High Speed Cameras Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

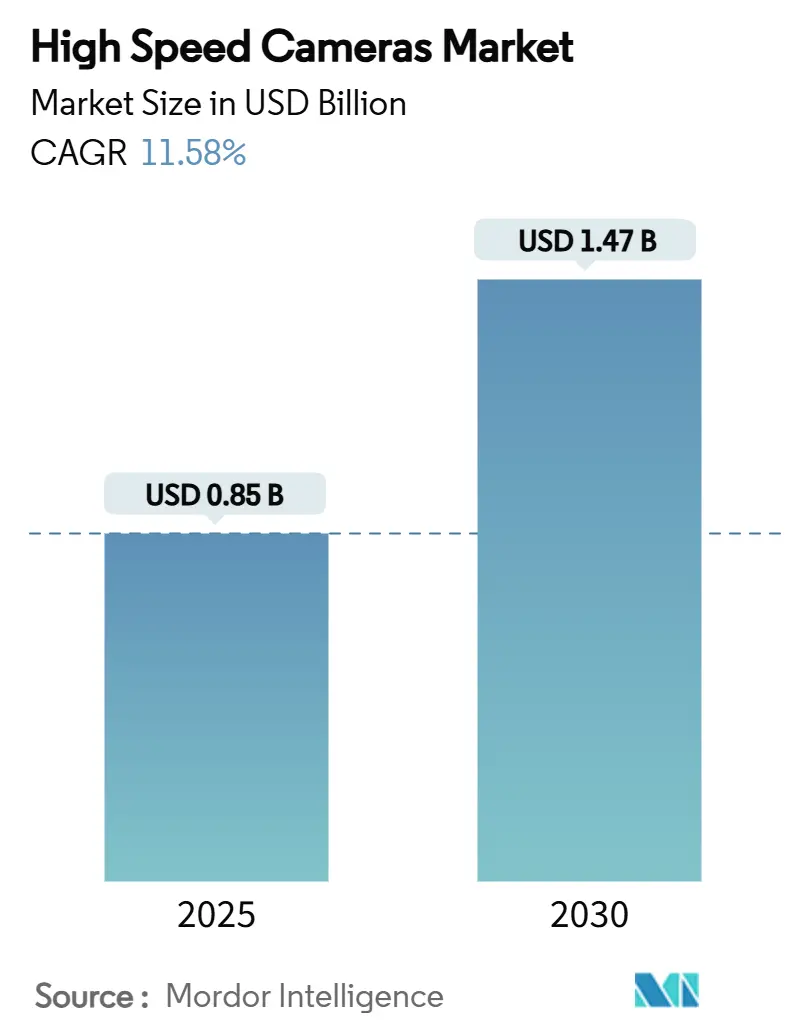

| Market Size (2025) | USD 0.85 Billion |

| Market Size (2030) | USD 1.47 Billion |

| Growth Rate (2025 - 2030) | 11.58% CAGR |

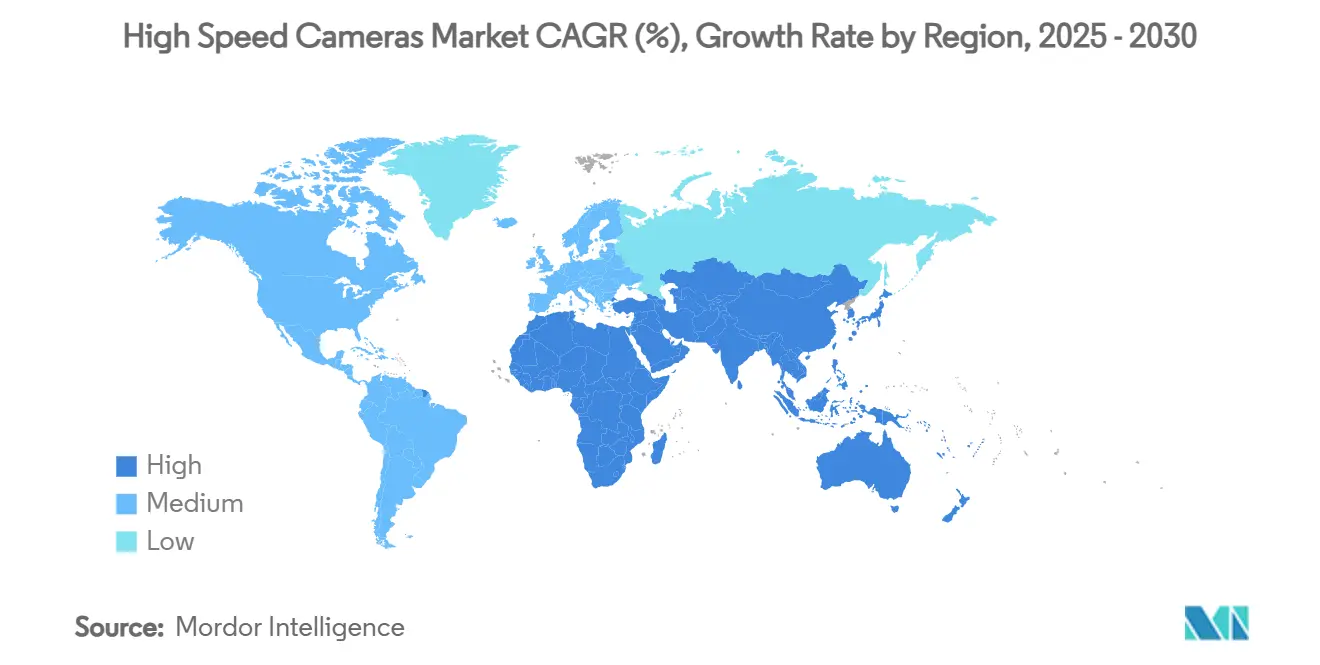

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High Speed Cameras Market Analysis by Mordor Intelligence

The high-speed camera market size is valued at USD 0.85 billion in 2025 and is projected to advance to USD 1.47 billion by 2030, translating to an 11.58% CAGR. Strong uptake stems from the ability of ultra-fast imaging to unravel phenomena that once escaped measurement—ranging from crash-test micro-deformations to hypersonic shock-wave propagation. Semiconductor wafer inspection, autonomous-vehicle safety validation, and live 8K sports broadcasting each demand frame rates well above 1,000 FPS, and often beyond 100,000 FPS. Edge storage cost declines, integration of AI-driven vision analytics, and widening rental access further broaden the customer base. Regional dynamics are shifting as Asia-Pacific fabs and defense agencies scale investment, while North America preserves leadership through defense R&D and premium sports production.

Key Report Takeaways

- By application: Industrial manufacturing led with 29% of high-speed camera market share in 2024; sports analytics and broadcast are expanding at a 14.5% CAGR through 2030.

- By frame rate: The 1,001–5,000 FPS tier commanded 38% share, whereas cameras above 100,000 FPS are forecast to rise at a 15.2% CAGR.

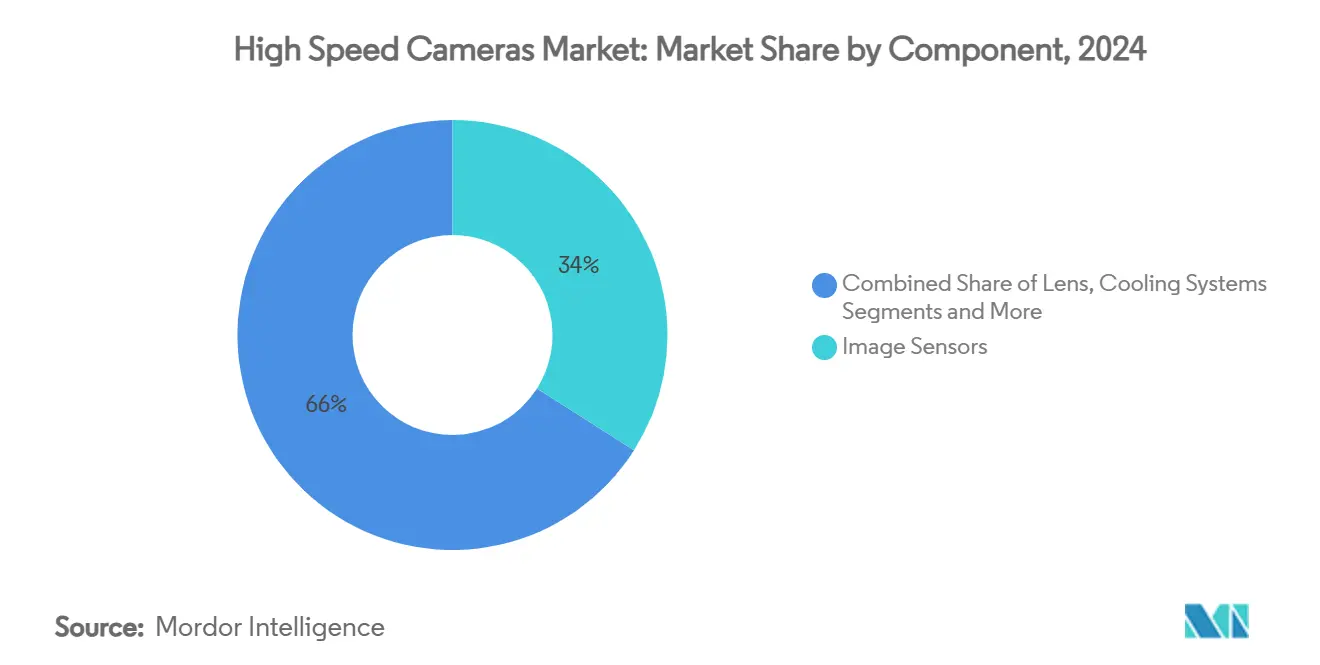

- By component: Image sensors held 34% share in 2024, while memory systems are set to post the quickest 13.8% CAGR.

- By resolution: The 2–5 MP bracket dominated with 42% share; sensors above 5 MP should grow at a 14.8% CAGR.

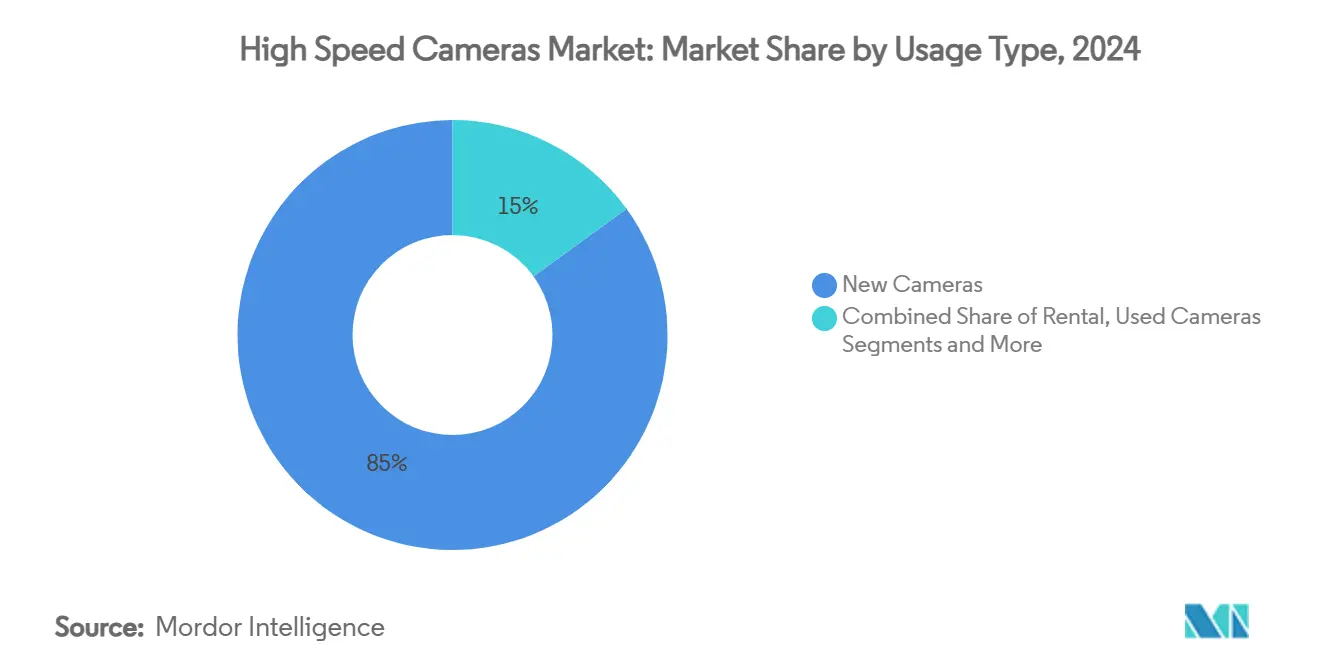

- By usage type: New purchases represented 85% of demand, yet the rental segment is projected to climb at 18% CAGR.

- By geography: North America accounted for 33% revenue in 2024; Asia-Pacific is on track for a 13% CAGR to 2030.

Global High Speed Cameras Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surge in AI-based vision analytics for crash-test labs | +2.1% | Germany & Japan, spillover to North America | Medium term (2-4 years) |

| SWIR high-speed cameras for semiconductor wafer inspection | +1.8% | South Korea & Taiwan, expanding to China | Short term (≤ 2 years) |

| Defense budgets targeting hypersonic weapon testing | +1.6% | U.S. & China, NATO allies | Long term (≥ 4 years) |

| Live 8K sports broadcasting boosting rental uptake | +1.4% | North America & EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Rugged battery-powered cameras for down-hole diagnostics | +0.9% | Middle East, expansion to North America shale | Short term (≤ 2 years) |

| Edge-storage price declines enabling SME adoption | +1.2% | ASEAN core, spillover to Latin America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in AI-Based Vision Analytics for Crash-Test Labs

Crash-test programs now rely on machine-learning algorithms that dissect micro-second deformation, airbag plume propagation, and sensor fusion events. German and Japanese facilities require frame rates beyond 50,000 FPS to deliver the data density that feeds neural-network training, accelerating demand for flagship cameras able to maintain low noise at extreme speeds. Autonomous-vehicle validation compounds the need as every synthetic crash scenario must be documented in granular temporal layers. The co-evolution of high-speed imaging and AI creates a virtuous cycle: richer data improves models, which in turn push frame-rate thresholds higher. Tier-1 suppliers are already embedding high-speed modules inside sleds to ensure direct datalogging. As regulatory bodies tighten passive-safety standards, the driver’s medium-term impact on the high-speed camera market strengthens.[1]“Automotive,” Forza Silicon, forzasilicon.com

Proliferation of SWIR High-Speed Cameras for Semiconductor Wafer Inspection

Advanced logic nodes below 5 nm demand defect detection that visible-light cameras cannot deliver. SWIR imagers, often based on InGaAs, penetrate silicon layers while operating at thousands of frames per second, allowing inline detection of voids, pattern collapse, and micro-contamination during lithography. South Korean and Taiwanese fabs have integrated these cameras across multiple process steps, reducing scrap and elevating line yield. The capital efficiency of SWIR upgrades has influenced procurement standards beyond premium fabs, with foundries in mainland China and Singapore adding similar capability. Thermal-management innovations—liquid-metal heat spreaders and proprietary lens coatings—are helping maintain quantum efficiency at high speeds. These factors underpin the driver’s immediate, short-term weight on market growth.

Defense Budgets Prioritizing Hypersonic Weapon Testing

Hypersonic glide bodies and scramjet stages create optical events too rapid for conventional imaging. Ultra-high-speed cameras exceeding 100,000 FPS, sometimes combined with laser-induced fluorescence, now document Mach-5-plus flows to validate CFD models. U.S. and Chinese defense agencies fund ruggedized sensors that tolerate blast shock and temperature spikes. Proprietary sensor coatings, reinforced data connectors, and integrated vibration isolation funnel R&D spending toward a handful of specialist OEMs. NATO programs replicate this architecture, broadening the installed base. Because hypersonic platforms remain mission-critical in long-range deterrence strategy, the driver provides reliable pull through the decade.

Live 8K Sports Broadcast Accelerating Rental Uptake

8K production workflows need frame rates near 120 FPS to enable ultra-smooth replays. Yet capital expenditure on 8K high-speed rigs rapidly depreciates. Broadcasters therefore rent cameras coupled with high-throughput storage nodes capable of 40 GB/s ingest, such as the BRYCK platform trialed by RED Digital Cinema partners. Rental houses handle calibration, firmware updates, and on-site engineers, reducing downtime for leagues. Episodic sports seasons align with rental economics, while regional rights holders upscale their coverage without locking cash into hardware. The shift reinforces the subscription-like revenue model emerging in the high-speed camera market.

Restraints Impact Analysis*

| RESTRAINTS | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Import tariffs on CoaXPress components raising BOM costs | −1.3% | U.S., secondary NAFTA effects | Short term (≤ 2 years) |

| Thermal noise and cooling needs above 50 k FPS | −0.8% | Global, acute in mobile platforms | Medium term (2-4 years) |

| Shortage of trained high-speed imaging technicians | −0.6% | Emerging markets, expanding to developed regions | Long term (≥ 4 years) |

| Data-stream bottlenecks (>10 Gbps) with legacy factory networks | −0.5% | Europe, industrial automation | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Import Tariffs on CoaXPress Components Raising BOM Costs

Escalating trade duties on specialized CoaXPress chipsets and cables inflate system costs for U.S. assemblers. CoaXPress remains unrivaled for carrying 25 Gbps over coaxial links, so substitution is limited. Vendors absorb part of the surcharge, yet full systems still list 8-12% higher. Incremental redesign toward Ethernet-based alternatives inches forward, but latency and determinism concerns persist. Integrators queue additional stock to hedge tariff swings, straining working capital. While policy could unwind, its short-term drag on the high-speed camera market is tangible.[2]“CoaXPress for High Speed Camera Connection,” Oxford Instruments, andor.oxinst.com

Thermal Noise & Cooling Needs Above 50 k FPS Limiting Portables

Photon shot noise rises with sensor temperature, and at 50,000 FPS the heat load becomes formidable. Deep-TEC assemblies must chill sCMOS sensors to −30 °C to keep noise near 1 e- RMS, adding bulk and power draw. Liquid cooling is sometimes mandatory, particularly for 4K sensors at >100 k FPS. Consequently, portable rigs weigh more than 10 kg, curbing field deployments. Start-ups are piloting microfluidic cold plates, but commercialization remains two-plus years away. The restraint therefore weighs on mid-term growth of mobile sub-segments.[2]

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Memory Systems Drive Innovation

Image sensors captured 34% of 2024 revenue, underscoring their centrality to any high-speed camera market size discussion. Yet memory subsystems are the flashpoint for future gains, climbing at a 13.8% CAGR as buffering demand explodes during 100,000 FPS bursts. Manufacturers integrate stacked DRAM closer to the sensor, shortening trace lengths and lowering latency. Parallel NVMe arrays now log UHD output without dropped frames, while FPGAs conduct on-the-fly compression. Cooling plates and vibration-damped chassis evolve to dissipate the extra thermal load, keeping dark current in check.

Edge storage affordability lets SMEs in ASEAN deploy high-speed imaging on factory lines previously limited to manual QC. Power modules follow suit; lithium-sulfur packs yield longer untethered runtime for down-hole probes. Meanwhile, lens manufacturers refine low-dispersion optics coated for SWIR transmission, complementing the surge in semiconductor inspection. Overall, component innovation sustains competitive differentiation inside the high-speed camera market.

By Resolution: Higher Megapixel Counts Accelerate

The 2–5 MP tier held 42% share, pairing adequate spatial detail with maintainable data rates, giving it the largest slice of current high-speed camera market share. However, sensors above 5 MP are rising at a 14.8% CAGR as pixel architectures gain quantum efficiency and read-out speeds. Cameras exceeding 12 MP now film semiconductor wafers, enabling AI defect classifiers to spot sub-micron anomalies without halting the line.

Emergent global-shutter CMOS tech supports 65 MP at 71 FPS, routed over CoaXPress-12 links. Sports analytics similarly benefits: 8K slow-motion clips reveal biomechanical subtleties once invisible. As host PCs adopt PCIe 5.0, the ceiling on megapixels will climb, reinforcing upward migration within the high-speed camera market.[3]“New High Speed, High Resolution Industrial Camera Launched,” Vision Systems Design, vision-systems.com

By Frame Rate: Ultra-High Speeds Define Premium Segment

Mid-tier cameras operating between 1,001 FPS and 5,000 FPS secured 38% share in 2024, anchoring the mainstream high-speed camera market size for industrial inspection. Yet ultra-high-speed units above 100,000 FPS are forecast to surge 15.2% through 2030, propelled by hypersonic weapons research and explosives testing. One laboratory prototype even reached 156 trillion FPS using SCARF imaging, illustrating the theoretical horizon.

Below 1,000 FPS, value models keep costs down for academic labs. Between 5,001 FPS and 20,000 FPS, automotive crash sleds find a sweet spot, balancing resolution, frame depth, and cost. Hardware advances such as sensor-side ADCs and fiber-based CoaXPress drives will compress price premiums, gradually widening access to the premium tier.

By Spectrum Type: Infrared Applications Expand

Visible-light systems generated 62% revenue in 2024, but infrared modalities—principally SWIR—are pacing at a 12.9% CAGR. Wafer inspection dominates SWIR demand thanks to silicon-penetrating wavelengths. In NIR and MWIR, thermal events like battery-cell venting or composite cure cycles require rapid capture. Uncooled bolometer arrays push entry prices downward, nurturing broader adoption.

UV and X-ray variants remain niche yet strategic in nondestructive testing of aerospace composites. Advancements in HgCdTe detector uniformity and back-thinned CMOS yield incremental gains, reinforcing spectral diversification inside the high-speed camera market.

By Usage Type: Rental Model Gains Momentum

Traditional ownership still accounts for 85% of shipments, but rentals are expanding at 18% CAGR, underscoring a behavioral shift across the high-speed camera industry. Professional rental houses maintain inventories of multi-million-FPS rigs, bundling calibration, lenses, and redundant storage so broadcasters and R&D labs sidestep capital lock-in.

Used-equipment channels also flourish as innovation cycles shorten. Depreciated flagship models migrate to universities, creating secondary demand. Together, rental and refurbished pathways democratize access, deepening the addressable base for the high-speed camera market.

By Application: Sports Analytics Drives Growth

Industrial manufacturing led with 29% revenue, from pick-and-place verification to fluid-filling studies. Sports analytics, advancing at 14.5% CAGR, capitalizes on 8K arenas and athlete performance metrics. Camera arrays capture pitch-level kinematics and ball-spin, feeding coaching analytics.

Automotive crash testing remains pivotal, bolstered by AI analytics seeking sub-millisecond object deformation. Aerospace and defense employ high-speed footage in wind tunnels and ballistic labs, where frame integrity cannot falter under G-loads. Healthcare, though nascent, investigates vascular flow and tissue elasticity at kilohertz rates, hinting at new diagnostic frontiers.

Geography Analysis

North America retained 33% of 2024 revenue, driven by hypersonic R&D, 8K sports broadcast pipelines, and an entrenched rental ecosystem. U.S. defense laboratories run cameras beyond 100,000 FPS to study plasma-induced shock, while Canadian aerospace facilities evaluate icing impacts on composite wings. Mexico’s automotive corridor brings steady crash-test demand. Regional suppliers hedge tariff risk by dual-sourcing CoaXPress boards, keeping supply chains resilient.

Asia-Pacific presents the steepest trajectory at a 13% CAGR. South Korean and Taiwanese fabs, locked in sub-5 nm competition, deploy SWIR high-speed arrays across lithography tracks. China channels defense budgets into ultra-fast optics, shrinking reliance on imported sensors. Japan fuses robotics and imaging for assembly lines requiring millisecond-level feedback, while India’s PLI schemes incentivize domestic electronics inspection capacity.

Europe grows steadily despite data-network inertia. German OEMs lead AI-enhanced crash loci, combining machine vision with digital twins. The United Kingdom advances aerospace turbofan research, and France integrates high-speed imaging into rail pantograph monitoring. In the Middle East, rugged, battery-powered cameras descend oil wells at 150 °C to diagnose obstructions, proving high-speed viability in harsh zones. Africa and South America remain embryonic but show upticks in mining blast analysis and university research programs, foreshadowing broader penetration of the high-speed camera market.

Competitive Landscape

The competitive arena is moderately fragmented. Vision Research, Photron, and Olympus anchor the premium tier with proprietary sCMOS sensors, deep-TEC cooling, and firmware tuned for deterministic latency. Their patents around read-out architectures create high barriers to entry. Emerging players chase biomimetic optics; a KAIST prototype mimics insect compound eyes at 9,120 FPS in a sub-1 mm stack, hinting at ultralight portable units.

Competition pivots on vertical integration: leaders pair captive sensors with in-house software, delivering turnkey analytics. Niche newcomers focus on specific gaps—portable SWIR rigs for field agronomy or frame-synchronized LED strobes for additive-manufacturing monitoring. Rental-service aggregators form a parallel front, bundling equipment, technicians, and per-event contracts, thereby influencing OEM roadmaps toward modular, field-swappable components.

Intellectual-property filings proliferate around thermal management—microchannel liquid loops and phase-change substrates. Meanwhile, connectivity innovation tilts toward fiber-based CoaXPress-12 and emerging 100 Gbps Ethernet variants to alleviate data choke points. As suppliers jockey for mindshare, thought-leadership content and open-source SDKs become soft-power levers within the high-speed camera market.

High Speed Cameras Industry Leaders

Photron Ltd.

Olympus Corporation

nac Image Technology Inc.

Mikrotron GmbH

PCO AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: KAIST researchers unveiled an insect-eye-inspired high-speed camera capable of capturing 9,120 frames per second with enhanced low-light sensitivity, representing a breakthrough in bio-inspired imaging technology that could revolutionize portable high-speed applications. The compact design, less than 1 mm thick, addresses thermal management challenges that have limited portability in ultra-high-speed cameras.

- June 2024: Nikon Corporation launched the AX R with NSPARC 2K Super-Resolution Confocal Microscope, offering sixfold faster imaging compared to traditional methods and expanding high-speed imaging capabilities in biotechnology research applications. This system enables detailed analysis of biological processes with significantly improved research efficiency in cancer and neurobiology studies.

- June 2024: Basler AG introduced the boA5328-100cm camera featuring 24 MP resolution at up to 100.07 fps using CoaXPress 2x CXP interface, demonstrating continued advancement in high-resolution, high-speed imaging capabilities for industrial applications. The camera incorporates Sony's IMX530 sensor with global shutter technology for demanding industrial inspection applications.

- March 2024: Canadian researchers at INRS developed the SCARF (swept-coded aperture real-time femtophotography) camera system capable of capturing 156.3 trillion frames per second, pushing the boundaries of ultrafast imaging for materials science and semiconductor applications.

Global High Speed Cameras Market Report Scope

A high-speed camera is an imaging device to capture pictures of fast and transient phenomena. It can analyze invisible objects beyond the human eye's capacity. High-speed photography is majorly used in biomechanical research, ballistics, medical research, and other fields such as healthcare, entertainment, aerospace, automotive, and military.

The High-Speed Cameras market is segmented by Component (Image Sensors, Lens, Battery, and Memory Systems), Frame Rate (1,000 to 5,000, 5,001 to 20,000, 20,001 to 100,000, and Greater Than 100,000), Application (Entertainment & Media, Sports, Consumer Electronics, Research & Design, Industrial Manufacturing, Military & Defense, and Aerospace), and Geography (North America, Europe, Asia-Pacific, and the Rest of the World). The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

| Image Sensors |

| Processors and Controllers |

| Lens |

| Memory Systems (On-board and External) |

| Body and Chassis |

| Cooling Systems |

| Battery and Power Modules |

| Others (Cables, Accessories, Software) |

| Less than 2 MP |

| 2 - 5 MP |

| 5 MP - 12 MP |

| Greater than 12 MP |

| 250 - 1,000 FPS |

| 1,001 - 5,000 FPS |

| 5,001 - 20,000 FPS |

| 20,001 - 100,000 FPS |

| Greater than 100,000 FPS |

| Visible (RGB) |

| Infrared (NIR and MWIR) |

| Short-Wave Infrared (SWIR) |

| X-ray |

| Ultraviolet (UV) |

| New Cameras |

| Rental Cameras |

| Used / Refurbished Cameras |

| Automotive and Transportation Crash Testing |

| Aerospace and Defense (Wind-Tunnel, Ballistics) |

| Industrial Manufacturing - Electronics and Semiconductor |

| Industrial Manufacturing - General Machinery |

| Research and Design - Universities and Labs |

| Media and Entertainment Production |

| Sports Analytics and Broadcast |

| Healthcare and Medical Diagnostics |

| Consumer Electronics Testing |

| Others (Energy, Mining) |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Image Sensors | |

| Processors and Controllers | ||

| Lens | ||

| Memory Systems (On-board and External) | ||

| Body and Chassis | ||

| Cooling Systems | ||

| Battery and Power Modules | ||

| Others (Cables, Accessories, Software) | ||

| By Resolution | Less than 2 MP | |

| 2 - 5 MP | ||

| 5 MP - 12 MP | ||

| Greater than 12 MP | ||

| By Frame Rate | 250 - 1,000 FPS | |

| 1,001 - 5,000 FPS | ||

| 5,001 - 20,000 FPS | ||

| 20,001 - 100,000 FPS | ||

| Greater than 100,000 FPS | ||

| By Spectrum Type | Visible (RGB) | |

| Infrared (NIR and MWIR) | ||

| Short-Wave Infrared (SWIR) | ||

| X-ray | ||

| Ultraviolet (UV) | ||

| By Usage Type | New Cameras | |

| Rental Cameras | ||

| Used / Refurbished Cameras | ||

| By Application | Automotive and Transportation Crash Testing | |

| Aerospace and Defense (Wind-Tunnel, Ballistics) | ||

| Industrial Manufacturing - Electronics and Semiconductor | ||

| Industrial Manufacturing - General Machinery | ||

| Research and Design - Universities and Labs | ||

| Media and Entertainment Production | ||

| Sports Analytics and Broadcast | ||

| Healthcare and Medical Diagnostics | ||

| Consumer Electronics Testing | ||

| Others (Energy, Mining) | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the high-speed camera market?

The market is valued at USD 0.85 billion in 2025.

How fast is the high-speed camera market expected to grow?

It is projected to expand at an 11.58% CAGR to reach USD 1.47 billion by 2030.

Which region is expanding the quickest?

Asia-Pacific is forecast at a 13% CAGR through 2030, fueled by semiconductor and defense investments.

What segment shows the highest growth by frame rate?

Cameras exceeding 100,000 FPS are expected to log a 15.2% CAGR due to hypersonic and explosives testing demand.

Why is the rental model gaining traction?

High acquisition costs and rapid technology turnover make renting cost-effective for broadcasters and short-term industrial projects.

What technological barrier most limits portable ultra-high-speed cameras?

Thermal noise above 50,000 FPS necessitates bulky cooling systems, constraining portability.

Page last updated on: