Anti-static Agents Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

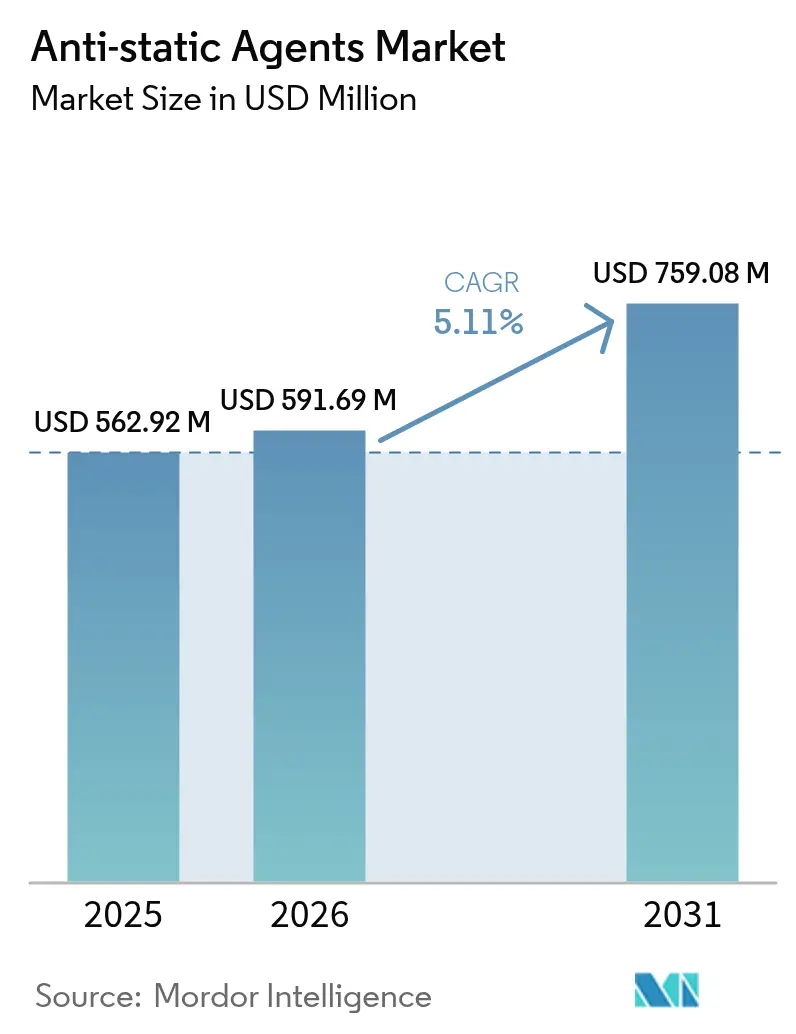

| Market Size (2026) | USD 591.69 Million |

| Market Size (2031) | USD 759.08 Million |

| Growth Rate (2026 - 2031) | 5.11% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Anti-static Agents Market Analysis by Mordor Intelligence

The Anti-static Agents Market size was valued at USD 562.92 million in 2025 and estimated to grow from USD 591.69 million in 2026 to reach USD 759.08 million by 2031, at a CAGR of 5.11% during the forecast period (2026-2031). A sharp rise in electronics miniaturization is magnifying electrostatic-discharge (ESD) sensitivity across semiconductor fabs and consumer electronics lines, reinforcing demand for both permanent and migratory additives. Water-borne masterbatch platforms are gaining share as brands and processors pivot away from solvent systems in response to PFAS and VOC regulations. Asia-Pacific’s contract manufacturing strength anchors global volume, while bio-based chemistry and silica-rich blends reshape competitive positioning. Automotive electrification, e-commerce packaging, and advanced health-care devices together create multi-year growth corridors that the antistatic agent market is gearing toward with higher-temperature, clean-room-ready, PFAS-free solutions.

Key Report Takeaways

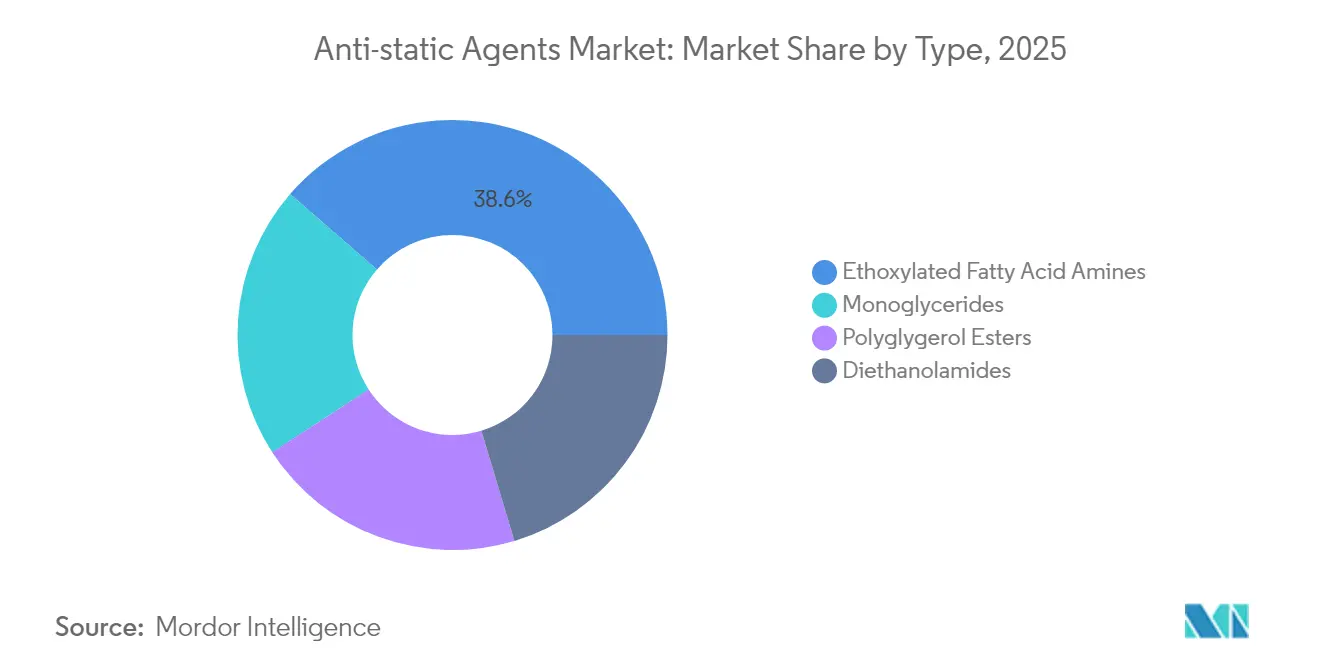

- By type, ethoxylated fatty acid amines held 38.62% revenue in 2025; the sub-segment is expanding at 6.82% CAGR on the back of high-temperature automotive molding demand.

- By source, petrochemical routes commanded 79.22% of 2025 value while bio-based variants are advancing at 7.21% CAGR under global sustainability mandates.

- By polymer, polypropylene accounted for 34.55% share of the antistatic agent market size in 2025 and is forecast to grow at 6.52% CAGR through 2031.

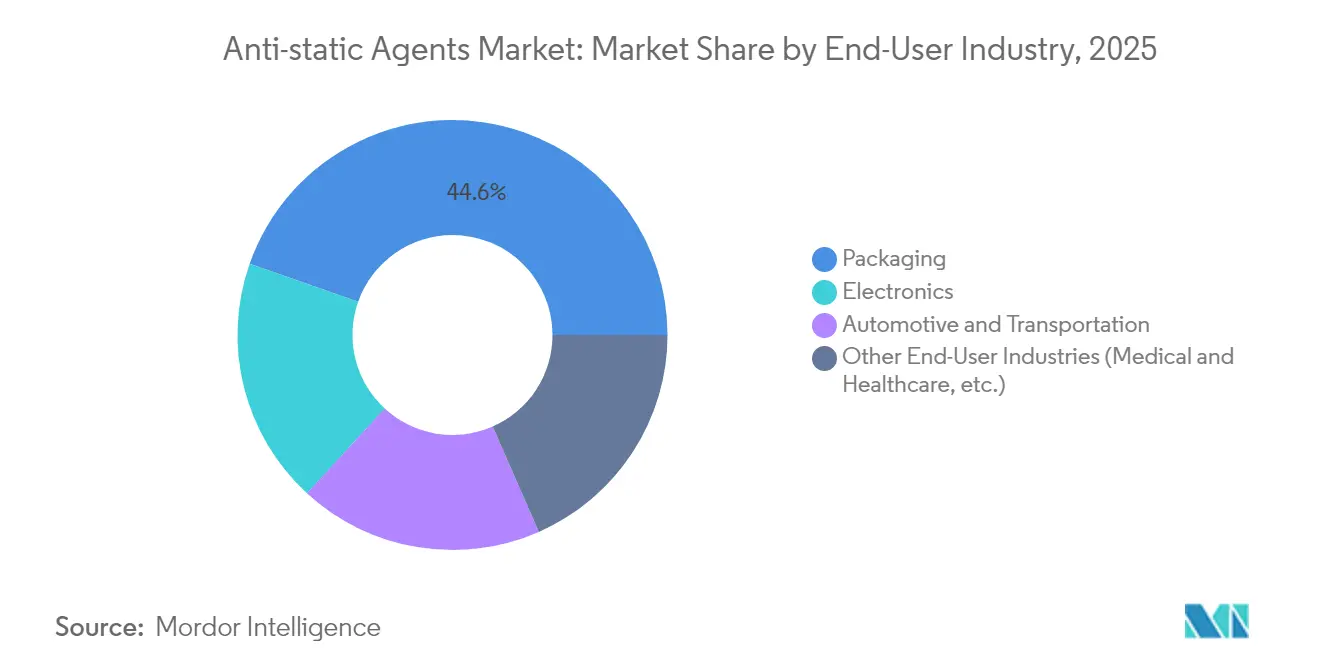

- By end-user industry, packaging retained 44.62% of the antistatic agent market share in 2025 while electronics is poised to post the fastest 6.28% CAGR to 2031.

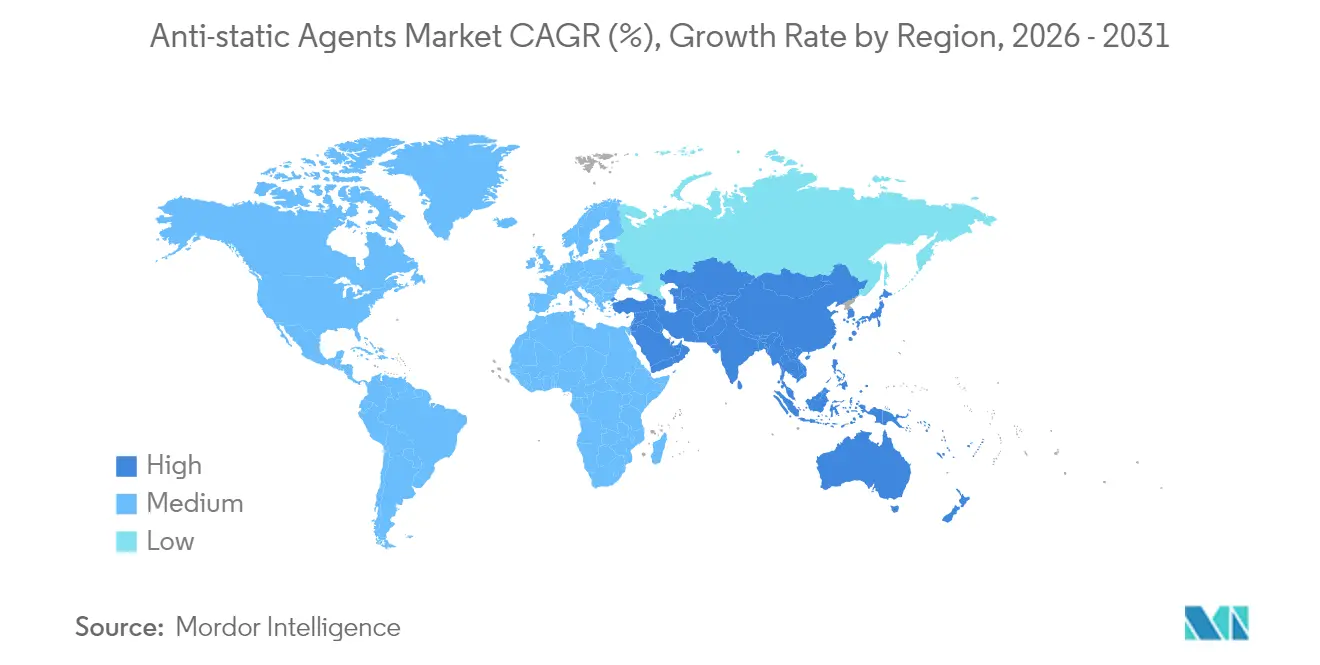

- Regionally, Asia-Pacific led with 42.75% revenue in 2025 and is set to rise at 6.63% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Anti-static Agents Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in e-commerce–led demand for antistatic packaging | +1.8% | Global, concentrated in North America & APAC | Short term (≤ 2 years) |

| Miniaturization of electronics heightening ESD risk | +1.5% | APAC core, spill-over to North America & EU | Medium term (2-4 years) |

| Shift from solvent-borne to water-borne masterbatch | +0.9% | EU & North America regulatory driven, APAC adoption | Medium term (2-4 years) |

| Expanding automotive electrification needs | +1.2% | Global, early gains in APAC & North America | Long term (≥ 4 years) |

| Growth in health-care and medical devices | +0.7% | North America & EU, emerging in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge In E-Commerce-Led Demand For Antistatic Packaging

Cross-border e-commerce shipments of consumer electronics outpace store deliveries, obliging parcel handlers to meet tighter surface-resistivity limits in low-density polyethylene (LDPE) films and bubble bags. Large logistics centers deploy high-speed sorters whose friction often exceeds 100 m/min, exacerbating static buildup that can cripple micro-controllers. Packaging converters therefore integrate permanent antistatic masterbatches that comply with RoHS and food-contact codes, keeping additive loading below 3 phr to preserve clarity and seal integrity. China’s online retail share, already above 50% of national sales, pushes local bag makers to qualify humidity-independent antistatic grades. Brands simultaneously pursue recyclable mono-material films, requiring amine-based chemistries that do not hinder mechanical-recycling streams.

Miniaturization Of Electronics Heightening ESD Sensitivity

FinFET and gate-all-around nodes below 3 nm withstand only 25% of the peak current tolerated by 14 nm devices, so fabs now specify room-air resistivity under 10^10 Ω for carrier trays and wafer boxes. Advanced system-in-package assemblies route power through ultrathin interposers, amplifying local heat during a discharge and demanding permanent antistatic coatings rated for 230 °C reflow. Research consortia such as imec document failure-current declines of 20–40% on thinned silicon, guiding additive suppliers toward silica-grafted polyether amides that avoid humidity dependence. The antistatic agent market, therefore, concentrates R&D on temperature-stable, migration-free grades for clean-room polymers.

Transition From Solvent-Borne To Water-Borne Masterbatches

The European Chemicals Agency’s PFAS roadmap and US state-level VOC caps accelerate the pivot to water-based carriers. Clariant’s AddWorks PPA, commercialized in 2024, replaces fluorinated process aids yet sustains film gloss and thickness uniformity[1]Clariant, “AddWorks PPA—PFAS-Free Processing Aid,” clariant.com. Formulators counter traditional moisture-reliant shortcomings by embedding ionic-conductive polyether blocks that function below 10% RH, enabling use in semiconductor back-end lines. Capital upgrades—stainless-steel tanks, high-shear dispersers, and drying ovens—pose hurdles for small extruders, yet tier-one automotive suppliers already report switchover savings from eliminate-to-substitute audits.

Growing Demand From The Automotive Industry

Electric-vehicle battery packs incorporate multi-layer polypropylene cell spacers coated with permanent antistatic waxes that dissipate charges in under 1 s at 50% RH, guarding against arc-flash risks. Passenger cabin textiles accumulate static up to 30 kV during seat egress; polyester filaments treated with quaternary ethoxylated amines curb dust adhesion and preserve infotainment touchscreen clarity[2]InTechOpen, “Electrostatic Hazards in Automotive Interiors,” intechopen.com. Molded-in-color polypropylene dashboards incorporating antistatic agents cut painting costs by 30% and erase VOC emissions, aligning with OEM sustainability scorecards. As advanced driver assistance systems (ADAS) multiply radar and camera modules, antistatic coatings shield sensors from electrostatic interference that can distort object detection.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in tallow-derived feedstocks | -1.1% | Global, acute in North America & EU | Short term (≤ 2 years) |

| Capital-intensive permanent ionic conductors | -0.8% | APAC manufacturing hubs, spill-over to emerging markets | Medium term (2-4 years) |

| Rising adoption of inherently dissipative polymers | -0.6% | North America & EU early adoption, APAC gradual | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility In Tallow-Derived Feedstocks

Surging biodiesel mandates elevate competition for beef-tallow, inflating prices and tightening supply for oleochemical antistatic intermediates. EU refineries channel more animal fat toward hydro-treated vegetable-oil diesel, hindering chemical availability and forcing formulators to hedge with palm-fatty-acid distillate routes. Renderers operate near capacity, and cold-chain logistics add freight premiums that erode cost advantages over petrochemical amines. Packaging firms using food-contact antistatic agents face further constraints as certain retailers restrict animal-derived ingredients. Producers consequently intensify trials of rapeseed- and used-cooking-oil-based esters that mimic tallow performance.

Capital-Intensive Permanent Ionic-Conductive Additives

Polyether-block-amide and sulfonated polyester chemistries promise static-decay times <0.1 s regardless of humidity, but their polymeric nature pushes compound prices as high as USD 20 per kg—triple conventional migratory agents. Mass-production in APAC injection-molding shops therefore remains limited to safety-critical electronics, while budget fabrics and films tolerate longer decay times. High melt viscosities require twin-screw extrusion and hot-runner retrofits, elevating capital thresholds for SMEs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Ethoxylated Amines Drive Chemical Innovation

Fatty-acid amines captured 38.62% revenue in 2025, leveraging proven efficacy in LDPE and PP films. Ethoxylated amine grades now post the fastest 6.82% CAGR, propelled by thermal stability up to 250 °C that suits glass-fiber-reinforced polypropylene used in instrument panels. Monoglycerides remain staples in FDA-regulated food-packaging applications, though growth is muted because inclusion levels cap at 0.5 phr. Polyglycerol esters serve medical-device pouches where biocompatibility offsets price premiums. Emerging quaternary polyethoxylated structures add hydroxyl functionality, improving dispersion in high-flow PP and reducing bloom, further cementing the antistatic agent market trajectory in performance vehicles.

The sub-segment’s ascent influences the antistatic agent market size for polypropylene interior parts, which is slated to expand at 6.52% CAGR between 2026-2031. Permanent additives such as polyether-bisphenol A copolymers command higher unit pricing but shield dashboards from dust for the full vehicle life, encouraging OEM uptake and lifting the antistatic agent market share for ethoxylated systems.

By Source: Bio-Based Transformation Accelerates

Petrochemical feedstocks supplied 79.22% of 2025 demand, a reflection of integrated cracker economics. Yet sustainability goals are steering capacity toward rapeseed-, palm-, and used-cooking-oil pathways that now clock a 7.21% CAGR. Regulatory carrots such as mass-balance certification and carbon-credit trading in Europe reduce the price delta to below 12%. Croda’s biodegradable Crodastat 400 demonstrates that bio-based systems can match conductivity while cutting CO₂ footprint by 60%.

Tallow volatility and consumer sentiment against animal derivatives amplify the pivot, making vegetable-oil esters the default for electronics shipping films by 2028. This shift could push the bio-based antistatic agent market size past USD 206.4 million by 2031, though competitive parity hinges on further scale-up in Asian bio-refineries.

By Polymer: Polypropylene Dominance Continues

Polypropylene held 34.55% value in 2025 and tops growth at 6.52% CAGR, underlining its omnipresence in rigid packaging, dashboards, and battery trays. Its non-polar backbone enjoys strong compatibility with fatty-amine and glyceride antistatics, enabling low dosages that safeguard gloss. Polyethylene remains vital in blown-film sack lines, while PVC advances in transparent medical blisters that need low haze. Engineering resins such as polycarbonate and polyamide add premium volume because clean-room parts demand sub-0.5 s decay. Graphene-nanotube-loaded PP compounds slash additive use ten-fold yet stay in early commercial stages while producers validate rheology and color stability.

New wax-grafted PP masterbatches achieve permanent performance without exudation, raising the antistatic agent market size attached to high-value injection-molded housings for 5G base-station components.

By End-User Industry: Packaging Leadership Amid Electronics Growth

Packaging preserved a 44.62% slice in 2025 as e-commerce escalated single-item shipments that impose strict ESD protections. Film convertors increasingly request antistatic agents that retain performance after 30+ recycling loops, consistent with upcoming EU circularity targets. Electronics follows as the fastest-moving customer set at 6.28% CAGR; fabs specify humidity-independent additives for IC trays, tape-reels, and clean-room garments. Automotive uptake stems from battery-pack insulation and cabin parts, while medical devices favor polymer-based permanent agents compatible with gamma sterilization.

Textile and industrial niches deploy antistatic fibers in explosion-prone environments, anchoring a steady pull for high-tenacity polyester, whereas aerospace composite panels integrate nanoscale antistatic coatings to divert lightning-strike energy without adding copper meshes.

Geography Analysis

Asia-Pacific controlled 42.75% of global revenue in 2025 and advances at a 6.63% CAGR through 2031. Mainland China’s wafer-fab expansion and India’s tier-1 auto-components surge build dense demand corridors for permanent antistatic chemistries. Regional formulators invest in high-capacity twin-screw lines: Sanyo Chemical’s 1,500 t/y Thai plant exemplifies supply-side scaling. Government incentives for biodegradable plastics further encourage bio-feedstock adoption, potentially bolstering the antistatic agent market size in ASEAN packaging.

North America rides advanced semiconductor packaging and electrified-vehicle platforms. Consortium programs such as US-JOINT funnel federal grants into ESD-safe materials R&D, which supports high-margin masterbatch suppliers. Corporate sustainability goals—most Fortune 500 electronics OEMs pledge carbon neutrality by 2030—accelerate PFAS-free conversions, reshaping the antistatic agent market landscape with water-borne offerings.

Europe’s stringent REACH updates and the continent-wide PFAS phase-out catalyze rapid pivots to silica-based and bio-based solutions. Clariant’s complete PFAS exit in 2023 exemplifies early compliance. Germany and France, housing leading auto makers, champion VOC-free molded-in-color interiors, lifting demand for heat-resistant, permanent antistatic agents. The Middle East, Africa, and South America remain price-sensitive but post high single-digit volume growth as e-commerce penetration and automotive assembly rise, making them emergent battlegrounds for cost-optimized migratory grades.

Value Chain Analysis

The value chain begins with petrochemical and oleochemical feedstocks that are converted into intermediates used in antistatic chemistries, including fatty amines, glyceride- and ester-based systems, and other surfactant building blocks. Specialty chemical producers then formulate these actives into neat additives and, increasingly, into polymer-compatible masterbatches and liquid additive platforms using high-intensity compounding equipment, notably twin-screw extrusion, to control dispersion, surface activity, and cleanliness for electronics and medical applications. The downstream chain runs through resin producers and compounders to converters and molders serving packaging, electronics, automotive, medical, and industrial segments, where targets such as humidity-independent static decay and low-bloom behavior affect the choice between migratory and permanent systems.

Route-to-market varies by application. High-volume packaging and automotive programs often use direct supply from additive producers or masterbatch compounders to film lines and molding plants, while mid-volume customers in textiles and general plastics typically use regional distributor networks that also provide technical service and multi-additive packages (slip, antiblock, and antistatic combinations). Qualification and supply stability become key friction points, especially around volatility in tallow-derived and other oleochemical inputs, and single-source dependencies for some high-grade conductive and carbon-based precursors, which can constrain availability of premium permanent solutions and accelerate qualification of alternative inputs. Supplier selection is also shaped by regulatory and performance compliance, including REACH alignment and electronics-focused ESD standards such as IEC 61340-5-1, elevating the value of formulation know-how, documentation, and traceability alongside cost and supply security.

Competitive Landscape

The antistatic agents market is moderately fragmented. Clariant’s PFAS-free additive portfolio positions it for regulatory¬-driven substitution gains, while Evonik’s January 2025 Smart Effects merger unifies silica and silane assets, creating a full-stack platform for permanent antistatic solutions in coatings and elastomers.

Players differentiate through application-specific formulations: BASF’s Elastostat TPU masterbatch secures dust-proof wearables, and Croda’s Ionphas enhances ESD-safe 3D-print filaments for aerospace. Graphene-nanotube specialists partner with compounders to cut loading levels, yet adoption is gated by dispersion hurdles in high-speed film lines. Suppliers with backward integration into fatty-amine intermediates absorb feedstock volatility more effectively, thus shielding margins.

Anti-static Agents Industry Leaders

Croda International plc

BASF

Clariant

Adeka Corporation

Ampacet Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Opportunities are tightening around permanent, low-migration antistatic solutions that maintain performance under low humidity and elevated processing temperatures, particularly for semiconductor packaging, cleanroom polymers, and high-temperature automotive components where consistent resistivity and minimal contamination matter. Material designs that reduce reliance on carbon-black-heavy approaches also create openings in transparency- and aesthetics-sensitive applications, including electronics packaging films and consumer-facing housings. Recent published work on conductive nanocomposites, including graphene and carbon-based hybrid filler systems, points to technical routes for tunable conductivity at lower filler loadings, aligning with the market need to protect mechanical properties, optical clarity, and processability.

Near-term commercial activity is concentrated in additive consolidation and the regional rollout of performance packages for films and engineered polymers. In April 2026, Avient commercialized Hiformer Slip + Antistatic in Latin America for BOPP films, combining slip and antistatic functions at low dosage (0.30-0.50%), which targets converter priorities around formulation simplification and dosing precision on high-speed film lines. In January 2026, Toray Industries introduced a highly antistatic Toyolacparel ABS grade, reported at 10^9 ohm/sq surface resistivity, using a continuous-layer 3D network polymer design, highlighting demand for inherently dissipative or polymer-integrated antistatic performance in durable parts where migratory additives and secondary coatings are less preferred. Across end uses, alignment with ESD standards (ANSI/ESD S20.20 and IEC 61340-5-1) and chemical-compliance constraints, including REACH and TSCA, continues to favor suppliers that can pair performance with documentation, low-VOC platforms, and traceable, non-migratory formulations.

Recent Industry Developments

- April 2026: The LYCRA Company launched LYCRA ANTISTATIC fiber at Techtextil in Frankfurt (April 21-24, 2026), integrating antistatic functionality directly into the fiber structure. This shifts performance delivery from topical finishes toward built-in solutions for workwear and PPE, improving consistency of ESD and safety performance across laundering and wear cycles.

- March 2025: Ampacet introduced ProVital+ Permstat, a non-migratory, medical-grade permanent antistatic masterbatch for polyolefin films used in pharmaceutical packaging and cleanroom applications. The launch supports the market shift toward permanent, low-contamination antistatic performance where migratory additives can be constrained by cleanliness and regulatory requirements.

- February 2024: Arkema expanded Pebax elastomers capacity by 40% at its Serquigny, France facility, including supply for bio-circular Pebax Rnew grades serving electronics and medical uses. Additional elastomer availability supports higher-value permanent antistatic formulations in durable and specialty applications that require toughness alongside controlled static dissipation.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers anti-static agents sold as additives or processing aids that reduce static charge build-up in polymers and finished plastic goods, and it is measured in revenue terms for the materials supplied into industrial value chains.

Scope exclusions: Revenues from finished plastic products, anti-static films as packaged goods, and ESD equipment are not counted in this market sizing.

Segmentation Overview

- By Type

- Monoglycerides

- Polyglygerol Esters

- Diethanolamides

- Ethoxylated Fatty Acid Amines

- By Source

- Bio-based (Vegetable-, Tallow-derived)

- Petrochemical-based

- By Polymer

- Polypropylene

- Polyethylene

- Polyvinyl Chloride

- Other Polymers(Polystyrene, etc.)

- By End-User Industry

- Packaging

- Electronics

- Automotive and Transportation

- Other End-User Industries (Medical and Healthcare, etc.)

- By Geography

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to frame the demand pool and keep assumptions realistic before we moved into interviews. Public sources such as UN Comtrade trade statistics, USITC data, Eurostat, and national statistics agencies helped us track polymer output, downstream plastic processing activity, and regional manufacturing direction.

We also reviewed sources such as plastics and chemical trade associations, peer reviewed journals that discuss additive performance and migration behavior, and regulatory and standards references tied to packaging and electronics handling. For company-level context, filings, investor presentations, and reputable press were used to understand product positioning and capacity discussions. In selected cases, we also leaned on paid subscriptions that support company financials and intelligence, patent searches, and shipment-level trade views. These examples are illustrative only, and there were many other sources used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work focused on validating how anti-static agents are bought and used across packaging, electronics, automotive, and other polymer-heavy end uses, and then checking pricing logic by form and chemistry. We spoke with a mix of additive suppliers, polymer compounders, converters, and downstream users across APAC, EMEA, and the Americas, so regional mix, substitution, and compliance-driven shifts could be reflected in assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 15% | APAC: 45% |

| Mid tier: 43% | Functional/Unit leaders: 42% | EMEA: 31% |

| Smaller Players: 20% | Managers: 43% | Americas: 24% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where polymer processing demand is reconstructed by region using plastics production indicators, trade movements, and end-use activity, and then translated into anti-static agent consumption through typical loading rates and penetration by application. Since end markets behave differently, inputs are tuned using market fingerprints such as packaging film and rigid packaging volumes, electronics and ESD-sensitive manufacturing output, polymer mix shifts (for example PP and PE versus PVC), and observed price bands by chemistry and form (liquid, pellets, or powder).

To keep totals grounded, results are corroborated with selective bottom-up approximations like sampled supplier revenue bands, channel checks with compounders and converters, and a simple volume times ASP cross-check for major regions. When a direct value for a smaller country or niche polymer is hard to confirm, it is bridged using proxy variables such as polymer demand growth, industrial production trends, and import dependence, and then reviewed again through interviews.

For forecasting, we rely on scenario analysis supported by short variable-based projections for plastics demand, packaging output, and electronics manufacturing momentum. The assumptions are adjusted when primary respondents signal step changes such as regulatory pressure on certain chemistries or faster adoption of bio-based sources.

Data Validation & Update Cycle

Validation is done through consistency checks between the modeled market value and independent signals like polymer processing trends, regional trade direction, and known pricing ranges for common anti-static chemistries. Any sharp jumps are investigated, and the drivers are re-tested through follow-up outreach or additional desk checks before the number is signed off.

A multi-step internal review is followed so assumptions, units, and currency conversions are aligned across regions and years. The report is refreshed on an annual cycle, and interim updates are triggered when material events occur (for example, a major regulatory change or a clear demand shock). Right before delivery, the model is re-run with the latest available public indicators so clients receive an updated view.

Mordor Intelligence's Anti Static Agents Market Size Compared With Other Published Estimates

Published market sizes for anti-static agents do not always match, even when they look like they are talking about the same topic. The gaps usually come from differences in what gets counted as revenue, which end uses are emphasized, and what base year and currency timing are applied.

Packaging and electronics demand signals, along with polymer processing activity and cross-checked price bands by common chemistries, are the evidence points that keep Mordor Intelligence's estimate tied to additives sold into industrial plastics value chains instead of adjacent finished goods revenue. Other figures can move higher when broader market items are included, such as downstream converted products, or when higher assumed loading rates and faster ASP progression are applied without re-checking adoption by polymer and region.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 562.92 M (2025) | |

| Global Consultancy A | USD 615.70 M (2024) | Uses a different base year and forecast window, and it appears to assume higher penetration in packaging and electronics, which can lift volumes when converted into revenue. |

| Industry Publisher B | USD 1361.00 M (2026) | Looks to use a wider product and application coverage that extends beyond industrial polymer additives, and the longer forecast horizon with higher growth expectations increases the stated value. |

Reading the three numbers together, most of the spread can be traced back to scope boundaries, base-year choice, and how adoption and pricing are projected across end uses and regions. By keeping inputs tied to observable polymer processing signals and then re-checking them through supplier and converter feedback, the final number stays transparent and repeatable.

Key Questions Answered in the Report

What is the current Anti-static Agents Market size?

The antistatic agent market is valued at USD 591.69 million in 2026, with a forecast to reach USD 759.08 million by 2031.

Which polymer consumes the most antistatic additives?

Polypropylene leads, representing 34.55% of 2025 demand and growing at 6.52% CAGR as it dominates e-commerce packaging and automotive interiors.

Why are bio-based antistatic agents gaining popularity?

Corporate sustainability goals and PFAS-related regulations are driving a 7.21% CAGR for bio-based variants, even as petrochemical grades remain cost competitive.

Which region is expanding fastest in antistatic agent consumption?

Asia-Pacific shows the quickest pace with a 6.63% CAGR thanks to semiconductor fabrication and automotive manufacturing hubs.

Page last updated on: