Aprotic Solvents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.24 Billion |

| Market Size (2031) | USD 23.47 Billion |

| Growth Rate (2026 - 2031) | 3.01% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aprotic Solvents Market Analysis by Mordor Intelligence

The Aprotic Solvents Market size was valued at USD 19.65 billion in 2025 and estimated to grow from USD 20.24 billion in 2026 to reach USD 23.47 billion by 2031, at a CAGR of 3.01% during the forecast period (2026-2031). Capital expenditures in lithium-ion battery manufacturing, semiconductor fabs, and peptide-based active pharmaceutical ingredient (API) plants drive incremental volumes even as regulatory compliance costs put a ceiling on short-term growth. Integrated chemical producers are passing through higher energy and feedstock costs to end users, which is reshaping procurement strategies toward long-term supply agreements that guarantee purity and availability. The emergence of biomass-derived dipolar solvents such as Cyrene and gamma-valerolactone (GVL) is redefining competitive boundaries by adding sustainability performance as a formal evaluation criterion. Across applications, price elasticity remains low because most end uses depend on specific polarity and boiling-point requirements that are difficult to replicate with substitute chemistries, leading to continued reliance on legacy molecules despite tightening regulatory scrutiny.

Key Report Takeaways

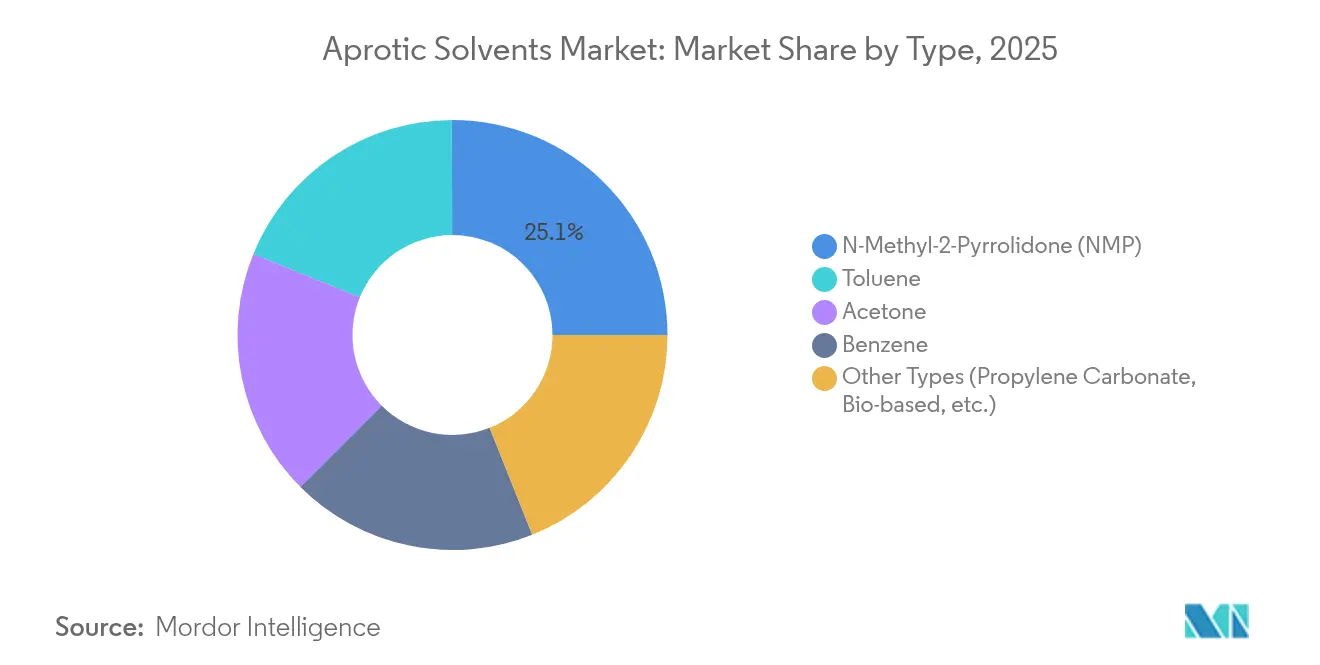

- By Type, N-Methyl-2-Pyrrolidone retained a 25.05% share of the aprotic solvents market in 2025, while the “Other Types” category led growth at a 3.70% CAGR through 2031.

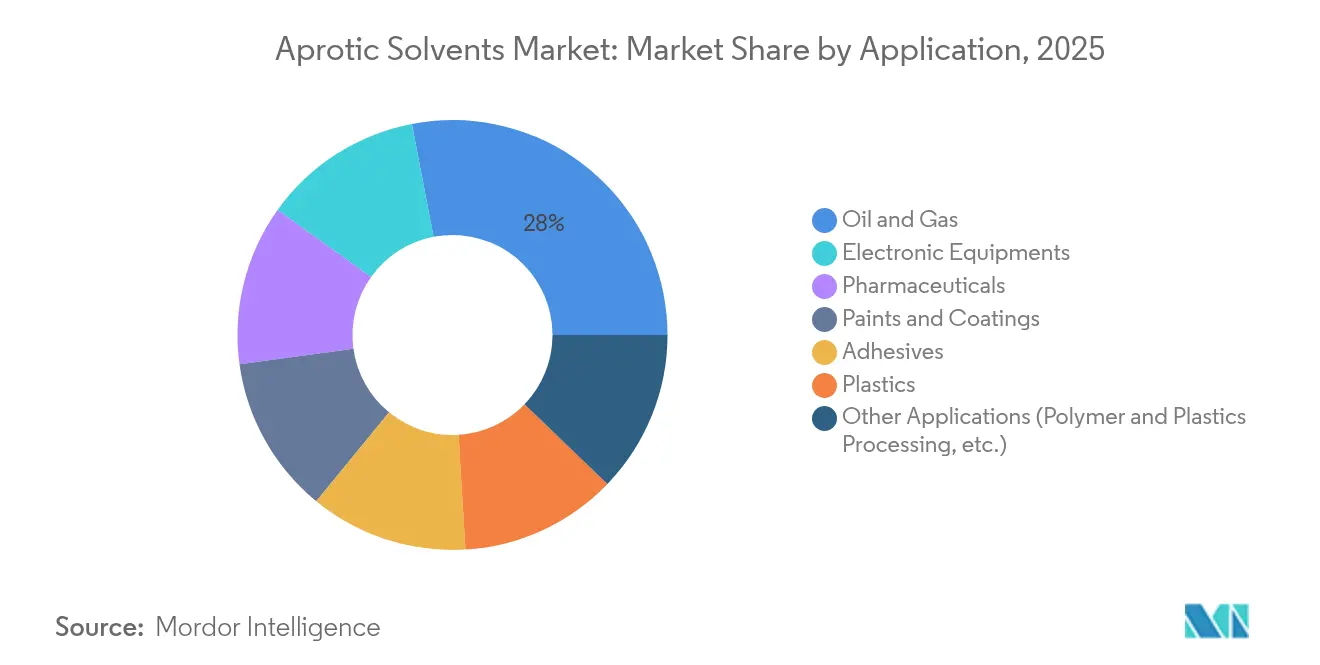

- By Application, Oil and Gas captured 28.03% of the aprotic solvents market size in 2025, and Electronic Equipment posted the highest 3.78% CAGR forecast to 2031.

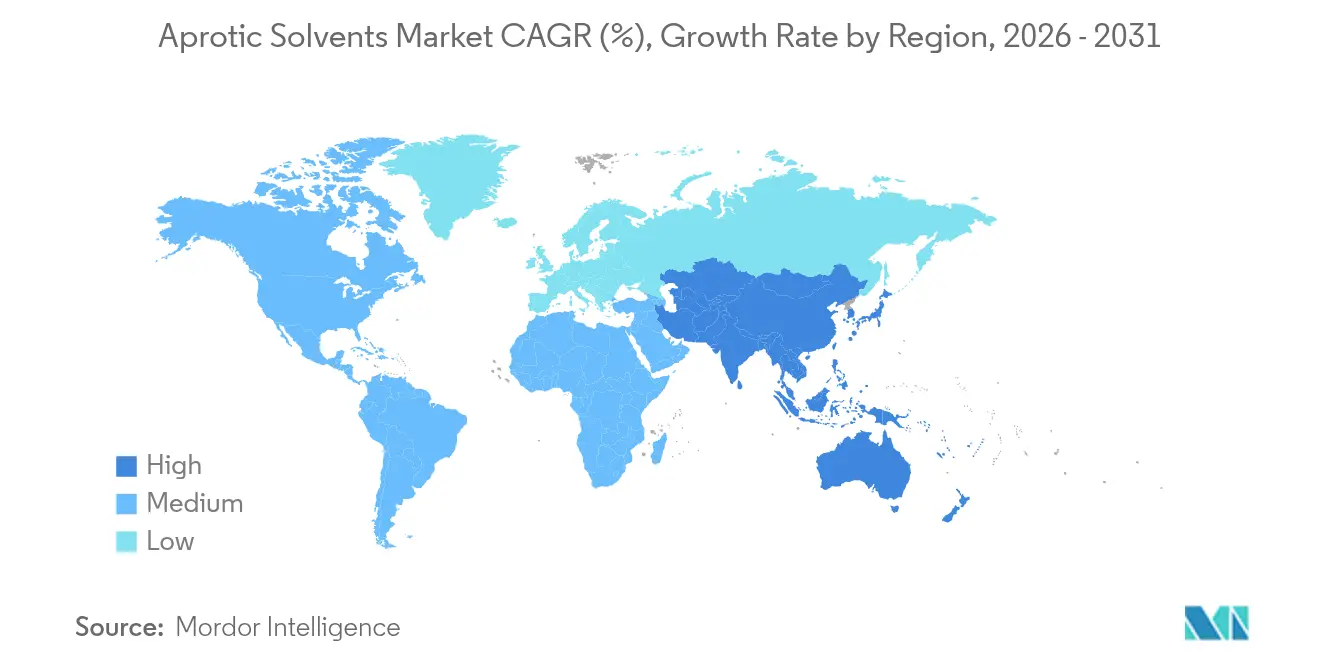

- By Geography, Asia-Pacific commanded 53.15% of the aprotic solvents market share in 2025 and is advancing at a 3.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aprotic Solvents Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid capacity additions in Asian lithium-ion battery production | +0.8% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Persistent demand spike from deep-well oil and gas extraction fluids | +0.6% | Global, concentrated in North America and Middle East | Short term (≤ 2 years) |

| Pharmaceutical greenfield API capacity expansions (2025-2029) | +0.5% | Global, early gains in Europe and North America | Long term (≥ 4 years) |

| Regulatory relaxation for high-purity electronic-grade solvents in China | +0.3% | Asia-Pacific, primarily China | Medium term (2-4 years) |

| Emergence of biomass-derived dipolar aprotics (e.g., Cyrene®, GVL) | +0.4% | Europe and North America core, expanding globally | Long term (≥ 4 years) |

| AI-accelerated solvent selection platforms cutting formulation times | +0.2% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Capacity Additions in Asian Lithium-Ion Battery Production

China’s battery gigafactory pipeline is on track to surpass 1,300 GWh per year of installed output by 2030, which raises annual N-Methyl-2-Pyrrolidone demand by 260,000–390,000 tons since each gigawatt-hour typically consumes 200–300 tons of solvent[1]Systems Assessment Center, “Quantification of Commercially Planned Battery Component Supply in the United States through 2035,” Argonne National Laboratory, anl.gov. Regional producers negotiate multiyear supply agreements that lock in pricing formulas tied to petrochemical feedstock indices, a practice that mitigates volatility but strengthens buyer bargaining power. As cell makers push cathode energy densities higher, viscosity control requirements favor dipolar aprotics with narrow impurity specifications, further entrenching NMP. Complementary investments in electrolyte co-solvents, such as dimethyl carbonate (DMC) and ethyl methyl carbonate (EMC), reinforce cross-solvent demand correlation, benefiting vertically integrated firms. Nevertheless, cost-competitive water-based electrode processing that cuts material costs by 96% threatens late-decade volumes. Dry-film techniques under development add a parallel route that could remove solvent use entirely in some cathode lines

Persistent Demand Spike from Deep-Well Oil and Gas Extraction Fluids

Horizontal and ultra-deep reservoirs require completion fluids that remain stable at temperatures exceeding 200 °C and pressures above 20,000 psi. Dipolar aprotic solvents enable high-salt solubility and thermal stability that water-based fluids cannot match. North American shale projects and Middle Eastern carbonate formations together underpin most incremental uptake. Adoption of natural deep eutectic solvents (NADES) for less severe conditions provides an environmentally favorable pathway, yet still relies on aprotic backbones for extreme conditions. Continued innovation in calcium nitrate-based completion systems highlights ongoing chemistry diversification that nonetheless reinforces demand for compatible aprotic carriers. Short-term growth is secure because equipment retrofits required for alternative fluid chemistries carry capital costs that operators defer during current high-rig utilization cycles.

Pharmaceutical Greenfield API Capacity Expansions (2025–2029)

The peptide therapeutics boom, exemplified by CordenPharma’s EUR 900 million construction program, is boosting dimethylformamide and dimethylacetamide volumes in solid-phase synthesis steps. Each metric ton of GLP-1 agonist active requires roughly 5 tons of aprotic solvent across coupling, cleavage, and crystallization. Modular, single-use reactor trains installed in new facilities support higher solvent recovery rates yet maintain demand for virgin material because regulatory filings limit reuse to defined cycles. Continuous manufacturing pilots offer a 40% solvent intensity reduction but remain limited to low-volume specialty APIs. As regulatory agencies fast-track obesity drug approvals, production timelines shorten, and solvent demand scales in tandem, extending the driver into the long-term horizon.

Regulatory Relaxation for High-Purity Electronic-Grade Solvents in China

China’s State Administration for Market Regulation revised import licensing rules in 2024, easing access to ultra-low metal contaminant variants of NMP and dimethyl sulfoxide for semiconductor fabs. The policy accelerates domestic procurement cycles for new 300 mm wafer facilities and multi-layer chip packaging plants. Fabricators now source directly from foreign producers while local compounding blenders co-produce photoresist strippers customized to equipment specifications. This measure boosts aprotic solvents market volumes for cleaning and etching where parts-per-trillion impurity levels are mandatory. Medium-term impact is moderate, yet the driver solidifies Asia-Pacific’s command of specialty solvent flows.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU REACH re-classification of NMP, DMF and NEP as reproductive toxics | -0.7% | Europe core, global regulatory spillover | Short term (≤ 2 years) |

| Rapid scale-up of super-critical CO₂ and ionic-liquid extraction tech | -0.4% | Global, early adoption in pharmaceuticals | Medium term (2-4 years) |

| Volatility of crude-based feedstocks widening cost swings | -0.3% | Global, pronounced in Asia-Pacific and North America | Short term (≤ 2 years) |

| Accelerated OEM bans on residual aprotics in semiconductor fabs | -0.2% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

EU REACH Re-classification of NMP, DMF and NEP as Reproductive Toxics

The European Commission’s addition of NMP, DMF, and NEP to Annex XVII introduces a 0.3% concentration limit in mixtures effective December 2026 and imposes employee exposure caps. Multinational manufacturers often adopt the strictest jurisdiction as their global default, extending compliance costs to plants beyond Europe[2]SGS, “EU Restricts Two Chemicals under REACH,” sgs.com. Immediate capital outlays include closed-loop handling systems, personal exposure monitoring, and enhanced ventilation. Membrane module producers for water treatment face qualification delays because alternative dipolars change polymer morphology. While exemption dossiers are possible, the administrative burden pushes users to accelerate substitution projects.

Rapid Scale-up of Supercritical CO₂ and Ionic-Liquid Extraction Technologies

Commercial-scale supercritical CO₂ columns now handle up to 5,000 L per hour in hop extraction, pharmaceutical purification, and fine-chemical dewaxing. ]. Process economics improve as compression energy declines with advanced heat-exchange loops. Ionic liquids and deep eutectic solvents (DES) deliver dual functionality, acting as solvents and polymerizable feedstocks in bioplastic synthesis. As these routes move beyond pilot scale, they can obviate large volumes of traditional aprotic solvents, particularly in natural-product extraction and catalyst recycling. Although adoption is unlikely to eclipse incumbent applications entirely by 2030, progressive displacement is expected in greener value chains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: NMP Dominance Faces Bio-Based Disruption

N-Methyl-2-Pyrrolidone accounted for 25.05% of the aprotic solvents market in 2025, underscoring its critical role in lithium-ion battery electrodes and high-performance polymer production. Despite EU classification pressure, cathode slurry rheology and polyimide precursor compatibility still favor NMP, sustaining premium pricing. Producers are installing additional purification trains that achieve 5 ppb metal specifications, catering to 3 nm node semiconductor fabs.

Parallel innovation in the “Other Types” category is reshaping competitive contours. Cyrene, GVL, and dimethyl isosorbide collectively lifted the group to the fastest 3.70% CAGR trajectory. Research published in 2024 confirmed GVL’s ability to maintain polyimide membrane tensile strength within 2% of NMP benchmarks while lowering toxicity classifications. This technical validation demonstrates diminishing performance barriers and suggests that new capacity additions, particularly in Europe, will be skewed toward bio-based molecules. Toluene and benzene segments continue to contract in advanced economies due to workplace exposure limits, whereas acetone benefits from cross-sector versatility, shielding it from steep declines.

By Application: Electronic Equipment Emerges as Growth Engine

Oil and Gas remained the single largest end-use, capturing 28.03% of the aprotic solvents market size in 2025 as unconventional drilling spread into deeper reservoirs. These downhole environments demand thermal-stable dipolars that deliver viscosity control where water-based systems fail. Investment in steam-assisted gravity drainage and high-density completion fluids supports ongoing consumption, but cumulative volume growth is modest because process optimization curbs per-well solvent usage. Pharmaceuticals are leveraging peptide drug demand and the proliferation of continuous-flow reactors that improve yield yet still require large solvent make-up volumes.

Electronic Equipment outpaced all other segments with a 3.78% CAGR outlook to 2031. Each advanced logic chip involves over 500 distinct process chemicals, and ultra-clean aprotic solvents are integral to immersion lithography, residue stripping, and wafer edge cleaning. The CHIPS Act incentives bring fresh capacity online in the United States, triggering supplier qualification programs that favor long-term contracts. Emerging chiplet architectures and high-bandwidth memory stacks require narrower impurity windows, increasing solvent value-added content. Plastics, Paints and Coatings, and Adhesives maintain baseline demand yet experience margin pressure because industry clients substitute lower-hazard alternatives where feasible.

Geography Analysis

Asia-Pacific held 53.15% of global revenue in 2025 and is projected to record a 3.55% CAGR through 2031, anchored by China’s rapidly expanding battery value chain and Japan’s targeted investments in electrolyte production. Gigafactory clusters around Sichuan, Guangdong, and Jiangsu provinces secure upstream DMC and EMC supply, which drives intra-regional solvent trade flows. Policy support for domestic semiconductor capacity further broadens the user base for high-purity variants. Nevertheless, process innovation, such as kosmotropic aqueous cathode slurry processing that cuts solvent intensity by 96% could erode long-term volume dependence.

North America is driven by CHIPS Act-driven fab construction and sustained shale output that relies on aprotic drill fluids. The buildout of a 160 kiloton per year propylene oxide plant in Texas improves backward integration for acetone co-product streams. Pharmaceutical greenfield projects in Colorado and Massachusetts, specializing in GLP-1 APIs, add another solvent offtake node while regional distributors consolidate to streamline logistics.

Europe experiences the sharpest regulatory overhang as REACH restrictions tighten reproductive toxicity thresholds. Producers respond by installing closed-loop recovery equipment that reaches 95% capture and 99% purity, as showcased by turnkey systems achieving payback in under three years. Large integrated firms still invest, evidenced by BASF’s alkyl ethanolamine plant in Antwerp delivering 140,000 tons per year capacity. Europe’s influence as a regulatory trendsetter accelerates global harmonization around safer solvents, reshaping future product portfolios.

Competitive Landscape

Global supply is moderately fragmented. Vertical integration into petrochemical feedstocks grants BASF, Dow, and INEOS scale advantages and refinery-grade naphtha access critical for cost leadership. Competitive success hinges on secure feedstock access, proprietary purification technology, and the agility to meet emerging sustainability criteria. Supply-chain resilience measures, including regional storage hubs and redundant production nodes, gain prominence as geopolitical uncertainties rise. Corporate climate pledges push firms toward green-power procurement and Scope 3 emission accounting, making end-to-end transparency a procurement prerequisite.

Aprotic Solvents Industry Leaders

Dow

Eastman Chemical Company

BASF

INEOS

LyondellBasell Industries Holdings B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: BASF has announced a price increase of USD 0.10 per pound for N-Methyl-2-Pyrrolidone. The adjustment applies to all sales in the United States and Canada.

- January 2025: INEOS Phenol disclosed the permanent closure of its high-cost Gladbeck, Germany, phenol and acetone (an aprotic solvent) site, citing energy and CO₂ costs.

Global Aprotic Solvents Market Report Scope

The word protic means "proton", and aprotic means "no proton". The solvents with no hydrogen atom or bond are said to be aprotic solvents. Aprotic solvents have large dielectric constants and large dipole moments. However, they do not participate in hydrogen bonding. Their high polarity allows them to dissolve charged species such as various anions, including nucleophiles. Thus, these solvents are more reactive in nature. The aprotic solvents market is segmented by type, application, and geography. By type, the market is segmented into n-methyl-2-pyrrolidone (NMP), toluene, benzene, acetone, and others. By application, the market is segmented into oil and gas, plastic, pharmaceutical, electronic equipment, paints and coatings, adhesives, and others. The report also covers the market size and forecasts for the aprotic solvents market in 15 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of revenue (USD million).

| N-Methyl-2-Pyrrolidone (NMP) |

| Toluene |

| Benzene |

| Acetone |

| Other Types (Propylene Carbonate, Bio-based, etc.) |

| Oil and Gas |

| Pharmaceuticals |

| Plastics |

| Electronic Equipments |

| Paints and Coatings |

| Adhesives |

| Other Applications (Polymer and Plastics Processing, etc.) |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | N-Methyl-2-Pyrrolidone (NMP) | |

| Toluene | ||

| Benzene | ||

| Acetone | ||

| Other Types (Propylene Carbonate, Bio-based, etc.) | ||

| By Application | Oil and Gas | |

| Pharmaceuticals | ||

| Plastics | ||

| Electronic Equipments | ||

| Paints and Coatings | ||

| Adhesives | ||

| Other Applications (Polymer and Plastics Processing, etc.) | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the current size of the aprotic solvents market?

The aprotic solvents market size reached USD 20.24 billion in 2026 and is projected to climb to USD 23.47 billion by 2031.

Which region holds the largest share of aprotic solvent demand?

Asia-Pacific accounts for 53.15% of global volume, led by China’s battery gigafactories and Japan’s electrolyte investments.

Why does N-Methyl-2-Pyrrolidone (NMP) remain dominant despite regulations?

NMP delivers unmatched cathode-slurry rheology and polymer compatibility, making immediate substitution in lithium-ion batteries technically difficult.

Which application segment is growing the fastest?

Electronic equipment, driven by semiconductor fabs and CHIPS Act incentives, is expanding at a 3.78% CAGR through 2031.

How are bio-based solvents impacting the market?

Commercial launches of Cyrene and gamma-valerolactone offer lower-toxicity drop-in alternatives, driving the “Other Types” segment at a 3.70% CAGR.

Page last updated on: