Asia-Pacific Online Grocery Delivery Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

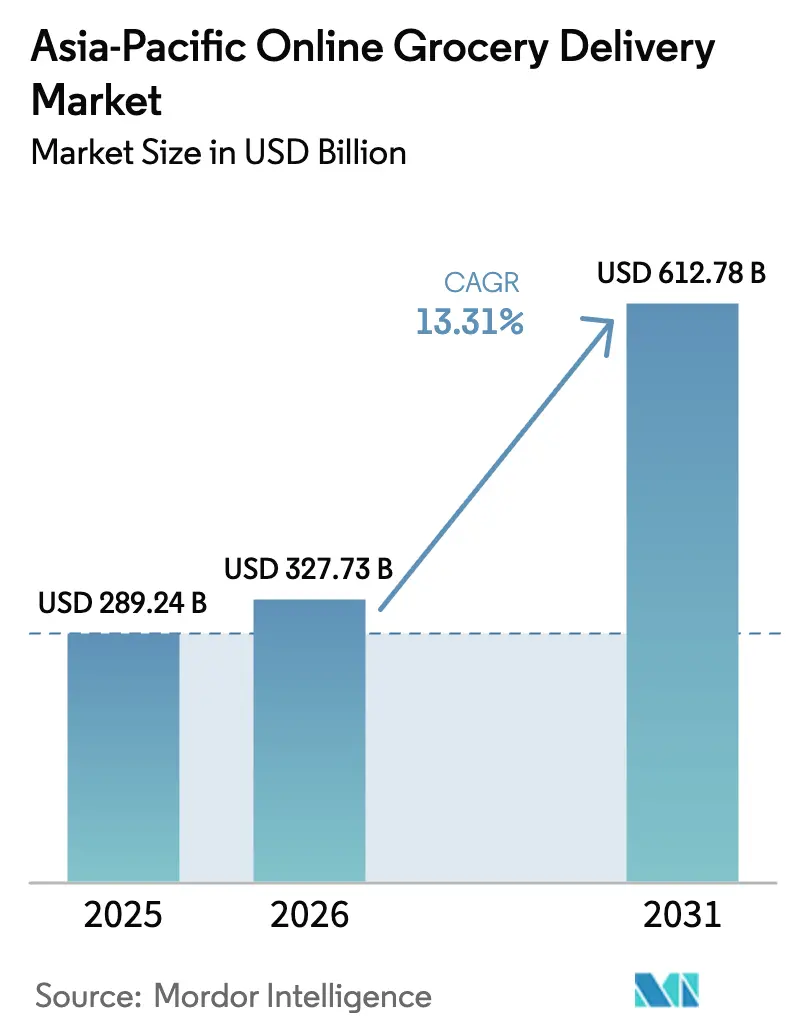

| Base Year Market Size (2025) | USD 289.24 Billion |

| Market Size (2026) | USD 327.73 Billion |

| Market Size (2031) | USD 612.78 Billion |

| Growth Rate (2026 - 2031) | 13.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Online Grocery Delivery Market Analysis by Mordor Intelligence

The Asia-Pacific online grocery delivery market size was valued at USD 289.24 billion in 2025 and estimated to grow from USD 327.73 billion in 2026 to reach USD 612.78 billion by 2031, at a CAGR of 13.31% during the forecast period (2026-2031). This growth trajectory highlights the pivotal role of widespread smartphone adoption, the convenience of digital wallets, and proactive government policies in minimizing purchase friction and broadening the market's reach. While same-day delivery remains the preferred choice, the ≤30-minute delivery window is rapidly gaining traction, driven by urban densification and the rise of automated micro-fulfillment networks in China, India, and Southeast Asia. Retailers are strategically positioning dark-store and warehouse-store formats within bustling neighborhoods. Concurrently, the adoption of open API standards is enhancing identity verification and fraud controls, ensuring first-time shoppers remain engaged. Furthermore, fast-moving consumer goods brands are significantly increasing their on-platform advertising expenditures, creating new revenue avenues and subsidizing delivery fees, thereby fueling a positive growth cycle for the Asia-Pacific online grocery delivery market.

Key Report Takeaways

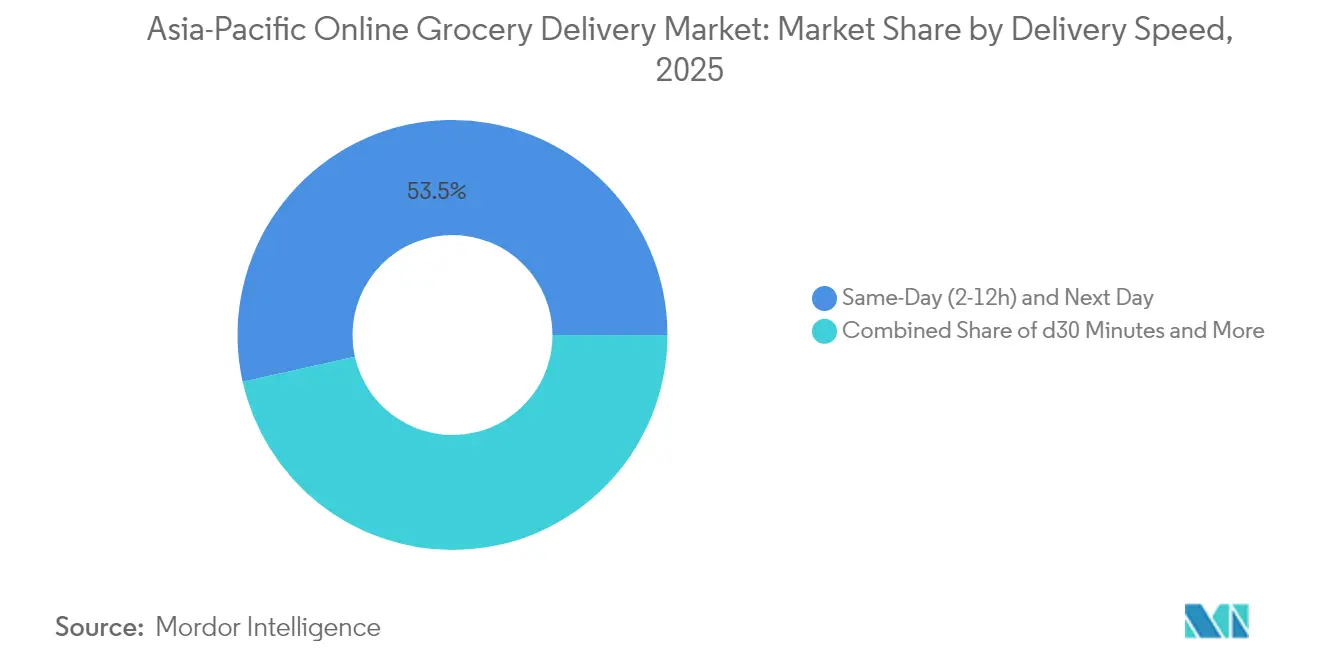

- By delivery speed, same-day and next-day services held 53.48% of the Asia-Pacific online grocery delivery market share in 2025, while the ≤30-minute category is forecast to post a 18.74% CAGR through 2031.

- By product type, staples and packaged goods led with 31.78% revenue share in 2025; fresh produce is projected to expand at a 17.35% CAGR to 2031.

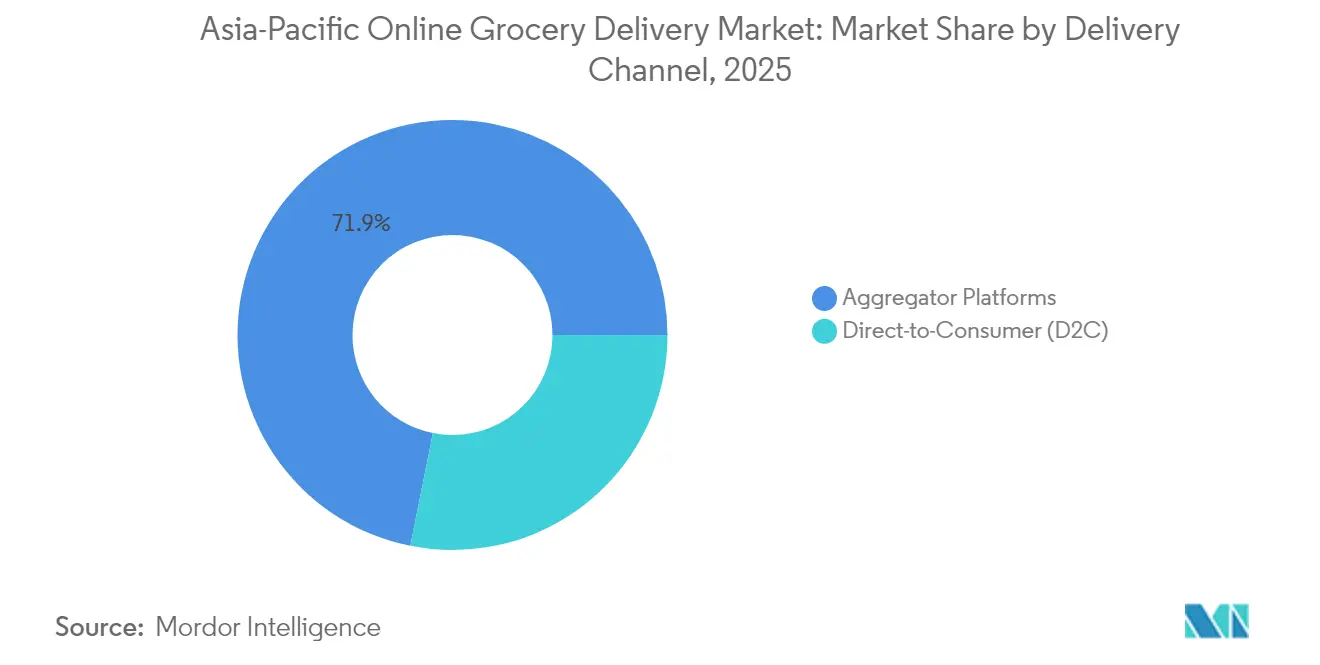

- By delivery channel, aggregator platforms commanded 71.86% share of the Asia-Pacific online grocery delivery market size in 2025, and direct-to-consumer models are advancing at a 15.92% CAGR through 2031.

- By geography, China accounted for 45.88% of the Asia-Pacific online grocery delivery market share in 2025, while India is recording the fastest CAGR of 16.55% to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia contributes to a system defined not by any single geography but by the interaction of many. The global online grocery delivery market data by Mordor Intelligence represents that combined structure.

Asia-Pacific Online Grocery Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Online Adoption of Fresh and Perishable Categories | +2.8% | China, India, Japan, Australia | Medium term (2-4 years) |

| Mobile-First Shopping Experience Enabled by Smartphone Penetration | +3.2% | Regional, with highest impact in India, Indonesia, Vietnam | Short term (≤ 2 years) |

| Growth of Quick Commerce Services for Instant Grocery Needs | +2.1% | Urban centers across India, China, Southeast Asia | Short term (≤ 2 years) |

| Booming On-Platform Advertising Budgets Among FMCG Brands | +1.4% | China, India, Philippines, Thailand | Medium term (2-4 years) |

| Subscription-Based Delivery Models for Daily Essentials | +1.7% | Japan, Singapore, Australia, urban China | Long term (≥ 4 years) |

| Government Initiatives Supporting Digital Infrastructure and Literacy | +2.3% | India, China, Singapore, Thailand | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Mobile-first shopping experience enabled by smartphone penetration

According to DHL, mobile commerce now dominates the digital transaction landscape in the Asia-Pacific, accounting for roughly 80%. By 2026, nations such as China and South Korea are set to surpass a 75% share in mobile commerce. In 2023, the region boasted a mobile internet user base of 1.4 billion, marking a 51% penetration rate. GSMA forecasts that India alone will see smartphone adoption soar to 1.2 billion devices by 2030[1]Source: GSMA Intelligence, “The Mobile Economy Asia Pacific 2024,” gsma.com. With such a robust infrastructure, grocery platforms are tapping into sophisticated mobile features, from real-time order tracking to augmented reality product previews and smooth digital wallet integrations. The rollout of 5G networks, coupled with GSMA's Open Gateway standardization, embraced by major players like Telstra, Singtel, and NTT Docomo, bolsters essential services for grocery deliveries. These include improved identity verification, precise location services, and enhanced fraud prevention. Furthermore, government-backed digital payment initiatives, such as Singapore's SGQR interoperability framework and India's UPI, boasting over 300 million users, are streamlining checkouts. This not only reduces friction but also accelerates mobile commerce adoption, especially among demographics traditionally reliant on cash.

Growth of quick commerce services for instant grocery needs

In 2024, India's ultrafast delivery segment seized two-thirds of the e-grocery market, underscoring a seismic shift in consumer expectations. Major players like Swiggy Instamart, Zepto, and Blinkit, buoyed by substantial capital, are swiftly broadening their dark store networks. Swiggy, for instance, aims to double its store count by March 2025, introducing larger outlets that can stock up to 20,000 SKUs, all to facilitate 10-30 minute delivery windows. Echoing this momentum, JD.com's 7Fresh in China is eyeing 20 new warehouse-store sites in Tianjin by June 2025, each backed by a fleet of over 20 couriers to ensure deliveries in under 30 minutes. The model thrives on dense urban fulfillment networks, challenging traditional supply chain norms. Yet, concerns loom over profitability due to the high operational demands and modest order values. To tackle throughput challenges, players are turning to automation, deploying technologies like Automated Storage and Retrieval Systems and Sorting Transfer Vehicles, all while ensuring perishables remain temperature-controlled.

Increasing online adoption of fresh and perishable categories

The fresh produce segment is undergoing rapid digitization, supported by investments in cold chain infrastructure and growing consumer trust in delivery quality. Indonesia marked a significant development with its first hybrid cold fulfillment warehouse in West Jakarta, which provides integrated multi-temperature storage for B2B and B2C customers, including e-commerce platforms. In India, substantial infrastructure gaps persist, with dairy and fisheries sectors facing cold storage capacity shortages of 80% and 90% respectively, limiting fresh produce delivery capabilities and increasing post-harvest losses. Platforms are implementing advanced demand forecasting systems to reduce food waste while expanding their perishable product offerings. For instance, Picnic utilizes detailed customer data to optimize inventory management and minimize environmental impact through accurate demand predictions. Across Asia-Pacific markets, regulatory requirements for traceability and temperature monitoring are increasing, as evidenced by Vietnam's implementation of digital food safety management systems and stricter import inspections for animal-origin products across multiple jurisdictions. Grocery platforms are forming technology partnerships with automation providers to manage operational challenges through solutions such as micro-fulfillment centers and AI-based inventory management systems designed specifically for perishable goods.

Booming on-platform advertising budgets among FMCG brands

FMCG brands are increasing their digital advertising investments in grocery platforms due to their effectiveness in influencing purchase decisions. Universal Robina Corporation's TikTok Shop expansion showed significant results, with a 227% increase in Total Gross Merchandise Value during promotions and an 8x return on advertising spend through targeted campaigns and live commerce. Grocery platforms' advertising revenues grow through targeted capabilities that use purchase history, demographic data, and shopping behavior to deliver personalized recommendations and offers. Social commerce features, especially in China, Vietnam, Indonesia, and the Philippines, allow brands to use influencer partnerships and live streaming for sales and engagement. These platforms now provide comprehensive advertising options, including sponsored listings, display advertising, and performance marketing tools that track both online and offline results. Their first-party data collection and analytics capabilities offer brands detailed consumer insights while maintaining compliance with various privacy regulations.

Restraints Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Last-Mile Delivery and Urban Congestion | -1.8% | Dense urban centers across China, India, Japan, Singapore | Short term (≤ 2 years) |

| Cold Chain Infrastructure Gaps in Tier-2 and Tier-3 Cities | -2.1% | India, Indonesia, Philippines, Vietnam | Medium term (2-4 years) |

| Rising Urban Warehouse Rents Eroding Quick-Commerce Margins | -1.3% | Major metropolitan areas globally | Medium term (2-4 years) |

| Intense Competition Leading to Profit Margin Pressure | -1.9% | Regional, particularly India and China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High cost of last-mile delivery and urban congestion

Last-mile delivery operations face significant challenges across dense Asian metropolitan areas due to traffic congestion and high labor costs, impacting delivery economics and reliability. Urban warehouse rental costs in prime locations continue to rise, forcing operators to balance customer proximity against operational expenses. The growth of quick commerce services adds pressure, as promises of sub-30-minute deliveries require extensive dark store networks within 2-3 kilometers of customers, increasing real estate costs in urban centers. Fleet operations become more complex as platforms expand their vehicle types to handle larger orders and diverse product categories. For instance, Foodpanda has expanded beyond motorcycles to include cars and vans for order fulfillment, according to Retail Asia[2]Source: Retail Asia, “Foodpanda automates dark stores in Singapore,” retailasia.com. Additional operational challenges arise from regulatory requirements, particularly food safety standards that mandate temperature-controlled vehicles and specific handling procedures, increasing both capital and operating costs. While technology solutions such as route optimization algorithms and predictive analytics help reduce some inefficiencies, fundamental cost pressures remain in markets with rising labor costs and urban congestion.

Cold chain infrastructure gaps in tier-2 and tier-3 cities

Infrastructure constraints limit fresh produce delivery expansion beyond major cities due to insufficient cold storage capacity, creating distribution bottlenecks for perishable goods. India faces significant challenges with regional disparities in cold storage development, with capacity shortages of over 80% in the dairy and 90% in the fisheries sectors, according to Plant Science Today. Energy limitations outside urban centers restrict cold chain expansion, particularly in markets like Indonesia, where power availability varies between Java-Bali and outer islands, as reported by the U.S. International Trade Administration[3]Source: U.S. International Trade Administration, “Indonesia Cold Chain Industry,” trade.gov. Temperature-controlled facility construction costs are typically triple those of conventional warehouses, with energy accounting for 30% of operating costs, limiting development in smaller markets. Government incentives and public-private partnerships are emerging to address these challenges, requiring targeted investments in underdeveloped regions to improve supply chain efficiency and reduce food waste. While solar-powered cooling systems and modular cold storage solutions could address infrastructure gaps, their implementation remains restricted by limited awareness and regulatory frameworks for energy-efficient alternatives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Delivery Speed: Same-Day Dominance Challenged by Instant Fulfillment

Same-Day delivery (2-12 hours) and Next Day services hold 53.48% market share in 2025, demonstrating the effectiveness of existing logistics networks and consumer preference for standard delivery timeframes in grocery purchases. The ≤30 Minutes delivery segment shows the highest growth potential with 18.74% CAGR through 2031, supported by increasing urbanization and rising demand for immediate delivery. JD.com illustrates this trend through its 7Fresh warehouse-store expansion, with plans to open 20 new locations in Tianjin by June 2025, utilizing dedicated courier teams to achieve sub-30-minute delivery times. Scheduled delivery (>24 hours) remains important for bulk orders and regular shopping patterns, particularly in markets where consumers follow weekly or monthly shopping routines.

Success in the market depends on extensive fulfillment networks and robust inventory management systems, particularly for instant delivery operations that require accurate demand prediction and strategic product placement across multiple micro-fulfillment centers. Alibaba's Freshippo demonstrates effective format adaptation by reducing large-format locations while increasing smaller fresh-food supermarkets to improve operational efficiency and delivery times. The integration of automated storage and retrieval systems is essential for handling frequent, small-volume orders while ensuring product quality and accuracy. Companies must comply with local food safety regulations and temperature control requirements during quick delivery operations, which affects operational protocols and delivery vehicle requirements across different regions.

By Product Type: Staples Leadership Amid Fresh Produce Innovation

Staples and Packaged Goods hold a dominant 31.78% market share in 2025, supported by extended shelf life, standardized packaging, and efficient supply chain operations that enable profitable delivery. Fresh Produce shows significant growth potential with a 17.35% CAGR through 2031, as consumers trust quality preservation methods and platforms expand their cold chain infrastructure. Dairy and Bakery segments present operational challenges due to specialized handling needs and quick turnover requirements, while creating opportunities for platforms with advanced temperature-controlled logistics. The Meat, Fish, and Seafood categories require robust cold chain management systems, with varying regulatory requirements across Asia-Pacific markets necessitating specific certifications and handling protocols.

Beverages remain a high-volume category with narrow margins, requiring efficient bulk distribution systems. Frozen Foods demand consistent temperature control throughout distribution, which limits expansion in regions lacking adequate cold storage facilities. Fresh category performance links directly to cold chain infrastructure development, evidenced by Indonesia's hybrid cold fulfillment warehouse implementation and Malaysia's growing demand for temperature-controlled facilities. Platforms achieve competitive advantage through fresh produce quality and selection, implementing advanced forecasting systems and supplier management to reduce waste while expanding product range. The integration of IoT temperature monitoring and AI inventory management systems becomes crucial for profitable perishable goods operations across different climate zones and regulatory frameworks.

By Delivery Channel: Aggregator Platforms Face D2C Disruption

Aggregator Platforms hold a dominant 71.86% market share in 2025, benefiting from network effects, established merchant partnerships, and robust logistics capabilities to address consumer needs across product categories. The Direct-to-Consumer (D2C) segment is growing at a 15.92% CAGR through 2031, as retailers seek to control customer relationships and data while improving margins by eliminating intermediaries. Woolworths demonstrated the potential of D2C implementation through MILKRUN, using a composable commerce architecture to deploy mobile channel capabilities across 30 stores shortly after launch. This D2C adoption reflects retailers' focus on managing customer experience, pricing, and data while reducing reliance on commission-based third-party platforms.

While Aggregator platforms retain advantages in customer acquisition, logistics scale, and technology infrastructure, they face growing competition from retailers investing in their delivery systems. Companies are adopting hybrid approaches through strategic partnerships, as seen in Naver's collaboration with Kurly to enhance fresh grocery services without developing separate logistics networks. Retailers are partnering with automation providers to scale D2C operations efficiently, implementing solutions from micro-fulfillment centers to AI-driven personalization systems. The market is moving toward an environment where success requires both aggregator scale and direct retail capabilities, potentially increasing industry consolidation and strategic partnerships.

Geography Analysis

China holds 45.88% market share in 2025, supported by advanced digital infrastructure, established logistics networks, and widespread consumer adoption of mobile commerce and digital payments. Government policies targeting 10% GDP contribution from core digital industries by 2025 provide a structured framework for platform development. Alibaba's Freshippo achieved profitability through format optimization, while JD.com's expansion of 7Fresh warehouse stores and quick commerce investments demonstrate ongoing market evolution. Recent regulatory frameworks for data governance and platform oversight establish clear operational guidelines for market growth.

India shows a 16.55% CAGR through 2031, propelled by increasing smartphone adoption, digital payment infrastructure, and urbanization. Quick commerce accounts for two-thirds of e-grocery orders in 2024, reflecting consumer preference for instant delivery. The UPI payment system processes over 10 billion monthly transactions across 300 million users, enabling widespread market access. Major platforms, including Swiggy Instamart, Zepto, and Blinkit, expand dark store networks and increase order values through larger formats. Infrastructure gaps persist, with an 80% shortage in dairy and 90% in fisheries cold chain capacity, requiring investment for fresh produce expansion.

Japan, Australia, and Southeast Asian markets present varied growth potential based on infrastructure development and regulatory frameworks. Japan's digital transformation laws and AI policies support grocery platform innovation. Australia advances in automation, with Coles implementing AI-powered shopping carts and Woolworths developing micro-fulfillment systems. Southeast Asian markets show strong mobile commerce adoption and digital payment growth, though cold chain infrastructure varies regionally, with Indonesia developing hybrid fulfillment while other markets address energy and logistics limitations.

The online grocery delivery market is analyzed by Mordor Intelligence across multiple other geographies, with in-depth regional assessments available for Middle East and Africa and South America.

Competitive Landscape

The Asia-Pacific online grocery delivery market is moderately fragmented, with competition remaining intense, as regional leaders emerge. This landscape showcases a distribution of market share across numerous players, rather than a clear dominance by a select few. Major players are increasingly focusing on vertically integrating their logistics capabilities. They're making substantial investments in proprietary fulfillment networks, cold chain infrastructure, and last-mile delivery. This strategy not only enhances service quality but also allows them to exert greater control over unit economics. Technology has emerged as a pivotal competitive tool. For instance, Foodpanda has automated its micro-fulfillment centers in Singapore, employing storage-and-retrieval systems and AI-driven demand forecasting. This move, highlighted by Retail Asia, aims to streamline inventory management and expedite order processing.

Tier-2 and tier-3 cities present white-space opportunities. While these areas have infrastructure gaps that pose entry barriers, they also offer first-mover advantages. This is especially true for players capable of crafting cost-effective cold chain solutions tailored for smaller markets. New entrants are harnessing composable commerce architectures and forging strategic partnerships. A case in point is Woolworths' MILKRUN, which swiftly rolled out mobile channel deployment across 30 stores in mere months, thanks to its cloud-native infrastructure and API integrations.

Consolidation is on the rise, evident from Macrovalue's SGD 125 million acquisition of DFI Retail's operations in Singapore. Additionally, technology partnerships are flourishing, as seen in Lotte's collaboration with Ocado for advanced fulfillment automation. Instead of directly entering new markets, many are opting for cross-border strategies that emphasize technology transfer and operational know-how. Successful entities are licensing their fulfillment technologies and management systems to local partners. Navigating regulatory compliance is becoming crucial. Platforms adept at mastering the intricacies of food safety, labeling, and cross-border regulations are carving out sustainable advantages, enabling them to cater effectively to the diverse regulatory landscapes across Asia-Pacific markets.

Asia-Pacific Online Grocery Delivery Industry Leaders

Alibaba Group (Tmall Supermarket, Freshippo)

JD.com (7Fresh)

Amazon (Amazon Fresh)

Reliance Retail (BigBasket/BB Now)

Zomato (Blinkit)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Alibaba's Freshippo grocery chain achieved first-time annual profitability for the fiscal year ended March 31, 2025, following strategic reforms including format optimization and operational restructuring under CEO Yan Xiaolei, with plans to open nearly 100 new stores and enter dozens of new cities.

- April 2025: Naver and Kurly announced a strategic partnership to integrate Kurly's fresh grocery delivery into Naver's Plus Store platform by year-end, enabling seamless grocery shopping without separate app downloads to challenge market leader Coupang's dominance in South Korea.

- March 2025: JD.com announced plans to open 20 new 7Fresh warehouse-store locations in Tianjin by June 2025, expanding its front-warehouse model to strengthen 30-minute delivery capabilities amid intense instant-retail competition.

- March 2025: Macrovalue agreed to acquire DFI Retail Group's Singapore food business for SGD 125 million, covering 48 Cold Storage stores, 41 Giant stores, and two distribution centers, with transaction completion expected in H2 2025.

Asia-Pacific Online Grocery Delivery Market Report Scope

Online Grocery is an online ordering facility offered by grocers functioning either as a brick-and-mortar supermarket, a grocery store, or a standalone e-commerce service providing grocery items. Online Grocers offer digital payment methods, optional delivery slots, and access to a large selection of products. The convenience of these factors made buyers shift to online grocery orders. Fresh and packaged goods like meat, seafood, cereals, fruits and vegetables, dairy, cereals, snacks, and more can be delivered to your doorstep with just a click of the mouse.

In terms of product type market is segmented into Product Type Retail Delivery, Quick Commerce, and Meal Kit Delivery, and the geographical scope of the report includes India, China, Japan, South Korea, Thailand, Indonesia, Australia, and the Rest of Asia Pacific.

| ≤30 Minutes |

| Same-Day (2-12 h) and Next Day |

| Scheduled (>24 h) |

| Fresh Produce |

| Dairy and Bakery |

| Meat, Fish, and Seafood |

| Staples and Packaged Goods |

| Beverages |

| Frozen Foods |

| Other Product Type |

| Direct-to-Consumer (D2C) |

| Aggregator Platforms |

| China |

| India |

| Japan |

| Australia |

| Indonesia |

| South Korea |

| Thailand |

| Singapore |

| South Korea |

| Vietnam |

| Philippines |

| Rest of Asia-Pacific |

| By Delivery Speed | ≤30 Minutes |

| Same-Day (2-12 h) and Next Day | |

| Scheduled (>24 h) | |

| By Product Type | Fresh Produce |

| Dairy and Bakery | |

| Meat, Fish, and Seafood | |

| Staples and Packaged Goods | |

| Beverages | |

| Frozen Foods | |

| Other Product Type | |

| By Delivery Channel | Direct-to-Consumer (D2C) |

| Aggregator Platforms | |

| By Geography | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| South Korea | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia Pacific online grocery delivery space in 2026?

The Asia Pacific online grocery delivery market size stands at USD 327.73 billion in 2026.

What is the projected growth rate for the next five years?

The market is forecast to register a 13.31% CAGR through 2031.

Which delivery speed category is growing the fastest?

The ≤30-minute fulfillment segment is expected to surge at a 18.74% CAGR over the forecast period.

Which product segment shows the strongest expansion?

Fresh produce is projected to record a 17.35% CAGR as cold-chain logistics mature.

Why is India considered the most dynamic geography?

India pairs rapid smartphone adoption with the UPI payment rail, producing a 16.55% CAGR and high quick-commerce uptake.

Page last updated on: