Digital Business Action Plan strengthens instant retail, live commerce, and rural e-commerce logistics, enabling faster delivery of necessities to urban areas. ASEAN governments have finalized a digital economy framework to streamline data flows, digital identity, and e-invoicing, fostering cross-border e-commerce growth. Expanding cloud infrastructure, 5G, and data centers allow retail platforms to leverage policy-driven ecosystems for reliable services and standardized compliance in last-mile operations.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High last-mile delivery costs and urban congestion challenges | -2.1% | Metro areas in India, Indonesia, Philippines, Thailand, China Tier-1 cities | Medium term (2-4 years) |

| Inadequate cold chain infrastructure in Tier-2 and Tier-3 cities | -1.8% | India, Indonesia, Vietnam, rural China, Philippines | Long term (≥ 4 years) |

| Rising Urban Warehouse Rents Eroding Quick-Commerce Margins | -1.3% | Major metropolitan areas globally | Medium term (2-4 years) |

| Intense Competition Leading to Profit Margin Pressure | -1.9% | Regional, particularly India and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Last-Mile Delivery Costs and Urban Congestion Challenges

Urban congestion and delivery density variability keep last-mile costs high, impacting unit economics for under-30-minute delivery. Platforms address these challenges through route clustering, batched picking, and dynamic labor allocation, but demand fluctuations driven by time of day and weather drive cost-to-serve variability. Perishable-heavy baskets can improve margins if spoilage is controlled, though temperature-controlled handling and returns management add costs requiring scale to offset. Retailer-owned store networks mitigate last-mile complexities by using backrooms and curbside pickup to smooth peak-hour demand and reduce delivery distances. Urban policies on curb space, delivery windows, and rider safety influence capacity planning, requiring compliance while maintaining delivery speed.

Inadequate Cold Chain Infrastructure in Tier-2 and Tier-3 Cities

Cold chain gaps in smaller cities and rural areas limit the availability of fresh products, increase shrinkage risk, and hinder the adoption of high-value perishables online[3]National Centre for Cold-chain Development Secretariat, “Post-Harvest Losses and Infrastructure,” NCCD, nccd.gov.in. Underinvestment in farmgate packhouses, reefer fleets, and multi-temperature storage causes inconsistent product quality, reducing repeat purchases for sensitive categories. Development finance initiatives and public-sector projects have improved temperature-controlled capacity and digitized logistics, but more infrastructure is needed for nationwide coverage. Expanding grocery platforms require sustainable cold-chain solutions to scale online categories like berries, dairy, and seafood. In high-energy-cost regions, operators deploy solar-powered facilities and energy-efficient refrigeration to enhance margins and support broader online assortments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Speed: Compressed Timelines Redefine Competitive Moats

Same-day and next-day services are projected to account for 53.48% of the market in 2025, with ultra-fast delivery within 30 minutes growing at a CAGR of 18.74% through 2031. Dense networks and automated fulfillment systems are transforming access to daily essentials across cities. The Asia-Pacific online grocery delivery market is shifting toward shorter delivery windows, balancing express deliveries for smaller orders with scheduled deliveries for larger baskets to optimize vehicle utilization and labor productivity. Automated customer fulfillment centers in Australia enhance throughput and accuracy for high-demand items, increasing two-hour delivery rates in metropolitan areas and strengthening trust in fresh delivery services. In China, networked warehouses integrated with online assortments enable 30-minute delivery in dense areas, supported by selective offline locations for instant delivery.

Advancements in routing, inventory visibility, and city logistics reduce cancellations and substitutions, improving customer experience in fast-delivery formats. Scheduled deliveries beyond 24 hours remain vital for bulk restocking in suburban areas, ensuring the relevance of longer delivery windows. Micro-fulfillment adoption compresses pick-to-ship times, expanding same-day delivery coverage. Hybrid models like click-and-collect lower last-mile costs and improve suburban pickup options. Platforms use short-window order data to refine assortments and pricing, enhancing conversion rates. The market trends toward shorter timelines while maintaining capacity for larger orders, mitigating peak demand and ensuring fresh product availability.

By Product Type: Fresh Produce Upends FMCG Economics

Fresh produce is the fastest-growing category with a CAGR of 17.35% through 2031, driving investment in temperature-controlled logistics and farm-direct integration. Staples and packaged goods accounted for 31.78% of the market in 2025. The Asia-Pacific online grocery delivery market benefits from improved cold chain infrastructure and quality assurance, reducing shrinkage and encouraging repeat purchases in fruits, vegetables, dairy, and meat. India’s post-harvest losses of 5–15% for fruits and vegetables highlight infrastructure challenges, prompting public and private investment. Australian retailers upgraded automated centers with multi-temperature zones and predictive restocking, enhancing fresh product fulfillment and expanding online offerings. China’s ecosystems support grocery needs through networked warehouses and subsidy programs, increasing throughput in fresh and ambient categories.

Fresh and chilled categories benefit from temperature-controlled last-mile delivery and smarter inventory placement, reducing returns and improving margins by 2026. Retailers use loyalty ecosystems and app telemetry to customize fresh assortments, improving picking efficiency and on-time, in-full rates for perishables. Improved cold chain standards and food safety compliance in Southeast Asia give integrated logistics platforms an edge over fragmented operators struggling with heat-sensitive SKUs. Automated quality checks at receiving and dispatch reduce substitution risks and waste in short shelf-life categories. Category leadership depends on network density and temperature-controlled capacity to sustain high service levels without eroding margins.

By Delivery Channel: Aggregators Face D2C Pressure as Brands Verticalize

Aggregator platforms held 71.86% of the market in 2025, while Direct-to-Consumer (D2C) channels are projected to grow at a 15.92% CAGR through 2031, driven by retailer and FMCG investments in proprietary last-mile systems and owned data to reduce aggregator commissions. The Asia-Pacific online grocery delivery market is balancing aggregator convenience with retailer-led channels leveraging store networks and micro-fulfillment centers to enhance speed and margins through private labels. In India, quick commerce and retailer-owned networks focus on two-hour delivery, supported by micro-fulfillment and farm-direct sourcing for fresh quality. China’s ecosystems optimize warehouse assortments, integrate offline assets to ensure consistency, and leverage merchant services and promotions to drive volume. Aggregators expand into beauty, pharmacy, and alcohol to improve basket economics and capture higher-margin trips.

Australia demonstrates dual-channel strategies, combining proprietary fulfillment with aggregator partnerships for urban reach. The market emphasizes loyalty programs, in-app advertising, and private-label expansion to offset costs, strengthening D2C models in dense store areas. Southeast Asia benefits from open digital economy initiatives and interoperable payment systems, fostering competition on speed and reliability[4]Grab Corporate Newsroom, “Category Expansion and Merchant Partnerships,” Grab, grab.com. Japan’s integrated ecosystems use fulfillment hubs linked to loyalty programs and fintech services to drive repeat purchases and tighten data control. A mixed model of aggregator and D2C channels will rely on automation and data to meet freshness and speed expectations.

Geography Analysis

China's share in the Asia-Pacific online grocery delivery market is expected to reach 45.88% in 2025, driven by integrated logistics, networked frontend warehouses, and ecosystem-driven promotions that have expanded grocery delivery in major cities. Consolidation efforts enhance capacity and coverage in the Jiangsu-Zhejiang-Shanghai corridor, combining online-first assortments with selective offline presence for instant fulfillment. Retailers balance online-only and hybrid warehouse store formats to achieve 30-minute delivery targets in core districts while extending to suburban areas with scheduled windows. Policy support for instant retail and live-streaming commerce fosters growth in daily necessities and fresh categories through digital channels. Investments in digital infrastructure ensure that fast and reliable delivery remains a priority by 2026.

India, with a projected CAGR of 16.55% through 2031, benefits from smartphone adoption, digital payment policies, and the expansion of micro-fulfillment centers in major cities. UPI facilitates seamless transactions and frequent purchases of essentials, while investments in direct-sourcing programs for fruits and vegetables improve quality and reduce shrinkage in Tier-1 and Tier-2 cities. Platforms adapt processes and pricing to evolving gig-worker protections, focusing on reliable two-hour delivery in dense areas. Growth in fresh and chilled categories is supported by advancements in cold chain and urban logistics. Southeast Asia, Japan, Australia, and New Zealand show diverse market maturity, shaping platform strategies by 2026. Southeast Asia's digital economy initiatives enable cross-border operations and scaling of aggregator and D2C models. Singapore's AI-enabled "Store of Tomorrow" technologies enhance online-physical integration. Australia's automated fulfillment centers expand two-hour delivery and improve order accuracy, supporting e-commerce growth while maintaining fresh quality. Emerging ASEAN markets benefit from improved last-mile reliability and logistics modernization, reducing costs and strengthening market prospects through 2031.

The online grocery market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for Canada, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The Asia-Pacific online grocery delivery market is moderately concentrated in large metropolitan areas but remains competitive across ecosystems, retailers, and aggregators, with a focus on speed, availability, and reliability. Leading platforms in China are expanding their warehouse networks to deliver daily necessities faster while establishing offline locations for near-instant service in high-density areas. Ecosystems are investing in hybrid warehouse-store formats, grocery subsidies, and merchant services to balance volume and profitability in fresh and ambient categories. In India, ecosystem players are scaling micro-fulfillment centers and fresh sourcing, while retailers with extensive store networks are developing direct-to-consumer (D2C) channels to improve data control and margins. Australian players are adopting dual-channel strategies, combining proprietary fulfillment with aggregator partnerships to extend reach for urgent deliveries while maintaining service quality for scheduled orders. Investments in automation, cold chain infrastructure, and policy-aligned capabilities are streamlining daily grocery delivery operations. Retail media and loyalty platforms are critical for margin defense, aligning with the focus on ecosystem-owned data and private-label growth.

Two-hour and sub-two-hour delivery depends on advancements in picking productivity, AI-driven forecasting, and slot management to maintain margins for perishable-heavy orders. Platforms are diversifying categories served through last-mile networks to increase order value and manage demand fluctuations. Expansion into Tier-2 locations requires aligning service promises with population density to ensure cost efficiency. Financial disclosures indicate a focus on warehouse automation, retail media, and scalable customer service. Ecosystems are integrating AI-driven fulfillment and customer support to manage peak demand, while retailers prioritize curbside pickup, "Direct to Boot," and rapid on-demand delivery. Policy measures on digital payments and data management are reducing barriers for small merchants and cross-border sellers, supporting disciplined growth in the market.

Asia-Pacific Online Grocery Industry Leaders

Alibaba Group

JD.com

Amazon

Reliance Retail

Flipkart

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: JD.com reported FY2025 results and launched its “Billion Supermarket” channel with multi-year product subsidies focused on daily necessities to drive additional branded sales growth.

- March 2026: Grab announced the acquisition of foodpanda Taiwan, expanding its regional footprint subject to regulatory approvals and integration milestones through 2027.

- February 2026: Meituan completed its USD 717 million acquisition of Dingdong Maicai’s China business, adding over 1,000 frontend warehouses and expanding instant retail capabilities in core urban clusters.

- June 2025: FairPrice Group and Google Cloud launched a strategic program to test and scale retail innovations, including AI-powered carts, price cards, hybrid formats, and predictive restocking tools.

Asia-Pacific Online Grocery Market Report Scope

The Asia-Pacific Online Grocery Delivery Market evaluates digital grocery fulfillment models, including rapid delivery, same-day, next-day, and scheduled services. It analyzes market size, growth projections, and segmentation by delivery speed, product type, delivery channel, and country-level geography. Key drivers include rising online adoption of perishables, smartphone-driven shopping, quick commerce expansion, and FMCG investments in digital promotions, while challenges such as last-mile delivery costs, cold-chain gaps, and competitive margin pressures are addressed. The report examines consumer behavior, regulatory frameworks, technological advancements, and competitive dynamics through market concentration, strategic initiatives, share analysis, and company profiles. Future opportunities and long-term trends are outlined, with values in USD billion.

| ≤30 Minutes |

| Same-Day (2-12 h) and Next Day |

| Scheduled (more than 24 h) |

| Fresh Produce |

| Dairy and Bakery |

| Meat, Fish, and Seafood |

| Staples and Packaged Goods |

| Beverages |

| Frozen Foods |

| Other Product Type |

| Direct-to-Consumer (D2C) |

| Aggregator Platforms |

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| South Korea |

| Vietnam |

| Philippines |

| Rest of Asia-Pacific |

| By Delivery Speed | ≤30 Minutes |

| Same-Day (2-12 h) and Next Day | |

| Scheduled (more than 24 h) | |

| By Product Type | Fresh Produce |

| Dairy and Bakery | |

| Meat, Fish, and Seafood | |

| Staples and Packaged Goods | |

| Beverages | |

| Frozen Foods | |

| Other Product Type | |

| By Delivery Channel | Direct-to-Consumer (D2C) |

| Aggregator Platforms | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| South Korea | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current size and outlook of the Asia Pacific online grocery delivery market?

The Asia-Pacific online grocery delivery market size is USD 327.73 billion in 2026 and is forecast to reach USD 612.78 billion by 2031 at a 13.31% CAGR, supported by mobile adoption, digital payments, and rapid fulfillment models.

Which delivery speeds are shaping customer expectations in Asia-Pacific grocery?

Same-day and next-day held 53.48% share in 2025, while under-30-minute delivery is the fastest-growing at an 18.74% CAGR through 2031, anchored by dense micro-fulfillment and automation.

Which categories are driving growth within the Asia-Pacific online grocery delivery market?

Fresh produce is the primary growth lever with a 17.35% CAGR through 2031, while staples and packaged goods held 31.78% in 2025 as platforms invest to improve freshness consistency and reduce shrink. .

How is competition evolving between aggregators and D2C channels?

Aggregators held 71.86% in 2025, but D2C is projected to grow at 15.92% as retailers leverage store networks, micro-fulfillment, and loyalty ecosystems to control data and margins.

Which geographies lead and which are growing fastest in the region?

China led with 45.88% in 2025, while India is the fastest-growing with a 16.55% projected CAGR through 2031, aided by smartphone ubiquity and scalable digital payments.

What policy shifts matter most for Asia-Pacific grocery delivery to 2031?

Digital payments support in India and cross-border data harmonization under ASEAN’s DEFA, along with China’s instant retail policy backing, reduce friction and improve scalability for platforms .

Page last updated on: