Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

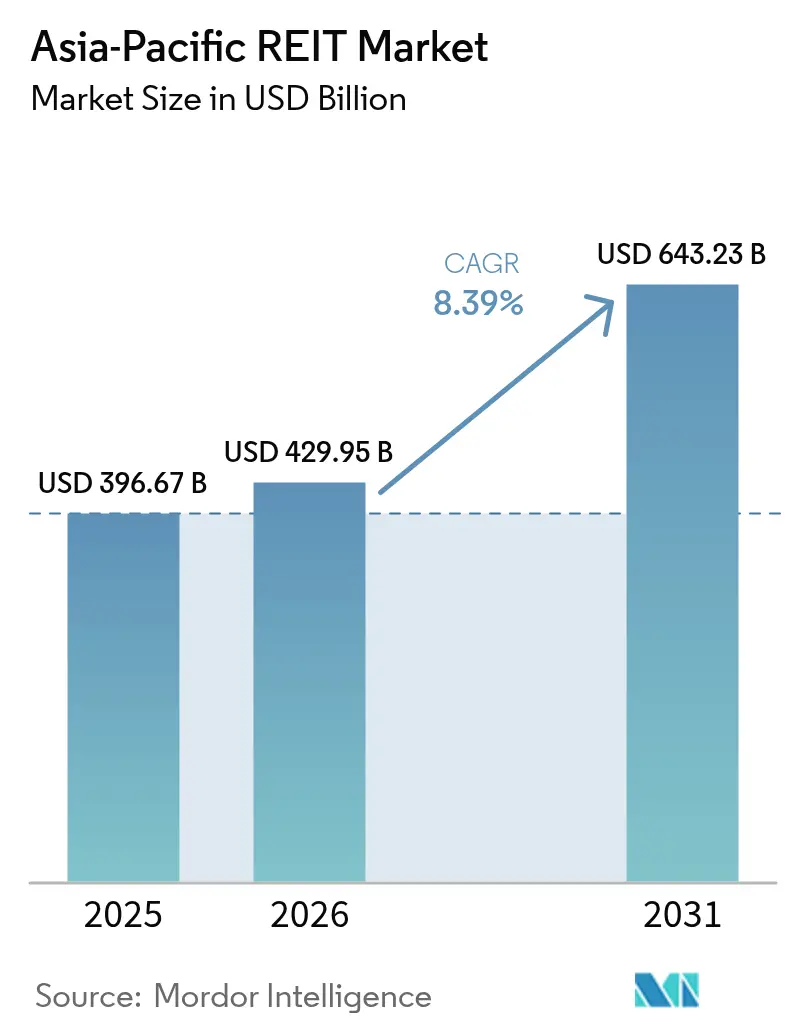

| Base Year Market Size (2025) | USD 396.67 Billion |

| Market Size (2026) | USD 429.95 Billion |

| Market Size (2031) | USD 643.23 Billion |

| Growth Rate (2026 - 2031) | 8.39% CAGR |

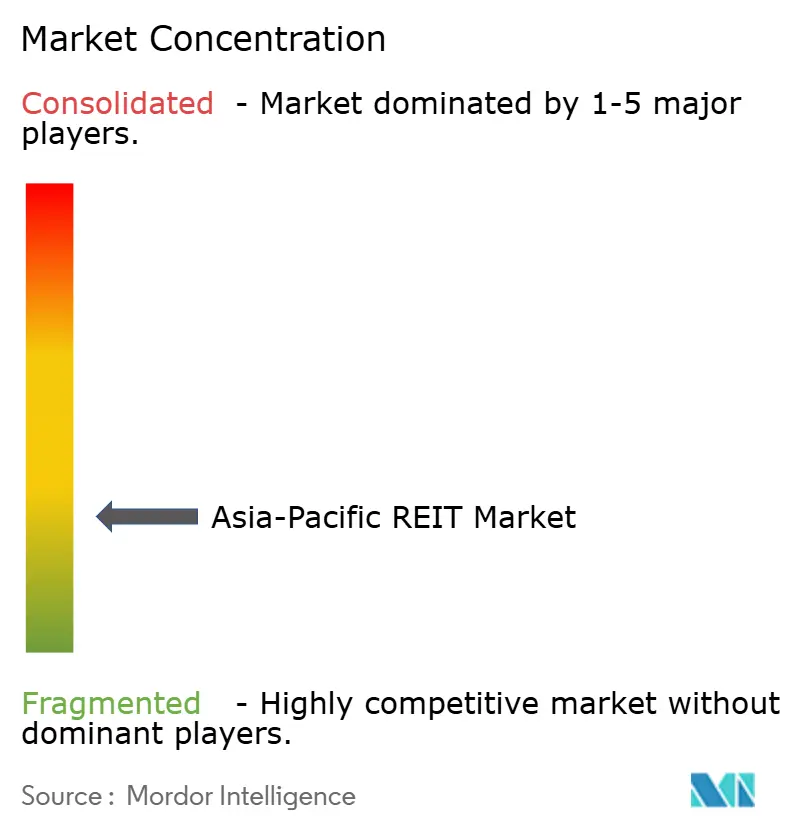

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific REIT Market Analysis by Mordor Intelligence

The Asia-Pacific REIT market size was valued at USD 396.67 billion in 2025 and estimated to grow from USD 429.95 billion in 2026 to reach USD 643.23 billion by 2031, at a CAGR of 8.39% during the forecast period (2026-2031). Strong capital reallocation by sovereign wealth funds, favorable regulatory tweaks that expand gearing headroom, and an accelerating shift toward digital infrastructure all underpin this growth trajectory. Cross-border investment flows into listed trusts rebounded on the back of widening yield spreads over government bonds, while accommodative monetary settings in Japan and selective easing cycles elsewhere tempered refinancing risk in early 2025. Policymakers across Singapore, India, and China continued to refine tax pass-through rules and listing frameworks, creating scalable entry points for both domestic and foreign sponsors. At the same time, ESG index inclusion requirements prompted sizable green-bond issuance and retrofit programs, reinforcing asset quality and broadening the investor base. Market participants also cited the privatization pipeline for data centers and telecom towers as a multi-year acquisition engine that should help sustain distribution growth despite pockets of interest-rate volatility.

Key Report Takeaways

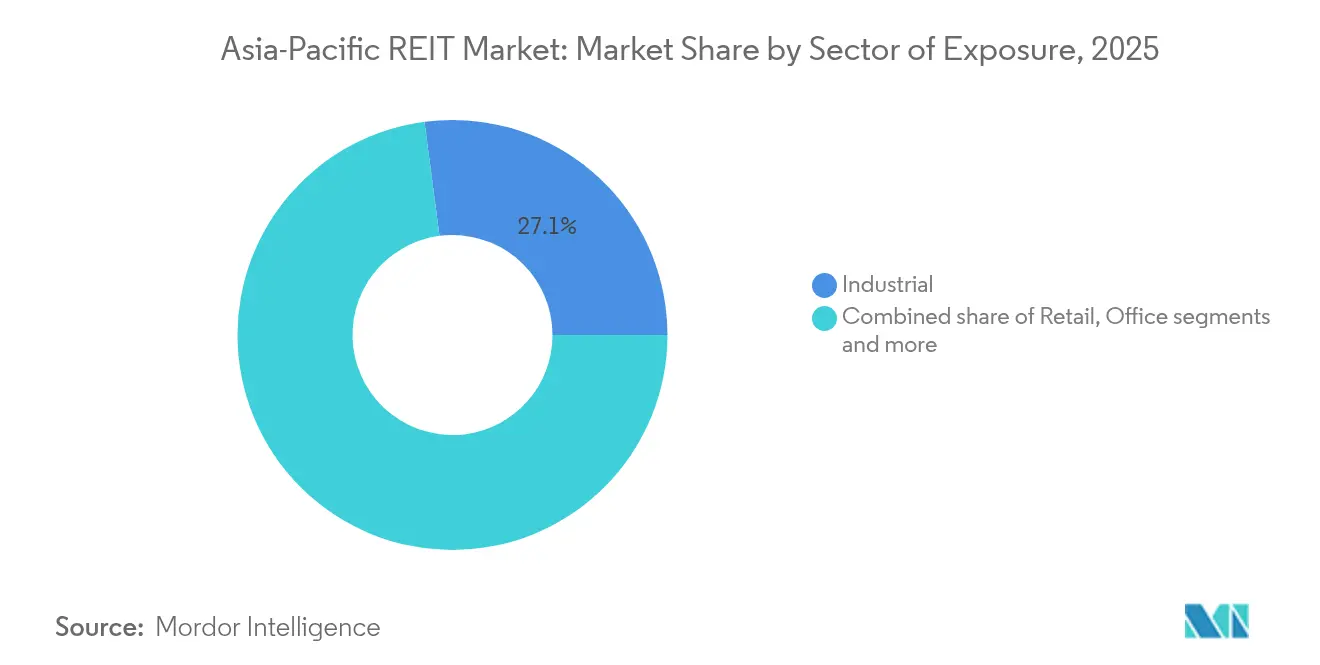

- By sector, industrial logistics assets led with 27.08% of the Asia-Pacific REIT market share in 2025; data centers are projected to expand at a 13.95% CAGR to 2031.

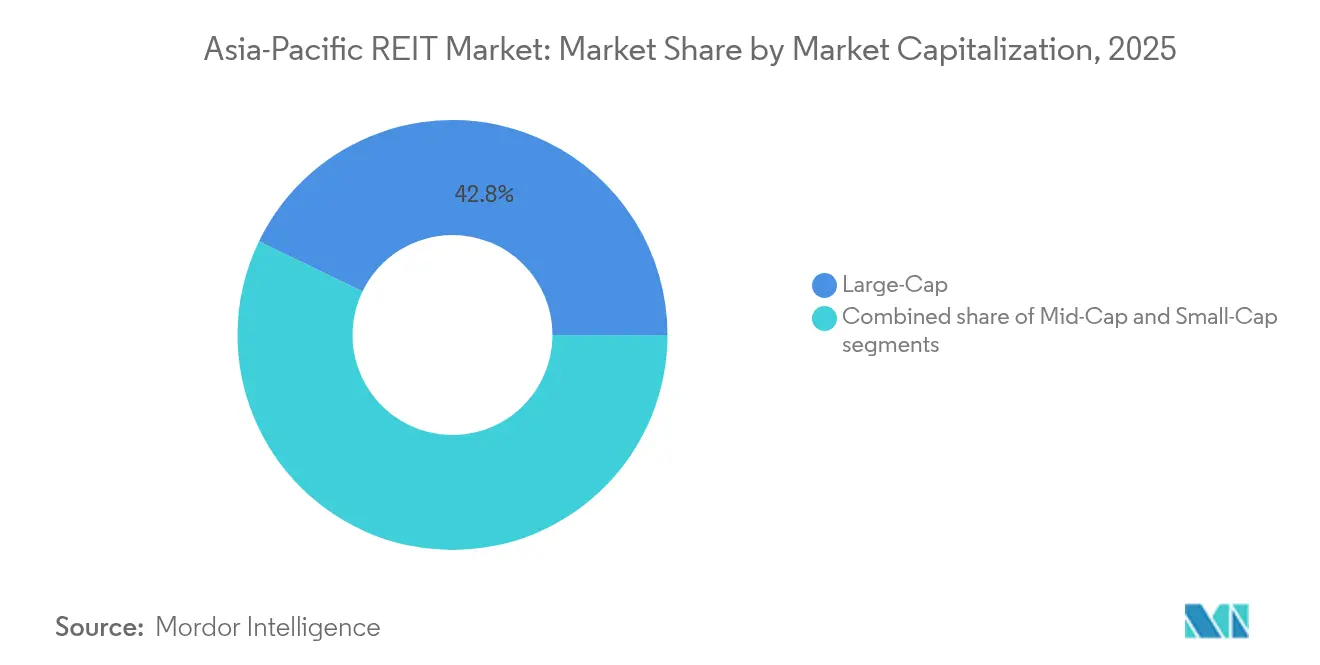

- By market capitalization, the large-cap cohort held 42.82% of the Asia-Pacific REIT market share in 2025, while the small-cap cohort is forecast to grow at a 10.22% CAGR through 2031.

- By geography, Japan accounted for 24.15% of the Asia-Pacific REIT market size in 2025, and India is advancing at an 11.07% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific REIT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising institutional allocations to listed property | +1.8% | Pan-regional | Medium term (2-4 years) |

| Supportive tax and REIT-enabling regulation | +1.2% | Singapore, India, Japan, Australia | Long term (≥ 4 years) |

| Surging e-commerce and urban logistics demand | +2.1% | China, India, Southeast Asia | Short term (≤ 2 years) |

| Portfolio diversification by pension and SWF capital | +1.5% | Global inflows to APAC | Medium term (2-4 years) |

| ESG index inclusion and green-financing channels | +0.9% | Core APAC with EU spillover | Long term (≥ 4 years) |

| Digital-infrastructure privatization pipeline | +1.0% | China, India, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Institutional Allocations to APAC REITs

Sovereign wealth funds and pension systems are systematically increasing APAC REIT allocations as part of broader portfolio diversification mandates. Cross-regional investment flows into Asia-Pacific surged 221% year-over-year in H2 2024, with institutional investors attracted by yield spreads averaging 130-133 basis points above risk-free rates[2]“Asia-Pacific Real Estate Market Outlook 2024,” CBRE, cbre.com. Singapore's Government Investment Corporation and Malaysia's Employees Provident Fund have expanded REIT exposure through both direct holdings and co-investment vehicles, while Australian superannuation funds allocated USD 2.82 billion (AUD 4.4 billion) to regional property securities in 2024. This institutional capital influx provides stable funding sources for REIT expansion and acquisition activity, particularly benefiting large-cap vehicles with established track records and diversified asset portfolios.

Supportive REIT-Enabling Regulations & Tax Incentives

Regulatory harmonization across APAC jurisdictions is reducing structural barriers to REIT formation and cross-border investment. Singapore's Monetary Authority introduced enhanced leverage flexibility for REITs in 2024, allowing temporary increases to 50% debt-to-assets for strategic acquisitions, while maintaining prudential oversight through quarterly reporting requirements[3]“MAS enhances REIT leverage framework,” Monetary Authority of Singapore, mas.gov.sg. India's Securities and Exchange Board implemented Small and Medium REIT regulations, enabling smaller property portfolios to access public markets, with Knowledge Realty Trust's USD 576 million IPO demonstrating investor appetite for Grade A office exposure. Japan's revised J-REIT taxation framework provides additional depreciation allowances for energy-efficient retrofits, supporting portfolio modernization initiatives across the sector.

Surging E-commerce & Urban Logistics Demand

Digital commerce expansion continues driving logistics real estate demand across APAC markets, with Indonesia projecting data center capacity growth from 150 MW to 1 GW by 2030[4]“Indonesia data-center capacity to reach 1 GW by 2030,” Indonesia-Investments, indonesia-investments.com. Goodman Group exemplifies this trend, with data centers comprising over 50% of its USD 13.7 billion work-in-progress pipeline and new projects in Hong Kong and Los Angeles targeting yield-on-cost returns around 9%. Urban logistics facilities command premium rents due to last-mile delivery requirements, with Singapore and Hong Kong warehouse rents increasing 8-12% annually as supply constraints intersect with e-commerce fulfillment needs. This sector benefits from long-term lease structures and built-to-suit development opportunities that provide predictable cash flows for REIT investors.

Portfolio-Diversification Hunger Among Pension & SWF Investors

Institutional investors are expanding APAC REIT allocations to reduce geographic concentration risk and capture yield premiums unavailable in developed markets. Australian superannuation funds increased international property exposure by 15% in 2024, while Canadian pension plans allocated USD 2.04 billion (CAD 2.8 billion) to Asia-Pacific real estate securities. This diversification drive particularly benefits healthcare and senior living REITs, with Parkway Life REIT's European expansion through €111.2 million French nursing home acquisitions demonstrating cross-border growth strategies. The aging demographic trend across developed Asia creates structural demand for specialized healthcare real estate, with Japan's 65+ population projected to reach 25% by 2065.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interest-rate volatility lifts funding costs | -2.3% | Global | Short term (≤ 2 years) |

| Foreign-ownership caps in select markets | -0.8% | China, Thailand, Malaysia | Long term (≥ 4 years) |

| Transition-risk CAPEX for aging non-green stock | -1.1% | Japan, Australia, Singapore | Medium term (2-4 years) |

| FX-mismatch risk on cross-border portfolios | -0.7% | Pan-regional | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising institutional allocations to listed property

Interest-rate volatility poses a significant restraint on the Asia-Pacific REIT market by inflating the overall cost of capital, making it more expensive for REITs to finance acquisitions, developments, or refinancing activities. As regional central banks adjust monetary policy in response to global inflationary pressures and geopolitical uncertainty, frequent and unpredictable rate shifts create challenges for long-term financial planning and capital allocation. Elevated borrowing costs can deter REITs from pursuing growth strategies, such as expanding their portfolios or undertaking value-enhancing redevelopment projects, due to thinner spreads and lower return prospects. Moreover, volatility in rates undermines investor confidence, as rising yields on government bonds and other fixed-income instruments erode the relative attractiveness of REIT dividend distributions. This dynamic often results in capital outflows, valuation pressures, and reduced liquidity across the REIT sector.

Supportive tax and REIT-enabling regulation

Foreign-ownership caps in select Asia-Pacific markets act as a structural barrier to broader investor participation and capital inflows. These regulatory limits, often designed to protect domestic interests or maintain economic sovereignty, restrict the percentage of REIT units that non-resident investors can hold. As a result, foreign institutional investors who are typically key drivers of liquidity and long-term capital may be deterred from entering or expanding their positions in these markets. It limits the pool of available capital and reduces competitive pressure on REITs to improve governance, transparency, and performance standards. Additionally, foreign-ownership restrictions can contribute to lower trading volumes and suppressed valuations, particularly in emerging REIT markets where local investor bases are still developing. In the long term, unless regulatory reforms are introduced, these caps could hinder cross-border investment, slow market maturation, and reduce the Asia-Pacific REIT sector’s global competitiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector of Exposure: Data centers accelerate digital transformation

Industrial logistics retained leadership with 27.08% share of the Asia-Pacific REIT market size in 2025, reflecting the structural need for cross-border e-commerce fulfillment capacity. Data-center REITs, although still a smaller slice of the pie, are projected to log the fastest 13.95% CAGR through 2031 as artificial-intelligence workloads fuel hyperscale leasing demand. The Asia-Pacific REIT market benefits from the region’s distinct scarcity of institutional-grade server farms, with power and land permits acting as entry barriers. Retail malls remained the largest absolute contributor at 29.18% but saw muted rent reversions compared with logistics. Office landlords continued to pivot toward flexible-floor plates and wellness retrofits to defend occupancy above 90% in CBD corridors, whereas healthcare trusts drew support from aging demographics and government spending. Diversified vehicles used internal capital recycling to tilt portfolios toward sectors with stronger NOI growth, cushioning distribution yields against cyclical headwinds.

Longer-dated power purchase agreements in data-center portfolios offer quasi-infra cash flow that commands premium valuations. Industrial warehouse landlords such as Goodman Group are embedding solar generation on-site, forging a natural ESG hedge. Retail REITs concentrated in essential-services sub-regional centers have outperformed discretionary mall peers on footfall recovery. Healthcare assets—particularly acute-care hospitals and stabilized nursing homes—carry yield spreads above 250 basis points to comparable office stock, making them attractive to yield-oriented investors. The multi-track nature of sector performance underscores why diversified strategies inside the Asia-Pacific REIT market can mitigate single-asset-class volatility.

By Market Capitalization: Small-cap outperforms in growth but large-cap owns liquidity

Large-cap names accounted for 42.82% of the Asia-Pacific REIT market share in 2025, anchored by platforms such as Link REIT and Goodman Group that each manage multi-jurisdiction portfolios. These giants enjoy lower funding costs-often 30-40 basis points inside small-cap peers-owing to better credit ratings and deep shareholder registers. Small-cap vehicles, however, are expected to advance at a 10.22% CAGR through 2031 as they capitalize on specialized niches-student housing in Japan, cold-storage warehouses in Malaysia, and boutique data hubs in India. Mid-cap trusts, sitting at roughly 34.7% market weight, balance external growth via acquisitions with internal value-add initiatives such as asset enhancement and cost-of-capital optimization.

Liquidity remains the key discriminator. Large-caps trade at an average free-float velocity of 0.8x compared with 0.2x for small-caps, a factor that keeps exchange-traded fund (ETF) inflows skewed toward the former. Yet, alpha-seeking active managers continue to mine the Asia-Pacific REIT industry for under-covered microcaps that can re-rate once they cross the USD 2 billion threshold. Private equity real-estate sponsors increasingly view take-private transactions as a pathway to turbo-charge growth strategies before re-listing assets at a larger scale.

Geography Analysis

Japan’s J-REIT universe delivers a stable 24.15% market share due to long-lease office and retail assets in Tokyo and Osaka. Distribution yields hover near 3.70%, a spread of 310 basis points over five-year JGBs, though analysts caution that a 50–75 basis-point lift in base rates could shave 7% off annual distributable income. Sponsors are proactively disposing of noncore assets and locking in fixed-rate debt tenors to preserve payout ratios. Industrial heavyweights are also experimenting with sustainability-linked loans to diversify funding channels. Australia’s platform boasts a 24.03% share on the back of deeply liquid capital markets and compulsory pension inflows. Goodman Group’s USD 13.7 billion work-in-progress pipeline is more than 50% allocated to data centers, underscoring how industrial landlords are evolving into infrastructure hybrids. Retail-anchored Scentre Group reported 99% occupancy despite weak discretionary spending, aided by a tilt toward service tenants.

India captured 13% of Grade-A office stock via publicly listed trusts by the end of 2024. The Asia-Pacific REIT market outlook for the country is underpinned by 70 million sq ft of annual gross leasing, the highest in the region. New SME-REIT rules lower the minimum asset value threshold to INR 0.5 billion, catalyzing listings from regional developers. Knowledge Realty Trust’s planned INR 48 billion IPO could lift the free-float market cap for India-listed vehicles by nearly 30%, accelerating index inclusion.

Potential headwinds include rising land-acquisition costs and a patchwork of state stamp duties that erode headline yields. China’s infrastructure-focused C-REIT segment leapt to USD 75.35 billion (RMB 550 billion) in market cap after the second batch of offerings in March 2025 targeted power-grid and cold-chain logistics assets. While foreign ownership remains capped, cross-border feeder funds are exploring quota allocations under Qualified Foreign Institutional Investor (QFII) rules to tap into the higher-growth domestic names. Currency volatility remains manageable as revenue streams are largely RMB-denominated against RMB debt.

Competitive Landscape

The Asia-Pacific REIT market is moderately concentrated but remains competitively fragmented, offering room for consolidation and strategic specialization. The leading REITs hold a significant portion of total market share, yet many mid-tier players create space for mergers and focused sector plays. Market leadership often reflects geographic strengths, with some REITs dominating retail and car park segments in key urban centers, while others lead in industrial or logistics assets across multiple countries. This landscape allows regional champions to emerge based on localized expertise and asset performance. As a result, the market presents both scale-driven and niche-focused growth opportunities.

Strategic differentiation is increasingly based on sector specialization and depth of operational capability. REITs focused on data centers are seeing stronger investor demand, driven by rising AI adoption and power infrastructure constraints. Industrial-focused REITs are developing large-scale capacity and high pre-leasing rates, while others concentrate solely on mission-critical digital infrastructure across Asia-Pacific. Geographic diversification is also becoming a key strategy, with some REITs expanding into healthcare assets in Europe or integrating regional platforms to optimize asset portfolios. These moves support portfolio resilience and help access broader pools of international capital.

Technology integration and strong ESG compliance have shifted from being value-add features to baseline requirements. Institutional investors now expect detailed sustainability disclosures, operational efficiency reporting, and evidence of climate-aligned investment strategies. Leading REITs are responding with measurable environmental targets, renewable energy investments, and sustainability initiatives to align with global benchmarks. At the same time, market consolidation is likely in fragmented segments such as healthcare and student housing, where achieving operational scale can attract institutional backing. Ultimately, management expertise and alignment with evolving investor expectations will define the next wave of market leaders in the region.

Asia-Pacific REIT Industry Leaders

-

Link REIT

-

Goodman Group

-

Ascendas REIT

-

Nippon Building Fund

-

Scentre Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CapitaLand Ascendas REIT completed a SGD 500.0 million private placement of 202.4 million new units at USD 1.81 billion each, with proceeds earmarked for strategic acquisitions and portfolio enhancement initiatives across Singapore and regional markets.

- May 2025: Goodman Group raised approximately USD 2.82 billion (AUD 4.4 billion) through institutional placement and retail offer to fund data center development pipeline expansion, with work-in-progress reaching USD 13.7 billion and data centers comprising over 50% of total development activity.

- March 2025: Dexus Research identified falling interest rates and stabilizing property values as key drivers for Australian commercial real estate recovery, with retail and industrial sectors showing the strongest resilience and transaction volumes rising 19% year-over-year in 2024.

- February 2025: Link REIT acquired the remaining 50% stake in Qibao Vanke Plaza, Shanghai, for USD 326.06 million (RMB 2.38 billion) at a 26.3% discount to the prior appraisal, demonstrating an opportunistic acquisition strategy amid Chinese market repricing.

Asia-Pacific REIT Market Report Scope

A real estate investment trust (REIT) is a publicly traded company that owns, operates, or finances income-producing properties. An understanding of the Asia Pacific REIT industry, regulatory environment, REITs, and their business models, along with detailed market segmentation, product types, revenues and dividends, current market trends, changes in market dynamics, and growth opportunities, are covered in the report. An in-depth analysis of the market size and forecast for the various segments is also provided in the report.

The Asia-Pacific REIT industry is segmented by type, application, and country. By type, the market is segmented as industrial, residential, and commercial. By application, the market is segmented as warehouses and communication centers, self-storage facilities, and data centers, among others. By country, the market is segmented as China, Australia, Japan, India, Singapore, South Korea, Malaysia, and the rest of Asia-Pacific.

The report offers market size and forecasts for the Asia-Pacific REIT industry in value (USD) for all the above segments.

By Sector of Exposure

| Retail |

| Industrial |

| Office |

| Residential |

| Diversified |

| Other Sectors |

| Data Centers |

| Healthcare |

By Market Capitalization

| Large-Cap (more than USD 10 billion) |

| Mid-Cap (USD 2–10 billion) |

| Small-Cap (less than USD 2 billion) |

By Geography

| India |

| China |

| Japan |

| Australia |

| South Korea |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) |

| Rest of Asia-Pacific |

| By Sector of Exposure | Retail |

| Industrial | |

| Office | |

| Residential | |

| Diversified | |

| Other Sectors | |

| Data Centers | |

| Healthcare | |

| By Market Capitalization | Large-Cap (more than USD 10 billion) |

| Mid-Cap (USD 2–10 billion) | |

| Small-Cap (less than USD 2 billion) | |

| By Geography | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines) | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large is the Asia-Pacific REIT market in 2026?

The Asia-Pacific REIT market size reached USD 429.95 billion in 2026 and is projected to grow at an 8.39% CAGR to 2031.

Which segment is expanding fastest?

Data-center REITs are forecast to post a 13.95% CAGR through 2031 owing to AI-driven demand for hyperscale capacity.

Why are institutional investors increasing exposure?

Yield spreads over government bonds and supportive tax frameworks are drawing sovereign wealth and pension funds into the region’s listed trusts.

What is the main regulatory tailwind?

Measures such as Singapore’s higher leverage cap and India’s SME-REIT rules have lowered structural barriers and improved cash yields.

Which geography is the fastest-growing?

India is expected to record an 11.07% CAGR through 2031, propelled by robust office absorption and new listing guidelines.

How significant are ESG considerations?

ESG index inclusion is driving substantial green-bond issuance and retrofit spending, lowering borrowing costs and broadening the investor base.

Page last updated on: