Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

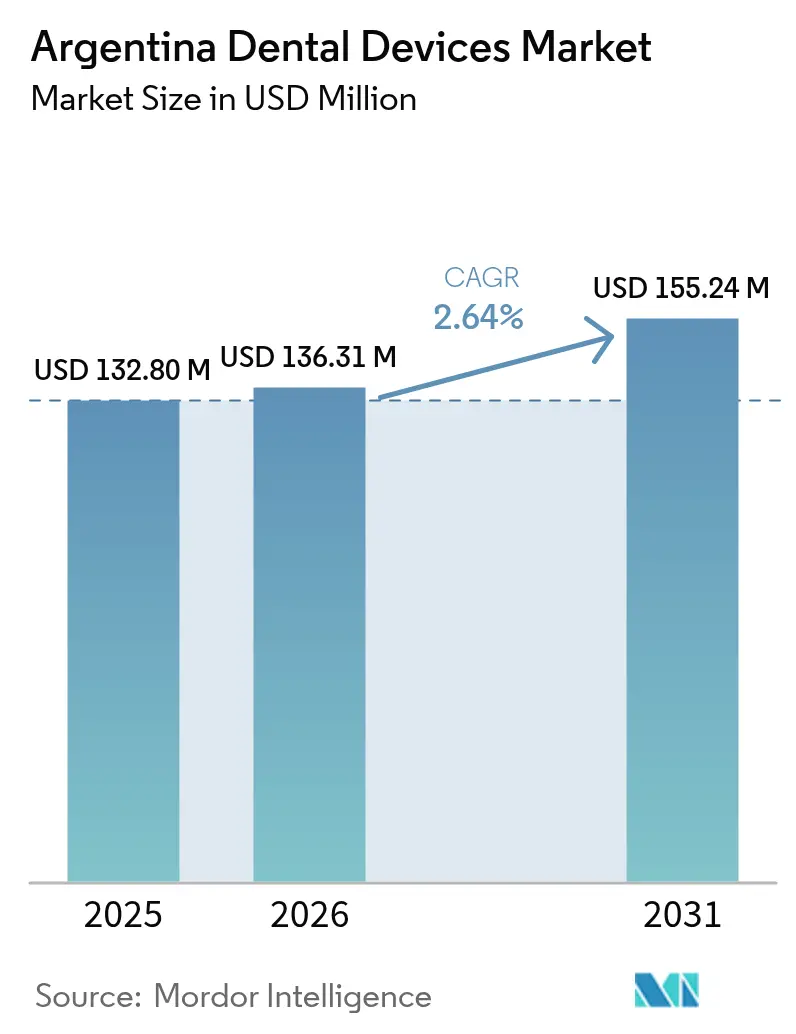

| Base Year Market Size (2025) | USD 132.80 Million |

| Market Size (2026) | USD 136.31 Million |

| Market Size (2031) | USD 155.24 Million |

| Growth Rate (2026 - 2031) | 2.64% CAGR |

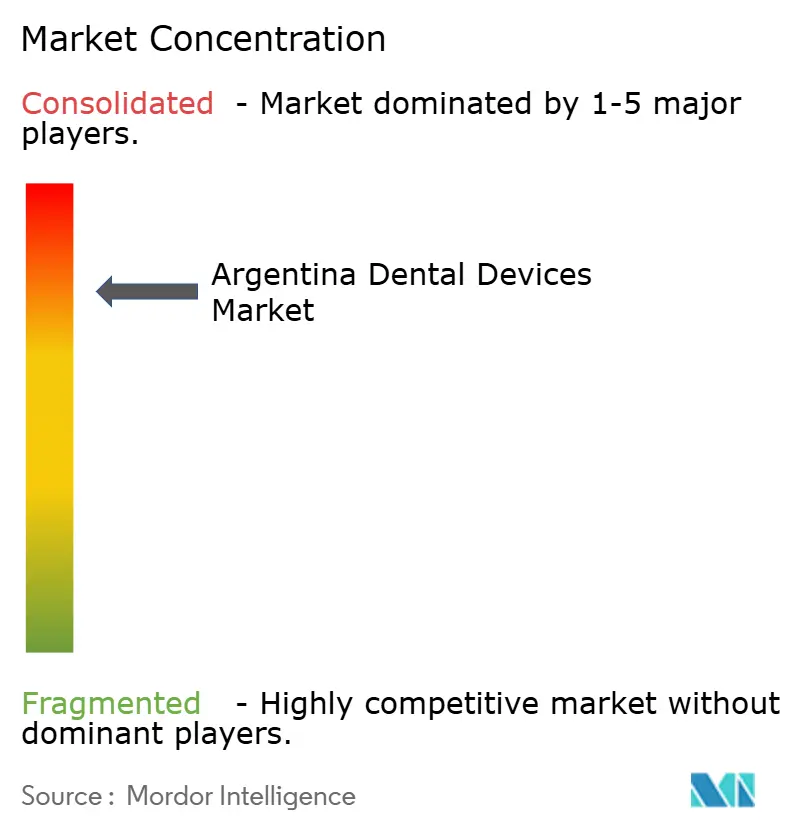

| Market Concentration | High |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Dental Devices Market Analysis by Mordor Intelligence

The Argentina Dental Devices market size is expected to grow from USD 132.80 million in 2025 to USD 136.31 million in 2026 and is forecast to reach USD 155.24 million by 2031 at 2.64% CAGR over 2026-2031.

Continued digitalization, rising private insurance penetration and government-led standardization of electrical safety rules are converging to keep demand resilient despite currency volatility and import-financing constraints. Urban clinics are prioritizing chair-side CAD/CAM systems and cone-beam CT scanners to compete for affluent local and inbound dental-tourism patients, while academic institutes accelerate purchases of research-grade imaging and prototyping platforms to support evidence-based care. Supply-side realignment—most notably faster import-clearance cycles and cloud-enabled service support—is shortening replacement timelines, nudging the installed base toward higher-margin digital devices. Meanwhile, manufacturers are adapting through localized training programs that counteract the persistent shortage of dentists certified to operate advanced systems, ensuring that the Argentine dental devices market continues to modernize even in the face of macro-economic headwinds

Key Report Takeaways

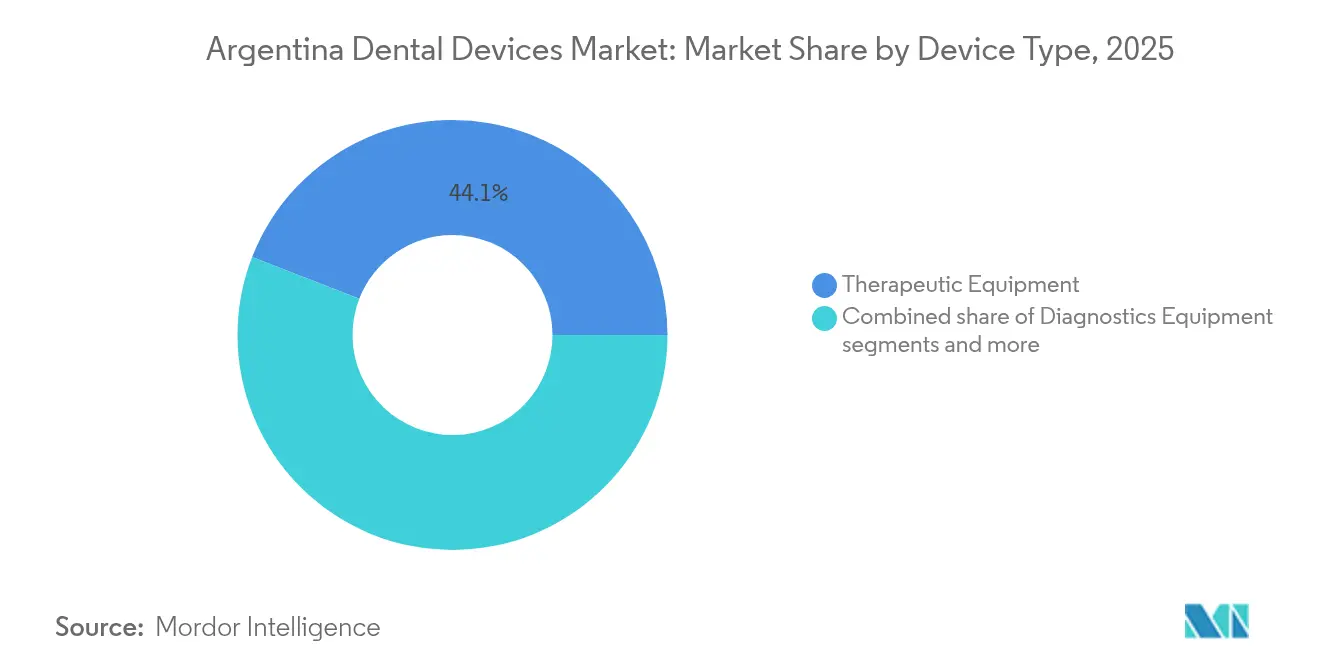

- By product category, dental equipment led with 44.10% of Argentina's dental devices market share in 2025, while dental consumables are projected to expand at a 3.18% CAGR through 2031.

- By treatment type, orthodontics accounted for a 33.10% share of the Argentine dental devices market size in 2025; periodontics is forecast to grow at a 2.97% CAGR to 2031.

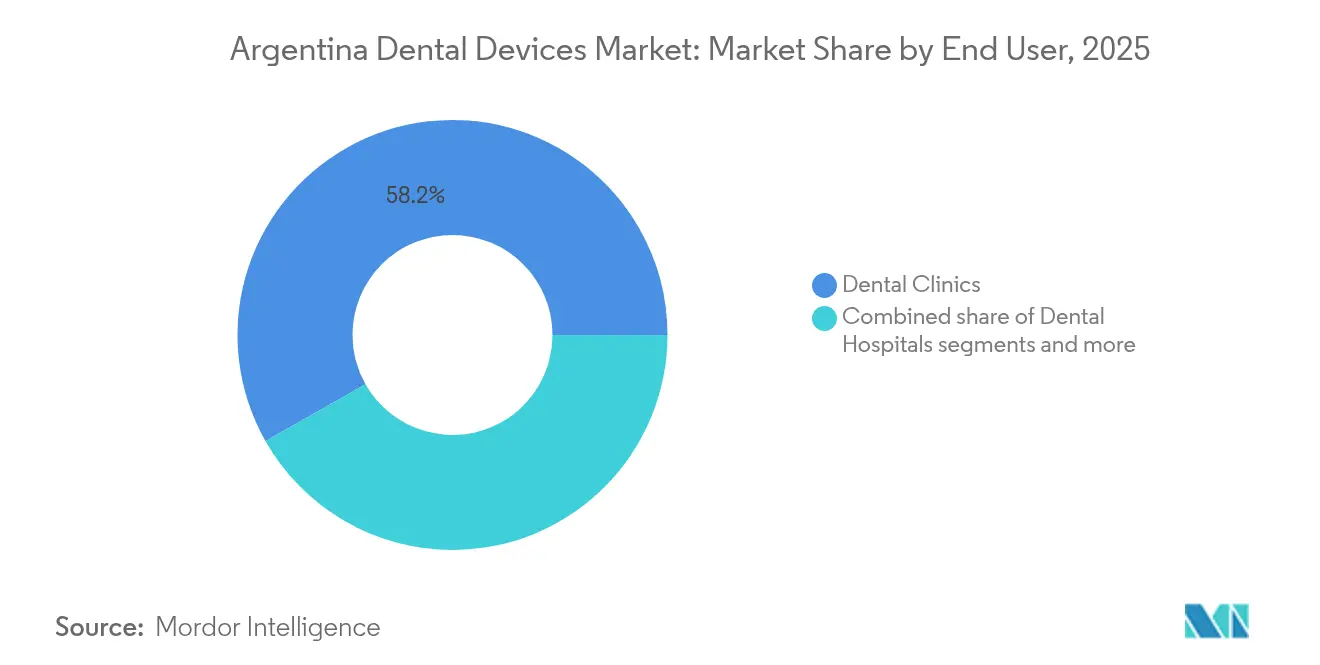

- By end user, dental clinics held 58.20% revenue share in 2025, whereas academic & research institutes are advancing at a 3.17% CAGR over 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Dental Devices Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Uptake of CAD/CAM-Enabled Chair-Side Dentistry in Buenos Aires Metro | +0.6 | Buenos Aires Metro, with spillover to Córdoba, Rosario | Medium term (~ 3-4 yrs) |

| Expansion of Private Dental Insurance Cover Among Middle-Income Argentines | +0.5 | National, concentrated in urban middle-class areas | Medium term (~ 3-4 yrs) |

| Government-Led "Sonrisas Argentinas" Oral-Health Programs Increasing Equipment Procurement | +0.4 | National, with emphasis on underserved regions | Short term (≤ 2 yrs) |

| Dental Tourism Inflow from Chile & Uruguay Boosting High-End Device Demand | +0.3 | Buenos Aires, Mendoza, border regions | Long term (≥ 5 yrs) |

| Rapid Growth of Clear-Aligner Clinics Targeting Millennials | +0.4 | National, primarily urban centers with high millennial population | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Rising Uptake of CAD/CAM-Enabled Chair-Side Dentistry

Urban practices adopting full chair-side workflows report a 37% reduction in average chair time and a 42% drop in patient revisits, strengthening their competitive position against clinics still reliant on traditional impression-taking. The mounting preference for same-day crowns is propelling intraoral-scanner penetration to 28% of practices in Buenos Aires alone, with Straumann’s Virtuo Vivo and Dentsply Sirona’s latest Primescan 2 acting as gateway devices that later stimulate purchases of milling units and cloud-based design software. These investments offset their higher upfront cost through faster throughput and higher case acceptance among time-pressed patients who now expect single-visit restorations. In parallel, distributors are bundling scanners with remote service contracts to guarantee uptime, lowering perceived risk for smaller clinics and extending the CAD/CAM footprint beyond Argentina’s largest cities.

Expansion of Private Dental-Insurance Cover

Abolition of price caps in April 2024 triggered a 40% spike in private health-insurance premiums, yet it simultaneously widened the menu of procedure reimbursements, including implantology and CAD/CAM restorations that were previously out-of-pocket luxuries. Insurers are forging preferred-provider networks that promise higher volumes to technologically advanced clinics, prompting those providers to prioritize equipment with real-time claims-integration features. As a result, CBCT scanners capable of automatically exporting DICOM files into cloud-based insurer portals are gaining traction. These networks further concentrate high-end device demand in metropolitan corridors, bolstering medium-term sales visibility for suppliers operating in the Argentina dental devices market.

Accelerating Adoption of 3D Printing Technology

Dental laboratories in Argentina invested heavily in polymer and metal printers during 2024, lowering fixture lead times from two weeks to less than 48 hours for surgical guides and temporaries. Materials innovation—exemplified by cobalt-chromium alternatives that deliver high tensile strength without compromising biocompatibility—is broadening clinical indications and supporting in-house prosthetics fabrication at mid-scale clinics. Printer vendors are bundling open-architecture design software that integrates seamlessly with existing intraoral-scanner outputs, creating a virtuous cycle of equipment purchases across the digital workflow. Importantly, Argentine dental schools are incorporating additive manufacturing modules into curricula, gradually closing the skills gap that has historically limited advanced equipment utilization.

Dental Tourism Inflow Boosting High-End Device Demand

Procedure costs that run 50-70% below U.S. and European benchmarks continue to attract international patients, particularly for multi-implant rehabilitations and cosmetic veneer packages. Clinics catering to this clientele are investing in premium CBCT units and real-time shade-matching spectrophotometers to deliver same-trip full-arch restorations. Airlines have reinstated direct flights to Buenos Aires and Mendoza, a factor that further cements the twin cities’ status as dental-tourism hubs and bodes well for sustained demand across the high-end tier of the Argentina dental devices market.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Peso Volatility Elevating Imported Device Costs in the Short Term | -0.5 | National, with acute impact on import-dependent regions | Short term (≤ 2 yrs) |

| Persistent Shortage of Certified Biomedical Engineers for Equipment Maintenance | -0.4 | National, severe in interior provinces | Medium term (~ 3-4 yrs) |

| Fragmented Distribution Network Outside Top-5 Provinces | -0.3 | Interior provinces, excluding Buenos Aires, Córdoba, Santa Fe, Mendoza, Tucumán | Short term (≤ 2 yrs) |

| Intensifying Gray-Market Consumables Undermining Branded Sales | -0.3 | National, particularly affecting price-sensitive segments | Medium term (~ 3-4 yrs) |

| Source: Mordor Intelligence | |||

Persistent Shortage of Skilled Professionals

Argentina records 15.35 dentists per 10,000 population—far above the global mean—yet only a fraction are certified in digital-imaging interpretation or CAD/CAM design. Rural provinces struggle the most, with some localities hosting one dentist for every 13,000 residents, constraining device utilization outside of major cities. Manufacturers respond by sponsoring hybrid learning platforms that mix on-site labs with cloud-delivered modules, but ramp-up cycles remain slow, delaying the full revenue potential of advanced units installed over the last two years.

Fragmented Distribution Network

More than 2,000 entities participate in equipment distribution, yet fewer than 25% manufacture locally, resulting in overlapping supply chains that increase transport and maintenance costs. Although Resolution No. 16/2025 simplifies electrical safety certification, and the government shortened import payment terms to 30 days in December 2024, many clinics in interior provinces still wait up to 11 weeks for spare parts. Distributors are experimenting with cloud-monitored inventory systems to anticipate failure and pre-position components, an initiative that could mitigate near-term headwinds for the Argentine dental devices market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Digital Integration Drives Segment Evolution

Dental equipment commanded 44.10% of Argentina dental devices market share in 2025, underscoring the country’s sizeable installed base of chairs, delivery units and imaging systems. Replacement demand is heavily skewed toward sensor-based intraoral radiography and CBCT scanners, pushing analogue film units toward obsolescence in urban zones. At the same time, the dental consumables sub-category is pacing at a 3.18% CAGR, a trajectory linked to rising implant placements and the shift from amalgam to resin-based composites that pair seamlessly with digital shade-matching tools. Straumann’s 2024 Annual Report highlights that intraoral-scanner adoption typically doubles material consumption per chair because clinicians upsell premium zirconia restorations once they control the CAD design pipeline. That dynamic is expected to keep consumables growth ahead of core equipment replacement through 2031.

Milling-unit installations grew 17% in 2024, driven by bundling strategies that pair scanners with open-architecture mills; yet only 28% of units reside outside the three largest provinces, signaling room for geographic catch-up. Supply-side obstacles remain centered on CAD license fees denominated in USD, which inflate local-currency costs during peso depreciation cycles.

By Treatment: Specialty Procedures Reshape Demand Patterns

Orthodontics maintained a dominant 33.10% stake in the Argentine dental devices market in 2025, driven by the penetration of clear aligners and the mainstream acceptance of early interceptive treatments among adolescents. Align Technology expanded its digital-treatment-planning center in Buenos Aires in late 2024, slashing turnaround times for aligner trays destined for Southern Cone clinics. Periodontic therapies, forecast to grow at 2.97% CAGR, benefit from emerging evidence linking periodontal status with systemic conditions, a narrative amplified by professional societies that now recommend annual periodontal screenings.

Prosthodontics is similarly driving the Argentine dental devices market toward integrated workflows, as single-visit crowns, full-arch implant planning, and immediate-load protocols require high-resolution intraoral imaging and chair-side milling accuracy within ±25 μm. Endodontic devices—especially nickel-titanium rotary systems with apex locator feedback loops—are gaining uptake in postgraduate training centers, setting new standards for private-practice workflow within two to three years. The cosmetic surgery segment is surging on the back of social-media aesthetics, compelling clinics to stock LED whitening lamps and spectrophotometers that promise shade consistency; these add-ons, though relatively low-price, enhance the revenue pyramid per patient visit.

By End User: Institutional Dynamics Reshape Equipment Procurement

Dental clinics retained 58.20% of Argentina's dental device market share in 2025, reaffirming their role as the country’s primary oral-care delivery platform. Clinic chains with three or more operatories exhibit the fastest upgrade cadence, replacing delivery systems every five years versus eight years in solo practices. Academic & research institutes, expanding at a 3.17% CAGR, are redefining purchasing criteria: simulation labs now demand haptic-feedback units and CBCT machines with research-grade voxel sizes under 90 μm, a specification exceeded by Dentsply Sirona’s Axeos and Morita’s Veraview X800.

Argentina's dental devices market size for hospitals is comparatively modest but strategically important: tertiary-level institutions house the only proton-beam radiotherapy units for maxillofacial tumors, positioning them as reference centers for complex cases that feed downstream restorations back to private clinics. Tele-dentistry pilots in Patagonia, reliant on smartphone-assisted intraoral cameras and AI-driven lesion classifiers, illustrate how public-sector innovation can shape equipment demand away from high-density corridors. As these programs scale, suppliers anticipate steady orders for portable chairs, battery-driven lights and low-radiation imaging panels that can operate off-grid.

Geography Analysis

The Buenos Aires metropolitan region accounted for roughly 44.75% of total shipments in 2025 and sustains the densest cluster of multi-chair clinics, dental school faculties, and specialty laboratories in the Argentine dental devices market. Digital workflow penetration exceeds 60% in premium practices here, creating a robust corridor for software license renewals and field-service contracts. Equipment leasing is more prevalent in the capital than anywhere else in the country, reflecting better access to dollar-denominated credit lines, which in turn accelerates replacement cycles for high-ticket items such as CBCT scanners and five-axis mills.

Córdoba and Santa Fe provinces form the second-largest consumption belt, buoyed by reputable dental schools that act as technology diffusion hubs. These provinces collectively accounted for 27% of new intraoral scanner installations in 2024. Provincial incentive schemes that refund up to 15% of capital expenditure on locally assembled components have spurred micro-assemblers to produce chair units and LED curing lights, signaling early import substitution for lower-complexity products. Nevertheless, over two-thirds of advanced diagnostic equipment still comes through import channels, reflecting domestic manufacturing gaps.

Interior provinces stretching from Salta in the northwest to Neuquén in Patagonia struggle with equipment penetration rates that lag the national average by almost 40 percentage points. Resolution No. 16/2025, which harmonizes safety testing with IEC 60601-1-2 standards, is expected to encourage distributors to stock certified devices closer to point-of-care, reducing transaction friction that has historically dissuaded smaller clinics from upgrading. The tele-oncology pilot in Patagonia illustrates the potential of technology to bridge geographic inequities: remote towns logged a 70% fall in referral wait times for suspected oral-cancer lesions within the project’s first 12 months. Follow-up funding under the federal Plan Aerocomercial could expand similar schemes into the arid northwest, potentially unlocking an underserved pocket for portable X-ray generators and battery-powered suction units.

Competitive Landscape

Market structure in the Argentina dental devices market is best described as moderately fragmented: the top five manufacturers—Straumann Group, Align Technology, Dentsply Sirona, Envista Holdings and Planmeca—collectively captured just under 50% of premium-tier revenue in 2024, while more than 60 local assemblers focused on entry-level chairs and lights supplied price-sensitive clinics. Multinationals leverage global scale and proprietary software ecosystems to differentiate; for instance, Straumann’s Virtuo Vivo scanner integrates with coDiagnostiX implant-planning software, locking users into a single digital continuum that discourages brand switching.

Distributor strategy is equally decisive. Major importers such as Bernardini Dental and Fadente maintain bonded warehouses near Ezeiza International Airport, accelerating customs clearance to under 72 hours for stock items. Meanwhile, local conglomerate GEA Group is piloting a predictive-maintenance portal that feeds anonymized usage data from cloud-connected compressors back to service engineers, reducing downtime and reinforcing brand loyalty. Academic partnership represents the other front: Dentsply Sirona co-financed a simulation center at the University of Buenos Aires in mid-2024, granting students open access to Primescan units—a move likely to seed long-term brand preference across graduating cohorts.

Price competition remains fiercest in bulk consumables—composite resins, impression materials and endodontic files—where Asian entrants undercut branded products by 15-25%. However, clinical preference for validated digital workflows shields high-end systems from direct price erosion, allowing manufacturers to preserve margins through subscription-based software upgrades rather than hardware alone. The elevation of electrical-safety conformity into a federal technical rule from February 2025 adds cost pressure to non-compliant importers, a change expected to subtly re-consolidate the Argentina dental devices market around players with established regulatory infrastructure.

Argentina Dental Devices Industry Leaders

Henry Schein, Inc.

Envista Holdings Corporation

3M

Straumann Holding AG

Planmeca OY

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Argentina’s Secretariat of Industry and Commerce published Resolution No. 16/2025, creating a new conformity-assessment pathway for electrical medical equipment.

- December 2024: The Argentine government shortened import-payment terms to 30 days after shipment arrival, easing working-capital strain on equipment importers

Argentina Dental Devices Market Report Scope

According to the scope of the report, medical devices are used to treat dental problems and maintain dental health. The Argentine dental devices market is segmented by product (general and diagnostics equipment, dental consumables, and other dental devices), treatment (orthodontic, endodontic, periodontic, and prosthodontic), and end user (hospital, clinics, and other end users). The report offers the value (in USD million) for the above segments.

By Product

| Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | ||

| Radiology Equipment | Extra Oral Radiology Equipment | |

| Intra-oral Radiology Equipment | ||

| Dental Chair and Equipment | ||

| Therapeutic Equipment | Dental Hand Pieces | |

| Electrosurgical Systems | ||

| CAD/CAM Systems | ||

| Milling Equipment | ||

| Casting Machine | ||

| Other Therapeutic Equipments | ||

| Dental Consumables | Dental Biomaterial | |

| Dental Implants | ||

| Crowns and Bridges | ||

| Other Dental Consumables | ||

| Other Dental Devices | ||

By Treatment

| Orthodontic |

| Endodontic |

| Peridontic |

| Prosthodontic |

By End User

| Dental Hospitals |

| Dental Clinics |

| Academic & Research Institutes |

| By Product | Diagnostics Equipment | Dental Laser | Soft Tissue Lasers |

| Hard Tissue Lasers | |||

| Radiology Equipment | Extra Oral Radiology Equipment | ||

| Intra-oral Radiology Equipment | |||

| Dental Chair and Equipment | |||

| Therapeutic Equipment | Dental Hand Pieces | ||

| Electrosurgical Systems | |||

| CAD/CAM Systems | |||

| Milling Equipment | |||

| Casting Machine | |||

| Other Therapeutic Equipments | |||

| Dental Consumables | Dental Biomaterial | ||

| Dental Implants | |||

| Crowns and Bridges | |||

| Other Dental Consumables | |||

| Other Dental Devices | |||

| By Treatment | Orthodontic | ||

| Endodontic | |||

| Peridontic | |||

| Prosthodontic | |||

| By End User | Dental Hospitals | ||

| Dental Clinics | |||

| Academic & Research Institutes | |||

Key Questions Answered in the Report

What is the current size of the Argentina dental devices market?

– The Argentina dental devices market size is USD 136.31 million in 2026 and is projected to reach USD 155.24 million by 2031.

What CAGR is forecast for the Argentina dental devices market?

– A 2.64% CAGR is projected for the period 2026-2031.

Which product category holds the largest share of revenue?

– Dental equipment, including chairs and imaging systems, captured 44.10% of revenue in 2025.

Which treatment segment is expanding fastest?

– Periodontic procedures are forecast to grow at a 2.97% CAGR through 2031 as awareness of systemic links rises.

Page last updated on: