Artificial Turf Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

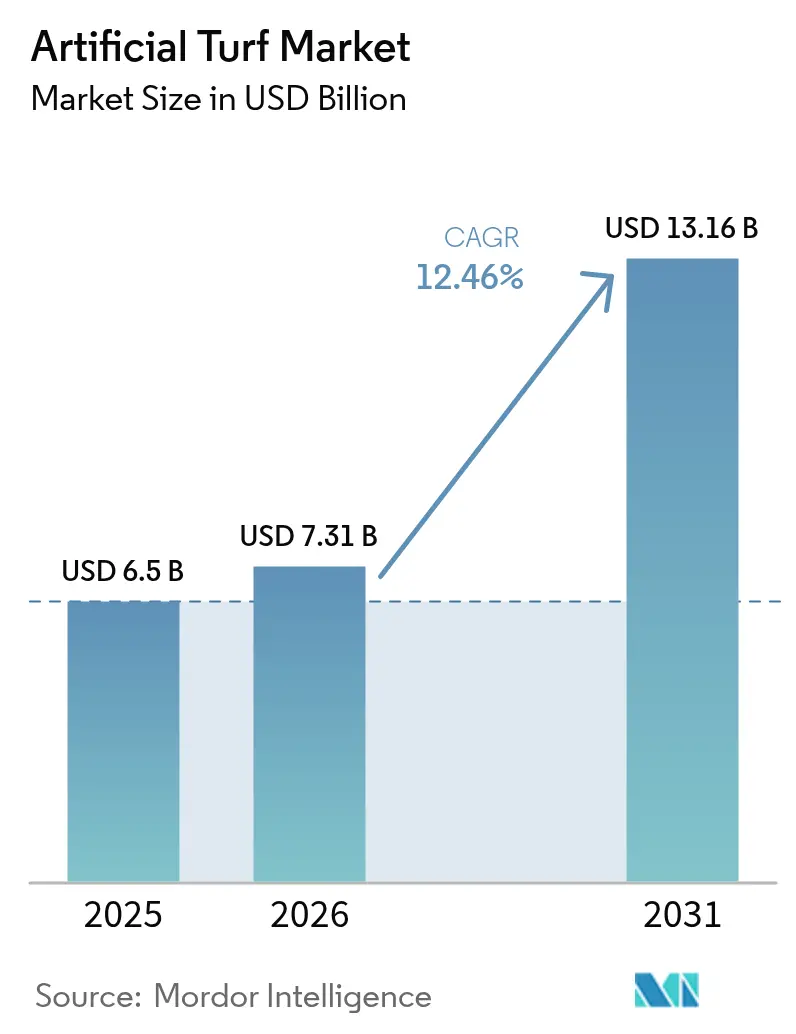

| Market Size (2026) | USD 7.31 Billion |

| Market Size (2031) | USD 13.16 Billion |

| Growth Rate (2026 - 2031) | 12.46% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

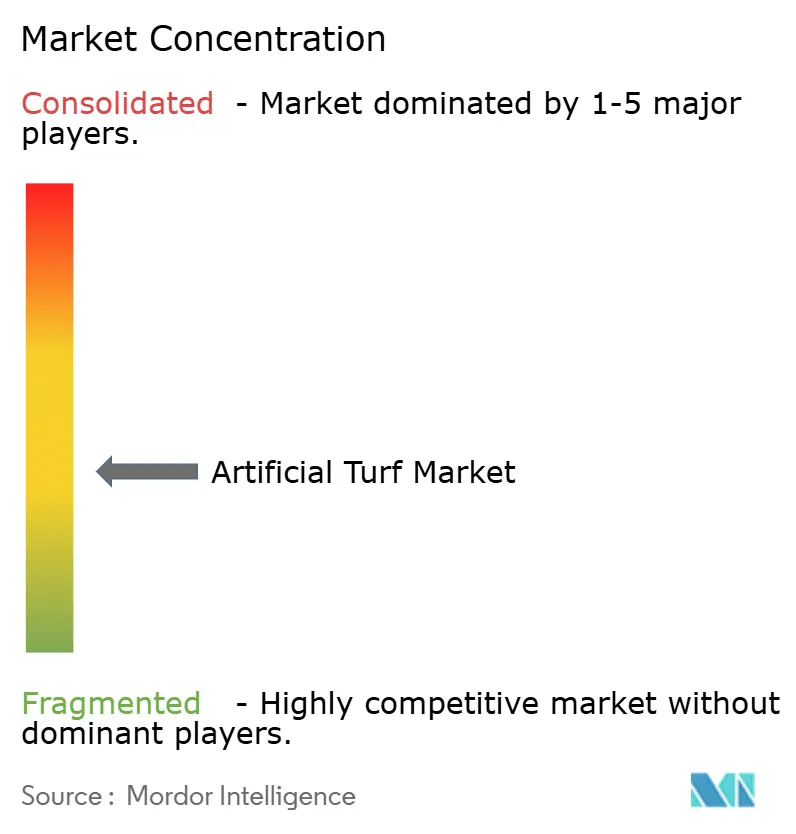

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Artificial Turf Market Analysis by Mordor Intelligence

Artificial turf market size in 2026 is estimated at USD 7.31 billion, growing from 2025 value of USD 6.5 billion with 2031 projections showing USD 13.16 billion, growing at 12.46% CAGR over 2026-2031. Heightened drought risk and mandatory water-conservation laws are shifting demand beyond sports venues into residential, commercial, and civic infrastructure. Competitive intensity remains moderate; global leaders such as Tarkett (FieldTurf) and TenCate Grass defend their share through large‐scale extrusion capacity and early-stage recycling programs, while Shaw Sports Turf, CCGrass, and a growing cadre of regional specialists leverage proximity and price agility to win municipal and school contracts. Innovation now centers on low-heat fiber chemistries, per- and polyfluoroalkyl substances-free formulations, and closed-loop recycling partnerships that address the tightening EU microplastics rules and North American extended producer responsibility proposals. Buyers are increasingly evaluating suppliers on end-of-life solutions and verified cooling performance, resulting in a pricing premium for technology owners, even as overall market fragmentation persists.

Key Report Takeaways

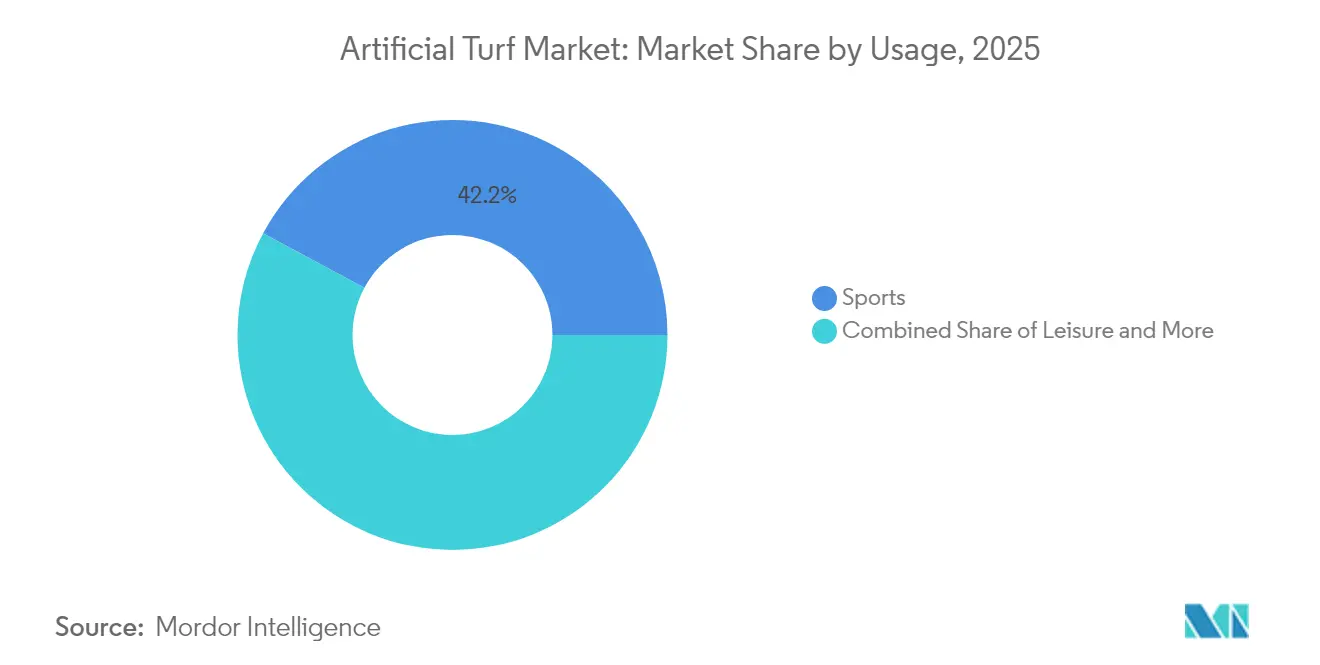

- By usage, sports led with 42.15% of the artificial turf market share in 2025, whereas landscapes are projected to expand at a 14.62% CAGR to 2031.

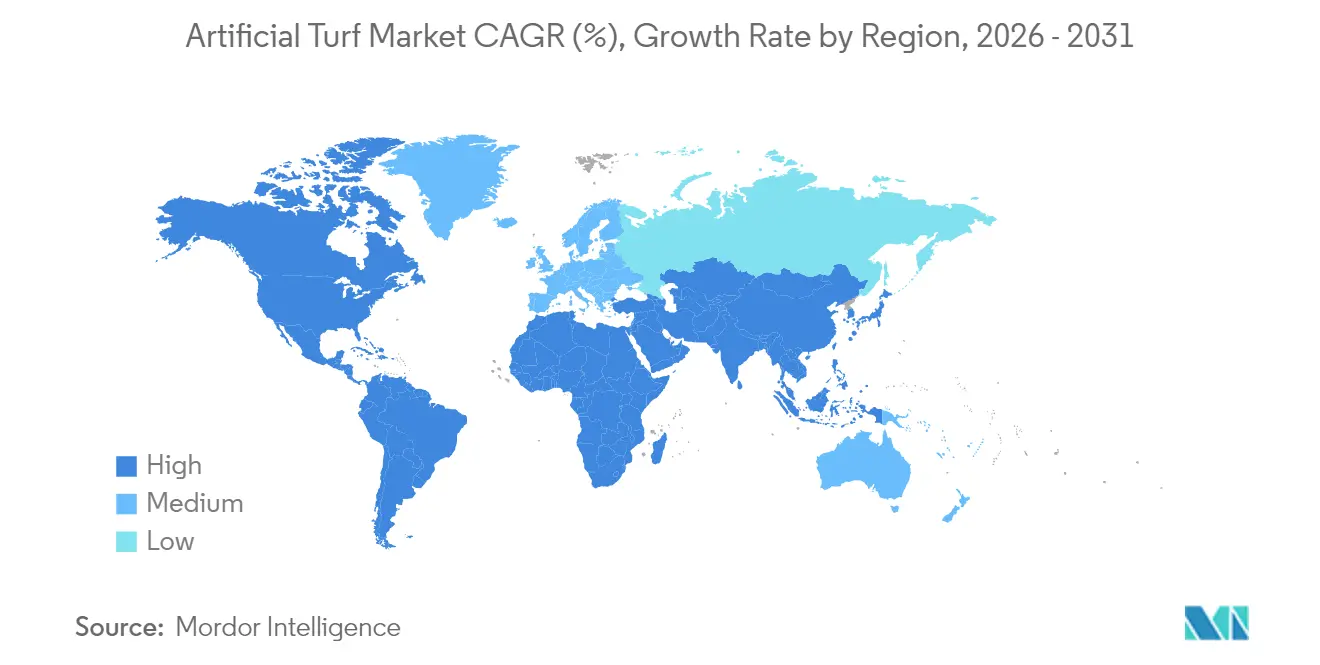

- By geography, North America captured a 37.74% share of the artificial turf market size in 2025, while Asia-Pacific is advancing at a 13.98% CAGR through 2031.

- The competitive landscape remains moderately fragmented. Tarkett (FieldTurf) and TenCate Grass lead the way with sustainability credentials, and recycling infrastructure is emerging as the primary differentiator, rather than price alone.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Artificial Turf Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent water-conservation mandates | +2.8% | North America and Australia core, expanding to Europe | Medium term (2-4 years) |

| Expanding installation in multi-sport stadia | +2.1% | Global, with a concentration in Asia-Pacific and the Middle East | Long term (≥ 4 years) |

| Surging residential and commercial landscaping demand | +3.2% | North America and Europe primary, Asia-Pacific emerging | Short term (≤ 2 years) |

| Urban-heat-island climate resilience projects | +1.4% | Global urban centers, priority in Asia-Pacific megacities | Long term (≥ 4 years) |

| Adoption of autonomous turf-laying robots | +0.9% | North America and Europe early adoption markets | Medium term (2-4 years) |

| Circular turf recycling/Extended Producer Responsibility programs | +1.1% | Europe mandatory, North America voluntary adoption | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Water-Conservation Mandates

California’s AB 1572 and Colorado’s SB 24-005 remove potable-water irrigation from nonfunctional lawns and ban new nonfunctional turf, converting discretionary upgrades into compliance obligations. Accelerated timelines strain installer capacity and pull forward replacement cycles, effectively anchoring the artificial turf market to public-policy calendars rather than team-season budgets. Municipalities in Arizona, Nevada, and parts of Australia have begun drafting parallel ordinances to safeguard dwindling aquifers.

Expanding Installation in Multi-Sport Stadia

Elite venues increasingly demand fields that can host football, soccer, and concerts within compressed scheduling windows. Mercedes-Benz Stadium’s 2025 FieldTurf CORE installation and SoFi Stadium’s hybrid turf pilot for the 2026 World Cup illustrate the visibility that large contracts create for next-generation systems. These specification uplifts migrate to collegiate and secondary facilities within two to three bid cycles, multiplying the revenue influence of each flagship project.

Surging Residential and Commercial Landscaping Demand

Landscaping applications benefit from convergent trends, including water conservation, maintenance cost reduction, and aesthetic consistency requirements. The segment's 15.3% CAGR reflects fundamental shifts in property management economics, where artificial turf's higher upfront costs become justified by the elimination of irrigation, fertilization, and maintenance expenses. Commercial property managers are increasingly specifying artificial turf for common areas to achieve predictable landscaping budgets and maintain year-round visual appeal[1]Source: Synthetic Turf Council, “Landscape Benefits Fact Sheet,” syntheticturfcouncil.org. Hospitality chains are standardizing the use of artificial turf in courtyards to meet ESG targets tied to water conservation and irrigation cuts.

Urban Heat-Island Climate-Resilience Projects

Cities integrate artificial turf cooling systems into broader urban heat mitigation strategies, transforming product specifications from performance-focused to climate-adaptive requirements. Dutch research demonstrating 25.5°C temperature reductions through subsurface water storage systems positions cooling-enhanced turf as infrastructure rather than a recreational amenity. Municipal procurement increasingly prioritizes heat reduction capabilities alongside durability metrics, creating differentiation opportunities for manufacturers developing climate-adaptive solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Micro and nano-plastic pollution scrutiny | -1.8% | Europe's regulatory leadership, global environmental advocacy | Medium term (2-4 years) |

| High upfront installation cost | -2.1% | Global, particularly price-sensitive emerging markets | Short term (≤ 2 years) |

| European Union ban on crumb-rubber infill | -1.4% | Europe's direct impact, global supply chain disruption | Short term (≤ 2 years) |

| Player heat-stress litigation risk | -0.7% | North America litigation environment, global safety standards | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Micro- and Nano-Plastic Pollution Scrutiny

The European Chemicals Agency estimates sports pitches contribute 16,000 metric tons of microplastics annually, accelerating momentum for a continent-wide crumb-rubber phase-out[2].Source: European Chemicals Agency, “Microplastics from Artificial Turf Pitches,” echa.europa.eu Manufacturers must redesign infill containment and explore polymer-bound or plant-based alternatives, which could increase system costs by 8-12%. The European Chemicals Agency has now confirmed the shedding of nano-plastic fibers under mechanical wear, strengthening arguments for tighter specification limits and extended producer responsibility schemes.

High Upfront Installation Cost

Installation cost barriers intensify in price-sensitive segments, where artificial turf competes against natural grass alternatives that have lower initial capital requirements. Municipal budget constraints limit the adoption of solutions despite long-term operational savings, particularly in emerging markets where financing mechanisms for infrastructure improvements remain underdeveloped. The cost differential becomes pronounced for smaller installations where economies of scale cannot offset preparation and installation expenses, creating market segmentation between premium applications and cost-constrained projects. Economic sensitivity increases during periods of elevated material costs and labor shortages, forcing manufacturers to balance margin preservation against market access objectives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Usage: Sports Dominate Despite Landscape Acceleration

Sports accounted for a 42.15% slice of the artificial turf market in 2025, anchoring recurring eight- to ten-year replacement cycles across professional and collegiate venues. Contact Sports, such as hockey, tennis, and baseball fields, pursue fiber blends that optimize ball roll and shock attenuation, reinforcing a premium tier that shields margins even when resin costs rise. Other sports applications, including baseball and multi-purpose fields, are increasingly specifying hybrid systems that combine synthetic reinforcement with natural grass playing surfaces.

Upgrades now include heat-reflective pigments and stitched labels that log maintenance data for warranty validation. Meanwhile, the landscape is advancing at a 14.62% CAGR to 2031, outpacing every sports sub-segment as municipalities pivot toward drought resilience. This acceleration reflects fundamental shifts in property management economics, where artificial turf's higher upfront costs become justified by the elimination of irrigation and maintenance expenses. Leisure applications, encompassing playgrounds and recreational areas, benefit from safety improvements and year-round usability that natural surfaces cannot provide consistently.

Geography Analysis

North America is projected to command a 37.74% market share in 2025, driven by its established sports infrastructure and predictable replacement cycle across professional, collegiate, and municipal facilities. The region's market maturity generates stable revenue streams through scheduled field renewals and regulatory compliance installations, particularly following the implementation of water conservation mandates. California’s potable-water ban for nonfunctional lawns and Colorado’s turf-planting moratorium create immediate compliance projects with limited scheduling flexibility. Mexico’s municipal parks favor synthetics to curb rising water bills and extend play hours despite temperature spikes.

The Asia-Pacific region emerges as the fastest-growing region, with a 13.98% CAGR from 2026 to 2031, driven by urbanization pressures and the development of sports infrastructure across major economies. China's massive stadium construction programs and India's growing investments in sports facilities create substantial installation opportunities that dwarf replacement-driven demand in mature markets. The region’s freight advantage supports exports across Southeast Asia, while Japan’s dense urban zones provide test beds for heat-mitigating fibers. Government grants in South Korea offset upfront costs for school pitches, thereby accelerating the penetration of primary education facilities.

The Europe, Middle East, and Africa regions represent emerging growth opportunities, despite regulatory headwinds from environmental restrictions. The European Union's ban on crumb rubber infill creates short-term disruption but drives innovation toward sustainable alternatives that may establish competitive advantages in global markets. South America's market development reflects economic constraints and infrastructure priorities that favor cost-effective solutions over premium specifications. Africa's limited current market presence suggests significant long-term potential as economic development and sports infrastructure investment accelerate across the continent.

Regulatory Landscape

The regulatory environment for artificial turf is increasingly shaped by microplastics restrictions and chemical-content requirements that influence infill choices, reporting duties, and product formulations. In the European Union, Regulation (EU) 2023/2055 (the microplastics restriction) sets a pathway toward prohibiting the placing on the market of synthetic polymer microparticle infill used in artificial turf, with the restriction taking effect on 17 October 2031. It also introduces ECHA-linked reporting requirements, with the first reporting cycle starting in 2026 for emissions occurring in the previous calendar year. This is pushing buyers and suppliers toward non-infill or contained-infill systems and is raising demand for documented shedding and containment performance in tenders.

In the United States, state-level actions are tightening around PFAS content in turf materials while federal PFAS reporting expands supply-chain compliance obligations. California Assembly Bill 1423 took effect on 1 January 2026, prohibiting the purchase, installation, manufacturing, distribution, and sale of artificial turf or synthetic surfaces containing regulated PFAS, shifting PFAS-free formulations from a preference to a market-access requirement in a major state. At the federal level, the US EPA finalized rules in February 2026 (40 CFR Part 372) adding specific PFAS to the EPCRA Section 313 list, triggering new reporting requirements beginning with the 2026 reporting year and increasing traceability expectations across resin, yarn, backing, and additive suppliers.

Competitive Landscape

The artificial turf market exhibits moderate fragmentation, featuring both global brands and regional specialists. Tarkett’s FieldTurf division runs extrusion plants in France, Germany, and Abu Dhabi, supplementing United States production to balance freight costs and diversify resin sourcing. Its Pennsylvania regeneration facility processes 2,600 metric tons of post-consumer turf annually in 2021, bolstering bids in jurisdictions that weigh end-of-life plans during tender scoring. TenCate Grass collaborates with ExxonMobil using Exxtend technology to convert reclaimed polyethylene into virgin-grade feedstock, enabling a closed-loop supply chain that aligns with EU circularity mandates.

Shaw Sports Turf competes on tufting speed and full-depth color consistency, targeting high-volume high-school fields where budget certainty trumps hybrid-grass aesthetics. CCGrass expands its Asian market coverage through lower-priced ranges backed by FIFA Preferred Producer status, while SIS Pitches focuses on turnkey hybrid systems for rugby venues that require stitched natural roots for scrum stability.

Emerging entrants explore sugar-cane-based yarns, silicone-free antistatic treatments, and AI-based wear diagnostics. Technology crossovers from geosynthetics and roofing membranes introduce UV-stabilizer packages that lengthen fiber life in equatorial climates. Competitive intensity is likely to rise once EU extended-producer-responsibility fees fully apply in 2027, pushing mid-tier firms to partner with recyclers or exit.

Artificial Turf Industry Leaders

CCGrass

Tarkett (FieldTurf)

TenCate Grass

Shaw Sports Turf

Sports Group (Polytan)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven redesign and verification are creating room for suppliers that can deliver documented low-emission and low-chemical systems at scale, particularly in public procurement where specifications increasingly reference microplastics control, infill alternatives, and material transparency. ASTM International published ASTM F3782-26 in May 2026, establishing a unified framework for sampling and testing PFAS in synthetic turf fibers and backing, which gives manufacturers a clearer basis for differentiating with validated PFAS-free bills of materials and test-backed declarations. At the same time, the EU microplastics rule has put 2026 into focus as an operational starting point for emissions reporting cycles tied to ECHA guidance, which reinforces demand for products and installation practices that reduce loss of polymer particles from pitches and surrounding drainage.

Circularity and end-of-life solutions are also becoming more visible in buying criteria, leading to partnership and project activity around recycling and microplastic-free system architectures. In June 2026, Aduro Clean Technologies and AstroTurf signed an MOU to evaluate Hydrochemolytic Technology (HCT) for recycling polyethylene and polypropylene fractions from end-of-life turf, indicating supplier interest in scalable recycling routes beyond mechanical processing. Also in 2026, the LIFE T4C consortium (including Polytan) presented a microplastic-free synthetic turf solution using Ecolastene infill after an installation at the Carlos III football field in Toledo, Spain, which provides a practical reference point for municipalities and clubs assessing alternatives under tightening microplastics constraints. Evidence remains mixed on environmental and health narratives: California OEHHA published a final study in March 2026 finding no significant human health risk from recycled tire crumb rubber in synthetic turf, while independent research scrutiny on field runoff and aquatic impacts continues to drive attention on stormwater management, containment, and non-crumb-rubber solutions in sensitive watersheds.

Recent Industry Developments

- July 2026: Urban Turf Solutions partnered with Wimbledon champion Pat Cash to launch a signature tennis surface. The collaboration targets a premium sports niche and uses athlete validation to support specification-driven sales for clubs and training venues.

- May 2026: CCGrass completed Canada’s first FIFA Arena pitch in the Township of Langley, British Columbia, using the LEAP non-infill turf system. The project expands reference installations for non-infill formats in North America and matches procurement trends that prioritize reduced infill migration and simplified maintenance.

- October 2024: The European Parliament approved an EU crumb-rubber infill ban. The decision accelerated work by suppliers and buyers on alternative infills and non-infill systems, while increasing the urgency of compliance planning across European pitch replacement cycles.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers the value of manufactured artificial turf systems sold for sports, leisure, and landscaping uses, including the turf backing and infill materials, and counting typical supply and installation value where it is part of the sale.

Scope exclusions: We exclude civil site works (such as excavation and drainage construction) and post-installation maintenance services from the market value.

Segmentation Overview

- By Usage

- Sports

- Contact Sports

- Field Hockey

- Tennis

- Other Sports

- Leisure

- Landscape

- Sports

- Geography

- North America

- United States

- Canada

- Mexico

- Rest of Noth America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with mapping demand signals and rules that affect how and where turf is installed, then aligning those signals to a consistent value definition. We rely on public sources such as US EPA water conservation references, USGS water-use series, Eurostat construction indicators, UN Comtrade trade statistics for relevant polymer and textile inputs, and customs or port datasets where available, since they help sanity-check activity levels by region.

To ground pricing and supply structure, we also review company annual reports, investor decks, trade association publications, and reputable press coverage on sports infrastructure and landscaping projects. In addition, we use select paid subscriptions for company financials and for patent and innovation scans, mainly to confirm product mix changes and broad pricing direction without overfitting the model. These are illustrative sources, and many other public references were also used during data collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary inputs were built from interviews and structured surveys with installers, distributors, raw material-linked stakeholders, facility operators, and procurement teams that buy turf for sports and landscaping. Since adoption and budgets vary by geography, outreach was balanced across APAC, EMEA, and the Americas so assumptions on installation value capture, replacement cycles, and average selling prices could be tightened and rechecked.

Respondent input also clarified what procurement teams typically include in quoted tender totals, especially around backing and infill sourcing versus turf supply only, which affects how we translate project activity into market value.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 14% | APAC: 38% |

| Mid tier: 60% | Functional/Unit leaders: 33% | EMEA: 35% |

| Smaller Players: 15% | Managers: 53% | Americas: 27% |

Market-Sizing & Forecasting

Sizing begins with a top-down build that reconstructs the demand pool from sports field additions and replacements, landscaping conversion activity in water-stressed areas, and regional construction and municipal spend signals, which are then translated into turf area and value. The model is corroborated with selective bottom-up checks, such as sampling installed-area pricing, reviewing distributor throughput patterns, and using supplier-side volume cues to adjust totals where the first pass looks stretched.

Key inputs used (illustrative) include installation density by application (sports vs landscape), field replacement cycles, infill and backing mix shifts, average installed price per square meter, and regional seasonality in project execution. Where data is thin, gaps are handled by applying conservative proxy ratios from similar climates and building types, then revalidating those proxies with installers and buyers before finalizing.

For forecasting, we mainly apply scenario analysis supported by a light multivariate view of drivers like urban sports infrastructure investment, water restriction intensity, and raw material price direction, and then we pressure-test the outputs with what practitioners expect for lead times and tender pipelines.

Data Validation & Update Cycle

Outputs are validated through triangulation across demand indicators, supply-side signals, and pricing checks so the final market value stays consistent with how projects are actually procured and delivered. Variances are flagged when regional growth implied by the model conflicts with trade flows, construction activity, or interview feedback, and those items are reviewed in a multi-step analyst check before sign-off.

The report is refreshed annually, and interim adjustments are made when material events occur, for example, major regulatory actions affecting infill choices or sudden raw material shocks. Before delivery, a fresh review pass is completed so the final numbers reflect the latest available public updates and recent primary confirmations.

Mordor Intelligence's Artificial Turf Market Size Compared With Other Published Estimates

Published market numbers for artificial turf often differ because the counted value chain is not consistent and the line between product value and project value is drawn differently. We see gaps most often when one study counts only turf rolls at factory gate, while another counts installed systems that include backing and infill and sometimes partial labor.

Civil site preparation and drainage construction sit outside Mordor Intelligence's scope, which tends to keep totals closer to the turf system itself even when installation value is included as part of the sale. Differences also come from how replacement demand is modeled for sports fields, whether landscaping demand is tied to water restriction signals, and how currency conversion timing is handled during volatile periods.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.31 B (2026) | |

| Industry Publisher A | USD 3.49 B (2024) | Uses an earlier base year and appears closer to product value only, with less explicit treatment of installed-system value and replacement-cycle driven demand. |

| Market Tracker B | USD 5.80 B (2024) | Includes a broader project spend lens for some applications, which can pull in more of the installation package and raise the total versus a tighter turf-system definition. |

The spread in values lines up with what gets counted and how fast demand is assumed to refresh, especially for sports replacements versus new-build landscaping. By keeping inputs tied to install activity, replacement timing, and observable pricing ranges, the model remains traceable and repeatable even when public data is uneven.

Key Questions Answered in the Report

What is the current value of the artificial turf market?

The artificial turf market is valued at USD 7.31 billion in 2026 and is projected to grow to USD 13.16 billion by 2031 at a 12.46% CAGR.

Which segment is expanding fastest within the artificial turf market?

Landscape applications are advancing at a 14.62% CAGR, outpacing all sports-related segments due to water-conservation mandates and lower lifetime maintenance costs.

Which region holds the largest share of the artificial turf market?

North America leads with 37.74% share in 2025, supported by mature stadium replacement cycles and strict drought legislation.

Why are microplastics a concern for artificial turf?

Studies attribute 16,000 metric tons of annual microplastic emissions in Europe to artificial-turf pitches, prompting regulations that phase out crumb-rubber infill and drive demand for sustainable alternatives.

How are manufacturers addressing end-of-life turf disposal?

Companies such as TenCate Grass and Tarkett are investing in advanced recycling programs that convert used polyethylene fibers into new resin, aligning with circular-economy regulations and buyer sustainability criteria.

What factors influence the total cost of ownership for artificial turf?

Primary factors include initial installation cost, irrigation savings, maintenance labor, field downtime, and eventual recycling or disposal fees, with water-stressed regions achieving the fastest payback periods.

Page last updated on: