Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

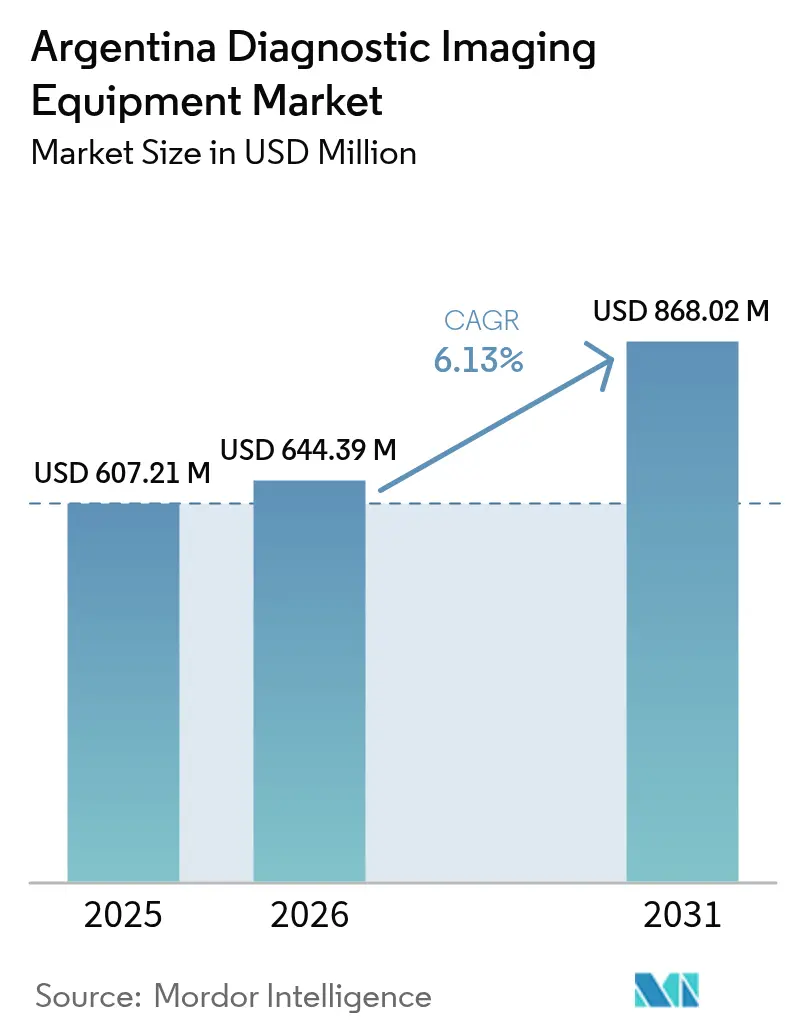

| Base Year Market Size (2025) | USD 607.21 Million |

| Market Size (2026) | USD 644.39 Million |

| Market Size (2031) | USD 868.02 Million |

| Growth Rate (2026 - 2031) | 6.13% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

Argentina diagnostic imaging equipment market size in 2026 is estimated at USD 644.39 million, growing from 2025 value of USD 607.21 million with 2031 projections showing USD 868.02 million, growing at 6.13% CAGR over 2026-2031. Growth is driven by private providers upgrading technology to retain urban middle-class patients, the proliferation of AI-enabled modalities that streamline physician workflow, and a nationwide push to diagnose chronic diseases earlier. Import dependence remains high, prompting manufacturers to expand local service networks while policymakers retain a streamlined four-tier device registration pathway that accelerates market entry. Fixed installations in large hospitals still dominate, yet portable systems gain traction as provincial health plans fund mobile outreach programs. Competition is intensifying as global vendors bundle AI software, cloud connectivity, and maintenance into integrated offerings that appeal to Argentina’s price-sensitive buyers.

Key Report Takeaways

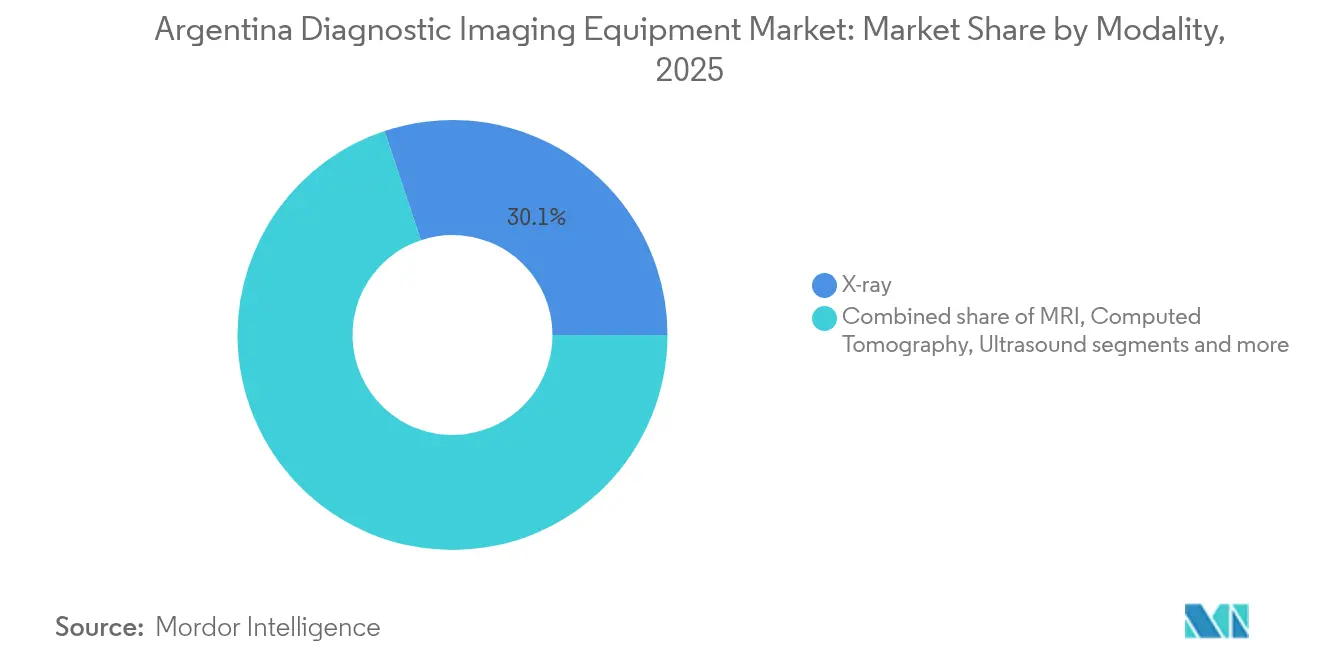

- By modality, X-ray systems held 30.12% of Argentina diagnostic imaging equipment market share in 2025, whereas MRI is projected to post the fastest 7.72% CAGR to 2031.

- By portability, fixed systems represented 79.45% of revenue in 2025; mobile and hand-held systems are expanding at a 6.85% CAGR.

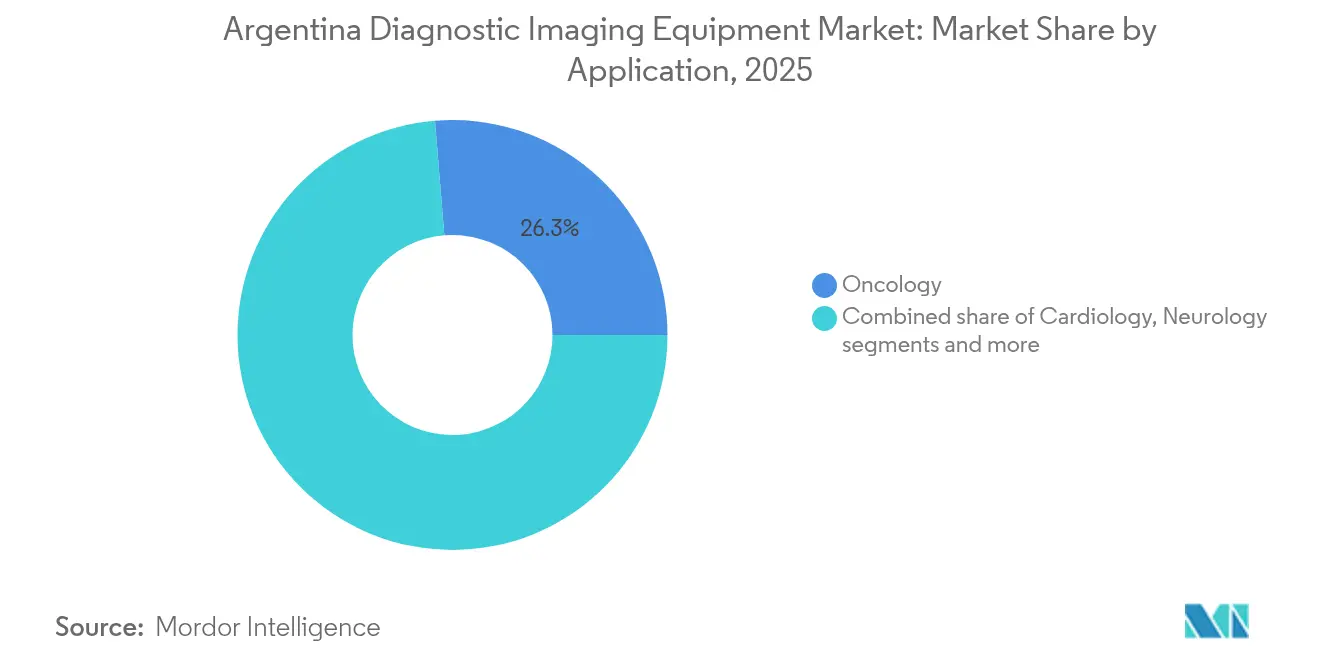

- By application, oncology contributed 26.30% revenue in 2025, while cardiology leads future growth at 7.98% CAGR.

- By end user, hospitals captured 63.15% of Argentina diagnostic imaging equipment market size in 2025; dedicated imaging centers are advancing at a 7.5% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of chronic diseases | +1.2% | National, concentrated in Buenos Aires, Córdoba, Rosario | Medium term (2-4 years) |

| Technological advancements in imaging systems | +1.8% | National, with early adoption in private facilities | Short term (≤ 2 years) |

| Growing geriatric population in Argentina | +0.9% | National, higher impact in urban centers | Long term (≥ 4 years) |

| Expansion of private health-insurance networks | +1.4% | National, strongest in metropolitan areas | Medium term (2-4 years) |

| Rapid uptake of AI-enabled teleradiology services | +0.7% | National, remote areas benefit most | Short term (≤ 2 years) |

| Government initiatives for early diagnosis | +0.3% | National, prioritizing underserved regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Chronic Diseases

Chronic cardiovascular and oncologic conditions now account for the heaviest diagnostic workload in Argentina’s hospitals, propelling procurement of high-resolution CT, MRI, and multimodal X-ray systems. Portable units equipped with AI triage software reached 97% sensitivity for COVID-related lung findings, proving their broader utility in busy emergency rooms. Provincial authorities respond by channeling Sumar Program funds toward imaging upgrades that support early detection campaigns. Combined, these factors sustain long-run equipment demand across urban and rural markets.

Technological Advancements in Imaging Systems

Vendors now tailor AI-driven workflow solutions for emerging economies, reducing contrast use, power, and helium dependency while automating repetitive tasks. A Bariloche research group achieved 89% accuracy in gadolinium-free cardiac fibrosis detection through AI post-processing of routine cine MRI scans. Siemens’ self-driving Ciartic Move C-arm trims surgical imaging time by 50%, a benefit in facilities grappling with personnel shortages. Such innovations shorten learning curves and widen adoption beyond Argentina’s largest centers.

Growing Geriatric Population in Argentina

Older adults seek more musculoskeletal, neurological, and cardiac imaging, pushing high-field MRI usage and spurring interest in proton-based oncology solutions commissioned in Buenos Aires.[1]Source: World Nuclear News, “Cyclotron Lifted into Place at Argentina’s Proton Therapy Centre,” world-nuclear-news.org Portable scanners support outreach to residential facilities, complementing home-care programs that mitigate hospital overcrowding. These demographic shifts ensure durable growth in both premium and point-of-care segments over the forecast horizon.

Expansion of Private Health-Insurance Networks

Price-control removal allows insurers such as OSDE and Swiss Medical to index premiums and earmark capital for state-of-the-art diagnostics that entice affluent members. As private centers proliferate, equipment vendors bundle financing, maintenance, and AI subscriptions to overcome high upfront costs. Yet persistent inflation risks could limit middle-class uptake, leaving premium imaging demand concentrated in major cities.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High acquisition & procedure costs | -1.5% | National, most severe in rural provinces | Medium term (2-4 years) |

| Fragmented reimbursement for outpatient imaging | -0.8% | National, varies by insurance provider | Short term (≤ 2 years) |

| Shortage of sub-specialty radiologists | -0.6% | National, critical in remote areas | Long term (≥ 4 years) |

| Stringent regulatory framework | -0.4% | National, affects all market participants | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition & Procedure Costs

Upfront scanner prices rise roughly 50% once import duties and logistics are added, forcing smaller hospitals to delay upgrades. The government’s BOPREAL (Bonds for the Reconstruction of a Free Argentina) bond offers currency-hedged payment relief, yet maintenance contracts, helium supply, and staff training remain costly.[2]Source: U.S. Department of Commerce, “Argentina Import Regulations and Payments,” International Trade Administration, trade.gov Vendors counter with refurbished models and pay-per-scan financing, although rural facilities still struggle to justify MRI or PET investments given patient throughput constraints.

Fragmented Reimbursement for Outpatient Imaging

Three overlapping payor systems dictate multiple prior-authorization rules that frequently exclude advanced modalities, shifting costs onto patients and discouraging diagnostic centers from installing newer platforms. The Compulsory Medical Plan covers basic X-ray but rarely reimburses AI-assisted CT. Until uniform payment codes emerge, equipment demand risks periodic slowdowns, particularly outside Buenos Aires where disposable income is lower.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: MRI Acceleration Challenges X-ray Leadership

Argentina diagnostic imaging equipment market share for X-ray stood at 30.12% in 2025. Ubiquity, swift scan times, and cost efficiency keep X-ray entrenched in emergency, orthopedic, and pulmonary pathways. However, MRI revenue is growing 7.72% annually, propelled by helium-free magnets. Hospitals adopt AI-accelerated reconstruction that halves scan time and expands daily volume. As reimbursement policies evolve, multi-contrast MRI’s superior soft-tissue characterization positions it for broader oncologic and neurologic use.

Adoption barriers persist, including room-shielding, radiologist availability, and power stability. Yet new cloud-based protocols allow remote protocoling and over-read, mitigating skills gaps. Ultrasound, mammography, and nuclear modalities carve specialized niches, but MRI’s innovation pace suggests its share of Argentina diagnostic imaging equipment market will widen through 2031.

By Portability: Mobile Systems Extend Reach

Fixed systems retain 79.45% market share thanks to embedded CT, angiography, and fluoroscopy suites within tertiary hospitals. High throughput and advanced service contracts justify their dominance. Nonetheless, mobile and hand-held devices are gaining a 6.85% CAGR as provincial health ministries deploy truck-mounted CT and battery-powered ultrasound to remote clinics.

Portable X-ray units with AI triage proved indispensable during the pandemic and now support tuberculosis, trauma, and neonatal screening programs. Cellular data integration permits cloud archiving for centralized reporting, expanding diagnostic capacity despite radiologist shortages.

By Application: Cardiology Gains Momentum

Oncology imaging generated USD 159.68 million in 2025, 26.30% of Argentina diagnostic imaging equipment market. It remains indispensable for staging lung, breast, and colorectal cancers. Yet cardiology is accelerating at 7.98% CAGR as AI algorithms quantify ventricular volume and detect fibrosis without contrast. Rising hypertension and obesity levels, alongside Medicare-style plan expansions, ensure sustained cardiac imaging volumes. Vendors integrate ultrasound, CT, and MRI data into single dashboards that guide interventional decisions, shortening hospital stays and boosting demand for multimodal suites.

Women’s health systems embed tomosynthesis and contrast-enhanced mammography to meet screening mandates, while neurologic and musculoskeletal applications leverage portable ultrasound for sports and stroke triage. Clinical breadth supports the continued diversification of Argentina diagnostic imaging equipment market.

By End User: Imaging Centers Narrow the Gap

Hospitals accounted for 63.15% of revenue in 2025, capitalizing on bundled capital budgets and in-house bio-engineering teams. Their volume throughput supports premium CT and hybrid PET-CT. Diagnostic centers, however, are growing faster at 7.5% CAGR as insurers authorize outpatient scans to reduce inpatient congestion. Lean staffing models, extended hours, and same-day reporting resonate with urban professionals.

Financing partners enable centers to refresh equipment every five years, accelerating technology cycles and pushing hospitals to modernize. Specialty clinics focusing on cardiology, orthopedics, or women’s health adopt compact scanners that align with procedure-based reimbursement, adding resilience to overall market expansion.

Geography Analysis

Buenos Aires metropolitan area houses high-end scanners, supported by Argentina’s densest private insurance base and research hospitals that attract vendor pilot projects. Córdoba and Rosario follow, leveraging university hospitals and growing expatriate communities. In contrast, northern provinces rely on refurbished X-ray and portable ultrasound, yet government programs earmark funds to narrow diagnostic gaps. Patagonia’s sparse population necessitates mobile CT caravans, and Bariloche’s AI cardiac imaging research underscores how regional centers can pioneer innovation even with modest budgets.

Provinces such as Salta, Tucumán, and Jujuy benefit from the Sumar Program, which subsidizes imaging for 20 million low-income residents. These initiatives stimulate modest but steady equipment purchases, particularly for digital radiography and point-of-care ultrasound.

Coastal hubs including Mar del Plata experience seasonal peaks linked to tourism, influencing scanner utilization and replacement cycles. Across geographies, manufacturers that bundle warranty, remote diagnostics, and local parts inventory command loyalty in the Argentina diagnostic imaging equipment market.

Competitive Landscape

Global majors GE HealthCare, Siemens Healthineers, and Philips collectively command significant revenue through broad modality portfolios, deep AI pipelines, and extensive service networks. Mid-tier contenders—Canon, Fujifilm, United Imaging, Samsung—target value-priced CT, digital radiography, and ultrasound niches, frequently partnering with distributors such as Digimed for nationwide coverage.

Local service capabilities and spare parts stocking remain key differentiators within the Argentina diagnostic imaging equipment market. White-space opportunities persist in tele-radiology platforms, AI decision support, and pay-per-scan leasing models that address persistent capital constraints.

Regulatory familiarity also shapes competition. Firms that streamline ANMAT submissions through the SEDI portal and provide Spanish-language documentation shorten time-to-market. Increasingly, manufacturers bundle cybersecurity features to satisfy new data-protection guidelines, a criterion that Argentine hospitals prioritize when selecting vendors.

Argentina Diagnostic Imaging Equipment Industry Leaders

Canon Medical Systems Corporation

Fujifilm Holdings Corporation

GE HealthCare

Koninklijke Philips N.V.

Siemens Healthineers AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2024: An Argentine critical-care study showed transcranial sonography’s growing adoption for rapid intracranial assessment at the bedside.

- April 2023: The Inter-American Development Bank greenlit a USD 200 million loan, marking the first tranche of a planned USD 600 million credit line. This funding aims to enhance access to diagnostic imaging and treatment services, prioritizing support for those dependent on public healthcare.

- April 2023: In São Paulo, Brazil, and Buenos Aires, Argentina, doctors upgraded their PET/CT scanners, allowing them to meet rising patient demands, ease scheduling challenges, and even venture into new care areas.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines Argentina's diagnostic imaging equipment market as all newly manufactured X-ray, MRI, CT, ultrasound, nuclear, and mammography systems installed in hospitals, stand-alone imaging centers, and specialty clinics nationwide. Value is reported in FOB USD, net of service contracts and disposable radiopharmaceuticals.

(Scope exclusion: refurbished devices and AI-only software platforms are kept outside this valuation.)

Segmentation Overview

- By Modality

- MRI

- Computed Tomography

- Ultrasound

- X-ray

- Nuclear Imaging

- Fluoroscopy

- Mammography

- By Portability

- Fixed Systems

- Mobile and Hand-held Systems

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics and Trauma

- Women’s Health

- Other Clinical Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Specialty Clinics and Others

Detailed Research Methodology and Data Validation

Primary Research

We conducted semi-structured interviews with radiologists, biomedical engineers, procurement officers, and Latin-based distributors covering Greater Buenos Aires, Cordoba, Rosario, and Mendoza. Conversations confirmed typical scanner utilization hours, warranty pricing, and the share of mobile ultrasound units now placed in primary-care chains, allowing us to adjust desk-derived assumptions and cross-check growth drivers highlighted by suppliers.

Desk Research

Analysts first reviewed public datasets, such as INDEC import statistics, ANMAT device registries, the Ministry of Health equipment census, and WHO Global Health Observatory, to size annual unit inflows. These were matched with modality-level replacement cycles discussed in peer-reviewed journals like Revista Argentina de Radiologia. Company 10-Ks and local investor presentations clarified average selling prices, while customs shipment records from Volza and news archives in Dow Jones Factiva helped validate quarterly volume spikes. Additional insights came from trade bodies, for example, the Argentine Society of Radiology. The sources listed illustrate, not exhaust, the collections consulted.

Market-Sizing & Forecasting

A top-down production and trade reconstruction, anchored on import data and minor domestic output, established the 2024 base. Results were corroborated through selective bottom-up roll-ups of the five largest distributors' shipments and sampled ASP × volume checks. Key variables in the model include installed base retirement rate, public tender budgets, private insurance enrollment, oncology incidence, and peso-dollar conversion trends. Multivariate regression links these drivers to modality demand before scenario analysis projects 2025-2030 outcomes. Gaps in bottom-up detail are bridged using price corridors agreed with interviewed channel partners.

Data Validation & Update Cycle

Outputs pass variance thresholds versus historical procurement, currency-adjusted ASP shifts, and regional peer markets. Outliers trigger re-contact with sources, followed by an analyst and team-lead review. The file is refreshed every twelve months, with mid-cycle amendments when policy or macro shocks alter equipment purchasing.

Why Mordor's Argentina Diagnostic Imaging Equipment Baseline Is Dependable

Published numbers differ because firms choose distinct scopes, pricing anchors, and refresh cadences.

Key gap drivers here are whether refurbished units are counted, how modality mix weights are applied, and the timeliness of ASP assumptions during peso volatility.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| US$ 607.21 M (2025) | Mordor Intelligence | - |

| US$ 298.7 M (2024) | Regional Consultancy A | Omits nuclear and handheld ultrasound; relies on 2019 physician-density ratios |

| US$ 474.8 M (2024) | Global Consultancy B | Uses constant 2019 ASP and partial refurbished import capture |

| US$ 250 M (2023) | Trade Journal C | Tracks only public-hospital tenders; excludes private clinic purchases |

The comparison shows estimates swing widely when scope or pricing discipline loosens. By combining transparent import data, modality-specific lifecycles, and live price checks, Mordor Intelligence delivers a balanced baseline that decision-makers can trace back to clear, repeatable steps.

Key Questions Answered in the Report

Which imaging modality sees the widest everyday use across Argentine hospitals?

Digital X-ray remains the workhorse because it is affordable, quick to operate, and versatile for emergency, orthopedic, and chest exams.

How is artificial intelligence changing diagnostic imaging practice in Argentina?

Hospitals and imaging centers are adopting AI algorithms that automate scan positioning, accelerate image reconstruction, and flag suspicious findings, helping radiologists cope with heavy workloads.

Why are portable scanners gaining traction outside Buenos Aires?

Mobile X-ray and ultrasound units allow clinicians to reach rural clinics and bedside patients, addressing the shortage of full-service imaging suites in provincial areas.

In what way does the growth of private health insurance shape equipment purchases?

Insurers compete on premium service levels, prompting private facilities to buy advanced MRI, CT, and AI-ready systems that shorten wait times and attract higher-income members.

What is the key regulatory pathway for bringing new imaging equipment into the country?

Manufacturers register devices through ANMAT’s SEDI portal, submitting technical dossiers and quality certificates that place products into one of four risk classes before approval.

Where do international suppliers find the greatest commercial openings?

Opportunities lie in offering integrated service contracts and financing that ease high import costs, coupled with training programs that build local expertise on advanced platforms.

Page last updated on: