Ascorbic Acid Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 2.23 Billion |

| Market Size (2031) | USD 2.87 Billion |

| Growth Rate (2026 - 2031) | 5.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

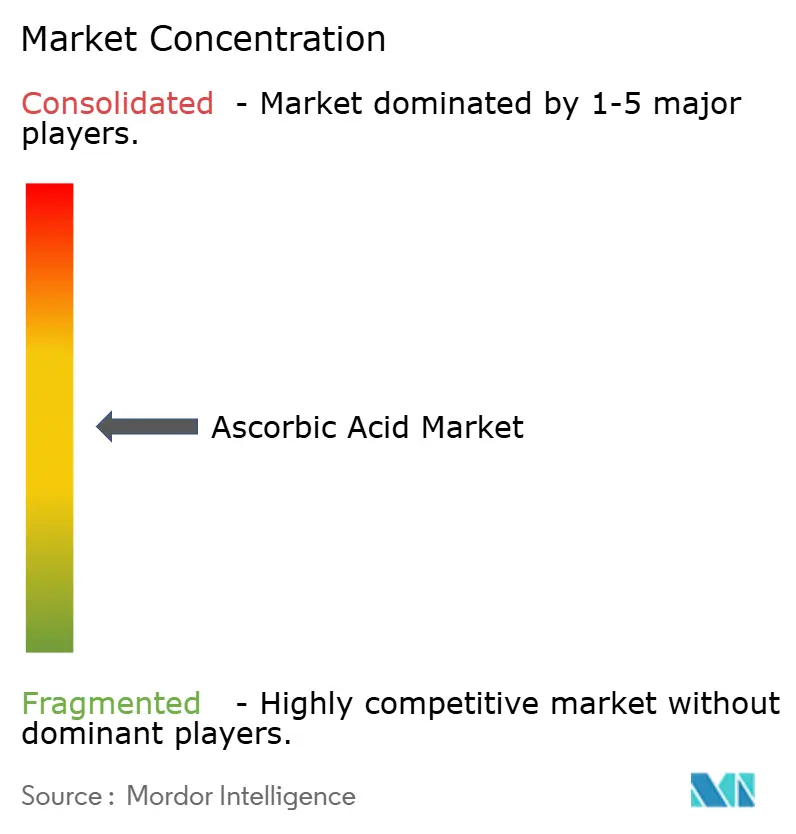

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ascorbic Acid Market Analysis by Mordor Intelligence

The global ascorbic acid market size in 2026 is estimated at USD 2.23 billion, growing from 2025 value of USD 2.12 billion with 2031 projections showing USD 2.87 billion, growing at 5.18% CAGR over 2026-2031. Structural changes are influencing the market as food, pharmaceutical, and cosmetic industries increasingly utilize vitamin C for preservation, immunity enhancement, and skincare applications. Chinese suppliers continue to implement production shutdowns to maintain price levels; however, overcapacity and weak downstream demand are exerting pressure on spot prices. Premium formats such as liposomal liquids, buffered mineral ascorbates, and coated powders are gaining market share due to their ability to address stability and absorption challenges while aligning with clean-label trends. Trade tensions between the United States and China are prompting North American buyers to explore dual sourcing or onshore blending options, leading to wider regional price disparities and shifts in trade flows. Additionally, innovation is expanding the application scope of ascorbic acid beyond traditional nutrition and preservation uses. Emerging applications include semiconductor stabilization and colon-cleansing solutions, indicating potential new revenue streams for the market.

Key Report Takeaways

- By type, sodium ascorbate led with 39.58% of the ascorbic acid market share in 2025, while potassium ascorbate is projected to grow at a 6.39% CAGR through 2031.

- By form, powder and granule formats accounted for 73.15% of the ascorbic acid market size in 2025; liquid concentrates are forecast to expand at 6.45% between 2026 and 2031.

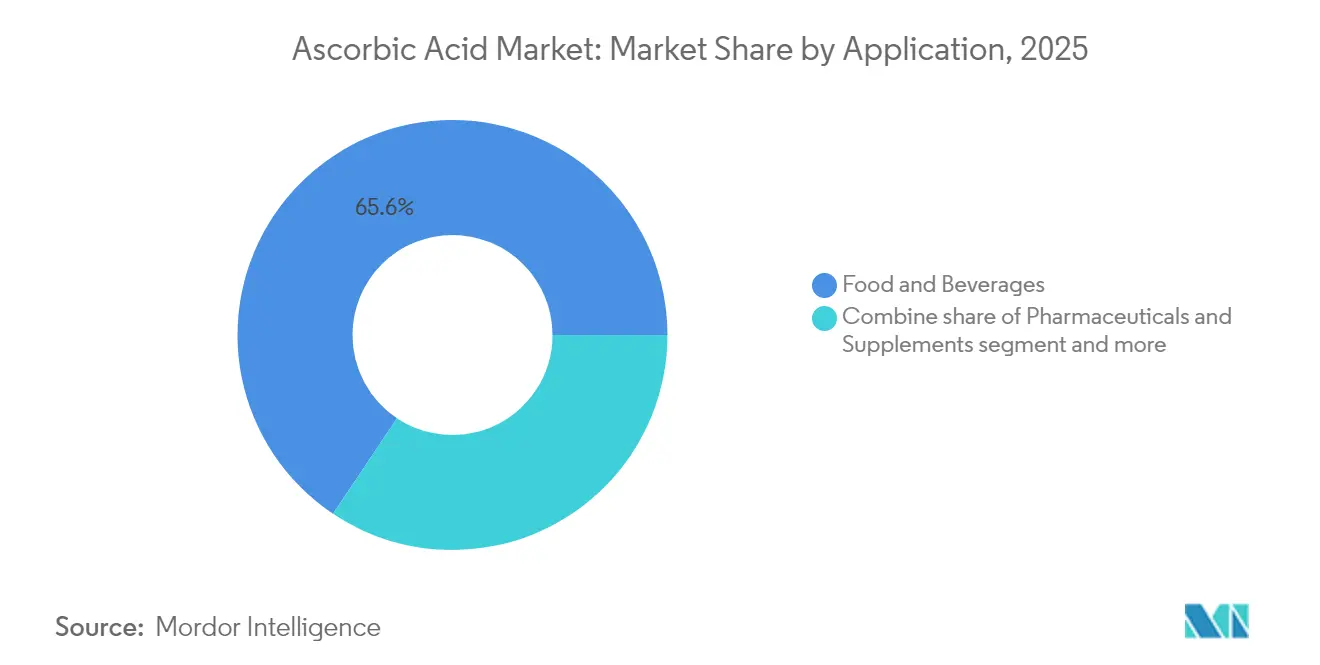

- By application, food and beverages held a 65.62% share of the ascorbic acid market size in 2025, whereas pharmaceuticals and supplements are advancing at a 6.05% CAGR to 2031.

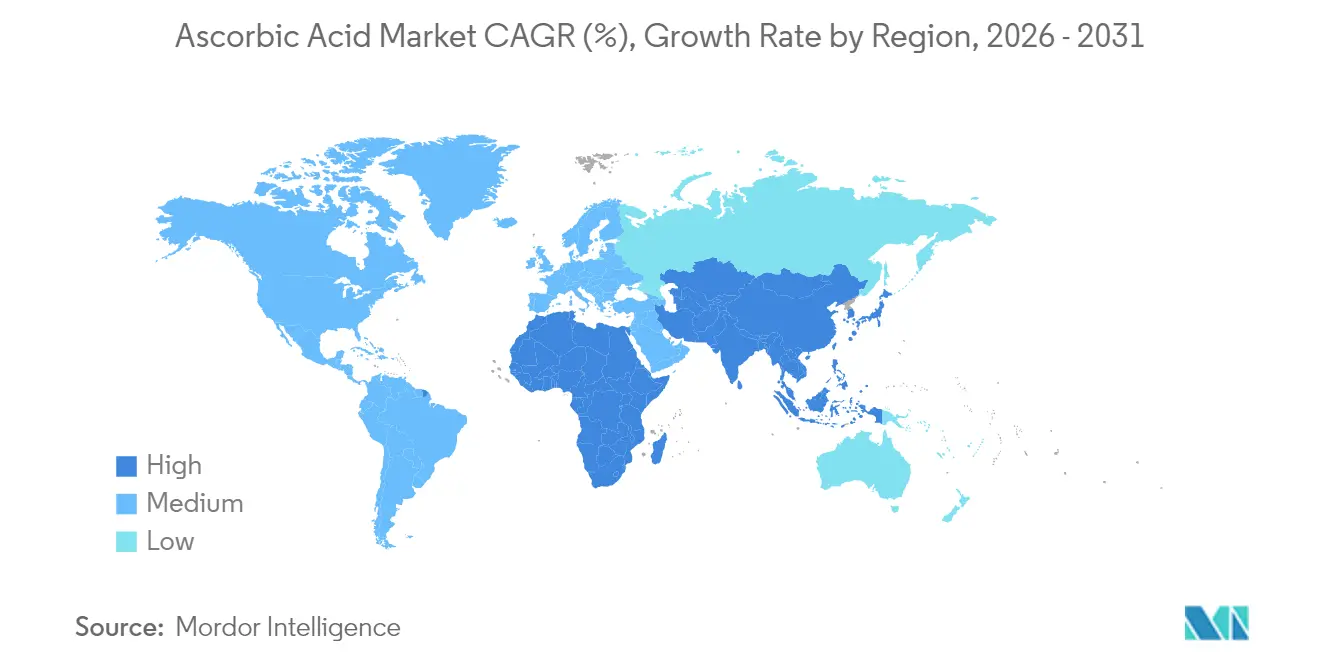

- By geography, Asia-Pacific captured 38.35% revenue in 2025 and is anticipated to post a 6.22% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ascorbic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising use of ascorbic acid as an antioxidant preservative in processed foods and beverages | +1.2% | Global, with concentration in North America and Europe | Medium term (2-4 years) |

| Expansion of fortified foods and beverages incorporating vitamin C ingredients for added health benefits | +1.0% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Increased application of vitamin C in nutricosmetics and skincare for anti-aging and antioxidant properties | +0.9% | North America, Europe, and urban Asia-Pacific | Long term (≥ 4 years) |

| Heightened clinical attention on vitamin C deficiency and associated health risks | +0.8% | Global, with emphasis on emerging markets | Short term (≤ 2 years) |

| Growth in demand for clean-label products utilizing ascorbic acid as a natural antioxidant | +0.7% | North America and Western Europe | Medium term (2-4 years) |

| Wider adoption of ascorbic acid in pharmaceutical formulations, including cold remedies and multivitamins | +1.0% | Global, with strong uptake in Asia-Pacific and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising use of ascorbic acid as an antioxidant preservative in processed foods and beverages

Food manufacturers are increasingly incorporating ascorbic acid into reformulation strategies to extend shelf life without relying on synthetic additives, a trend driven by European clean-label mandates. Ascorbic acid serves a dual purpose as an oxygen scavenger and color stabilizer, making it essential in products such as fruit juices, cured meats, and baked goods, where oxidative rancidity can compromise product quality. DSM-Firmenich has highlighted that its Quali-C brand, produced at its Dalry, Scotland facility since 1983, achieves 59 percent lower greenhouse gas emissions compared to major alternative sources. This is a key consideration for corporate sustainability buyers addressing Scope 3 (indirect emissions from a company’s value chain) reporting requirements. Regulatory approvals, including Food and Drug Administration (FDA) Generally Recognized as Safe (GRAS) listings and European Food Safety Authority (EFSA) authorization for specific use levels in oils, position ascorbic acid as a compliance-friendly option. However, its instability during thermal processing, where degradation accelerates above 70 degrees Celsius, necessitates the use of encapsulation techniques or the addition of synergistic tocopherols. This balance between regulatory support and technical challenges is driving investments in coated ascorbic acid powders designed to release vitamin C after processing. In this niche market, Chinese suppliers on Made-in-China.com offer products priced between USD 3.50 and USD 7.00 per kilogram, depending on the coating technology used.

Expansion of fortified foods and beverages incorporating vitamin C ingredients for added health benefits

Fortification mandates and voluntary enrichment programs are incorporating vitamin C into staple foods such as cereals, dairy analogs, and infant formula at levels exceeding baseline dietary intake. Increased health consciousness following the pandemic has driven demand for immune-support claims, leading beverage brands to significantly increase vitamin C concentrations in functional drinks and ready-to-drink teas. Liposomal vitamin C formulations, such as LiposoMax Liposomal PureWay-C, offer 30 percent higher plasma absorption within the first four hours compared to calcium ascorbate-calcium threonate forms. This enhanced bioavailability supports premium pricing in nutraceutical markets. Regulatory frameworks, such as Regulation (EU) No. 1169/2011, mandate nutrient reference value (NRV) labeling, standardizing consumer expectations and facilitating cross-border product launches [1]Source: UK government, “Regulation (EU) No 1169/2011 of the European Parliament and of the Council,” legislation.gov.uk. However, maintaining ascorbic acid stability in liquid formulations presents technical challenges, as pH levels below 4 accelerate degradation. To address this, formulators are increasingly using fat-soluble derivatives like ascorbyl palmitate or magnesium ascorbyl phosphate, which resist oxidation and effectively penetrate lipid-rich tissues. This shift has led to a bifurcation between water-soluble commodity ascorbic acid and lipophilic specialty derivatives, prompting Indian and Chinese manufacturers to expand esterification capacity to capture higher-margin market segments.

Increased application of vitamin C in nutricosmetics and skincare for anti-aging and antioxidant properties

Topical vitamin C serums have transitioned from niche dermatology clinics to mainstream beauty aisles, supported by clinical evidence linking L-ascorbic acid to collagen production and tyrosinase inhibition. Magnesium ascorbyl phosphate, a water-soluble derivative, has demonstrated an 89 percent reduction in oxidative stress and a 34 percent improvement in skin firmness in preclinical assays, although these results lack peer-reviewed validation. The instability of pure ascorbic acid, which is prone to oxidation when exposed to air and light, has driven innovation in stabilization technologies. For instance, Fuji Oil Holdings patented a water-in-oil emulsion with an aqueous phase pH of greater than or equal to 4 and particle size less than or equal to 300 nanometers, addressing issues such as unpleasant taste and discoloration while simplifying manufacturing processes. Similarly, Natura Cosméticos secured a patent in July 2024 for a stable skin-lightening composition containing high-concentration ascorbic acid combined with complementary active ingredients, targeting hyperpigmentation markets in Latin America and Asia. Regulatory compliance with cosmetic safety standards, such as International Organization for Standardization (ISO) 22716 for Good Manufacturing Practices, adds complexity to the market [2]Source: International Organization for Standardization, “Cosmetics — Good Manufacturing Practices (GMP) — Guidelines on Good Manufacturing Practices,” iso.org. This compliance tends to favor established companies with in-house toxicology laboratories over contract manufacturers that rely on third-party testing. Additionally, the convergence of ingestible and topical vitamin C in the form of nutricosmetics is blurring category boundaries, with brands introducing synchronized oral-and-serum regimens that claim to promote inside-out skin renewal.

Heightened clinical attention on vitamin C deficiency and associated health risks

Public health agencies are revisiting vitamin C adequacy thresholds as emerging research links marginal deficiency, defined as serum levels below 11.4 micromoles per liter, to impaired immune function and delayed wound healing. The World Health Organization's (WHO) acceptable daily intake of up to 1.25 milligrams per kilogram of body weight provides regulatory flexibility for high-dose supplementation [3]Source: World Health Organization, “Evaluation Of Certain Food Additives And Contaminants” iris.who.int. However, clinical trials exploring intravenous ascorbic acid for sepsis and COVID-19 have yielded mixed results, tempering enthusiasm for its therapeutic claims. Pharmaceutical formulators are responding with multi-dose vial formats, such as 200 milligrams per vial and 500 milligrams per vial, that enable titration in hospital settings. This is evidenced by 343 finished-dosage-form dossiers and 20 United States Food and Drug Administration (FDA) Orange Book entries for ascorbic acid injectables. The regulatory pathway for intravenous vitamin C remains stringent, as United States Drug Master File (USDMF) and Certificate of Suitability to the Monographs of the European Pharmacopoeia (CEP) filings require batch-to-batch purity documentation. CSPC Pharmaceutical's DMF 23162 and Royal DSM's DMF 30618 serve as benchmarks for compliance. Smokers, who require 35 milligrams per day more than non-smokers due to oxidative stress, represent a targeted cohort for fortified tobacco-cessation products. However, consumer skepticism of functional tobacco alternatives continues to limit adoption in this segment.

Restraints Impact Analysis*

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict regulations on purity, safety, and labeling impact food, pharmaceutical, and cosmetic industries | -0.6% | Global, with stringent enforcement in North America and Europe | Medium term (2-4 years) |

| Price fluctuations of raw materials affect ascorbic acid production costs and market stability | -0.8% | Global, with acute impact in Asia-Pacific production hubs | Short term (≤ 2 years) |

| Vitamin C degradation during processing, storage, and distribution reduces its effectiveness in applications | -0.5% | Global, particularly in tropical and subtropical regions | Long term (≥ 4 years) |

| Alternative antioxidants replace vitamin C in certain food and cosmetic formulations, limiting its usage | -0.4% | North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Strict regulations on purity, safety, and labeling impact food, pharmaceutical, and cosmetic industries

Regulatory agencies impose complex compliance requirements that disproportionately impact smaller manufacturers without in-house analytical laboratories. The United States Food and Drug Administration (FDA)'s Inactive Ingredients Database lists ascorbic acid for oral, rectal, and topical applications, each necessitating specific purity profiles and residual-solvent limits. The Food Standards Agency (FSA)'s re-evaluation of antioxidants in 2024 introduced stricter acceptable daily intake calculations, compelling reformulation of products exceeding the revised thresholds. In India, the Food Safety and Standards Authority of India (FSSAI) mandates batch-wise testing for heavy metals, requiring lead levels to remain below 2 parts per million and arsenic levels to remain below 1 part per million. This standard must be met by Chinese exporters to access the expanding supplement market in the region. The cost of United States Drug Master File (USDMF) and Certificate of Suitability to the Monographs of the European Pharmacopoeia (CEP) filings, which exceed USD 50,000 per submission along with annual maintenance fees, creates significant entry barriers. This has consolidated supply among established players such as CSPC Pharmaceutical (DMF 23162, CEP R1-CEP 2004-019 Rev 06) and Royal DSM (DMF 30618, CEP R1-CEP 1996-078 Rev 05). Labeling requirements further complicate cross-border trade. Regulation (EU) No. 1169/2011 mandates nutrient reference values, allergen declarations, and origin statements, while U.S. Nutrition Facts panels adhere to the FDA's 2016 format. This regulatory landscape benefits multinational corporations with dedicated compliance teams, leaving regional players to compete primarily on price in less-regulated markets.

Price fluctuations of raw materials affect ascorbic acid production costs and market stability

Corn-derived glucose, which serves as the primary feedstock for fermentation-based ascorbic acid, is influenced by agricultural commodity cycles. Prices tend to increase during droughts or when biofuel mandates reduce the available supply. Chinese producers, who dominate global production, often reduce their operating schedules to manage inventory levels and support prices. However, this coordination remains fragile. Weak demand in the end markets during 2024 led to price declines despite extended production shutdowns. A planned five-month shutdown by a major Chinese producer in mid-2025 may stabilize spot markets, but buyers remain cautious due to previous failures to maintain production discipline. Freight cost inflation has further exacerbated raw material volatility. For example, container shipping rates from Shanghai to Rotterdam increased by 40 percent in early 2024, squeezing margins for importers unable to pass on these costs. Additionally, United States tariffs on Chinese goods, raised to 20 percent in March 2025, have introduced geopolitical challenges. North American buyers are increasingly exploring Indian and European suppliers, but capacity outside China remains constrained. Notably, Northeast Pharmaceutical Group and Shandong Luwei collectively control an estimated 60 percent of global production. The lack of long-term supply contracts, with buyers typically maintaining coverage for only three months, further amplifies price volatility and discourages capital investment in new production capacity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Electrolyte-Balanced Salts Gain Pharmaceutical Traction

Sodium ascorbate accounted for 39.58% of the type segment in 2025, driven by its dual functionality as a reducing agent in meat curing and an antioxidant in fruit juice processing. Potassium ascorbate is projected to grow at a rate of 6.39% through 2031, gaining traction among pharmaceutical formulators seeking electrolyte-balanced delivery systems for oral rehydration salts and sports nutrition products, particularly where sodium overload poses cardiovascular concerns. Calcium ascorbate is favored by bone-health brands for its combination of vitamin C and calcium, supporting claims related to collagen synthesis. Magnesium ascorbate is positioned for stress-relief supplements, leveraging magnesium's calming properties.

D-isoascorbic acid, a stereoisomer without vitamin activity, is utilized as a cost-effective color stabilizer in cured meats, though its adoption is limited by regulatory restrictions in certain regions. Patent activity highlights niche innovations, such as Norgine BV's 2024 patent for colon-cleansing solutions containing 300 to 800 millimoles per liter of ascorbate anion, which is a blend of ascorbic acid and ascorbate salts. This demonstrates applications that extend beyond nutrition.

By Form: Liquid Concentrates Bypass Recrystallization Bottlenecks

In 2025, powder and granule forms accounted for 73.15% of the market, primarily due to their stability, ease of transport, and compatibility with dry-blending processes in food and supplement manufacturing. Liquid ascorbic acid, projected to grow at a rate of 6.45% through 2031, is gaining traction among beverage manufacturers who prioritize ready-to-use concentrates. These formulations eliminate recrystallization steps and reduce batch-to-batch variability. Additionally, liquid formulations support precise dosing in high-speed bottling lines, offering a technical advantage that justifies a 15% to 20% price premium over powder alternatives.

However, liquid ascorbic acid faces stability challenges, as it oxidizes within weeks unless the pH is maintained below 4 and oxygen exposure is minimized. This has driven innovations such as nitrogen-flushed packaging and the use of chelating agents like ethylenediaminetetraacetic acid (EDTA) to sequester trace metals that catalyze degradation.

Liposomal liquid vitamin C, such as LiposoMax Liposomal PureWay-C, offers 30% higher plasma absorption within four hours compared to non-liposomal forms. This enhanced bioavailability appeals to nutraceutical brands targeting premium market segments.

By Application: Pharmaceutical Segment Accelerates on Immunity Narratives

In 2025, the food and beverages segment accounted for 65.62% of the application market, driven by the widespread use of ascorbic acid in products such as fruit juices, baked goods, and cured meats, where it helps prevent oxidative rancidity and color fading. The pharmaceuticals and supplements segment, projected to grow at a rate of 6.05% through 2031, is supported by increased focus on immunity post-pandemic and clinical interest in high-dose intravenous applications for conditions like sepsis and viral infections, despite mixed trial outcomes.

Over-the-counter cold remedies are incorporating 1,000 milligrams of vitamin C per tablet, leveraging consumer belief in its immune-supporting properties, while multivitamin manufacturers are transitioning to buffered mineral ascorbates to minimize gastric irritation.

In animal feed applications, vitamin C is used to enhance immune function in aquaculture and reduce stress in poultry; however, this segment faces challenges as price-sensitive buyers opt for cheaper alternatives during periods of margin compression. The personal care and cosmetics segment, though smaller, is experiencing rapid innovation. Topical vitamin C serums utilize L-ascorbic acid for its collagen-boosting and tyrosinase-inhibiting effects, with advancements in stabilization technologies such as water-in-oil emulsions and lipophilic derivatives being patented.

Geography Analysis

In 2025, the Asia-Pacific region emerged as the leading segment, contributing 38.35% of global revenue. This dominance is attributed to China's significant production capacity and India's growing demand for supplements. Chinese manufacturers, including CSPC Pharmaceutical, Northeast Pharmaceutical Group, and Shandong Luwei, collectively account for approximately 60% of global ascorbic acid production. These companies utilize fermentation-based processes to convert corn-derived glucose into L-ascorbic acid on a large scale. Efforts to stabilize prices through coordinated production shutdowns in 2024 were undermined by persistent overcapacity and weak end-market demand, leading to declining spot prices despite reduced production volumes.

The fastest-growing segment is India, driven by fortification programs mandated by the Food Safety and Standards Authority of India (FSSAI). These programs incorporate vitamin C into staple foods such as wheat flour, rice, and edible oils. Additionally, urban consumers are increasingly purchasing immunity supplements and nutricosmetics. In Japan, the pharmaceutical sector is navigating supply chain disruptions. Nichi-Iko Pharmaceutical's ascorbic acid injectables (100 milligrams and 500 milligrams) were delisted from national health insurance pricing in 2024, forcing hospitals to seek alternative suppliers.

Other regions, including North America, Europe, South America, and the Middle East and Africa, are also contributing to the market. North America and Europe remain high-value markets, with premium formulations such as liposomal vitamin C and buffered mineral ascorbates commanding higher margins. In the United States, tariffs on Chinese goods were raised to 20% in March 2025, prompting buyers to explore Indian suppliers like Reckon Organics and West Bengal Chemicals, although capacity constraints limit substitution. European buyers are prioritizing sustainability, with DSM-Firmenich's Dalry facility securing contracts due to its 59% lower greenhouse gas emissions compared to alternative sources. In South America, Brazil's food fortification programs aimed at addressing iron-deficiency anemia combine ferrous sulfate with ascorbic acid to enhance iron absorption, driving dual demand. In Nigeria, pharmaceutical imports are increasing as local manufacturers lack the fermentation capacity to produce ascorbic acid domestically, creating opportunities for Chinese and Indian exporters with National Agency for Food and Drug Administration and Control (NAFDAC) registrations. In the Middle East, particularly in the United Arab Emirates and Saudi Arabia, the cosmetics market is adopting vitamin C serums and nutricosmetics. However, high ambient temperatures in the region accelerate product degradation, necessitating cold-chain logistics that increase landed costs by 10 to 15 percent.

Competitive Landscape

The ascorbic acid market demonstrates moderate fragmentation, characterized by a dual structure. Chinese commodity producers focus on high-volume, low-cost production, while Western companies prioritize specialty formulations to capture higher margins. Key players in the low-cost segment include CSPC Pharmaceutical, Northeast Pharmaceutical Group, and Shandong Luwei, which utilize fermentation-based production processes with capacities exceeding 10,000 metric tons annually. These companies rely on corn-glucose feedstock and coordinated production shutdowns to manage supply. In contrast, DSM-Firmenich and BASF dominate the premium segment, offering branded products such as ROVIMIX Stay-C 35 and Quali-C, which command 20 to 30 percent price premiums due to their emphasis on sustainability with 59 percent lower greenhouse gas emissions, stability, and regulatory compliance such as United States Drug Master File (USDMF) and Certificate of Suitability to the Monographs of the European Pharmacopoeia (CEP) filings.

Vertical integration serves as a key competitive advantage in the market. For instance, DSM-Firmenich's Dalry facility produces ascorbic acid internally and incorporates it into animal nutrition premixes, enabling value capture across the supply chain. Patent activity highlights diversification into non-nutrition applications, such as DSM-Firmenich's stable vitamin C formulations for cosmetics, Norgine BV's colon-cleansing solutions, and Fuji Oil Holdings' water-in-oil emulsions. These developments reflect efforts to leverage ascorbic acid's redox chemistry in adjacent markets. Emerging opportunities include bioavailability-enhanced formats and non-food applications. Liposomal vitamin C, which offers 30 percent higher plasma absorption compared to standard forms, remains underutilized in mass-market supplements, with most products limited to premium channels. Additionally, industrial applications, such as ascorbic acid's use as a stabilizer for n-type organic semiconductors as noted in a 2024 Nature Materials study, suggest potential demand in electronics manufacturing, though commercialization timelines remain uncertain.

New entrants, such as Indian manufacturers Reckon Organics and West Bengal Chemicals, are scaling Current Good Manufacturing Practice (cGMP)-certified production capacities to cater to North American and European buyers seeking alternatives to Chinese suppliers amid tariff pressures. Technology adoption varies across regions. Chinese producers predominantly use traditional Reichstein-Grüssner fermentation methods, while Western companies invest in advanced technologies like enzymatic synthesis and continuous-flow reactors, which reduce energy consumption and waste. The competitive landscape is likely to see consolidation as regulatory compliance costs such as United States Drug Master File (USDMF) filings, batch-release testing, and sustainability audits favor larger players. However, regional quality standards and tariff barriers continue to sustain a fragmented supplier base.

Ascorbic Acid Industry Leaders

DSM-Firmenich N.V.

BASF SE

CSPC Pharmaceutical Group Ltd

Northeast Pharmaceutical Group Co. Ltd

Shandong Luwei Pharmaceutical Co. Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Seiwa Kasei launches iVC 3GA-green, a plant-derived 3-Glyceryl Ascorbate (ascorbic acid derivative) with patented technology. The preservative-free ingredient targets anti-aging skincare through enhanced collagen production and melanin inhibition, offering superior stability for concentrated serums and vitamin C cosmetics.

- September 2024: Norgine BV was granted U.S. Patent 12083179 for colon-cleansing solutions using 300 to 800 millimoles per liter ascorbate anion (mixture of ascorbic acid and ascorbate salts), demonstrating medical applications beyond nutrition

- March 2024: DSM-Firmenich Divests Jiangshan Vitamin C Plant in China – DSM-Firmenich completed divestiture of its Jiangshan ascorbic acid (Vitamin C) manufacturing facility in China, marking strategic portfolio repositioning within global vitamin C supply chain amid intensifying competition from Chinese producers.

Global Ascorbic Acid Market Report Scope

Ascorbic acid helps prevent vitamin C deficiency in individuals who do not get enough vitamin content from their daily diet. The ascorbic acid market is segmented by application and geopgraphy. Based on application the market is segmented into food and beverage, pharmaceuticals and healthcare, beauty and personal care, and animal feed. Based on geography the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle-East and Africa. For each segment, the market size and forecast have been done based on value (in USD million).

| Sodium Ascorbate |

| Calcium Ascorbate |

| Potassium Ascorbate |

| Magnesium Ascorbate |

| D-Isoascorbic Acid |

| Powder/Granules |

| Liquid |

| Food and Beverages |

| Pharmaceuticals and Supplements |

| Animal feed |

| Personal Care and Cosmetics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Type | Sodium Ascorbate | |

| Calcium Ascorbate | ||

| Potassium Ascorbate | ||

| Magnesium Ascorbate | ||

| D-Isoascorbic Acid | ||

| By Form | Powder/Granules | |

| Liquid | ||

| By Application | Food and Beverages | |

| Pharmaceuticals and Supplements | ||

| Animal feed | ||

| Personal Care and Cosmetics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the ascorbic acid market in 2026 and how fast is it growing?

The ascorbic acid market size stands at USD 2.23 billion in 2026 and is projected to reach USD 2.87 billion by 2031 on a 5.18% CAGR.

Which region generates the greatest revenue?

Asia-Pacific leads with 38.35% of global revenue in 2025 and is expected to maintain the fastest regional CAGR at 6.22% through 2031.

What segment is expanding faster than the overall market?

Pharmaceuticals and supplements are advancing at 6.05% per year, outpacing the aggregate growth rate as immunity and clinical applications rise.

What innovations are shaping future demand?

Liposomal liquids that boost absorption, buffered mineral ascorbates that reduce gastric irritation, and patents extending vitamin C into semiconductors and colon-cleansing solutions are redefining market frontiers.

Page last updated on: