Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

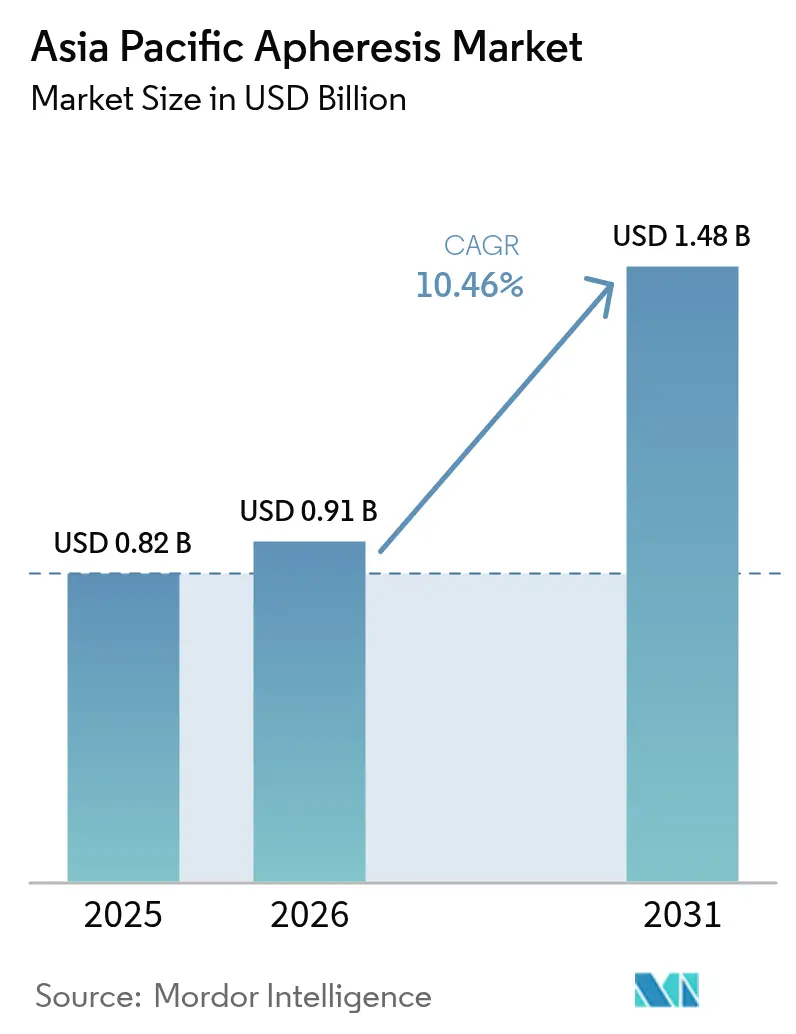

| Base Year Market Size (2025) | USD 0.82 Billion |

| Market Size (2026) | USD 0.91 Billion |

| Market Size (2031) | USD 1.48 Billion |

| Growth Rate (2026 - 2031) | 10.46% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific Apheresis Market Analysis by Mordor Intelligence

The Asia Pacific Apheresis Market size is projected to be USD 0.82 billion in 2025, USD 0.91 billion in 2026, and reach USD 1.48 billion by 2031, growing at a CAGR of 10.46% from 2026 to 2031.

Rising adoption of precision cell-separation platforms that support CAR-T manufacturing, neurology protocols, and national blood-safety programs positions the Asia Pacific apheresis market for sustained double-digit expansion. China’s regulatory push for component separation, Japan’s reimbursement stability, and India’s neurology-driven demand are the dominant revenue anchors. At the same time, membrane-filtration photopheresis, single-use disposables, and outpatient specialty-clinic models are injecting fresh growth vectors. Device vendors that couple equipment placement with technologist training and local manufacturing enjoy a competitive edge as hospitals seek turnkey solutions to offset workforce and capital constraints.

Key Report Takeaways

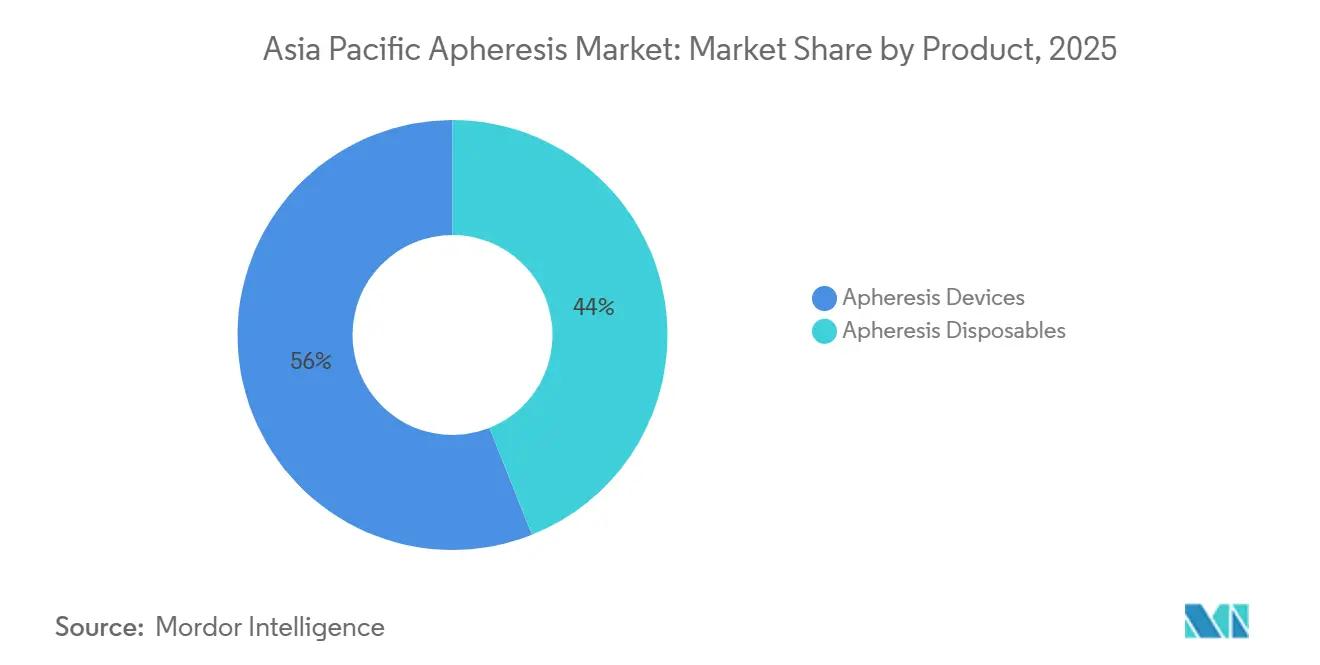

- By product, apheresis disposables accounted for 56.02% of the Asia Pacific apheresis market in 2025; devices are the fastest-growing product segment, with a 11.46% CAGR.

- By procedure type, plasmapheresis led the Asia Pacific apheresis market with 41.67% share in 2025, while photopheresis is projected to advance at a 13.62% CAGR through 2031.

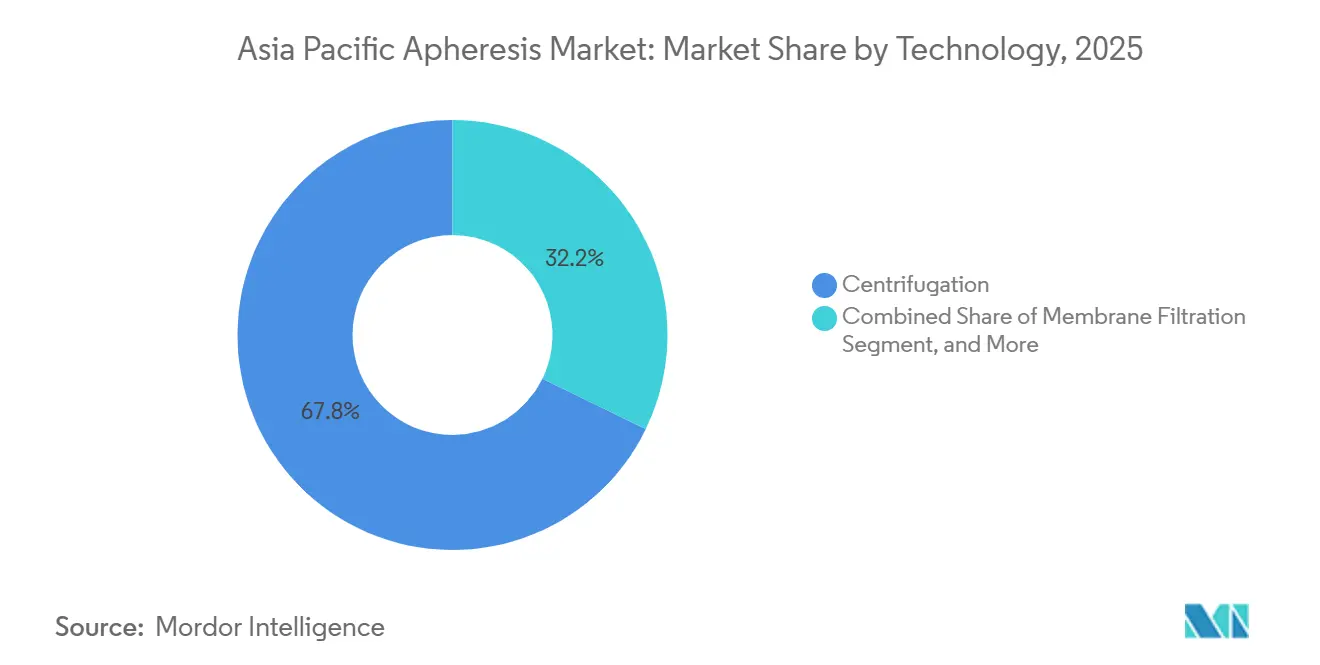

- By technology, centrifugation accounted for 67.79% of revenue in 2025, yet membrane filtration is forecast to expand at a 12.03% CAGR between 2026 and 2031.

- By application, neurology indications accounted for 28.08% in 2025; autoimmune diseases are the fastest-growing application, with a 12.65% CAGR.

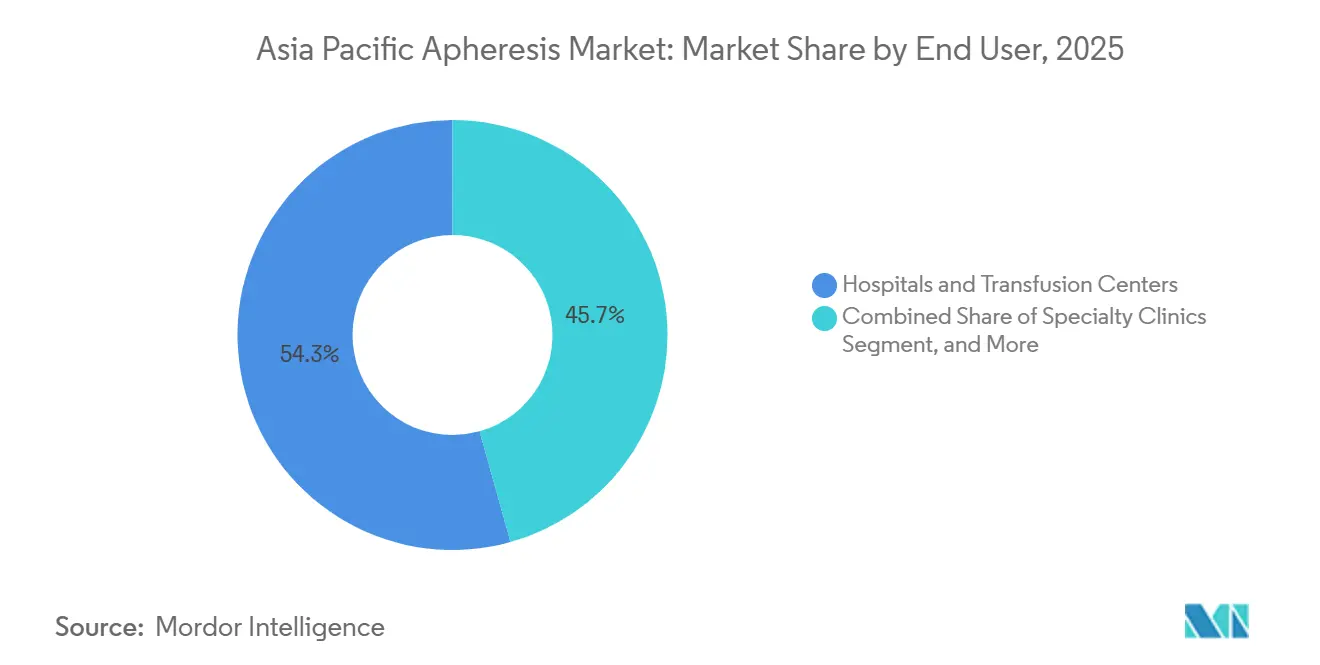

- By end user, hospitals and transfusion centers generated 54.34% 2025 revenue, but specialty clinics are slated to grow at 11.81% CAGR as lower-acuity procedures migrate to outpatient settings.

- By country, China retained 36.78% of the Asia Pacific apheresis market share in 2025; India is the fastest climber, with a 13.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia Pacific Apheresis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence of Hematologic & Autoimmune Disorders | +2.1% | India, China, Japan; spillover to Southeast Asia | Medium term (2-4 years) |

| Rising Demand for Convalescent Plasma Programs | +0.8% | Global, with early adoption in Australia, Singapore | Short term (≤ 2 years) |

| Expansion of Cell & Gene Therapy Manufacturing Hubs in APAC | +2.5% | Japan, Singapore, South Korea, China | Long term (≥ 4 years) |

| Government-Funded Blood-Safety Modernization Initiatives | +1.9% | India, China, Australia | Medium term (2-4 years) |

| Rapid Adoption of Single-Use Apheresis Disposables | +1.4% | China, India, Japan | Short term (≤ 2 years) |

| Accelerated Adoption of Advanced Plasmapheresis Technologies | +1.3% | Japan, South Korea, Australia; diffusion to India, China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Hematologic & Autoimmune Disorders

Neurological autoimmune conditions are reshaping procedure volumes in India, where myasthenia gravis, Guillain-Barré syndrome, and chronic inflammatory demyelinating polyneuropathy already account for more than 60% of therapeutic plasma-exchange cases.[1]Indian Journal of Critical Care Medicine, “Therapeutic Plasma Exchange in Neurological Disorders: A Retrospective Analysis,” journals.lww.com Initiating treatment within seven days of symptom onset drives functional recovery to 83%, prompting emergency departments to pre-authorize apheresis before electromyography confirmation. China’s new reimbursement for hyperviscosity syndrome and Japan’s pediatric-optimized kits are widening the addressable base, while the Southeast Asia TPE Consortium harmonizes protocols across 12 tertiary centers, boosting safety and training capacity.

Rising Demand for Convalescent Plasma Programs

The infrastructure created for COVID-19 now supports readiness for emerging infections. Australia maintains a surge capacity of 500 apheresis donations per week, which can be activated within 72 hours of a public health declaration. Japan invested JPY 2.4 billion in automated platforms that fractionate plasma into hyperimmune globulin concentrates, while China’s draft ISO 13485 guidance would harmonize quality standards and enable stockpiling agreements with Singapore. Selective collection of high-titer units via apheresis has cut downstream fractionation losses by up to 40%, demonstrating the long-term economic rationale of keeping these programs active.

Expansion of Cell & Gene Therapy Manufacturing Hubs In APAC

Japan’s conditional approval pathway has green-lit 17 regenerative therapies since 2019, each starting with leukapheresis.[2]Journal of Clinical Apheresis, “Extracorporeal Photopheresis: Technical Aspects and Clinical Applications,” onlinelibrary.wiley.com Terumo BCT responded by fusing its Global Therapy Innovations unit with its core apheresis division to offer integrated leukapheresis-washing systems that can trim CAR-T production time from 21 to 14 days. China’s Hainan Free Trade Port now grants 15% corporate tax to firms localizing apheresis manufacture, and Singapore earmarked 40% of 2024 biomedical grants for cell-therapy projects, all of which stipulate FACT-JACIE-certified apheresis sourcing.

Government-Funded Blood-Safety Modernization Initiatives

India aims to lift component separation to 70% of total collections by 2028, budgeting INR 8.5 billion (USD 102 million) to procure 450 additional devices. China mandates at least two dual-needle systems at every blood station serving more than 500,000 residents, a move worth about USD 120 million in annual tenders. Australia tightened post-market surveillance following filter delamination events, requiring GS1 traceability for disposables and mandating upgrades to quality management systems.[3]Therapeutic Goods Administration, “Medicine Shortages and Post-Market Surveillance,” tga.gov.au

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital Cost of Apheresis Devices | -1.8% | India, Southeast Asia; moderate impact in Chinese tier-3 cities | Short term (≤ 2 years) |

| Shortage of Trained Apheresis Nurses & Technologists | -1.5% | APAC-wide, acute in India, Indonesia, Philippines | Medium term (2-4 years) |

| Reimbursement Gaps for Therapeutic Procedures | -0.9% | India, China tier-3 cities, much of Southeast Asia | Medium term (2-4 years) |

| Supply-Chain Vulnerability for Filters & Kits | -0.7% | Global, with acute episodes in Australia, New Zealand | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Capital Cost of Apheresis Devices

Equipment prices range from USD 80,000 to USD 250,000, placing them out of reach for many district hospitals where annual equipment budgets fall below USD 500,000. Pay-per-procedure models at USD 150-200 cover placement, kits, and maintenance shift costs, aligning with operating budgets and shortening payback periods, but Chinese volume-based procurement slated for 2026 could drop headline prices by 20-30%, favoring local manufacturers with Class III approvals.

Shortage of Trained Apheresis Nurses & Technologists

Only 15% of Southeast Asian tertiary hospitals retain dedicated apheresis staff, and regional training centers graduate far fewer technologists than demand dictates. Attrition remains high as trainees migrate to higher-pay dialysis roles, prompting vendor-sponsored curricula and remote-mentoring platforms that bundle education with equipment sales.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Disposables Anchor Revenue, Devices Drive Growth

Disposables accounted for 56.02% of the 2025 revenue in the Asia Pacific apheresis market, as every installed separator consumes 200-400 kits annually. Devices remain the growth engine with an 11.46% CAGR thanks to dual-mode centrifugal-membrane platforms that support photopheresis and future CAR-T workflows. Terumo BCT’s integrated leukapheresis-washing system commands 15-20% price premiums yet compresses cell-therapy production timelines by 30%, reinforcing capital-upgrade intent among high-volume centers.

Hospitals in Beijing, Shanghai, and Guangzhou report that single-use kits trimmed labor by 22 minutes per procedure, freeing scarce nurses to manage higher caseloads and directly supporting Asia Pacific apheresis market expansion. Ped-sized 120 mL bowls from Haemonetics now enable safe collection for patients weighing less than 15 kg, carving a niche that strengthens vendor differentiation.

By Procedure Type: Photopheresis Outpaces Legacy Modalities

Plasmapheresis retained 41.67% procedure share in 2025, equaling roughly USD 0.34 billion of the Asia Pacific apheresis market size, underpinned by Japan’s JPY 90,000-384,000 reimbursement band. Photopheresis, however, is expanding at a 13.62% CAGR due to rising second-line use for graft-versus-host disease and new approvals for Crohn’s disease, cutaneous T-cell lymphoma, and solid-organ rejection. Inline photopheresis halves session time, making outpatient models feasible and accelerating adoption across Australia and South Korea.

Leukapheresis volumes grow in tandem with 17 approved Japanese regenerative therapies and 5 new South Korean TIL protocols, each requiring 3-5 sessions per patient. Plateletpheresis growth is capped by donor scarcity, as Japan’s eligible donor pool shrank by 8% since 2020. LDL apheresis remains a niche yet stable treatment and is dominated by Kaneka’s adsorption columns, which spare HDL and coagulation factors.

By Technology: Membrane Filtration Gains on Inline Efficiency

Centrifugation still accounts for 67.79% revenue on the strength of legacy Haemonetics and Terumo fleets, yet membrane filtration is clocking a 12.03% CAGR. Fresenius Kabi’s inline Amicus-Phelix photopheresis module, already installed at 12 Japanese centers, delivers an overall response rate of 71% with just 5.9% adverse events, underscoring its clinical edge. Adsorption columns serve LDL and antibody-mediated transplant rejection, offering selective removal profiles unmatched by other technologies.

China’s forthcoming Unique Device Identification requirement forces all platforms to comply by 2026, harmonizing regulations and smoothing multicountry rollouts, which in turn bolsters Asia Pacific apheresis market penetration.

By Application: Autoimmune Diseases Surge on Clinical Evidence

Neurology indications led with a 28.08% share in 2025, fueled by therapeutic plasma exchange for myasthenia gravis and Guillain-Barré syndrome, which achieves 83% recovery when started early. Autoimmune diseases are the fastest-growing segment, with a 12.65% CAGR, expanding beyond neurology into systemic lupus erythematosus and catastrophic antiphospholipid syndrome. Hematology remains high-value but low-volume, dominated by thrombotic thrombocytopenic purpura, where 24/7 readiness commands premium pricing.

Oncology adds a durable demand layer as every CAR-T therapy starts with leukapheresis, although donor-pool limits keep platelet collections from matching that trajectory. Renal uses grow with rising transplant activity in China and India, where 8-10% of recipients experience antibody-mediated rejection treatable by plasma exchange.

By End-user: Specialty Clinics Capture Outpatient Migration

Hospitals and transfusion centers generated 54.34% of 2025 revenue, but specialty clinics are racing ahead with a 11.81% CAGR. Outpatient models cut session costs by 30-40% by avoiding inpatient bed fees and operating with 1:4 nurse-to-patient ratios. China’s GMP update raises compliance costs for small labs, nudging lower-acuity plateletpheresis and LDL apheresis toward centralized high-volume clinics that can amortize regulatory overheads. Research institutes remain a sub-10% sliver yet drive innovation such as selective T-regulatory-cell apheresis prototypes from Japan’s RIKEN.

Geography Analysis

China held 36.78% market share in the Asia Pacific apheresis market in 2025, propelled by a National Health Commission mandate for component separation and dual-needle acquisitions worth USD 120 million annually. The 2026 Unique Device Identification rule and domestic-content preference under volume-based procurement favor Terumo BCT’s USD 15 million Shenzhen joint venture slated for 2027 production.

Japan offers predictable reimbursement—JPY 90,000-384,000 per plasmapheresis session—and quick device approval cycles that have enabled Fresenius Kabi to install inline photopheresis systems in nearly all transplant centers, trimming adverse events from 14.8% to 5.9%.

India is expanding the fastest, at a 13.28% CAGR through 2031, underpinned by a plan to raise component separation to 70% and fund 450 new devices. Early-intervention protocols for Guillain-Barré and myasthenia gravis deliver 76-83% recovery, strengthening the clinical case for increased capacity.

Australia’s Therapeutic Goods Administration now requires quarterly adverse-event reporting for disposables and reimburses photopheresis at USD 950 per session, encouraging device upgrades. South Korea subsidizes membrane-filtration plasmapheresis at KRW 2.5 million, incentivizing hospitals to transition from aging centrifugal models. The rest of Asia-Pacific shows patchy adoption; Singapore mandates FACT-JACIE-certified apheresis for grant recipients, whereas Indonesia and the Philippines rely on consortium training to standardize protocols.

Competitive Landscape

The Asia Pacific apheresis market is moderately concentrated: Terumo BCT, Haemonetics, Fresenius Kabi, Asahi Kasei, and Baxter together hold roughly 60-65% share, leaving scope for Kaneka, Nikkiso, and emerging contract-service providers. Terumo BCT’s integrated product roadmap bundles leukapheresis, washing, and photopheresis, offering a one-stop platform that resonates with CAR-T developers. Fresenius Kabi differentiates through inline photopheresis, which halves chair time and secures premium pricing.

Haemonetics’ pediatric 120 mL bowl kit strengthens its foothold in a previously underserved segment, while Asahi Kasei leverages adsorption-column know-how in LDL therapy. Contract mobile units in India have demonstrated 40% lower costs than hospital-owned setups, pressuring vendors to roll out pay-per-procedure financing. Regulatory harmonization between China’s UDI and Japan’s ISO 13485 aligns markets, cutting market-entry time for smaller players, making service and training partnerships central to defending incumbents’ market share.

Asia Pacific Apheresis Industry Leaders

B. Braun Melsungen AG

Cerus Corporation

Kaneka Corporation

Terumo Corporation

Asahi Kasei Medical Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Haemonetics Corporation completed the sale of its whole blood assets to GVS S.p.A for USD 67.8 million, including USD 45.3 million upfront and potential earn-outs of USD 22.5 million over four years. This strategic divestiture allows Haemonetics to focus exclusively on its core apheresis business, retaining manufacturing capabilities for automated blood collection devices and disposable kits for platelets, plasma, and red cell collection.

- January 2025: India's Central Drugs Standard Control Organization approved varnimcabtagene autoleucel (var-cel) as the country's second CAR-T cell therapy, priced at approximately USD 60,000 per dose. This approval significantly expands the addressable market for specialized apheresis services required for cell collection and processing in CAR-T therapy protocols.

- November 2024: Terumo Blood and Cell Technologies announced a strategic partnership to localize production in China, investing USD 15 million in Hangzhou manufacturing facilities. The initiative focuses on producing the Trima Accel Automated Blood Collection System and Spectra Optia™ Apheresis System to support the "Healthy China 2030" agenda.

- November 2024: Terumo Blood and Cell Technologies launched its Global Therapy Innovations business unit, merging therapeutic apheresis and cell and gene therapy operations to enhance patient care across the treatment journey. The integration aims to optimize processes for conditions like sickle cell disease and improve access to advanced therapies.

Asia Pacific Apheresis Market Report Scope

Apheresis is a medical technique, where the blood of an individual, either a donor or patient, is passed through an apparatus that separates a particular constituent and returns the rest of the blood to the circulatory system. This is an extracorporeal therapy.

The Asia Pacific Apheresis Market Report is Segmented by Product (Apheresis Devices, Apheresis Disposables), Procedure Type (Plasmapheresis, Plateletpheresis, Leukapheresis, LDL Apheresis, Photopheresis, Other Procedures), Technology (Centrifugation, Membrane Filtration, Adsorption Columns), Application (Neurology, Hematology, Renal Disorders, Autoimmune Diseases, Oncology & Cell Therapy, Other Applications), End-user (Hospitals & Transfusion Centers, Specialty Clinics, Blood Component Providers, Research & Academic Institutes), and Geography (China, Japan, India, Australia, South Korea, Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

By Product

| Apheresis Devices |

| Apheresis Disposables |

By Procedure Type

| Plasmapheresis |

| Plateletpheresis |

| Leukapheresis |

| LDL Apheresis |

| Photopheresis |

| Other Procedures |

By Technology

| Centrifugation |

| Membrane Filtration |

| Adsorption Columns |

By Application

| Neurology |

| Hematology |

| Renal Disorders |

| Autoimmune Diseases |

| Oncology & Cell Therapy |

| Other Applications |

By End-user

| Hospitals & Transfusion Centers |

| Specialty Clinics |

| Blood Component Providers |

| Research & Academic Institutes |

By Country

| China |

| Japan |

| India |

| Australia |

| South Korea |

| Rest of Asia-Pacific |

| By Product | Apheresis Devices |

| Apheresis Disposables | |

| By Procedure Type | Plasmapheresis |

| Plateletpheresis | |

| Leukapheresis | |

| LDL Apheresis | |

| Photopheresis | |

| Other Procedures | |

| By Technology | Centrifugation |

| Membrane Filtration | |

| Adsorption Columns | |

| By Application | Neurology |

| Hematology | |

| Renal Disorders | |

| Autoimmune Diseases | |

| Oncology & Cell Therapy | |

| Other Applications | |

| By End-user | Hospitals & Transfusion Centers |

| Specialty Clinics | |

| Blood Component Providers | |

| Research & Academic Institutes | |

| By Country | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How fast is CAR-T manufacturing growth increasing device demand in Asia Pacific apheresis market?

Leukapheresis volumes linked to 17 Japanese approvals and new South Korean TIL protocols are driving double-digit equipment utilization increases through 2031.

Which application area is the quickest to expand?

Autoimmune diseases are advancing at a 12.65% CAGR on strong evidence for early plasma exchange in neurology and expanding use in systemic lupus and antiphospholipid syndrome.

Why are single-use disposables gaining ground over reusable bowls?

China’s 2026 GMP update raised cleaning-validation costs, and single-use kits cut labor time by 22 minutes per procedure while mitigating cross-contamination risk.

What limits plateletpheresis growth despite stable demand?

Donor-pool shrinkage, especially in aging Japan, constrains collection capacity even as oncology support needs persist.

How does volume-based procurement in China affect equipment pricing?

Centralized tenders expected from 2026 could shave 20-30% off list prices, benefiting local manufacturers and hospitals upgrading legacy fleets.

Page last updated on: