Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

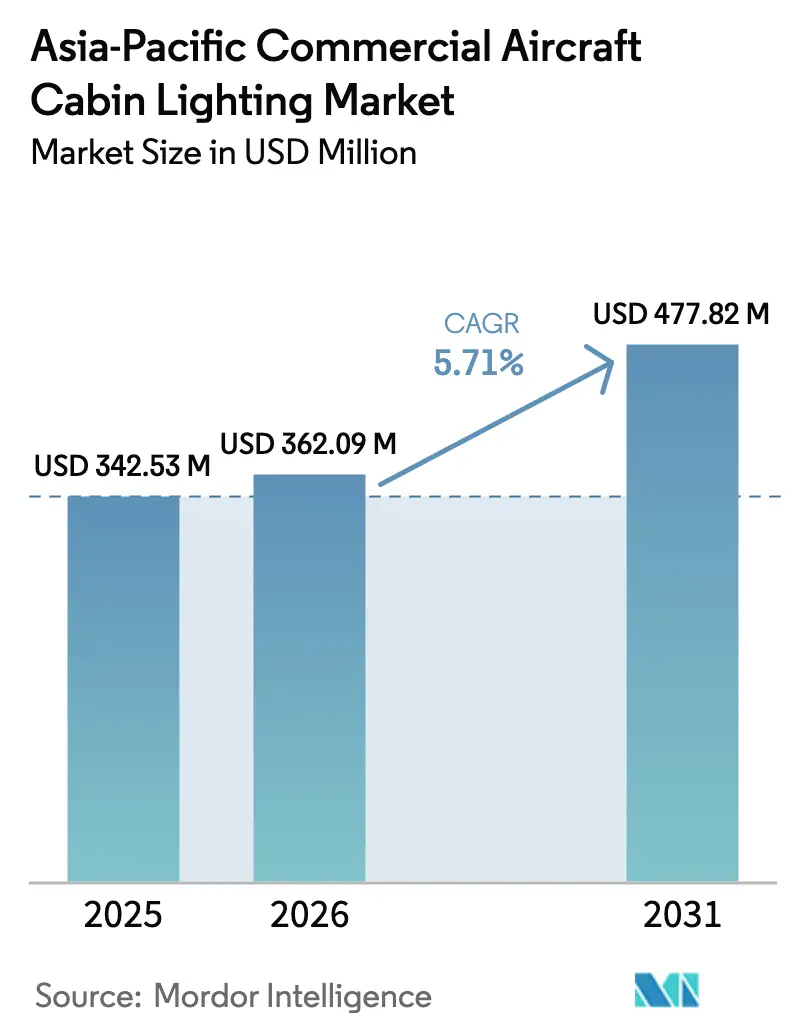

| Base Year Market Size (2025) | USD 342.53 Million |

| Market Size (2026) | USD 362.09 Million |

| Market Size (2031) | USD 477.82 Million |

| Growth Rate (2026 - 2031) | 5.71% CAGR |

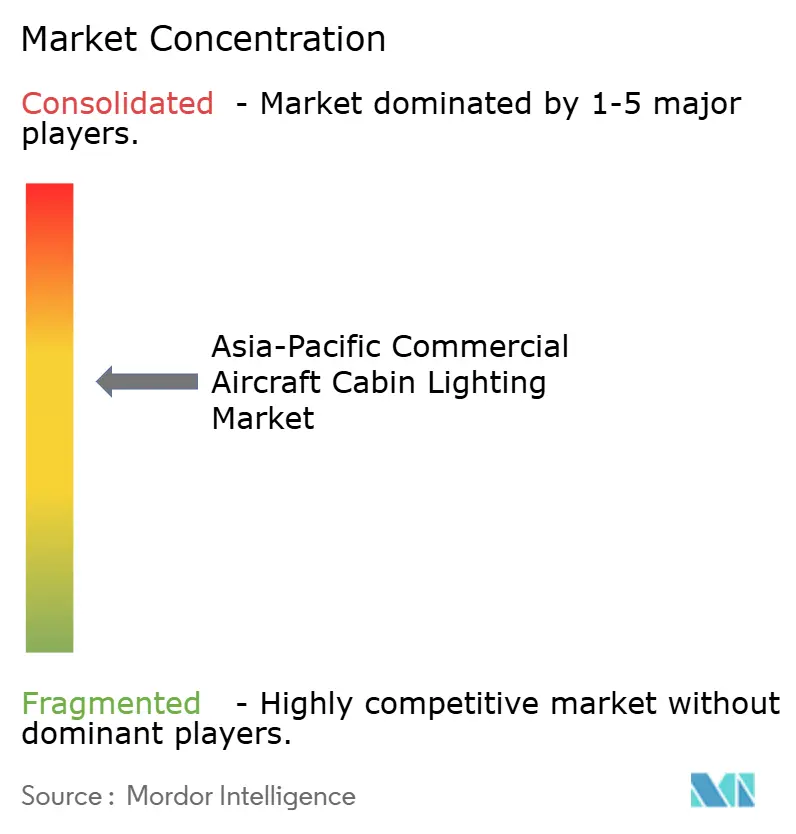

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Commercial Aircraft Cabin Lighting Market Analysis by Mordor Intelligence

The Asia-Pacific commercial aircraft cabin lighting market size is expected to grow from USD 342.53 million in 2025 to USD 362.09 million in 2026 and is forecast to reach USD 477.82 million by 2031 at 5.71% CAGR over 2026-2031. Airlines are not just renewing their narrowbody and widebody fleets but are also aligning with mercury-phase-out mandates. They're increasingly turning to human-centric LED solutions, underscoring a commitment to passenger wellness. These weight-saving LEDs not only trim fuel consumption but also minimize maintenance downtimes. Moreover, retrofit packages empower carriers to modernize older cabins without lengthy aircraft groundings. As global tier-1 suppliers fiercely guard their line-fit positions, nimble regional vendors are making strategic inroads into the aftermarket. With flight hours rebounding and a strong order backlog in China, India, and Southeast Asia, the momentum for cabin lighting programs remains robust.

Key Report Takeaways

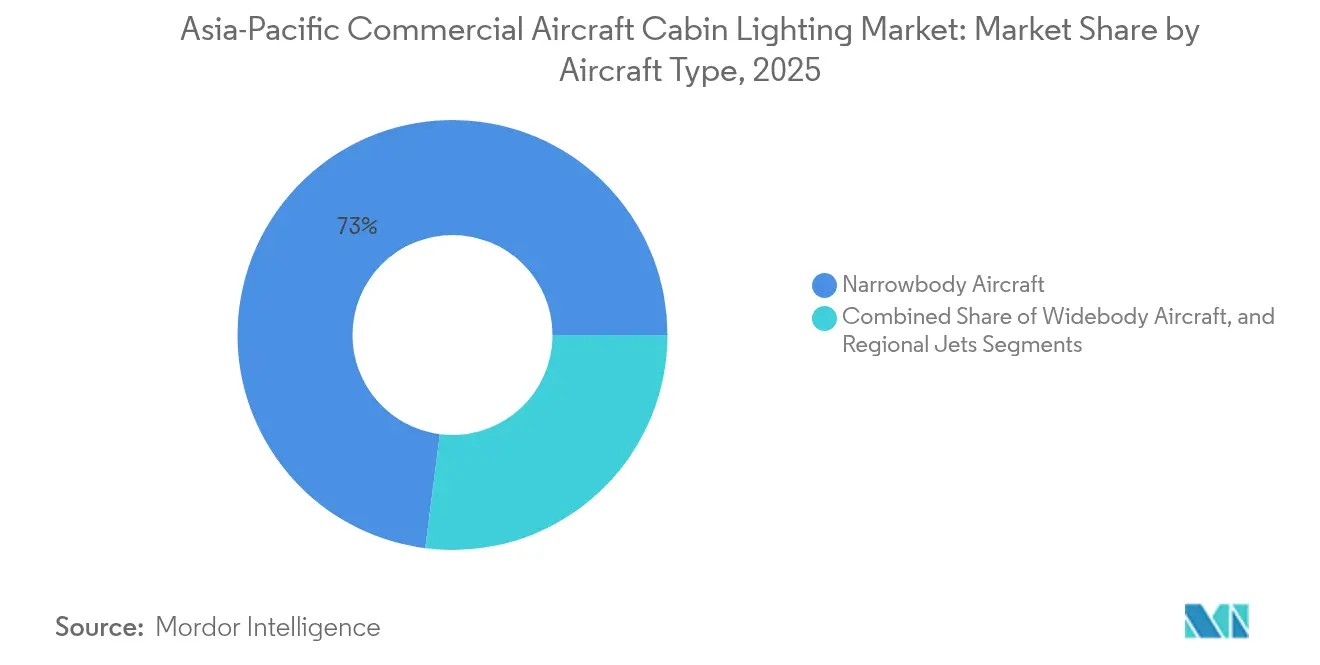

- In 2025, narrowbody jets dominated the Asia-Pacific commercial aircraft cabin lighting market, securing a 72.98% share. Meanwhile, widebody aircraft are projected to experience the highest growth rate, with a CAGR of 8.41% through 2031.

- Ceiling and wall lights led the Asia-Pacific commercial aircraft cabin lighting market in 2025, holding a 32.12% share. In contrast, reading lights are on track to grow at a robust 8.98% CAGR until 2031.

- By cabin class, economy class captured 58.12% stake in 2025. On the other hand, the premium economy is anticipated to see a notable expansion, boasting a forecasted CAGR of 10.41%.

- By source, OEM line-fit installations made up 51.43% of the Asia-Pacific commercial aircraft cabin lighting market in 2025. However, aftermarket retrofits are outpacing them with an annual growth rate of 9.54%.

- China commanded a significant 46.08% of the regional value in 2025. Yet India is poised for rapid growth, projected to achieve the fastest CAGR of 9.66% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Commercial Aircraft Cabin Lighting Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweight LED retrofits reduce jet weight and lower fuel burn | +2.8% | Global, strongest in Asia-Pacific LCC markets | Medium term (2-4 years) |

| Circadian-rhythm lighting enhances comfort on long-haul flights | +1.9% | Asia-Pacific hub carriers, trans-Pacific routes | Long term (≥ 4 years) |

| RoHS and Minamata mercury bans accelerate fluorescent phase-out | +2.1% | Fleets serving EU-Asia sectors | Short term (≤ 2 years) |

| Rapid LCC fleet growth boosts demand for PSU reading lights | +1.7% | Southeast Asia and India domestic networks | Medium term (2-4 years) |

| Digital ceiling panels create new branding and ancillary revenue | +1.2% | Premium carriers across Asia-Pacific | Medium term (2-4 years) |

| IoT-enabled seat-power bundles drive upgraded personal lighting | +1.0% | Business and premium-economy retrofits worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweight LED Retrofit Reduce Jet Weight, Boost Fuel Efficiency

By replacing fluorescent lights with lightweight LEDs, airlines can reduce the weight of a single-aisle jet by about 15 kg and cut power consumption by 60%. This transition results in notable fuel savings, particularly on routes commonly serviced by low-cost carriers (LCCs).[1]Boeing, “AERO, Quarter 4-06,” Boeing Aeromagazine, boeing.com Airlines can recoup their retrofit investments in merely two years, thanks to diminished fuel costs and the impressive 50,000-hour lifespan of the new lamps.[2]John T. Petrick, “High-Brightness LEDs in Aerospace Applications,” SPIE Proceedings, spie.org Removing ballasts not only streamlines wiring for airlines but also lessens maintenance checks and boosts dispatch reliability. Such enhancements are crucial for airlines targeting a 12-hour daily jet utilization. Suppliers now provide LEDs with sophisticated drivers, guaranteeing uniform color temperatures across cabin zones, thereby enhancing passenger comfort. In the Asia-Pacific, weight-driven economics heavily sway the commercial aircraft cabin lighting market, given that fuel expenses are the primary controllable cost for budget airlines.

Airlines Embrace Circadian Lighting for Long-Haul Flights

Major airlines are now implementing lighting systems replicating the natural solar cycle to enhance passenger comfort on flights exceeding 14 hours. Following successful trials, Delta's retrofitting of its domestic fleet demonstrated that circadian lighting boosts traveler alertness upon arrival.[3]Delta Air Lines, “Delta Becomes First U.S. Airline to Introduce Circadian Lighting on Entire Domestic Fleet,” delta.com This success has prompted carriers in the Asia-Pacific region to consider similar enhancements, especially for their upcoming Sydney–New York and Singapore–Los Angeles routes. These advanced LED systems transition from energizing blue hues during boarding to warm ambers at mealtime and finally to deep reds, which are known to stimulate melatonin production. Backed by scientific research from the University of Sydney’s Project Sunrise, this lighting approach is recognized as an aesthetic upgrade and a genuine wellness initiative.[4]University of Sydney, “Qantas Project Sunrise Research Partnership,” sydney.edu.au While premium cabins were the first to adopt this technology, decreasing component costs make it accessible in refurbished economy sections.

EU's RoHS Directive and Minamata Convention Push for Swift Phase-Out of Mercury Lamps

Operators must replace legacy tubes by 2027, as mandated by the EU's RoHS Directive and the Minamata Convention, or face route restrictions. Airlines from the Asia-Pacific region, flying into Europe, grapple with a tight compliance deadline, leading to an urgent surge in demand for LED kits. To ensure permanence, regulators have also prohibited fluorescent replacement parts. As these programs expand, the resulting drop in unit costs encourages voluntary adoption among domestic fleets. This swift transition is steering the Asia-Pacific commercial aircraft cabin lighting market towards more lucrative digital control systems, built on an LED foundation.

LCC Fleet Expansion Fuels Demand for PSU Lighting

IndiGo, AirAsia, and VietJet have placed orders for over 1,000 narrowbody aircraft, each equipped with passenger service unit (PSU) reading lights. With denser seating configurations, the number of lamps required multiplies. Low-Cost Carriers (LCCs) prefer straightforward screw-in fixtures, designed for rapid cleaning and frequent passenger use. In response, vendors now offer tamper-proof bezels and modular LEDs. These new LEDs can easily clip into existing PSU rails without rewiring, significantly reducing installation time to fit within overnight layovers. As aircraft utilization increases, so does the accumulation of lamp hours, boosting replacement revenue despite the extended life of LEDs. This growing segment solidifies the dominance of narrowbodies in the Asia-Pacific commercial aircraft cabin lighting market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain delays shift airline budgets away from cabin upgrades | −1.8% | Region-wide, most acute in Asia-Pacific | Short term (≤ 2 years) |

| Lessor restrictions limit use of lower-cost PMA lighting parts | −1.3% | Leased aircraft across Asia-Pacific | Medium term (2-4 years) |

| Limited MRO certification slots slow retrofit throughput | −0.9% | Major hubs in China, Singapore, Malaysia | Medium term (2-4 years) |

| Extended LED lifetimes reduce recurring aftermarket sales | −1.1% | Mature LED-equipped widebody fleets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Woes Delay Aircraft Deliveries, Shifting Focus on Budgets

Due to supply-chain shortages, new aircraft handovers have been pushed to 2026. This shift has compelled carriers to redirect funds from cabin overhauls to crucial maintenance tasks like engine and landing-gear servicing. Additionally, deferred line-fit slots are causing delays in pre-installed lighting systems, affecting the revenue stream for the Asia-Pacific commercial aircraft cabin lighting market. Extending beyond their planned airframe cycles, operators prioritize structural checks over ambiance enhancements, leading to a slowdown in retrofit orders. While delivery schedules are set to stabilize, and pent-up demand is anticipated to resurface, the immediate repercussions have dampened market acceleration.

Asia-Pacific Airlines Face Squeeze as Lessors Tighten Grip on Lighting Parts

In Asia-Pacific, over 50% of narrowbody aircraft are leased, with many contracts stipulating the exclusive use of OEM components. These stipulations prevent airlines from opting for Parts Manufacturer Approval (PMA) alternatives, which could lead to 15% or more savings on lamp assemblies. For regional carriers operating on slim margins, it means either absorbing the higher costs of OEM pricing or delaying necessary retrofits, ultimately stunting the aftermarket growth. While lessors defend these rules to safeguard residual value, a notable shift is occurring: some lessors are now open to dual certification, provided PMA vendors can demonstrate comparable reliability. This suggests a potential softening of their stance by 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Narrowbodies Lead, Widebodies Upsell

In 2025, narrowbody models, led by the A320neo and B737 MAX, dominated the Asia-Pacific commercial aircraft cabin lighting market, securing a 72.98% share. The dense route networks of low-cost carriers in India and Southeast Asia bolstered this dominance. With these models racking up higher flight cycles, the demand for aftermarket services surged, driven by increased lamp hours accrued. Meanwhile, widebody aircraft are projected to grow at an 8.41% CAGR through 2031. Airlines, particularly hub operators, are retrofitting A350 and B787 cabins with circadian lighting presets, allowing them to command premium ticket prices. As non-stop long-haul services expand, the market size for widebody cabin lighting in the Asia-Pacific is expected to reach USD 75.6 million by 2031. Operators recognize the revenue benefits of enhanced passenger comfort, leading to increased lighting budgets per aircraft. While narrowbody programs anchor the market's volume, the retrofits in widebodies spearhead technological innovations, which are subsequently adopted in single-aisle fleets.

By Lighting Type: Ceiling Lights Lead, While Reading Lights Shine Brighter

In 2025, ceiling and wall assemblies accounted for 32.12% of shipments, serving as the cornerstone of cabin lighting. Airlines are now infusing dynamic color washes and sunrise sequences into these fixtures, elevating them from necessities to bold brand statements. While reading lights constitute a smaller segment, they are witnessing a robust annual growth of 8.98%. This surge is primarily attributed to their integration with smart power hubs and the increasing use of personal devices. By 2031, the Asia-Pacific market for reading lights in commercial aircraft cabins is projected to reach an estimated USD 27.3 million, encompassing retrofit kits and OEM line-fits. Signage lights play a crucial role in marking exits, yet their limited technological differentiation results in steady, flat revenue. Lavatory and floor-path lighting products benefit from broader cabin refresh cycles. Emergency lighting upgrades are sometimes bundled with LED pathway strips, serving as ambient perimeter accents.

There's a growing preference for integrated fixtures with replaceable LED clusters over traditional monolithic units. This shift enables a simple diode swap rather than a complete assembly replacement. Additionally, the review of wireless bus standards could reshape the economics of light types, potentially reducing harness weight and simplifying future upgradesattributed mainly. These technical advancements broaden the revenue lifecycle opportunities within the Asia-Pacific commercial aircraft cabin lighting market.

By Cabin Class: Economy vs. Premium: The Diverging Paths of Cabin Class Lighting Revenues

Economy rows dominate the installed units landscape, with each seat benefiting from at least one reading lamp and shared overhead illumination. This volume translates to a projected 58.12% of total revenue in 2025, even with a lower spend per seat. Meanwhile, premium economy lighting is on a rapid ascent, boasting a 10.41% CAGR, as airlines enhance this hybrid class with tailored mood lighting and USB-connected reading spots. Business cabins are elevating their lighting game, integrating seat-shell LEDs and privacy-panel uplights that respond to touchscreen controls. This innovation drives a higher value per seat, even as the occupied square footage diminishes. Although fewer in number, first-class suites are equipped with bespoke luminaires featuring color-tunable panels and fiber-optic star domes, ensuring the continuation of profitable custom-engineering contracts.

Airlines strategically use lighting to differentiate services: employing cooler whites during economy boarding and warmer ambers in premium cabins to create a lounge-like atmosphere. Such strategies underscore the influence of cabin-class segmentation on lighting specifications in the Asia-Pacific commercial aircraft market.

By Source: OEM Integration vs. Retrofit Agility

Airframers are pre-wiring LED harnesses and seat-power junctions at the factory, leading line-fit programs to capture 51.43% of the 2025 spend. Direct supplier contracts not only secure volumes but also offer economies of scale. The aftermarket, growing at a 9.54% CAGR, sees airlines extending aircraft lifespans beyond their original design goals and lessors refurbishing assets for secondary leases. If current schedules persist, the Asia-Pacific commercial aircraft cabin lighting market, tied to retrofitting, is expected to reach nearly USD 98.6 million by 2031. Suppliers are setting themselves apart with rapid-installation kits designed for overnight C-checks and bundled warranty support that aligns with OEM standards. While certification costs pose challenges, an expanding STC library shortens approval cycles, allowing smaller carriers to partake in the upgrade trend.

Geography Analysis

China's dominance is underscored by its vast fleet size. Flag carriers are retrofitting A320ceo jets with local LED kits to align with RoHS timelines. Meanwhile, new COMAC C919s are rolling off the production line, boasting factory-installed digital mood lighting integrated with cabin management systems developed in China. Provincial airlines benefit from state subsidies that alleviate retrofit expenses, ensuring a steady flow of orders even amidst traffic declines. The domestic supply of LEDs mitigates currency risks for Chinese operators and bolsters the nation's technological independence.

India's aviation boom is fueled by a consistent 15% annual growth in passenger numbers and a historic backlog of over 1,300 narrowbody aircraft, all earmarked for low-cost carriers. Airlines now utilize plug-and-play PSU fixtures, allowing technarrow-bodynicians to make swaps in three minutes. This efficiency significantly reduces downtime during tight turnaround periods. As full-service carriers introduce premium economy classes, there's a surge in investments for zone-controllable ceiling lights and personalized reading fixtures in Indonesia. This trend steers the Asia-Pacific commercial cabin lighting market towards more lucrative service contracts.

Southeast Asia showcases a diverse landscape, and Indonesia, the unique archipelago, demands lighting solutions that can withstand humidity and salt exposure. As a result, suppliers are providing conformal-coated PCBs. In Thailand and Vietnam, leased A321s are being retrofitted to enhance cabin ambiance for tourism branding. These installations are often synchronized with mandatory heavy maintenance visits in Singapore. Together, these smaller Southeast Asian markets contribute to a steady increase in volume, bolstering regional MRO clusters and solidifying long-term demand in the Asia-Pacific commercial aircraft cabin lighting market.

Competitive Landscape

Hotbed of Innovation Amidst Intense Competition

Collins Aerospace, Diehl Stiftung, and Astronics Corporation, key players in the integrated tier-1 group, capitalize on their enduring agreements with industry titans Airbus and Boeing. Their diverse offerings, ranging from drivers and lenses to cabin management software, enable them to bundle complete lighting suites, clinching multiyCollin'sly deals. Collin's latest deliveries, featuring sealed RGBW strips certified for an impressive 100,000-hour lifespan, set a new industry benchmark. In Safran's latest move, its interior division boosts program value by adeptly cross-selling, pairing business-class seats with its exclusive reading-light modules.

Lighting experts like Luminator, SCHOTT, and Oxley swiftly stake their claim in the aftermarket, leveraging quick STC pathways and modular kits. Marking SCHOTT'sSafran's niche market, exemplified by its fiber-optic star-ceiling panel, designed for high-end A350 retrofits, has found favor with Asian boutique carriers. Meanwhile, securing multi-yearAstronics is integrating data-driven reading lights into its EmPower seat-power system, unlocking potential recurring software revenue streams that transcend traditional hardware sales.

Regional contenders, especially Chinese LED firms and Japanese SMEs, aggressively chase cost leadership. By licensing Western driver boards, they're revving up local assembly lines, slashing lead times for domestic airlines. Strategic moves, like Loar Holdings' 2024 acquisition of Applied Avionics, bolster smaller firms, enhancing their global reach through efficient distribution. While established players dominate as line-fit volumes surge, a niche remains for challengers targeting budget-conscious retrofit clients. This vibrant landscape showcases the continuous innovation driven by competitive forces in the Asia-Pacific commercial aircraft cabin lighting market.

Asia-Pacific Commercial Aircraft Cabin Lighting Industry Leaders

Collins Aerospace (RTX Corporation)

Diehl Stiftung & Co. KG

Astronics Corporation

Safran SA

Luminator Holding, LP

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Satair and Collins Aerospace announced a four-year extension of their distribution agreement for cabin interior components. This renewed contract also encompasses lighting solutions.

- March 2025: Diehl Aviation showcased its state-of-the-art cabin illumination technologies at the AIX in Hamburg. These advancements, which include accent lighting and high-quality materials, aim to significantly enhance the passenger experience.

- June 2023: STG Aerospace announced the launch of the Curve, a new flexible cabin lighting product from STG Aerospace's universal lighting family. The Curve is intended for the business jet cabin market.

Asia-Pacific Commercial Aircraft Cabin Lighting Market Report Scope

Narrowbody and widebody are covered as segments by Aircraft Type. China, India, Indonesia, Japan, Singapore, and South Korea are covered as segments by Country.

By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By Light Type

| Reading Lights |

| Ceiling and Wall Lights |

| Signage Lights |

| Lavatory Lights |

| Floor-path Lighting Strips |

By Cabin Class

| Economy Class |

| Premium Economy Class |

| Business Class |

| First Class |

By Source

| OEM Line-fit |

| Aftermarket/Retrofit |

By Geography

| China |

| India |

| Indonesia |

| Japan |

| Singapore |

| South Korea |

| Rest of Asia-Pacific |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By Light Type | Reading Lights |

| Ceiling and Wall Lights | |

| Signage Lights | |

| Lavatory Lights | |

| Floor-path Lighting Strips | |

| By Cabin Class | Economy Class |

| Premium Economy Class | |

| Business Class | |

| First Class | |

| By Source | OEM Line-fit |

| Aftermarket/Retrofit | |

| By Geography | China |

| India | |

| Indonesia | |

| Japan | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific |

Market Definition

- Product Type - The interior lights of aircraft which provide illumination for instruments, cabins, and other sections that are occupied by passengers are included in this study.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms