Flame Detectors Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.75 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 4.19% CAGR |

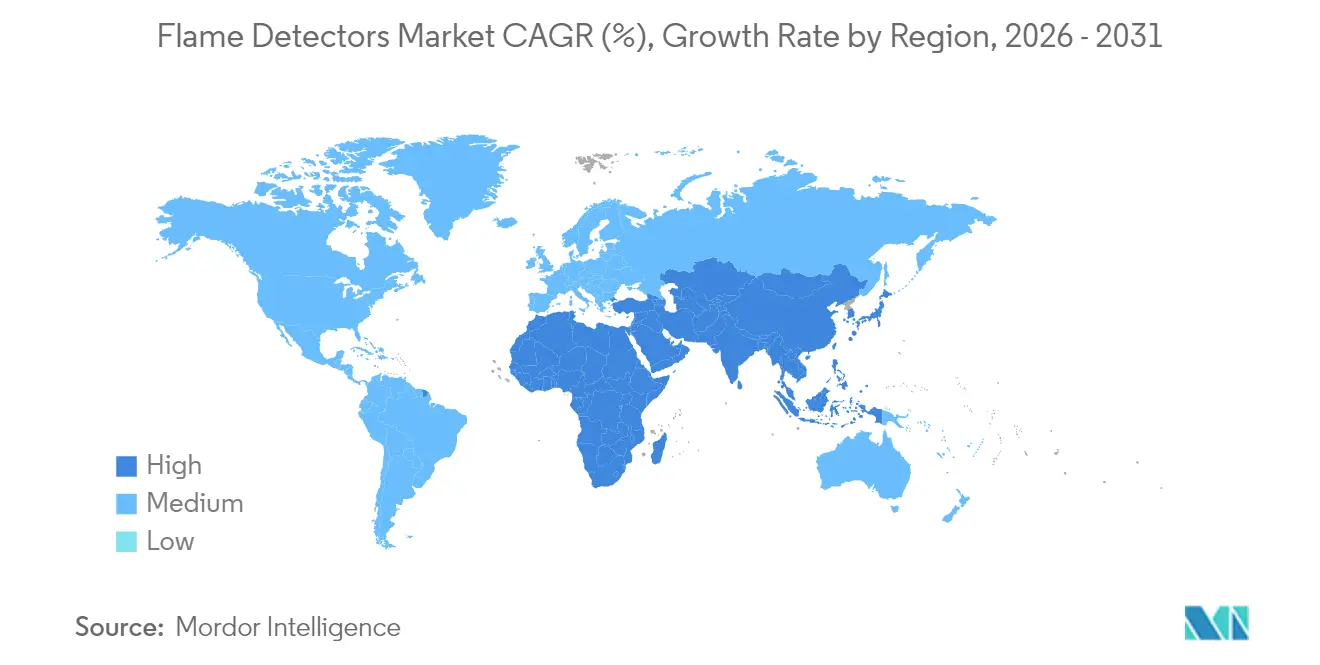

| Fastest Growing Market | Middle East |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Flame Detectors Market Analysis by Mordor Intelligence

Flame detector market size in 2026 is estimated at USD 1.75 billion, growing from 2025 value of USD 1.68 billion with 2031 projections showing USD 2.15 billion, growing at 4.19% CAGR over 2026-2031. A sizable installed base across hydrocarbon facilities will keep replacement demand steady, while new installations are shifting toward lithium-ion battery warehouses, data centers and green-hydrogen electrolyser plants where hydrogen flames create novel sensing challenges. Stricter global safety rules-most notably the latest ATEX Zone-0 update that elevates SIL-2 certification to a baseline requirement-are nudging buyers toward multi-spectrum infrared (IR) and AI-equipped visual imaging detectors that minimise nuisance alarms and downtime. LNG mega-train construction in Qatar and Saudi Arabia is broadening project pipelines and setting higher performance benchmarks that favour premium solutions. In parallel, North American insurance carriers are linking coverage terms to ultra-low false-alarm specifications, effectively steering procurement toward advanced, diagnostics-rich devices that lower both operational risk and total cost of ownership.

Key Report Takeaways

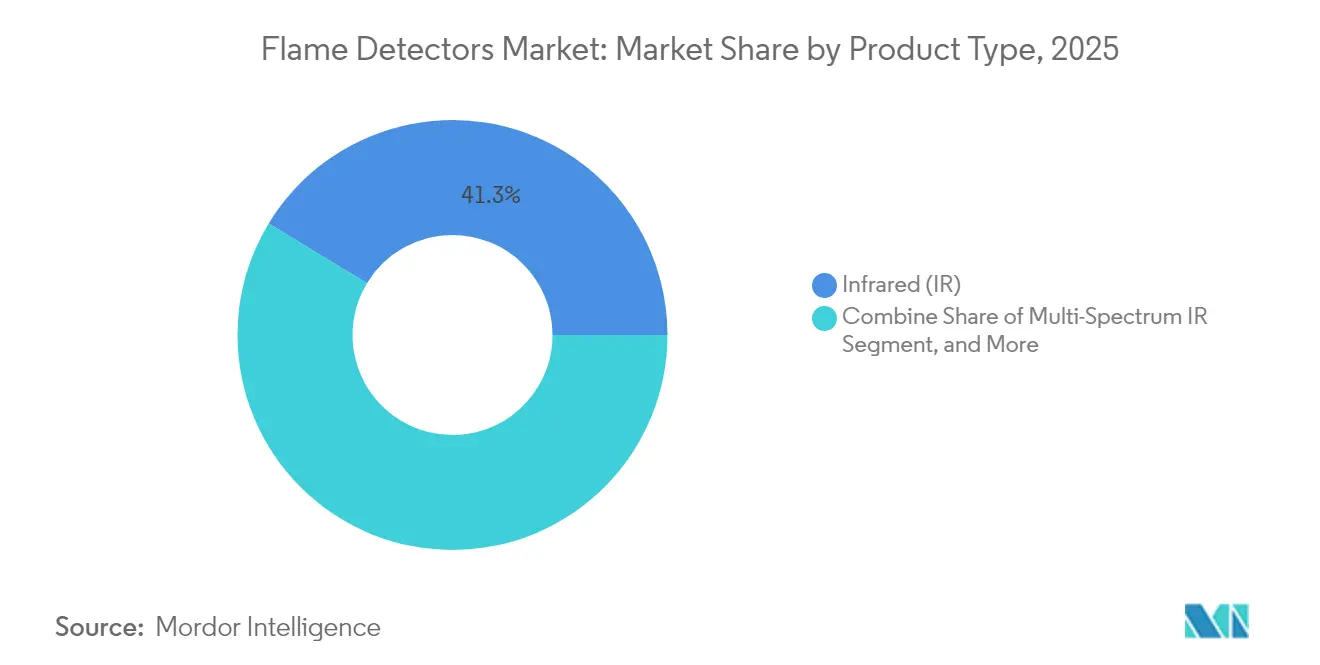

- By product type, infrared detectors led with 41.32% flame detector market share in 2025, while multi-spectrum IR units are forecast to post the fastest 5.02% CAGR through 2031.

- By mounting type, fixed devices commanded 86.05% revenue share in 2025; portable detectors are projected to expand at a 5.84% CAGR to 2031.

- By service, inspection, testing and maintenance captured 51.12% of the flame detector market size in 2025, whereas retrofit and replacement services show the highest 4.34% CAGR to 2031.

- By end-user industry, oil and gas held 36.64% revenue share in 2025, but warehousing and data centers are advancing at a 6.05% CAGR through 2031.

- By geography, North America represented 31.88% of 2025 revenues, while the Middle East is poised for the fastest 5.96% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Flame Detectors Market*

| Driver | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| LNG mega-train construction boosting multi-spectrum IR adoption | +0.80% | Middle East & North Africa with spillover to Asia-Pacific | Medium term (2-4 years) |

| Lithium-ion battery data-center demand under FM 5560 | +0.60% | North America & Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| ATEX and IECEx Zone-0 revisions mandating SIL-2 detectors | +0.50% | Europe with global replication | Long term (≥ 4 years) |

| Offshore FPSO retrofits adopting AI-enabled visual imaging | +0.40% | Brazil and North Sea, expanding to West Africa | Medium term (2-4 years) |

| Green-hydrogen electrolyser installations lifting UV/IR sales | +0.30% | Asia-Pacific core, early uptake in Japan and South Korea | Long term (≥ 4 years) |

| Insurance underwriting standards for ultra-low false alarms | +0.20% | North America with global influence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

LNG mega-train construction boosting multi-spectrum IR adoption

Middle Eastern LNG projects such as the North Field expansion and Jafurah gas development require detectors that can track hydrocarbon fires across wide separators and storage tanks. Plant owners are specifying multi-spectrum IR units to overcome solar radiation interference, a mandate that is elevating premium vendors with multi-band optical arrays and built-in diagnostics. Unmanned process areas reinforce the need for 99.9% device availability, and asset-integrity teams are migrating from time-based to condition-based maintenance models that rely on embedded health monitoring.

Lithium-ion battery data-center demand under FM 5560

FM 5560 now sets detection rules for energy-storage arrays, prompting hyperscale operators to retrofit existing sites with multi-criteria flame detectors that recognise electrolyte off-gas signatures before thermal runaway escalates. The 2024 International Fire Code adds NFPA 855 obligations, tightening compliance timelines for facilities exceeding 50 kWh of installed storage. System integrators are embedding AI classifiers that learn normal battery-module heat profiles to avoid spurious trips that may sideline revenue-critical compute clusters.

ATEX and IECEx Zone-0 revisions mandating SIL-2 detectors

The 2025 revision of the ATEX Directive 2014/34/EU removes legacy exemptions and requires SIL-2 certification in Zone-0 hazardous areas. Certification windows approach 36 months, tipping procurement toward established brands that already possess approved designs and creating an attractive retrofit backlog across European petrochemical and pharmaceutical complexes.

Offshore FPSO retrofits adopting AI-enabled visual imaging

Visual flame imaging paired with deep-learning analytics is cutting nuisance alarm rates by up to 60% on floating production, storage and offloading vessels operated by Petrobras and Equinor. Algorithms evaluate flame morphology and colour to distinguish flare stack activity from uncontrolled events, a vital capability in harsh North Atlantic and Brazilian environments where salt spray impairs UV/IR optics.

Restraints Impact Analysis of Flame Detectors Market*

| Restraint | (≈) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-cost Chinese IR cameras eroding premium revenue | -0.70% | Price-sensitive global markets | Short term (≤ 2 years) |

| Dirty-optics downtime limiting underground-mining uptake | -0.40% | Australia, South Africa, Chile | Medium term (2-4 years) |

| Lengthy FM & EN54-10 approval cycles delaying launches | -0.30% | Global | Long term (≥ 4 years) |

| Cybersecurity concerns over networked detectors | -0.20% | North America & Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Low-cost Chinese IR cameras eroding premium revenue

Thermal-imaging vendors from China are releasing IR flame detectors priced 40-60% lower than Western equivalents, gaining traction in mid-tier industrial sites that do not mandate SIL-2 ratings . [3]Hikvision, “2023 Annual Report,” hikvision.com Western manufacturers are countering with lifecycle cost models that monetise false-alarm reductions and longer service intervals.

Dirty-optics downtime limiting underground-mining uptake

In coal and hard-rock mines, dust accumulation on detector lenses demands weekly cleaning, lowering effective availability and raising labour costs. Operators often default to suppression-only strategies rather than installing optical detectors, limiting revenue upside in a sector otherwise prone to conveyor-belt and equipment fires.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Flame Detectors Market Segment Analysis

By Product Type:

Multi-Spectrum IR Drives Premium Segment GrowthInfrared devices captured 41.32% of 2025 revenue, underpinning the flame detector market with a long record of hydrocarbon-fire reliability. Adoption persists in refineries, terminals and petrochemical plants where users value proven single-channel optics. Yet the multi-spectrum IR sub-category is forecast to expand at 5.02% CAGR because it blends three or more wavelength bands to reject solar glare and hot-surface reflections. Operators in unmanned LNG trains see the higher capital spend as justifiable insurance against costly process shutdowns. Visual flame imaging is growing fastest as algorithms mature and price points fall, allowing simultaneous detection and root-cause analytics. UV detectors remain the niche solution for hydrogen or metal-combustion risks, while combined UV/IR units balance performance and cost in mixed-fuel installations.

In tandem, AI-ready sensor firmware is turning detectors into edge-computing nodes that self-diagnose lens obscuration and optical degradation. Remote firmware upgrades further shorten maintenance cycles. This trend is nudging engineering, procurement and construction (EPC) teams to specify cloud-connected devices despite cybersecurity reservations. The flame detector market benefits because predictive analytics underpin value-added service agreements that stretch beyond warranty periods, boosting aftermarket margins for manufacturers with integrated software roadmaps.

By Mounting Type:

Portable Growth Reflects Inspection IntensificationFixed detectors delivered 86.05% of 2025 billings and remain the backbone for continuous zone coverage in process areas, jetty off-loading points and compressor stations. Layouts rarely change over asset lifecycles, keeping demand tied to replacement and regulatory upgrades rather than greenfield projects. Portable detectors, however, are accelerating at a 5.84% CAGR as operators adopt test-before-touch safety procedures. Inspection teams validate fixed-system integrity during turnarounds without halting production, and first responders carry handheld units to quickly assess unknown scenes.

Battery density improvements have doubled mission time for portable devices while maintaining sensitivity parity with fixed platforms. Rugged enclosures and intrinsically safe ratings now enable safe use in Zone-1 locations. The result is a complementary relationship rather than a competitive one: rising portable uptake does not cannibalise fixed demand but instead banks additional revenue on every maintenance cycle. The flame detector market therefore gains two revenue streams from the same installed base: capital expenditure on fixed points and operational expenditure on portable verification equipment.

By Service:

Retrofit Segment Accelerates Amid Aging InfrastructureInspection, testing and maintenance accounted for 51.12% of 2025 service revenue, illustrating the market’s pivot from hardware supply to lifecycle support. Regulatory bodies increasingly require proof of detector performance integrity, and operators are outsourcing verification to OEM-trained technicians. Retrofits—spanning optical upgrades, smarter communication cards and SIL-2 certification replacements—are forecast for a 4.34% CAGR as industrial clients chase compliance deadlines under ATEX, IECEx and FM. Service providers are bundling cloud dashboards that log calibration drift, alarm events and environmental conditions, allowing predictive maintenance scheduling.

Design, installation and commissioning work retains a stable footing thanks to record LNG, data-center and green-hydrogen capacity additions. Yet the greatest margin upside now lies in five-year support contracts that guarantee mean-time-between-failures and embed consumables such as lens heaters and weather shields. The flame detector market is therefore evolving toward an annuity model where services may overtake hardware revenues near the end of the decade.

By Communication/Loop:

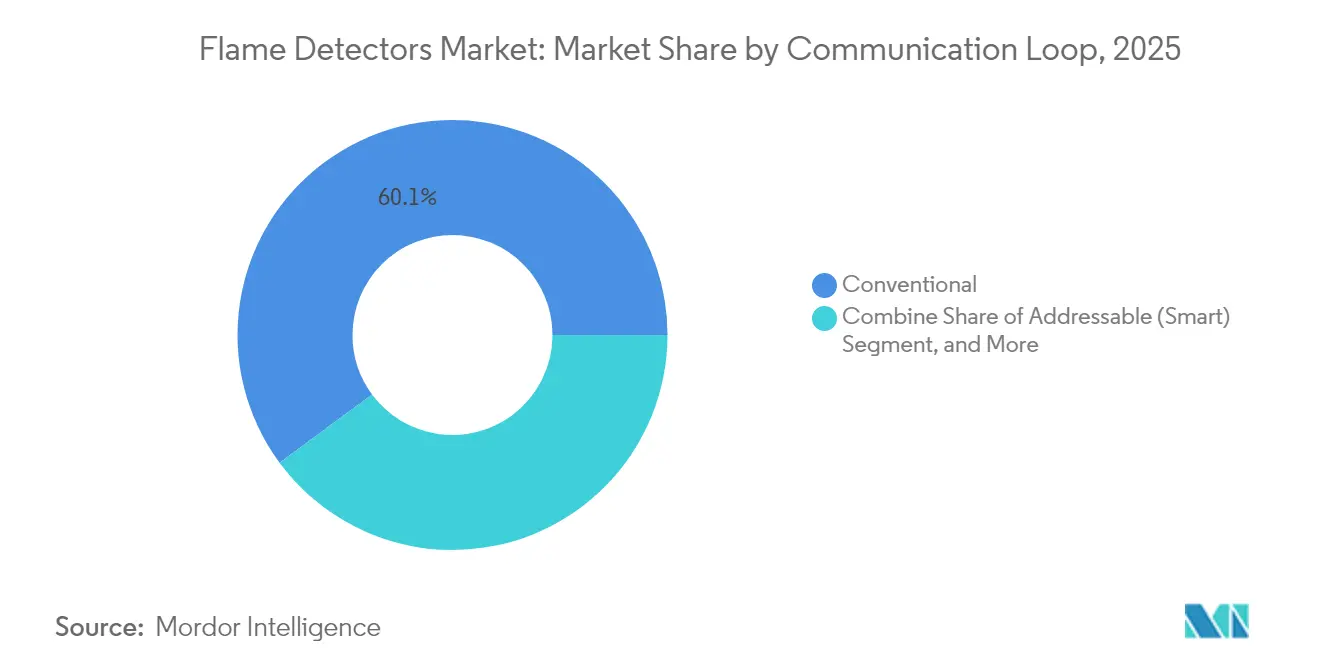

Smart Detectors Gain Despite Cybersecurity ConcernsConventional detectors still represented 60.12% of 2025 shipments because analog loops are rugged and easy to troubleshoot. Addressable smart detectors, with a forecast 6.74% CAGR, promise serialised device identification, continuous health polling and remote firmware updates. These capabilities reduce field visits and keep safety systems online. Facility owners weigh those benefits against new cyber-attack surfaces introduced by Ethernet or wireless protocols. Mitigation strategies include dedicated, air-gapped safety LANs and encryption under IEC 62443 guidelines.

Vendors now pre-install secure bootloaders and signed firmware, making tampering evident to control-room operators. Asset owners can then lock software versions through change-management processes. Successful deployments in North American chemical plants demonstrate that cybersecurity is a manageable variable rather than a deal-breaker, keeping smart devices on a growth trajectory that outpaces the overall flame detector market.

By End-User Industry:

Data Centers Challenge Oil & Gas DominanceOil and gas preserved a 36.64% revenue share in 2025 as flaring, loading and compressor facilities present sustained thermal-hazard density. Yet data centers and automated warehouses are advancing at 6.05% CAGR, propelled by lithium-ion battery racks that introduce fast-spreading fire dynamics. Hyperscale operators are reallocating capex from legacy smoke-only arrays to integrated flame and gas detection suites that recognise battery off-gas well before visible flame. Chemicals and petrochemicals maintain stable demand, driven by greenfield complexes in East Asia and mandatory upgrades in the European Union.

Manufacturing segments benefit from sensors that protect robotic lines where human vigilance is no longer the primary safety control. Aerospace and defense, while small in absolute size, require Class-A reliability ratings that command premium prices. Mining remains constrained by dust-management challenges, but field trials of sealed optical windows and air-purge systems could unlock latent demand by mid-decade.

Geography Analysis

North America Flame Detectors Market

North America led the flame detector market with 31.88% of 2025 revenue, supported by insurance mandates that link policy premiums to ultra-low false-alarm rates. Mature refining and chemical assets drive steady replacement cycles, and new rules under FM 5560 are expanding detector counts per facility. The region also pioneers addressable smart loops, backed by cybersecurity frameworks that assure underwriters and regulators of network resilience.

GCC Flame Detectors Market

The Middle East shows the highest 5.96% CAGR forecast to 2031 thanks to USD 200 billion in LNG expansions that require stringent flame supervision across train, storage and jetty areas. Harsh desert conditions favour stainless-steel housings, window heaters and optical diagnostics that predict sand abrasion. Successful deployments in Qatar are migrating to neighbouring GCC states, creating a technology lighthouse effect that shapes global specifications.

Europe, APAC and South America Flame Detectors Market

Europe continues to invest in detector retrofits to comply with the updated ATEX Zone-0 and SIL-2 mandates. Multinational petrochemical operators are standardising on the same certified model across global sites, amplifying replacement demand beyond the continent. Asia-Pacific’s growth rests on industrial electrification agendas, notably Japan and South Korea’s hydrogen roadmaps that elevate UV/IR detector counts in electrolyser halls.. South America’s offshore pre-salt finds need AI-enabled visual imaging to discriminate flare bundles from deep-sea production decks.

Competitive Landscape

Leading manufacturers Honeywell, Emerson and MSA Safety anchor the moderate-fragmentation profile through integrated fire-and-gas platforms that combine detectors, controllers and suppression systems. Continuous R&D investment is funnelled into multi-spectrum optics, AI classifiers and cyber-hardened firmware, translating into premium‐priced offerings that meet SIL-2 and FM certification without long approval lags. Honeywell’s earlier acquisition of Fire Sentry broadened its IR and UV/IR range, allowing cross-portfolio bundling in EPC bids. [2]Security Systems News, “Honeywell Acquires Fire Sentry,” securitysystemsnews.com

Chinese firms such as Hikvision and Jade Bird Fire are pushing commoditised IR solutions into price-sensitive markets. Their stepped-up pursuit of FM and ATEX approvals suggests future competition in higher-spec segments. Western incumbents respond with outcome-based service contracts that guarantee detector availability and tie penalties to unwanted trips, thereby reinforcing customer stickiness. White-space opportunities in hydrogen production and data-center energy storage are spurring niche specialists to design purpose-built optics and filters.

Lifecycle services are turning into the core battleground. Vendors now offer five-year inspection bundles with cloud dashboards that flag optical contamination and spectral-filter decay. The flame detector market is thus tilting toward solutions that wrap hardware, analytics and support into a single procurement line. This integrative approach poses a barrier to new entrants who can offer sensors but not the full spectrum of compliance and maintenance capabilities.

Flame Detectors Industry Leaders

Honeywell International Inc.

Emerson Electric Co. (Det-Tronics and Spectrex)

Johnson Controls plc (Tyco/Kidde)

MSA Safety Incorporated

Siemens AG

- *Disclaimer: Major Players sorted in no particular order

Flame Detectors Market Companies Covered in this Report

- Honeywell International Inc.

- Emerson Electric Co. (Det-Tronics, Spectrex)

- Johnson Controls plc (Tyco)

- MSA Safety Inc.

- Siemens AG

- Bosch Security Systems B.V.

- Drägerwerk AG and Co. KGaA

- Teledyne Gas and Flame (Simtronics, Oldham)

- 3M Co. (Scott Safety)

- Micropack Engineering Ltd.

- FLIR Systems (Teledyne)

- Hochiki Corporation

- Crowcon Detection Instruments Ltd.

- Fike Corporation

- Minimax Viking GmbH

- Firefly AB

- Sense-WARE Fire and Gas Detection B.V.

- Omniguard Flame Detectors

- General Monitors (now part of MSA)

- Kidde Fire Safety (Carrier)

Recent Industry Developments in Flame Detectors Market

- January 2025: Warringtonfire opened a USD 30 million fire-resistance test laboratory at Birchwood Park that triples certification capacity and shortens approval queues for flame detectors

- July 2024: Johnson Controls agreed to sell its Residential and Light Commercial HVAC division to Bosch for USD 8.1 billion, freeing capital for industrial fire-safety growth

- June 2024: Sentinel Capital Partners carved out Carrier’s industrial fire unit, forming Spectrum Safety Solutions with 1,400 staff and Autronica’s detector portfolio

- June 2024: Halma bought Global Fire Equipment for EUR 42.5 million to deepen its international detection presence

Flame Detectors Market Report Scope and Research Methodology

Market Definition and Coverage

Our study defines the flame detectors market as revenues generated from new, stand-alone optical flame sensors, including UV, IR, UV/IR, multi-spectrum IR, and visual imaging units that are factory-calibrated, certified for hazardous or general industrial areas, and sold with or without mounting hardware. These devices trigger alarms or suppression systems across oil and gas, chemicals, power, metals, mining, aerospace, warehousing, and public infrastructure settings.

Scope exclusion: Modules embedded only inside larger OEM machines (for example, turbine combustor scanners or missile guidance sensors) are not counted here.

Segments Covered in This Report

- By Product Type

- Ultraviolet (UV)

- Infrared (IR)

- Ultraviolet/Infrared (UV/IR)

- Multi-Spectrum IR (Triple/Quad)

- Visual Flame Imaging

- Combined Gas and Flame Detectors

- By Mounting Type

- Fixed Flame Detectors

- Portable/Hand-held Flame Detectors

- By Service

- Design, Installation and Commissioning

- Inspection, Testing and Maintenance

- Retrofit and Replacement

- By Communication/Loop

- Addressable (Smart) Detectors

- Conventional Detectors

- By End-User Industry

- Oil and Gas (Up-, Mid-, Down-stream)

- Chemicals and Petrochemicals

- Energy and Power Generation

- Manufacturing and Process Industries

- Mining and Metals

- Aerospace and Defense

- Warehousing, Logistics and Data-Centers

- Marine and Offshore

- Commercial and Public Infrastructure

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Nordics

- Rest of Europe

- South America

- Brazil

- Rest of South America

- Asia-Pacific

- China

- Japan

- India

- South-East Asia

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Gulf Cooperation Council Countries

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- Middle East

- North America

Data Sources, Market Sizing, and Validation

Primary Research

We then interview engineering leads at EPC contractors, safety officers at onshore terminals, mining maintenance heads, and regional fire-code inspectors across North America, Europe, the Gulf, and Asia-Pacific. These discussions test lifespan assumptions, typical detector density per hectare, and attainable average selling prices before we finalize any model pivots.

Desk Research

Our analysts first map the installed base and new build pipeline by drawing on open, high-credibility records such as OSHA and NFPA incident logs, Eurostat PRODCOM sensor shipments, UNECE industrial production data, API refinery statistics, and regional fire-safety association audits. Company 10-Ks, investor decks, and trade-show white papers add pricing and technology refresh cues, while patent analytics from Questel reveal emerging multi-spectrum designs.

To size replacement demand, we reference tender portals like Tenders Info, customs records from Volza, and facility upgrade case notes published by the Chemical Safety Board. Subscription resources, D&B Hoovers for vendor revenues and Dow Jones Factiva for deal flow, round out the desk work. The sources cited are illustrative, not exhaustive; many additional public and paid datasets guide our validation steps.

Market-Sizing & Forecasting

A top-down construct begins with global hazardous-area facility counts, which are multiplied by penetration rates for each industry cohort and refined with retrofit cycles evident from maintenance contracts. Select bottom-up checks, supplier revenue roll-ups and channel ASPx volume probes, alert us to over- or under-shoots. Key variables feeding the model include upstream CAPEX trends, refinery turnaround schedules, regulatory compliance deadlines, detector ASP learning curves, industrial production indices, and fire incident ratios. Forecasts employ multivariate regression blended with scenario analysis so shocks in oil prices or code revisions flow through logically. Gaps in granular bottom-up data are bridged with conservative midpoint estimates that our senior reviewers must approve.

Data Validation & Update Cycle

Outputs face three-stage variance checks, peer review, and a last-minute news scan. Mordor refreshes every twelve months, but extraordinary recalls, code amendments, or mergers trigger an interim revision so clients always receive a current baseline.

How Mordor Intelligence's Flame Detectors Market Size Compares to Other Published Estimates

Published figures seldom align because each firm tweaks scope, currency year, and refresh rhythm. Our team discloses definitions upfront, applies uniform exchange rates, and time-stamps every datapoint, which shields users from hidden inflation or currency drifts.

Key gap drivers arise when others bundle flame sensors with broader fire detection kits, apply optimistic retrofit cycles, or freeze pricing over the forecast horizon, whereas Mordor Intelligence factors certified device ASP erosion and phased compliance uptake.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.68 B (2025) | Mordor Intelligence | - |

| USD 1.70 B (2022) | Global Consultancy A | Older base year and omits portable units, inflating share of fixed devices |

| USD 0.98 B (2023) | Trade Journal B | Counts only semiconductor and electronics clients, excludes oil and gas retrofit pool |

| USD 1.78 B (2023) | Industry Portal C | Includes integrated sensor modules and ancillary flame-gas combos |

In sum, differences stem less from arithmetic and more from scope discipline, input transparency, and update cadence. By grounding every step in verifiable variables and a documented review chain, Mordor's numbers give decision-makers a balanced, repeatable baseline they can trust.

Key Questions Answered in the Report

What is the current size of the flame detector market?

The flame detector market size reached USD 1.75 billion in 2026 and is projected to grow to USD 2.15 billion by 2031.

Which region will grow fastest through 2031?

The Middle East leads with a forecast 5.96% CAGR thanks to USD 200 billion in LNG mega-train investments that require advanced flame monitoring.

Why are multi-spectrum IR detectors gaining traction?

Multi-spectrum IR devices analyse several wavelength bands simultaneously, cutting false-alarm rates in sunny or hot industrial environments and meeting new insurance and ATEX Zone-0 requirements.

How are lithium-ion battery installations affecting market demand?

Data centers and warehouses with energy-storage systems must comply with FM 5560 and NFPA 855, driving adoption of smart flame detectors capable of detecting electrolyte off-gas before thermal runaway escalates.

Page last updated on: