ASEAN Inland Waterway Transport Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

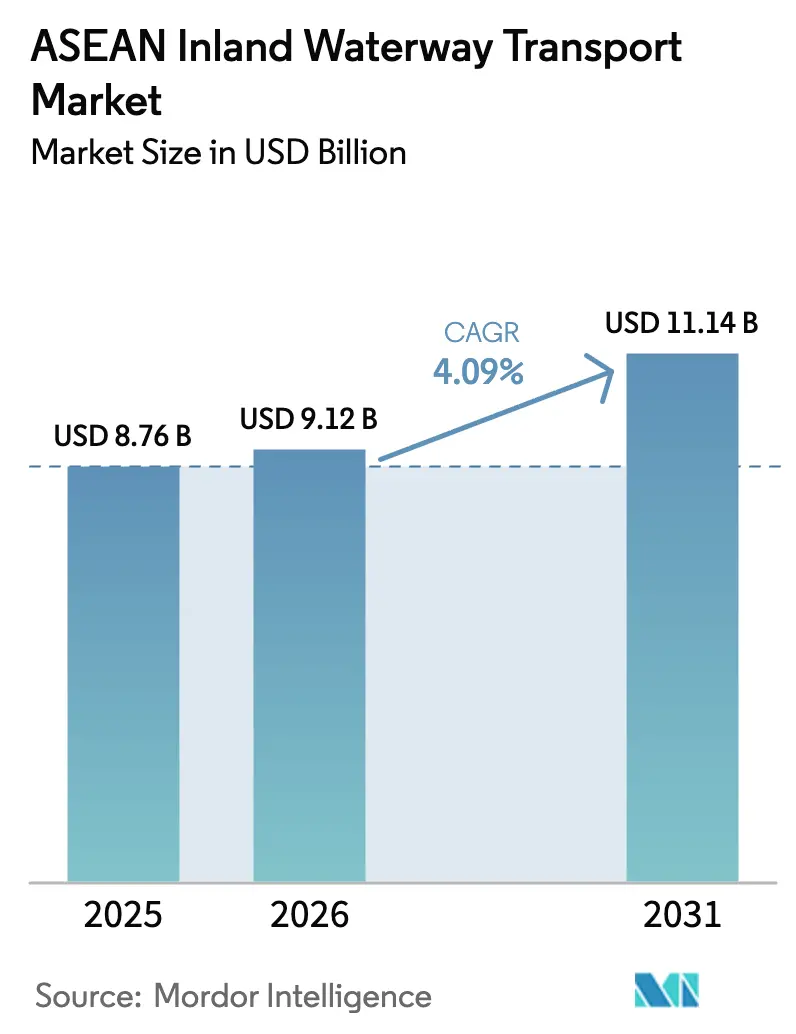

| Base Year Market Size (2025) | USD 8.76 Billion |

| Market Size (2026) | USD 9.12 Billion |

| Market Size (2031) | USD 11.14 Billion |

| Growth Rate (2026 - 2031) | 4.09% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Inland Waterway Transport Market Analysis by Mordor Intelligence

ASEAN Inland Waterway Transport Market size in 2026 is estimated at USD 9.12 billion, growing from 2025 value of USD 8.76 billion with 2031 projections showing USD 11.14 billion, growing at 4.09% CAGR over 2026-2031.

Governments are accelerating capital outlays for new canals, port expansions, and dredging programs at the same time that shippers are demanding digital visibility and lower-carbon operations, changing the basis of competition from pure cost to service integration. Large public works in Cambodia, Vietnam, and Thailand are expanding navigable lengths, yet draft volatility during dry seasons and the rapid build-out of competing rail lines are tightening margins for operators that still rely on older diesel barge fleets. Rising e-commerce cargo, growing agricultural exports, and pilot green-fuel corridors provide demand tailwinds, but fragmented customs procedures continue to impose two- to three-day delays on cross-border legs, diluting the historic cost advantage of river freight[1]ASEAN Secretariat, “ASEAN Transport Strategic Plan,” asean.org. Competitive intensity is shifting toward privately led logistics integrators that bundle barge, road, and warehouse assets to win contracts requiring same-day or next-day delivery windows.

Key Report Takeaways

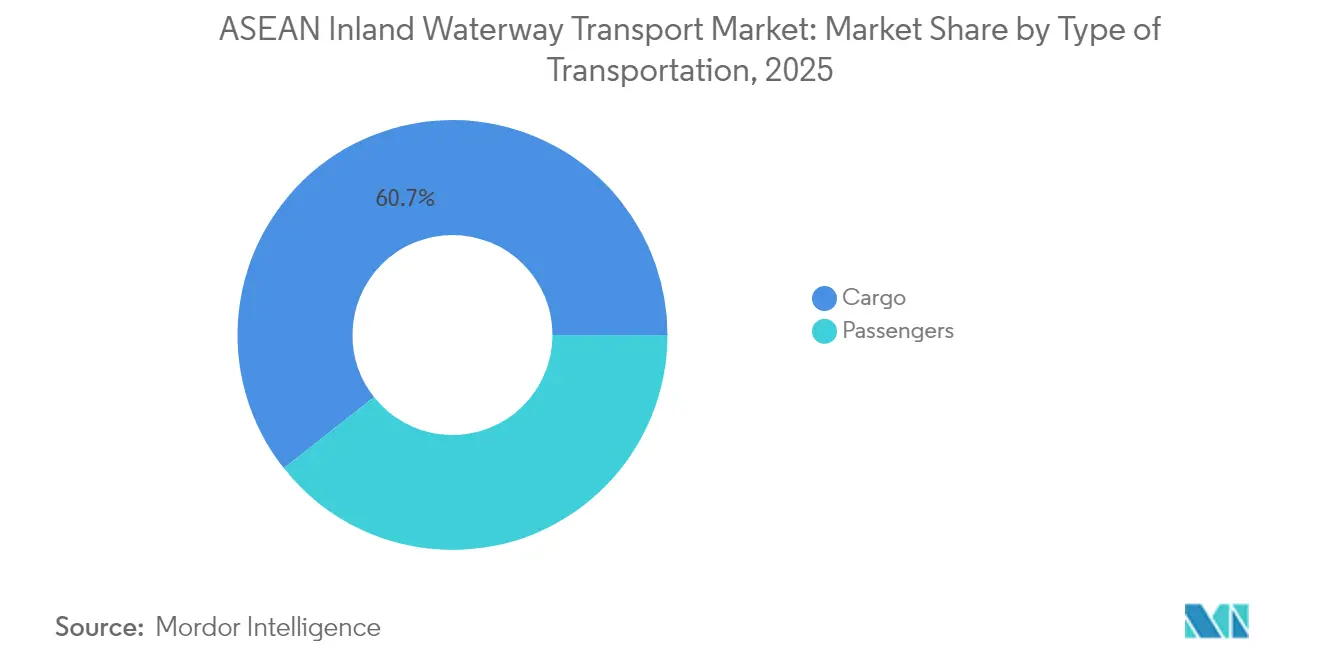

- Cargo movements captured 60.65% of ASEAN inland water transport market share in 2025, while passenger services are projected to advance at a 4.15% CAGR through 2031.

- Vietnam accounted for 22.51% of 2025 revenue and Indonesia is forecast to post the fastest country-level growth at a 4.26% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Inland Waterway Transport Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-led investments in waterway infrastructure | +0.9% | Vietnam, Cambodia, Thailand, Laos, Myanmar | Medium term (2-4 years) |

| Multimodal logistics cost advantage | +0.7% | Indonesia, Vietnam, Thailand | Long term (≥ 4 years) |

| Surging ASEAN e-commerce freight volumes | +0.8% | Indonesia, Vietnam, Philippines, Thailand | Short term (≤ 2 years) |

| Agricultural bulk export growth via Mekong and Ayeyarwady | +0.5% | Vietnam, Myanmar, Thailand | Medium term (2-4 years) |

| Emergence of LNG bunkering and green corridors | +0.4% | Singapore, Malaysia, Indonesia | Long term (≥ 4 years) |

| Digital vessel-traffic-management roll-outs | +0.3% | Singapore, Malaysia, Indonesia, Vietnam | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government-Led Investments in Waterway Infrastructure

State spending is lengthening river corridors and deepening drafts across Southeast Asia. Vietnam’s Southern Waterway Corridors program is dredging 12 priority routes to three-meter depth, enabling 1,000-ton barges to operate year-round and reducing seasonal idle capacity. Cambodia and Laos have aligned inland ports with Belt and Road Initiative finance, while Thailand’s land-bridge scheme pairs a new Ranong–Chumphon freight corridor with river-feeder upgrades that link hinterland provinces to both seaboards. China’s CNY 72.7 billion Pinglu Canal, slated for 2026 completion, will connect the Xijiang River to the Beibu Gulf, allowing 5,000-ton vessels to reach ASEAN markets directly and lowering freight costs for Chinese exporters by as much as 25%[2]Xinhua News Agency, “Pinglu Canal Construction Update,” news.cn. These overlapping projects will open more than 500 kilometers of additional navigable capacity by 2028, forcing operators to diversify fleet deployment across multiple corridors to hedge against traffic shifts. Because coordination remains voluntary inside the Mekong River Commission, benefits accrue mainly to countries able to self-finance upgrades or secure bilateral funding.

Multimodal Logistics Cost Advantage

River freight still enjoys a 30–40% per-ton cost lead over trucking for bulk shipments exceeding 500 kilometers, yet transit-time penalties cap the addressable cargo mix. An Asian Development Bank study shows that a 1% improvement in customs digitalization and port dwell-time cuts can boost bilateral trade by 1.5%, underscoring the value of process efficiency over additional concrete[3]Asian Development Bank, “Trade Facilitation in ASEAN’s Digital Era,” adb.org. Integrators such as Gemadept knit barge, rail, and depot assets into closed-loop services that capture e-commerce freight tolerant of only minimal schedule slippage. Indonesia’s archipelagic sprawl magnifies the opportunity: ASDP’s government-backed ferry grid forms the backbone for inter-island commerce, yet private firms are adding Kalimantan river feeders that shave one to two days off coastal loops, freeing export capacity for palm oil and coal. The China–Laos Railway’s 10-hour Kunming–Vientiane run has already siphoned electronic and perishable cargo from the Mekong, proving that time-critical loads will pay a premium to bypass slow river legs. Operators unable to combine barge legs with reliable last-mile transport risk confinement to low-margin commodity hauling.

Surging ASEAN E-Commerce Freight Volumes

Gross merchandise value rose from USD 139 billion in 2023 to USD 186 billion in 2025, placing sustained strain on last-mile networks. Platforms now book palletized river moves into Vietnam’s Mekong Delta to bypass road congestion that adds up to six hours for truck deliveries, while passenger ferries in Indonesia double as parcel carriers under a public-service-obligation model. The Philippines’ 2GO Group is testing refrigerated containers on river ferries to displace costly domestic air freight for seafood and pharmaceuticals. Customs bottlenecks remain the weakest link: the ASEAN Customs Transit System is live but not fully enforced, leaving parcel flows subject to two- to three-day border holds that erode the speed advantage e-commerce shippers crave.

Agricultural Bulk Export Growth via Mekong and Ayeyarwady

The Mekong and Ayeyarwady rivers handle up to 30 million tons of rice, maize, and fruit each year, but severe 2024 droughts pushed salt intrusion 90 kilometers inland and stopped barge traffic during the critical spring harvest. Exporters paid up to 50% more for road haulage, shrinking margins and temporarily rerouting Thai cassava through coastal ports. Myanmar’s Ayeyarwady remains vulnerable to political instability, forcing carriers to negotiate ad-hoc passage fees that raise freight costs by as much as 20%. To reduce exposure, Thailand is piloting satellite-based water-level forecasts that allow barges to reposition ahead of low-draft periods, an approach under review for replication in Vietnam. Sustained investment in predictive hydrology tools could lessen seasonal capacity shocks and stabilize export flows.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shallow-draft constraints in dry season | -0.6% | Vietnam, Thailand, Myanmar | Short term (≤ 2 years) |

| Modal competition from new road and rail corridors | -0.5% | Laos, Thailand, Vietnam, Cambodia | Medium term (2-4 years) |

| Fragmented cross-border regulations | -0.3% | All ASEAN member states | Long term (≥ 4 years) |

| Climate-driven extreme weather variability | -0.4% | Vietnam, Thailand, Myanmar, Philippines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shallow-Draft Constraints in Dry Season

Seasonal water-level drops sideline up to 30% of the regional barge fleet for several months each year. The 2024 Mekong drought recorded the lowest flows in a century and halted navigation on vital Phnom Penh–Ho Chi Minh City stretches for almost eight weeks. Thailand’s Chao Phraya depths fell under two meters, forcing vessels to half-load and doubling per-ton costs. Myanmar’s navigable Ayeyarwady length shrinks by one-third at peak dry season, isolating up-country commodities. Vietnam’s dredging program will secure three-meter drafts on 12 routes, yet high siltation rates demand continual maintenance. Operators are testing modular hulls that ride higher in low water, but unit costs run 20–25% above conventional designs, limiting adoption to larger fleets.

Modal Competition from New Road and Rail Corridors

Fast rail and upgraded highways are absorbing time-sensitive freight. The Kunming–Vientiane line moves goods in under ten hours, a journey that once took multiple days by river, while Thailand’s Eastern Economic Corridor high-speed link will cut Bangkok–Rayong transit to 90 minutes. Vietnam’s North–South Expressway, due for full commissioning in 2025, will enable Hanoi–Ho Chi Minh City truck runs in 18 hours. An ADB survey finds shippers willing to pay up to 20% premiums for services that trim transit time by two days, a benchmark that modern land routes already meet. To stay relevant, barge operators must embed road and rail legs into unified contracts or cede value-added cargo to intermodal specialists.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Transportation: Cargo Dominance Masks Passenger Revival

Cargo carried 60.65% of ASEAN inland water transport market share in 2025, driven by bulk shipments of rice, coal, petroleum products, and construction materials that move in 500- to 2,000-ton lots. Liquid bulk enjoys dedicated tanker-barge fleets that circumvent road weight limits and deliver 25–30% savings on hauls over 300 kilometers. Dry bulk remains the largest sub-segment, underpinned by Vietnam’s 25 million ton rice export pipeline and Thailand’s cassava trade. Containerized river volumes are expanding in tandem with e-commerce fulfillment centers that locate near inland depots, enabling palletized moves that bypass congested urban highways.

Passenger services, though smaller at 39.35% in 2025, are set to outpace cargo with a 4.15% CAGR to 2031 as archipelagic nations extend subsidized ferry grids. ASDP’s 226-route network moves up to 30 million travelers yearly and now carries parcels under a dual-use model that raises vessel utilization. The Philippines’ 2GO Group is refitting ferries with shore-power and Wi-Fi to win middle-income passengers migrating from short-haul flights as fuel costs climb. Malaysia’s Sarawak expresses on the 563-kilometer Rajang River remain critical for populations lacking road links and also transport e-commerce parcels and medical supplies. Regulatory harmonization under the ASEAN Single Shipping Market remains incomplete, leaving carriers to manage country-specific licensing that extends route launches by months.

Geography Analysis

Vietnam captured 22.51% of 2025 revenue as the Mekong Delta’s 41,000-kilometer grid funneled half of the nation’s rice and fruit exports toward Ho Chi Minh City terminals. The Southern Waterway Corridors dredging will secure three-meter depths and permit 1,000-ton barges year-round, reducing seasonal idle time and protecting Vietnam’s leading position. Severe 2024 droughts exposed vulnerability, however, when stretches closed for weeks and exporters turned to trucks at much higher cost.

Indonesia is forecast to deliver the fastest 4.26% CAGR through 2031 on the strength of ASDP’s subsidized ferry services linking 17,000 islands. The government pairs fare support with rural-connectivity grants that underwrite unprofitable legs, keeping the marine highway accessible for cargo and passengers alike. PT Pelindo is expanding hinterland links in Kalimantan and Sumatra, trimming one- to two-day transit times for palm oil and coal exports.

Thailand holds roughly one-fifth of market value, anchored by Chao Phraya operations and a USD 28 billion land-bridge that will link Ranong and Chumphon ports. The project is paired with river-feeder upgrades that give barges faster access to both seaboards, potentially increasing cargo flows through Bangkok’s industrial belt. Malaysia’s share clusters in Sarawak and Sabah, where rivers remain the backbone for timber and palm-oil logistics, while Singapore functions as the regional transshipment node through its Tuas Mega Port and LNG bunkering hub. The Philippines struggles with inland penetration beyond Pasig and Cagayan rivers but is dredging secondary routes and adding roll-on/roll-off terminals as funding allows. The rest of ASEAN—Laos, Cambodia, Myanmar, and Brunei—accounts for under 10% of value but could rise once Cambodia’s new sea-access canals and Laos’ feeder links come online.

Competitive Landscape

The ASEAN inland water transport market features moderate fragmentation. State-owned leaders such as Vietnam National Shipping Lines, ASDP Indonesia Ferry, and Indonesia Port Corporation leverage exclusive route licenses and public subsidies to secure bulk and passenger contracts. Private integrators, including Gemadept, Rhenus Logistics, and SCG Logistics, differentiate through multimodal bundling and digital platforms that provide real-time tracking and single-invoice billing. Singapore’s AIS mandate exposed an unregistered barge segment estimated at 20% of capacity, tightening compliance and shifting cargo toward transparent operators.

White-space opportunities concentrate in green-fuel retrofits and bonded-corridor services. Singapore is set to approve floating LNG bunkering by early 2026, creating a pathway for compliant river-to-sea feeders. Operators financing dual-fuel conversions at USD 1.5–2.0 million per vessel can earn premiums from shippers committed to scope-3 emission cuts. The ASEAN Customs Transit System, once fully implemented, will reward integrators that establish bonded depots and automate documentation, slashing border delays from days to hours. Smaller owners face consolidation pressure unless they enter equipment-sharing pools or technology partnerships.

ASEAN Inland Waterway Transport Industry Leaders

Vietnam National Shipping Lines (VIMC)

Gemadept Corporation

Vinafco Logistics

Siam Shipping

Vinafreight

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Gemadept Corporation committed USD 150 million to add two 8,000-TEU berths at Gemalink terminal and build a direct rail spur to Mekong depots, targeting seamless barge-to-rail transfers.

- September 2024: ASDP Indonesia Ferry ordered six dual-fuel LNG ferries worth USD 85 million for Java–Sumatra high-traffic routes, positioning its fleet for future IMO emission mandates.

- July 2024: Rhenus Logistics opened a USD 35 million multimodal hub in Vietnam’s Binh Duong province with a dedicated Dong Nai River terminal, aiming at e-commerce clients that require 24-hour inventory visibility.

- June 2024: 2GO Group secured a USD 45 million Asian Development Bank credit line to retrofit eight ferries with shore-power and wastewater systems in advance of tighter Philippine clean-water rules.

ASEAN Inland Waterway Transport Market Report Scope

Inland waterway freight transport refers to the transportation of goods made entirely on navigable inland rivers employing seagoing vessels.

The ASEAN inland water freight transport market is segmented by type of transportation (liquid bulk transportation and dry bulk transportation), vessel type (vessel type, cargo ships, container ships, tankers, and other vessel types), and geography (Singapore, Thailand, Vietnam, Indonesia, Malaysia, Philippines, and Rest of ASEAN). The report offers market sizes and forecasts in value terms (USD) for all the above segments.

| Passengers | |

| Cargo | Liquid Bulk |

| Dry Bulk | |

| Others |

| Singapore |

| Thailand |

| Vietnam |

| Indonesia |

| Malaysia |

| Philippines |

| Rest of ASEAN |

| By Type of Transportation | Passengers | |

| Cargo | Liquid Bulk | |

| Dry Bulk | ||

| Others | ||

| By Country | Singapore | |

| Thailand | ||

| Vietnam | ||

| Indonesia | ||

| Malaysia | ||

| Philippines | ||

| Rest of ASEAN | ||

Key Questions Answered in the Report

What is the current value of the ASEAN inland waterway transport market?

The ASEAN Inland Waterway Transport Market stands at USD 9.12 billion in 2026 and is projected to grow to USD 11.14 billion by 2031 at a 4.09% CAGR.

Which country contributes the largest share to regional inland water revenues?

Vietnam contributes 22.51% of 2025 revenue, supported by its 41,000-kilometer Mekong Delta waterway network.

Which segment is expanding faster, cargo or passenger transport?

Passenger services are expected to grow at a 4.15% CAGR through 2031, slightly ahead of cargo’s 3.98% growth.

How are decarbonization rules affecting operators?

Singapore, Malaysia, and Indonesia are introducing LNG bunkering, shore-power, and hydrogen pilots that require costly vessel retrofits but allow compliant fleets to win premium contracts.

What are the biggest operational challenges for barge operators?

Seasonal draft shortages, fragmented cross-border regulations, and rising competition from upgraded road and rail corridors weigh on service reliability and margins.

Where do consolidation opportunities lie?

Mid-sized fleets that invest in dual-fuel retrofits, bonded depots, and digital tracking platforms can merge or partner with logistics integrators to capture e-commerce growth and climate-linked shipping premiums.

Page last updated on: