Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

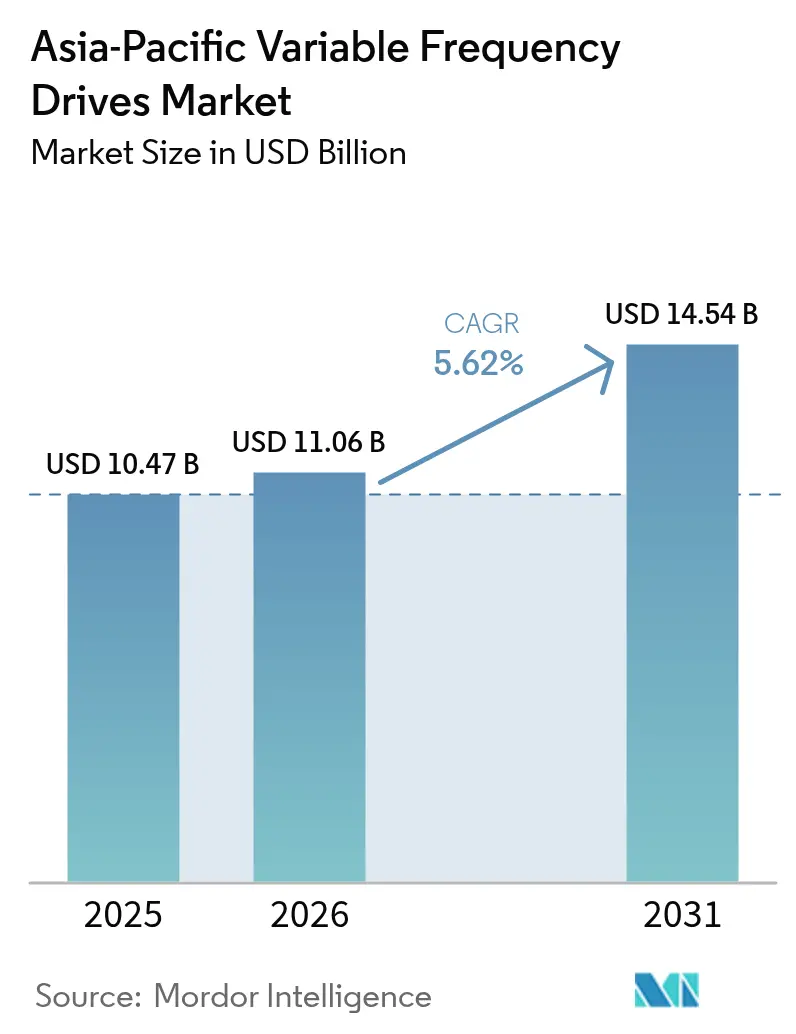

| Base Year Market Size (2025) | USD 10.47 Billion |

| Market Size (2026) | USD 11.06 Billion |

| Market Size (2031) | USD 14.54 Billion |

| Growth Rate (2026 - 2031) | 5.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Variable Frequency Drives Market Analysis by Mordor Intelligence

Asia-Pacific variable frequency drives market size in 2026 is estimated at USD 11.06 billion, growing from 2025 value of USD 10.47 billion with 2031 projections showing USD 14.54 billion, growing at 5.62% CAGR over 2026-2031. Rising electricity tariffs, decarbonization policies, and the expanding automation base are steering capital toward energy-saving motor control, creating a sizeable addressable market for Variable Frequency Drives (VFD) retrofits and new installations. Precision HVAC requirements in hyperscale data centers, together with stricter power-usage-effectiveness (PUE) limits, are boosting demand for high-performance drives in cooling loops. Wide-bandgap semiconductors, especially silicon-carbide MOSFETs, are increasing drive efficiency by as much as 50%, thereby shortening the payback periods for energy-efficiency upgrades. Competition remains moderate; global brands defend premium niches, while Chinese and Taiwanese rivals undercut prices in low-power ranges, intensifying margin pressure. Governments across China, India, and Southeast Asia are now linking procurement incentives to minimum-efficiency standards, favouring suppliers able to certify compliance under the latest IEC classification for high-voltage motors.

Key Report Takeaways

- By type, AC drives led with 73.40% revenue share in 2025, while servo drives are projected to expand at an 8.02% CAGR through 2031.

- By voltage class, low-voltage units captured 86.90% of the Asia-Pacific variable frequency drives market share in 2025; medium-voltage models are forecasted to record the highest CAGR at 6.85% from 2026 to 2031.

- By power rating, the >200 kW class is expected to grow at a 8.55% CAGR between 2026 and 2031.

- By application, pumping systems accounted for 30.40% of the Asia-Pacific variable frequency drives market size in 2025; HVAC is projected to advance at an 8.25% CAGR through 2031.

- By end-user, the oil and gas sector accounted for a 22.05% share of the Asia-Pacific variable frequency drives market size in 2025, while the water and wastewater treatment sector is projected to rise at a 9.02% CAGR through 2031.

- By country, china commanded 43.25% of 2025 turnover, propelled by its vast manufacturing network and the 2024 NDRC expansion of mandatory efficiency lists. India is the fastest climber at a projected 9.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Variable Frequency Drives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Government-led Industrial Energy-Efficiency Mandates in China and India | +1.80% | China, India, with spillover effects to ASEAN |

| Manufacturing-Sector Automation Wave Post-2023 | +1.20% | APAC-wide, strongest in China, South Korea, Japan |

| Rising Electricity Tariffs Prompting Energy-Saving Retrofits | +0.90% | India, Australia, Singapore, Malaysia |

| Rapid Build-out of Data Centres Requiring Precision HVAC Drives | +1.40% | Singapore, Japan, China, India, Australia |

| Infrastructure Boom in Southeast Asia Boosting Pumps and Fans Demand | +0.70% | Indonesia, Vietnam, Thailand, Philippines |

| Shift to Electric Propulsion in Mining and Marine Equipment | +0.50% | Australia, Indonesia, South Korea |

| Source: Mordor Intelligence | ||

Government-Led Industrial Energy-Efficiency Mandates in China and India

National regulations now tie industrial upgrades to quantified energy-performance targets. China’s 2024 specification expansion to 23 product categories obliges factories to adopt premium-efficiency motors and matching drives, prompting a step-change in retrofit volumes.[1]TUV SUD, “China: Announcement (2024) Edition on Energy Efficiency Specifications,” tuvsud.com New Delhi’s budget sets aside INR 6,500 crore (USD 780 million) to solarize 3.5 million irrigation pumps, directly embedding VFDs into distributed renewable systems. These measures, aligned with China’s 2060 carbon-neutrality goal and India’s renewable energy push, are cascading through supply chains, prompting local OEMs to certify IEC-compliant, sensor-rich drives at scale. Vendors able to prove 20-40% electricity savings now enjoy priority listing in government procurement.

Rapid Build-Out of Data Centers Requiring Precision HVAC Drives

Asia Pacific data-center capex is projected to surpass USD 75 billion by 2025, overtaking North America.[2]Siemens Press Center, “Siemens Strengthens Data Center Presence with New Center of Competence for APAC,” press.siemens.com Server-densification elevates thermal loads, so operators are shifting from fixed-speed chillers to VFD-based cooling loops. PUE mandates in Beijing and Singapore encourage dynamic airflow control, and silicon-carbide power stages are cutting HVAC energy draw by up to 17% annually. Drives with embedded fieldbus and cyber-secure firmware enable real-time feedback to building-management systems, turning cooling from a cost center into a performance variable.

Manufacturing-Sector Automation Wave Post-2023

Factory owners across Asia-Pacific are replacing legacy starters with vector-controlled VFDs to synchronize with robot cells and IIoT dashboards. Integration with real-time Ethernet protocols allows predictive maintenance based on drive telematics, reducing unscheduled downtime. Journal research confirms that sensorless vector control in low-power AC drives trims energy use by 50% in variable-load machines.[3]MDPI, “Leveraging Variable Frequency Drive Data for Nondestructive Testing Applications,” mdpi.com Automation budgets, buoyed by reshoring and supply-chain resilience plans, prioritize drives as foundational components of digital twins.

Rising Electricity Tariffs Prompting Energy-Saving Retrofits

Between 2024 and 2025, industrial tariffs increased by 7-15% in India, Australia, and Singapore. CFOs responded by fast-tracking payback-positive projects such as VFD retrofits on pumps, fans, and compressors, each capable of 25-40% energy reduction. Finance teams now view premium-efficiency drive packages as a risk mitigation strategy against future energy price volatility. Utilities in Australia have introduced demand-response rebates, further shortening the return period for retrofits.[4]International Energy Agency 4E, “Policy Development on Energy Efficiency of Data Centres,” iea-4e.org

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance |

|---|---|---|

| Price Competition from Low-Cost Chinese Vendors | -0.80% | APAC-wide, strongest in price-sensitive markets like India, Indonesia |

| Harmonic and EMI Compliance Challenges in Medium-Voltage Drives | -0.50% | Japan, South Korea, Singapore, Australia |

| Subsidy Withdrawal for Industrial Efficiency Projects in Australia | -0.30% | Australia, New Zealand |

| Skilled Workforce Shortage for VFD Commissioning in ASEAN | -0.60% | Indonesia, Malaysia, Thailand, Philippines, Vietnam |

| Source: Mordor Intelligence | ||

Price Competition from Low-Cost Chinese Vendors

Aggressive pricing from Inovance, Hiconics, and other Chinese suppliers erodes margins for premium brands, particularly in the <40 kW bracket. With support from Beijing’s green-industrial policy, these firms price 15-25% below global averages. While customers enjoy lower capex, a race-to-the-bottom threatens long-term R&D funding for advanced topologies and cybersecurity features. Tier-one players are countering by bundling drives with digital service contracts and extended warranties, repositioning themselves on lifecycle value rather than upfront cost.

Skilled Workforce Shortage for VFD Commissioning in ASEAN

Rapid industrial development in Indonesia, Vietnam, and Thailand has outpaced the technical training pipelines. Incorrect parameterization or poor harmonic-filter sizing can negate promised energy savings, dampening word-of-mouth adoption. OEMs are releasing wizard-driven setup software and offering cloud-based remote commissioning; however, these tools only partially offset the technician gap. Industry associations are lobbying for the inclusion of advanced motor-control modules in vocational curricula to sustain growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: AC Dominance Persists While Servo Surges

AC drives retained a 73.40% command of 2025 revenues, anchored by their versatility across pumps, fans, and conveyors. The Asia-Pacific variable frequency drives market size for servo units is forecast to jump at an 8.02% CAGR as robotics, CNC machining, and collaborative cobots proliferate. Lifecycle economics favour AC units in constant-torque uses, but the servo’s higher price premium is justified by positional accuracy within ±0.01°. In the current cycle, servo adoption is strongest in electronics assembly lines of South Korea and Japan. Silicon-carbide power stages and embedded encoders now enable microsecond-level feedback, reducing overshoot and scrap rates. As OEMs miniaturize machinery, board-mount drives and PCB stator motors are shrinking cabinet footprints, enabling retrofit into crowded factory floors.

Service models are also diverging. AC drives typically ship with five-year warranties and basic monitoring, while servo packages bundle cloud dashboards that track torque ripple and vibration. Suppliers are upselling maintenance-as-a-service contracts that utilize algorithms to predict bearing wear weeks in advance. This shift from transactional sales to recurring revenue is reshaping channel incentives across the Asia-Pacific variable frequency drives market.

By Voltage Class: Low-Voltage Prevalence, Medium-Voltage Acceleration

Low-voltage systems <690 V command 86.90% of 2025 shipments, a reflection of the region’s concentration of small to mid-sized motors. Yet, the medium-voltage segment is expanding at a forecasted 6.85% CAGR as petrochemical complexes, desalination plants, and metro-rail projects scale up pump duties. IEC’s first-ever efficiency grading for high-voltage motors has prompted EPC contractors to integrate active-front-end configurations to comply with THD limits. The Asia-Pacific variable frequency drives market share for air-cooled medium-voltage packages is growing in markets where ambient temperatures exceed 40°C, prompting vendors to develop derating-resistant heat-sink alloys.

Product strategy is converging on modular building blocks. Drawer-style power cells simplify field replacement; digital twins simulate harmonic interaction with weak grids, reducing commissioning time by 20%. Low-voltage platforms continue to innovate with regenerative braking and STO (Safe Torque Off) functions, catering to intralogistics and warehousing clients adopting automated guided vehicles.

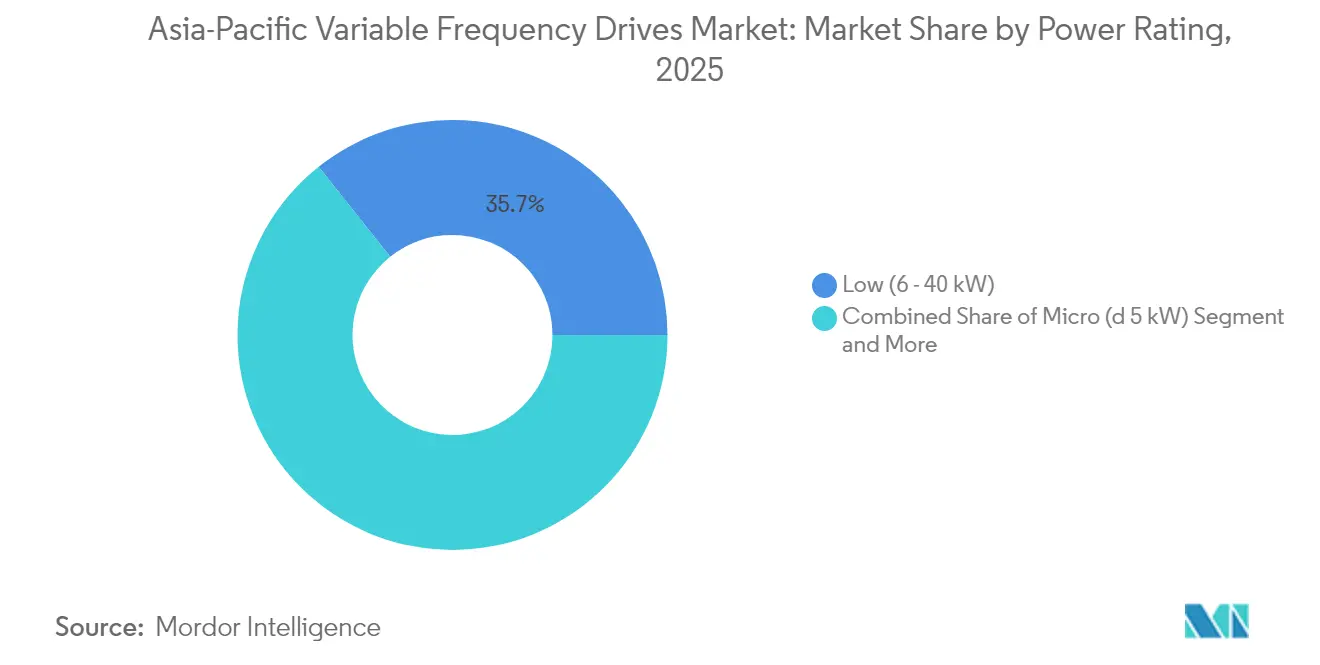

By Power Rating: Low kW Dominance, High kW Acceleration

The 6-40 kW bracket delivered 35.70% of 2025 revenues, supported by economies of scale in commercial HVAC and municipal pumping. However, units exceeding 200 kW exhibit the fastest 8.55% CAGR, as mining conveyors, rolling mills, and district cooling plants modernize. The Asia-Pacific variable frequency drives market size for high-power liquid-cooled variants is increasing, where space constraints intersect with stringent acoustic limits, notably in underground metro stations. Explosion-proof enclosures certified to IECEx Zone 1 are gaining traction in offshore rigs, with smart pressure sensors enabling non-intrusive condition monitoring.

At the opposite end, micro-drives with a capacity of ≤5 kW are finding new homes in smart buildings. These DIN-rail units interface over BACnet with occupancy sensors, adjusting fan speeds in real-time. Mid-range 41-200 kW systems remain a workhorse for industrial compressors and blowers, and vendors are layering AI chipsets to balance multiple drives on a common DC bus, shaving peak load charges.

By Application: Pumps Lead, HVAC Speeds Up

Pump duties generated 30.40% of the 2025 turnover, thanks to their omnipresence in water transfer, slurry handling, and irrigation. Soft-start capability curbs water hammer, extending pipe life. VFD retrofits on municipal pump stations have yielded energy savings of 25-35% and shortened maintenance intervals from quarterly to semiannual. Conversely, HVAC registers the highest 8.25% CAGR as data centers and green-building codes escalate airflow precision. Drives with fire-mode override now satisfy life-safety regulations while still delivering variable speed in normal operation.

Compressor installations, spanning ammonia refrigeration to PET bottle blowing, value drives for discharge-pressure trim, cutting energy waste during partial load. Fan systems in road tunnels and metros exploit VFDs to adapt airflow to CO and NOx readings, reducing energy overhead during off-peak traffic. Extruders in plastics benefit from torque-boost functions that maintain uniform melt viscosity. Conveyor and crane drives are increasingly integrating torque-proving routines to prevent load slip, which is critical in automated warehouses.

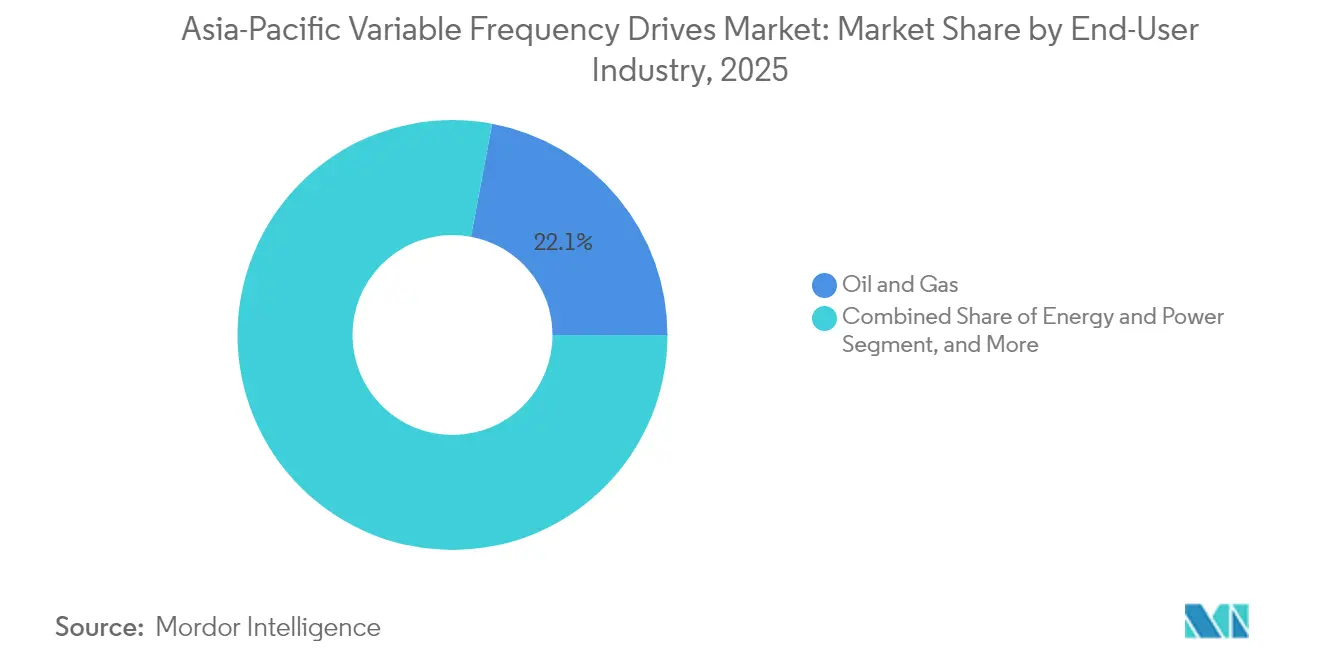

By End-User Industry: Oil and Gas Leads, Water Treatment Surges

Oil and gas entities held a 22.05% share, driven by downstream refinery upgrades and upstream artificial-lift electrification. VFDs enable stepless speed control of progressive-cavity pumps, reducing flaring volumes and lowering scope-1 emissions. The Asia-Pacific variable frequency drives market size in water and wastewater treatment is on a 9.02% CAGR trajectory as megacities overhaul aged infrastructure. Drives aid variable-flow filtration, reducing membrane fouling and chlorine consumption.

Power utilities deploy VFDs in FGD scrubber pumps and induced-draft fans; co-location with renewables creates a need for low-harmonic, grid-friendly designs. Food and beverage processors are embracing wash-down rated stainless-steel drives, which minimize bacterial harborage. Metals and mining operations rely on sensor fusion within high-power drives to smooth torque on crushing mills, improving throughput. The marine segment, spurred by IMO’s 2030 carbon intensity targets, is pivoting to electric propulsion with VFD-fed permanent-magnet thrusters.

Geography Analysis

China commanded 43.25% of 2025 turnover, propelled by its vast manufacturing network and the 2024 NDRC expansion of mandatory efficiency lists. Provincial subsidies reward factories that meet top-tier efficiency grades, resulting in bulk tenders for tens of thousands of low-voltage drives each quarter. Domestic innovators, such as Zhejiang Yongfa Electromechanical, are patenting permanent-magnet integrated motor-drive systems that claim 96% efficiency, thereby tightening local competition. Beijing’s dual-carbon targets anchor a predictable policy runway, encouraging multinational OEMs to localize assembly to circumvent tariff volatility.

India is the fastest climber at a projected 9.38% CAGR. Government solar-pump schemes inject a steady volume into the ≤5 kW class, while Make in India incentives help Delta Electronics and Fuji Electric deepen localization. Industrial corridors, such as Delhi-Mumbai, are installing regenerative drives on automated storage and retrieval systems, leveraging time-of-day tariffs to maximize energy exports to the grid. Skill-development partnerships are emerging between drive manufacturers and polytechnic institutes to bridge commissioning engineer shortages.

Japan and South Korea maintain high unit values through advanced semiconductor, automotive and battery plants that demand tight torque control. Both countries champion harmonics-compliant medium-voltage fleets, fostering local champions such as LS Electric. Singapore’s data-center capacity, already topping 1.6 GW, propels demand for silicon-carbide drives in chilled-water loops. In Southeast Asia, Indonesia and Vietnam benefit from infrastructure megaprojects; VFD-ready pumping packages are baked into tender specs for new metro lines and flood-control canals. Australia and New Zealand’s proposed step-up to IE4 motor standards by 2029 signals a pending surge in retrofit activity, though subsidy phase-outs temper immediate adoption.

Regulatory Landscape

Across Asia-Pacific, variable frequency drives (VFDs) are shaped by national electrical safety and performance requirements, alongside cross-border IEC alignment for power drive systems. The IEC 61800 series provides the reference framework for safety and functional requirements (for example, IEC 61800-5-1:2022), as well as for EMC and energy-efficiency assessment, giving multinational suppliers a common compliance baseline across APAC markets.

China has tightened its national standard set for drives and related motor-control equipment through the State Administration for Market Regulation (SAMR). SAMR issued GB/T 14048.6-2025 and GB/T 14048.12-2025 on October 31, 2025, with implementation from May 1, 2026, covering requirements for semiconductor motor controllers and contactors used in drive systems. China also updated VFD technical conditions and test methods effective July 1, 2025 through GB/T 30844.1-2024 and GB/T 30844.2-2024 for low-voltage drives (1 kV and below), and GB/T 30843.1-2024 for medium-voltage drives (>1 kV to 35 kV). This raises the rigor of qualification and type testing for suppliers targeting industrial projects and government-linked procurement. In India, the Ministry of Heavy Industries published the Machinery and Electrical Equipment Safety (Omnibus Technical Regulation) Order, 2024 on August 28, 2024, steering machinery and electrical equipment toward unified safety compliance based on IS 16819:2018 and international standards, which increases documentation and conformity expectations for drive OEMs and importers serving Indian industrial end users.

Competitive Landscape

The market is moderately fragmented with a three-tier hierarchy. Top-tier multinationals (ABB, Siemens, Mitsubishi Electric, Schneider Electric) leverage end-to-end portfolios plus global service footprints. Mid-tier regionals (Delta Electronics, Fuji Electric, LS Electric) focus on localized firmware and channel intimacy. A long tail of niche specialists targets micro-drives or harsh-duty SKUs. Strategic differentiation is shifting from raw efficiency to digital intelligence. ABB embeds MQTT brokers, Siemens layers edge analytics, and Mitsubishi integrates AI chips that learn load patterns in under five duty cycles.

Wide-bandgap semiconductors represent a disruptive input; Onsemi’s EliteSiC SPM 31 module sliced annual fan energy in data centers by 52%. Component makers, such as Infineon and Wolfspeed, are thus becoming key influencers in the ecosystems. Joint development agreements between drive OEMs and chip vendors are reducing design cycles and securing supply. Service models evolve toward subscription analytics; Schneider Electric’s EcoStruxure Connect Box streams motor health data into cloud dashboards, turning drives into IoT sensors.

Regional price pressure persists in the market studied. Chinese challengers bundle free IIoT gateways and undercut on volume, forcing global brands to defend with extended warranties and firmware-secure supply chains. Intellectual-property enforcement remains uneven, prompting premium players to integrate tamper-detection circuits. The new IEC efficiency standard for high-voltage motors raises the bar, and vendors already meeting IE4 can seize first-mover advantage in retrofit-heavy petrochemical hubs.

Asia-Pacific Variable Frequency Drives Industry Leaders

ABB Ltd.

Siemens AG

Mitsubishi Electric Corporation

Schneider Electric SE

Fuji Electric Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Large-scale energy-efficiency programs and tighter minimum energy performance approaches across APAC keep the retrofit pool active, especially where pump, fan, and compressor fleets still rely on fixed-speed starters. China continues to apply GB/T 12668.901-2021 and GB/T 12668.902-2021 alongside the IEC 61800-9-1/9-2 ecodesign measurement methods, and MEPS-style toolkits for electric motor systems are promoted regionally through initiatives such as United for Efficiency (U4E). This supports opportunities for vendors that can package verifiable system-level savings, covering the motor, VFD, and controls, while also providing compliance-ready test documentation for both low-voltage and medium-voltage installations.

A second opportunity is the shift from speed control to intelligent, networked drives, which can be easier to commission and maintain in environments facing skills constraints. In 2026, Mingchuang Electric highlighted integration pathways for wide-bandgap power devices, edge computing, and AI methods in VFD architectures for smart manufacturing. That emphasis supports demand for compact, higher-efficiency power stages and firmware capabilities for diagnostics and industrial connectivity. It also aligns with buyers in regulated, uptime-sensitive applications, including data-center HVAC loops and municipal water infrastructure, where standardization is increasing for drives with embedded monitoring, cybersecurity-aware connectivity, and serviceable digital tools, allowing suppliers to compete on lifecycle services rather than only unit price.

Recent Industry Developments

- June 2026: Mitsubishi Electric announced joint development with Semikron Danfoss of a new LV100-type standard package for power modules intended for industrial drive equipment. The work targets more standardized, compact, and manufacturable power stages, influencing inverter availability and design cycles for VFD OEM platforms across industrial automation.

- October 2025: ABB India expanded local production capacity for energy-efficient drives by 25% at its Peenya, Bengaluru facility. The added output supports shorter lead times and localization requirements tied to industrial efficiency programs, strengthening ABBs ability to serve price-competitive tenders and retrofit projects in India.

- May 2024: Fuji Electric disclosed an investment program focused on strengthening manufacturing capabilities for power electronics and related products used in industrial systems. The move supports supply assurance for inverter-driven equipment and helps enable higher-volume delivery into APAC factory automation and infrastructure demand cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market is defined as revenues generated from variable frequency drives used to control electric motor speed and torque across Asia-Pacific, counted in value terms at the point of sale into end users and projects.

Scope exclusions: Excludes regions outside Asia-Pacific and non-drive items such as standalone motors, motor starters, and unrelated power electronics that are not sold as VFDs.

Segmentation Overview

- By Type

- AC Drives

- DC Drives

- Servo Drives

- By Voltage Class

- Low-Voltage (More than 690 V)

- Medium-Voltage (1 - 35 kV)

- By Power Rating (kW)

- Micro (Less than 5 kW)

- Low (6 - 40 kW)

- Medium (41 - 200 kW)

- High (More than 200 kW)

- By Application

- Pumps

- Fans

- Compressors

- Conveyors

- HVAC

- Extruders

- Others

- By End-User Industry

- Oil and Gas

- Energy and Power

- Water and Waste-water Management

- Food and Beverage Processing

- Pulp and Paper

- Metals and Mining

- Chemicals and Petrochemicals

- Marine and Shipbuilding

- Other Industries

- By Country

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by mapping where VFD demand typically shows up, then tying it back to measurable signals in industry and country data. We reviewed public sources such as International Energy Agency energy efficiency and electricity consumption series, UN Comtrade trade statistics for drive-related HS codes, International Electrotechnical Commission standards references, and country industrial output releases from national statistics offices in major APAC economies.

To keep assumptions grounded, we also used company annual reports and investor presentations, association websites covering motor systems and industrial automation, and reputable press coverage of capacity additions in power, oil and gas, and manufacturing. Where needed, paid subscriptions covering company financials and shipment-level import and export records were used to cross-check revenue scale and trade flows. These sources are illustrative, and we also relied on additional public and paid references during collection, validation, and gap clarification.

Primary Interviews and Surveys

Primary work focused on validating what the desk data could not fully explain, especially country differences in VFD adoption and pricing. We spoke with channel participants, system integrators, project contractors, and end-user maintenance and engineering teams across key APAC demand centers to confirm application mix, voltage and power rating splits, and realistic ASP movement assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 16% | |

| Mid tier: 57% | Functional/Unit leaders: 33% | |

| Smaller Players: 17% | Managers: 51% |

Market-Sizing & Forecasting

The core model is built using a top-down approach where industrial activity, energy use patterns, and motor-driven load intensity are translated into a demand pool for drives by major application areas (such as pumps, fans, compressors, conveyors, and HVAC). Results are then corroborated with selective bottom-up approximations, mainly sampled ASP times unit volumes from channel checks, and a sanity roll-up of revenues implied by the active supplier and distributor landscape.

Inputs used in the model include trends in industrial electricity consumption, additions in power generation and grid-related projects, manufacturing output and capex direction, motor efficiency regulation and retrofit activity, and mix shifts between low-voltage and medium-voltage drives. Price progression is handled through a practical ASP ladder by voltage class and power rating, which is then adjusted using interview feedback on discounting and the split between project sales versus MRO share. For forecasting, we used scenario analysis supported by a simple multivariate regression overlay, where industrial output and electricity demand indicators anchor the base case, and then adoption-rate adjustments are applied for energy efficiency programs and automation spending.

Where bottom-up inputs were incomplete for smaller countries or fragmented channels, gaps were handled by applying country-level penetration proxies derived from similar markets, and then re-checked against trade flows and end-user capex patterns before finalizing totals.

Data Validation & Update Cycle

We validate outputs by checking whether the implied VFD spend aligns with independent signals such as industrial electricity use, import intensity for drive equipment, and application-linked capex cycles, then reviewing outliers one by one. When a variance looks too large, assumptions are revisited, and targeted re-contacts are triggered with interviewees to confirm whether the issue is pricing, scope, or timing.

Before sign-off, the model and key assumptions go through multiple analyst reviews, with country totals, application splits, and ASP ladders tested for internal consistency. Reports are refreshed annually, and interim updates are made when material events change demand, such as major policy moves, large project delays, or sudden currency swings. Right before delivery, a final pass is completed so clients receive the latest updated view.

Mordor Intelligence's Asia Pacific Variable Frequency Drive Market Market Estimate Compared With Other Published Estimates

Published market sizes for APAC VFDs often differ even when the topic sounds identical, because the country list, product boundaries, and the year used as the anchor point are not consistent. Pricing treatment also varies, especially when project-heavy industries and distributor discounts are not handled carefully.

Key gaps typically come from whether DC drives and servo drives are fully included, how low-voltage versus medium-voltage revenue is split, and whether the estimate is tied to equipment sales into end users or mixed with broader automation spending. Currency conversion timing and refresh cadence also matter, because fast-moving input costs and local pricing can shift a single-year value by a noticeable amount.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 11.06 B (2026) | |

| Industry Publisher A | USD 9.47 B (2024) | Uses an earlier base year, and the published view is presented with a different forecast window, which can understate the effect of later-cycle industrial capex and price resets in key APAC countries. |

| Regional Consultancy B | USD 13.50 B (2024) | Applies a higher growth trajectory from a 2024 base, and may be using broader inclusion rules on drive-related revenues, which can lift the headline number when project and retrofit activity is counted more aggressively. |

The table shows a wide spread mainly because the anchor year differs and the counted revenue boundary is not uniform. In Mordor Intelligence's model, the APAC total is built from application demand signals and voltage and power rating mix, and it is only recognized when the product sold is a variable frequency drive rather than adjacent automation or motor hardware.

Key Questions Answered in the Report

What is the current valuation of the Asia Pacific variable frequency drives market?

The market stands at USD 11.06 billion in 2026 and is projected to climb to USD 14.54 billion by 2031.

Which segment shows the fastest growth in power rating?

Drives above 200 kW exhibit the quickest expansion, forecast at a 8.55% CAGR through 2031.

Why are VFDs critical for APAC data centers?

They enable precision control of HVAC systems, lowering cooling energy use by up to 25-30% and helping operators meet tight PUE targets.

How do government policies influence VFD adoption in China and India?

Mandatory efficiency standards and subsidies for renewable pumping solutions directly stimulate large-scale VFD installations in industrial and agricultural sectors.

Which application area currently leads in revenue?

Pumping systems contribute the largest share, accounting for 30.40% of 2025 revenues across municipal and industrial uses.

What technological trend is most affecting drive efficiency?

The integration of silicon-carbide and gallium-nitride power devices is cutting switching losses by up to 80%, markedly improving overall drive performance.

Page last updated on: