Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

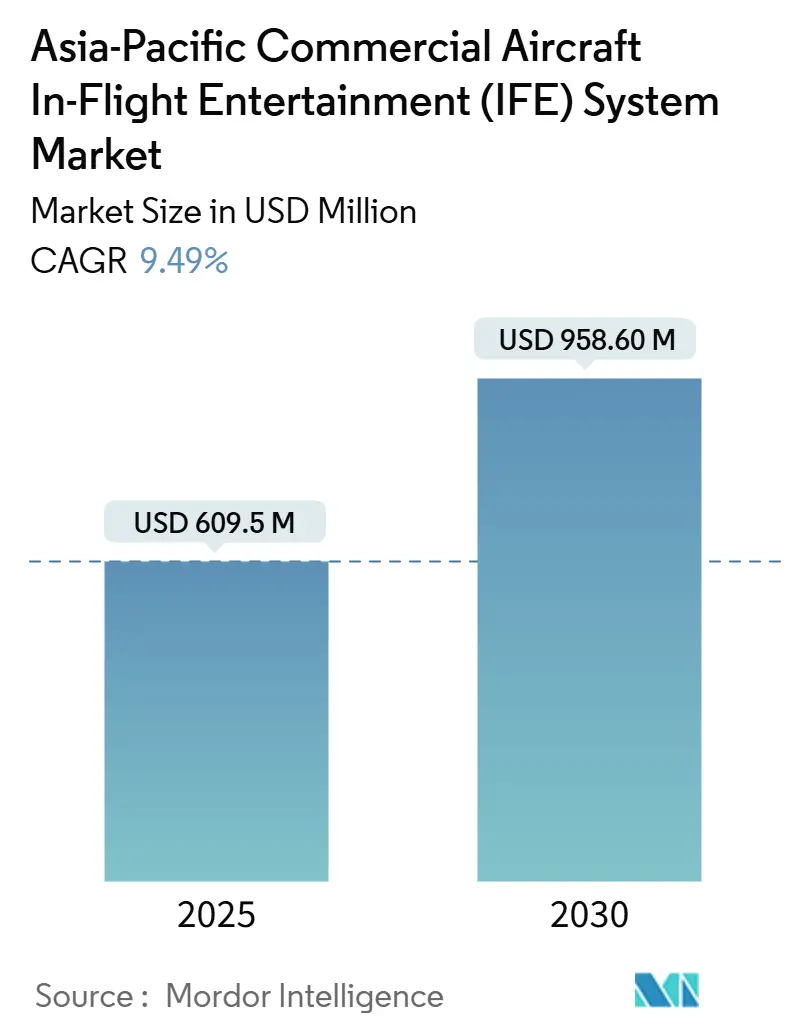

| Market Size (2025) | USD 609.5 Million |

| Market Size (2030) | USD 958.60 Million |

| Growth Rate (2025 - 2030) | 9.49% CAGR |

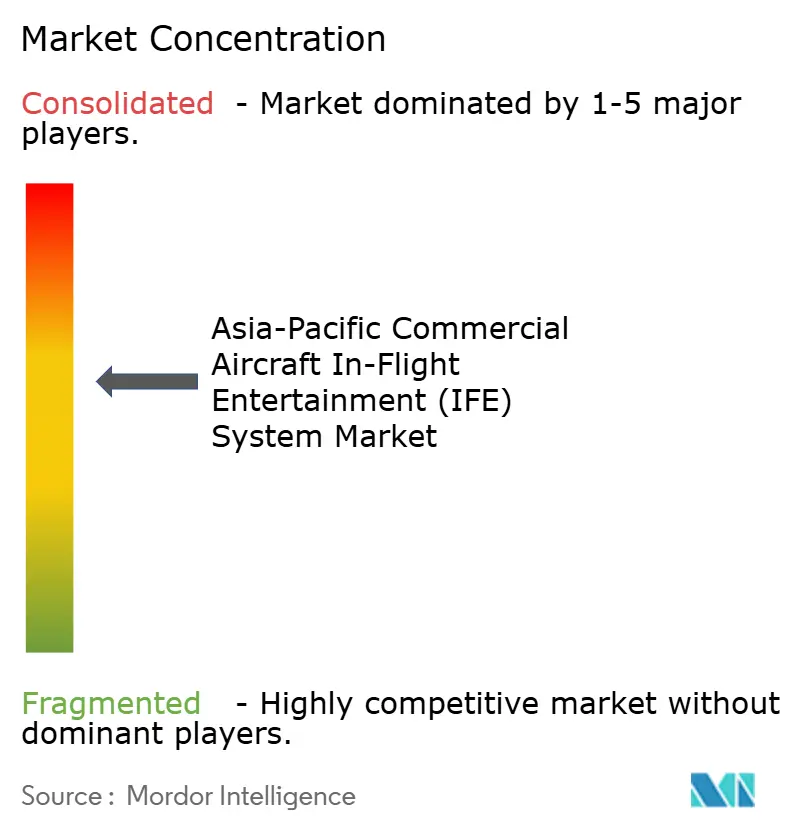

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Commercial Aircraft In-Flight Entertainment System Market Analysis by Mordor Intelligence

The Asia-Pacific commercial aircraft IFE system market size is estimated at USD 609.50 million in 2025 and is projected to reach USD 958.60 million by 2030, at a CAGR of 9.49% during the forecast period. This trajectory underscores how post-pandemic fleet modernization, rising low-cost-carrier (LCC) traffic, and mandatory connectivity mandates reshape onboard digital experiences. Operators are replacing aging hardware with lighter, cloud-managed platforms to lower fuel burn while satisfying passengers who increasingly treat in-flight connectivity (IFC) as a basic utility. Airlines are also turning seat-centric screens into retail storefronts, integrating biometric payments and advertising engines to generate ancillary income. China’s 2026 high-speed connectivity law, India’s traffic surge, and a 180-satellite LEO constellation geared to the region collectively cement Asia-Pacific as the global testing ground for end-to-end digital cabins.

Key Report Takeaways

- By aircraft type, narrowbody jets commanded 63.72% of the Asia-Pacific commercial aircraft IFE system market share in 2024 and will expand at a 9.15% CAGR through 2030.

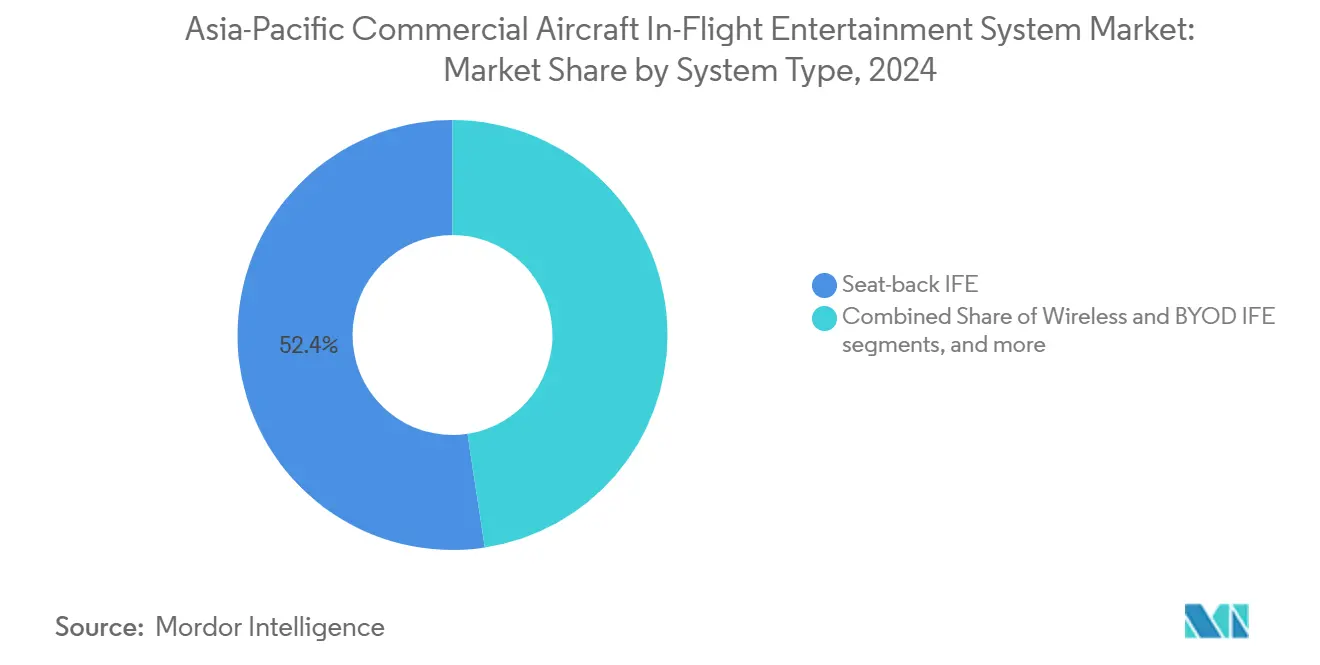

- By system type, wireless and BYOD platforms are projected to post the fastest growth, with a 10.40% CAGR, while embedded seat-back systems still held a 52.40% revenue share in 2024.

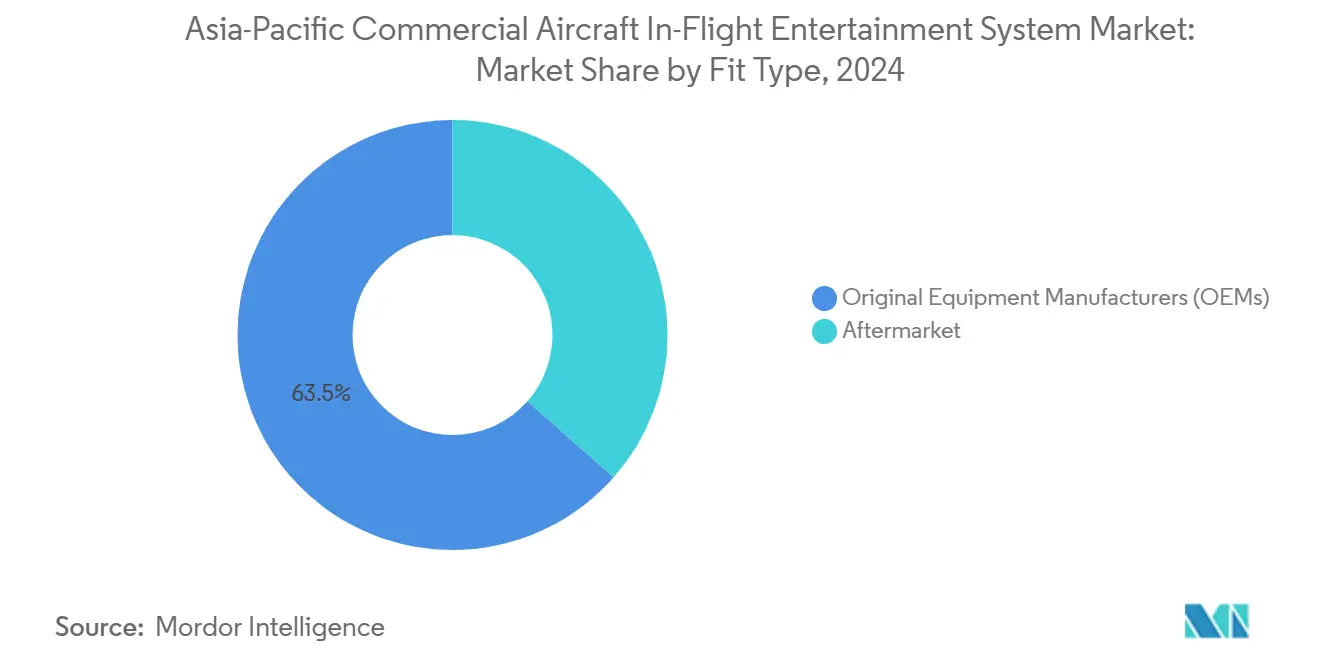

- By fit type, OEM fitment accounted for 63.50% of deployments in 2024; aftermarket programs are growing at a 9.70% CAGR due to weight-saving wireless upgrades.

- By cabin class, economy cabins contributed 51.80% revenue in 2024, whereas premium economy led growth at an 8.75% CAGR to 2030.

- By country, China accounted for 43.46% of the Asia-Pacific commercial aircraft IFE system market share in 2024, while Indonesia is projected to grow at a 7.12% CAGR.

Asia-Pacific Commercial Aircraft In-Flight Entertainment System Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-pandemic fleet expansion and LCC route proliferation | +1.8% | Core APAC, spill-over to Southeast Asia | Medium term (2-4 years) |

| Mandatory high-speed connectivity on Chinese trunk routes | +1.5% | China; secondary effect on regional carriers | Short term (≤2 years) |

| Airlines’ shift to ancillary-revenue digital platforms | +1.2% | Singapore, Japan, wider APAC | Medium term (2-4 years) |

| Lightweight wireless-IFE retrofits lowering fuel burn | +1.0% | Regional carriers scaling to mainline fleets | Long term (≥4 years) |

| 180-satellite APAC LEO constellation launch | +0.9% | Japan, South Korea, broader APAC | Medium term (2-4 years) |

| Embedded-seat biometric payment pilots on Singapore-based carriers | +0.6% | Singapore; potential regional rollout | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Post-pandemic fleet expansion and LCC route proliferation

Domestic traffic in Asia-Pacific exceeded 2019 levels during early-2024, prompting bulk aircraft orders and accelerating wireless IFE procurement by carriers keen to avoid the downtime of seat-back retrofits.[1]International Air Transport Association, “Asia-Pacific’s Air Travel Market: Opportunities and Challenges,” IATA.ORG AirAsia’s fleet-wide Ka-band upgrade and Vietjet Thailand’s rapid Blueview rollout show how LCCs favor turnkey wireless solutions that scale with high-frequency short-haul schedules. Point-to-point networks in Indonesia, Vietnam, and Thailand intensify demand for platforms installed overnight and updated over-the-air. These dynamics force legacy suppliers to pivot from heavy seat-back hardware to app-centric ecosystems that can monetize every passenger touchpoint.

Mandatory high-speed connectivity on Chinese trunk routes (2026)

China’s Civil Aviation Administration (CAAC) now requires multi-megabit broadband on trunk routes by 2026, pushing carriers to accelerate satellite-antenna installations and software certification.[2]Civil Aviation Administration of China, “Unified Authentication Interface Specifications MH/T 3032-2023,” CAAC.GOV.CN The agency’s unified-authentication interface standard governs how portals, payment engines, and passenger devices authenticate, effectively setting a regional technical baseline. International airlines serving China must retrofit qualified hardware, driving a ripple effect across neighboring markets as fleets are optimized for cross-border compliance. Early movers such as China Southern are already marketing real-time streaming and e-commerce onboard, validating the commercial upside of regulation-driven adoption.

Airlines’ shift to ancillary-revenue digital platforms

Cabin connectivity is no longer a sunk cost. Boeing’s Digital Direct retrofit kit lets carriers blend wireless IFE with onboard retail and catering workflows, squeezing revenue from ads, food pre-ordering, and destination activities.[3]Boeing, “Boeing Digital Direct,” BOEING.COM Singapore Airlines invests in 4K displays and curated content to justify fare premiums, while AirAsia equips crew with tablet-based point-of-sale tools to shorten transaction times. Introducing biometric seat-integrated payments in Singapore reduces checkout friction, enabling real-time upselling based on loyalty and flight context.

Lightweight wireless-IFE retrofits lowering fuel burn

A TE Connectivity 2024 white paper shows that replacing heavy copper cabling with single-pair Ethernet can cut wiring weight by 73%, translating to tangible fuel and carbon savings.[4]TE Connectivity, “Aerospace Cabin Connectivity Weight Reduction White Paper,” TE.COM Wireless/BYOD platforms eliminate hundreds of screens, freeing airlines to install slimmer seats or add extra rows. Regional operators embracing narrowbody high-density layouts thus view wireless IFE as a passenger-service upgrade and a cost-avoidance strategy. These savings help justify retrofit programs even amid tight capital budgets.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High STC certification costs for multi-orbit antennas | -1.2% | Regional carriers scaling to mainline | Medium term (2-4 years) |

| Cabin weight penalties for legacy seat-back systems | -0.9% | Fleets with older widebodies | Long term (≥4 years) |

| Spectrum-coordination delays in ASEAN corridors | -0.8% | Southeast Asian flights | Short term (≤2 years) |

| Cyber-hardening gaps in older Linux IFEC servers | -0.6% | Operators with legacy platforms | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High STC certification costs for multi-orbit antennas

Supplemental type-certificate packages for tri-band antennas can exceed USD 1 million per aircraft and add six to twelve months to retrofit timelines, discouraging smaller carriers from adopting next-gen connectivity.[5]Independent Aircraft Modifier Alliance, “Standardizing Supplemental Type Certificates,” IAMALLIANCE.AERO OEM linefit options amortize this cost over larger production runs, tilting the field toward new deliveries and away from in-service upgrades.

Cabin weight penalties for legacy seat-back systems

Traditional widebody wiring looms weigh nearly 1,800 kg and incur annual fuel outlays approaching USD 0.40 million per aircraft. Airlines juggling older fleets must weigh downtime and structural rework against passenger-experience parity, leading some to strip screens altogether on high-frequency regional routes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Wireless Platforms Outpace Embedded Hardware

Seat-back units still held a 52.40% share in 2024, reflecting legacy linefit pipelines; yet, wireless and BYOD solutions are racing ahead at a 10.40% CAGR. Airlines like Vietjet Thailand rolled out Blueview across 18 A320-family aircraft within a quarter, underscoring the speed advantage of tablet streaming hubs that mount in overhead bins. Premium brands counter by raising display quality to 4K HDR and adding Bluetooth audio pairing, preserving embedded appeal on ten-hour sectors.

Hybrid approaches are gaining favor. New seat architectures embed slim tablets that detach for BYOD service on short hops but dock to provide seat-controlled sessions on long journeys. Supplier competition, therefore, tilts toward software extensibility, open APIs, app stores, and real-time analytics, more than raw screen counts.

By Aircraft Type: Narrowbody Jets Anchor Growth

The segment generated 63.72% of the Asia-Pacific commercial aircraft IFE system market revenue in 2024 and is tracking a 9.15% CAGR through 2030. Narrowbody demand hinges on domestic and regional routes where rapid turnaround calls for lightweight wireless kits that minimize maintenance downtime. Operators such as Malaysia Aviation Group plan A321neo cabin upgrades alongside A330neo long-haul replacements, signaling a hybrid fleet strategy that balances cost and premium experience. Widebody programs remain critical for brand differentiation on intercontinental services, with Cathay Pacific installing 4K seat-back displays and fleet-wide Wi-Fi in 2025.

Second-order impacts cascade into supplier portfolios: embedded specialists now tailor modular seat architectures for stretched narrowbody cabins. At the same time, wireless vendors design server-less mesh networks to serve 200-plus seats without rack-space penalties. As LCCs open thin routes, narrowbody buyers seek off-the-shelf content packages localized for Vietnamese, Bahasa, or Thai audiences, adding complexity to digital-rights workflows across the supply chain.

By Fit Type: Retrofits climb on weight and schedule pressures

OEM installations accounted for 63.50% revenue in 2024. However, retrofit programs are accelerating at a 9.70% CAGR as delivery-slot shortages prompt airlines to extend asset utilization and as wireless kits mature into overnight installations. All Nippon Airways began upgrading its B767-300ERs with Viasat hardware in August 2025, utilizing heavy-maintenance windows to standardize connectivity across its mixed fleet. Retrofit vendors offer power-only kits that avoid fuselage cuts, lowering certification hurdles and shortening ground time.

Regulatory bottlenecks persist, particularly for multi-orbit antennas that require bespoke STCs. Still, rising fuel prices and sustainability targets strengthen the ROI argument as every kilogram saved translates to measurable emissions cuts. Airlines are increasingly bundling retrofits with cabin refreshes to spread engineering costs across multiple upgrade lines.

By Cabin Class: Premium economy leads incremental revenue

The economy accounted for 51.80% of 2024 spending. Yet, the premium economy is forecast to expand at 8.75% CAGR through 2030 as Asia-Pacific middle-class travellers trade up for extra comfort and streaming bandwidth. Carriers are fitting 13-inch 4K displays, Bluetooth pairing, and high-power USB-C outlets in premium-economy shells to justify fare stepping. EVA Air’s 2025 Astrova deal covers 54 aircraft with OLED screens and an e-commerce portal that personalizes duty-free offers based on loyalty data.

Business-class and first-class investments concentrate on privacy suites with 32-inch panels and zero-latency mirroring from personal devices. However, airlines are careful to avoid cost creep, leveraging modular seat electronics that share common media servers across classes to cap spares inventory.

Geography Analysis

China remains the largest buyer, propelled by mandatory broadband and the “Air Silk Road” strategy that upgrades Beijing, Shanghai, and Guangzhou into digital hubs. Domestic RPKs surpassed pre-COVID peaks in 2024, and carriers must certify portals that handle multilingual content and facial-verification payment flows to meet regulator guidelines. The requirement pulls global airlines into compliance when operating trunk routes, standardizing hardware choices across regional fleets.

India is the fastest-growing territory as it will become the third-largest passenger market by 2027. Indigo and Air India expand widebody networks and retrofit narrowbodies with streaming kits that support Hindi, Tamil, and Bengali interfaces. Air India’s 2025 Astrova order showcases a pivot to premium service on US and European routes while maintaining wireless economics on domestic stages. Regulatory clarity around in-flight Wi-Fi since 2024 has accelerated investment.

Japan and South Korea are early adopters of multi-orbit antennas, leveraging the 180-satellite LEO constellation to guarantee low-latency sessions on dense trans-East Asian corridors. Meanwhile, Indonesia, Thailand, Malaysia, and the Philippines push LCC penetration above 50%, making them laboratories for ultra-light, pay-as-you-go streaming platforms. Spectrum coordination delays inside ASEAN still slow seamless roaming offers, yet the ongoing policy dialog aims to set a multilateral template by 2027.

Competitive Landscape

The Asia-Pacific commercial aircraft IFE system industry features a moderately concentrated field. Panasonic Avionics, Thales, and Collins Aerospace hold long-term supply contracts that secure content bundles, seat-back monitors, and global support networks. New entrants focus on software-defined, hardware-agnostic models that pivot around portable servers and subscription analytics.

Airbus-Panasonic’s 2025 MoU couples an open HBCplus avionics backbone with the Converix cabin server, letting airlines plug in apps for maintenance, e-commerce, or wellness monitoring without rewiring. Thin-profile antennas from multiple vendors compete on drag coefficients and LEO-GEO handoff algorithms, though high certification costs remain a barrier for tier-two airlines.

Strategic alliances increasingly target payment integration. Thales and Singapore-based carriers co-develop biometric checkout, while Boeing markets Digital Direct as an ancillary revenue accelerator rather than a cost center. Airlines weigh vendor selections on screen resolution and roadmap transparency, cybersecurity credentials, and the ability to split revenue from ads, shopping, and data insights.

Asia-Pacific Commercial Aircraft In-Flight Entertainment System Industry Leaders

Thales Group

Panasonic Holdings Corporation

LATECOERE S.A.

Burrana Pty Ltd.

Imagik Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Cathay Pacific finished equipping every aircraft with seat-back 4K displays and full-fleet Wi-Fi, offering free connectivity to premium passengers.

- August 2025: All Nippon Airways (ANA) implemented the free Viasat IFC across all international classes on its B767-300ER aircraft. The airline aims to install Wi-Fi services on more than 80% of its international fleet by 2030.

- June 2025: VietJet Thailand partnered with Bluebox Aviation Systems to introduce an IFE service powered by the Blueview digital platform.

- April 2025: Airbus signed a Memorandum of Understanding (MoU) with Panasonic Avionics to explore a strategic partnership for the future Connected Aircraft platform. Both parties plan to develop a new on-board architecture using Panasonic Avionics' next-generation IFE hardware and software server platform, Converix, subject to a definitive agreement expected later in 2025.

Asia-Pacific Commercial Aircraft In-Flight Entertainment System Market Report Scope

Narrowbody, Widebody are covered as segments by Aircraft Type. China, India, Indonesia, Japan, Singapore, South Korea are covered as segments by Country.By Aircraft Type

| Narrowbody Aircraft |

| Widebody Aircraft |

| Regional Jets |

By System Type

| Seat-back IFE |

| Wireless and BYOD IFE |

| In-seat Power and Peripherals |

By Fit

| Original Equipment Manufacturers (OEMs) |

| Aftermarket |

By Cabin Class

| First |

| Business |

| Premium Economy |

| Economy |

By Country

| China |

| India |

| Indonesia |

| Japan |

| Singapore |

| South Korea |

| Rest of Asia-Pacific |

| By Aircraft Type | Narrowbody Aircraft |

| Widebody Aircraft | |

| Regional Jets | |

| By System Type | Seat-back IFE |

| Wireless and BYOD IFE | |

| In-seat Power and Peripherals | |

| By Fit | Original Equipment Manufacturers (OEMs) |

| Aftermarket | |

| By Cabin Class | First |

| Business | |

| Premium Economy | |

| Economy | |

| By Country | China |

| India | |

| Indonesia | |

| Japan | |

| Singapore | |

| South Korea | |

| Rest of Asia-Pacific |

Market Definition

- Product Type - Entertainment provided to aircraft passengers during a flight refers to In-flight entertainment. The seatback screens which are used to provide entertainment are included under the IFE system product type.

- Aircraft Type - All the passenger aircraft such as narrowbody and widebody which are single-aisle and twin-aisle are included in this study.

- Cabin Class - Business and First Class, economy and premium economy are classes of air travel provided by the airlines that offer various services to the passengers.

| Keyword | Definition |

|---|---|

| Gross domestic product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| High Dynamic Range (HDR) | Dynamic range describes the ratio between the brightest and darkest parts of an image. HDR is used to capture a greater dynamic range than SDR. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| European Aviation Safety Agency (EASA) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| 4K Display | 4K resolution refers to a horizontal display resolution of approximately 4,000 pixels. |

| Organic Light Emitting Diode (OLED) | It is the light-emitting diode (LED) in which the emissive electroluminescent layer is a film of organic compound that emits light in response to an electric current. |

| Mean Time Between Failures (MTBF) | The mean time between failures is the predicted elapsed time between inherent failures of a mechanical or electronic system, during normal system operation. |

| (Low-Cost Carrier (LCCs) | It is an airline that is operated with an especially high emphasis on minimizing operating costs and without some of the traditional services and amenities provided in the fare |

| Electronically Dimmable Windows (EDW) | It is a type of window that blocks up to 99.96% of all visible light and provide full opacity, integrated into the window cassette of the sidewall panel. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step 1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step 2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step 3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step 4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms