Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

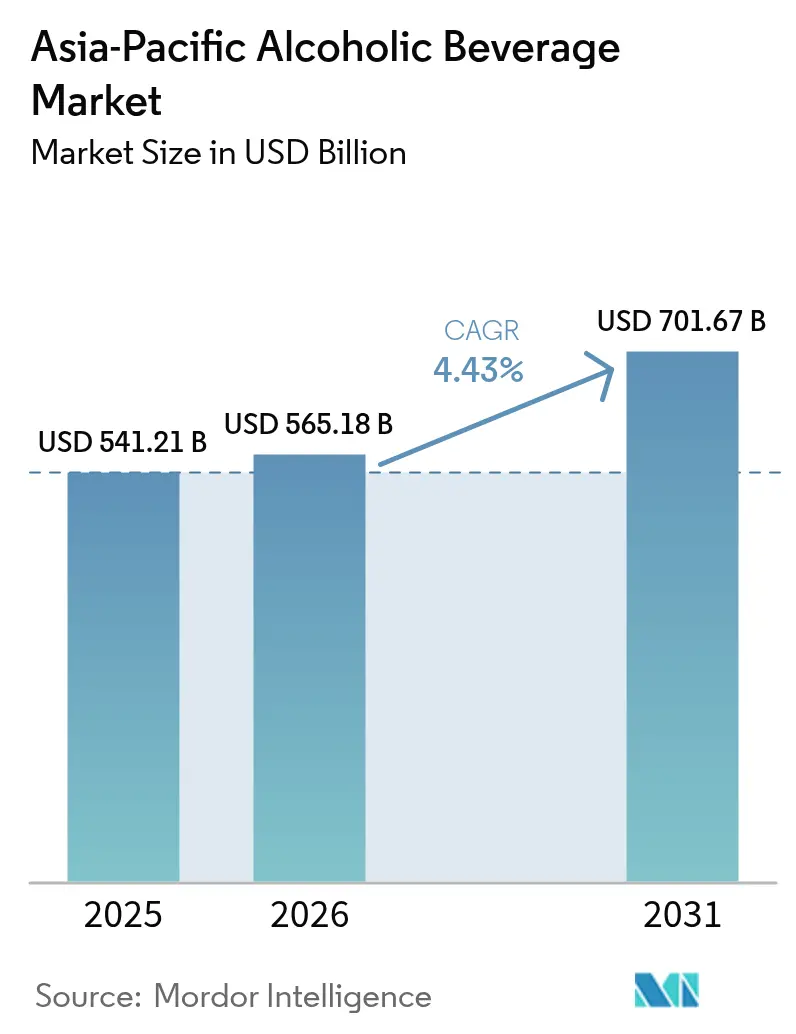

| Base Year Market Size (2025) | USD 541.21 Billion |

| Market Size (2026) | USD 565.18 Billion |

| Market Size (2031) | USD 701.67 Billion |

| Growth Rate (2026 - 2031) | 4.43% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Alcoholic Beverage Market Analysis by Mordor Intelligence

The Asia-Pacific alcoholic beverages market size was valued at USD 541.21 billion in 2025 and estimated to grow from USD 565.18 billion in 2026 to reach USD 701.67 billion by 2031, at a CAGR of 4.43% during the forecast period (2026-2031). Urbanization and rising incomes are significantly expanding the pool of legal-age drinkers, creating a larger consumer base for alcoholic beverages. At the same time, digital retail is effectively breaking down long-standing access barriers, making products more accessible to consumers. Despite facing fiscal and regulatory challenges, consumer demand remains robust, showcasing the resilience of the market. A growing premium gap is enabling brewers, vintners, and distillers to introduce higher-margin products, which cater to evolving consumer preferences for premium and diverse offerings. Meanwhile, omnichannel strategies are seamlessly connecting modern trade, last-mile delivery, and experiential venues, ensuring a broader and more integrated market reach. The market is also experiencing a surge in venture, merger, and acquisition activities, which are channeling significant capital into craft startups and regional leaders. This influx of investment not only diversifies the product mix but also accelerates portfolio refresh cycles, keeping the market dynamic and competitive.

Key Report Takeaways

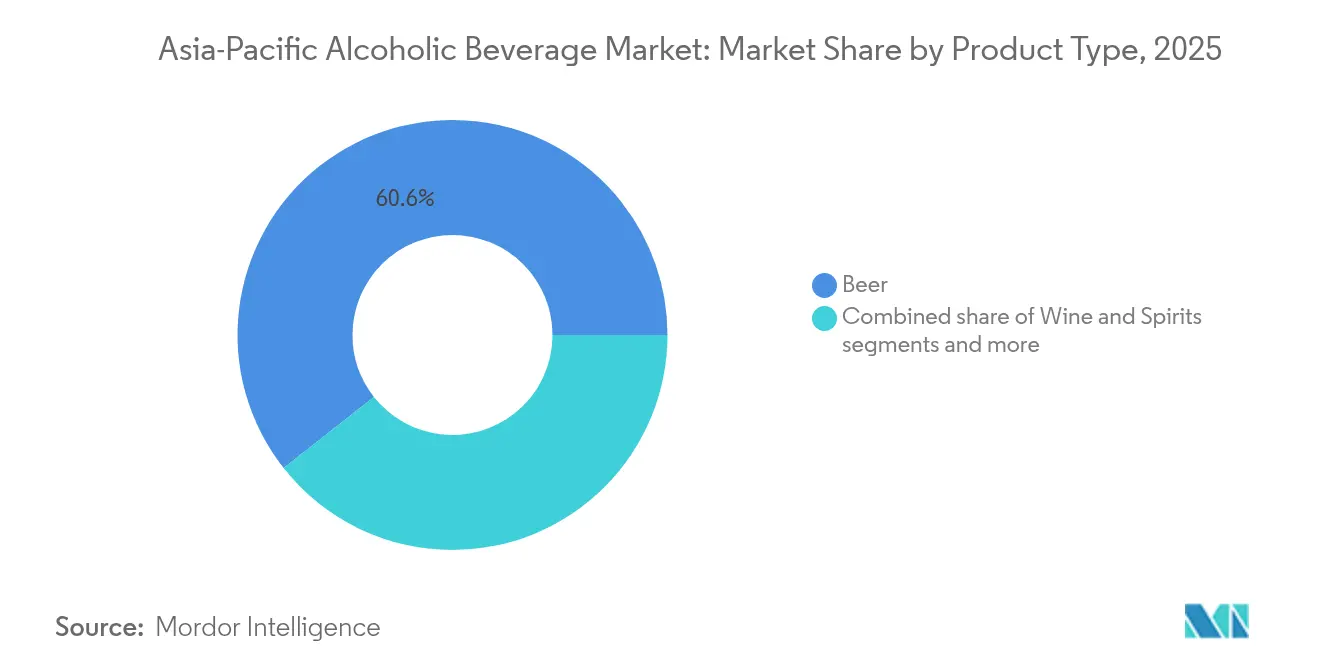

- By product type, beer led with 60.62% of the Asia-Pacific alcoholic beverages market share in 2025, while wine is projected to grow at a 5.63% CAGR through 2031.

- By packaging, bottles accounted for 72.64% of the Asia-Pacific alcoholic beverages market size in 2025, and cans are expected to expand at a 5.12% CAGR to 2031.

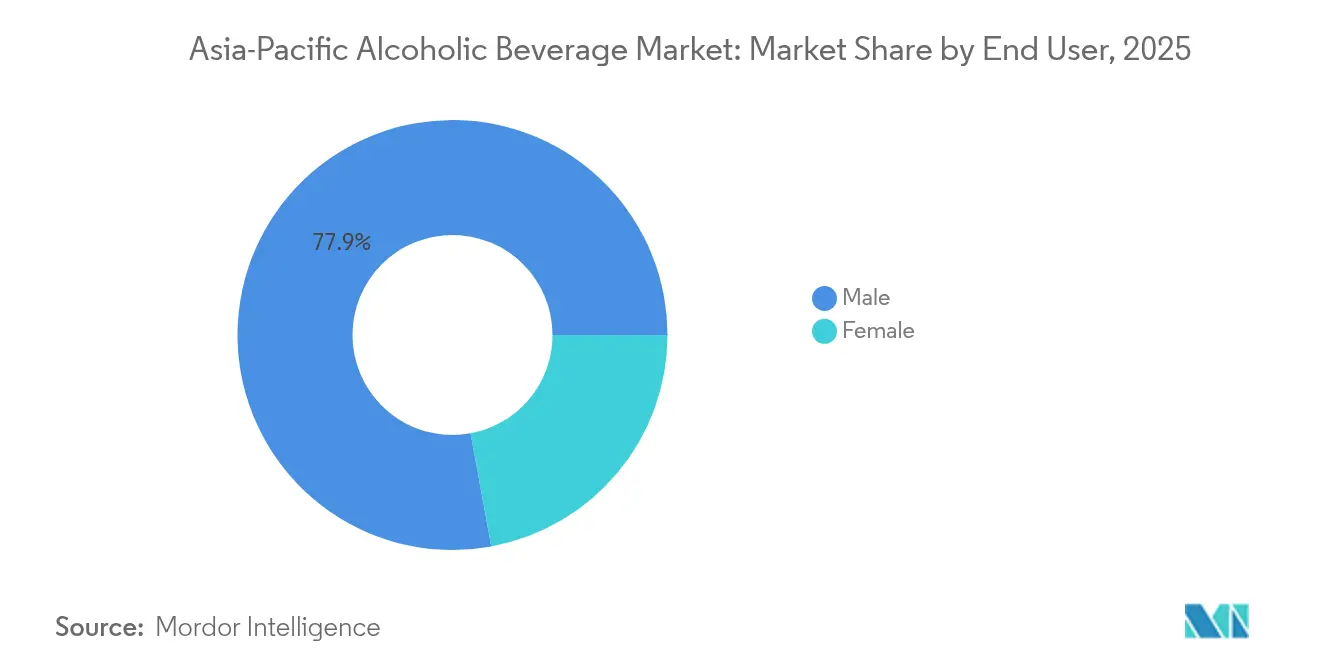

- By end user, male consumers held 77.89% share of the Asia-Pacific alcoholic beverages market size in 2025; female consumption is set to climb at a 5.49% CAGR over 2026-2031.

- By distribution channel, off-trade captured 68.21% revenue share in 2025, whereas on-trade bookings anticipate a 5.58% CAGR through 2031.

- By geography, China represented 27.55% of the Asia-Pacific alcoholic beverages market share in 2025, while India registered the strongest growth momentum at a 5.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Alcoholic Beverage Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising disposable incomes and urbanization | +1.1% | China, India, Southeast Asia | Long term (≥ 4 years) |

| Expansion of modern retail and e-commerce | +0.8% | Japan, Australia, regional urban hubs | Medium term (2-4 years) |

| Premiumization across beer, wine and spirits | +0.7% | Japan, South Korea, Australia, tier-1 Chinese cities | Medium term (2-4 years) |

| State-level alcohol-delivery liberalization | +0.6% | Thailand, Singapore, selected Indian states | Short term (≤ 2 years) |

| Low/No-alcohol and functional innovation | +0.5% | Japan, Australia, wellness-oriented metros | Long term (≥ 4 years) |

| Sustainable and circular packaging adoption | +0.4% | Australia, Japan, premium export segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising disposable incomes and urbanization

As urban areas expand and household incomes rise, per-capita alcohol spending sees a notable uptick. This trend is particularly pronounced in second-tier cities of China and India, where modern retail is making swift inroads. For instance, in Vietnam, the urban populace rebounded beer consumption to 43 liters per capita in 2024, shaking off the pandemic's grip. Younger professionals, with their increasing earnings, are channeling more of their discretionary income into social drinking. They're often leaning towards imports or craft labels, viewing them as status symbols. Retail hubs are sprouting around new transit lines, amplifying buying opportunities. Meanwhile, denser apartment living is making at-home socializing the norm. This shift is broadening the appeal of ready-to-drink (RTD) beverages and bolstering e-commerce delivery models. With rising purchasing power, there's a noticeable tilt towards exploring premium non-domestic categories. This trend is enriching the SKU diversity found in both supermarkets and specialty shops.

Expansion of modern retail and e-commerce

In 2024, Japan's beverage e-commerce achieved significant growth and success, highlighting a pronounced shift from traditional shopping to online carts. Collaborations like Carlsberg's tie-up with Grab are not just redefining sales channels but also equipping brewers with crucial last-mile data for targeted micro-campaigns. Meanwhile, Singapore's updated online licensing regulations showcase regulators' efforts to strike a balance between accessibility and social responsibility. Today's consumers are increasingly browsing online, even if they ultimately make their purchases in-store. This behavior compels brands to harmonize their content, promotions, and inventory across various platforms, from apps and dark stores to physical retail locations. Armed with detailed data, retailers are gaining insights into variant preferences and price sensitivities. This intelligence empowers suppliers to tailor their offerings with precision, down to specific city blocks rather than broader provinces.

Premiumization across beer, wine and spirits

Middle-class consumers are placing a premium on craftsmanship and origin stories, leading to a shift in focus from quantity to quality. In Japan, there's a robust demand for domestic whisky, with an increasing appreciation for local labels. Meanwhile, in Seoul, bar menus prominently showcase imported Scotch and Highland malts, highlighting a burgeoning enthusiasm for whisky, even in the face of hefty import costs. The craft spirits movement is gaining momentum, driven by stories of local ingredients and artisanal methods. This trend extends to beer, where small-batch ales are now viewed as premium, and to wine, with sparkling varieties becoming festive favorites. In light of this, major beverage corporations are rolling out upscale product lines and experimenting with barrel-aged editions. At the same time, boutique brands are making their mark with handcrafted selections rich in narrative.

State-level alcohol-delivery liberalization

In 2024, Thailand lifted its mid-day sales bans and relaxed advertising regulations, granting brewers and distillers a long-elusive promotional opportunity. Meanwhile, Hong Kong drastically reduced its spirits levy from 100%, creating a more equitable landscape for imported bourbons and cognacs. In Australia, the licensing process was streamlined, significantly reducing the paperwork duration for newcomers. These regulatory shifts not only acknowledge the sector's contributions to taxes and employment but also validate delivery models that emerged during the pandemic. Following the green light for web-only storefronts, early adopters in Singapore are witnessing impressive double-digit growth in direct-to-consumer sales. This wave of liberalization is spurring innovative market approaches, paving the way for subscription clubs, QR-coded vending, and influencer-driven flash drops.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High excise duties and complex taxation | -0.9% | Vietnam, Malaysia, high-tax jurisdictions | Short term (≤ 2 years) |

| Strict advertising/sales-hour curbs | -0.7% | India, Indonesia, certain Muslim markets | Medium term (2-4 years) |

| Glass-supply bottlenecks and cost spikes | -0.5% | Global manufacturing hubs | Short term (≤ 2 years) |

| Cross-border e-commerce compliance risk | -0.4% | Import-reliant microbrands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High excise duties and complex taxation

Government taxation policies and excise duties significantly impact the Asia-Pacific alcoholic beverages market by affecting pricing and influencing consumer behavior. By 2030, Vietnam's draft law could significantly increase beer taxes. This move echoes Malaysia's 2015 tax shock, which not only slashed revenue but also nudged consumers towards informal purchasing channels, such as unregulated markets and smuggled goods. In 2023, Vietnam's beer sector grappled with a profit decline, with industry giants Sabeco and Habeco witnessing notable double-digit drops, driven by rising operational costs and declining consumer spending[1]Source: Asia Brewers Network," Vietnam’s beer industry sees 23% profits drop in 2023", asiabrewersnetwork.com. The introduction of tiered tax schemes has led to an uptick in compliance filings, increasing administrative burdens for smaller players. This burden pushes smaller labels to lean on distributors with robust back-office capabilities, inadvertently consolidating market share among established players who are better equipped to handle these complexities. Furthermore, this fiscal unpredictability has stymied capital expenditure plans, leaving brewers wary of investing in new fermenters or expanding production capacity due to looming margin pressures and uncertain returns.

Strict advertising/sales-hour curbs

Vietnam's Decree 100, with its tougher fines for drink-driving, has significantly curtailed on-premise traffic, forcing businesses to adapt their route-to-market strategies by shifting focus towards off-trade channels such as retail stores and e-commerce platforms. In India, state-by-state advertising bans are creating significant barriers for national campaigns, making it challenging for new entrants to establish their presence and build brand recognition. Additionally, restricted sales windows are severely limiting impulse purchases, particularly in convenience channels where beer and ready-to-drink (RTD) beverages typically thrive due to their quick and easy accessibility. These regulatory and operational constraints are tilting the competitive landscape in favor of domestic giants, whose well-established labels already enjoy widespread recognition and loyalty among consumers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Beer Dominance Faces Wine Innovation

In 2025, beer solidifies its dominance in the Asia-Pacific's alcoholic beverage scene, commanding a substantial 60.62% of the market. Lager, a staple of the mass-market segment, enjoys widespread appeal across the region's diverse demographics. Meanwhile, craft ales are carving out a niche in the premium segment, buoyed by the burgeoning tap-room culture and heightened visibility through e-commerce. Not to be overlooked, non-alcoholic beer is gaining traction, with Japan proudly standing as the world's second-largest market, hinting at a shift towards varied consumption moments beyond just traditional drinking. In a bid to adapt to these evolving preferences, brewers are venturing into adjacent categories, experimenting with hard seltzers and hop-infused non-alcoholic teas. This strategic maneuvering showcases the beer category's blend of steadfast mainstream appeal and a nimble pivot towards premium and non-alcoholic offerings.

On the other hand, wine is rapidly ascending as the Asia-Pacific's fastest-growing segment, with projections pointing to a CAGR of 5.63% over the period 2026-2031. Sparkling wine, in particular, is leading this charge, riding the wave of celebratory dining trends in China and South Korea, where premium bubbly has become a festive staple. The sophistication of consumer palates is on the rise, thanks in part to the surge in cross-border e-commerce. Imports like boutique Rioja, Oregon Pinot, and Tasmanian gin are elevating the region's wine culture to a more cosmopolitan level. Wineries are quick to adapt, introducing innovative packaging like cans to cater to festival-goers and the younger crowd. This premium trend is evident in Nielsen’s scan data, highlighting that revenue growth in USD terms is nearly double that of volume growth, pointing to a surge in spending per unit. Given these trends, wine is not only solidifying its position as the standout growth driver in the regional alcoholic market but is also proving to be the most attuned to lifestyle shifts, globalization, and the premiumization wave.

By Packaging: Bottles Lead While Cans Accelerate

In 2025, glass packaging accounted for a significant 72.64% share of the Asia-Pacific alcoholic beverages market. Its sustained dominance is attributed to deep-rooted heritage associations and a pronounced shelf presence, particularly benefiting wine and brown spirits in maintaining their premium pricing. Traditional glass bottles are the preferred choice for gifting, formal events, and fine dining, underscoring their cultural and commercial significance. Despite the rise of alternatives, glass packaging remains synonymous with authenticity and trust qualities paramount for the region's increasingly premium beverage categories. Supply shortages have spurred refillable trial initiatives in nations like Thailand and Australia, where modernized deposit-return systems now feature QR-coded refund mechanisms. By marrying time-honored preferences with sustainability trials, glass packaging continues to play a pivotal yet adaptive role in the alcoholic beverage sector.

Meanwhile, cans are emerging as the region's fastest-growing packaging format, boasting a 5.12% CAGR, a testament to their resonance with evolving lifestyles. Their lightweight nature appeals to consumers prioritizing convenience, whether for outdoor activities or home deliveries. Additionally, urban recycling infrastructures favor aluminum's processing over glass. Breweries are increasingly adopting slim-can designs, trimming up to 15 grams of aluminum per unit, achieving both cost savings and reduced freight emissions, an embodiment of cost-efficiency and environmental mindfulness. Cans also facilitate category diversification, with offerings like nitro stouts and ready-to-drink highball cocktails gaining popularity in venues like beaches and festivals, where glass is often prohibited. Beyond cans, packaging innovation itself has become a hallmark of brand modernity, evident in Japanese distillers' foray into paper-bottle trials and the rising prominence of RTD pouches in online grocery orders. Thus, cans epitomize the evolving landscape of beverage consumption in the Asia-Pacific, where themes of sustainability, convenience, and occasion-driven drinking coalesce to drive growth.

By End User: Male Dominance Shifts Toward Female Growth

In 2025, male drinkers commanded a significant 77.89% of the total spending in the Asia-Pacific alcoholic beverages market, highlighting the industry's pronounced masculine tilt. This dominance, largely sustained by beer and brown spirits, aligns with traditional male-centric social venues like sports events, izakayas, and nightclubs. Men's spending forms the backbone of out-of-home consumption, driving revenue through volume-heavy purchases and loyalty to established formats. These male consumption patterns influence the strategies of major brewers and distillers, ensuring mainstream products like lager and whisky maintain a robust market share. While marketers diversify their strategies, elements like heritage branding and premiumization resonate deeply with male consumers. However, this heavy reliance on male drinkers poses saturation risks, prompting brands to seek broader appeal among emerging consumer demographics.

Meanwhile, female drinkers are swiftly carving out their space in the market, boasting a 5.49% CAGR, making them the region's fastest-growing segment. Key to this surge are lower-ABV formats and flavor-forward RTDs, with pastel-hued hard seltzers and cocktail kits gaining traction, especially through influencer-led mixology showcases on social media. This momentum is bolstered by shifting social dynamics: as women achieve greater financial independence and workplaces become more inclusive, after-work consumption among females rises. This gender convergence is evident in Japanese karaoke bars, where mixed groups now favor sparkling wine flights over the traditional beer pitchers. Marketers are tapping into lifestyle themes like wellness, fashion, and travel to resonate with female aspirations in the alcoholic beverage realm. Concurrently, product developers are fine-tuning sweetness and aroma profiles to appeal broadly while maintaining authenticity. In India, the hospitality sector is taking note, with a reported significant uptick in female patronage post-COVID, underscoring women's pivotal role in steering both premium and accessible beverage choices.

By Distribution Channel: Off-trade Dominance With On-trade Recovery

In 2025, off-trade channels, encompassing supermarkets, convenience stores, and e-commerce platforms, dominated the Asia-Pacific alcoholic beverages market, accounting for 68.21% of total revenue. Consumer behaviors, shaped by pandemic-era pantry stocking, have solidified at-home drinking habits, underscoring the importance of off-trade distribution for both mainstream and premium beverages. While supermarkets and convenience stores benefit from high-frequency shopping and routine replenishment, e-commerce platforms have broadened the reach of niche products and enabled cross-border imports. Retailers are adapting to changing consumer profiles, dedicating more space to craft beverage festivals and in-store tastings, akin to traditional on-trade experiences, thereby boosting foot traffic in a competitive market. Logistical innovations further enhance the appeal of off-trade channels, ensuring convenience and variety for consumers. Collectively, these elements reinforce the pivotal role of off-trade settings in the region’s alcoholic beverage landscape.

On-trade venues are rapidly emerging as the fastest-growing distribution segment, with projections indicating a 5.58% CAGR expansion through 2031, driven by a resurgence in experiential dining and nightlife. China's bar and restaurant sector has already eclipsed pre-pandemic seat occupancy rates, underscoring a strong consumer appetite for social drinking and attentive service. Hybrid models are redefining traditional norms; diners can now use QR-code menus to order six-packs for takeaway, and tap-rooms are evolving into both direct-to-consumer hubs and community gathering spots. Ultra-premium spirits, typically sidelined by conventional retail due to their price, find a thriving platform in curated cocktail programs at upscale lounges and boutique bars. However, Vietnam's on-trade sector lags behind the regional upswing, a delay attributed to stringent road-safety measures impacting the nation's social drinking habits. As these trends unfold, on-trade formats are increasingly influencing how consumers engage with and discover new products, with the industry harnessing hybrid models to elevate the beverage purchasing experience.

Geography Analysis

China commands a dominant 27.55% share, solidifying its pivotal role in the Asia-Pacific's alcoholic beverages landscape. Urban millennials gravitate towards premium local baijiu and craft lagers, driven by a growing preference for unique and high-quality offerings, while consumers in lower-tier cities are turning to budget-friendly ready to drinks, reflecting a demand for affordability and convenience. E-commerce now boasts a 53% penetration rate, significantly reshaping purchasing behaviors and expanding market access. Additionally, provincial deregulation has slashed license wait times, creating a more favorable environment for foreign entrants to establish a foothold. India, riding on its youthful demographic and an expanding middle class, emerges as the region's volume powerhouse, recording a 5.41% CAGR. A patchwork of liberalization, such as Kerala’s Sunday closures juxtaposed with Maharashtra’s doorstep delivery, paints a diverse and complex regulatory landscape. Savvy players are capitalizing on this by customizing pack sizes and ABVs to align with local preferences, ensuring their offerings resonate with varied consumer needs.

Japan, while mature, offers lucrative prospects as premiumization counters its aging demographic challenge. In 2024, the government rolled out a directive for pure-alcohol labeling, urging producers to highlight lower-ABV SKUs, which cater to health-conscious consumers and align with evolving consumption trends. Whisky tourism, encompassing distillery trails and tasting passes, not only bolsters rural economies by attracting domestic and international visitors but also amplifies export marketing efforts, positioning Japanese whisky as a global premium product. Meanwhile, Australia and New Zealand are setting benchmarks with their regulatory clarity and logistics tailored for exports, making them attractive markets for both domestic and international players. A case in point: Australian bitters, under the craft initiative of Innovation Beverage Group, seized a notable 45% share of the domestic market, showcasing the potential of niche categories even under the watchful eyes of industry giants. This success highlights how innovation and targeted strategies can drive growth in specialized segments.

Southeast Asia showcases a tapestry of policy variations, for instance, Thailand's liberalization opens marketing avenues, enabling brands to engage more effectively with consumers, while Malaysia enforces stricter norms for its Muslim-majority populace, limiting market opportunities. Vietnam is considering substantial excise tax increases, which could lead to higher retail beer prices by 2026, reshape consumer purchasing patterns, and impact market dynamics. Striking a balance, the Philippines enjoys a steady annual growth, even in the face of duty increases, highlighting the market's demand resilience and untapped potential. Tourist corridors like Singapore–Johor and Hong Kong–Greater Bay are not just conduits for tasting-room sales and duty-free transactions; they weave together subregional micro-markets, fostering interconnected growth. These corridors also serve as strategic hubs for brands to test new products and expand their reach, leveraging the high footfall and diverse consumer base.

Competitive Landscape

In the Asia-Pacific alcoholic beverages market, a blend of established multinationals and emerging craft players creates a landscape of moderate concentration. Asahi's acquisition of Carlton & United not only solidifies its foothold in Australia but also amplifies its influence over raw material sourcing. Looking ahead to 2025, ThaiBev's strategic move to acquire Asiaeuro International Beverage underscores its ambition to enhance distribution channels in Greater China, highlighting a growing trend of intra-regional consolidation. Meanwhile, Suntory is channeling its investments in the Asia-Pacific towards capacity expansion and product innovation, with a keen focus on upgrading whisky still-houses and diversifying its hard-seltzer offerings.

In today's market, digital fluency is a defining competitive edge. Carlsberg, for instance, harnesses APIs from platforms like Grab, foodpanda, and Meituan to roll out geo-targeted promotions, achieving delivery times of less than one hour in cities like Manila and Kuala Lumpur. The uptick in patent filings related to dealcoholization membranes and bio-yeast strains hints at a burgeoning research and development race, all vying for a stake in the burgeoning low and no-alcohol segment. Craft brands, leveraging direct-to-consumer (DTC) exemptions and compelling narratives, are making significant waves; for instance, Japanese gin labels infused with yuzu botanicals are turning heads in Seoul's premium supermarkets, despite accounting for less than 1% of the volume.

Strategic decisions are increasingly influenced by supply-chain resilience. With glass ovens operating under capacity stress, major players are pivoting towards multi-continent sourcing contracts and establishing in-house bottle production. To shield against margin fluctuations, tactics like aluminum hedging and vertical integration come into play, exemplified by Asia Brewery's stake in a Luzon-based can manufacturer. Furthermore, as Environmental, Social, and Governance credentials gain prominence, they are becoming pivotal in procurement bids for coveted global supermarket listings, prompting industry laggards to take proactive steps, including commitments to Scope 3 emission audits.

Asia-Pacific Alcoholic Beverage Industry Leaders

-

Anheuser-Busch InBev

-

Heineken Holding NV

-

China Resources Beer

-

Tsingtao Brewery

-

Kirin Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Carabao Pattaya Beach Beer, a brand based in Thailand, unveiled its latest light beer boasting a 3.9% ABV. Infused with a refreshing lime aroma derived from hops, this innovative beer features the industry's first fully openable can, designed to enhance convenience and appeal. The product specifically targets a younger demographic, aiming to cater to their evolving preferences for lighter and more accessible beer options.

- July 2025: Ochre Spirits introduced its latest offering, the Mango Citron Rum. This flavored rum, infused with tart raw green mango and citrus, represents the fourth product in Ochre Spirits' portfolio. The brand aims to attract modern rum enthusiasts by offering a unique flavor profile that blends traditional rum characteristics with contemporary, fruit-forward notes, appealing to a diverse and adventurous consumer base.

- June 2025: Diageo India's Godawan Triple Cask brand debuted a new single malt exclusively for travel retail. This premium spirit, matured in bourbon barrels, is further enhanced with finishes in virgin oak, cherry wood, and PX sherry, creating a complex and layered flavor profile. Positioned as a premium gifting option, the product is tailored for discerning travelers seeking high-quality, exclusive offerings.

- May 2025: Cashmir Vodka rolled out its inaugural small-batch luxury vodka, hailing from the pristine valleys of Kashmir. Crafted from organic winter wheat and glacial water, this vodka undergoes a meticulous 7x distillation process to ensure purity and smoothness. Bottled at 42.8% ABV, it is positioned as a premium product that highlights the unique terroir and craftsmanship of the region.

Asia-Pacific Alcoholic Beverage Market Report Scope

An alcoholic beverage is a drink or brew that contains alcohol as an active ingredient. The Asia-Pacific alcoholic beverage market is segmented by product type, distribution channel, and geography. Based on product type, the market is segmented into beer, wine, and spirits. Based on distribution channels, the market is segmented into on-trade and off-trade. The off-trade segment is further divided into supermarkets/hypermarkets, specialist stores, online stores, and other off-trade channels. Based on geography, the market is segmented into China, Japan, India, Australia, and the rest of the Asia-Pacific region. For each segment, the market sizing and forecasts have been done based on value (in USD million).

By Product Type

| Beer | Ale |

| Lager | |

| Non/Low Alcohol Beer | |

| Other Beer Types | |

| Wine | Still Wine |

| Sparkling Wine | |

| Fortified Wine | |

| Other Wine Types | |

| Spirits | Whiskey |

| Liqueur | |

| Rum | |

| Brandy and Cognac | |

| Tequila and Mezcel | |

| White Spirits | |

| Others |

By Packaging

| Bottles |

| Cans |

| Others |

By End User

| Male |

| Female |

Distribution Channel

| On trade | |

| Off trade | Specialty/Liquor Stores |

| Others Off trade Channels |

By Geography

| China |

| Japan |

| India |

| Australia |

| New Zealand |

| Indonesia |

| Thailand |

| Vietnam |

| Malaysia |

| Philippines |

| Rest of Asia-Pacific |

| By Product Type | Beer | Ale |

| Lager | ||

| Non/Low Alcohol Beer | ||

| Other Beer Types | ||

| Wine | Still Wine | |

| Sparkling Wine | ||

| Fortified Wine | ||

| Other Wine Types | ||

| Spirits | Whiskey | |

| Liqueur | ||

| Rum | ||

| Brandy and Cognac | ||

| Tequila and Mezcel | ||

| White Spirits | ||

| Others | ||

| By Packaging | Bottles | |

| Cans | ||

| Others | ||

| By End User | Male | |

| Female | ||

| Distribution Channel | On trade | |

| Off trade | Specialty/Liquor Stores | |

| Others Off trade Channels | ||

| By Geography | China | |

| Japan | ||

| India | ||

| Australia | ||

| New Zealand | ||

| Indonesia | ||

| Thailand | ||

| Vietnam | ||

| Malaysia | ||

| Philippines | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the 2026 value of the Asia-Pacific alcoholic beverages market?

The market is valued at USD 565.18 billion in 2026.

How fast is the Asia-Pacific alcoholic beverages market expected to grow?

It is projected to post a 4.43% CAGR from 2026-2031.

Which product segment is growing quickest?

Wine is the fastest, with a 5.63% CAGR expected through 2031.

Which country offers the fastest demand growth?

India leads with a projected 5.41% CAGR to 2031.

Page last updated on: