Asia-Pacific Pharmaceutical PET Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

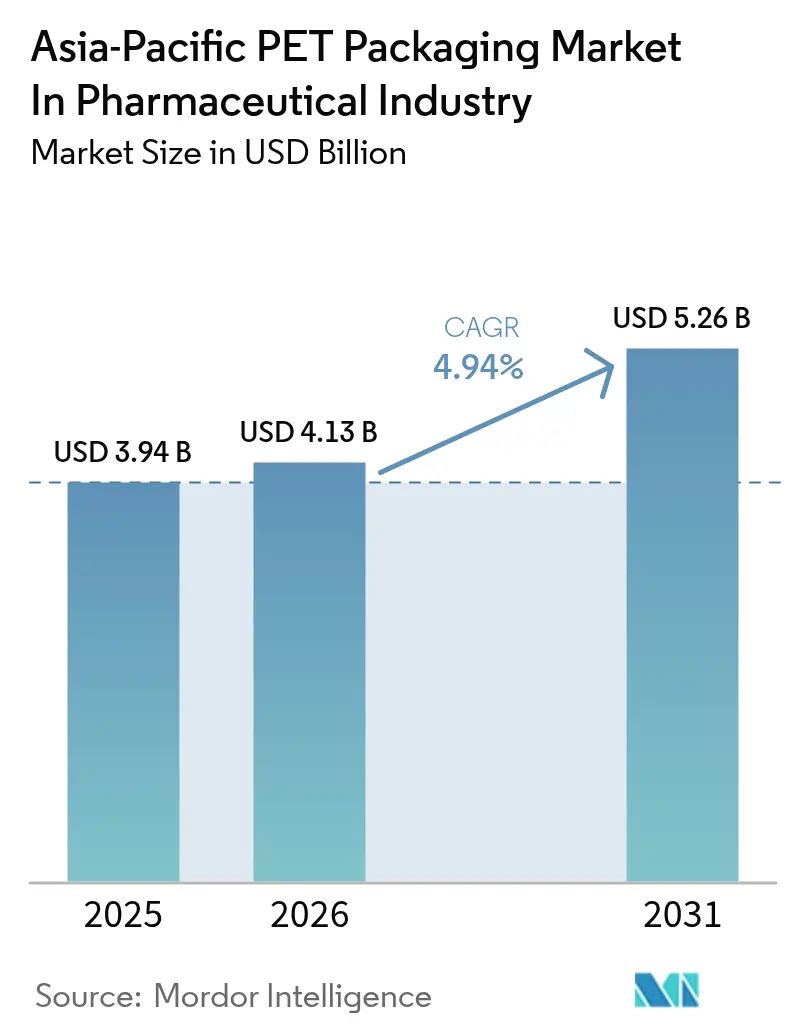

| Base Year Market Size (2025) | USD 3.94 Billion |

| Market Size (2026) | USD 4.13 Billion |

| Market Size (2031) | USD 5.26 Billion |

| Growth Rate (2026 - 2031) | 4.94% CAGR |

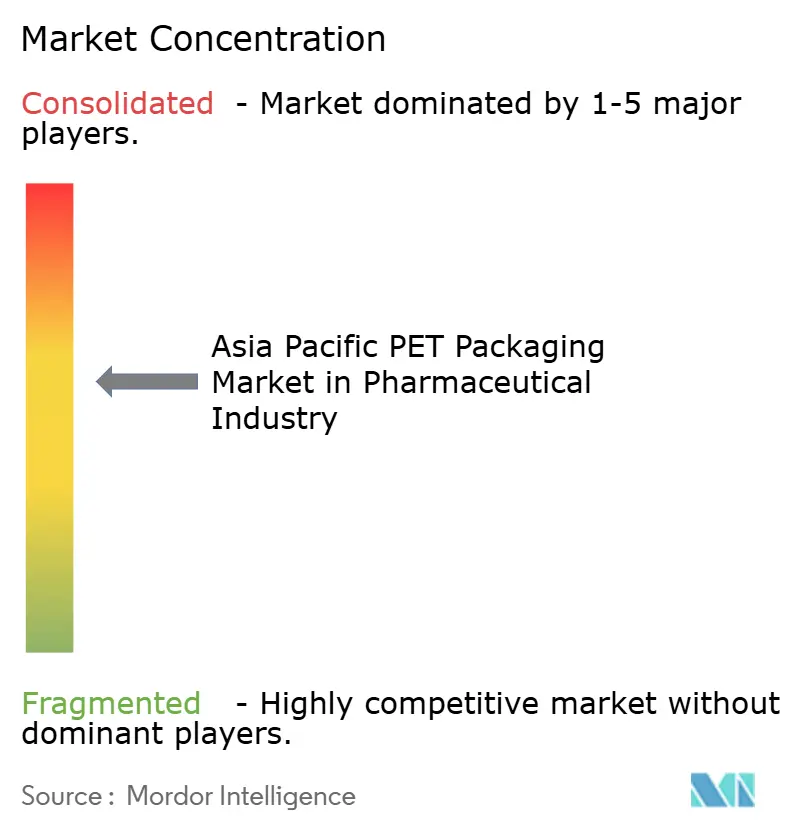

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Pharmaceutical PET Packaging Market Analysis by Mordor Intelligence

The Asia-Pacific PET packaging market size in the pharmaceutical sector market size in 2026 is estimated at USD 4.13 billion, growing from 2025 value of USD 3.94 billion with 2031 projections showing USD 5.26 billion, growing at 4.94% CAGR over 2026-2031. Growth is tied to a decisive shift from glass to lightweight polyethylene terephthalate containers, regional dominance in active pharmaceutical ingredient manufacturing, and resilient supply chains that shorten lead times. Widening generic-drug coverage in India, expansion of contract manufacturing hubs across Vietnam and Thailand, and sustained investments in tamper-evident formats for fast-growing online pharmacy channels are all reinforcing demand. Feedstock pricing swings and pending extended producer responsibility rules in China, Japan, and South Korea inject cost uncertainty, yet they simultaneously accelerate vertical integration as pharmaceutical companies acquire stakes in recycling facilities to secure food-grade rPET. Competitive intensity remains moderate, with the top five converters accounting for roughly 35% of the installed capacity, leaving room for regional specialists to focus on small-run vials, dropper bottles, and custom tints.

Key Report Takeaways

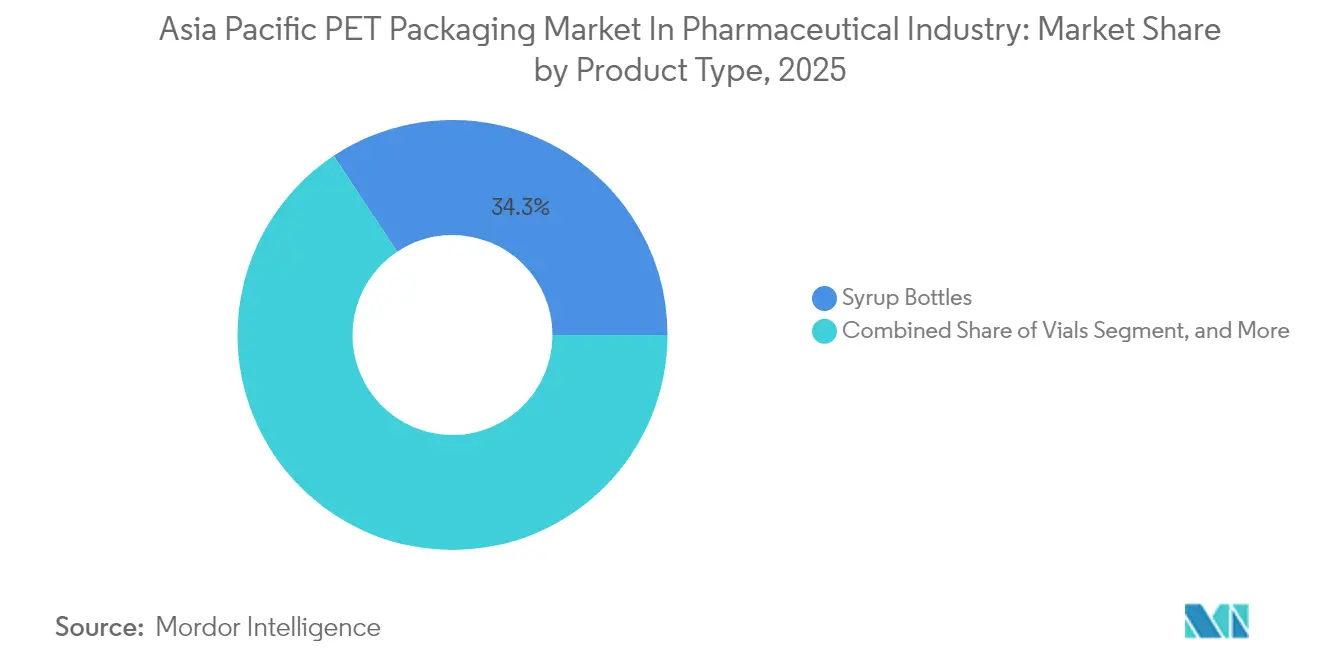

- By product type, syrup bottles led with a 34.32% of the Asia-Pacific PET packaging market share in 2025, while vials posted the fastest growth rate of 6.12% through 2031.

- By color, amber bottles captured 45.98% of the Asia-Pacific PET packaging market share in 2025, whereas transparent variants are expanding at a 6.56% CAGR.

- By capacity, the 101–250 milliliter range accounted for 37.12% of the Asia-Pacific PET packaging market share in 2025, and sub-50 milliliter formats are advancing at a 6.97% CAGR.

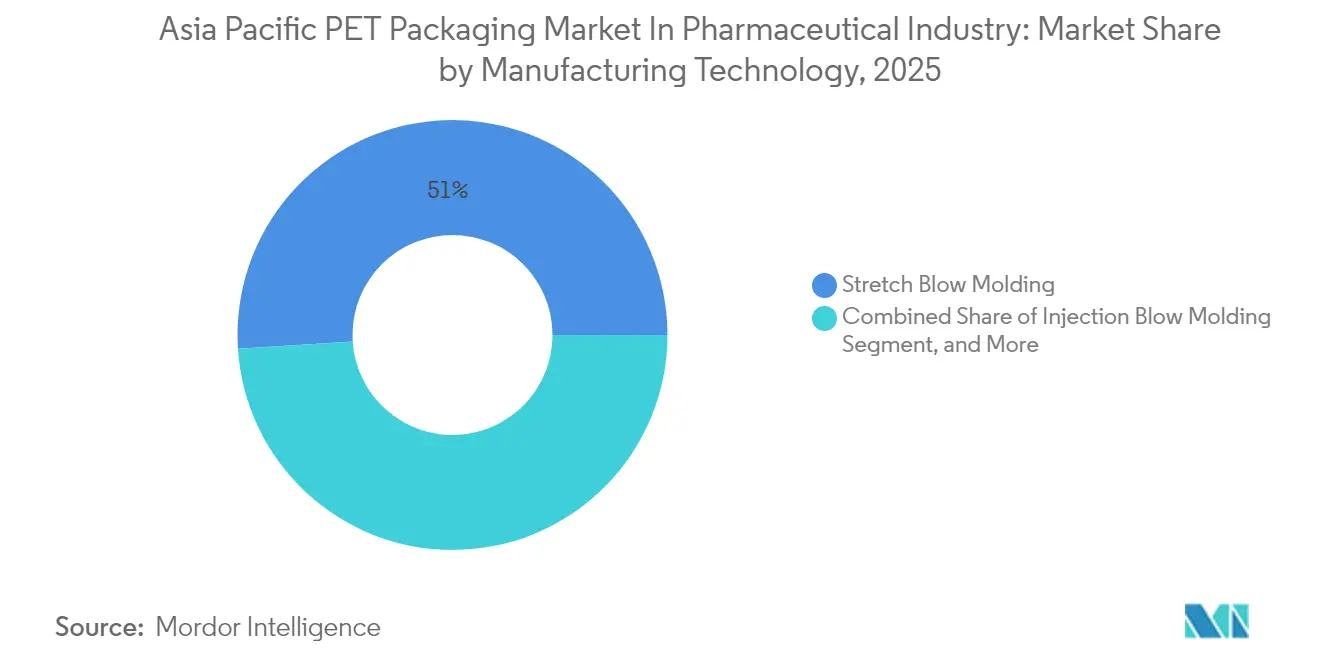

- By manufacturing technology, stretch blow molding accounted for 51.02% of the Asia-Pacific PET packaging market share in 2025; injection blow molding is gaining market share at a 7.35% CAGR.

- By end-user, pharmaceutical manufacturers accounted for 50.88% of the Asia-Pacific PET packaging market share in 2025, while contract manufacturing organizations are growing at a 6.88% CAGR.

- By country, China secured a 28.16% share of the Asia-Pacific PET packaging market in 2025, while India is projected to have the top regional CAGR of 7.86% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Pharmaceutical PET Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing pharmaceutical production and exports | +1.2% | China, India, Vietnam, Thailand | Medium term (2-4 years) |

| Shift toward lightweight durable packaging solutions | +0.9% | Global, strongest in China and India | Short term (≤ 2 years) |

| Cost efficiency and versatility of PET versus glass alternatives | +0.8% | Asia-Pacific core, spillover to Middle East | Medium term (2-4 years) |

| Surge in online pharmacy and cold chain logistics demanding tamper-evident PET bottles | +1.1% | Urban centers in China, India, Japan, South Korea | Short term (≤ 2 years) |

| Government-led healthcare access schemes expanding generic drug distribution | +0.7% | India, Indonesia, Philippines | Long term (≥ 4 years) |

| Adoption of recycled PET following circular-economy targets | +0.5% | Japan, South Korea, early adoption in China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Pharmaceutical Production and Exports in the Asia-Pacific

China and India supplied 62% of global generic-drug volumes in 2024, drawing secondary and tertiary packaging operations into bonded manufacturing zones that reward export-oriented output.[1]Reuters Staff, “Asia Pacific Pharmaceutical Production and Export Growth,” Reuters, reuters.com Vietnam’s 14% rise in pharmaceutical production and Thailand’s green-lit plants under Board of Investment incentives have each added on-site PET bottle blow-molding lines, slashing transit buffers and inventory costs. Multinational firms are increasingly co-locating filling and packaging near ingredient sites, which reduces lead times from weeks to days. This tight clustering, however, magnifies risk; an unplanned PTA outage in South Korea disrupted several Asian supply chains within 72 hours. Overall, elevated output sustains resin throughput, expands converter order books, and lifts the Asia-Pacific PET packaging market’s five-year growth outlook.

Shift Toward Lightweight Durable Packaging Solutions

Between 2020 and 2024, pharmaceutical companies cut bottle weight by 12% without losing drop-test integrity, thanks to refined preform stretch ratios and stronger neck finishes.[2]Bloomberg News, “Biologics Packaging Drives PET Vial Demand,” Bloomberg, bloomberg.com Freight-sensitive biologics shippers report that trimming 500 g per 1,000 bottles lowers air-cargo fees on lanes from India to sub-Saharan Africa by double-digit percentages. PET’s shatter resistance, evidenced by breakage rates below 0.3% versus 1.8% for glass during rural distribution, underpins its durability appeal. Regulatory bodies, such as Japan’s Ministry of Health, now permit thinner walls for non-sterile oral solids once barrier equivalence is proven, thereby broadening the design envelope. The durability plus lightweight combination lifts profitability, improves brand perception in over-the-counter aisles, and drives faster adoption across the Asia-Pacific PET packaging market.

Cost Efficiency and Versatility of PET Versus Glass Alternatives

Average 2024 PET resin pricing hovered at USD 1,250 per metric ton, while pharmaceutical-grade borosilicate glass cost USD 2,800, creating a 55% raw material gap. PET blow molding draws roughly 40% less electricity than glass annealing, thereby multiplying cost savings. Design flexibility enables the incorporation of child-resistant closures, tamper-evident bands, and embedded barcodes in a single pass, thereby avoiding the secondary operations inherent to glass.[3]Financial Times Reporters, “Contract Manufacturing Trends in Pharma Packaging,” Financial Times, ft.com Indian firms realized a 22% drop in packaging costs by switching 100 milliliters of cough syrup bottles from glass to PET, citing lower breakage, freight, and cullet disposal costs. Color customization further differentiates brands without requiring retooling of molds, a value that glass suppliers struggle to match. Collectively, these advantages solidify PET’s position as the preferred solution in the Asia-Pacific PET packaging market.

Surge in Online Pharmacy and Cold Chain Logistics Demanding Tamper-Evident PET Bottles

Asia-Pacific online pharmaceutical sales reached USD 38 billion in 2024, a 19% increase, and every parcel faces multiple handling points that raise the stakes for tamper and thermal integrity. Pharmaceutical firms willingly pay a 7% packaging premium for induction-sealed, tamper-banded PET bottles that assure consumers of authenticity. Cold chain capacity increased by 23% in 2024, driving demand for resin blends that resist stress cracking at sub-zero temperatures. India’s regulator has mandated tamper-evident closures on all e-commerce prescriptions, effectively cementing PET as the material of choice for online distribution channels. Converters able to meet both tamper-evidence and thermal cycling standards command 12-15% higher price points, reinforcing premiumization within the Asia-Pacific PET packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying regulatory scrutiny on plastic waste and single-use packaging | -0.6% | Japan, South Korea, urban China | Medium term (2-4 years) |

| Volatility in PET resin prices due to feedstock fluctuations | -0.4% | Asia-Pacific core, linked to crude oil markets | Short term (≤ 2 years) |

| Low heat resistance limiting PET usage for sterile injectable packaging | -0.3% | Global, most acute in biologics segment | Long term (≥ 4 years) |

| Consumer perception shift toward biodegradable polymers in OTC products | -0.2% | Japan, South Korea, affluent urban markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying Regulatory Scrutiny on Plastic Waste and Single-Use Packaging

Japan’s draft 2024 amendments require 30% recycled content in pharmaceutical PET bottles by 2028, with non-compliance triggering escalating disposal levies. South Korea imposes fines up to KRW 50 million (USD 37,500) on delinquent lines, pushing firms to lock long-term rPET supply contracts. China’s extended producer responsibility draft extends financial accountability to converters, fragmenting compliance regimes across the region. Food-grade rPET trades at a 34% premium over virgin resin, squeezing margins and narrowing PET’s cost advantage. Smaller pharmaceutical players with limited purchasing power may delay PET migration, thereby slowing the growth momentum of the Asia-Pacific PET packaging market.

Volatility in PET Resin Prices Due to Feedstock Fluctuations

Purified terephthalic acid fluctuated between USD 820 and USD 1,050 per metric ton in 2024, driven by crude swings and refinery outages, while monoethylene glycol showed similar volatility. Generic drug makers, whose packaging cost share hovers around 10%, experienced a 200-300 basis-point margin erosion when resin prices surged. Index-linked contracts are emerging, yet smaller buyers remain exposed to spot spikes. The resulting capex hesitation in new PET lines leads to a start-stop pattern that chills innovation cycles and drags on Asia-Pacific PET packaging market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Demand Concentrates on Syrup Bottles as Vials Accelerate

The syrup-bottle segment accounted for 34.32% of 2025 sales, anchoring the Asia-Pacific PET packaging market share for oral liquids that demand wide mouths, calibrated caps, and ultraviolet protection. This dominance reflects robust pediatric cough and multivitamin volumes, especially in China and Indonesia, where government formularies favor bulk liquid prescriptions. Despite its lead, syrup bottle uptake is moderating as converters reach high line-speed ceilings while generics pivot to unit-dose regimens.

Vials, although a smaller slice, are rising at a 6.12% CAGR, aligned with biologics pipelines and biosimilar launches, which require precision containers of 10–30 milliliters. Injection blow molding’s ±0.05 millimeter neck-finish accuracy supports syringe compatibility and sterility, giving vials a premium price position within the Asia-Pacific PET packaging market. Tablet and dropper bottles offer steady but slower growth, while pandemic-fueled hand sanitizer formats have normalized at above-2019 baselines, supplying niche converters specializing in mold change agility.

By Color: Amber Retains Lead While Transparent Gains Regulatory Tailwinds

Amber bottles secured 45.98% of 2025 revenue, thanks to their superior UV shielding, which is vital for photosensitive antibiotics and vitamin blends. This share embodies decades of pharmacopeial specifications that list amber as the default. Transparent bottles, advancing at a 6.56% CAGR, are driven by mandatory serialization in China and India, which favors clear sidewalls for high-contrast barcode scans. Pharmaceutical lines equipped with machine-vision inspection achieve 6–8% higher throughput with clear bottles, incentivizing changeovers despite the need for UV-stabilizing excipients.

The Asia-Pacific PET packaging market size for transparent formats is also boosted by consumer confidence in e-commerce channels that value visible fill levels. Regulatory guidance in Japan further legitimizes clear packaging for non-photosensitive drugs, accelerating migration. Specialty hues, although niche, fetch double-digit price premiums, allowing brands to differentiate OTC variants without incurring extensive marketing costs.

By Capacity: Sub-50 Milliliter Formats Race Ahead

Containers of 101–250 milliliters captured 37.12% of 2025 volumes, underscoring their role in standard syrup and antacid packs served through retail pharmacies. Larger formats above 250 milliliters are supplied to hospitals, but grow slowly due to higher breakage insurance costs and sterile-dispense system obligations.

Sub-50 milliliter bottles, propelled by adherence-friendly single-dose antibiotics and trial sizes for e-commerce, are scaling at a 6.97% CAGR. The Asia-Pacific PET packaging market size attached to this micro-format reflects its alignment with personalized medicine protocols that minimize waste and enhance dosage compliance. Injection blow molding dominates production here, achieving precise neck finishes for dropper or child-resistant closures, while converters chase thinner preform walls to offset resin premiums.

By Manufacturing Technology: Stretch Blow Versus Injection Blow

Stretch blow molding retained a 51.02% market share in 2025, driven by sub-8-second cycle commodity bottle lines that underpin cost leadership. Its stronghold lies in high-clarity transparent bottles that satisfy serialization rules at scale. Conversely, injection blow molding, now growing at 7.35% annually, excels in precision containers such as vials and ophthalmic droppers, where dimensional tolerances dictate closure integrity.

Capital outlay for stretch blow plants ranges from USD 800,000 to USD 1.2 million, which is double the need for double injection blow, so converters often dual-track their capacity decisions. Extrusion blow molding supplies large handles or grip features for bulk packs, while co-injection is slowly emerging as a solution for multilayer oxygen barriers. The Asia-Pacific PET packaging market continues to bifurcate, prompting converters to fine-tune their asset portfolios around volume versus precision trade-offs.

By End-Users: Contract Manufacturing Organizations Command Momentum

Pharmaceutical manufacturers generated 50.88% of 2025 demand, reflecting legacy in-house packaging lines that guarantee proprietary mold control and IP security. Yet, contract manufacturing organizations (CMOs) are rising 6.88% per year due to the back-shoring of filling and packaging to India and Vietnam, where labor and compliance costs remain competitive. CMOs aggregate volumes across clients, negotiating 8-12% resin discounts, and insist on ISO 15378 certification as gateway criteria, steadily shaping supplier rosters within the Asia-Pacific PET packaging market.

Other end-users, including compounding pharmacies and nutraceutical brands, maintain low-single-digit contributions but deliver healthy gross margins for converters that can accommodate frequent mold changes. Overall, the end-user mix indicates a shift toward ecosystem players able to standardize bottle families, embed track-and-trace features, and manage recycled-content compliance across multiple export destinations.

Geography Analysis

China accounted for 28.16% of regional revenue in 2025, supported by vertically integrated conglomerates that house ingredient synthesis and bottle molding under one roof, compressing order cycles from six weeks to ten days. The National Medical Products Administration's guidance now permits thinner PET walls for non-sterile oral solids, unlocking resin savings that encourage wider substitution of glass. However, looming extended producer responsibility rules may levy disposal fees on virgin-only packaging, nudging converters toward in-house recycling partnerships.

India is advancing at an 7.86% CAGR, the fastest within the Asia-Pacific PET packaging market, driven by universal healthcare schemes distributing generics through more than 10,000 Janaushadhi stores, which standardize 100-milliliter syrup and 30-milliliter dropper bottles. The Drugs Controller General’s 2024 recycled-content guidelines further favor large converters capable of validated rPET traceability, subtly consolidating market share. Rapid e-pharmacy uptake also increases tamper-evident demand, prompting the establishment of new stretch blow molding lines in areas such as Bengaluru and Ahmedabad.

Japan exhibits modest mid-single-digit value growth, while sustaining premium unit margins due to stringent child-resistant and tamper-evident packaging mandates. The Pharmaceuticals and Medical Devices Agency’s recommendation for transparent bottles on non-photosensitive drugs has sparked pilot projects among the top ten domestic labs, positioning transparency as a differentiator despite higher UV-shield formulation costs. South Korea benefits from its biologics contract-manufacturing base, which services the United States and European pipelines, spawning ISO 15378-certified PET lines near Incheon to meet vial demand for cold chain exports.

The rest of the Asia-Pacific, including Vietnam, Thailand, Indonesia, and the Philippines, collectively contribute an expanding slice, supported by double-digit hikes in healthcare budgets and the installation of greenfield CMO plants with integrated PET blow molding to reduce freight spend. Vietnam’s 14% output jump in 2024 confirms supply-chain diversification away from China, while Thailand’s Board of Investment approval of 11 pharmaceutical projects last year embeds captive packaging capacity at inception. Indonesia’s archipelagic logistics challenges elevate shatter-resistant PET over glass for rural distribution, cementing PET’s early mover advantage. The Philippines helps round out regional momentum by courting Southeast Asian generic exports, thereby amplifying order flow to converters in Luzon's economic zones.

Competitive Landscape

The Asia-Pacific PET packaging market exhibits a moderate concentration, with the top five converters accounting for approximately 35% of the capacity, resulting in intense but not monopolistic rivalry. Large incumbents, such as Gerresheimer, extended 2024 investments into India and China to align with CMO capacity additions and serialization mandates, including a EUR 45 million Pune expansion equipped with automated inspection lines. Technology adoption differentiates leaders: investments in injection blow molding and in-mold labeling deliver ±0.05 millimeter neck precision, removing secondary labeling steps and cutting unit costs by up to 8%.

Regionally specialized players thrive by offering rapid prototyping on 12-cavity experimental tools, enabling new drug launches in under eight weeks. Recycled-content capability is a growing competitive battleground, with Indian pharmaceutical firms now holding minority stakes in recyclers to ensure food-grade rPET feedstock and protect against volatility in virgin resin. Patent filings in Japan emphasize barrier-coating recipes that extend biologic shelf life, signaling upcoming product tiers that justify higher ASPs. Dual compliance with ISO 15378 and the Global Recycled Standard currently sits at just 12% of suppliers, granting certified firms a clear pricing and negotiation edge.

Emerging disruptors include Chinese recyclers vertically integrating into bottle production, wielding feedstock control to win three-year supply contracts at sub-benchmark resin prices. Meanwhile, Southeast Asian converters collaborate with local governments to co-finance recycling infrastructure, ensuring future regulatory alignment. Overall, sustained capex in precision equipment, recycled-content validation, and smart packaging features defines the path to above-market growth.

Asia-Pacific Pharmaceutical PET Packaging Industry Leaders

Gerresheimer AG

Alpha Packaging Holdings Inc.

Takemoto Packaging Inc.

TPAC Packaging India Private Limited

Dongguan Fukang Plastic Products Co. Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Alpha Packaging Holdings Inc. committed USD 28 million to build a pharmaceutical-grade PET bottle plant in Bangalore, India, equipped with injection blow molding lines that can produce 80 million vials per year for biosimilar contract manufacturers; the site targets ISO 15378 certification by Q2 2026 and will include recycled-content resin to fulfill India’s extended-producer-responsibility rules.

- July 2025: Gerresheimer AG signed a strategic pact with a Chinese pharmaceutical manufacturer to supply tamper-evident PET bottles for an expanded generic portfolio aimed at Southeast Asian exports; the multi-year deal, valued at EUR 35 million (USD 38 million), covers technology transfer for serialization-ready designs and co-located blow-molding lines at the partner’s Jiangsu facilities.

- May 2025: TPAC Packaging India Private Limited secured Central Drugs Standard Control Organisation approval to deliver PET bottles containing 25% recycled content for non-sterile oral solids, becoming one of India’s first converters certified to help drug makers meet national plastic-waste mandates without raising unit costs.

- March 2025: Takemoto Packaging Inc. introduced sub-30-milliliter PET vials tailored for lyophilized biologics, featuring multi-layer preforms that heighten moisture-barrier performance; initial output of 50 million units per year will flow from the company’s Osaka plant to Japanese biosimilar producers serving domestic and export channels.

Asia-Pacific Pharmaceutical PET Packaging Market Report Scope

The Asia-Pacific PET Packaging Market in the Pharmaceutical Sector refers to the market for polyethylene terephthalate (PET) packaging solutions specifically designed for pharmaceutical applications. PET packaging is widely used in the pharmaceutical sector due to its lightweight, durability, and ability to maintain the integrity of the contents.

The Asia-Pacific PET Packaging Market in Pharmaceutical Sector Report is Segmented by Product Type (Tablet Bottles, Syrup Bottles, Vials, Dropper Bottles, Handwash and Hand Sanitizer Bottles, Mouthwash Bottles, Other Product Types), Color (Transparent, Amber, Other Colors), Capacity (Below 50 mL, 51-100 mL, 101-250 mL, Above 250 mL), Manufacturing Technology (Stretch Blow Molding, Injection Blow Molding, Extrusion Blow Molding, Other Technologies), End-users (Pharmaceutical Manufacturers, Contract Manufacturing Organizations, Other End-users), and Country (China, India, Japan, South Korea, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Tablet Bottles |

| Syrup Bottles |

| Vials |

| Dropper Bottles |

| Handwash and Hand Sanitizer Bottles |

| Mouthwash Bottles |

| Other Product Types |

| Transparent |

| Amber |

| Other Colors |

| Below 50 mL |

| 51 mL-100 mL |

| 101 mL-250 mL |

| Above 250 mL |

| Stretch Blow Molding |

| Injection Blow Molding |

| Extrusion Blow Molding |

| Other Manufacturing Technologies |

| Pharmaceutical Manufacturers |

| Contract Manufacturing Organizations |

| Other End-users |

| China |

| India |

| Japan |

| South Korea |

| Rest of Asia-Pacific |

| By Product Type | Tablet Bottles |

| Syrup Bottles | |

| Vials | |

| Dropper Bottles | |

| Handwash and Hand Sanitizer Bottles | |

| Mouthwash Bottles | |

| Other Product Types | |

| By Color | Transparent |

| Amber | |

| Other Colors | |

| By Capacity | Below 50 mL |

| 51 mL-100 mL | |

| 101 mL-250 mL | |

| Above 250 mL | |

| By Manufacturing Technology | Stretch Blow Molding |

| Injection Blow Molding | |

| Extrusion Blow Molding | |

| Other Manufacturing Technologies | |

| By End-users | Pharmaceutical Manufacturers |

| Contract Manufacturing Organizations | |

| Other End-users | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific PET packaging market in pharma in 2026?

The Asia Pacific PET packaging market size in pharmaceuticals reached USD 4.13 billion in 2026 and is projected to climb to USD 5.26 billion by 2031.

What is driving the fastest growth segment in product types?

Vials are growing at a 6.12% CAGR as biologics and biosimilars expand, demanding precise, moisture-barrier containers.

Which country is expected to post the highest growth through 2031?

India is forecast to lead with an 7.86% CAGR thanks to universal health programs and a strong generic-drug network.

How are regulatory changes affecting PET usage?

New recycled-content mandates in Japan, South Korea, and China compel converters to secure food-grade rPET, raising compliance complexity and costs.

What technology shift is notable among converters?

Injection blow molding adoption is accelerating because it offers ±0.05 millimeter precision essential for small-format vials and droppers.

How fragmented is the supplier landscape?

The top five converters account for about 35% capacity, reflecting moderate concentration and opportunities for niche specialists.

Page last updated on: