Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

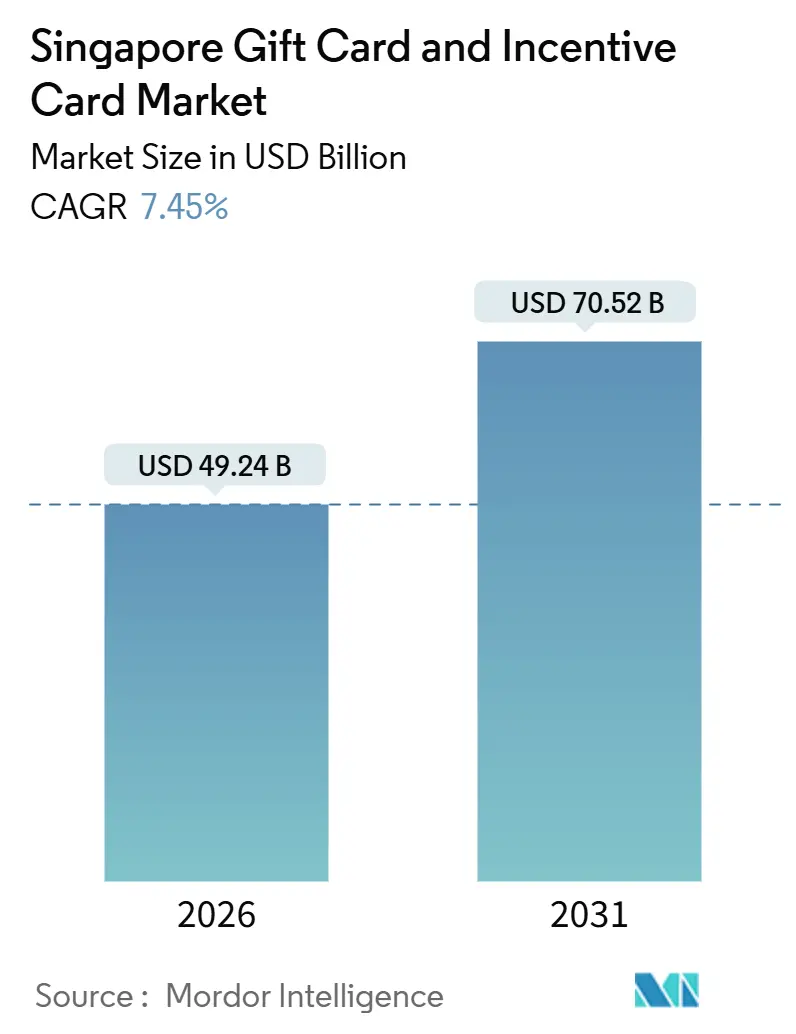

| Market Size (2026) | USD 49.24 Billion |

| Market Size (2031) | USD 70.52 Billion |

| Growth Rate (2026 - 2031) | 7.45% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Singapore Gift Card And Incentive Card Market Analysis by Mordor Intelligence

The Singapore gift card and incentive card market size is USD 49.24 billion in 2026 and is projected to reach USD 70.52 billion by 2031 at a 7.45% CAGR during the forecast period (2026-2031).

This growth is supported by very high digital payments adoption, where cashless usage at retail points of sale and PayNow registration rates among adults have normalized QR-based redemption across everyday spending[1]Monetary Authority of Singapore, “E-Payments and PayNow Adoption Updates,” Monetary Authority of Singapore, mas.gov.sg. . Government vouchers are a key demand catalyst, with supermarket-directed SG60 allocations and cumulative CDC voucher redemption validating large-scale acceptance among heartland merchants. Corporate incentive budgets are rising faster than consumer-led gifting as employers standardize gift cards for rewards and retention, reinforced by program rules that maintain tax efficiency for lower-value awards. Tourism recovery and cross-sector partnerships further channel visitor spending into curated gift-card bundles that target high-value experiences rather than general merchandise[2]Singapore Tourism Board, “Visitor Arrivals and Tourism Receipts 2024,” Singapore Tourism Board, stb.gov.sg..

Key Report Takeaways

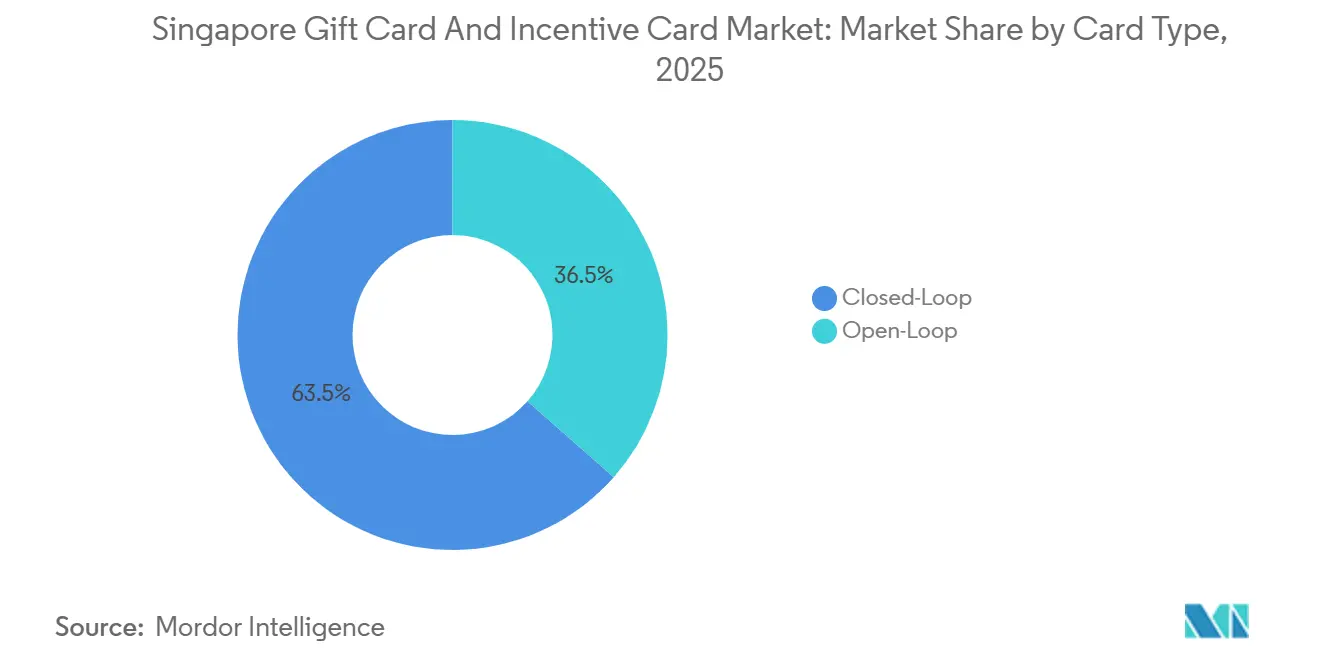

- By card type, closed-loop led with 63.50% of the Singapore Gift Card and Incentive Card Market revenue share in 2025, while open-loop is forecast to expand at a 9.82% CAGR through 2031.

- By format, physical cards held a 56.80% share of the Singapore Gift Card and Incentive Card Market in 2025, while digital cards are projected to grow at a 13.66% CAGR through 2031.

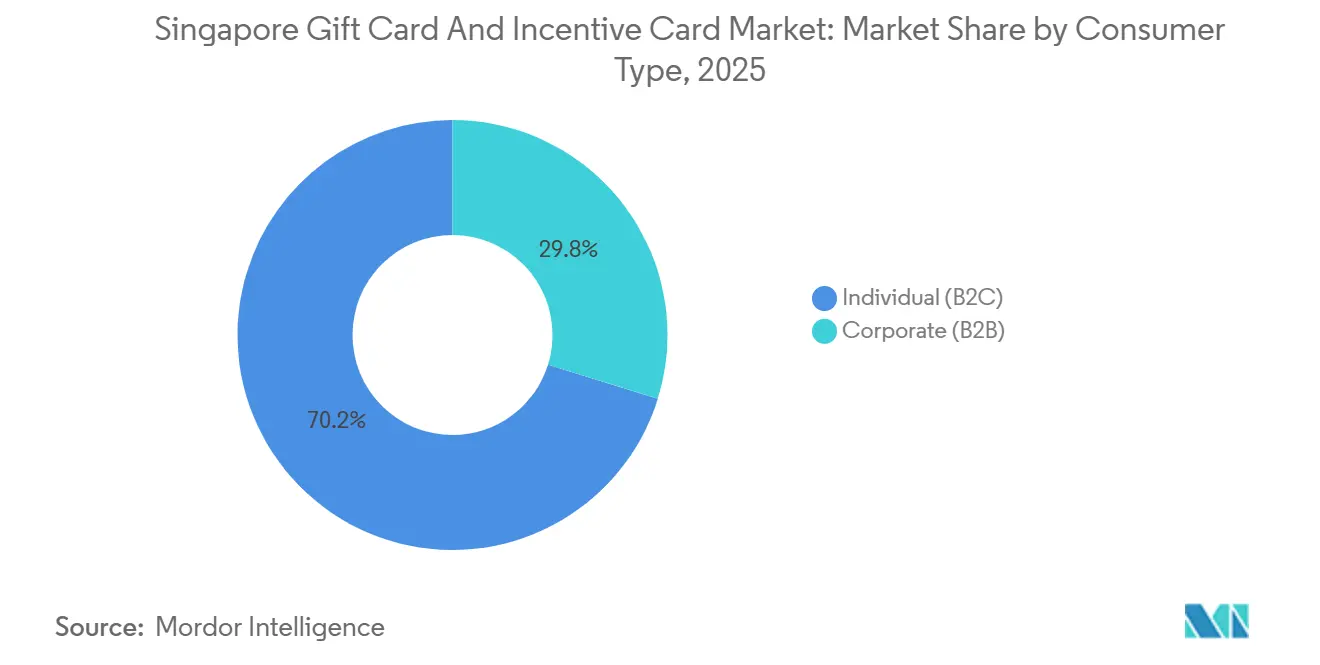

- By consumer type, the Individual segment accounted for 70.20% share of the Singapore Gift Card and Incentive Card Market in 2025, while the Corporate segment is set to record a 10.23% CAGR through 2031.

- By distribution channel, offline commanded a 58.70% share of the Singapore Gift Card and Incentive Card Market in 2025, while online is expected to expand at a 12.93% CAGR through 2031.

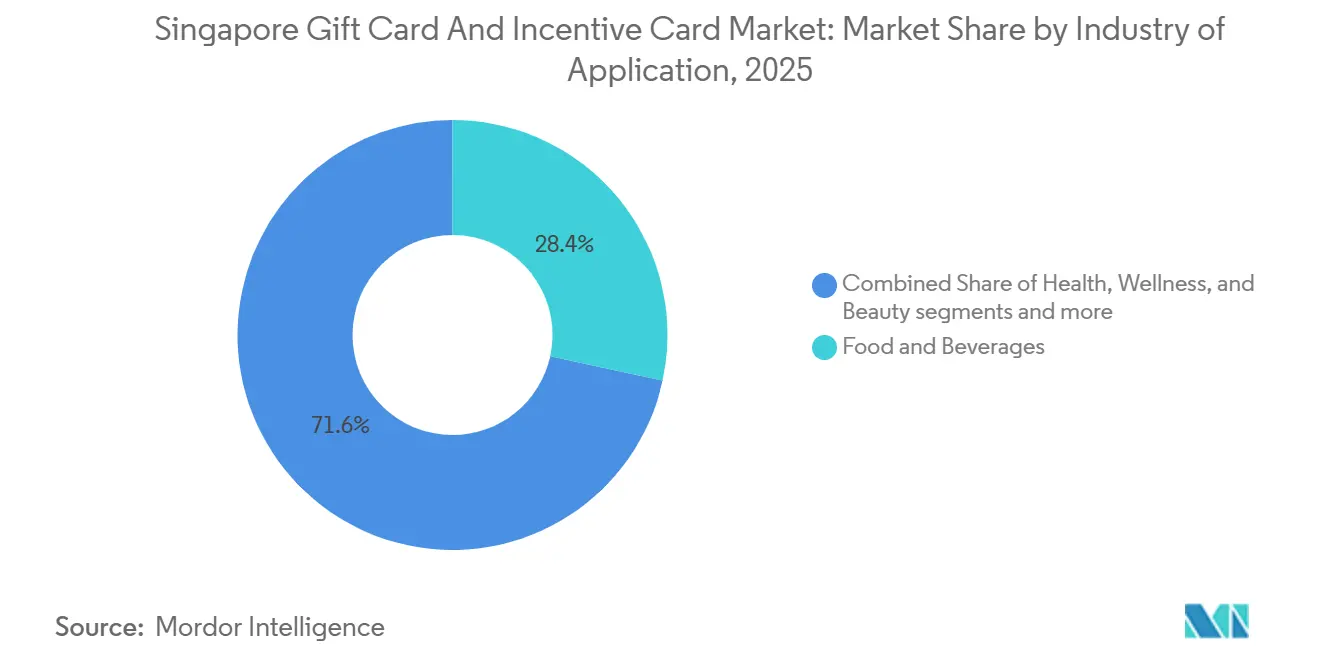

- By industry application, Food and Beverages captured a 28.40% share of the Singapore Gift Card and Incentive Card Market in 2025, while Consumer Electronics is projected to advance at an 11.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Singapore Gift Card And Incentive Card Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Voucher Programs: SG60 Vouchers Boost Adoption | +2.8% | National, with early gains in heartland neighborhoods and HDB estates (Ang Mo Kio, Tampines, Jurong West) | Short term (≤ 2 years) |

| Advanced Digital Infrastructure: Mobile & E-Wallet Integration | +1.9% | National, with spillover to cross-border ASEAN PayNow linkages (Thailand, India, Malaysia, Indonesia) | Medium term (2-4 years) |

| Corporate Incentive Demand: Employee Rewards in a Competitive Talent Market | +1.5% | National, concentrated in CBD and regional HQ clusters (Marina Bay, Tanjong Pagar, Raffles Place) | Medium term (2-4 years) |

| Tourism Recovery: Driving Visitor Spending Post-Pandemic | +1.2% | National, with concentration in Orchard Road, Marina Bay, Sentosa tourist zones, and Changi Airport transit retail | Short term (≤ 2 years) |

| E-Commerce Expansion: Digital Gifting in Singapore’s Smart Nation Push | +1.0% | National, driven by Lazada, Shopee, and Grab platforms with the highest penetration among the 20-40 age cohort | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Voucher Programs Normalize Digital Gift Card Infrastructure

The SG60 Voucher scheme that allocates SGD 600 to SGD 800 per citizen through 2026 and the multi-year CDC Vouchers that reach households have scaled universal merchant onboarding beyond what private pilots achieved[3]Open Government Products, “RedeemSG, Building Trusted Voucher Infrastructure,” Open Government Products, ogp.gov.sg.. RedeemSG’s coverage spans tens of thousands of outlets, and cumulative voucher redemption volumes in the billions of dollars show widespread usage across hawker centers and supermarkets. This baseline has trained a large pool of merchants to process QR redemptions, which lowers acquisition costs for private issuers moving into the same channels in the Singapore gift card market. DBS reported that SG60-linked supermarket sales grew year over year across multiple months in 2025, which highlights the demand lift that voucher tranches can create for targeted categories. As technology becomes commoditized, differentiation shifts toward curated reward design and merchant networks rather than raw acceptance features in the Singapore gift card market.

Corporate Incentive Demand Fueled by Talent Retention Imperatives

FlexiGrow budgets assign SGD 500 per year to 86,000 civil servants, marking a clear shift toward structured non-cash benefits that align with wellness and upskilling aims. Large employers and regional headquarters adopt gift cards as tax-aware rewards that can stay below the SGD200 GST threshold for non-input-tax gifts without triggering output tax obligations. The Corporate segment’s projected 10.23% CAGR through 2031 reflects operational preferences for scalable, API-driven fulfillment instead of manual procurement. Giftbit’s March 2025 launch in Singapore with options across Grab, Lazada, and Shopee underscores how centralized platforms simplify budget distribution for multi-brand catalogs[4]Giftbit, “Giftbit Launches in Singapore with Grab, Lazada, Shopee,” Giftbit, giftbit.com. The Singapore gift card market stands to benefit from continued HR digitization as incentive portfolios become a standard feature in retention and engagement strategies.

Tourism Recovery Converts Visitor Spend into Gift Card Momentum

Singapore received 16.5 million arrivals in 2024 with SGD 29.8 billion in tourism receipts, shifting retailer focus toward experience-led gift vouchers that align with new visitor preferences. Integrated resorts deploy bespoke gift credit such as Resort Dollars that add value per booking and encourage on-site spending across dining, attractions, and retail. Cross-sector tie-ups like Singapore Airlines with Takashimaya attach store vouchers to loyalty journeys to pre-commit spend before travelers arrive. Chinese visitor recovery strengthened in 2024, and familiarity with super-app payments raises expectations for seamless QR redemption in Singapore. The Singapore gift card market captures this momentum through bundled, itinerary-aligned instruments that match high-value traveler segments.

Advanced Digital Infrastructure Enables Frictionless Redemption at Scale

Cashless adoption at retail and very high PayNow usage among adults underpin a nationwide baseline for QR-based redemption and digital issuance. SGQR interoperability across 30 or more payment schemes compresses consumer education needs by presenting a single code for vouchers, bank wallets, and private gift cards. Cross-border PayNow links to regional instant payment systems and Project Nexus planned for 2026 present cross-market scaling routes for issuers in Singapore. Large POS networks, including more than 130,000 NETS terminals, offer near-ubiquitous acceptance for merchants across the island. The Singapore gift card market benefits from this ubiquity but must also manage trust exposure when cybersecurity incidents affect shared infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Scam and Fraud Risks: Need for Consumer Education & Verification | -1.3% | National, with higher incidence in digitally active but less tech-savvy senior cohorts (60+ age group) | Short term (≤ 2 years) |

| Cybersecurity Vulnerabilities: Exposure to Hacks and Platform Outages | -0.9% | National, systemic risk concentrated in NETS, DBS PayLah!, GrabPay infrastructure serving 95%+ of digital transactions | Medium term (2-4 years) |

| GST Compliance Burden: Output Tax on Gifts Above SGD 200 | -0.7% | National, particularly affecting corporate B2B segment above gift threshold and multinational HQ compliance teams | Medium term (2-4 years) |

| Market Saturation: Intense Competition in a Mature Payments Landscape | -0.5% | National, acute in supermarket and convenience store segments with 95%+ digital wallet penetration already achieved | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fraud Proliferation Outpaces Consumer Education Despite Regulatory Countermeasures

Phishing scam losses rose 134% to SGD 30.4 million in the first half of 2024, indicating a pivot to higher-value targets including corporate bulk purchases and tourist voucher claims. Mobile wallet phishing generated hundreds of reports and significant losses in late 2024, often using spoofed links that mimic official voucher portals. Regulators and banks responded with 12-hour cooling-off periods for new payees and the shift from SMS one-time passwords to in-app tokens along with Money Lock that quickly attracted large balances. These protections improve security but add steps that can slow instant fulfillment flows that corporate users expect for same-day recognition. The Singapore gift card market must balance safety and speed while educating users to avoid phishing traps tied to high-profile voucher campaigns.

GST Compliance Complexity Constrains High-Value Corporate Gifting

Singapore’s GST rate at 9% since January 2024, combined with output tax rules for gifts over SGD200 when input tax is claimed, requires careful tracking by issuers. Companies running large incentive programs must monitor cumulative values per recipient to avoid triggering unexpected GST liabilities. IRAS clarified in November 2025 that free gift vouchers treated as rights rather than goods are exempt in promotional contexts where input tax is not claimed. This carve-out does not cover performance bonuses or retention gifts, which keeps compliance effort high for the fastest growing B2B use cases. The Singapore gift card market sees practical caps near the threshold for many corporate awards, which nudges larger awards toward open-loop cash substitutes or payroll channels.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Card Type: Closed-Loop Dominance Meets Open-Loop Flexibility

Closed-loop cards held 63.50% share in 2025, anchored by programs at NTUC FairPrice and Sheng Siong that keep redemption inside known ecosystems with tight control of margins and loyalty data. Open-loop instruments are expanding at 9.82% CAGR through 2031 in the Singapore gift card market size for card type, which aligns with corporate demand for flexible redemption across merchants. Interoperability through SGQR and the breadth of NETS terminals reduce friction that historically limited cross-merchant usage when issuers lacked direct retailer agreements. Giftbit’s March 2025 entry with options across Grab, Lazada, and Shopee reflects an emphasis on one-stop catalogs that support API-based fulfillment for enterprise buyers. Closed-loop issuers still show risk control advantages, as seen when retailers conduct mass reissuance or adjustments to support customers during inflationary phases in 2025.

Government SG60 and CDC vouchers are technically closed-loop but behave like open-loop in practice due to 28,656 participating outlets that accept redemptions across many categories. This ubiquity raises user expectations for broad acceptance regardless of issuer, which shifts competition toward catalog relevance in the Singapore gift card market. Mid-sized retailers that cannot match government-backed breadth use open-loop aggregators or white-label processors to reach more users without adding integration overhead. Takashimaya’s partnership with DBS, including voucher-linked rebates, shows how closed-loop brands can extend beyond their footprint by tapping bank infrastructure. Threshold-driven behavior around SGD200 steers high-value corporate awards to open-loop for maximum recipient autonomy while low-value promotions continue to favor closed-loop simplicity in the Singapore gift card market.

By Format Type: Physical Cards Persist Despite Digital Surge

Physical cards accounted for 56.80% share in 2025 as ceremonial gifting norms in corporate settings and senior preferences kept boxed presentations relevant. Digital cards are projected to grow at 13.66% CAGR through 2031 as e-commerce and same-day delivery make instant issuance the default for many use cases. Wallets such as DBS PayLah and GrabPay encourage in-app gifting and help merchants close loops from promotions to payment with minimal friction. API-enabled delivery supports distributed workforces and lets HR teams manage periodic rewards without manual handling in the Singapore gift card market. Apple’s December 2025 launch of Tap to Pay on iPhone reduces hardware costs, which expands digital acceptance for micro-merchants and home-based businesses.

Format preferences map to age and context, as younger cohorts prefer QR redemptions while older users still expect physical options as a reliable backup. Issuers maintain both digital and physical inventories to match demand across consumer gifting and corporate protocols in the Singapore gift card market. Courts uses e-gift cards bundled with appliances to create instant gratification, which nudges conversion without broad discounts that dilute margin. Companies continue to present physical cards at milestone ceremonies and route reloads through digital channels to streamline operations. This coexistence marks a transition period for the Singapore gift card industry as digital formats lead growth while physical cards anchor the installed base.

By Consumer Type: B2C Volume Meets B2B Velocity

The Individual segment accounted for a 70.20% share in 2025, driven by festive gifting and broad-based voucher reach across households and adult citizens. Corporate spend represented 29.80% but is on a faster trajectory with a 10.23% CAGR through 2031 in the Singapore gift card market size for corporate incentives. FlexiGrow assigns SGD 500 per year to 86,000 civil servants and many employers replicate low-value awards to maintain tax efficiency under GST rules. Giftbit focuses on API-based bulk distribution across major platforms to support centralized incentive programs with minimal manual effort. As a result, corporate adoption is the primary acceleration lever while B2C activity appears more mature in the Singapore gift card market.

B2C redemption concentrates in supermarkets and hawker centers where government vouchers channel spend into daily necessities across neighborhood clusters. The SG60 allocation of SGD 1 billion to supermarkets translated to 12% of 2024 supermarket sales, which signals how users prioritize essentials when they receive broad vouchers. Employers are steering awards into wellness and upskilling, and FlexiGrow codifies this with categories tied to health and personal development. This directional shift expands specialized catalogs and strengthens wellness and learning as anchor categories in the Singapore gift card industry. With cashless acceptance already near universal, additional B2C growth relies more on program design than on onboarding new digital users in the Singapore gift card market.

By Distribution Channel: Offline Anchors Meet Online Acceleration

Offline channels held 58.70% share in 2025 because supermarkets and convenience stores drive high-frequency transactions and host a large share of voucher redemptions. Online distribution is projected to grow at 12.93% CAGR through 2031, and the Singapore gift card market size for online channels benefits from native checkout integrations across e-commerce platforms. Giftbit’s 2025 launch showcases API-based fulfillment that links HR systems to issuance triggers without manual handling. Offline purchases often serve same-day and ad hoc gifting, while online purchases align with planned distributions at scale in the Singapore gift card market. Tourism-centric venues continue to deliver cards at physical touchpoints where concierge teams encourage top-ups and cross-sell experiences.

Retailers face margin pressure in physical locations and use gift cards to boost basket sizes, while convenience chains adopt gift cards to increase traffic. Online fulfillment removes production and logistics costs, which raises unit economics when acquisition costs stay under control. PayNow at checkout lowers processing fees compared with card rails and improves margins for online-first issuers in the Singapore gift card market. API-triggered workflows that connect HR and marketing stacks to issuance engines reduce manual steps and speed time to delivery in the Singapore gift card industry. High-value contexts still favor in-person service, so both channels remain relevant as programs scale in the Singapore gift card market.

By Industry of Application: F&B Dominance with Electronics Gaining

Food and Beverages captured 28.40% of the Singapore gift card market share in 2025 because hawkers and supermarkets accept government vouchers and serve daily needs. Consumer electronics is projected to grow at an 11.12% CAGR through 2031 as retailers bundle grocery vouchers with appliances to ease price sensitivity. Health, wellness, and beauty remain niche yet strategic as corporate programs encourage preventive care and fitness usage. Other categories such as entertainment, travel, and services benefit from integrated resort and mall-wide cards that aggregate spend under a single instrument in the Singapore gift card market. Partnerships like DBS and Takashimaya vouchers for KrisFlyer members help department stores convert window shoppers into buyers.

F&B growth rates moderate as acceptance saturates, while electronics ride steady product refresh cycles that sustain recurring gifting and promotion-led conversion. Sheng Siong maintains senior discounts through 2026 and harnesses voucher acceptance to defend share against online grocery rivals. Integrated resorts expand multi-category gift cards to capture a larger share of each visitor’s wallet in the Singapore gift card market. Vertical catalogs give issuers more room to tailor offers by need-state, which supports margin discipline without broad markdowns. As supermarkets protect share and electronics retailers manage price-conscious shoppers, gift cards align incentives with sell-through rather than reduce sticker prices.

Geography Analysis

Singapore’s 728.6 square kilometer footprint concentrates redemption in heartland estates where supermarkets and hawker centers dominate everyday transactions. Government voucher programs normalized digital redemption at tens of thousands of neighborhood merchants, which entrenched QR-based gifting behavior in the Singapore gift card market. Corporate incentives cluster in the Central Business District across Marina Bay, Tanjong Pagar, and Raffles Place with high demand for wellness, training, and premium dining redemptions. Tourism zones like Orchard Road, Sentosa, and Marina Bay record higher face values because hotels, airlines, and department stores align gift cards with itineraries. Per-visitor yields tied to 16.5 million arrivals and SGD 29.8 billion in receipts reinforce premium opportunities that targeted gift cards can unlock in these districts in the Singapore gift card market.

Cross-border PayNow links with Thailand, India, Malaysia, and Indonesia open up use cases that extend beyond domestic shoppers and create new routes for cross-border gifting. Project Nexus aims to establish multilateral instant settlement in 2026, which supports regional distribution for issuers based in Singapore. Changi Airport duty-free and transit retail act as specialized zones where outbound travelers purchase gift cards for future use to capture value before trips. Regional HQ density around the CBD shapes catalog mix because companies distribute incentives to employees and partners across Southeast Asia. As the rails strengthen, platforms in the Singapore gift card market aim to serve as regional hubs that clear cross-border gifting through interoperable payments.

High urban density enables near-universal terminal coverage and short distances between acceptance points, which lowers redemption friction for everyday use. The same density concentrates operational risk when shared service providers face outages or breaches, which organizations must address in service-level planning in the Singapore gift card market. Hawker digitalization programs and voucher onboarding expanded acceptance for micro-merchants, which brought more seniors and low-income households into digital redemption. This inclusiveness keeps gift-card activity embedded in daily life across neighborhoods instead of isolating it to malls or tourist corridors in the Singapore gift card market. Government-backed onboarding continues to trim customer acquisition costs for issuers that rely on existing merchant networks rather than field-building their own.

Competitive Landscape

The Singapore gift card and incentive card market remains low in concentration, with no single player dominating the market because state-backed infrastructure reduces barriers to entry and lets small merchants match acceptance breadth. NETS has more than 130,000 terminals, and RedeemSG onboards 28,656 outlets, which neutralizes many scale advantages for incumbents. Retail incumbents such as NTUC FairPrice and Sheng Siong emphasize closed-loop programs that capture data and push private-label value. New entrants like Giftbit and wallet ecosystems, including YouTrip and Revolut, prioritize open-loop aggregation and cross-merchant flexibility. Regulators place cross-border instant payments on the roadmap, which aligns with issuers’ regional expansion goals from a Singapore base in the Singapore gift card market.

API-driven bulk fulfillment is a core differentiator for B2B because it connects HR and CRM systems directly to issuance without manual steps. Fraud analytics and QR monitoring are competitive levers as banks like OCBC highlight growth in scan-and-pay usage supported by backend risk controls. Grab turns wallet engagement into gifting distribution power while CapitaLand shows how mall-wide cards unify dozens of tenants under one program. These platform-first models let ecosystems internalize economics and protect customer relationships inside their own environments in the Singapore gift card market. Retailers and travel brands respond through cross-sector bundles such as Singapore Airlines and Takashimaya and Marina Bay Sands Resort Dollars to lock in spend early.

Security baselines such as 12-hour payee cooling periods and Money Lock changed onboarding and redemption patterns and require clear user education. SGQR+ commercialization across tens of thousands of points improves interoperability and extends acceptance into hawker segments without custom deployments. Apple’s Tap to Pay on iPhone expands acceptance for micro and home-based sellers and improves the long tail for digital gift-card usage. Tencent’s TenPay Global Checkout support for PayNow enables Chinese merchants and platforms to connect to local rails for mainland visitor flows. Competition therefore centers on catalog depth, fraud safeguards, and integration quality rather than raw footprint in the Singapore gift card market.

Singapore Gift Card And Incentive Card Industry Leaders

NTUC FairPrice Co-operative Pte Ltd

Dairy Farm International Holdings Ltd

Shen Siong Supermarket Pte Ltd

Takashimaya Co Ltd

Mustafa Holdings Pte Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: NTUC FairPrice and rival supermarkets launched return-voucher promotions targeting CDC Voucher recipients, offering up to SGD 8 in rebates for SGD 60 minimum spend, a tactical response to the government's SGD 300 per-household allocation that drove 10 percent voucher-to-voucher conversion rates and reinforced supermarket chains' dependence on government-subsidized redemption volume to sustain foot traffic.

- December 2025: Apple launched Tap to Pay on iPhone across Singapore, enabling micro-merchants to accept contactless gift-card payments without dedicated NETS terminals, potentially expanding redemption infrastructure to hawker stalls and home-based businesses currently excluded from formal acceptance networks due to hardware costs.

- November 2025: Tencent announced its TenPay Global Checkout service will launch in Singapore later in 2025, allowing Weixin Mini Program merchants to accept local payment methods including PayNow, positioning Chinese e-commerce platforms to capture gift-card redemption volume from Singapore's 2.13 million annual mainland Chinese tourist arrivals.

- September 2025: DBS, OCBC, and UOB banks introduced Money Lock feature at MAS directive, attracting over 400,000 customers who locked SGD 30 billion within weeks, a fraud-mitigation mechanism that inadvertently complicates instant gift-card fulfillment workflows because the 12-hour unlocking delay conflicts with same-day corporate incentive distribution expectations.

Singapore Gift Card And Incentive Card Market Report Scope

The study focuses on the industry participants and the players' partnerships, mergers, acquisitions, and collaborations taking place across the Gift Card and Incentive Card market. The study also sheds light on the technological developments around the Gift Card and Incentive Card Market. The study further sheds light on the regional dimensions across the Gift Card and Incentive Card Market landscape. The consistent changes across the Gift Card and Incentive Card Market in Singapore and the repercussions of the changes have been specifically included in the report. The Singapore Gift Card and Incentive Card Market are Segmented By Product (E-Gift Card, Physical Card), By Consumer (Individual, Corporate), By Distribution Channel (Online, Offline).

By Card Type

| Open-Loop Card |

| Closed-Loop Card |

By Format Type

| Digital Card |

| Physical Card |

By Consumer Type

| Individual (B2C) |

| Corporate (B2B) |

By Distribution Channel

| Online |

| Offline |

By Industry of Application

| Food and Beverages |

| Health, Wellness, and Beauty |

| Apparel, Footwear, and Accessories |

| Consumer Electronics |

| Other Industries |

| By Card Type | Open-Loop Card |

| Closed-Loop Card | |

| By Format Type | Digital Card |

| Physical Card | |

| By Consumer Type | Individual (B2C) |

| Corporate (B2B) | |

| By Distribution Channel | Online |

| Offline | |

| By Industry of Application | Food and Beverages |

| Health, Wellness, and Beauty | |

| Apparel, Footwear, and Accessories | |

| Consumer Electronics | |

| Other Industries |

Key Questions Answered in the Report

What is the current size and projected growth of the Singapore gift card market?

The Singapore gift card market size is USD 49.24 billion in 2026 and is projected to reach USD 70.52 billion by 2031 at a 7.45% CAGR.

Which segments lead by share and which grow the fastest in Singapore?

Closed-loop cards lead by share at 63.50% and physical cards hold 56.80%, while open-loop cards, digital formats, corporate buyers, online channels, and consumer electronics record the fastest CAGRs through 2031.

How are government vouchers shaping Singapore's gift card demand?

SG60 and CDC vouchers scaled QR redemption across heartland merchants and supermarkets, lowering acquisition costs for private issuers and sustaining high-frequency use in daily essentials.

What role does tourism play in Singapore's gift card dynamics?

Tourism recovery to 16.5 million arrivals and SGD 29.8 billion in receipts has encouraged hotels and retailers to bundle gift credits to capture visitor spending across dining, attractions, and retail.

How is B2B gifting evolving among employers in Singapore?

Employers use gift cards for rewards and retention with a 10.23% CAGR outlook for corporate programs, supported by API fulfillment and GST-aware budget design under the SGD 200 threshold.

What risks could slow adoption of gift cards in Singapore?

Fraud and phishing have prompted 12-hour cooling-off periods and Money Lock measures, while GST compliance for gifts above SGD 200 adds administrative complexity for corporate issuers.

Page last updated on: