Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

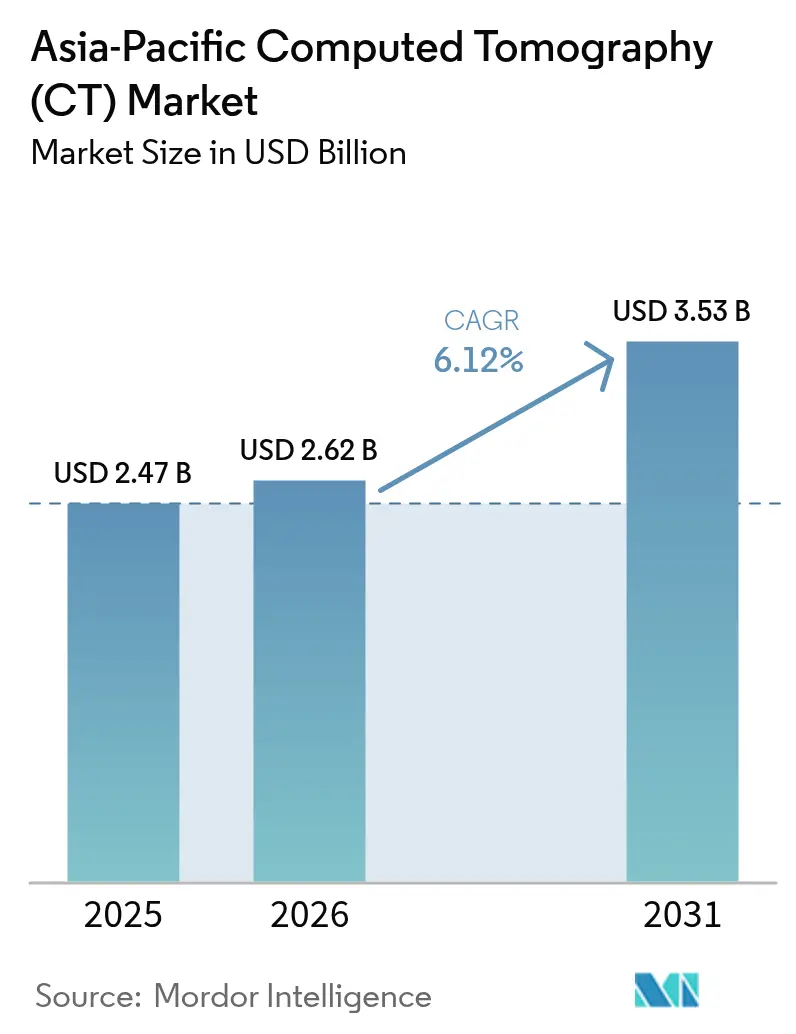

| Base Year Market Size (2025) | USD 2.47 Billion |

| Market Size (2026) | USD 2.62 Billion |

| Market Size (2031) | USD 3.53 Billion |

| Growth Rate (2026 - 2031) | 6.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Computed Tomography (CT) Market Analysis by Mordor Intelligence

Asia-Pacific Computed Tomography (CT) market size in 2026 is estimated at USD 2.62 billion, growing from 2025 value of USD 2.47 billion with 2031 projections showing USD 3.53 billion, growing at 6.12% CAGR over 2026-2031. Widening health-insurance coverage, a rising chronic-disease caseload, and procurement incentives in China and India are sustaining annual system installations even as reimbursement pressures persist. Large private hospital chains are moving beyond routine 16-/32-slice scanners toward ≥64-slice platforms, while provincial governments in China continue to mandate domestic sourcing to bolster self-reliance. Simultaneously, Japan and South Korea are validating photon-counting configurations in tertiary centers, setting a technology benchmark for neighboring markets. Vendor financing—from OEM-backed leasing in China to non-bank medical-equipment loans in India—remains the decisive enabler for customers that lack upfront capital yet require rapid capacity expansion.

Key Report Takeaways

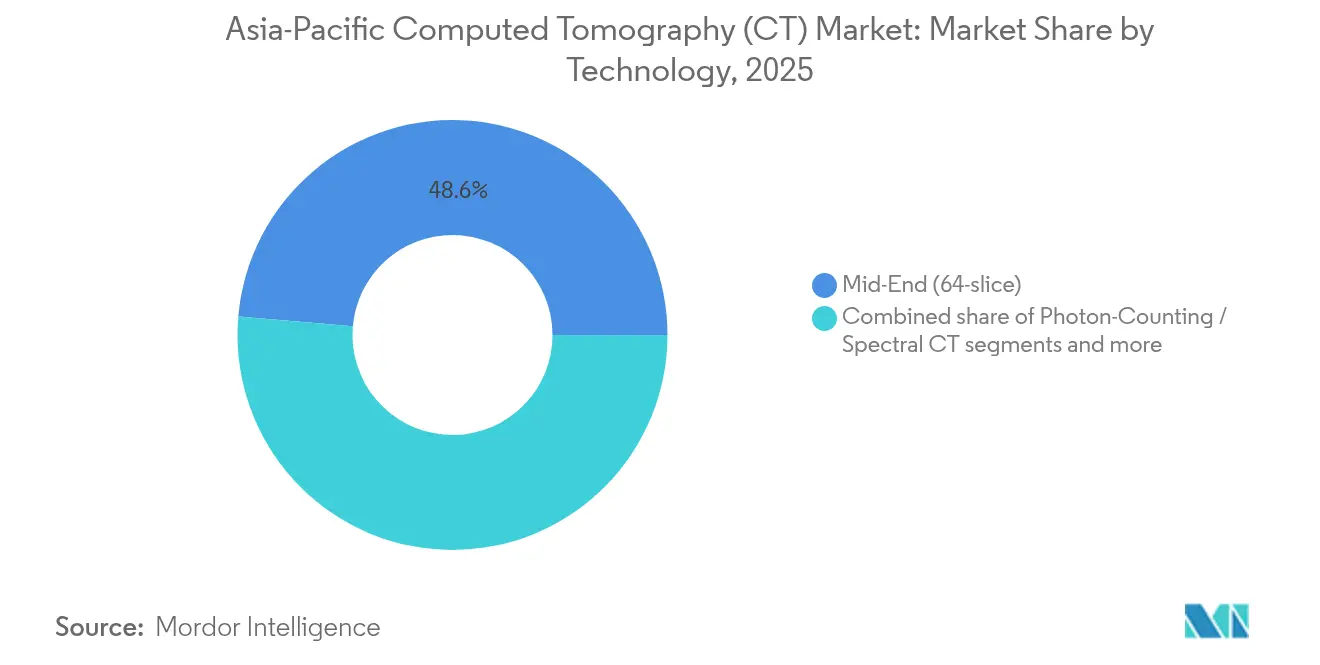

- By technology, 64-slice scanners led with 48.62% of the Asia-Pacific Computed Tomography (CT) market share in 2025, whereas photon-counting and other spectral systems are forecast to post the highest CAGR at 7.02% through 2031.

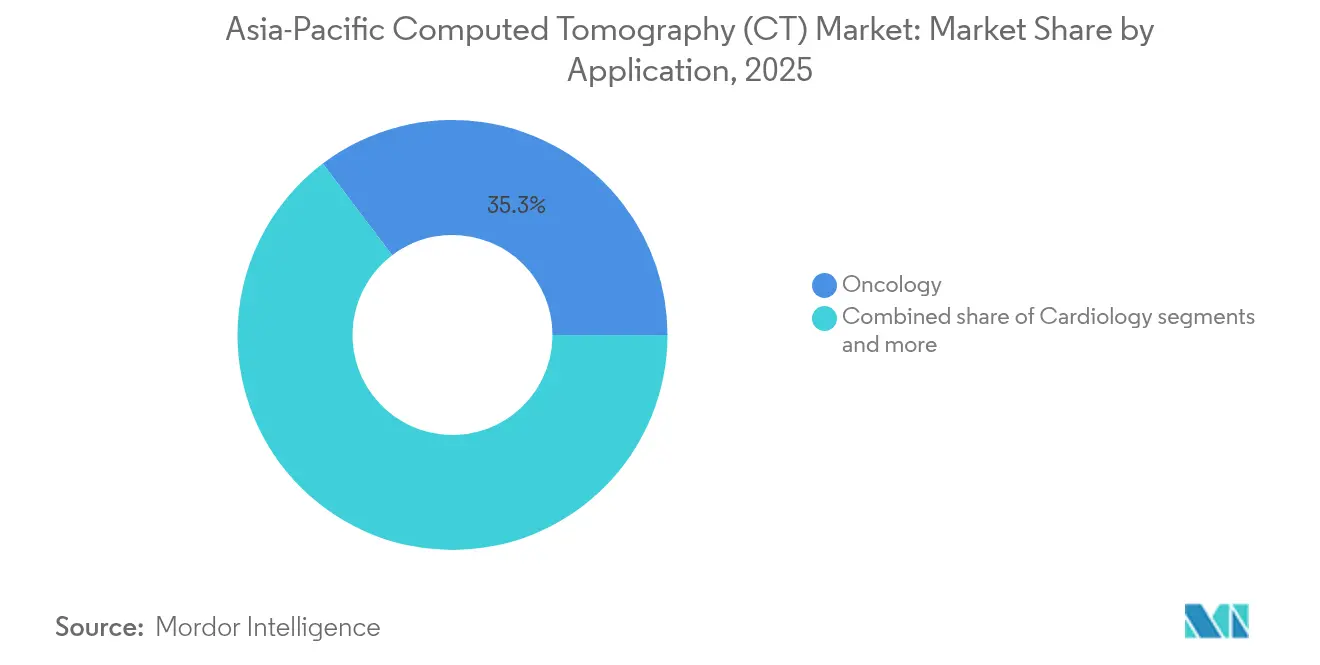

- By application, oncology accounted for a 35.31% share of the Asia-Pacific Computed Tomography (CT) market size in 2025; cardiology is set to expand at a 7.28% CAGR to 2031.

- By end-user, hospitals held 54.05% of the Asia-Pacific Computed Tomography (CT) market in 2025, while private hospitals are projected to register a 7.26% CAGR over the same horizon.

- By product type, stationary systems controlled 76.20% revenue in 2025; portable scanners are advancing at a 6.84% CAGR on wider point-of-care uptake.

- By country, China remained the single largest revenue contributor in 2025; India is expected to log the fastest six-year growth owing to 20% capital subsidies and lower import duties on key components.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Computed Tomography (CT) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Aging population & chronic-disease burden surge | +1.8% | Global APAC, strongest in Japan, South Korea, China | Long term (≥ 4 years) |

| Government imaging-equipment subsidy programs (China, India) | +1.2% | China, India with spillover to Southeast Asia | Medium term (2-4 years) |

| Hospital upgrade cycle from 16/32-slice to ≥64-slice systems | +1.0% | China, India, Southeast Asia core markets | Medium term (2-4 years) |

| Surge in cardiac CT angiography post-2024 guideline changes | +0.8% | Global APAC, early adoption in Singapore, Japan | Short term (≤ 2 years) |

| OEM trade-in schemes accelerating spectral/photon-counting installs | +0.6% | Developed APAC markets, urban centers | Short term (≤ 2 years) |

| Domestic OEM financing for lower-tier city roll-outs | +0.5% | China, India tier-2/3 cities, rural expansion | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Aging Population & Chronic-Disease Burden Surge

Rising life expectancy in Japan, South Korea, and urban China is shifting the disease profile toward oncology, cardiovascular, and neurodegenerative disorders that depend on cross-sectional imaging for diagnosis and treatment monitoring. National cancer-screening campaigns have broadened CT access in secondary cities, while diabetes-related vascular complications are increasing abdominal and peripheral CT angiography studies in India. Radiology departments therefore budget for higher-performance scanners that permit multi-phase protocols within a single breath-hold and deliver thin-slice reconstructions suitable for AI decision-support tools. Dose-optimization guidance from Australia’s ARPANSA is also influencing protocol standardization across the region, reinforcing the need for detector advancements and iterative reconstruction engines that can maintain image quality while lowering patient exposure.

Government Imaging-Equipment Subsidy Programs (China, India)

China’s “Made in China” procurement directive links public-tender eligibility to local manufacturing, favoring domestic vendors that package scanners with multi-year service contracts and staff training. India’s Production-Linked Incentive scheme offers a 20% capital subsidy on CT-scanner components and retains a 5% concessional customs duty on X-ray tubes through March 2025, reducing total landed cost for assemblers. These initiatives compress payback periods for hospitals and drive cluster-based manufacturing investments that shorten lead times for export customers in Southeast Asia.

Hospital Upgrade Cycle from 16/32-Slice to ≥64-Slice Systems

Ealry installations are reaching end-of-life, pushing administrators to evaluate trade-in offers that bundle new scanners with predictable service plans. Replacement demand is strongest in metropolitan China and tier-1 Indian cities where daily scan volumes exceed 50 patients per system. OEMs now position 64-slice models as the “minimum viable platform,” stressing their readiness for spectral upgrades and AI applications. This mid-tier refresh results in higher average selling prices yet leaves a well-maintained secondary-market inventory that can be redeployed into rural outreach programs.

Surge in Cardiac CT Angiography Post-2024 Guideline Changes

The Society of Cardiovascular Computed Tomography’s 2024 consensus transformed coronary CT angiography from a qualitative to a quantitative modality, prompting insurance payors in Singapore and Japan to reimburse software-based plaque analysis. Scanner demand thus pivots to systems capable of sub-0.3-second rotation times and dual-energy acquisition. Vendors additionally promote tube-current-modulation features and wide-detector arrays that capture the entire heart in a single beat, critical for arrhythmia cases

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High service-contract & X-ray-tube replacement costs | -0.9% | Global APAC, acute in cost-sensitive markets | Long term (≥ 4 years) |

| Uneven reimbursement outside Tier-1 APAC cities | -0.7% | China, India, Southeast Asia rural/suburban | Medium term (2-4 years) |

| CT-radiation dose cap proposals in Australia & Japan | -0.4% | Australia, Japan with regional influence | Medium term (2-4 years) |

| Refurbished-scanner imports eroding new-system demand | -0.6% | Price-sensitive APAC markets, emerging economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Service-Contract & X-Ray-Tube Replacement Costs

Annual service fees range from USD 42,000 for entry-level systems to more than USD 100,000 for ≥64-slice models, an outlay that many mid-size hospitals struggle to recoup under fixed patient tariffs. Tube failure remains the single largest unplanned cost; a replacement assembly for a 64-slice platform typically lists above USD 100,000. Some hospitals negotiate risk-sharing service plans that cap downtime penalties, yet others postpone upgrades altogether, stimulating a refurbished-scanner channel that offers 30–50% up-front savings.

Uneven Reimbursement Outside Tier-1 APAC Cities

National health-insurance programs in China and India reimburse CT procedures at rates calibrated for public hospitals in capital regions, leaving suburban and rural facilities with margins too thin to justify premium equipment. Consequently, newer scanners cluster in megacities, while patients in peripheral zones depend on mobile units or transport to urban centers, delaying diagnosis and limiting revenue growth for OEMs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Mid-End Dominance, Spectral Momentum Picks Up

Mid-range 64-slice scanners held 48.62% of the Asia-Pacific Computed Tomography (CT) market in 2025, reflecting broad compatibility with oncology, trauma, and pulmonary indications. Hospitals regard this class as the baseline for forward compatibility with cardiac workflows, balancing capex against insurance coverage thresholds. Photon-counting and other spectral platforms are forecast at a 7.02% CAGR to 2031 as Japan and Singapore validate superior calcium-scoring reproducibility and dose reductions of up to 40%. Early adopters leverage OEM trade-in credits to temper the premium, repurposing outgoing scanners into satellite clinics. At the opposite end, sub-64-slice systems lose share each year because government tenders in China and Malaysia now stipulate ≥64-slice capability as a minimum eligibility criterion. High-slice (≥128) configurations fill a premium niche in pediatric and cardiovascular centers where wide detector arrays shorten breath-hold times and mitigate motion artifacts; their installed base is expanding 5–6 percentage points per annum in tertiary facilities.

Trading dynamics revolve around bundled AI software that automates bone subtraction, lung-nodule quantification, and metal-artifact reduction. These features prolong the useful life of mid-end scanners and ease the transition toward spectral imaging by offering incremental clinical value without immediate detector upgrades. OEMs also position subscription-based algorithm libraries that transform conventional 64-slice hardware into provisional dual-energy systems, preserving account loyalty ahead of full photon-counting conversion.

By Application: Oncology Holds Lead While Cardiology Accelerates

Oncology maintained the largest share at 35.31% in 2025, buoyed by lung-cancer screening mandates in China and rising PET-CT hybrid referrals that necessitate complementary contrast CT. Routine staging protocols, encompassing chest, abdomen, and pelvis, keep utilization rates high even in resource-limited settings. Still, cardiology is the fastest-growing vertical at a 7.28% CAGR, propelled by guideline-endorsed CT angiography and widening reimbursement for calcium scoring packages. Hospitals now seek scanners capable of single-beat whole-heart coverage, integrated ECG gating, and AI-driven stenosis quantification. These technical requirements narrow vendor options and elevate the average deal size, increasing overall revenue contribution from cardiac imaging despite its smaller case volume. Neurology benefits from portable CT installations in mobile stroke units, aligning with regional pre-hospital care initiatives that prioritize rapid door-to-needle times. Musculoskeletal imaging maintains steady demand in sports-medicine clinics across Australia and South Korea, leveraging low-dose protocols that safeguard pediatric and athlete cohorts.

Growing subspecialization drives hospitals to negotiate multi-scanner packages that allocate oncology workloads to 64-slice rooms while reserving spectral or photon-counting suites for coronary and perfusion studies. This case-mix optimization maximizes scanner throughput and accelerates return on investment. Software ecosystems further segment applications; for example, AI-based lung-nodule follow-up modules secure oncology revenue streams, whereas plaque-quantification suites capture cardiology workflows, fostering brand lock-in.

By End-User: Hospitals Retain Majority, Private Chains Outpace Public Installations

Hospitals commanded 54.05% of the Asia-Pacific Computed Tomography (CT) market in 2025, and their purchasing committees increasingly favor long-term managed-equipment services over outright capital purchases to stabilize maintenance costs. Private hospital groups are projected to expand at a 7.26% CAGR as investors target cash-pay medical tourism in Thailand, Malaysia, and India. These for-profit operators differentiate through premium imaging suites encompassing photon-counting CT, 3 Tesla MRI, and hybrid operating rooms, thereby elevating average revenue per occupied bed. Diagnostic imaging centers compete on patient convenience and turnaround time, deploying mid-end scanners in malls and transport hubs to capture outpatient traffic. Ambulatory surgery centers selectively add 32-slice scanners for intra-operative guidance during orthopedic and spinal procedures, though volumes remain modest relative to hospital demand.

Shifting payer mixes stimulate divergent procurement models: public facilities rely on multilateral loans or donor financing—such as the Islamic Development Bank’s EUR 803 million SIHREN project—to acquire bulk stationary units, whereas private chains use operating-lease structures to refresh scanners every five to seven years. This heterogeneity enables OEM segmentation strategies that bundle service tiers, training, and AI licenses according to site type, extracting higher lifetime value from private customers while retaining volume commitments from the public sector.

By Product Type: Stationary Platforms Dominate, Portable Growth Remains Niche but Persistent

Stationary systems retained 76.20% revenue in 2025 owing to superior gantry aperture, high-power generators, and multi-energy options essential for comprehensive oncology and cardiac studies. Hospitals allocate dedicated rooms with lead shielding and HVAC infrastructure, reinforcing the installed-base advantage of fixed scanners. Portable CT units, though starting from a smaller base, are growing at a 6.84% CAGR as stroke ambulances, intensive-care wards, and battlefield trauma centers require imaging at the point of care. These scanners feature 16–32 slices, lightweight carbon-fiber gantries, and battery or generator power sources that allow deployment without reinforcing floors. Accuracy and image quality have improved sufficiently for triage and follow-up exams, but portable units remain supplementary rather than substitutive.

Manufacturers now market modular service contracts that rotate portable gantries across locations, smoothing utilization and minimizing idle time. In China, county-level hospitals employ mobile CT buses equipped with 64-slice scanners to deliver lung-cancer screening to remote villages, funded by provincial public-health budgets. Meanwhile, Australia’s Royal Flying Doctor Service is piloting collapsible CT pods capable of air-transport, widening the geographical reach of trauma imaging. Although portable systems are unlikely to displace stationary rooms in high-volume centers, their strategic value in tele-radiology networks and disaster-response frameworks underpins steady demand

Geography Analysis

China preserved its leadership position in the Asia-Pacific Computed Tomography (CT) market during 2024 through domestic procurement policies that favor locally manufactured systems. United Imaging and other home-grown vendors secured multi-year supply contracts with provincial hospital alliances, benefiting from shortened delivery schedules and integrated financing packages. Urban tertiary hospitals in Beijing, Shanghai, and Guangzhou accelerated replacements toward ≥128-slice and photon-counting configurations, whereas county hospitals favored cost-optimized 64-slice models bundled with five-year service. Concurrently, OEM-backed leasing worth RMB 31 million aided private orthopedic centers in northern provinces, underscoring financing as a key adoption lever.

India is emerging as the fastest-expanding market following its 20% capital subsidy on CT-scanner components and concessional import duties on X-ray tubes. Domestic assemblers leverage these incentives to supply 64-slice systems at prices 15–20% below imported equivalents, making advanced imaging more accessible to tier-2 cities. Rising lifestyle diseases fuel scan volumes, while increasing private-insurance penetration elevates patient willingness to pay for lower-dose and cardiac-optimized protocols. Public-private-partnership models in several states outsource radiology services to private operators, guaranteeing minimum scan volumes and ensuring predictable cash flows that make equipment financing viable.

Japan and South Korea remain premium-technology early adopters given their stringent quality standards and mature reimbursement schemes. Photon-counting CT has completed more than 1,800 clinical cases at a single Singaporean hospital, catalyzing interest across other developed APAC markets. Australia’s dose-cap proposals from ARPANSA are shaping specification criteria, pushing hospitals toward scanners with real-time organ-dose tracking. Smaller Southeast Asian economies are importing refurbished 64-slice systems for provincial hospitals while reserving new purchases for national referral centers, illustrating a two-tier technology diffusion pattern that continues to widen overall regional unit growth.

Competitive Landscape

Market competitiveness centers on detector innovation, integrated AI, and flexible ownership models rather than headline list prices. Siemens Healthineers leads the photon-counting race after securing FDA clearance for the NAEOTOM Alpha.Pro and Alpha.Prime, widening its spectral portfolio. Canon Medical and GE HealthCare are accelerating their own photon-counting roadmaps, while Philips commercializes deep-learning reconstruction across existing detector architectures to hedge against technology transitions. Local champions such as United Imaging capitalize on government sourcing rules to gain share and have started exporting 128-slice scanners to Southeast Asia, challenging incumbents with feature-comparable yet lower-priced offerings.

Financing is now a primary battleground. OEM leasing arms structure seven-year operating leases with step-up payments tailored to projected patient volumes, reducing front-loaded cash requirements. In India, non-bank finance firms lend up to INR 8 million for CT purchases with 48-hour disbursal, shortening acquisition cycles. Service differentiation further sharpens competition: Philips promotes circular-economy refurbishments that guarantee part availability, while GE HealthCare bundles predictive-maintenance analytics to cut unplanned downtime by up to 25%. These service propositions create switching costs that rival upfront discounts.

Regulatory compliance and local assembly have become entry tickets rather than strategic advantages. All major vendors now operate ISO-certified facilities in either China or India, integrate cybersecurity features to meet Japan’s personal-data standards, and maintain regional training centers. Consequently, sustained leadership will hinge on successful photon-counting commercialization, AI-driven workflow orchestration, and ecosystem partnerships that harmonize imaging with longitudinal patient data in emerging digital-health platforms.

Asia-Pacific Computed Tomography (CT) Industry Leaders

Canon Medical Systems Corporation

GE Healthcare

Koninklijke Philips NV

Siemens Healthineers

Hitachi Healthcare Systems

- *Disclaimer: Major Players sorted in no particular order

_Market.webp)

Recent Industry Developments

- March 2025: Siemens Healthineers obtained FDA clearance for NAEOTOM Alpha.Pro dual-source and Alpha.Prime single-source photon-counting CT systems, extending its spectral portfolio

- February 2024: Philips introduced the CT 5300 , featuring Precise Image deep-learning reconstruction that cuts dose by up to 80%

Asia-Pacific Computed Tomography (CT) Market Report Scope

As per the scope of the report, computed tomography (CT) is an imaging process that customizes special X-ray equipment to generate a sequence of exhaustive images, or scans, of areas inside the body. Also called computerized axial tomography (CAT) scanning, it is primarily used in cancer diagnosis.

The Asia-Pacific Computed Tomography (CT) Market is Segmented by Type (Low Slice, Medium Slice, and High Slice), Application (Oncology, Neurology, Cardiovascular, Musculoskeletal, and Other Applications), End User (Hospitals, Diagnostic Centers, and Other End Users), and Geography (China, Japan, India, Australia, South Korea, and Rest of Asia-Pacific). The report offers the market size in value terms in USD for all the abovementioned segments.

By Technology (Slice Count) – Value

| Low (<64) |

| Medium (64) |

| High (≥128) |

| Cone-Beam CT |

By Application – Value

| Oncology |

| Cardiology |

| Neurology |

| Musculoskeletal |

| Others |

By End-User – Value

| Hospitals |

| Diagnostic Imaging Centers |

| Ambulatory Surgery Centers |

| Others |

By Product Type – Value

| Stationary CT |

| Portable CT |

By Country – Value

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Rest of Asia-Pacific |

| By Technology (Slice Count) – Value | Low (<64) |

| Medium (64) | |

| High (≥128) | |

| Cone-Beam CT | |

| By Application – Value | Oncology |

| Cardiology | |

| Neurology | |

| Musculoskeletal | |

| Others | |

| By End-User – Value | Hospitals |

| Diagnostic Imaging Centers | |

| Ambulatory Surgery Centers | |

| Others | |

| By Product Type – Value | Stationary CT |

| Portable CT | |

| By Country – Value | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific Computed Tomography (CT) market in 2026?

It reached USD 2.62 billion in 2026 and is forecast to hit USD 3.53 billion by 2031.

Which technology segment leads unit shipments?

64-slice scanners command nearly half of current shipments, balancing cost with multipurpose capability.

What drives the fastest growth within applications?

Cardiac CT angiography is expanding quickest after 2024 guideline revisions that standardized quantitative plaque assessment.

Why are private hospitals outpacing public facilities in new purchases?

Private chains leverage higher self-pay volumes and flexible leasing to refresh fleets every five to seven years, capturing premium imaging demand.

How are governments influencing procurement?

China mandates local manufacturing in public tenders, while India offers a 20% capital subsidy and lower customs duties on key components, both reducing acquisition costs.

What is the outlook for portable CT systems?

Portable scanners remain a small share today but are advancing at 6.84% annually as stroke ambulances and ICU deployment models prove clinical utility.

Page last updated on: