Cementitious Grout Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

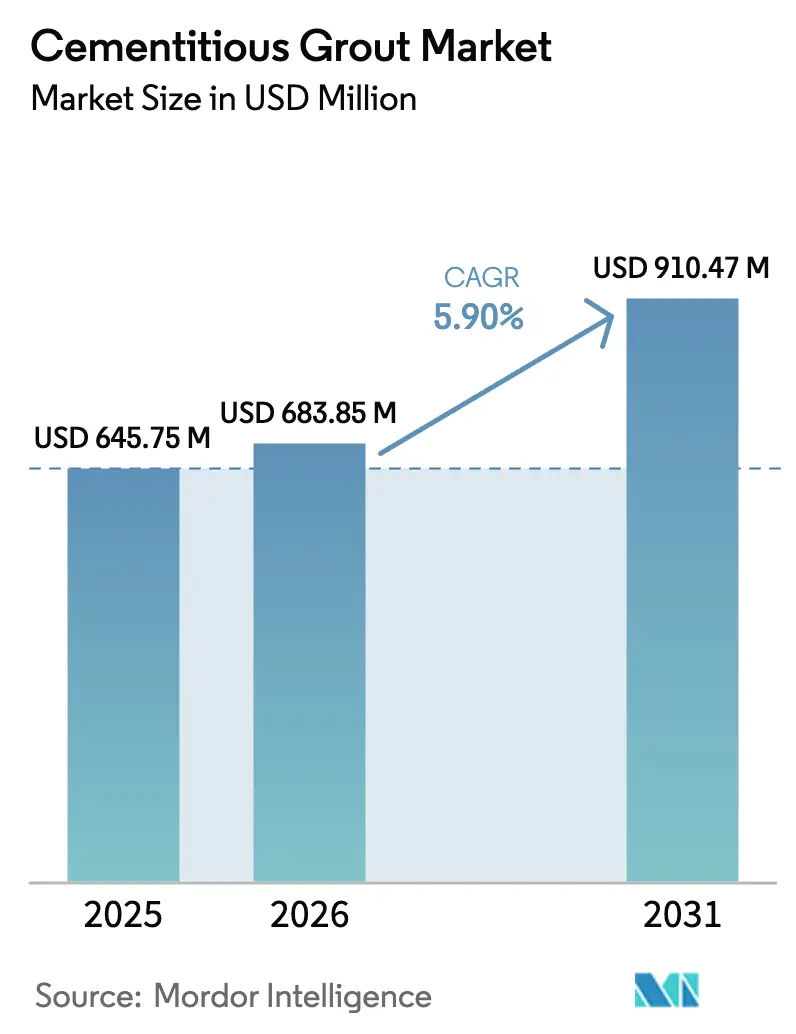

| Market Size (2026) | USD 683.85 Million |

| Market Size (2031) | USD 910.47 Million |

| Growth Rate (2026 - 2031) | 5.90% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cementitious Grout Market Analysis by Mordor Intelligence

Cementitious Grout market size in 2026 is estimated at USD 683.85 million, growing from 2025 value of USD 645.75 million with 2031 projections showing USD 910.47 million, growing at 5.90% CAGR over 2026-2031. The expansion reflects steady demand from transportation corridors, utility upgrades, and industrial facilities that require durable connection materials. Intensifying urbanization, performance-based construction specifications, and the need for vibration-resistant foundations continue to propel the cementitious grout market across both developed and emerging regions. The Asia-Pacific region remains the principal growth engine, as governments continue to finance megaprojects that rely on precision grouting to extend the structural service life. Meanwhile, manufacturers are increasingly relying on shrink-compensated formulations to limit settlement, a feature that encourages long-term asset managers to select premium blends despite the higher upfront costs. Raw-material volatility and skilled-labor shortages temper profitability; yet, ongoing innovation in ultra-fine cements and rapid-setting additives offsets these headwinds, supporting stable adoption even in price-sensitive segments.

Key Report Takeaways

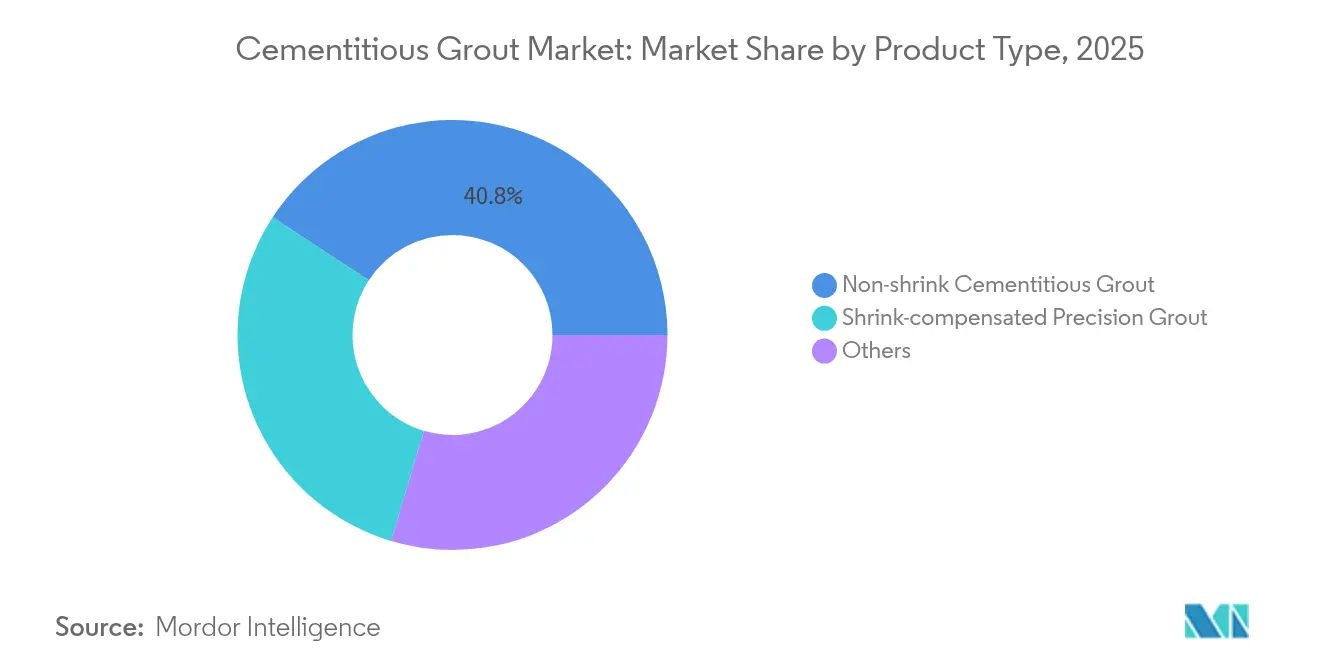

- By product type, non-shrink cementitious grout led the cementitious grout market, accounting for a 40.78% share in 2025, and is forecast to expand at a 6.28% CAGR through 2031.

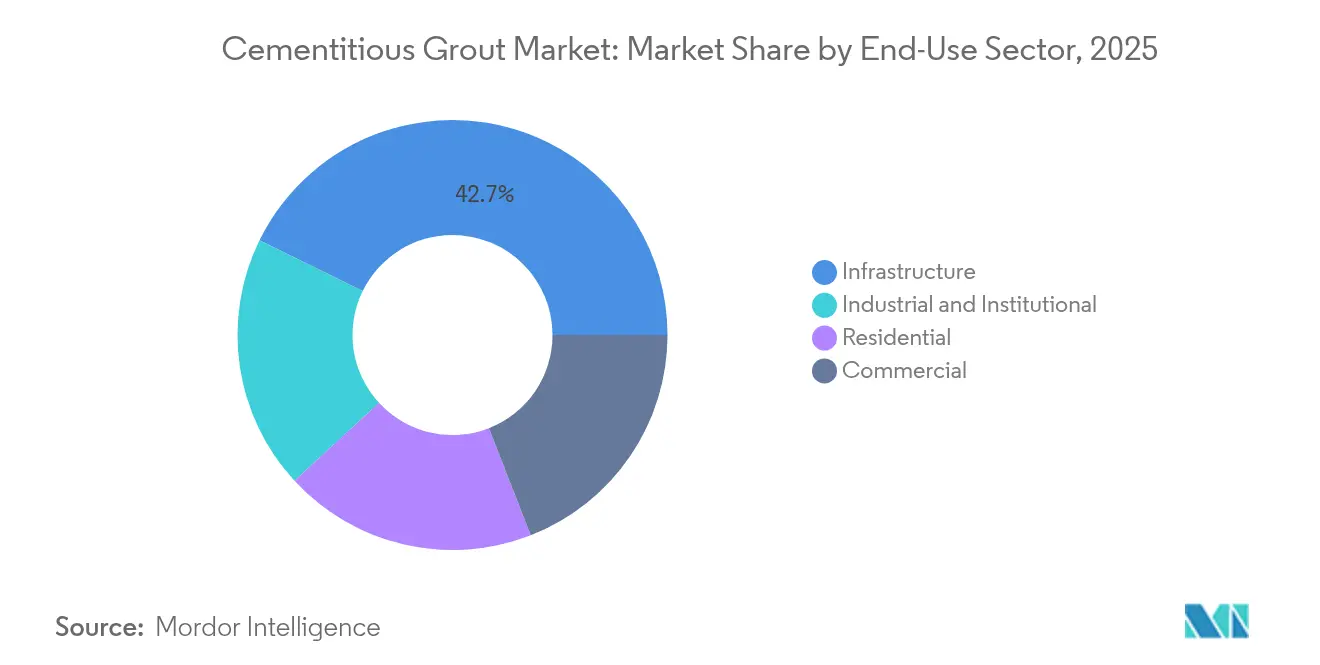

- By end-use sector, infrastructure captured a 42.74% revenue share of the cementitious grout market size in 2025; the residential segment is projected to advance at a 7.03% CAGR through 2031.

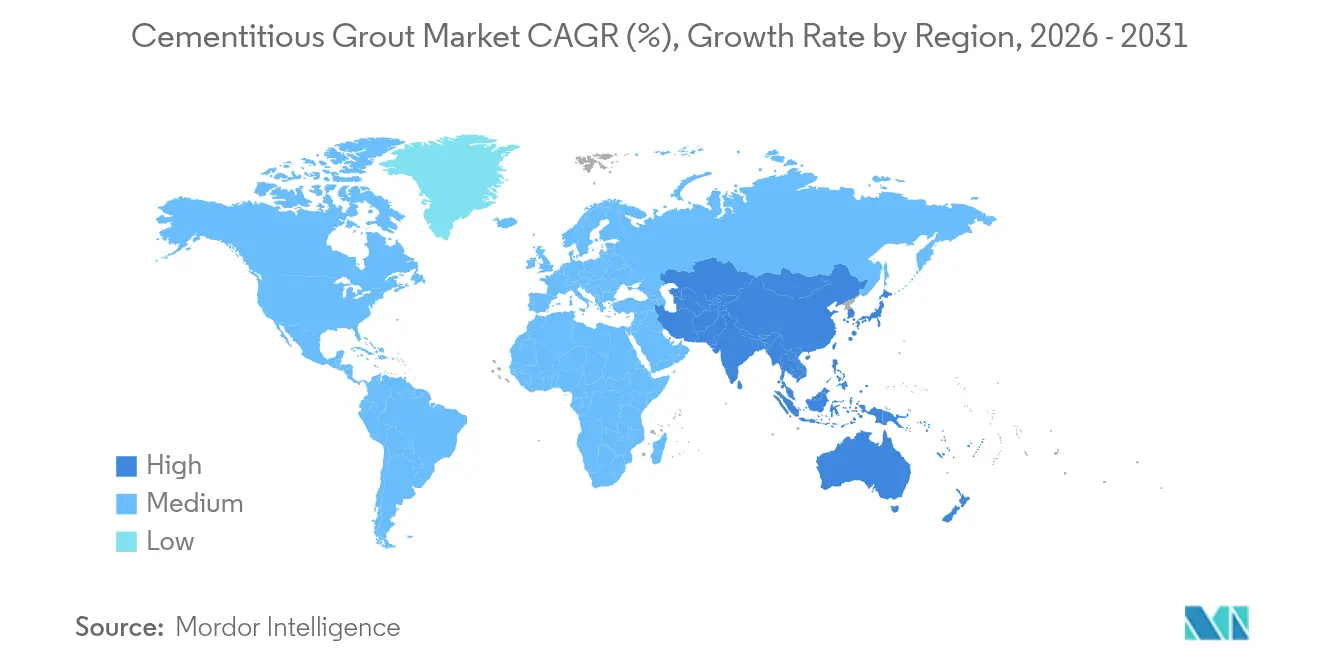

- By geography, Asia-Pacific commanded 40.35% of the cementitious grout market in 2025 and is projected to rise at a 6.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Cementitious Grout Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanisation-fuelled infrastructure spending | +1.8% | Global, with APAC leading at 65% contribution | Medium term (2-4 years) |

| Increasing adoption of shrink-compensated, non-shrink formulations | +1.2% | North America and EU primarily, expanding to APAC | Long term (≥ 4 years) |

| Precision machinery installation requirements in industrial facilities | +0.9% | Global, concentrated in manufacturing hubs | Short term (≤ 2 years) |

| Surge in offshore wind foundations needing ultra-high-strength grouts | +0.7% | Europe and North America coastal regions | Long term (≥ 4 years) |

| Performance-based specifications replacing prescriptive mixes | +0.6% | Developed markets initially, global adoption | Medium term (2-4 years) |

| Demand for ultra-fine cements enabling micro-fracture sealing | +0.5% | Global, with infrastructure-heavy regions leading | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Urbanization-Fueled Infrastructure Spending

Large-scale rail, highway, and metro developments now dominate public-works pipelines across high-growth economies. Asia alone requires USD 26 trillion in cumulative infrastructure funding through 2030, and each tunnel segment, bridge bearing, and utility vault consumes specialty grout to achieve service-life expectations[1]Asian Development Bank, “Asia Needs to Invest $26 Trillion in Infrastructure to 2030,” adb.org . The cementitious grout market, therefore, expands in lockstep with city-building, particularly where transit corridors cut through weak alluvial soils that demand low-shrink products to deter post-construction settlement. Contractors are also selecting rapid-setting options to keep traffic disruptions minimal in dense urban cores. Coupled with smart-city programs that embed sensors into concrete assemblies, the need for dimensionally stable grouts capable of protecting embedded electronics continues to climb, reinforcing a growth path that outperforms general construction spending.

Increasing Adoption of Shrink-Compensated, Non-Shrink Formulations

Bridge decks, precast column pockets, and heavy-equipment bases often experience micro-voids and shrinkage-induced gaps. Shrink-compensated mixes counteract this problem by expanding slightly during curing, thereby maintaining contact pressure and eliminating the need for long-term maintenance. Field data from U.S. transportation departments indicate that 40% fewer intervention events occur when non-shrink formulations replace conventional Portland cements, leading engineers to incorporate shrinkage compensation into procurement language[2]Colorado Department of Transportation, “Shrink-Compensated Grout Performance Study,” codot.gov. European repair codes, notably EN 1504-6, also specify expansion properties, which incentivize suppliers to offer pre-verified products that arrive with laboratory expansion curves for multiple humidity ranges. As contractors become comfortable with dosage controls, demand for these premium blends filters into emerging markets, lifting the cementitious grout market beyond its historical commodity status.

Precision Machinery Installation Requirements in Industrial Facilities

Semiconductor fabs and pharmaceutical cleanrooms house equipment whose calibration tolerance measures in microns. Any baseplate movement triggers costly downtime, so operators rely on ultra-fine cementitious grout that flows easily yet cures into a stable matrix. The cementitious grout industry has responded with blends containing particles below 10 microns and tailored rheology that allows full encapsulation in confined plinths. Once set, these products deliver vibration-dampening comparable to epoxy systems yet hold a cost advantage at scale. Adoption is particularly intense in Asia-Pacific manufacturing clusters that build new fabs to meet electronics demand, further reinforcing regional consumption patterns for high-value grout grades.

Surge in Offshore Wind Foundations Needing Ultra-High-Strength Grouts

Offshore wind developers poured 8.8 GW of new capacity in 2024, and each turbine relies on annular grout to connect monopile sections. Marine-grade cementitious grout must resist chloride ingress, cyclic fatigue, and freeze-thaw loading while achieving compressive strengths above 80 MPa. Those demanding criteria elevate average material costs, yet they also position suppliers with specialized formulations to command premium margins. The European Union’s 60 GW offshore target implies a USD 2.1 billion opportunity for high-strength grouts, an amount that bolsters long-run sales projections for the cementitious grout market. Parallel policy support in the United States broadens the customer base, solidifying global revenue visibility for manufacturers with proven records of marine performance.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of raw materials supply chains | -1.4% | Global, with emerging markets most affected | Short term (≤ 2 years) |

| Skill gap in correct grout placement practices | -0.8% | Global, particularly acute in developing regions | Medium term (2-4 years) |

| Rising competition from epoxy/PU hybrids in heavy-duty niches | -0.6% | Developed markets initially, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility of Raw Materials Supply Chains

Cement producers experienced an average 18% price hike in 2024 due to energy-cost inflation and freight disruptions, which increased vessel charter rates. Aluminum powder, silica fume, and superplasticizers share a similarly volatile sourcing situation because their supply is concentrated in select regions. Tariffs, such as the 25% duty on Canadian cement, directly impact bid prices, forcing smaller grout producers to either sacrifice their margins or exit certain tenders. Larger multinationals mitigate risk by hedging and deploying multi-regional supply contracts; however, not every contractor benefits from this scale advantage, which dampens demand in cost-sensitive projects and creates pockets of substitution using less-expensive but less-capable materials.

Skill Gap in Correct Grout Placement Practices

Grout performance depends on strict adherence to water ratios, mixing sequences, and curing protocols. However, 89% of construction firms worldwide report difficulty hiring qualified field technicians, and the shortage is even more acute for trades that work with specialty chemicals. Incorrect practices can reduce compressive strength by up to 50%, triggering crack propagation and early repairs that erode owner confidence. Certification programs exist, yet uptake varies markedly across regions and is often voluntary. The knowledge gap prompts some project owners to default to epoxy alternatives, despite their higher cost, which curtails potential volume for the cementitious grout market until training initiatives reach wider coverage.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Non-Shrink Formulations Sustain Leadership and Innovation

Non-shrink cementitious grouts accounted for 40.78% of the cementitious grout market share in 2025, and they are expected to continue growing at a 6.28% CAGR through 2031, as engineers prioritize dimensional stability to prevent bearing-pad settlement. The category’s dominance stems from a broad application envelope that spans precast connection sleeves, bridge seats, and machine-base grouting, where long-term compression integrity is critical. Manufacturers expand the portfolio with metallic-powder and calcium-oxide systems that offer calibrated expansion to match ambient temperature bands, reducing field variability and minimizing callbacks. A parallel wave of research and development focuses on rheology modifiers that maintain flow for 45-60 minutes yet achieve initial set in under four hours, a balance that benefits contractors working on tight traffic-management schedules.

Shrink-compensated precision grout, a subset within the same category, continues to outpace the broader cementitious grout market as tighter construction tolerances migrate from specialized industrial projects to mainstream civil works. These formulations consistently deliver compressive strengths exceeding 70 MPa within 24 hours, a property that accelerates equipment commissioning and enables faster lane reopenings during bridge deck repairs. Specialty “other” blends, including underwater grouts and fiber-reinforced mixes, carve out high-margin niches by solving unique placement problems. Although volume remains comparatively modest, the price premium preserves supplier profitability and spurs continuous material science investment across the wider cementitious grout industry.

By End-Use Sector: Infrastructure Leads While Residential Accelerates

Infrastructure accounted for 42.74% of the cementitious grout market in 2025 and continues to draw the largest allocation of public funding. Subway expansions, bridge retrofits, and utility tunnels all rely on dense, non-shrink material to transfer loads and limit water ingress. Governments now attach performance-based clauses to contracts, encouraging the switch to premium grouts that maintain bond integrity over multi-decade horizons. As a result, infrastructure buyers remain less price-sensitive, sustaining steady volumes and high average selling prices even when raw material costs spike.

Residential construction exhibits the fastest trajectory, with a 7.03% CAGR through 2031, as urban real estate developers adopt precast systems that require grout-tied joints for lateral load transfer. The rapid-assembly advantage shortens project schedules by several weeks, a timeline benefit that offsets the incremental material cost of performance grouts. Growth also stems from retrofit programs that strengthen aging apartment blocks in seismic regions through column-jacketing and beam-end repairs, both of which specify shrink-compensated products. Commercial and industrial facilities continue to experience consistent mid-single-digit growth, bolstered by production-line upgrades that favor ultra-fine formulations, enabling sub-millimeter equipment alignment.

Geography Analysis

The Asia-Pacific region led the cementitious grout market with a 40.35% share in 2025, owing to substantial rail, highway, and energy investments financed under China’s Belt and Road Initiative and India’s National Infrastructure Pipeline. The region is forecast to register a 6.56% CAGR through 2031 as megacities expand their metro networks and coastal provinces accelerate offshore wind farm rollouts. Local producers gain cost advantages from shorter cement supply routes, while multinational groups concentrate on high-performance grades that carry larger margins and satisfy demanding project specifications.

North America and Europe collectively comprise a mature yet technologically advanced customer base. Strong public-works allocations for bridge rehabilitation and corridor electrification sustain baseline demand, and policies that reward lifecycle performance push specifiers to select shrink-compensated mixes over commodity Portland blends. Offshore wind installation along the North Sea and Atlantic seaboard further expands the need for ultra-high-strength marine grouts, reinforcing a premium tilt within the regional product mix.

The Middle East and Africa region demonstrates rising potential, stimulated by Saudi Arabia’s Vision 2030 program and power-station builds across sub-Saharan nations. Extreme daytime temperatures and saline conditions require specialized blends, leading international suppliers to partner with local distributors for technical training. South America remains comparatively small but benefits from Brazilian logistics-corridor upgrades and Chilean mining expansions that rely on high-strength grout for crusher bases and concentrate pipelines. While exchange-rate volatility occasionally defers tender awards, underlying infrastructure deficits imply an upward sales baseline for the cementitious grout market over the planning horizon.

Competitive Landscape

The cementitious grout market exhibits moderate fragmentation. Global leaders invest heavily in product differentiation, creating barriers to entry through patent portfolios, certified test data, and expansive distribution networks. Regional manufacturers leverage lower labor and logistics costs to offer competitive pricing in standard-grade mixes; however, they often lack the necessary laboratory infrastructure to certify performance under evolving codes. Some partner with multinational groups through toll-blending arrangements, enabling quicker response to local tenders while sharing compliance documentation. Innovation centers on ultra-fine cements, hybrid fiber reinforcement, and smart admixtures that adjust rheology on demand, thereby broadening end-use scenarios. Suppliers also deploy digital tools that guide installers through mix-water calculations and temperature adjustments, helping to close the skilled-labor gap by embedding best practices into mobile apps. Competing technologies, particularly epoxy-based hybrids, continue to encroach on heavy-duty niches, such as equipment bases in pulp mills. However, cementitious solutions maintain cost and compatibility advantages when large volumes are required. Environment-focused regulation intensifies scrutiny of embodied carbon, prompting producers to explore portland-limestone cement substitutions and recycled microfillers, a pathway likely to reshape competitive dynamics over the next decade.

Cementitious Grout Industry Leaders

Sika AG

Saint-Gobain

MAPEI S.p.A.

RPM International

Ardex Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Sika AG announced a strategic enhancement to its tile grout product category, aimed at improving brand cohesion, product accessibility, and design flexibility within the cementitious grout segment. As part of this initiative, Sika is integrating the Merkrete grout product line into the SikaTile brand, creating a unified offering that supports both SikaTile and Merkrete tile and stone installation systems. The product includes sanded and unsanded cementitious grouts.

- February 2025: Saint-Gobain has finalized its acquisition of Fosroc, a prominent global player in construction chemicals, significantly enhancing its presence across India, the Middle East, and the Asia-Pacific region. This strategic move, announced in June 2024 and completed in February 2025, marks a pivotal expansion of Saint-Gobain’s construction chemicals portfolio, including cementitious grouts.

Global Cementitious Grout Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Asia-Pacific, Europe, Middle East and Africa, North America, South America are covered as segments by Region.| Non-shrink Cementitious Grout |

| Shrink-compensated Precision Grout |

| Others |

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

| Asia-Pacific | Australia |

| China | |

| India | |

| Indonesia | |

| Japan | |

| Malaysia | |

| South Korea | |

| Thailand | |

| Vietnam | |

| Rest of Asia-Pacific | |

| North America | Canada |

| Mexico | |

| United States | |

| Europe | France |

| Germany | |

| Italy | |

| Russia | |

| Spain | |

| United Kingdom | |

| Rest of Europe | |

| South America | Argentina |

| Brazil | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle-East and Africa |

| By Product Type | Non-shrink Cementitious Grout | |

| Shrink-compensated Precision Grout | ||

| Others | ||

| By End-Use Sector | Commercial | |

| Industrial and Institutional | ||

| Infrastructure | ||

| Residential | ||

| By Geography | Asia-Pacific | Australia |

| China | ||

| India | ||

| Indonesia | ||

| Japan | ||

| Malaysia | ||

| South Korea | ||

| Thailand | ||

| Vietnam | ||

| Rest of Asia-Pacific | ||

| North America | Canada | |

| Mexico | ||

| United States | ||

| Europe | France | |

| Germany | ||

| Italy | ||

| Russia | ||

| Spain | ||

| United Kingdom | ||

| Rest of Europe | ||

| South America | Argentina | |

| Brazil | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle-East and Africa | ||

Market Definition

- END-USE SECTOR - Cementitious grouts consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of cementitious grouts for precast construction and ground stabilization applications are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms