Asia Pacific Gas Detector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

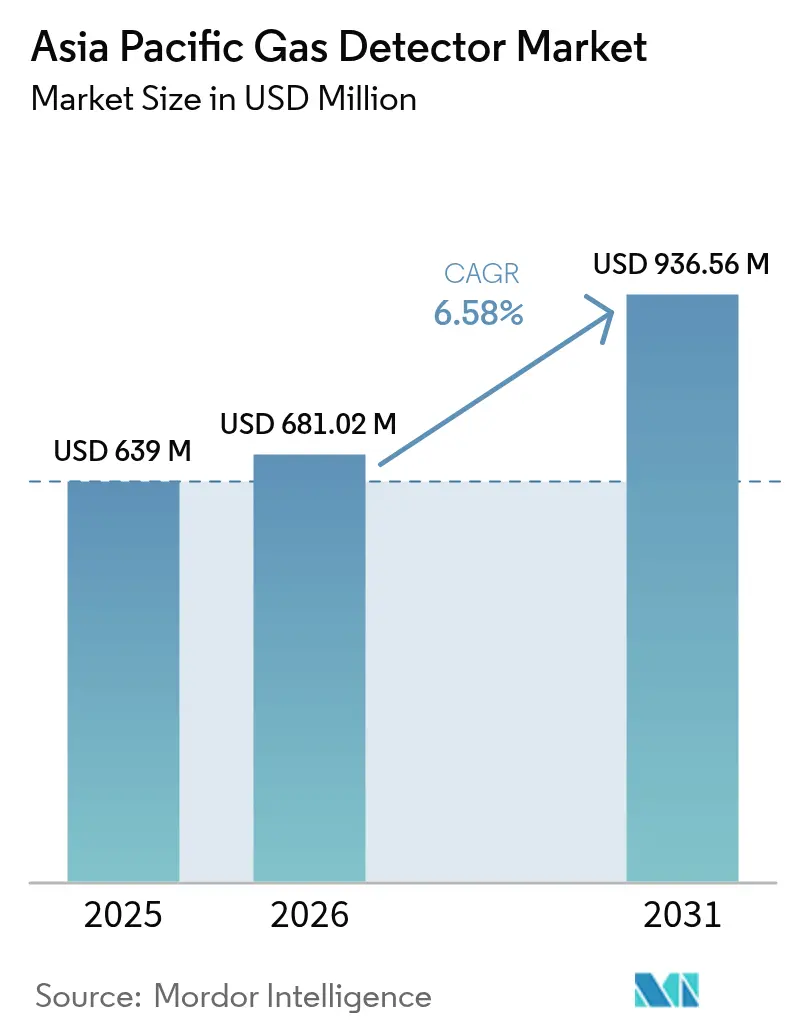

| Base Year Market Size (2025) | USD 639 Million |

| Market Size (2026) | USD 681.02 Million |

| Market Size (2031) | USD 936.56 Million |

| Growth Rate (2026 - 2031) | 6.58% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Gas Detector Market Analysis by Mordor Intelligence

The Asia Pacific gas detector market size was valued at USD 639 million in 2025 and estimated to grow from USD 681.02 million in 2026 to reach USD 936.56 million by 2031, at a CAGR of 6.58% during the forecast period (2026-2031). Accelerating industrialization, stringent workplace-safety requirements, and multi-billion-dollar oil, gas, and petrochemical projects continue to stimulate equipment upgrades across fixed, portable, and wireless detection platforms. China’s dominant industrial base anchors regional demand, while India’s manufacturing expansion and Smart Cities Mission fuel rapid incremental growth. Wired systems retain a deployment edge because of established infrastructure, yet wireless architectures gain ground as IIoT adoption eases brownfield retrofits and supports predictive maintenance analytics. Robust safety mandates ranging from Malaysia’s Occupational Safety and Health Amendment 2022 to South Korea’s Industrial Safety and Health Act raise minimum compliance thresholds, prompting enterprises to standardize multi-gas monitoring throughout confined-space operations. Competitive intensity rises as multinational leaders integrate cloud connectivity, self-calibrating sensors, and AI-driven diagnostics, while regional suppliers leverage localized production and service networks to win cost-sensitive projects.

Key Report Takeaways

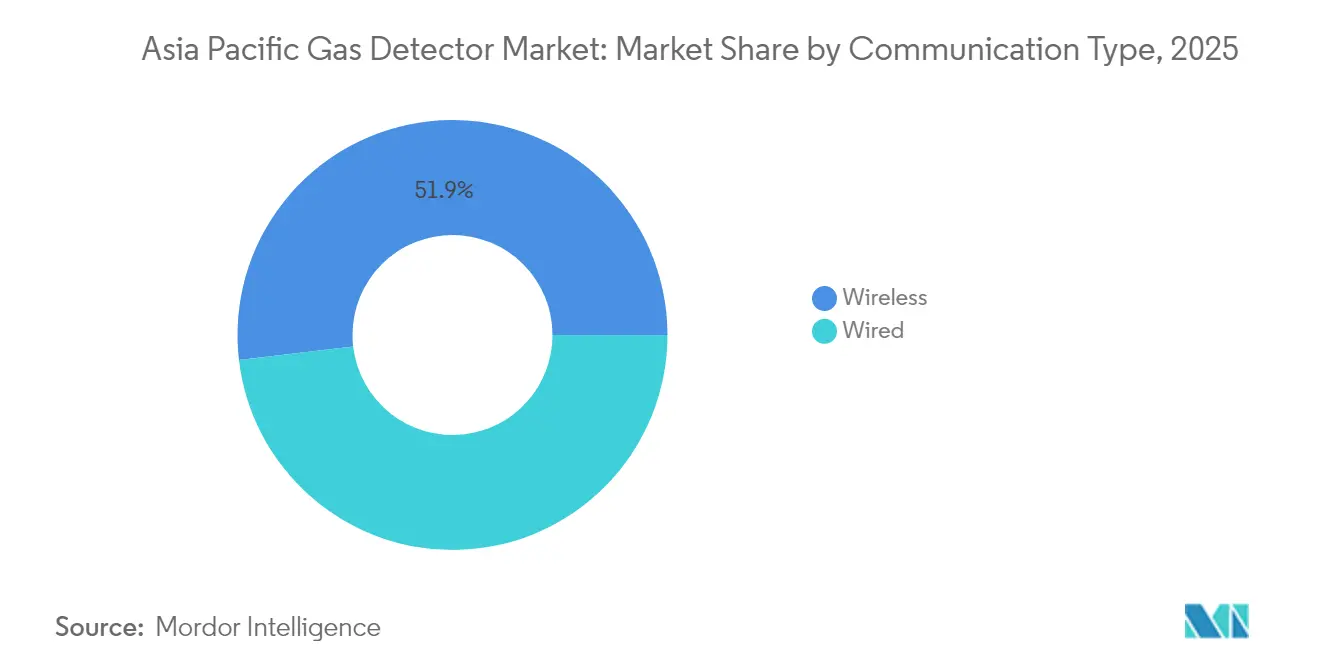

- By communication type, wired systems led with 48.15% of the Asia Pacific gas detector market share in 2025, whereas wireless solutions are forecast to post a 8.62% CAGR through 2031.

- By detector type, fixed installations accounted for 47.75% of the Asia Pacific gas detector market size in 2025, while portable detectors are projected to grow at an 8.14% CAGR to 2031.

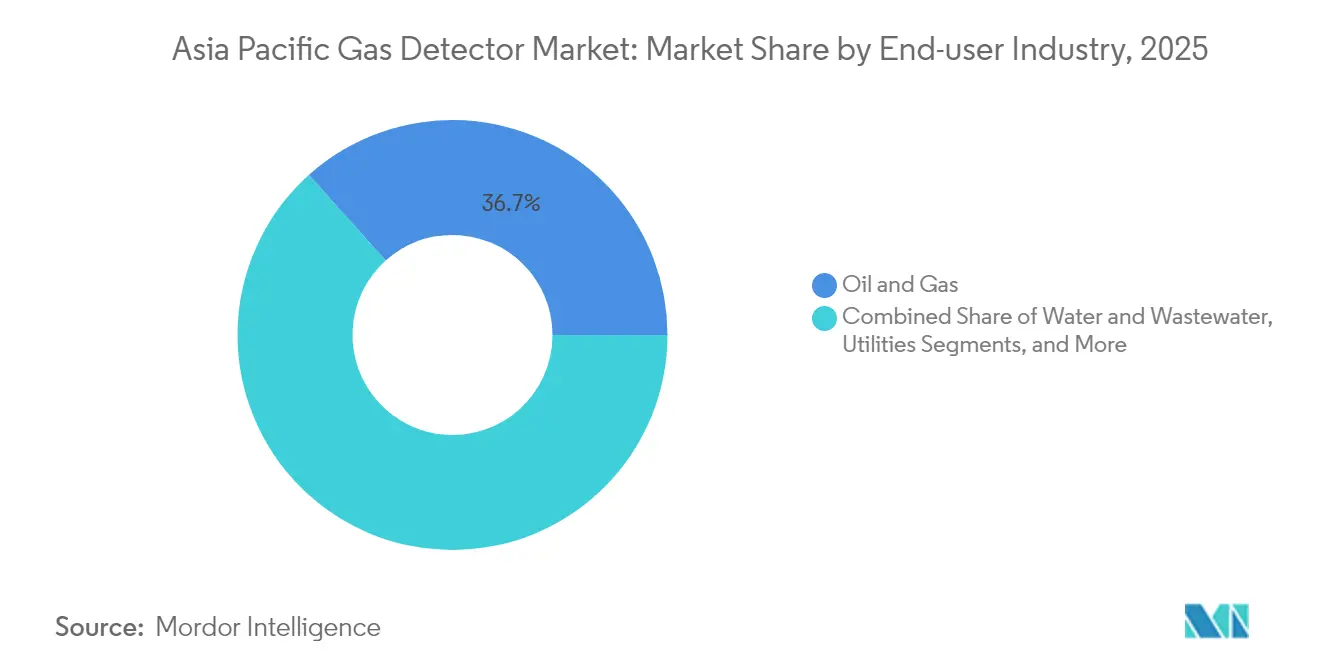

- By end-user industry, oil and gas captured 36.65% of the Asia Pacific gas detector market share in 2025; utilities represent the fastest-growing application, advancing at an 8.29% CAGR over the outlook period.

- By geography, China held 35.25% of regional revenue in 2025, yet India is poised to expand at an 8.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Gas Detector Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent workplace safety regulations | +1.8% | China, India, Southeast Asia | Medium term (2-4 years) |

| Expansion of oil and gas and petrochemical capex | +1.5% | Southeast Asia, India, spillover to China | Long term (≥ 4 years) |

| Rapid uptake of IIoT-enabled wireless detection | +1.2% | Japan, Korea, Australia; early regional adoption | Short term (≤ 2 years) |

| Smart-city air-quality mandates | +0.9% | Major Asia-Pacific urban centers | Medium term (2-4 years) |

| Hydrogen-economy pilots (H₂ sensors) | +0.7% | Japan, Korea, Australia | Long term (≥ 4 years) |

| China GB/T-2025 methane-leak rules | +0.6% | National China; influence on regional norms | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent workplace-safety regulations across the Asia-Pacific heavy industries

National authorities continue to ratchet up occupational-safety statutes, compelling manufacturers, refiners, and utilities to install certified multi-gas monitors across confined spaces and hazardous process areas. Malaysia’s Occupational Safety and Health Amendment 2022 obliges every employer to appoint safety coordinators and document atmospheric-monitoring practices, boosting fixed-detector penetration across chemical and palm-oil processing clusters.[1]Source: Federation of Malaysian Manufacturers, “Businesses in a Bind Over Safety,” fmm.org.my Australia enforces intrinsically safe instrumentation under AS/NZS standards for confined-space entry, while South Korea mandates five-gas measurement (O₂, CO, LEL, H₂S, CO₂) at worksites, standardizing demand for portable multi-gas detectors.[2]Source: Safegas Korea, “MicMeta-5C Five-Gas Measurement Mandate,” safegaskorea.kr Corporate harmonization plays a multiplier role: multinationals export internal safety protocols to satellite facilities in Vietnam and Indonesia, driving uniform procurement of networked gas-detection platforms across the supply chain. The result is a structural uplift in baseline sensor specifications, faster response times, wider operating ranges, and digital calibration logs that favour differentiated technology providers.

Expansion of oil and gas and petrochemical projects in emerging Asia-Pacific economies

Southeast Asia’s petrochemical build-out supplies the region’s single largest capital-expenditure catalyst for detection equipment. Projects such as Malaysia’s USD 3.5 billion Pengerang Energy Complex and Indonesia’s 555 km Dumai–Sei Mangkei transmission pipeline embed continuous monitoring for volatile organic compounds, methane, and H₂S, creating a durable pull-through for fixed sensor arrays. Thailand’s PTTEP allocates USD 21.2 billion over five years to upstream gas and LNG, magnifying offshore platform demand for flameproof detectors, while Vietnam’s Long Son complex adds cryogenic ethane tanks requiring leak-before-break detection architectures. The swing toward integrated refinery-petrochemical hubs and deep-water gas fields raises hazard complexity, accelerating the adoption of networked infrared, ultrasonic, and laser-based detectors with continuous self-diagnostics.

Rapid uptake of IIoT-enabled wireless gas detection platforms

Industrial Internet of Things integration refashions the cost-benefit calculus for safety managers by eliminating cable runs, enabling asset-health analytics, and facilitating real-time alerts across distributed sites. MSA Safety’s ALTAIR io 4 combines CAT-M LTE connectivity with “Shared Alerts”, instantly notifying nearby workers when a team member triggers an alarm. Emerson’s Rosemount 928 Wireless Monitor leverages WirelessHART to stream diagnostics to the plant historian, while tool-less sensor replacement reduces maintenance downtime.[3]Source: Emerson Electric Co., “Gas Detection in Power Generation,” emerson.com Cloud-based dashboards such as Industrial Scientific’s iNet Control+ aggregate fleet data, automate compliance records, and predict sensor-end-of-life, shrinking calibration costs. Wireless systems, therefore, penetrate brownfield petrochemical sites, upstream well pads, and temporary turnaround projects, despite higher per-unit sensor prices.

Smart-city air-quality mandates boosting demand for IoT-linked detectors

Urban-development programs embed environmental monitoring into the core of smart-city platforms, extending gas-detection use cases beyond heavy industry. India’s 100-city Smart Cities Mission funds integrated command-and-control centers that track industrial emissions, solid-waste decomposition gases, and potable-water odorants.[4]Source: IEEE Smart Cities, “Smart City Mission of India,” smartcities.ieee.org China’s GB 50325-2020 mandates testing for formaldehyde, xylene, benzene, and radon in new civil buildings, steering procurement toward multi-parameter sensors certified for occupancy health standards. Municipal gas utilities deploy smart meters with embedded leak detection, such as the 650,000 prepaid units financed under Bangladesh’s ADB-backed installation program. Guangzhou’s gas-management ordinance layers QR-code cylinder tracking with centralized cloud dashboards, showcasing how urban regulators harness IoT networks for public-safety oversight.[5]Source: Guangzhou Municipal Justice Bureau, “Measures of Guangzhou Municipality for Gas Management,” sfj.gz.gov.cn These initiatives distribute incremental demand across portable, wall-mount, and meshed sensor nodes linked to GIS dashboards.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| High upfront CAPEX for advanced fixed systems | -1.1% | SME-heavy markets in Southeast Asia and India | Medium term (2-4 years) |

| Post-pandemic budget compression among SME manufacturers | -0.8% | Thailand, Vietnam, and Malaysia are manufacturing hubs | Short term (≤ 2 years) |

| Shortage of certified calibration technicians | -0.6% | Vietnam, Indonesia, wider Southeast Asia | Medium term (2-4 years) |

| Tariff-driven sensor-module cost volatility | -0.4% | China's supply chains with Asia-Pacific spillover | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High upfront CAPEX for advanced fixed detection systems

Price sensitivity remains the principal adoption hurdle for small and medium manufacturers. Installation of networked infrared detectors with redundancy loops can cost multiples of annual safety budgets, especially when compliance training already absorbs MYR 500–900 per coordinator in Malaysia. Hardware savings achieved by regional suppliers are partly offset by integration, calibration gas, and cloud subscription fees, prolonging payback periods. Multilateral credit facilities exist, yet awareness among SMEs is limited, delaying mass roll-outs in Thailand’s automotive supply chain and Vietnam’s garment clusters. Vendors respond with subscription-based “gas-detection-as-a-service” models bundling hardware, calibration, and software into monthly operating expenditures, but regulatory acceptance of service-model compliance certificates varies across jurisdictions, constraining scale.

Post-pandemic budget compression among SME manufacturers

Lingering pandemic-era liquidity stress forces SMEs to prioritize core production investments over safety-system upgrades. Asian Development Bank’s 2024 survey indicates working-capital loans remain skewed toward export-credit lines rather than safety infrastructure, even though standards enforcement has tightened. Consequently, many dyeing mills and furniture workshops extend calibration intervals or rely on single-gas spot checkers rather than holistic multi-gas networks, heightening incident risk. Enforcement agencies in Malaysia and Indonesia consequently stage compliance sweeps targeting high-risk sectors, yet financial relief such as grant-backed detector procurement remains in early pilot phases. Until macro-economic recovery broadens profit margins, unit growth among SMEs will lag top-line regional expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Communication Type: Wireless Gains Despite Wired Dominance

The wired architecture retained 48.15% of the Asia Pacific gas detector market share in 2025, mainly because process industries already possess intrinsic analogue and digital cabling, and failure-mode-and-effect analyses favor redundant, hard-wired loops for life-critical alarms. Wireless, however, is forecast to compound at 8.62% through 2031 as battery-powered nodes slash installation labor, a major cost component in brownfield facilities. LTE-M and NB-IoT modules coupled with over-the-air firmware updates simplify large-scale asset-management cycles, while WirelessHART meshes satisfy determinism requirements in continuous processes. Field trials in Korean shipyards confirm that wireless detectors cut deployment time by 60% and eliminate cable-tray rework.

Portable devices increasingly embed BLE beacons and cloud gateways, blending portability with fleet-wide visibility. Fixed-wireless hybrids emerge where ATEX-rated power lines feed detectors, but signal backhaul occurs via 2.4 GHz mesh, avoiding copper cable runs over rotating machinery and hazardous zones. Telecom-operator partnerships in Japan and Australia enable bundled SIM data plans, reducing recurring connectivity charges for end users. Given these structural advantages, wireless is poised to erode the wired share, yet legacy system inertia and corporate qualification cycles suggest wired dominance persists at least until 2027.

By Detector Type: Fixed Systems Lead Amid Portable Growth

Fixed systems occupied 47.75% of the Asia Pacific gas detector market size in 2025 on the back of mandatory continuous monitoring in refineries, LNG terminals, and power plants. Infrared point detectors configured for 0–100% LEL hydrocarbon measurement remain the default in process areas, while open-path lasers guard perimeter fence lines. Portable detectors, nonetheless, are poised for the fastest 8.14% CAGR, supported by regulatory five-gas measurement standards in South Korean and Australian confined-space codes and by the need for flexibility during maintenance turn-arounds. Asia Pacific gas detector market share for portable devices is on track as battery runtimes extend beyond 25 hours and sensor swap-out becomes tool-less.

Technological miniaturization allows four-gas capabilities within palm-sized enclosures weighing under 100 g, improving worker compliance. Calibration-free disposable single-gas units meet entry-level needs for SMEs, while multi-gas models integrate man-down alarms and GPS beacons. Transportable detectors bridge gaps during plant commissioning or pipeline hot-work, operating as stand-alone nodes with wireless backhaul to central command. The resulting product stratification enables suppliers to segment portfolios by price, spec, and service bundle, maximizing revenue capture across user tiers.

By End-User Industry: Oil and Gas Leadership with Utilities Surge

Oil and gas operations generated 36.65% of the Asia Pacific gas detector market revenue in 2025, reflecting stringent process-safety mandates and the hazard spectrum spanning benzene, H₂S, and combustible gases. Upstream and midstream projects in Malaysia, Thailand, and Australia continue to specify triple-redundant fixed detectors plus flame and ultrasonic additions, locking in high average selling prices. In contrast, the utilities segment, covering power generation and gas-distribution networks, is projected to grow at an 8.29% CAGR, propelled by hydropower refurbishments, coal-to-gas conversion projects, and hydrogen co-firing pilots across Japan and Korea.

Chemical and petrochemical users maintain steady sensor replacements driven by catalyst change-outs and feedstock diversification. Water and wastewater utilities boost dissolved-gas monitoring to prevent anaerobic hazards in digesters, while metal-mining operations invest in methane and oxygen monitors to comply with New South Wales Mine Design Registration requirements. The competitive implication is a broader mix of detector types, infrared, electrochemical, and photoionization, tailored to industry-specific gas profiles.

Geography Analysis

China captured 35.25% of the Asia Pacific gas detector market share in 2025, benefiting from extensive industrial clusters and stringent standards such as GB 50325-2020, which prescribes multi-parameter air-quality testing in new civil buildings. Ongoing municipal pipeline upgrades under GB/T-2025 add thousands of continuous-monitoring nodes, and city-level ordinances in Guangzhou require QR-coded LPG cylinder tracking plus real-time leak alerts. Domestic suppliers leverage local certifications to penetrate SME segments, while export-oriented factories procure global-brand detectors to match multinational corporate standards.

India, the fastest-growing geography at an 8.52% CAGR, mobilizes demand through 100-smart-city deployments, Make-in-India manufacturing incentives, and progressive workplace-safety codes. Integration of gas detection within municipal solid-waste processing and water-treatment PPP contracts widens application scope. Adoption accelerates further as power-generation projects adopt gas turbines configured for hydrogen blends, requiring H₂ partial-discharge monitors.

Japan and South Korea sustain mid-single-digit growth via hydrogen-economy pilots and stringent confined-space regulations. Japan’s Ministry of Economy, Trade and Industry backs liquid-hydrogen demonstration voyages, mandating class-society approval of H₂-specific detectors on board carriers. Australia and New Zealand contribute stable demand anchored by mining safety and refinery refurbishments; open-path IR and ultrasonic detectors dominate LNG-export terminals here. Southeast Asia, Indonesia, Malaysia, Thailand, and Vietnam collectively represent the region’s highest greenfield opportunity, thanks to USD 220 billion worth of gas and petrochemical projects in the pipeline, each specifying extensive detector networks.

Regulatory Landscape

Across Asia-Pacific, gas detector specifications and procurement are being tightened through a mix of national workplace-safety rules and international hazardous-area certification schemes. China has been updating and rolling out a sequence of GB/GB/T standards relevant to toxic and combustible gas detection, including the implementation of GB 12358-2024 in June 2025 (general technical requirements for workplace gas detection and alarm instruments), GB/T 45524-2025 implemented in November 2025 (public safety field flammable/explosive gas detection and alarm devices), and GB/T 46692.1-2025 implemented in May 2026 (performance requirements for toxic gas detectors in workplace atmospheres). In April 2026, China issued GB/T 47438.3-2026 covering combustible gas detection and alarm systems in hazardous chemical workplaces, with implementation scheduled for May 2027, strengthening system-level requirements for chemical-site deployments.

For cross-border industrial projects and multinational operators, compliance is commonly anchored to IECEx (IEC 60079 series) for explosion-protected equipment, while local certification infrastructure supports enforcement and conformity assessment. Australia references explosive-atmosphere compliance pathways through state bodies such as TestSafe NSW, which tests and certifies equipment against IECEx/ANZEx expectations for hazardous-area use. India is also tightening digital integrity requirements around emissions-related measurement equipment: in June 2026, the Ministry of Road Transport and Highways issued Amendment No. 1 to AIS-137 (Part 8), requiring cryptographic signing of pollution test data prior to transmission to the National Informatics Centre server. This reinforces the broader shift toward traceable, tamper-resistant compliance data flows that influence connected sensing and monitoring ecosystems.

Value Chain Analysis

The Asia-Pacific gas detector value chain spans sensor materials and components (electrochemical cells, catalytic beads, IR sources/detectors, MEMS elements), module and instrument manufacturing (fixed and portable detectors, controllers, gateways), certification and calibration infrastructure, and downstream system integration and lifecycle services. Upstream supply is shaped by hazardous-area and performance standards (including IECEx and national GB/GB/T requirements), which drive design validation, type testing, and documentation, while midstream manufacturing ranges from high-volume domestic production for cost-sensitive customers to premium, certified platforms for oil and gas, chemicals, utilities, and mining users.

China anchors regional manufacturing capacity and domestic project fulfillment, supported by local suppliers with integrated production and service footprints. For example, Chengdu Action Electronics Joint-Stock Co., Ltd. positions itself as a major gas alarm manufacturer and supplier to PetroChina, Sinopec, and CNOOC, with automated SMT/DIP production lines and large-scale unit capacity, supporting rapid delivery into industrial clusters and municipal gas-grid programs. Regional players also operate integrated models combining R&D, manufacturing, sales, and after-sales support, as seen with Tianjin U-Tai Technology Development Co., Ltd., which coordinates Southeast Asia activity through its Malaysia presence. Downstream, distributors and integrators bundle detectors with controllers, WirelessHART/LTE connectivity, commissioning, periodic bump tests and calibration gas logistics, and increasingly software subscriptions for fleet management and compliance records. In this setup, service network depth and technician availability shape total cost of ownership for end users.

Competitive Landscape

The regional competitive arena is moderately fragmented. Honeywell, MSA Safety, and Draegerwerk command premium positions through global certifications, vertically integrated sensor technology, and comprehensive service footprints. Honeywell’s 2025 acquisition of Norcross Safety Products broadens PPE partnership, enabling bundled detector-plus-respirator tenders in refinery turn-arounds. MSA’s local assembly partnerships cut lead times and circumvent import duties, a decisive advantage in India and Saudi Arabia. Industrial Scientific differentiates itself via its iNet SaaS platform that automates compliance logs and predicts sensor end-of-life, lowering the total cost of ownership for fleet operators.

Regional manufacturers Hanwei Electronics, New Cosmos Electric, and Riken Keiki capture share among SMEs by offering cost-optimized detectors compatible with domestic calibration gases. Their agile engineering cycles allow rapid localization of firmware for local languages and alarm set-points tied to national standards. Technology competition centers on self-calibrating sensors, long-life Li-SOCl₂ batteries, and intrinsically safe Bluetooth gateways. As hydrogen applications rise, component suppliers race to certify palladium-alloy catalytic sensors with sub-0.4% LEL detection thresholds, opening niches for new entrants specialized in H₂.

Strategic moves increasingly couple hardware with digital ecosystems. Draeger’s INARA digital safety guard extends multi-site monitoring through wearable beacons, while Teledyne integrates optical gas imaging with methane quantification analytics for fugitive-emission reporting. Market entrance barriers remain moderate: certification costs and service-network investments deter opportunistic entrants, yet local assembly rules in Indonesia and India foster domestic-supplier emergence, intensifying price competition in low-to-mid tier segments.

Asia Pacific Gas Detector Industry Leaders

Honeywell Analytics Inc.

Drägerwerk AG & Co. KGaA

MSA Safety Incorporated

Teledyne Gas & Flame Detection

Industrial Scientific Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity is moving gas detection from standalone hardware toward connected safety and compliance systems that unify portable and fixed device data, alarm history, and audit records across multi-site operations. The 2026 product and project activity shows this direction: Honeywell expanded its Safety Suite 2.0 capabilities to provide real-time visibility into portable gas detector status and historical alarm events, aligning with utilities and chemical operators that manage large fleets and frequent compliance checks. MSA Safety also introduced connectivity infrastructure for the Pacific-Asia region (FieldServer ProtoNode Gateway with MSA Grid), enabling legacy fixed gas and flame detection to be monitored remotely and visualized centrally, which supports brownfield upgrades where cabling and manual rounds are constraints.

Beyond oil and gas, whitespace is widening in urban and commercial-industrial environments where gas detection is tied to statutory safety regimes and facility operations. Refrigeration and cold-chain facilities using ammonia illustrate this: in April 2026, Geronik deployed ionic ammonia gas detectors at a Singapore industrial cold storage site and integrated them into existing monitoring infrastructure to support Workplace Safety and Health Act compliance. At the same time, China is tightening the technical baseline for workplace toxic and combustible gas detection through successive GB/GB/T standard implementations (2025-2026) and a hazardous chemical workplace systems standard issued in 2026 for later implementation. This creates an upgrade cycle for installed bases that need to meet newer performance and system requirements while keeping hazardous-area certification alignment (IECEx/ANZEx) for multi-jurisdiction operations.

Recent Industry Developments

- June 2026: Honeywell launched enhanced capabilities for its Safety Suite 2.0 industrial software, adding tools that help safety leaders track compliance, manage device inventory, and review historical alarm events from portable gas detectors in near real time. The update strengthens Honeywell's software-led differentiation by tying detector fleets to centralized safety workflows across utilities and chemical operations.

- March 2026: Honeywell introduced the 4-Series NDIR Hydrocarbon Gas Sensor designed for integration into fixed and portable gas detectors to detect flammable gases such as methane, propane, and butane while improving resistance to environmental poisoning. The sensor-level upgrade supports longer service intervals and more consistent field performance in harsh industrial settings, which can lower lifecycle costs for detector OEMs and end users.

- September 2025: MSA Safety launched the FieldServer ProtoNode Gateway in the Pacific-Asia region, enabling cloud-based remote monitoring and data visualization via MSA Grid for fixed gas and flame detector installations. This expands the addressable upgrade path for installed wired systems by adding connectivity and centralized oversight without requiring a full detector replacement program.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue earned from selling gas detectors across Asia Pacific, including fixed and portable devices, plus related communication features used to sense hazardous or combustible gases for safety monitoring.

Scope exclusions: This sizing excludes standalone gas analyzers used mainly for process measurement, and it also excludes installation-only services that are not bundled with the detector sale.

Segmentation Overview

- By Communication Type

- Wired

- Wireless

- By Detector Type

- Fixed

- Electrochemical

- Semiconductor

- Photo-ionization

- Catalytic

- Infra-red

- MEMS

- Portable and Transportable

- Multi-Gas

- Single-Gas

- Fixed

- By End-User Industry

- Oil and Gas

- Chemicals and Petrochemicals

- Water and Wastewater

- Metal and Mining

- Utilities

- Other End-User Industries

- By Country

- China

- Japan

- India

- South Korea

- Southeast Asia

- Australia and New Zealand

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

To set the market boundary and build the initial demand picture, we start with public sources that describe industrial activity and safety needs across the region. These typically include the International Labour Organization for safety and workforce context, national statistical offices in China, Japan, India, South Korea, and Australia for industry indicators, and trade data portals such as UN Comtrade for import and export patterns relevant to detection equipment. We also refer to standards and guidance bodies such as ISO and IEC, since detector performance requirements often follow these references.

The model is then grounded using supplier disclosures that are publicly available, including annual reports, regulatory filings, and investor presentations. These documents help capture product mix changes and regional exposure. Where we need additional cross-checking on company scale or patent activity, we use paid subscriptions for company financials and intelligence, news and financials, and patent databases, which helps fill gaps in smaller private disclosures without changing the scope definition. The desk sources listed here are not exhaustive, and other public documents and databases were also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Next, we validate assumptions through expert interviews and structured surveys across the value chain, covering manufacturers, distributors, system integrators, and large end users in industries such as oil and gas, chemicals, mining, and manufacturing. The input is used to confirm adoption patterns for fixed versus portable detectors, typical replacement cycles, and how communication features are specified in projects across major Asia Pacific countries.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 38% | CXOs: 15% | |

| Mid tier: 45% | Functional/Unit leaders: 28% | |

| Smaller Players: 17% | Managers: 57% |

Market-Sizing & Forecasting

The core sizing is built using a top-down approach where industrial output and facility activity are translated into a practical demand pool for gas detection, then filtered by adoption levels and replacement needs across the region. To keep the totals realistic, we corroborate results with selective bottom-up checks, such as sampled ASP times shipment proxies by detector type, plus channel conversations on annual order run rates.

A few inputs that matter most in this market include the installed base of fixed safety systems in process industries, the pace of greenfield and brownfield projects, portable detector replacement frequency, observed price bands by detector class, and the penetration of connected communication features in new tenders. When some local supplier revenue is not disclosed, it is bridged using peer ratios, distributor coverage checks, and country-level weighting that is subsequently reviewed in interviews.

For forecasting, scenario analysis is used with a base case that ties growth to industrial expansion, safety spending priority, and project cycles, and then the path is sanity-checked against how experts expect pricing and replacement timing to move over the next few years. The forecast is adjusted when expected shifts are confirmed, such as faster uptake in higher-risk end-user industries or a slower refresh cycle during capex pauses.

Data Validation & Update Cycle

Before numbers are finalized, outputs are triangulated across independent signals such as trade flow direction, supplier regional disclosures, and implied detector spend per facility type, then unusual jumps are flagged for review. If a country-level trend looks inconsistent with safety activity or project timing, we re-check assumptions, and respondents may be re-contacted to confirm whether the shift is real or a modeling artifact.

A multi-step analyst review is followed so that unit logic, currency conversion timing, and year-to-year movements are consistent across the model. Reports are refreshed annually, and interim updates are made when material events change demand expectations, such as large project delays, major regulatory actions, or notable pricing shifts. Right before delivery, a fresh pass is completed so clients receive the most current view available.

Mordor Intelligence's Asia Pacific Gas Detector Market Market Size Compared With Other Published Estimates

Published market values for gas detectors in Asia Pacific can differ because the product boundary is not always the same, and because analysts choose different ways to estimate volumes and average selling prices. Timing choices also matter, since some studies cite a base year, others cite the current year, and currency conversion dates are not always aligned.

Trade patterns for detection equipment, supplier regional revenue splits, and project-led demand signals from high-risk industries are used as evidence checks to keep the estimate anchored. These checks are applied to the 2026 value published by Mordor Intelligence. The biggest spread usually comes from whether gas leak detectors for residential use are included, and whether broader gas detection systems and installation services are counted as part of the market.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 681.02 M (2026) | |

| Trade Journal B | USD 1647.00 M (2024) | Uses a gas leak detector framing and an older forecast window, which can pull in broader safety purchases and make the scope less aligned to detector-only revenue in industrial settings. |

| Industry Newsletter A | USD 2100.00 M (2026) | Includes residential and commercial leak detection and often treats connected systems as a combined category, which can expand the counted value beyond detector device revenue alone. |

The table shows that the gap is mainly explained by scope, especially when leak detection in homes and bundled system components are added on top of industrial detector sales. By tying totals back to observable demand signals and then pressure-testing price and replacement assumptions in interviews, we end up with a number that is easier to trace and repeat year after year.

Key Questions Answered in the Report

What is the current value of the Asia Pacific gas detector market?

The market is valued at USD 681.02 million in 2026 and is projected to reach USD 936.56 million by 2031.

Which detector type is growing fastest in the Asia Pacific?

Portable multi-gas detectors are advancing at an 8.14% CAGR during the forecast period (2026-2031) due to heightened confined-space safety protocols.

Why are wireless gas detectors gaining traction?

Wireless systems cut installation labor, enable IIoT analytics, and support predictive maintenance, driving a 8.62% CAGR during the forecast period (2026-2031).

Which country leads demand for gas detectors in the Asia Pacific?

China holds the largest share at 35.25% in 2025 thanks to comprehensive industrial and municipal safety regulations.

What drives utilities-sector demand for detectors?

Expansion of power-generation capacity and hydrogen co-firing pilots push utilities toward integrated H? and combustible-gas monitoring.

Page last updated on: