Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

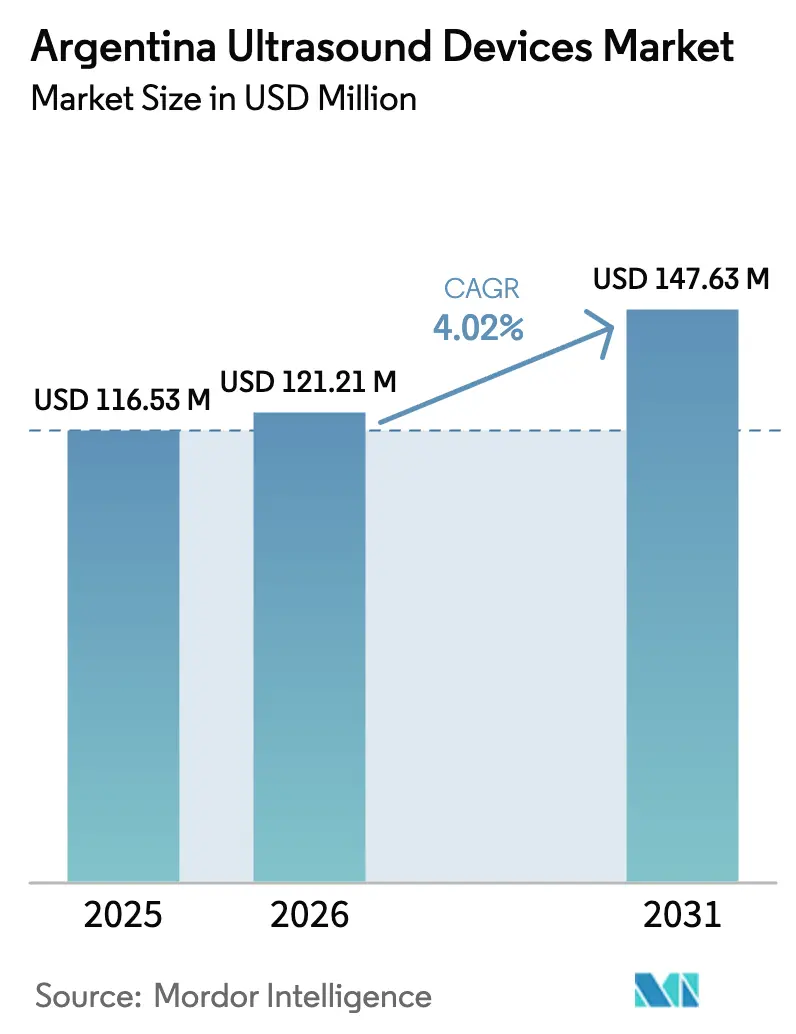

| Base Year Market Size (2025) | USD 116.53 Million |

| Market Size (2026) | USD 121.21 Million |

| Market Size (2031) | USD 147.63 Million |

| Growth Rate (2026 - 2031) | 4.02% CAGR |

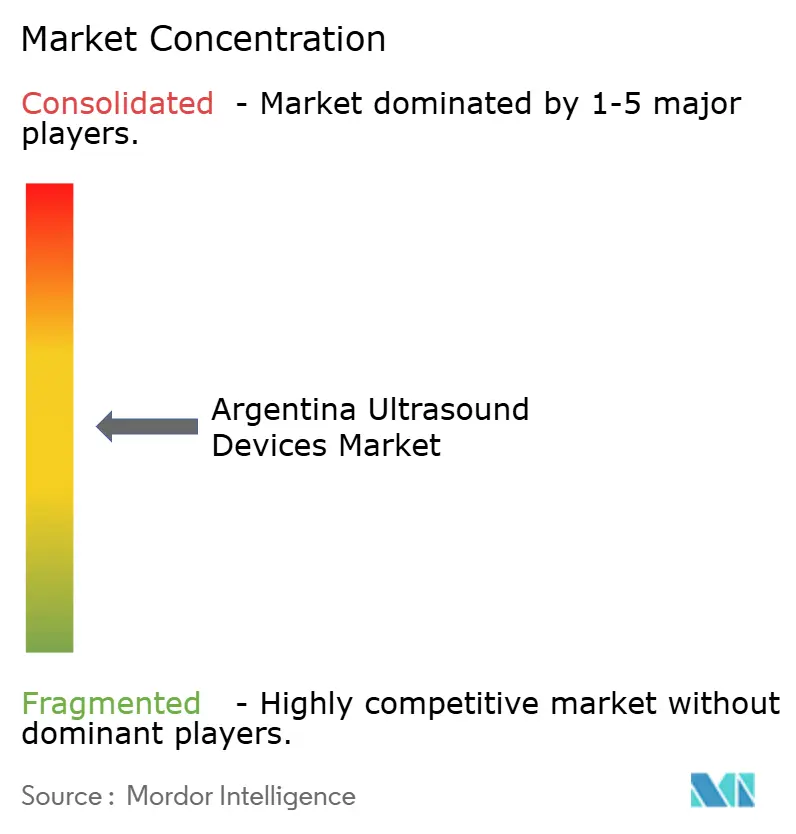

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Ultrasound Devices Market Analysis by Mordor Intelligence

The Argentina Ultrasound Devices Market size is expected to grow from USD 116.53 million in 2025 to USD 121.21 million in 2026 and is forecast to reach USD 147.63 million by 2031 at 4.02% CAGR over 2026-2031.

Rising demand for real-time diagnostics in chronic disease management, the mandatory roll-out of electronic prescriptions from January 2025, and a World Bank–backed USD 535 million health-system modernization package are the foremost growth catalysts. Supply, however, remains import-dependent, exposing stakeholders to currency volatility even as local distributors deepen partnerships with multinational manufacturers. Intensifying competition around AI-enabled workflow automation, handheld form factors, and tele-ultrasound connectivity is reshaping pricing and procurement dynamics across public and private institutions. Long-term demographic aging and the government’s pivot toward value-based care further reinforce medium-term growth visibility.

Key Report Takeaways

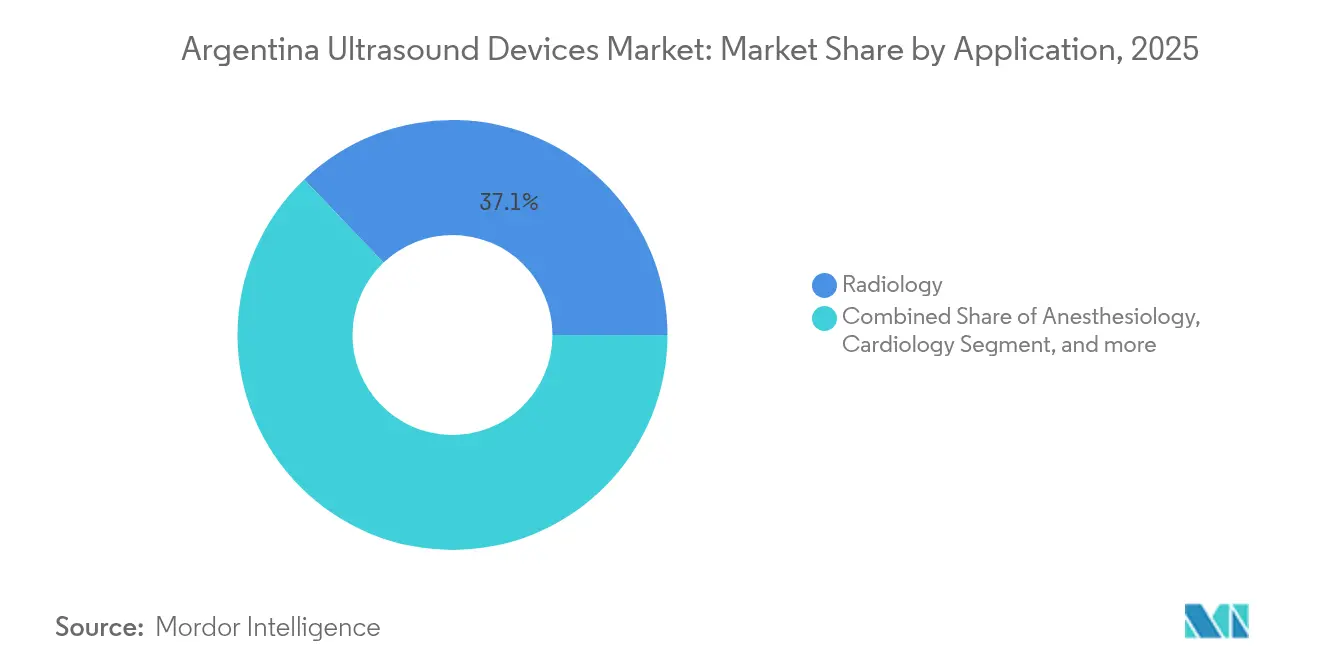

- By application, radiology led with 37.12% revenue share in 2025, while critical care is forecast to expand at a 6.18% CAGR through 2031.

- By technology, 3D & 4D technology captured 37.42% of Argentina ultrasound devices market share in 2025; high-intensity focused ultrasound is projected to grow fastest at 5.71% CAGR.

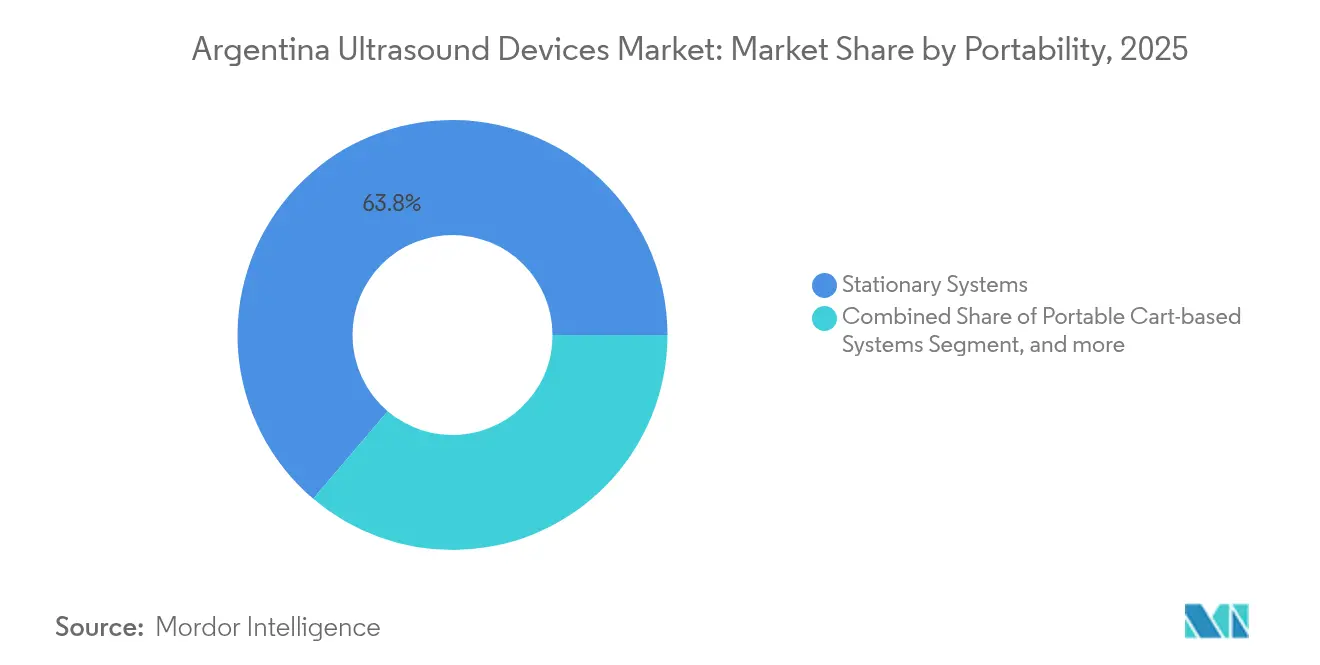

- By portability, stationary systems held 63.78% share of Argentina ultrasound devices market size in 2025, whereas handheld/pocket devices are set to increase at an 7.65% CAGR to 2031.

- By end user, public hospitals accounted for 42.68% usage share in 2025, yet home-health settings are on track for the highest 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Ultrasound Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing chronic disease prevalence | +1.2% | National; urban hubs | Long term (≥ 4 years) |

| Expansion of point-of-care ultrasound (POCUS) | +0.8% | Public hospitals nationwide | Medium term (2-4 years) |

| Maternal-health initiatives | +0.5% | Underserved provinces | Medium term (2-4 years) |

| AI-powered workflow automation | +0.7% | Major metropolitan areas | Short term (≤ 2 years) |

| Tele-ultrasound in remote regions | +0.4% | Rural Patagonia & north | Long term (≥ 4 years) |

| Integration in value-based care | +0.3% | Private sector | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Chronic Disease Prevalence

An aging population and the post-pandemic surge in non-communicable diseases are lifting utilization of cardiac, vascular, and musculoskeletal scanning. Maternal mortality climbed to 7.4 per 10,000 births in 2024, underscoring unmet prenatal imaging needs. AI-assisted ultrasound shortens exam times, supporting over-burdened clinicians tackling higher patient volumes. Argentina’s Universal Child Allowance, covering 4.37 million beneficiaries, reinforces steady pediatric demand for routine sonographic monitoring.[1]“Proyecto de Receta Electrónica,” Argentina.gob.ar, argentina.gob.ar These factors collectively underpin sustained equipment replacement cycles and fresh installations across tertiary hospitals.

Expansion of Point-of-Care Ultrasound (POCUS) in Emergency & Primary Care

Handheld systems deliver bedside diagnostics without dedicated radiology suites. Devices such as Butterfly iQ+, Clarius, and Vscan Air now demonstrate performance approaching cart-based machines, yet cost a fraction and operate from smartphones. Workforce shortages PAHO projects a regional gap of up to 2 million health workers by 2030, making user-friendly POCUS indispensable, especially for general practitioners in provincial clinics.[2]“Health Workforce in the Americas,” Pan American Health Organization, paho.orgArgentina’s 29 medical schools already embed ultrasound proficiency into curricula, ensuring incoming physicians view POCUS as standard practice.

Federal & State-Supported Maternal Health Initiatives

UNDP-funded programs valued at USD 671.3 million for universal health coverage and USD 19.7 million for early-childhood support mandate wider prenatal screening in low-resource districts. AI-driven fetal assessment software can slash measurement time from 2 minutes to 5 seconds per exam, raising throughput and diagnostic confidence. ANMAT’s streamlined 90- to 365-day device registration windows further expedite availability of advanced obstetric systems.

AI-Powered Workflow Automation in Private Imaging Centers

Partnerships such as GE HealthCare-NVIDIA integrate autonomous scanning protocols that reduce repetitive strain on sonographers and unify image quality. Acquisitions like Samsung Medison’s USD 92.4 million purchase of Sonio highlight the premium attached to domain-specific AI algorithms. Financial upsides include fewer rejected claims and improved reimbursement accuracy, factors that resonate with cash-flow-conscious private providers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain disruptions & import dependency | -0.9% | Nationwide | Short term (≤ 2 years) |

| Shortage of skilled sonographers | -0.6% | Rural provinces | Medium term (2-4 years) |

| Fragmented healthcare funding | -0.4% | Provincial variability | Long term (≥ 4 years) |

| Infrastructure gaps in remote areas | -0.3% | Patagonia & north | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Chain Disruptions & Import Dependency

Roughly 80% of ultrasound units are imported, leaving buyers exposed to currency swings and freight delays. Global component shortages that began in 2022 continue to impact probe availability, while 224% domestic inflation in 2024 squeezed hospital budgets.[3]“Argentina Country Report 2024,” International Comparative Legal Guides, iclg.com Strategic sourcing alliances and local warehousing are becoming essential risk-mitigation tactics.

Shortage of Skilled Sonographers

Residency bottlenecks mean fewer than half of new medical graduates secure advanced imaging training slots, constraining throughput in provincial hospitals. AI-assisted acquisition and automated measurements partly offset the human gap but cannot fully replace specialized expertise, limiting volume growth in high-acuity settings.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Critical Care Drives Innovation

Radiology retained leadership with 37.12% of Argentina ultrasound devices market share in 2025, underpinned by entrenched imaging workflows in large urban hospitals. Critical care, however, posts the highest 6.18% CAGR as emergency physicians adopt bedside scanning to manage hemodynamic instability and guide interventions. The Argentina ultrasound devices market size attributed to critical-care deployments is forecast to gain further momentum as AI algorithms quantify lung and cardiac metrics within seconds, expediting triage decisions. Secondary growth pockets include cardiology, gynecology/obstetrics, and musculoskeletal imaging, each benefiting from specialized software packages that automate complex measurements and reduce inter-observer variability.

In gynecology/obstetrics, government-funded prenatal programs spur installations of 3D-enabled systems across provincial maternity centers, while private clinics race to offer AI-augmented fetal anomaly scans. Cardiology leverages Siemens’ Acuson Origin, whose deep-learning engine captures over 5,000 echocardiographic data points per exam, minimizing manual input errors. Musculoskeletal and vascular sub-segments gain traction through elastography and Doppler enhancements that raise diagnostic yield without radiation exposure.

By Technology: AI Integration Accelerates Innovation

3D & 4D modalities commanded 37.42% share in 2025, reflecting local appetite for volumetric imaging in obstetrics and interventional planning. High-intensity focused ultrasound is projected to outpace other technologies at 5.71% CAGR, buoyed by non-invasive oncology and pain-management procedures. The Argentina ultrasound devices market size derived from HIFU remains small but illustrates a pivot toward therapeutic applications that compress hospital stays.

Across all platforms, embedded AI now automates segmentation, quantification, and reporting. Canon’s Smart Fusion overlays CT/MRI datasets onto live ultrasound, facilitating lesion targeting without contrast agents. 2D ultrasound endures as a budget-friendly workhorse for primary care, and Doppler remains indispensable in cardiology and nephrology. Emerging elastography systems provide quantitative tissue stiffness data, aiding early fibrosis detection.

By Portability: Handheld Revolution Transforms Access

Stationary consoles still dominate with 63.78% share, prized for premium transducers and advanced processing that complex cases demand. Yet handheld units are the fastest risers at an 7.65% CAGR, democratizing imaging in ambulances, field clinics, and home settings. The Argentina ultrasound devices market size attributable to handhelds expands as devices like Butterfly iQ3 integrate 3D visualization and AI-guided workflows. Port-based systems serve middle-ground needs in operating theaters and outpatient suites, balancing mobility with performance.

Comparative assessments show no single handheld outperforms rivals in every application; instead, vendors optimize for cardiac, superficial, or abdominal use cases. Real-time AI coaching mitigates operator variability, a critical factor in rural deployments where formal sonography training is scarce.

By End User: Public Sector Leadership Faces Private Innovation

Public hospitals captured 42.68% of Argentina ultrasound devices market share in 2025, supported by universal-coverage mandates and multilateral financing that shield procurement budgets during economic turbulence. Diagnostic centers and private hospitals increasingly adopt AI-rich premium systems to shorten patient backlogs and secure higher reimbursements. The Argentina ultrasound devices market size flowing into home-health environments grows fastest at 7.12% CAGR, propelled by tele-ultrasound platforms that connect nurses and general practitioners with remote specialists in real time.

Fragmentation across public, social-insurance, and private payors complicates procurement cycles, often prolonging tender approvals but also creating niche opportunities for vendors able to navigate multi-stakeholder negotiations. Ambulatory surgical centers constitute an emerging channel where portable scanners facilitate minimally invasive procedures, aligning with cost-containment policies.

Geography Analysis

Argentina’s ultrasound adoption skews heavily toward Buenos Aires and the Central region, where 40% of the population resides and ICU bed density peaks at 2,567 units. These hubs concentrate high-end platform sales and specialist expertise. Provincial disparities remain stark; remote northern and Patagonian provinces face infrastructure gaps that slow diffusion of advanced imaging. Government e-prescription mandates and health-information-exchange projects are expected to unify data flows, thereby lowering integration hurdles for field-deployed devices.

Targeted UNDP and World Bank investments exceeding USD 700 million, focusing on maternal and universal coverage programs and channeling funds into ultrasound procurement for provincial hospitals. MERCOSUR regulatory harmonization eases cross-border supply logistics, yet currency devaluation and inflation continue to disrupt planning cycles. Innovations in tele-ultrasound, riding on 87.2% internet penetration, help bridge geographic gaps by enabling metropolitan radiologists to supervise scans performed in community clinics.

Provincial health-equity mapping using census and geospatial analytics identifies high-vulnerability districts, guiding deployment of handheld units where static imaging suites are unviable. Wealthier provinces such as Córdoba adopt premium AI consoles, while northern areas prioritize rugged, battery-operated systems. These divergent needs reinforce the importance of a tiered product portfolio for vendors seeking national coverage.

Competitive Landscape

The market exhibits moderate concentration: global majors GE HealthCare, Siemens Healthineers, and Philips collectively exceed 60% share, while agile disruptors target white-space niches. Acquisitions Samsung Medison’s USD 92.4 million purchase of Sonio and GE HealthCare’s USD 51 million buyout of Intelligent Ultrasound underline a strategic race for AI competencies. Partnerships with cloud leaders (e.g., GE with AWS) accelerate the development of generative-AI reporting tools that promise faster clinical turnaround.

Butterfly Network’s USD 76 million capital raise funds next-gen chip-based probes intended to lower entry price points and expand handheld penetration. Canon and Olympus co-develop endoscopic ultrasound to tap interventional and gastroenterology demand. Local distributors strengthen after-sales networks to offset import lead times, while some are exploring joint-assembly models to hedge currency risk.

Competitive differentiation increasingly hinges on workflow metrics, scan duration, automated reporting, and reimbursement success rather than solely on image resolution. Vendors demonstrating measurable productivity gains secure premium placements in budget-constrained private hospitals. Rural market access, conversely, rewards cost-effectiveness, portability, and tele-guidance features.

Argentina Ultrasound Devices Industry Leaders

GE Healthcare

Mindray Medical International Limited

Koninklijke Philips N.V.

Canon Medical Systems

Siemens Healthineers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: GE HealthCare and NVIDIA announced a strategic collaboration to develop autonomous X-ray and ultrasound technologies, utilizing NVIDIA's Isaac for Healthcare platform to train and test autonomous devices in virtual environments. This partnership aims to reduce workload on technicians and radiologists while improving imaging standardization and efficiency.

- February 2025: Butterfly Network announced plans to raise USD 76 million through a public stock offering, with funds supporting new product development and general corporate purposes. The company reported 50% growth in annual recurring revenue and 35% year-over-year revenue increase in Q4 2024.

Argentina Ultrasound Devices Market Report Scope

As per the report's scope, a diagnostic ultrasound, also known as sonography, is an imaging technique that uses high-frequency sound waves to produce images of the different structures inside the body. They assess various kidney, liver, and other abdominal conditions. They are also majorly used in chronic diseases, including heart disease, asthma, cancer, and diabetes. Therefore, these devices are being utilized as diagnostic imaging and therapeutic modalities and have a wide range of applications in the medical field. The ultrasound devices market is Segmented by application (anesthesiology, cardiology, gynecology/obstetrics, musculoskeletal, radiology, critical care, and other applications), technology (2D ultrasound imaging, 3D and 4D ultrasound imaging, Doppler imaging, and high-intensity focused ultrasound) type (stationary ultrasound and portable ultrasound). The report offers the value (in USD) for the above segments.

By Application

| Anesthesiology |

| Cardiology |

| Gynecology / Obstetrics |

| Musculoskeletal |

| Radiology |

| Critical Care |

| Urology |

| Vascular |

| Other Applications |

By Technology

| 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging |

| Doppler Imaging |

| High-Intensity Focused Ultrasound |

| Other Technologies |

By Portability

| Stationary Systems |

| Portable Cart-based Systems |

| Hand-held / Pocket Devices |

By End User

| Public Hospitals |

| Private Hospitals & Clinics |

| Diagnostic Imaging Centers |

| Ambulatory Surgical Centers |

| By Application | Anesthesiology |

| Cardiology | |

| Gynecology / Obstetrics | |

| Musculoskeletal | |

| Radiology | |

| Critical Care | |

| Urology | |

| Vascular | |

| Other Applications | |

| By Technology | 2D Ultrasound Imaging |

| 3D & 4D Ultrasound Imaging | |

| Doppler Imaging | |

| High-Intensity Focused Ultrasound | |

| Other Technologies | |

| By Portability | Stationary Systems |

| Portable Cart-based Systems | |

| Hand-held / Pocket Devices | |

| By End User | Public Hospitals |

| Private Hospitals & Clinics | |

| Diagnostic Imaging Centers | |

| Ambulatory Surgical Centers |

Key Questions Answered in the Report

How large is the Argentina ultrasound devices market in 2026?

It is valued at USD 121.21 million in 2026 and is forecast to reach USD 147.63 million by 2031 at a CAGR of 4.02% over 2026-2031.

Which application is growing fastest?

Critical-care ultrasound shows the highest 6.18% CAGR due to greater bedside adoption in ICUs and emergency departments.

What technology segment leads current revenue?

3D & 4D systems hold 37.42% share, reflecting demand for volumetric imaging in obstetrics and surgical planning.

Why are handheld devices important?

Handheld probes are forecast to grow at 7.65% CAGR because they expand access in ambulances, rural clinics, and home-health settings.

How dependent is Argentina on imports for ultrasound equipment?

Imports supply about 80% of domestic demand, exposing buyers to exchange-rate risk and global supply disruptions.

Which provinces are priority targets for tele-ultrasound roll-outs?

Remote northern and Patagonian regions with limited specialist access are top priorities for tele-enabled scanning programs.

Page last updated on: