Asia Pacific Pharmaceutical Glass Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

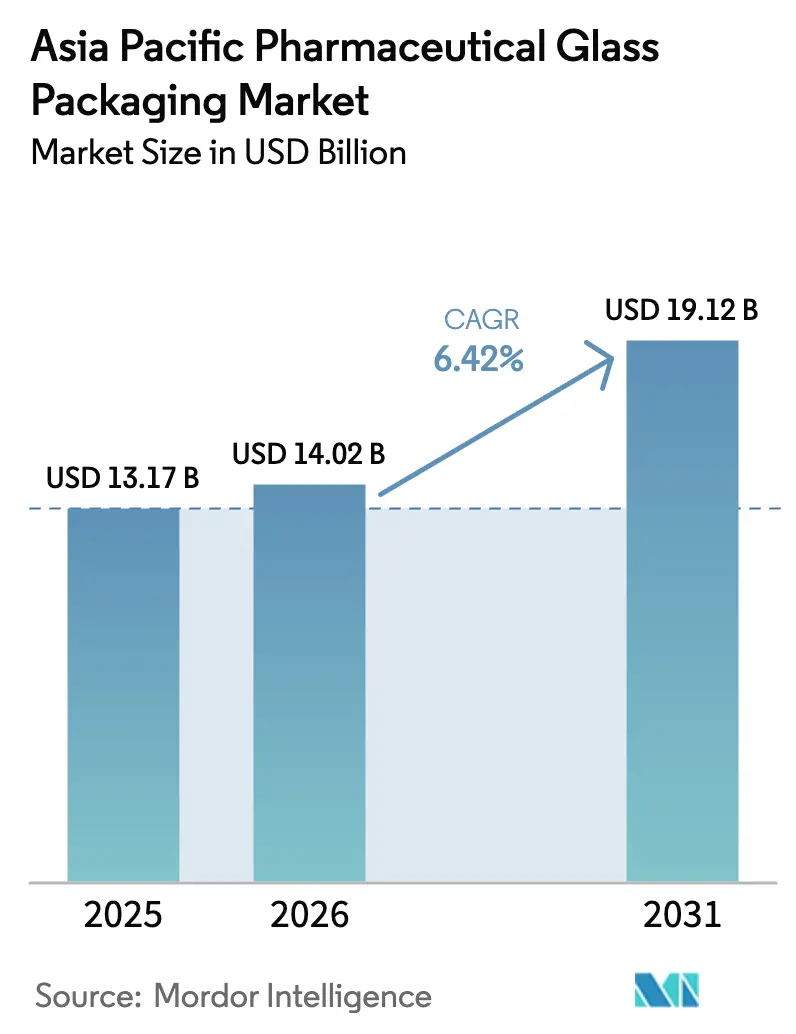

| Base Year Market Size (2025) | USD 13.17 Billion |

| Market Size (2026) | USD 14.02 Billion |

| Market Size (2031) | USD 19.12 Billion |

| Growth Rate (2026 - 2031) | 6.42% CAGR |

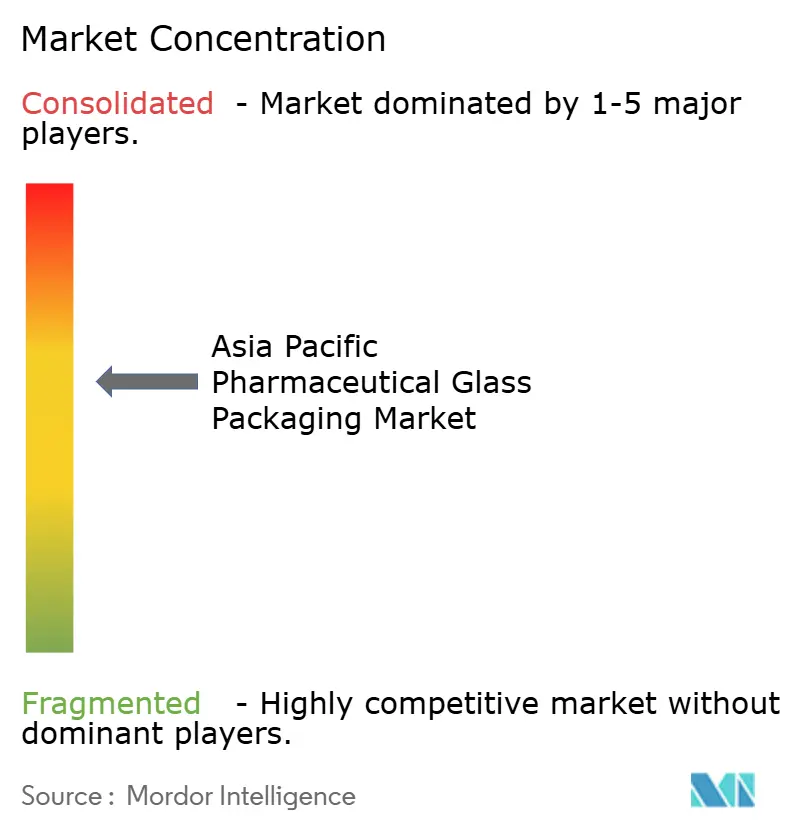

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Pharmaceutical Glass Packaging Market Analysis by Mordor Intelligence

The Asia Pacific pharmaceutical glass packaging market size is expected to grow from USD 13.17 billion in 2025 to USD 14.02 billion in 2026 and is forecast to reach USD 19.12 billion by 2031 at 6.42% CAGR over 2026-2031. Rising biologics output, rapid vaccine scale-up, and a regional shift toward self-administered injectable therapies underpin demand for premium primary containers. Capacity expansions by contract development and manufacturing organizations (CDMOs) in China and India shorten supply chains and raise local content thresholds, further lifting the Asia Pacific pharmaceutical glass packaging market. Sustainability commitments add momentum, as infinitely recyclable glass is increasingly preferred over plastics in regulated drug applications. Competitive strategies focus on ready-to-use (RTU) vials and cartridges that cut changeover times and support high-speed fill-finish lines, while innovations such as low-friction “velocity vials” capture share in mRNA vaccine programs.

Key Report Takeaways

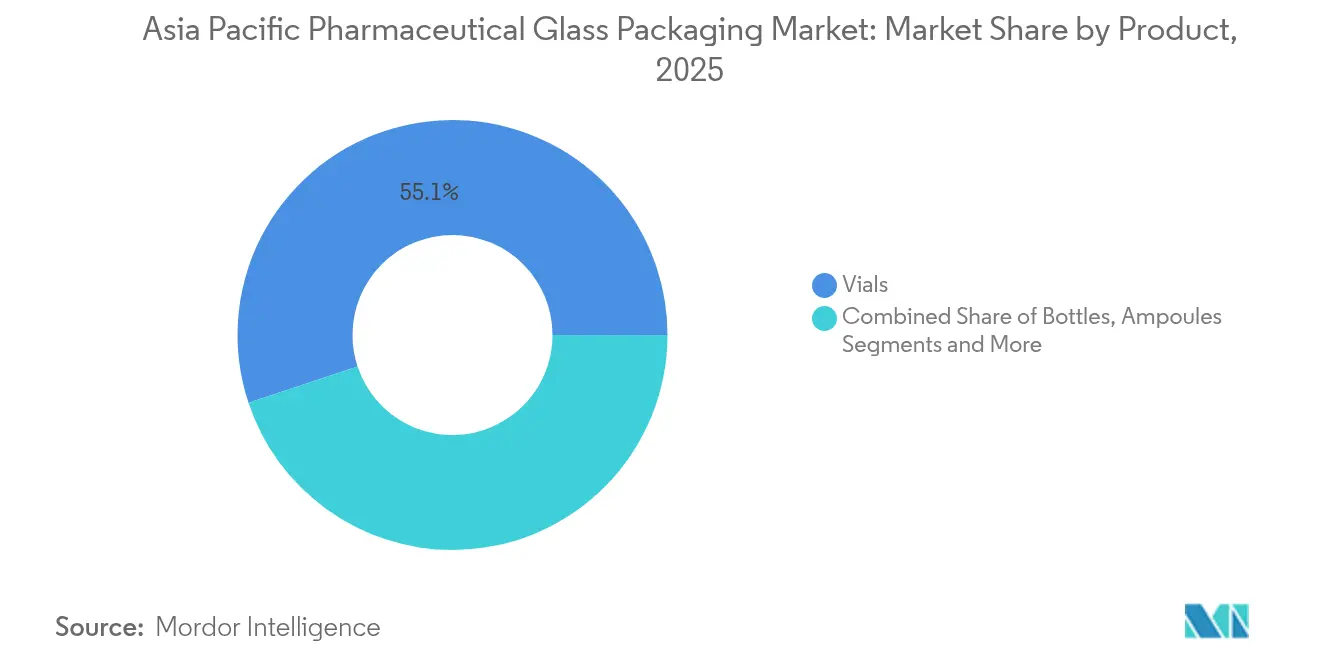

- By product, vials led with 55.10% revenue share of the Asia Pacific pharmaceutical glass packaging market in 2025; cartridges and prefillable syringes are forecast to grow at a 7.6% CAGR through 2031.

- By glass type, Type I borosilicate held 61.50% of the Asia Pacific pharmaceutical glass packaging market share in 2025, whereas Type III glass is poised to expand at an 7.9% CAGR to 2031.

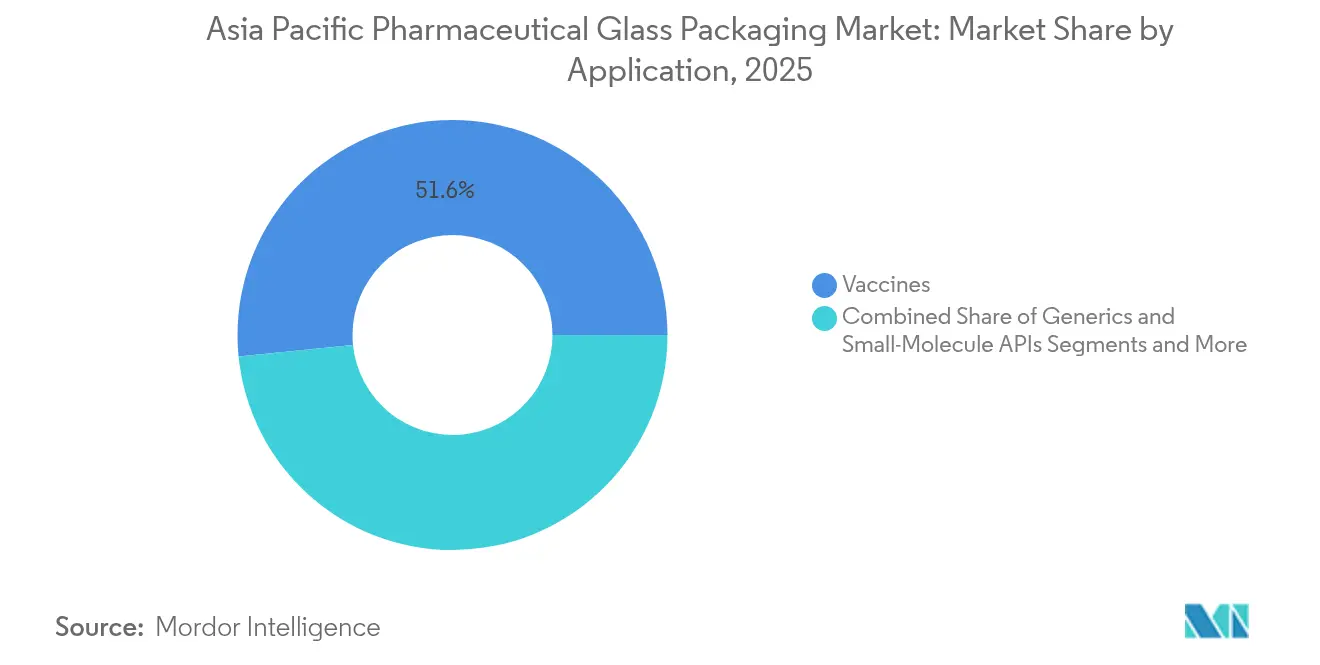

- By application, vaccines accounted for 51.60% share of the Asia Pacific pharmaceutical glass packaging market size in 2025; generics and small-molecule APIs are expected to rise at a 7.25% CAGR over the same horizon.

- By end-user, branded pharmaceutical companies commanded 57.00% share in 2025, while biotechnology firms show the fastest growth at a 6.85% CAGR.

- By country, China dominated with 44.00% share in 2025; India records the highest projected CAGR at 6.6% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Pharmaceutical Glass Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| R&D spending surge in biologics and vaccine fill-finish lines | +1.2% | China, India, South Korea | Medium term (2-4 years) |

| Sustainability push favouring infinitely recyclable glass | +0.8% | Global, with early adoption in Japan, Australia | Long term (≥ 4 years) |

| Local CDMO capacity expansions across China and India | +1.5% | China, India | Short term (≤ 2 years) |

| Rapid scale-up of mRNA "velocity vials" | +0.7% | APAC core, spill-over to Southeast Asia | Medium term (2-4 years) |

| Zero-defect GMP audits accelerating switch to Type I+ borosilicate | +0.9% | Global, with focus on export-oriented facilities | Medium term (2-4 years) |

| Cold-chain biologics need low-alkali glass for deep-freeze logistics | +0.6% | China, Japan, South Korea | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

R&D Spending Surge in Biologics and Vaccine Fill-Finish Lines

Escalating biologics pipelines and the continual build-out of pandemic-ready vaccine lines are resetting quality expectations in the Asia Pacific pharmaceutical glass packaging market. SCHOTT committed capacity equal to 2 billion vaccine doses, signalling the high-volume environment in which Type I borosilicate remains indispensable. Specialized formulations resist delamination and ensure protein stability under cold-chain conditions that often reach –80 °C. CDMOs in India and China have aligned investments in high-speed filling suites with zero-defect audit philosophies, concentrating purchasing power among suppliers that can prove sub-ppm particle counts. These stringent thresholds narrow acceptable supply options, reinforcing incumbency advantages for firms able to certify global GMP compliance. Elevated biologics funding therefore delivers both volume and margin growth opportunities to the Asia Pacific pharmaceutical glass packaging market.

Sustainability Push Favouring Infinitely Recyclable Glass

Corporate net-zero roadmaps and evolving legislation in Australia and Japan mandate higher recycled-content thresholds, bolstering glass demand as plastics face recycling-rate scrutiny. SGD Pharma launched primary containers containing 20% post-consumer recycled cullet without compromising pharmacopeia compliance. Electric furnaces and heat-recovery loops now feature in greenfield projects, trimming Scope 1 emissions while preserving melt consistency. Early-mover glass producers secure long-term contracts by offering transparent lifecycle assessments, positioning sustainability as a commercial differentiator instead of a cost burden. The Asia Pacific pharmaceutical glass packaging market thus benefits from policy alignment that simultaneously limits polymer substitution and rewards circular manufacturing practices.

Local CDMO Capacity Expansions Across China and India

Geopolitical risk mitigation and the United States Biosecure Act accelerate the on-shoring of drug substance and fill-finish capabilities to vetted partners in India and China. SK pharmteco’s USD 260 million plant in Sejong exemplifies the region’s surge in advanced small-molecule and peptide output. Proximity sourcing slashes container lead times, prompting CDMOs to embed glass converters within multi-year framework agreements. In parallel, domestic regulators tighten quality standards, driving upgrades from legacy Type III containers to Type I. These factors collectively elevate base demand and shift the customer mix toward globally accredited sites, broadening the Asia Pacific pharmaceutical glass packaging market footprint.

Rapid Scale-Up of mRNA “Velocity Vials”

Faster cycle times are critical for next-generation vaccines that face surge procurement scenarios. Corning’s Velocity technology reduces friction on high-speed lines, cutting jams and cosmetic rejects by up to 50% while preserving sterility[1]Corning Incorporated, “Velocity Vial Technology Overview,” corning.com . A Corning–SGD joint venture in India will localize supply, ensuring price accessibility for emerging-market immunization campaigns. Because line-rate uplifts translate into fewer filling suites and lower capex per dose, conversion economics justify the premium paid for advanced coatings. The Asia Pacific pharmaceutical glass packaging market therefore records incremental revenue streams from value-added vial formats that mesh with mRNA platform scale-up strategies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from cyclic-olefin polymer syringes and HDPE bottles | -0.9% | Global, with particular impact in cost-sensitive segments | Medium term (2-4 years) |

| Volatile energy and soda-ash costs inflating furnace OPEX | -1.1% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Port disruptions choking high-purity quartz-sand imports | -0.7% | APAC core, with spillover to global supply chains | Short term (≤ 2 years) |

| Long validation timelines for lightweight molded glass formats | -0.5% | Global, with focus on regulated markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Competition from Cyclic-Olefin Polymer Syringes and HDPE Bottles

Advanced polymer systems such as cyclic-olefin polymer syringes enjoy inertia-free plunger travel and shatter resistance, encroaching on glass share in auto-injectors and home-care kits. TOPAS materials now meet USP 661.1, reducing regulatory hesitation for biologic fills. However, extraction risk and permeability to certain gases still steer high-value oncology and vaccine products toward glass. Hybrid multilayer designs such as Mitsubishi Gas Chemical’s OXYCAPT blur boundaries but require lengthy validation, moderating uptake. The Asia Pacific pharmaceutical glass packaging market thus sees selective displacement rather than wholesale substitution, limiting the magnitude of the restraint.

Volatile Energy and Soda-Ash Costs Inflating Furnace OPEX

Natural-gas prices and soda-ash feedstock swings pressure margins, particularly for mid-tier regional furnaces without hedging programs. Spot soda-ash softness in late-2024 masked structural tightness, as long-range demand is forecast to grow from 66 million t to 83 million t by 2030. Forward-priced supply contracts and electric-boosted melters mitigate volatility yet demand capital outlays that favor large producers. Unexpected shocks to high-purity quartz sand flow—such as Hurricane Helene’s hit on the Spruce Pine mining cluster—underscore exposure to concentrated raw-material supply. Cost pass-through clauses cushion revenue but cannot fully offset cash-flow stress, slightly tempering the Asia Pacific pharmaceutical glass packaging market growth profile.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Vials Anchor Revenue While Syringes Accelerate

Vials generated 55.10% of Asia Pacific pharmaceutical glass packaging market revenue in 2025, buoyed by universal compatibility with parenteral drugs, straightforward line integration, and established regulatory dossiers. Cartridges and prefillable syringes, although holding smaller base volumes, are rising at a 7.6% CAGR as obesity, diabetes, and autoimmune therapies migrate to patient-managed pen injectors. The Asia Pacific pharmaceutical glass packaging market size for cartridges is expected to grow from an estimated USD 2.28 billion in 2025 to almost USD 3.58 billion by 2031. Ready-to-use configurations reduce washing and depyrogenation steps, facilitating shorter changeovers and smaller batch economics suitable for orphan drugs. Bottles remain relevant for oral liquids and OTC cough formulations, but their flat trajectory reflects limited innovation. Ampoules persist in niche hospital settings where single-use sterility overrides handling drawbacks. Overall, value realization tilts toward high-margin RTU vials and syringes, reinforcing product-mix upgrades across the Asia Pacific pharmaceutical glass packaging market.

Continued preference for borosilicate containers stems from unmatched hydrolytic resistance critical to biologic stability, yet lightweight molded formats are gaining share in regional distribution where freight costs are sensitive. Alliance for RTU partners SCHOTT Pharma, Gerresheimer, and Stevanato Group now deliver harmonized nests and tubs, simplifying machine validation and making multisourcing feasible for pharma buyers. Downstream, CDMOs leverage modular fillers designed around 2R and 6R vial standards, underscoring vials’ entrenched status even as cartridges expand.

By Glass Type: Type I Holds Sway Amid Cost-Driven Type III Gains

Type I borosilicate retains leadership at 61.50% market share, anchored in biologics, vaccines, and oncologics where low alkali extraction and thermal shock resilience are mandatory. Premium variants such as Type I+ push cosmetic defect limits below 0.01 per million and enhance delamination resistance, satisfying zero-defect audit regimes in export-oriented plants. Type III’s 7.9% CAGR results from aggressive generic and OTC production, particularly in India where cost parity outweighs incremental leachable risk for oral liquids. The Asia Pacific pharmaceutical glass packaging market size for Type III containers is on track to reach USD 5.28 billion by 2031, reflecting formulary expansion and private-label growth.

Surface-treated Type II addresses acidic solutions at a price point between Type I and Type III, yet its share plateaus as users either trade up to pure borosilicate or down to soda-lime for non-parenterals. Furnace upgrades toward oxy-fuel or hybrid-electric firing enable tighter redox control that improves Type I clarity, marginally lifting yields and narrowing cost differentials with lower classes. As regulatory pathways tighten, especially for exported injectables, Type I’s incumbent position solidifies, assuring sustained dominance in the Asia Pacific pharmaceutical glass packaging market.

By Application: Vaccines Dominate While Generics Gather Pace

Immunization programs maintain 51.60% revenue share, upheld by multiyear contracts for COVID-19 boosters and national drive expansions in influenza, HPV, and respiratory syncytial virus. Multi-dose vials remain common in resource-constrained settings, yet single-dose formats gain traction where wastage control is paramount. Generics and small-molecule APIs advance at 7.25% CAGR, propelled by the patent cliffs of blockbuster therapies and biosimilar penetration that heighten cost focus. Oncology injectables demand stringent particulate thresholds and continue to justify Type I+ adoption. Consequently, the Asia Pacific pharmaceutical glass packaging market size for oncology uses is projected to cross USD 2.18 billion by 2031.

Biologics, including monoclonal antibodies and cell-based treatments, require deep-cold distribution and low-extractables glass, incentivizing container innovations such as coated plungers and laser-etched traceability codes. Nutraceuticals, though price sensitive, increasingly specify amber vials to counteract photo-oxidation in herbal extracts, modestly diversifying the application mix. These divergent needs sustain a broad container portfolio and secure long-term growth avenues within the Asia Pacific pharmaceutical glass packaging market.

By End-User: Branded Pharma Commands Volume, Biotech Drives Momentum

Branded pharmaceutical enterprises account for 57.00% of 2025 demand by virtue of legacy blockbuster pipelines and entrenched procurement frameworks. Their preference for multi-year sole-source agreements anchors baseline volume for the Asia Pacific pharmaceutical glass packaging market. Biotechnology start-ups and mid-caps post a 6.85% CAGR as venture funding flows into mRNA, gene therapy, and rare-disease assets. Agile biotech launches favor RTU nests that expedite clinical lot production and scale flexibly as trials progress.

Generic drug makers retain a cost-centric stance, catalyzing growth in Type III bottles and vials, especially across India and emerging Southeast Asian hubs. CDMOs act as ecosystem integrators, aggregating demand from virtual biopharma clients and standardizing container specifications to maximize filler utilization rates. Hospital compounding pharmacies require small-batch sterile packaging, stimulating take-up of modular isolators compatible with 50-unit RTU tub formats. As a result, supplier sales teams must navigate diverse buyer archetypes, reinforcing segmentation complexity inside the Asia Pacific pharmaceutical glass packaging industry.

Geography Analysis

China retains leadership with 44.00% of 2025 shipments, supported by an expansive domestic drug-manufacturing base and factory-gate pricing advantages stemming from vertical integration of tubing and conversion lines. Stringent environmental policy pushes plants toward oxy-fuel furnaces and waste-heat recovery, raising capex but aligning with global pharmaceutical sustainability audits. The government’s dual-circulation strategy sustains local demand even as foreign buyers diversify sourcing, anchoring core volumes for the Asia Pacific pharmaceutical glass packaging market.

India registers the fastest CAGR at 6.6% through 2031. Massive capex flows, including Corning’s Rs 1,500 crore borosilicate project in Hyderabad set for 2025 start-up, deepen local raw glass supply and curtail import dependency. The Production Linked Incentive scheme incentivizes domestic formulation plants, lifting adjacent primary-packaging requirements. Regulatory bodies extend transition windows for updated GMP rules, giving SMEs time to adopt higher-grade containers while maintaining market access. Together these factors elevate India’s share of the Asia Pacific pharmaceutical glass packaging market in the medium term.

Japan, South Korea, and Australia form a triad of mature yet technologically progressive markets. Japan’s fast-track approval reforms nurture advanced therapy medicinal products, triggering orders for ultra-clean RTU vials with traceable Data Matrix codes. South Korea’s pharmaceutical sales reached 24.31 trillion won in 2019 and continue to climb, boosted by SK pharmteco’s peptide expansion that embeds local glass demand. Australia leads on packaging regulation, mandating higher recycled-content thresholds that encourage suppliers to invest in cullet-handling systems and transparent audit trails. Southeast Asian nations collectively broaden the Asia Pacific pharmaceutical glass packaging market as they attract vaccine and biologic fill-finish investments under ASEAN mutual-recognition frameworks.

Competitive Landscape

The Asia Pacific pharmaceutical glass packaging market exhibits moderate concentration, with SCHOTT, Gerresheimer, Stevanato Group, and SGD Pharma holding technological leadership through proprietary tubing, coating, and RTU platforms. Their combined share sits near 45%, leaving space for agile regional players such as Shandong Pharmaceutical Glass to leverage proximity logistics and lower labor costs. To defend share, incumbents emphasize RTU alliances, zero-defect digital inspection, and supply-chain transparency that resonates with multinational pharma procurement rules[3]SCHOTT Pharma, “Alliance for RTU Launch Press Release,” schott.com .

Asian challengers scale through both greenfield furnaces and acquisitions. Sisecam’s USD 285 million soda-ash deal illustrates vertical-integration moves that secure raw-material certainty and price insulation. Corning’s localization of Velocity vials in India exemplifies technology transfer models that embed advanced know-how in cost-competitive geographies, narrowing historical capability gaps. Meanwhile, polymer-based container specialists encroach on niche high-performance spaces, prompting glass makers to pitch hybrid solutions or enhanced barrier coatings.

Strategic roadmaps now pair container supply with analytical support, offering drug-product compatibility testing and regulatory filing assistance. Automated vision controls feeding real-time SPC dashboards reduce batch-release cycle times, adding service value beyond the glass itself. Suppliers pursuing ESG credibility disclose cradle-to-gate emissions and deploy solar arrays on plant roofs, factors that increasingly count in tender evaluations. The evolving playbook indicates sustained but dynamic rivalry inside the Asia Pacific pharmaceutical glass packaging industry.

Asia Pacific Pharmaceutical Glass Packaging Industry Leaders

AGI glaspac - AGI Greenpac Limited

Schott AG

Becton, Dickinson, And Company

Gerresheimer AG

SGD S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stevanato Group posted record EUR 1,104 million (USD 1,294.81 million) revenue for FY 2024, citing 34% biologics contribution and ongoing capacity optimization.

- January 2025: China released guidelines covering 24 measures to overhaul drug and device regulation by 2027, targeting faster reviews and greater compliance.

- December 2024: SCHOTT Pharma recorded 12% revenue growth and a 27.8% EBITDA margin, driven by glass syringe expansion and RTU partnerships.

- September 2024: SK pharmteco announced a USD 260 million plant in Sejong, South Korea, adding eight production trains and a peptide R&D center.

Asia Pacific Pharmaceutical Glass Packaging Market Report Scope

Glass has long been the preferred material for producing secure packaging in the pharmaceutical industry. Its chemical stability and immobility properties make it an ideal material for packaging medicinal products, including solids, liquids, injectables, and reconstituted products.

The Asia-Pacific pharmaceutical glass packaging market is segmented by products (bottles, vials, ampoules, cartridges, syringes, and other products) and country (China, Japan, India, Australia and New Zealand, and Rest of Asia-Pacific). The market sizes and forecasts are provided in value (USD) for all the above segments.

| Bottles |

| Vials |

| Ampoules |

| Cartridges and Prefillable Syringes |

| Other Products |

| Type I |

| Type II |

| Type III |

| Type I+ |

| Vaccines |

| Oncology Drugs |

| Biologics and Biosimilars |

| Generics and Small-Molecule APIs |

| Nutraceuticals and OTCs |

| Branded Pharma Manufacturers |

| Generic Pharma Manufacturers |

| Contract Development and Manufacturing Organisations (CDMOs) |

| Biotechnology Firms |

| Hospital and Compounding Pharmacies |

| China |

| Japan |

| India |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Product | Bottles |

| Vials | |

| Ampoules | |

| Cartridges and Prefillable Syringes | |

| Other Products | |

| By Glass Type | Type I |

| Type II | |

| Type III | |

| Type I+ | |

| By Application | Vaccines |

| Oncology Drugs | |

| Biologics and Biosimilars | |

| Generics and Small-Molecule APIs | |

| Nutraceuticals and OTCs | |

| By End-user | Branded Pharma Manufacturers |

| Generic Pharma Manufacturers | |

| Contract Development and Manufacturing Organisations (CDMOs) | |

| Biotechnology Firms | |

| Hospital and Compounding Pharmacies | |

| By Country | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the current value of the Asia Pacific pharmaceutical glass packaging market?

The market is valued at USD 14.02 billion in 2026 and is forecast to reach USD 19.12 billion by 2031.

Which product segment generates the most revenue?

Vials lead with 55.10% revenue share, reflecting their versatility across vaccines, biologics, and small-molecule injectables.

Why is glass preferred over plastic in pharmaceutical packaging?

Glass offers superior chemical resistance, zero gas permeability, and compatibility with deep-cold storage, all critical for biologics and vaccines.

Which country is growing fastest in demand for pharmaceutical glass packaging?

India exhibits the highest projected CAGR at 6.6% through 2031, helped by outsourcing shifts and domestic capacity additions.

How are sustainability trends influencing the market?

Regulations mandating higher recycled content and corporate net-zero goals encourage the use of infinitely recyclable glass and drive investments in low-emission furnaces.

What technological advances are shaping the competitive landscape?

Ready-to-use containers, low-friction velocity vials, and digital zero-defect inspection systems are key innovations that enhance efficiency and product safety across the region.

Page last updated on: