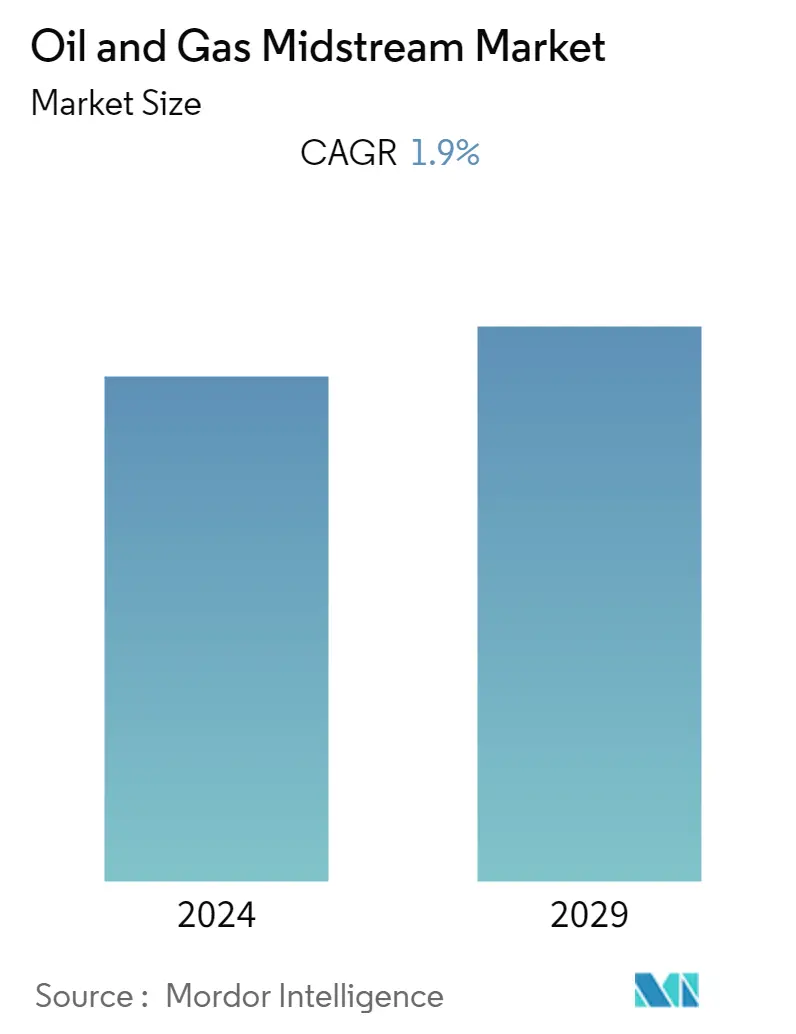

Oil and Gas Midstream Market Size

| Study Period | 2020 - 2029 |

| Base Year For Estimation | 2023 |

| CAGR | 1.90 % |

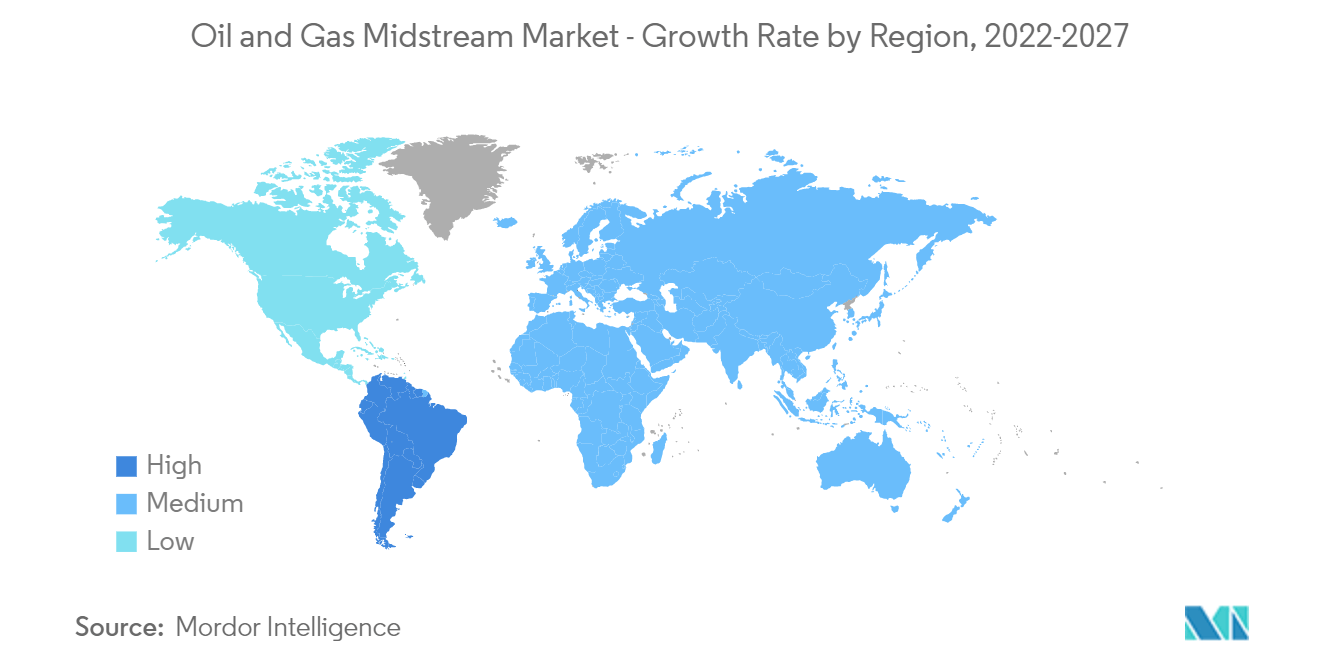

| Fastest Growing Market | South America |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Oil and Gas Midstream Market Analysis

The global operating oil and gas pipeline length was estimated to be around 2079.72 thousand km in 2020, which is expected to reach 2400 thousand km by the end of 2027, registering a CAGR of about 1.9% during the forecast period of 2022-2027. The oil and gas midstream was fairly unaffected by the COVID-19 pandemic since the constant usage of storage facilities for storing hydrocarbons, usage of pipelines for fuel transportation, and resilient demand for LNG in 2020 kept the demand for midstream services normalized. Factors such as increasing production and consumption of natural gas and refined petroleum products are expected to boost the demand for pipeline services in the coming years and are likely to drive the oil & gas midstream market during the forecast period. However, environmental concerns regarding new pipelines and transportation infrastructure are likely to restrain the growth of the oil & gas midstream market in the coming years.

- The transportation segment is likely to dominate the market during the forecast period due to the increasing demand for refined products.

- Increasing investments and development of small and complex offshore fields in different regions are expected to increase the demand for midstream services. Therefore, this is expected to provide a great opportunity for the midstream sector during the forecast period.

- South America is expected to be the fastest-growing market during the forecast period, mainly due to the growing demand for LNG in countries like Chile, Brazil, and Argentina.

Oil and Gas Midstream Market Trends

This section covers the major market trends shaping the Oil & Gas Midstream Market according to our research experts:

The Transportation Sector to Dominate the Market

- The oil and gas transportation industry is dominated by pipelines. The oil and gas supply in different regions is expected to exceed the existing transportation capacity, requiring expansions and the construction of new pipelines.

- Globally, the rising energy demand has resulted in an increase in new pipeline constructions and transportation facilities as the continuous need for energy demands new oil and gas infrastructure. This increasing energy demand has increased new terminals and pipeline construction, including oil and gas pipelines and transportation, especially in Asia-Pacific (APAC) and Africa.

- For instance, in May 2021, Russia and Pakistan signed an agreement to construct about a 1,100-km gas pipeline worth USD 2 billion by the end of 2023. Further, Russia and India also signed a deal worth USD 40 billion on natural gas exports to India. Russia is a significant exporter of LNG, which presents an opportunity in the pipeline industry for the market players during the forecast period.

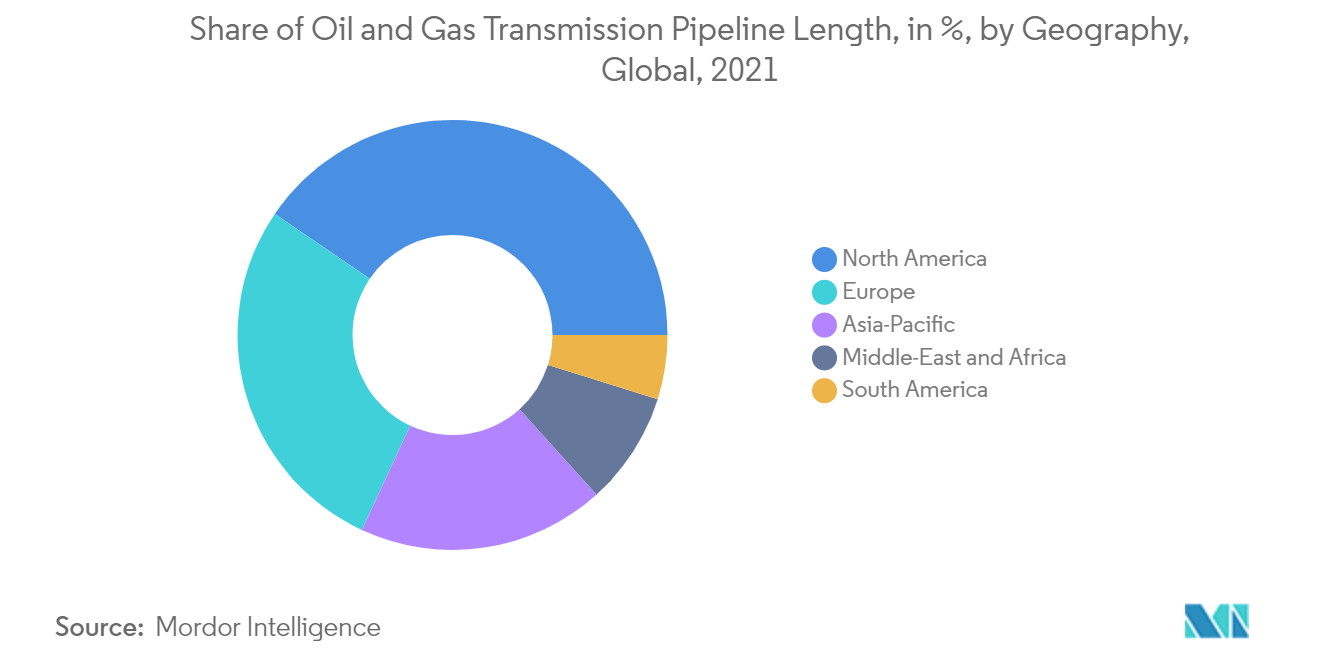

- Moreover, the largest market for the oil and gas midstream sector, North America, had its pipeline infrastructure started developing over half a century ago. Hence, a lot of pipelines are old and demand expansion as per the forecasted demand rise for petroleum products and natural gas.

- The new oil and gas exploration and production activities globally, along with an improved and efficient pipelines network for transportation, will significantly influence the market growth during the forecast period.

- Hence, the transportation sector covers the major markets in the midstream sector. Hence, with the increasing transportation sector, the midstream sector is also expected to increase during the forecast period.

South America to be the Fastest Growing Market

- South America is expected to be the fastest-growing market for the oil and gas midstream market during the forecast period.

- South America is home to some of the largest countries globally in terms of proven oil and gas reserves. The region also hosts one of the largest offshore oil and gas markets across the world. Brazil, Venezuela, Argentina, and Colombia are the major countries in the region's oil and gas industry.

- Oil and gas projects, both offshore and onshore, in South America have lower breakeven prices and competitive payback times as compared to similar projects across the world, which makes them more resilient in the current turbulent times. Around 30 offshore oil & gas projects are expected to be given the green light across the region over three years (2021-2023), which will require a cumulative greenfield investment in the range of USD 50 billion. These projects are operated by a mix of national oil companies (NOCs) and major independent companies; further, the increasing pipeline infrastructure, with the development of oilfields, is expected to propel the midstream market in South America during the forecast period.

- For instance, Petrobras is planning to invest around USD 55 billion for the period 2021 to 2025. Of this total investment, 84% is being allocated to oil and gas exploration and production (E&P). The investment of around USD 46 billion in E&P involves approximately USD 32 billion, 70%, in pre-salt assets. This indicates that the upstream oil & gas sector, especially the offshore oil & gas assets in Brazil, is expected to witness significant investments into pipeline infrastructure for crude oil transportation during the forecast period.

- Furthermore, there are three major pipeline projects in Brazil, including both capacity expansion pipelines and newly constructed pipelines. Capacity expansion pipeline includes the Bolivia-Brazil pipeline (GASBOL), which is anticipated to increase the pipeline capacity to an estimated 3.6 million cubic meters by 2022. The new construction of the gas pipeline includes the gas pipeline between Argentina and Brazil, and Sao Carlos, Sao Paulo, and Brazil.

- Moreover, the region has been witnessing growth in the LNG market due to increasing gas demand from countries like Chile, Brazil, and Argentina. Chile, Brazil, and Argentina have been top LNG importers in the region, with imports of 3.7, 3.3, and 1.8 billion cubic meters, respectively, in 2020. In 2020, the entire South and Central American region imported a total of 13.9 billion cubic meters of LNG.

- In March 2021, Bill 4476/2020, which institutes the New Gas Law, was passed by the Chamber of Deputies in Brazil. The bill shifts control away from the state-controlled Petrobras and allow companies that want to build gas pipelines to follow a simple authorization process rather than the previous more complex contract, and gives more power to the energy regulator, the Brazilian National Agency of Petroleum, Natural Gas, and Biofuels. The law is expected to generate significant shifts in the sector, as private companies can quickly get import permits for natural gas along with the third parties that can access LNG terminal infrastructure.

- Therefore, owing to the above points, South America is expected to be the fastest-growing region in the oil and gas midstream market during the forecast period.

Oil and Gas Midstream Industry Overview

The oil and gas midstream market is moderately consolidated. Some of the key players in this market include APA Group, Chevron Corporation, BP PLC, Enbridge Pipelines Inc., and Shell PLC, among others.

Oil and Gas Midstream Market Leaders

APA Group

Chevron Corporation

BP PLC

Enbridge Pipelines Inc.

Shell PLC

*Disclaimer: Major Players sorted in no particular order

Oil and Gas Midstream Market News

- In December 2020, the Petroleum Ministry of India announced a plan to invest approximately USD 60 billion in expanding the gas infrastructure in India by 2024. Through this, the government plans to increase the share of natural gas to 15% by 2030 in the country's energy mix. The investment will majorly focus on the development of pipeline networks and LNG terminal across the country.

- In February 2021, the Heads of the State of Nigeria and Morocco reaffirmed their commitment to constructing a joint gas pipeline expected to expand energy access across West Africa. The 5,660 km pipeline, which is estimated to cost approximately USD 25 billion, is expected to serve as an extension to the existing West African Gas Pipeline currently serving Benin, Togo, and Ghana and connect with Spain through Cadiz.

- In July 2021, after years of tense relations, Kenya and Tanzania signed a USD 1 billion gas pipeline agreement. The gas pipeline deal will transport gas between the coastal town of Mombasa in Kenya and Dar es Salaam in Tanzania. The project will cover over 600 kilometers.

Oil and Gas Midstream Market Report - Table of Contents

1. INTRODUCTION

1.1 Scope of the Study

1.2 Market Definition

1.3 Study Assumptions

2. EXECUTIVE SUMMARY

3. RESEARCH METHODOLOGY

4. MARKET OVERVIEW

4.1 Introduction

4.2 Oil and Gas Operating Pipeline Length Forecast (in km), till 2027

4.3 Oil Production and Consumption Trend in thousand barrels per day, 2010-2021

4.4 Gas Production and Consumption Trend in billion cubic feet per day (bcf/d), 2010-2021

4.5 Key Midstream Projects Information

4.5.1 Existing Projects

4.5.2 Projects in Pipeline

4.5.3 Upcoming Projects

4.6 Recent Trends and Developments

4.7 Government Policies and Regulations

4.8 Market Dynamics

4.8.1 Drivers

4.8.2 Restraints

4.9 Supply Chain Analysis

4.10 Porter's Five Forces Analysis

4.10.1 Bargaining Power of Suppliers

4.10.2 Bargaining Power of Buyers/Consumers

4.10.3 Threat of New Entrants

4.10.4 Threat of Substitutes Products and Services

4.10.5 Intensity of Competitive Rivalry

5. MARKET SEGMENTATION

5.1 Sector

5.1.1 Transportation

5.1.2 Storage and Terminals

5.2 Geography

5.2.1 North America

5.2.2 Europe

5.2.3 Asia Pacific

5.2.4 South America

5.2.5 Middle-East and Africa

6. COMPETITIVE LANDSCAPE

6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

6.2 Strategies Adopted by Leading Players

6.3 Company Profiles

6.3.1 APA Group

6.3.2 Chevron Corporation

6.3.3 BP PLC

6.3.4 Enbridge Pipelines Inc.

6.3.5 Shell PLC

6.3.6 Baker Hughes Company

6.3.7 Williams Inc.

6.3.8 Enlink Midstream LLC

- *List Not Exhaustive

7. MARKET OPPORTUNITIES AND FUTURE TRENDS

Oil and Gas Midstream Industry Segmentation

The oil and gas midstream market report includes:

| Sector | |

| Transportation | |

| Storage and Terminals |

| Geography | |

| North America | |

| Europe | |

| Asia Pacific | |

| South America | |

| Middle-East and Africa |

Oil and Gas Midstream Market Research FAQs

What is the current Oil and Gas Midstream Market size?

The Oil and Gas Midstream Market is projected to register a CAGR of 1.9% during the forecast period (2024-2029)

Who are the key players in Oil and Gas Midstream Market?

APA Group , Chevron Corporation, BP PLC , Enbridge Pipelines Inc. and Shell PLC are the major companies operating in the Oil and Gas Midstream Market.

Which is the fastest growing region in Oil and Gas Midstream Market?

South America is estimated to grow at the highest CAGR over the forecast period (2024-2029).

Which region has the biggest share in Oil and Gas Midstream Market?

In 2024, the North America accounts for the largest market share in Oil and Gas Midstream Market.

What years does this Oil and Gas Midstream Market cover?

The report covers the Oil and Gas Midstream Market historical market size for years: 2020, 2021, 2022 and 2023. The report also forecasts the Oil and Gas Midstream Market size for years: 2024, 2025, 2026, 2027, 2028 and 2029.

Oil and Gas Midstream Industry Report

Statistics for the 2024 Oil and Gas Midstream market share, size and revenue growth rate, created by Mordor Intelligence™ Industry Reports. Oil and Gas Midstream analysis includes a market forecast outlook to 2029 and historical overview. Get a sample of this industry analysis as a free report PDF download.