Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

| Market Size (2026) | USD 3.52 Billion |

| Market Size (2031) | USD 4.27 Billion |

| Growth Rate (2026 - 2031) | 3.93% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Argentina Oil And Gas Upstream Market Analysis by Mordor Intelligence

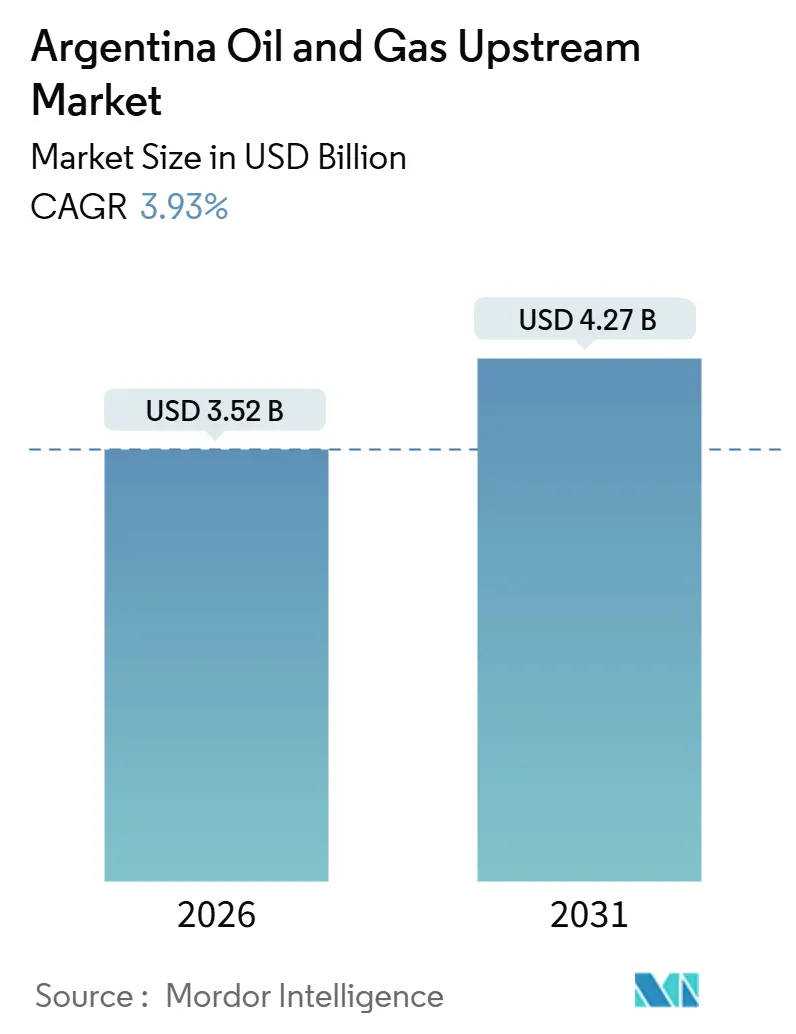

The Argentina Oil And Gas Upstream Market size is estimated at USD 3.52 billion in 2026, and is expected to reach USD 4.27 billion by 2031, at a CAGR of 3.93% during the forecast period (2026-2031).

This trajectory is anchored in the rapid build-out of the Vaca Muerta Sur crude line, the doubling of the Néstor Kirchner gas corridor, and the 30-year fiscal protection granted under the RIGI framework, all of which lower sovereign-risk premiums and shorten payback cycles. Operators are prioritizing export optionality over price speculation, channeling capital toward pad drilling that synchronizes oil and gas completions so that each wellhead can feed both domestic and international markets. Service companies are rolling out digital frac fleets that keep lifting costs below USD 5/boe and allow cycle times that rival U.S. shale analogs, reinforcing the competitiveness of the Argentina oil and gas upstream market. Foreign majors remain willing to share risk with state-owned YPF, but they monitor midstream congestion, water-sourcing litigation, and currency volatility as the decisive variables that can moderate the forecast.

Key Report Takeaways

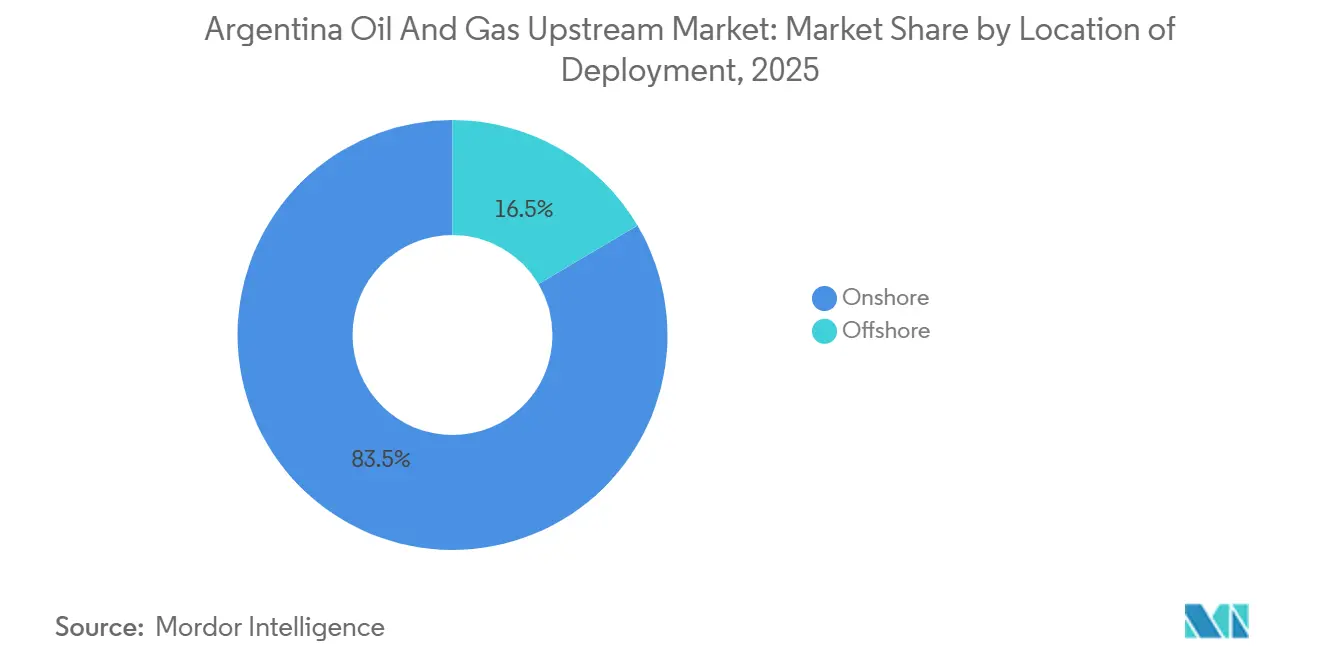

- By location of deployment, onshore acreage held 83.5% of the Argentine oil and gas upstream market share in 2025, while offshore projects are set to record the fastest 5.4% CAGR through 2031.

- By resource type, crude oil led with a 60.4% revenue share in 2025; natural gas is forecast to expand at a 4.9% CAGR, reflecting LNG export momentum.

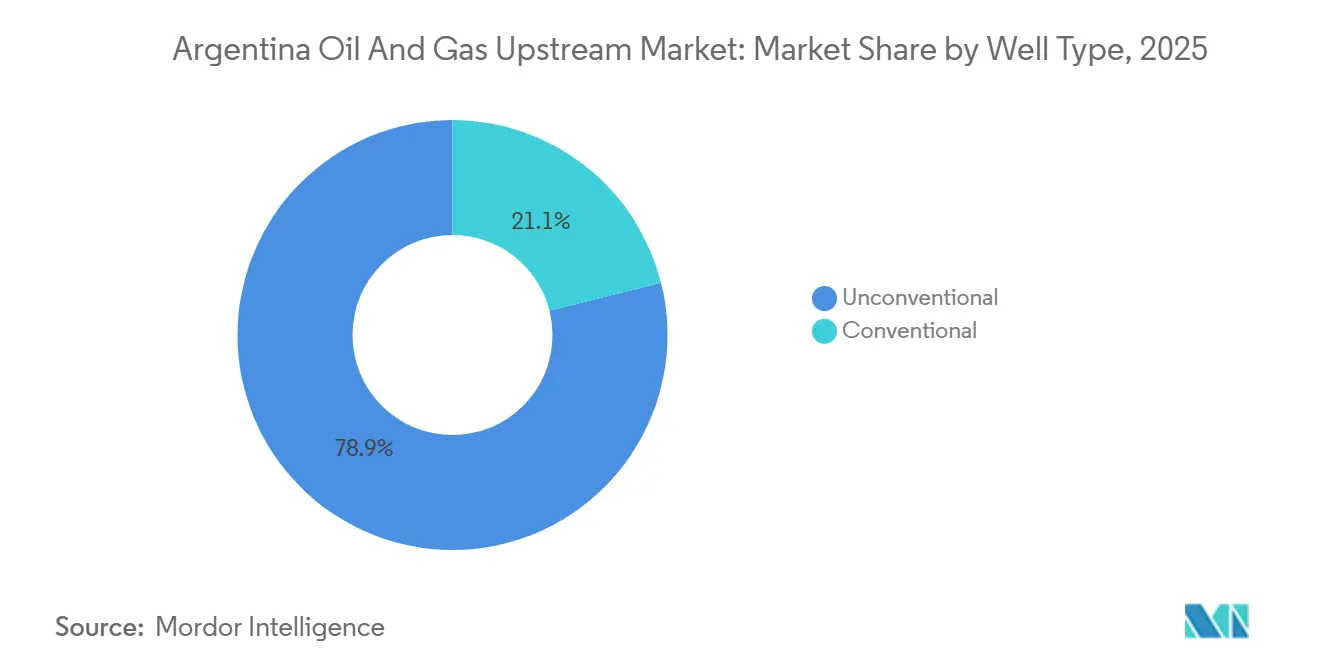

- By well type, unconventional completions accounted for 78.9% of 2025 activity and are expected to advance at a 4.5% CAGR thanks to pad drilling and zipper-frac efficiencies.

- By service, development and production captured 80.1% of spending in 2025, while decommissioning services will rise at a 6.8% CAGR as conventional fields approach end-of-life.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Argentina Oil And Gas Upstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating capacity of Vaca Muerta Sur & Norte pipelines | +0.9% | Neuquén Basin, with export terminals in Buenos Aires Province | Medium term (2-4 years) |

| RIGI tax-&-FX regime attracting > USD 30 billion FDI commitments | +1.2% | National, with concentration in Neuquén, Mendoza, and offshore blocks | Long term (≥ 4 years) |

| Néstor Kirchner gas-pipe Phase II enabling LNG feedstock surplus | +0.6% | Neuquén to Buenos Aires corridor, spillover to LNG terminals | Short term (≤ 2 years) |

| Digital frac-fleet rollout cutting shale OPEX < USD 5/boe | +0.4% | Vaca Muerta core area (Loma Campana, Bandurria Sur) | Medium term (2-4 years) |

| Progressive liberalization of crude export permits | +0.3% | National, with early gains in Patagonia and Neuquén | Short term (≤ 2 years) |

| Ultra-deep offshore Malvinas basin 3-D modelling revealing new kitchens | +0.2% | Argentine offshore continental shelf (CAN basins) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating capacity of Vaca Muerta Sur & Norte pipelines

The 437-kilometer Vaca Muerta Sur trunk line came onstream in 2024, adding as much as 700,000 b/d of takeaway capacity that eliminates costly trucking and secures Brent-linked netbacks for Neuquén barrels. Complementary expansion of the Norte gas system lets operators co-develop liquids-rich and dry-gas zones from the same pads, spreading surface infrastructure costs across multiple streams and improving capital efficiency. Modular pump-station design allows throughput to rise in 75,000 b/d increments without a full shutdown, reducing the lag between drilling success and first cash. Lower evacuation risk compresses discount rates applied by financial institutions, making project economics more robust in stress tests at USD 50/bbl. Together, the oil and gas lines reposition the Argentine oil and gas upstream market as an export-oriented supply source rather than a swing domestic producer.

RIGI tax-&-FX regime attracting above USD 30 billion FDI commitments

Enacted in mid-2024, RIGI locks in 30 years of fiscal terms, accelerated depreciation, and offshore dollar retention for projects above USD 200 million, trimming 400-600 bps from typical hurdle rates. Chevron’s USD 4.3 billion expansion and Shell’s USD 3.2 billion gas monetization plan were the first large approvals under the framework, proving its practical enforceability.[1]Financial Times Correspondent, “Chevron Bets Big on Argentine Shale,” Financial Times, ft.com The arbitration clause that channels disputes to international courts enhances lender confidence, which is critical for LNG sponsors that must align 20-year offtake with debt maturities. RIGI’s threshold naturally skews capital toward integrated majors while leaving conventional independents exposed to peso volatility, accelerating the bifurcation between well-capitalized shale developers and legacy conventional operators. As more projects secure RIGI status, the Argentine oil and gas upstream market accrues an embedded layer of contractual stability that reduces the sensitivity of long-cycle returns to political shocks.

Néstor Kirchner gas corridor Phase II enabling LNG feedstock surplus

Phase II doubled throughput to 22 MMcmd in 2025, flipping a regional deficit into a surplus that underpins Southern Energy’s twin 2.5 Mtpa FLNG vessels scheduled for 2026. Firm transportation allows operators to lock in gas sales agreements without fear of curtailment, thereby justifying new drilling programs in gas-rich northern Vaca Muerta blocks. YPF, Shell, and Eni’s 10 Mtpa LNG project hinges on the same corridor, showing that pipe reliability is more critical than headline gas prices for project bankability. Seasonal balancing also improves: instead of flaring or choking wells in summer, producers can now redirect volumes to export cargos. The corridor, therefore, elevates natural-gas value chains and tilts drilling toward formations previously sidelined by price caps.

Digital frac-fleet rollout cutting shale OPEX below USD 5/boe

Electric fleets equipped with real-time down-hole sensors and automated sand-handling systems cut completion time by up to 30%, slashing diesel use by 50% and driving operating cost below USD 5/boe in tier-one acreage. Algorithm-driven pump-rate adjustments optimize fracture geometry on the fly, boosting initial-30-day production rates by up to 25% against 2023 vintages. The capital-light nature of the upgrade (swapping out pumps and software rather than rigs) lets operators scale quickly without expanding headcount. Early adopters such as YPF and Vista record double-digit improvements in estimated ultimate recovery, widening the performance gap with analog completions. The technology’s success encourages lenders to model higher cash-flow resilience, a factor that improves the credit profile of the Argentine oil and gas upstream market during commodity downturns.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Midstream bottlenecks during winter peak demand | -0.4% | Neuquén Basin to Buenos Aires corridor, localized constraints in Río Negro | Short term (≤ 2 years) |

| Foreign-exchange volatility & capital-control snap-backs | -0.3% | National, affecting all operators with peso-denominated cost bases | Medium term (2-4 years) |

| Water-stress litigation in Neuquén & Río Negro | -0.3% | Neuquén Province and Río Negro Province, concentrated in Vaca Muerta core areas | Medium term (2-4 years) |

| High well-cost inflation vs WTI parity | -0.5% | National, with highest impact in Vaca Muerta unconventional development | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Midstream bottlenecks during winter peak demand

Winter gas demand spikes from June to August frequently exceed combined pipeline and storage capacity, forcing operators to flare or shut-in associated gas despite the recent capacity additions.[2]Reuters Staff, “Winter Gas Crunch Forces Neuquén Shut-Ins,” Reuters, reuters.com Curtailments can trim field-level output by as much as 15% during the critical high-decline months of new wells, permanently lowering cumulative recovery. Residential prioritization rules raise the uncertainty premium for producers, who must supply regulated domestic customers at capped prices before honoring higher-value industrial or export contracts. Temporary compression fleets and on-site storage blunt the impact but add up to USD 1/boe in lifting cost, offsetting part of the savings achieved through digitalization. Unless incremental compression and looped segments are installed, peak-season volatility will remain a headwind to the Argentine oil and gas upstream market.

Foreign-exchange volatility & capital-control snap-backs

Recurring peso devaluations widen the spread between official and parallel rates, inflating local-currency cost bases even while revenues accrue offshore in dollars.[3]Financial Times Correspondent, “Peso Plunge Raises Costs for Oil Producers,” Financial Times, ft.com Service contracts, royalties, and labor remain peso-linked, exposing operators to cost surprises when the government adjusts exchange bands. Capital controls since 2019 have obliged companies to maintain dual treasury structures, locking up working capital at 50% plus peso borrowing costs during turbulence. RIGI shields sanctioned projects from revenue repatriation limits but does not cover exploration ventures, leaving a subset of investments exposed. The resultant financial friction erodes the net-present-value buffer of long-cycle shale and deepwater projects, tempering the overall CAGR outlook of the Argentine oil and gas upstream market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location of Deployment: Offshore Gains Momentum

Offshore prospects represented only 16.5% of the Argentine oil and gas upstream market in 2025, yet they will post a 5.4% CAGR through 2031, the fastest among location segments. The Argentina oil and gas upstream market size tied to ultra-deepwater Malvinas leads has already attracted Equinor and Harbour Energy, whose 2024 seismic reprocessing unveiled Cretaceous kitchens analogous to West Africa. In contrast, onshore Neuquén acreage dominates near-term production but concentrates geological and regulatory risk. Offshore blocks promise larger, less contested reservoirs and no surface land-use conflicts, albeit at higher capital intensity. Equipment imports and long-lead subsea kits necessitate early procurement, which is why spending rises years before first oil flows. The acceleration reflects mobilization and appraisal, not immediate barrel additions, but it nonetheless injects diversification into the Argentine oil and gas upstream market.

Jack-up and drillship demand is altering service-sector procurement, with local yards eyeing joint ventures to fabricate topsides domestically. Exploration plans project 5-to-7-year lead times, so barrels sanctioned in 2026 could start flowing in the early 2030s, smoothing the production plateau that would otherwise depend solely on Vaca Muerta. Tax terms for deepwater fall under federal purview, which offers clearer permitting lines than the provincial split that governs onshore projects. If the first two exploration wells encounter commercial volumes, the Argentina oil and gas upstream market share allocated to offshore could rise sharply, bringing a new cohort of international contractors into Argentina’s supply chain.

By Resource Type: Gas Monetization Reshapes Economics

Natural gas revenues are forecast to grow at a 4.9% CAGR from 2026 to 2031, outstripping oil despite oil’s 60.4% dominance in 2025. The Argentina oil and gas upstream market size attributable to gas hinges on the LNG value chain backed by the Néstor Kirchner corridor and two 2.5 Mtpa FLNG units. Operators are recompleting legacy oil wells to capture gas that was previously flared under domestic price caps, thereby unlocking additional cash flow without drilling new holes. The seasonal gas surplus allows producers to structure annual supply curves that maximize spot LNG sales in the southern winter when Asian demand peaks. Oil production growth remains constrained by export permits and inland transport costs that erode Brent netbacks, limiting its incremental contribution to the Argentine oil and gas upstream market.

Gas-centric drilling is migrating toward the northern Neuquén blocks, which alters contractor patterns and shifts drilling mud and proppant supply chains. Integrated players such as TotalEnergies balance oil and gas volumes to hedge price cycles, a strategy unavailable to single-commodity independents. Should long-term Asian offtake reach financial close by 2028, the gas share could climb further, reducing Argentina’s dependence on gasoline imports and improving the country’s trade balance. In that scenario, the Argentina oil and gas upstream market share for gas could approach parity with oil by the mid-2030s.

By Well Type: Unconventional Dominance Entrenches

Unconventional wells captured 78.9% of 2025 activity and are projected to register a 4.5% CAGR through 2031, underscoring how Vaca Muerta has transitioned from exploration to factory-style development. The Argentina oil and gas upstream market size attached to these wells benefits from 10%–15% annual productivity gains driven by higher proppant loads and tighter stage spacing. Conventional drilling persists in Austral and Cuyana but primarily for workovers that defend decline curves rather than grow volumes. Pad drilling of 50–100 well campaigns trims surface disturbance and shares infrastructure, reducing per-well capex by up to 20%.

Acreage quality drives a spread in returns: Tier-one blocks such as Loma Campana yield post-tax IRR above 20%, while fringe acreage struggles to clear mid-teens. This divergence propels consolidation as cash-rich majors acquire underperforming blocks to bolt onto core positions. Regulatory oversight under Ley de Hidrocarburos imposes environmental and abandonment obligations that could accelerate decommissioning of marginal conventional fields, indirectly channeling more capital toward unconventional wells inside the Argentine oil and gas upstream market.

By Service: Decommissioning Emerges as Growth Vector

Development and production services held an 80.1% share in 2025, but decommissioning is poised for a 6.8% CAGR as regulators enforce tighter end-of-life standards. The Argentina oil and gas upstream market size for decommissioning expands as operators relinquish conventional concessions in the Austral Basin, where aging offshore jackets and onshore wellbore clusters must be safely abandoned. Environmental bonding rules adopted in 2024 require operators to escrow the full abandonment cost, which forces budget allocation regardless of commodity prices. Specialized contractors offering turnkey plug-and-abandon solutions thus gain a predictable revenue stream even in downturns.

Meanwhile, exploration services remain relevant for Vaca Muerta delineation and offshore wildcats, though at a smaller base. Digital well-intervention tools, such as coiled-tubing deployed fiber-optic logging, replace legacy wireline, boosting service-quality expectations. Over time, decommissioning and exploration will erode development’s share, diversifying service-company revenue lines and cushioning them against drilling cycles, thereby stabilizing supplier margins across the Argentine oil and gas upstream market.

Geography Analysis

Neuquén Basin produced roughly 70% of Argentina’s hydrocarbons in 2025, cementing its role as the growth engine for the Argentine oil and gas upstream market.[4]Reuters Staff, “Neuquén Output Hits Record on Pipeline Ramp-Up,” Reuters, reuters.com The basin’s Jurassic source rocks and the brittle Vaca Muerta shale sit within a robust infrastructure grid of centralized processing plants and dual-service pipelines, cutting per-well costs by up to 30% relative to greenfield zones. Provincial incentives such as royalty rebates for exceeding production targets accelerate pad approvals and keep rig utilization near nameplate capacity.

Offshore Malvinas and Argentine basins form the highest-risk frontier but also the largest potential reserve upside. Equinor and Harbour Energy plan two ultra-deep exploration wells by late 2026, a timeline that aligns with rig availability in the South Atlantic. Federal stewardship simplifies permitting, contrasting with the provincial-federal dual-layer onshore. Discoveries would diversify the Argentine oil and gas upstream market beyond Neuquén, spreading geopolitical and environmental risk.

Secondary areas such as the Austral and Cuyana basins contributed an estimated 15% of national output in 2025, yet decline at 3%–5% annually. Decommissioning liabilities are rising as these conventional fields approach economic limit, creating new demand for abandonment contractors. Logistical concentration in Neuquén raises systemic risk: strikes, extreme weather, or pump-station failures can curtail national production, prompting operators to evaluate rail or barge alternatives despite USD 3-5/bbl higher costs. The geography mix thus balances prolific shale, nascent deepwater, and mature conventional assets, each shaping the medium-term profile of the Argentina oil and gas upstream market.

Competitive Landscape

YPF and its joint-venture affiliates held about 40% of national production in 2025, granting the state firm scale to dictate drilling cadence, service pricing, and technology adoption. Chevron, Shell, TotalEnergies, and ExxonMobil operate predominantly as non-operated partners, mitigating political risk but limiting operational autonomy. Independents such as Vista Energy and Pan American Energy focus on tier-two acreage, using lean overhead and performance-based service contracts to preserve margins.

Technology deployment is the main differentiator. Operators using electric frac fleets, fiber-optic geosteering, and automated rigs generate 15%–25% productivity gains over peers. YPF’s 2024 down-hole sensor patents underscore its commitment to tech-led cost reduction. Competitive intensity remains highest in Vaca Muerta’s core, where acreage trades above USD 10,000/acre, while offshore blocks draw interest from companies with deepwater portfolios.

Regulation exerts strong influence. The Secretaría de Energía controls export permits and domestic price caps, wielding de facto veto power on commercial strategies. Capital discipline has sharpened: majors sanction only RIGI-approved projects, while independents recycle cash through asset rotations to fund drilling. Consolidation is likely as fringe players exit and majors deepen exposure, reshaping the ownership matrix of the Argentina oil and gas upstream market.

Argentina Oil And Gas Upstream Industry Leaders

-

YPF SA

-

Pan American Energy LLC

-

Vista Energy SAB de CV

-

Chevron Argentina SRL

-

TotalEnergies SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: YPF has inked a significant USD 600 million contract with Archer, spanning five years, to oversee operations of seven state-of-the-art drilling rigs in Argentina's Vaca Muerta shale formation.

- November 2025: Eni and YPF, Argentina's top energy firm, inked a non-binding deal with XRG, a member of the ADNOC Group. This agreement hints at XRG's potential role in the 12 MTPA liquefied natural gas (LNG) phase of the Argentina LNG (ARGLNG) project.

- August 2025: TotalEnergies' affiliate, Total Austral, inked a deal with YPF SA, offloading its 45% stake in two unconventional oil and gas blocks in Argentina's Vaca Muerta region. The Rincon La Ceniza and La Escalonada blocks fetched a price tag of USD 500 million. Situated in the Neuquén Basin, these concessions are currently in a pilot development phase.

Argentina Oil And Gas Upstream Market Report Scope

The upstream segment of the oil and gas industry contains exploration activities, which include creating geological surveys and obtaining land rights, and production activities, which include onshore and offshore drilling.

The Argentine oil and gas upstream market is segmented by location of deployment, resource type, well type, service, and geography. By location of deployment, the market is segmented into onshore and offshore operations. By resource type, the market is classified into crude oil and natural gas. By well type, the market is segmented into conventional and unconventional wells. By service, the market is segmented into exploration, development and production, and decommissioning activities. For each segment, market sizing and forecasts have been conducted on the basis of value (USD).

By Location of Deployment

| Onshore |

| Offshore |

By Resource Type

| Crude Oil |

| Natural Gas |

By Well Type

| Conventional |

| Unconventional |

By Service

| Exploration |

| Development and Production |

| Decomissioning |

| By Location of Deployment | Onshore |

| Offshore | |

| By Resource Type | Crude Oil |

| Natural Gas | |

| By Well Type | Conventional |

| Unconventional | |

| By Service | Exploration |

| Development and Production | |

| Decomissioning |

Key Questions Answered in the Report

What is the current value of the Argentina oil and gas upstream market?

The market is valued at USD 3.52 billion in 2026 and is forecast to reach USD 4.27 billion by 2031.

Which segment is expanding fastest in Argentina’s upstream activities?

Offshore projects are projected to post the quickest 5.4% CAGR through 2031, driven by ultra-deepwater exploration.

How much foreign direct investment has RIGI attracted so far?

Commitments exceed USD 30 billion, including Chevron’s USD 4.3 billion and Shell’s USD 3.2 billion projects.

What is the main bottleneck restraining winter production in Neuquén?

Pipeline congestion during peak residential demand can force curtailments of up to 15% of field output.

Why are decommissioning services growing in importance?

Stricter environmental bonding rules and aging conventional fields drive a 6.8% CAGR for abandonment services through 2031.

Page last updated on: