Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

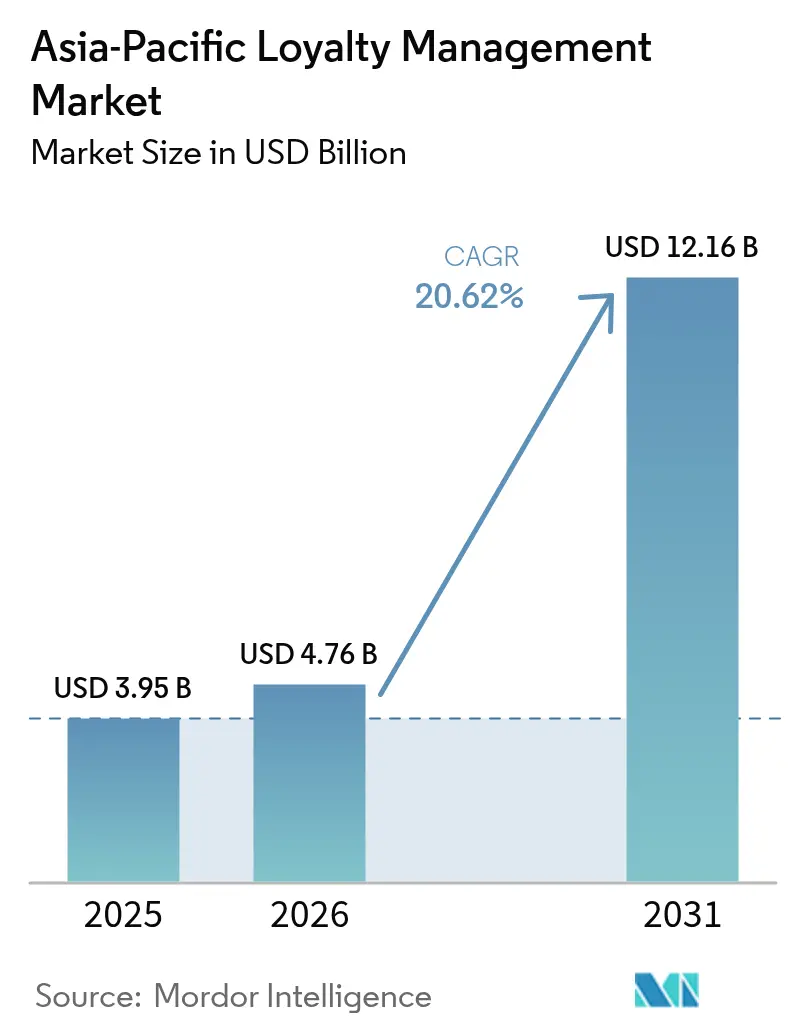

| Base Year Market Size (2025) | USD 3.95 Billion |

| Market Size (2026) | USD 4.76 Billion |

| Market Size (2031) | USD 12.16 Billion |

| Growth Rate (2026 - 2031) | 20.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Loyalty Management Market Analysis by Mordor Intelligence

The Asia-Pacific loyalty management market size is expected to grow from USD 3.95 billion in 2025 to USD 4.76 billion in 2026 and is forecast to reach USD 12.16 billion by 2031 at 20.62% CAGR over 2026-2031. Sustained double-digit growth springs from rapid digital payments adoption, cloud-native platform roll-outs, and government investment in real-time payment rails that make rewards issuance and redemption instantaneous. Financial-services incumbents intensify spending on AI-driven loyalty engines to arrest customer attrition, while retailers experiment with coalition models that share acquisition costs and unlock cross-brand insights. Interoperable QR codes and super-app ecosystems compress the distance between purchase and reward, vaulting mobile-first programs ahead of plastic card predecessors. Simultaneously, data-privacy legislation pushes vendors toward privacy-by-design architectures that embed consent orchestration from the ground up. Venture funding remains buoyant as private-equity investors back tokenized rewards and generative-AI orchestration layers that promise hyper-personalized value exchanges.

Key Report Takeaways

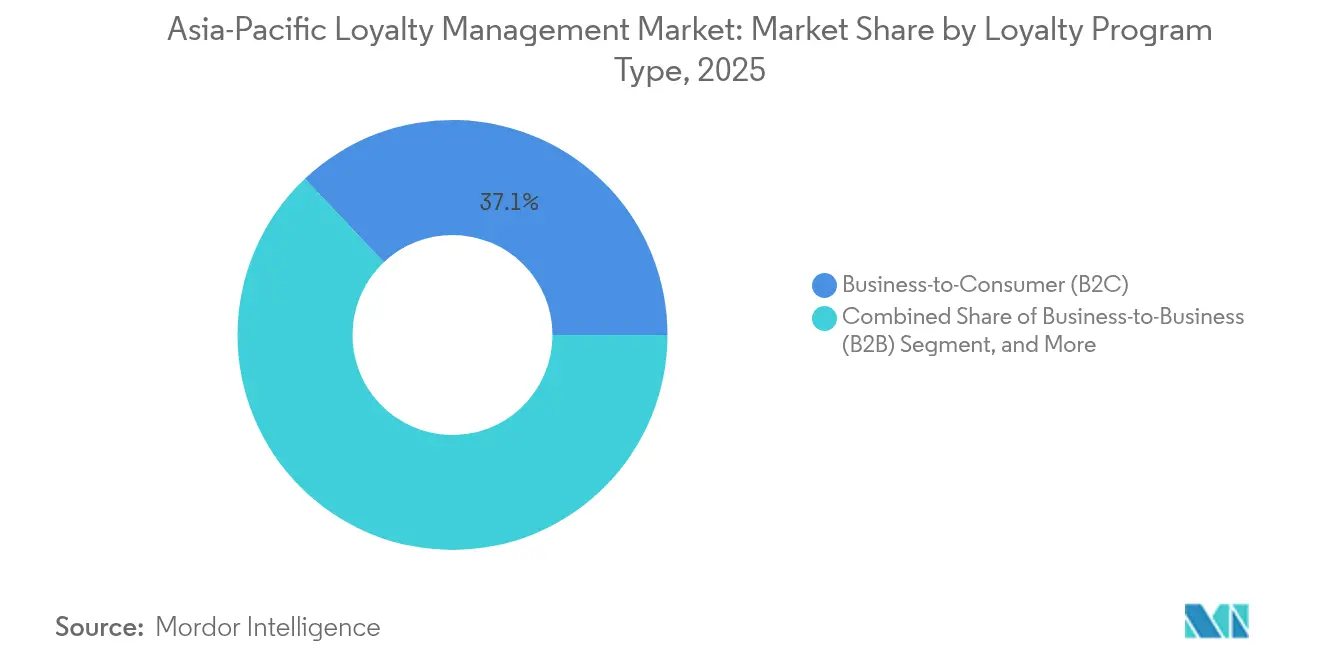

- By loyalty program type, business-to-consumer schemes held 37.05% of the Asia-Pacific loyalty management market share in 2025, while coalition and multipartner programs are expected to grow at a 21.13% CAGR through 2031.

- By component, software captured a 56.82% share of the Asia-Pacific loyalty management market size in 2025, while services are projected to advance at a 21.45% CAGR through 2031.

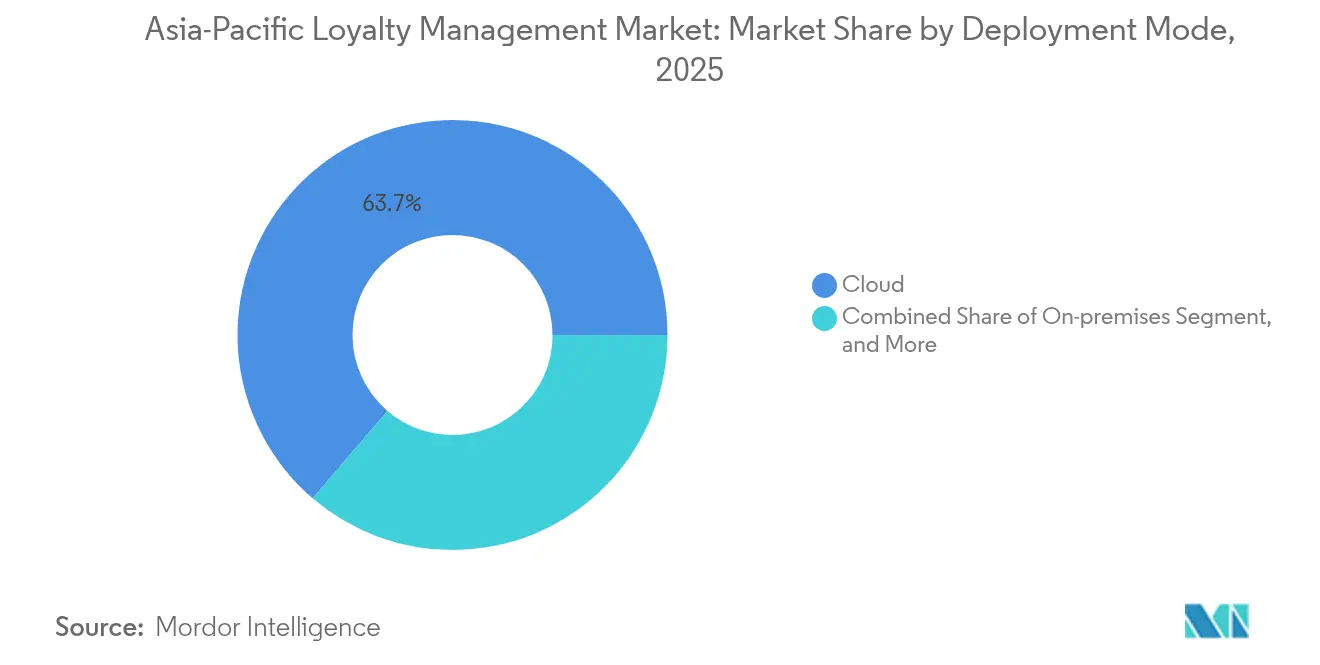

- By deployment mode, cloud led with a 63.73% revenue share in 2025 in the Asia-Pacific loyalty management market and is forecast to post a 21.68% CAGR through 2031.

- By end-user vertical, BFSI commanded 29.52% share of the Asia-Pacific loyalty management market size in 2025, while healthcare and pharmaceuticals record the fastest projected 21.06% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Loyalty Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of e-commerce and digital payments | +4.2% | Asia-Pacific-wide, strongest in China, India, Southeast Asia | Medium term (2-4 years) |

| Rapid smartphone penetration and mobile wallets | +3.8% | India, Indonesia, Philippines, Vietnam core markets | Short term (≤ 2 years) |

| Intensifying retail-bank competition for retention | +3.1% | Singapore, Australia, Japan, South Korea | Long term (≥ 4 years) |

| Advances in cloud-based loyalty tech platforms | +2.9% | Global, early adoption in Singapore, Australia | Medium term (2-4 years) |

| Interoperable QR / real-time payment rails (Govt-led) | +2.7% | Thailand, India, Malaysia, Singapore | Short term (≤ 2 years) |

| Loyalty-as-a-Service lowering SME entry barriers | +2.4% | Asia-Pacific emerging markets, SME-dense regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Proliferation of E-commerce and Digital Payments

Digital marketplaces multiply reward-eligible touchpoints, turning each checkout into a data-rich loyalty moment. Alipay Tap! surpassed 100 million users in 2024, demonstrating how super-apps can seamlessly integrate earn-and-burn loops into everyday payments.[1]Alipay, “Tap! Program Reaches 100 Million Users,” alipay.com India’s Unified Payments Interface enables instant point-to-point transfers between banks and merchants, reducing settlement cycles from days to seconds.[2]National Payments Corporation of India, “UPI Monthly Statistics 2025,” npci.org.in Coalition programs thrive because shared payment rails eliminate technical friction, allowing shoppers to redeem across verticals without additional logins. These real-time connections feed machine-learning models that refine offers with each swipe, boosting cart-conversion rates as personalization accuracy improves. Cloud-native loyalty engines dominate since only microservice architectures can orchestrate the high-velocity data streams generated by omnichannel checkouts.

Rapid Smartphone Penetration and Mobile Wallets

More than 82% of adults in Indonesia and 79% in the Philippines are expected to own a smartphone by 2026, providing merchants with a direct line to shoppers who were previously cash-only.[3]GSMA, “The Mobile Economy Asia Pacific 2025,” gsma.com OVO’s integration with Superbank shows how mobile wallets can layer card-free loyalty on top of savings and credit products, turning payments data into predictive churn alerts. In Malaysia, buy-now-pay-later apps reward early repayments with extra points, illustrating how embedded finance expands the scope of engagement beyond traditional retail coupons. Mobile-first strategies, especially for small merchants, benefit from white-label wallet SDKs, which enable them to launch QR-based rewards without building proprietary apps. As handset penetration surpasses legacy card infrastructure in rural areas, loyalty-as-a-service vendors capture a first-mover advantage by provisioning turnkey mobile journeys in weeks rather than months.

Intensifying Retail-Bank Competition for Retention

Asia-Pacific banks face compressing net-interest margins and treat loyalty as a defensive moat. DBS Bank operates over 800 AI models that transform transaction histories into targeted product recommendations, increasing cross-sell rates among millennial segments.[4]DBS Bank, “AI@DBS Use Case Library,” dbs.com Lifestyle coalitions between banks, airlines, and gyms deepen customer lock-in by rewarding everyday spending with travel perks and wellness upgrades. White-label platform providers profit as mid-tier lenders license ready-made engines instead of building in-house stacks. Regulatory hurdles surrounding the safeguarding of depositor data elevate entry barriers, giving incumbents with compliance credentials a head start. Over the long term, open-banking mandates are expected to nudge rivals into interconnected ecosystems where loyalty data and payment data co-mingle to boost share of wallet.

Advances in Cloud-Based Loyalty Tech Platforms

Shift to micro-services dismantles monolithic legacy systems, trimming time-to-market for new reward rules from weeks to hours. SAP Emarsys reports that Asia-Pacific retailers deploying cloud loyalty flows saw 37% faster campaign iteration during 2024. Auto-scaling clusters accommodate festival shopping spikes without the capital outlay of on-premise servers, and built-in geo-replication satisfies data-localization clauses in Singapore and India. Coalition operators depend on cloud hubs to run shared ledgers that reconcile points in real time across dozens of brands. Vendors offering region-specific data-residency zones win business from global apparel chains that must keep Indian customer records inside national borders. Reliance on hyperscalers does raise concentration risk, prompting procurement teams to demand multi-cloud failover strategies and stricter service-level clauses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy regulations and trust concerns | -2.8% | China, India, Singapore, Australia, Vietnam | Medium term (2-4 years) |

| Fragmented regulatory landscape across Asia-Pacific | -2.1% | Southeast Asia, cross-border operations | Long term (≥ 4 years) |

| Legacy POS / IT integration complexity | -1.9% | Japan, South Korea, Australia enterprise markets | Medium term (2-4 years) |

| Surge in loyalty-currency fraud via real-time wallets | -1.6% | India, Indonesia, Thailand, Philippines | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Regulations and Trust Concerns

China’s Personal Information Protection Law and Vietnam’s 2024 Data Decree require explicit consent for cross-border transfers, driving program operators to spin up local storage cluster. Compliance costs swell as privacy impact assessments become mandatory each time loyalty data flows between subsidiaries. Smaller vendors find legal retainers and certification audits onerous, surrendering deals to bigger rivals with established governance frameworks. Consumers grow wary after several high-profile breaches in Australia’s financial sector, trimming data-sharing opt-in rates for new app installs. In response, platforms bake consent receipts directly into wallet checkouts and publish transparent data-usage dashboards, turning privacy posture into a competitive differentiator rather than a simple checkbox.

Fragmented Regulatory Landscape Across Asia-Pacific

Where Singapore’s Payment Services Act defines e-money float limits, Thailand lacks equivalent clarity, forcing multi-country coalitions to maintain separate operating entities. Dentons notes that Australia’s wholesale CBDC sandbox, Project Acacia, could realign settlement models, yet leaves unanswered how tokenized points fit under existing consumer-credit rules. Compliance teams juggle divergent KYC thresholds, marketing-message opt-out windows, and tax reporting formats, adding layers of complexity with each geographic expansion. Economies of scale erode when every new market requires fresh legal reviews and localized terms of service. Regulatory sandboxes in Hong Kong and Malaysia offer experimentation leeway, yet permanent frameworks remain years away, elongating payback periods for cross-border investments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loyalty Program Type: Coalition Models Drive Cross-Platform Integration

The Asia-Pacific loyalty management market size for business-to-consumer programs stood at USD 1.46 billion in 2025, translating into 37.05% category share. Coalition and multipartner schemes are forecast to expand at a 21.13% CAGR through 2031 as consumers seek point portability and merchants aim to dilute acquisition costs. The Asia-Pacific loyalty management market share for coalition models is expected to climb steadily because standardized QR payment rails lower technical friction at checkout, allowing shoppers to redeem across supermarkets, fuel stations, and cinemas in one tap. Smaller retailers treat coalition participation as an affordable substitute for proprietary programs, leveraging shared customer-data lakes to refine inventory decisions and promotional calendars.

Second-order effects emerge as pharmaceutical wholesalers launch B2B coalitions that reward clinics for formulary adherence, illustrating how coalition architectures stretch beyond traditional consumer contexts. Employee-loyalty sub-segments see renewed interest among manufacturers that embed performance-based rewards into supply-chain dashboards, creating a virtuous loop between operational KPIs and workforce motivation. Business-to-business programs also adopt blockchain-anchored smart contracts to automate payout triggers once distributors hit quarterly sales thresholds. The interplay of these models signals a future where coalition logic underpins both customer and partner engagement strategies across the Asia-Pacific loyalty management market.

By Component: Services Growth Outpaces Software Platforms

Software platforms generated USD 2.24 billion in 2025, representing 56.82% of total revenue, yet services are on a faster 21.45% CAGR trajectory to 2031. Implementation consulting, regulatory compliance advisory, and managed operations top enterprise procurement checklists as organizations struggle to staff in-house loyalty teams. The Asia-Pacific loyalty management market size allocation toward services will widen further once new privacy laws trigger demand for data-protection audits and consent-workflow redesigns. Vendors specializing in regional compliance nuances win retainer contracts because they translate legal text into technical controls that pass regulator scrutiny.

Managed-service models gain ground among mid-market chains that lack the bandwidth to monitor campaign performance daily. Service partners take over A/B testing, reward-ledger reconciliation, and customer-support queues, charging outcome-based fees pegged to incremental revenue lift. As cloud platforms mature, software margins thin out, shifting negotiating power toward value-added consultancy. This component mix evolution aligns with a broader industry pivot from technology delivery to business-outcome accountability within the Asia-Pacific loyalty management industry.

By Deployment Mode: Cloud Dominance Accelerates

Cloud deployments captured 63.73% revenue in 2025 and are projected to grow at a 21.68% CAGR, cementing their position as the backbone of the Asia-Pacific loyalty management market. Low upfront capital, elastic scaling, and built-in patch management make cloud the default choice for enterprises rolling out region-wide programs. The Asia-Pacific loyalty management market size attributed to cloud is poised to top USD 8.17 billion by 2031. On-premise implementations persist only in defense, government, and certain financial institutions where statutory data-sovereignty clauses override cost calculus. Hybrid architectures emerge when conglomerates segment workloads by sensitivity, keeping personally identifiable information on-shore while offloading analytics to hyperscale clusters.

Cloud dominance fosters a flourishing marketplace of third-party micro-services, from gamification widgets to AI-driven offer engines, that plug into loyalty hubs via REST APIs. Enterprises appreciate how micro-service orchestration permits modular upgrades, letting them toggle new features without disrupting core ledgers. Latency concerns recede as CDN nodes proliferate across Tier-2 cities, ensuring real-time reward accrual even during flash sales. Still, reliance on stable connectivity makes fall-back offline modes vital in geographies prone to network outages, nudging providers to offer edge-caching options.

By End-User Vertical: Healthcare Emerges as Growth Leader

Banks, insurers, and fintechs together commanded 29.52% revenue share in 2025 due to entrenched reward-card ecosystems and high wallet transaction volumes. Yet healthcare and pharmaceuticals are forecast to be the fastest-growing vertical at a 21.06% CAGR as hospitals digitize patient journeys and drugmakers incentivize physician adherence to therapy protocols. The Asia-Pacific loyalty management market share generated by healthcare is expected to double by 2031, propelled by telemedicine, wearable-linked wellness points, and chronic-care adherence programs. Aging populations in Japan and Australia spur insurers to bundle preventive-health incentives with coverage renewals, pushing program complexity beyond simple point systems.

Consumer-goods manufacturers embrace data-rich collaborative campaigns that reward cross-brand basket combinations, turning supermarket scanners into loyalty enrollment touchpoints. Telecom operators extend points ecosystems to device-financing programs and streaming bundles, reinforcing stickiness in markets where prepaid churn remains high. Travel and hospitality rebound fuels renewed airline-hotel partnerships that layer flexible currencies atop dynamic-pricing engines, giving travelers more redemption optionality during peak seasons.

Geography Analysis

China and India collectively contribute more than 57.68% of Asia-Pacific loyalty management market revenue, powered by massive consumer bases and flourishing mobile-payment ecosystems. China’s super-app dominance lets users accrue points, pay bills, and trade vouchers within a single interface, condensing the purchase-to-reward cycle into seconds. India’s UPI rails deliver similar immediacy; the latest Reserve Bank of India data show monthly transaction counts surpassing 12 billion in 2025, creating fertile ground for real-time rewards attached to peer-to-merchant transfers. Both nations illustrate how payment infrastructure directly shapes loyalty innovation trajectories.

Singapore and Australia punch above their population weight in per-capita loyalty spending, acting as living labs for biometric authentication and bank-wallet interoperability pilots. Regulatory clarity in these markets accelerates vendor experimentation, and successful prototypes often cascade to larger economies once proof-points mature. Japan and South Korea display near-universal loyalty card enrollment yet battle growth plateaus because of demographic stagnation and market saturation. Their operators pivot toward experiential perks and gamified fitness challenges to rekindle engagement among younger cohorts.

Southeast Asian markets, Indonesia, Thailand, Vietnam, and the Philippines, score the highest forward CAGR as smartphone adoption and e-commerce GMV outstrip regional averages. Governments champion interoperable QR networks that reduce merchant fees and level the playing field for neighborhood stores. Regional tourism corridors offer coalition opportunities; for instance, Singapore-Malaysia rail commuters can soon redeem points earned in Kuala Lumpur coffee chains at Singapore bookstores once payment networks link. The Rest of Asia-Pacific cluster, including emerging economies like Bangladesh and Cambodia, lags today but offers long-run upside once 4G coverage, digital-ID systems, and consumer-credit penetration reach critical mass.

Competitive Landscape

Competitive intensity remains moderate as legacy enterprise software giants square off against nimble cloud-native disruptors. Capillary Technologies raised USD 95 million in February 2024 to bolster AI experimentation and has since pursued inorganic expansion, acquiring Kognitiv in May 2025 to import advanced analytics and deepen its North American client roster. Enterprise suites defend incumbency with holistic feature sets, native compliance modules, and deep system-integration pedigrees that appeal to regulated verticals such as banking. Disruptors undercut on speed and cost, offering modular APIs and outcome-based pricing attractive to SMEs and digital-first brands.

Blockchain tokenization surfaces as a white-space battleground. Mastercard’s pilots demonstrate how programmable rewards can limit fraud and seamlessly translate into multiple partner currencies. Traditional vendors race to embed ledger connectors to avoid dis-intermediation. Meanwhile, marketing-cloud majors tighten cross-sell motions between email automation, CDP layers, and loyalty engines, positioning themselves as end-to-end engagement suites. Consolidation is expected to continue as scale economics favor platforms that can amortize R&D across diverse client bases and compliance jurisdictions.

Strategic alliances also reshape the field. DBS partnered with e-commerce giants to pipe transactional insights into its lifestyle rewards hub, proving the value of cross-industry data pooling. Telecom carriers court hospitality chains to craft mobile-centric travel passes redeemable for roaming data. Vendors able to orchestrate such tri-party ecosystems secure competitive moats anchored in network effects rather than feature checklists.

Asia-Pacific Loyalty Management Industry Leaders

Aimia Inc.

Comarch SA

Edenred SA

Epsilon Data Management LLC

Maritz Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: HeyMax raised USD 2.6 million in seed funding and acquired Krip to enhance AI-driven predictive analytics for Southeast Asian clients

- March 2025: Hong Kong Monetary Authority launched Phase 2 of the e-HKD pilot, enabling programmable tokenized loyalty redemption across border-linked wallets.

- January 2025: Capillary Technologies completed its acquisition of Kognitiv, adding advanced analytics capabilities and accelerating North American expansion.

- March 2024: Alipay Tap! crossed 100 million users, extending FamilyMart integrations across multiple Asia-Pacific markets.

Asia-Pacific Loyalty Management Market Report Scope

Loyalty management is an approach to the marketing of products based on strategic management in which a company focuses on increasing its new customer base and retaining its existing customers through various types of incentives and offers. The APAC Loyalty Management Market is segmented by Loyalty Program Type (Business-to-Consumer (B2C) and Business-to-Business (B2B)), End-User Vertical (BFSI, Consumer Goods & Services, IT & Telecom, Travel & Hospitality), and Country (China, Japan, South Korea, India, Singapore, the Philippines, Thailand, Vietnam, and the Rest of Asia Pacific).

The market sizes and forecasts are provided in terms of value (USD million) for all the above segments.

By Loyalty Program Type

| Business-to-Consumer (B2C) |

| Business-to-Business (B2B) |

| Coalition / Multipartner |

| Employee / Channel Loyalty |

By Component

| Software |

| Services |

By Deployment Mode

| Cloud |

| On-premises |

| Hybrid |

By End-user Vertical

| BFSI |

| Consumer Goods and Retail |

| Travel and Hospitality |

| IT and Telecom |

| Healthcare and Pharmaceuticals |

| Other End-user Verticals |

By Country

| China |

| India |

| Japan |

| South Korea |

| Australia |

| Singapore |

| Indonesia |

| Thailand |

| Vietnam |

| Philippines |

| Rest of Asia-Pacific |

| By Loyalty Program Type | Business-to-Consumer (B2C) |

| Business-to-Business (B2B) | |

| Coalition / Multipartner | |

| Employee / Channel Loyalty | |

| By Component | Software |

| Services | |

| By Deployment Mode | Cloud |

| On-premises | |

| Hybrid | |

| By End-user Vertical | BFSI |

| Consumer Goods and Retail | |

| Travel and Hospitality | |

| IT and Telecom | |

| Healthcare and Pharmaceuticals | |

| Other End-user Verticals | |

| By Country | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Singapore | |

| Indonesia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

What is the 2026 valuation of the Asia-Pacific loyalty management market?

The market stands at USD 4.76 billion in 2026 and is projected to hit USD 12.16 billion by 2031.

Which loyalty-program type is expanding fastest in Asia-Pacific?

Coalition and multipartner programs lead with a 21.13% CAGR forecast through 2031.

Why are healthcare organizations adopting loyalty platforms?

Patient-engagement digitization and pharmaceutical channel incentives push healthcare to the highest 21.06% CAGR among verticals.

How dominant is cloud deployment across loyalty platforms?

Cloud models already hold 63.73% revenue share and will continue to outpace on-premise setups through 2031.

What key regulation influences loyalty data transfers in Asia-Pacific?

China’s Personal Information Protection Law and similar statutes in Vietnam and India impose strict consent and localization rules affecting cross-border programs.

Page last updated on: