Antimicrobial Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

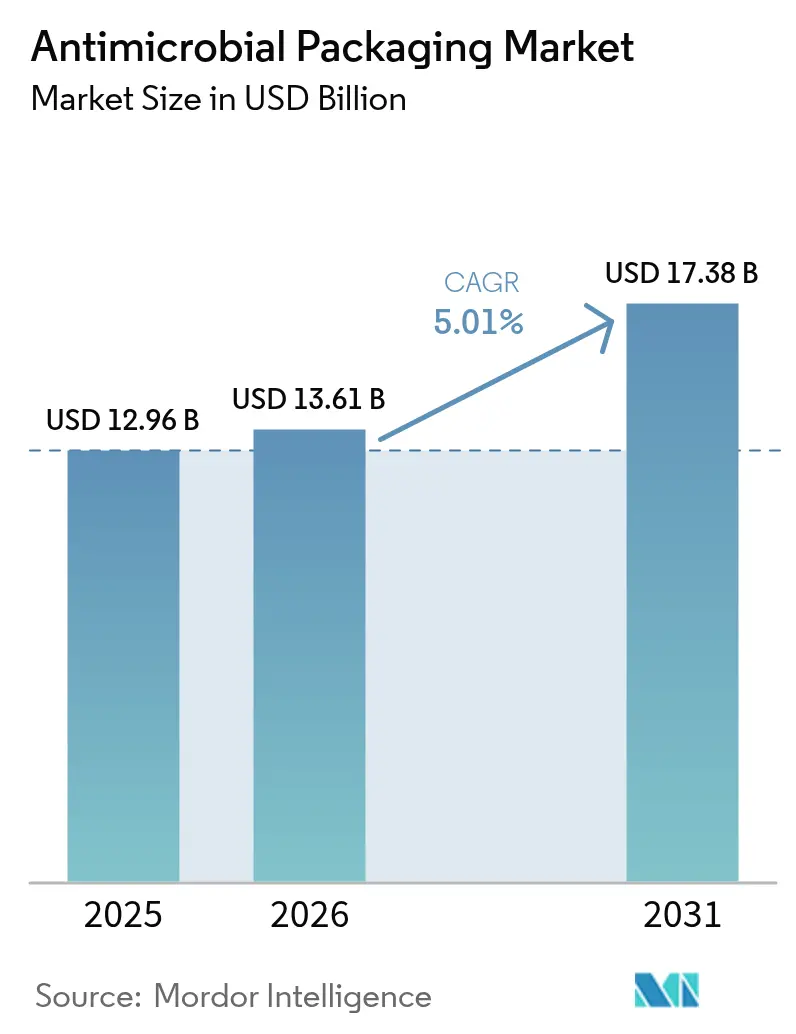

| Market Size (2026) | USD 13.61 Billion |

| Market Size (2031) | USD 17.38 Billion |

| Growth Rate (2026 - 2031) | 5.01% CAGR |

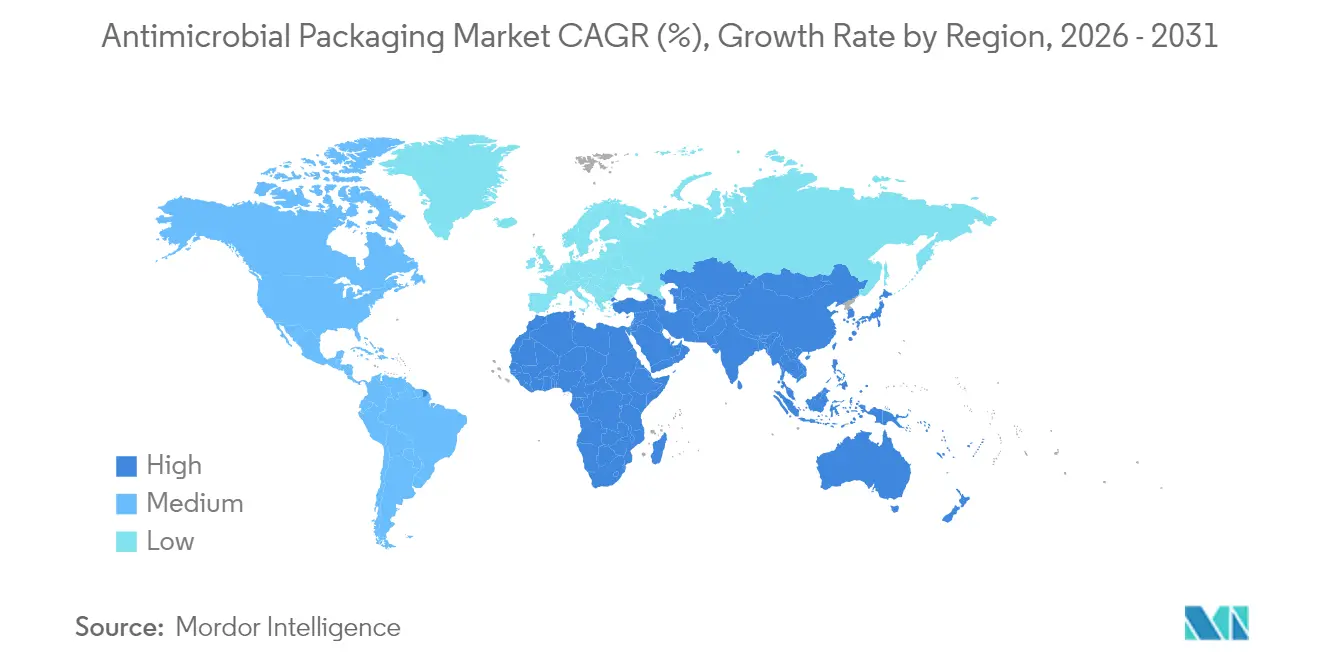

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

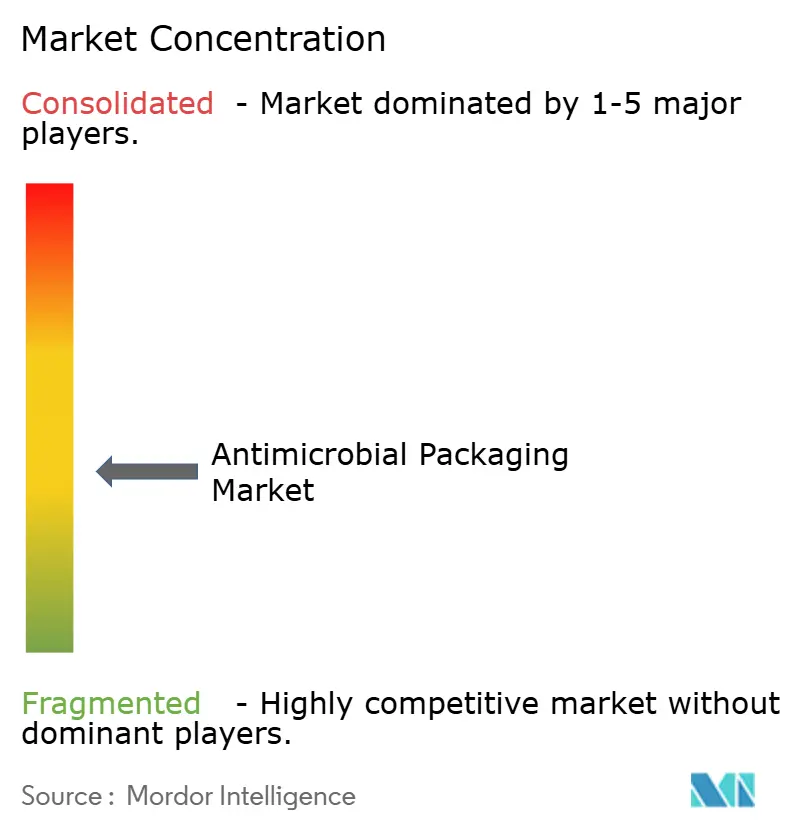

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Antimicrobial Packaging Market Analysis by Mordor Intelligence

The Antimicrobial Packaging Market size was valued at USD 12.96 billion in 2025 and estimated to grow from USD 13.61 billion in 2026 to reach USD 17.38 billion by 2031, at a CAGR of 5.01% during the forecast period (2026-2031). Demand is propelled by stricter food-contact regulations, the phase-out of PFAS substances, and corporate sustainability mandates that elevate antimicrobial functionality to a mainstream packaging requirement. Regulatory momentum has sparked a pivot toward bio-based antimicrobial agents that balance microbial efficacy with environmental credentials. Asia-Pacific remains the fulcrum of growth, driven by evolving sanitation laws, a booming e-grocery sector, and rapid cold-chain upgrades. Parallel advances in controlled-release nano-silver films, natural compound integration, and smart-sensor pairing are reshaping competitive innovation priorities. As a result, the antimicrobial packaging market continues to diversify across materials, technologies, and end-use sectors.

Key Report Takeaways

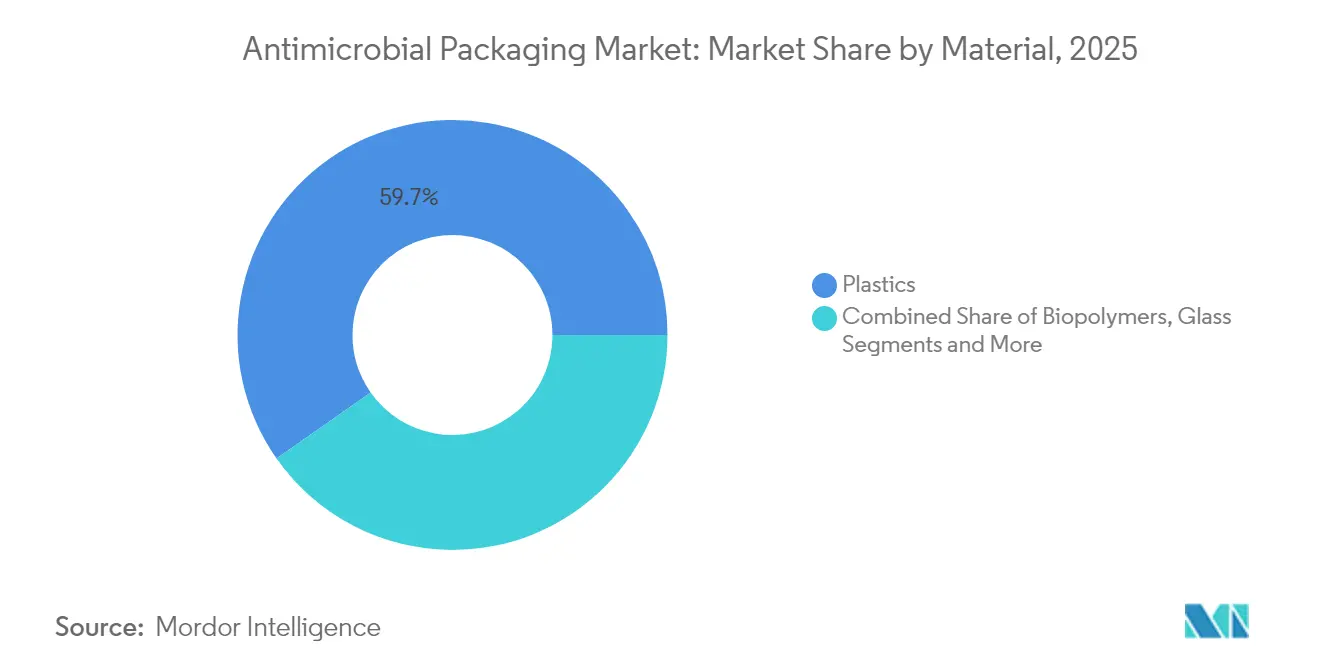

- By material, plastics led with 59.74% revenue share in 2025, while biopolymers are set to climb at an 8.05% CAGR through 2031.

- By antimicrobial agent, organic acids held 45.12% of the antimicrobial packaging market share in 2025; bacteriocins and enzymes record the fastest 7.29% CAGR to 2031.

- By technology, active surface coatings commanded 56.11% share of the antimicrobial packaging market size in 2025; controlled-release systems are projected to expand at 6.51% CAGR between 2026-2031.

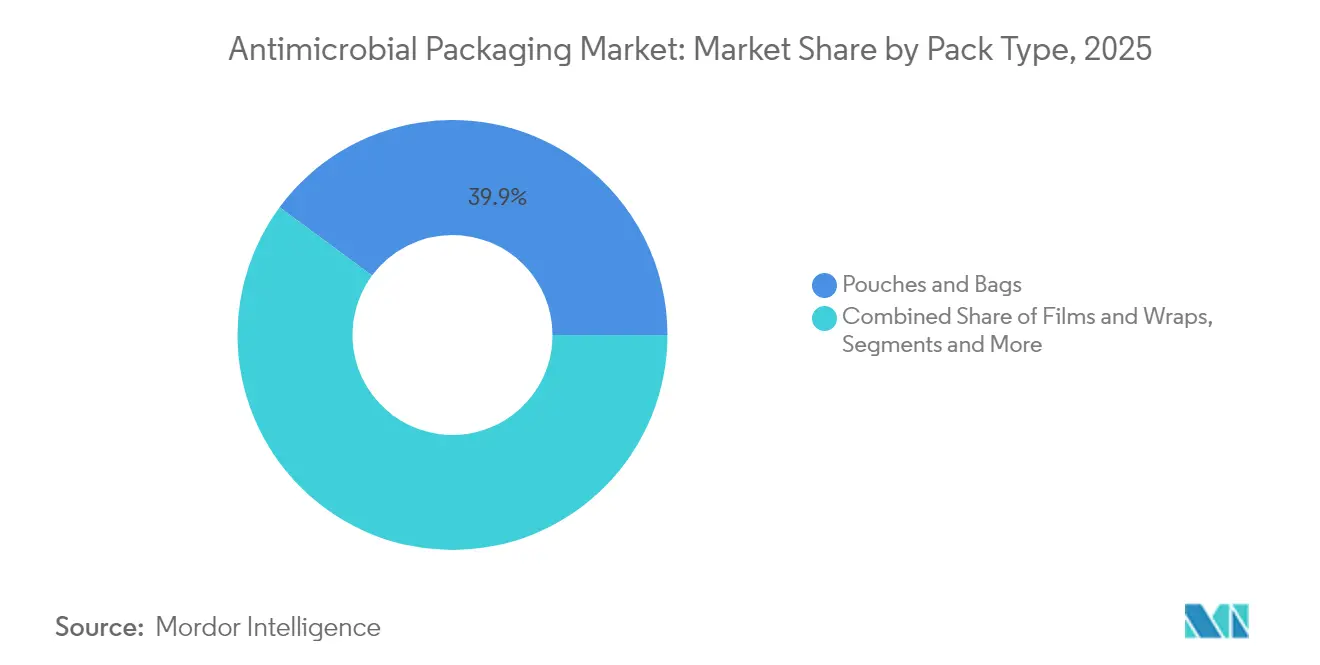

- By pack type, pouches and bags accounted for 39.88% of the market in 2025, whereas cartons post the highest 8.17% CAGR.

- By end-user, food and beverages captured 45.10% share in 2025, yet healthcare and medical devices advance at a 8.66% CAGR.

- By geography, Asia-Pacific dominated with 40.74% share in 2025 and is forecast to grow fastest at 8.44% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Antimicrobial Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent post-COVID food-safety regulations | +1.2% | Global, with emphasis on North America and EU | Medium term (2-4 years) |

| Acceleration of e-grocery cold-chain investments | +0.8% | Asia-Pacific core, spill-over to North America | Short term (≤ 2 years) |

| Breakthroughs in controlled-release nano-silver films | +0.6% | Global, led by North America and EU research hubs | Long term (≥ 4 years) |

| Inclusion of antimicrobial features in ESG scorecards | +0.4% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Shift to reusable medical-device trays in hospitals | +0.3% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| Adoption of edible, antimicrobial coatings for fresh-produce export | +0.5% | Asia-Pacific export economies, MEA emerging markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Post-COVID Food-Safety Regulations

The global reset of food-contact oversight is amplifying uptake of antimicrobial solutions. The United States Human Foods Program now reassesses legacy PFAS notifications, creating an opening for safer antimicrobial alternatives. [1]FDA, “FDA Determines Authorization for 35 Food Contact Notifications Related to PFAS Are No Longer Effective,” fda.gov European agencies simultaneously flag persistent pathogens such as Listeria monocytogenes, compelling processors to adopt packaging that adds an extra microbial barrier. These converging mandates accelerate investment in naturally-derived agents that fulfil both safety and “clean-label” expectations. For suppliers able to document efficacy and recyclability, regulatory tightening translates into clear growth runway within the antimicrobial packaging market.

Acceleration of E-Grocery Cold-Chain Investments

Explosive demand for online groceries places unprecedented stress on temperature-controlled logistics. In Asia-Pacific, thousands of micro-fulfilment warehouses now require packaging that maintains quality over extended last-mile journeys. When refrigeration falters, antimicrobial layers serve as a critical secondary safeguard, reducing spoilage claims. Emerging smart packs pair time-temperature indicators with embedded antimicrobials, giving platforms data-driven control over freshness. As same-day delivery windows shrink, retailers increasingly make antimicrobial functionality a procurement prerequisite, particularly for high-risk perishables. This e-commerce momentum solidifies near-term gains for the antimicrobial packaging market.

Breakthroughs in Controlled-Release Nano-Silver Films

Academic labs have engineered film-forming silver assemblies that deliver zero bacterial adhesion for 30+ days without toxic burst release. [2]American Chemical Society, “Durable Surfaces from Film-Forming Silver Assemblies for Long-Term Zero Bacterial Adhesion,” acs.org While legacy nano-silver raised migration alarms in dry foods, new hierarchical matrices meter release to regulatory-acceptable thresholds. Controlled-release architecture widens use cases from wound-care trays to extended-shelf-life bakery films. Ongoing refinement toward bio-compatibility positions the technology as a long-term growth catalyst for the antimicrobial packaging market.

Inclusion of Antimicrobial Features in ESG Scorecards

Major brand owners now credit antimicrobial packaging in ESG audits for its role in curbing food waste—roughly 30% of global output. Amcor reports 95% of rigid packs are recyclable while simultaneously extending product life through antimicrobial layers. [3]Amcor, “Amcor Sustainability Report,” amcor.com Investors reward demonstrable waste-reduction metrics, making antimicrobial capability a route to improved sustainability rankings. As comparable disclosures proliferate, suppliers that align antimicrobial efficacy with recyclability establish a stronger value proposition throughout the antimicrobial packaging industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU biocide regulation (BPR) hurdles for nano-metals | -0.7% | EU, with spillover effects to global markets | Medium term (2-4 years) |

| Price volatility in silver and copper feedstocks | -0.5% | Global, particularly affecting cost-sensitive applications | Short term (≤ 2 years) |

| Consumer push-back on synthetic preservatives in packaging | -0.4% | North America and EU, expanding to Asia-Pacific markets | Medium term (2-4 years) |

| Scale-up challenges for bio-based antimicrobial polymers | -0.3% | Global, concentrated in developed manufacturing hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU Biocide Regulation (BPR) Hurdles for Nano-Metals

Europe’s Biocidal Products Regulation requires exhaustive dossiers before nano-silver or nano-copper can enter food-contact channels. With no nano-metal yet authorised for direct food or feed applications, innovators face multi-year toxicology programs. Wide-ranging data demands inflate time-to-market, prompting some firms to pivot toward plant-based actives that clear regulatory pathways more swiftly. The deterrent effect narrows near-term growth for metallic solutions inside the antimicrobial packaging market.

Price Volatility in Silver and Copper Feedstocks

Spot prices for silver and copper continue to swing on industrial demand, complicating cost models for antimicrobial masterbatches. Producers buffer volatility through hedging, recycling recovery, and dilution with hybrid organic agents. Nevertheless, thin-margin applications such as fresh-produce wraps remain sensitive to price spikes, slowing adoption. These economics reinforce R&D focus on bio-sourced compounds with more predictable cost curves, subtly tempering CAGR contributions for metal-based formats across the antimicrobial packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Biopolymers Drive Sustainability Transition

Plastics currently anchor the antimicrobial packaging market size, capturing 59.74% revenue share in 2025 due to scalable extrusion lines and robust barrier performance. Yet policy targets that mandate full recyclability by 2030 propel biopolymers to an 8.05% CAGR, the fastest among materials. Poly-lactic acid and polyhydroxyalkanoate blends enhanced with chitosan or essential oils now match microbial kill rates seen in petrochemical films while supporting compostable end-of-life routes.

Investment is accelerating in closed-loop collection schemes that recover biopolymer offcuts without sacrificing antimicrobial potency. Research also evidences that paper fibres coated with phenolic-rich polysaccharides retain recyclability and deliver broad-spectrum bacterial inhibition. These advances ensure biopolymers will continue eroding plastic share, reshaping supplier portfolios throughout the antimicrobial packaging market.

By Antimicrobial Agent Type: Natural Compounds Gain Momentum

Organic acids command 45.12% of 2025 revenue owing to regulatory familiarity and cost efficiency. However, bacteriocins and enzymes accelerate at 7.29% CAGR, mirroring consumer migration to recognizable, label-friendly additives. Synergistic systems marry bacteriocins with nano-silver, doubling kill efficiency while curbing metal dosage.

Essential oils protected within cyclodextrin cages provide controlled vapor release that suppresses spoilage organisms in high-moisture produce. As biocide scrutiny intensifies, plant-derived agents gain strategic heft, positioning natural actives as pivotal to future differentiation in the antimicrobial packaging market.

By Technology: Controlled-Release Systems Show Promise

Active surface coatings sit atop the technology hierarchy with 56.11% share, benefitting from simple gravure or spray deposition onto existing substrates. Nonetheless, controlled-release platforms advance at 6.51% CAGR as converters incorporate multi-layer films that stagger antimicrobial diffusion. Hierarchical polymer matrices now enable day-long zero-bacterial adhesion without leaching.

Smart sensors paired with release triggers respond to pH or temperature shifts, extending protection only when spoilage risk rises. These functional synergies encourage wider uptake, bolstering the antimicrobial packaging market’s premium tiers.

By Pack Type: Carton Innovation Drives Growth

Flexible pouches and bags held 39.88% of 2025 sales, reflecting light-weight economics. Yet cartons climb at 8.17% CAGR, powered by fibre-based formats that incorporate high-barrier antimicrobial coatings while meeting recyclability thresholds. AmFiber Performance Paper illustrates how 80%+ paper content can integrate antimicrobial layers without compromising MRF recovery streams.

Concurrently, antimicrobial shrink films for trays combine oxygen scavenging with microbial kill to safeguard case-ready meat. Continuous innovation across both rigid and flexible formats confirms packaging engineers’ commitment to raising performance across the antimicrobial packaging market.

By End-User Industry: Healthcare Accelerates Adoption

Food and beverages accounted for 45.10% of spending in 2025 as retailers demanded extended shelf life for high-risk proteins and fresh produce. Post-pandemic infection-control protocols propel healthcare packaging to a 8.66% CAGR, the fastest across verticals. SteriTite reusable trays illustrate how long-cycle medical packs rely on antimicrobial aluminium alloys to maintain sterility across autoclave runs.

Single-barrier sterile wraps that cut medical waste while preserving microbial integrity further expand hospital demand. This healthcare momentum diversifies revenue streams, underpinning long-term resilience within the antimicrobial packaging market.

Geography Analysis

Asia-Pacific tops the global leaderboard, holding 40.74% revenue in 2025 and registering the highest 8.44% CAGR to 2031. China’s Food Safety Law amendments and India’s FSSAI hygiene codes mandate microbiological safeguards that funnel capital toward advanced packs. Japanese converters add smart indicators and controlled-release antimicrobials to premium seafood exports, elevating unit margins. Regional government initiatives to counter antimicrobial resistance further incentivise adoption, reinforcing Asia-Pacific’s pull on the antimicrobial packaging market.

Europe follows, its trajectory shaped by the EU Packaging and Packaging Waste Regulation that forces recyclability and recycled-content compliance. Germany and France spearhead R&D into bio-based actives, whereas Mediterranean exporters deploy antimicrobial cartons to secure shelf life during cross-border produce shipments. While the BPR slows nano-metal roll-outs, it simultaneously accelerates botanical innovation, keeping Europe central to technology leadership.

North America sustains steady gains anchored by FDA oversight and robust healthcare demand. The United States channels grant funding toward PFAS alternatives, indirectly uplifting antimicrobial packaging market size for natural actives. Canadian institutes pilot cellulose-based films infused with enzyme cocktails, targeting seafood supply chains. Mexico, leveraging near-shoring trends, scales antimicrobial pouch production for both domestic brands and US retailers.

Competitive Landscape

The antimicrobial packaging market remains moderately fragmented. Mega-merger activity, exemplified by Amcor’s all-stock combination with Berry Global, yields a vertically integrated giant poised to extract USD 650 million in synergies by 2028. Simultaneously, niche technology firms such as Microban extend portfolios into PFAS-free water-resistant textiles, broadcasting expertise that can cross-pollinate into food and medical packs.

Strategic focus pivots on proprietary antimicrobial formulations, controlled-release patents, and demonstrable recyclability. Corporate venturing accelerates deal flow; Amcor’s Lift-Off fund backs start-ups like Bloom Biorenewables to secure early access to biobased chemistries. Patent landscapes reveal clustering around enzyme-grafted coatings and nano-porous release reservoirs, areas where first-mover IP can translate into sustainable price premiums. Competitive intensity will hinge on multinationals’ ability to harmonise global regulatory submissions, maintain cost discipline in volatile metals markets, and supply chain-proof biopolymer feedstocks—all critical to consolidating share within the antimicrobial packaging market.

Antimicrobial Packaging Industry Leaders

BASF SE

Mondi PLC

BioCote Limited

Dunmore Corporation

Avient Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: BASF closed purchase of DOMO Chemicals’ 49% stake in the Alsachimie joint venture, reinforcing upstream control of polyamide intermediates for antimicrobial applications.

- June 2025: Microban unveiled H₂O Shield, a PFAS-free water-resistant textile finish that complements its antimicrobial line.

- April 2025: Amcor completed its all-stock combination with Berry Global, creating a USD 3 billion annual cash-flow powerhouse.

- April 2025: BASF debuted Verdessence Maize biodegradable styling polymer, extending natural ingredient portfolio.

Global Antimicrobial Packaging Market Report Scope

Antimicrobial packaging relates to the application of active packaging. The specially designed antimicrobial packaging checks the superficial evolution of bacteria and pathogens in food by applying antimicrobial medium where a large portion of spillage and contamination happens, permitting a well-ordered discharge of antimicrobial mediators into the food surface throughout the storage.

| Plastics |

| Biopolymers |

| Paper and Paperboard |

| Glass |

| Metals |

| Organic Acids |

| Bacteriocins and Enzymes |

| Silver and Copper Nanoparticles |

| Essential Oils and Plant Extracts |

| Active Surface Coating |

| Controlled-Release Systems |

| Pouches and Bags |

| Films and Wraps |

| Trays and Lids |

| Carton Packages |

| Food and Beverages | Meat, Poultry and Seafood |

| Bakery and Confectionery | |

| Fruits and Vegetables | |

| Healthcare and Medical Devices | |

| Personal Care and Cosmetics | |

| Animal Feed and Pet Food | |

| Other End-User Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Plastics | ||

| Biopolymers | |||

| Paper and Paperboard | |||

| Glass | |||

| Metals | |||

| By Antimicrobial Agent Type | Organic Acids | ||

| Bacteriocins and Enzymes | |||

| Silver and Copper Nanoparticles | |||

| Essential Oils and Plant Extracts | |||

| By Technology | Active Surface Coating | ||

| Controlled-Release Systems | |||

| By Pack Type | Pouches and Bags | ||

| Films and Wraps | |||

| Trays and Lids | |||

| Carton Packages | |||

| By End-user Industry | Food and Beverages | Meat, Poultry and Seafood | |

| Bakery and Confectionery | |||

| Fruits and Vegetables | |||

| Healthcare and Medical Devices | |||

| Personal Care and Cosmetics | |||

| Animal Feed and Pet Food | |||

| Other End-User Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the antimicrobial packaging market?

The market is valued at USD 13.61 billion in 2026 and is projected to reach USD 17.38 billion by 2031 at a 5.01% CAGR.

Which region leads the antimicrobial packaging market?

Asia-Pacific holds 40.74% of global revenue in 2025 and posts the fastest 8.44% CAGR through 2031.

Which material segment is growing fastest?

Biopolymers expand at an 8.05% CAGR as regulations favor recyclable and bio-based substrates.

Why are healthcare applications gaining momentum in antimicrobial packaging?

Post-pandemic infection-control priorities push healthcare packaging to a 8.66% CAGR, the swiftest among end-user industries.

Page last updated on: