Global Animal Sedative Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

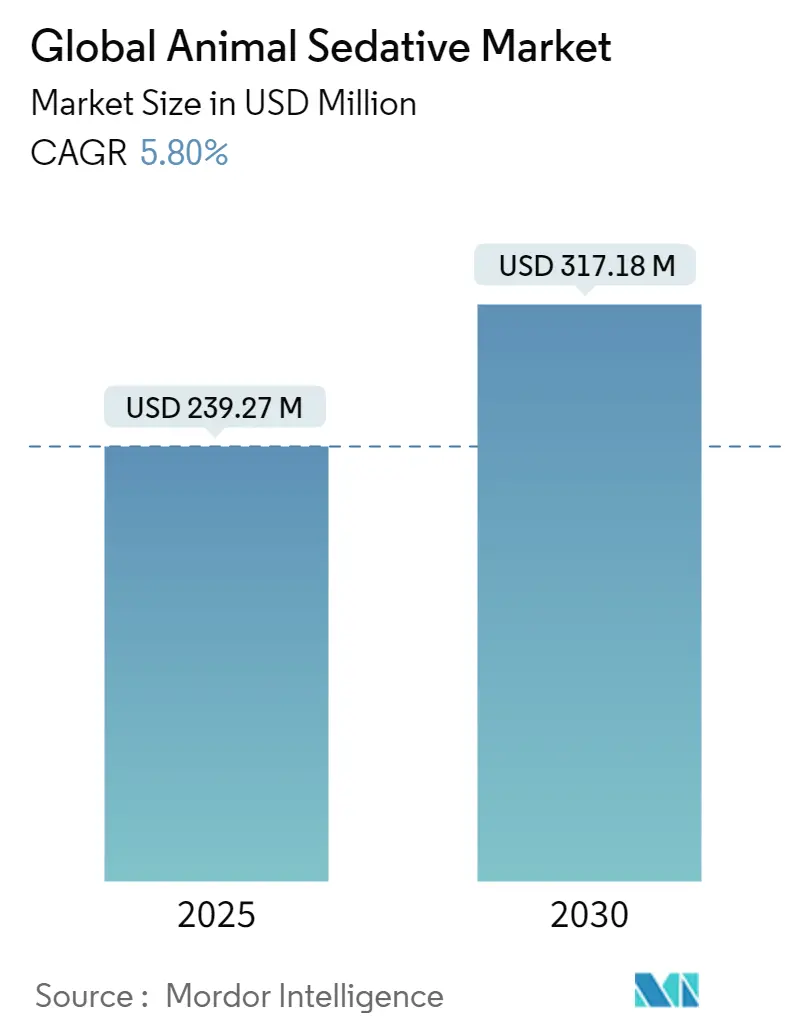

| Market Size (2025) | USD 239.27 Million |

| Market Size (2030) | USD 317.18 Million |

| Growth Rate (2025 - 2030) | 5.80% CAGR |

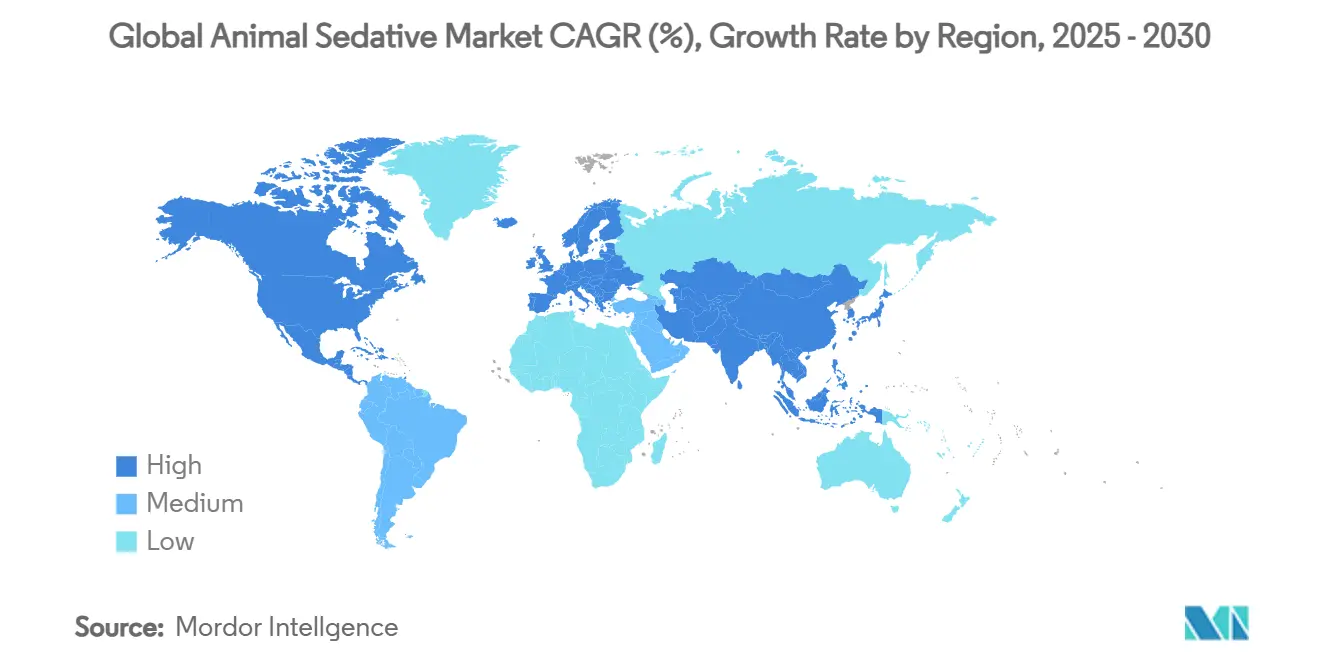

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

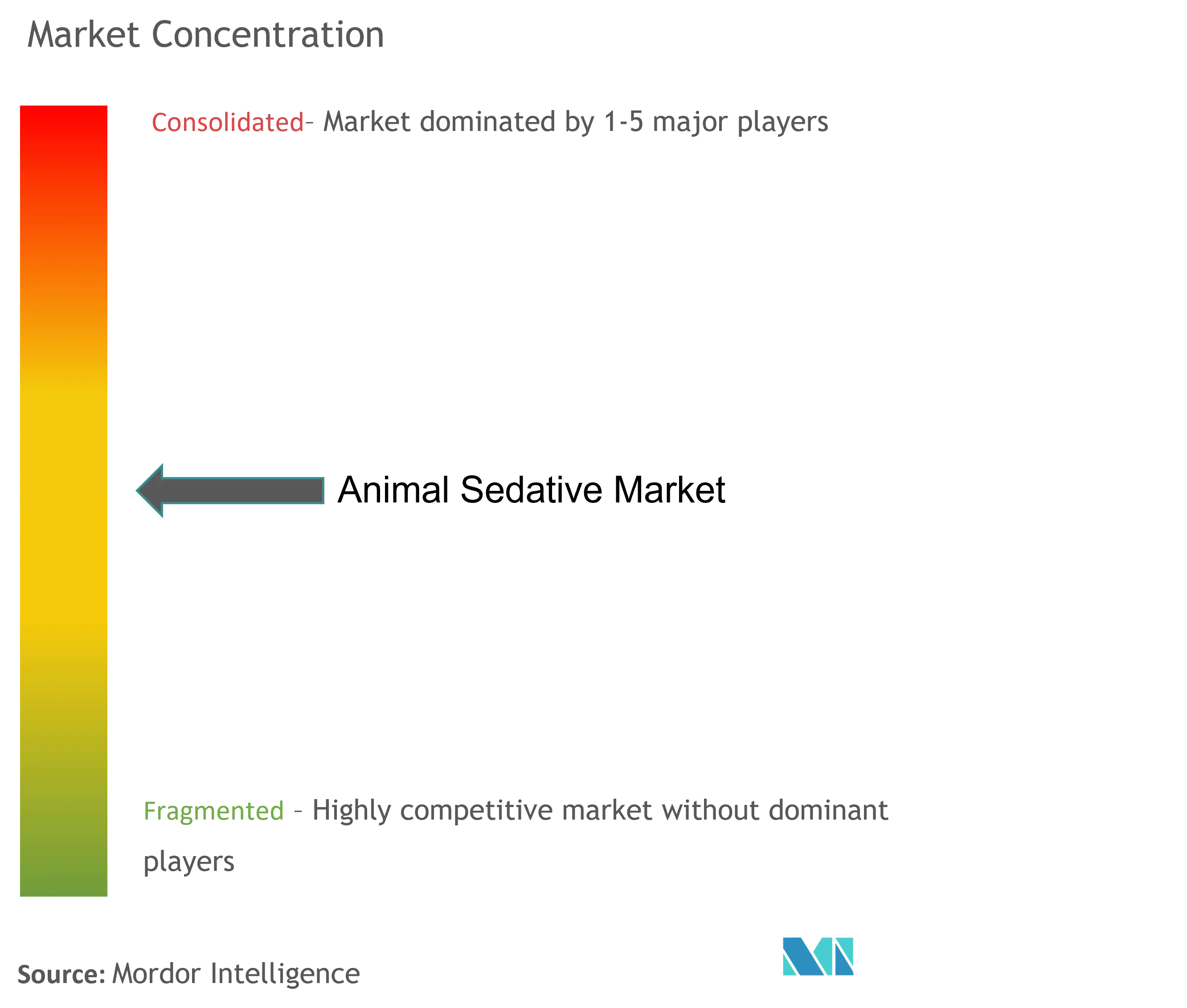

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Animal Sedative Market Analysis by Mordor Intelligence

The animal sedative market is valued at USD 239.27 million in 2025 and is projected to reach USD 317.18 million by 2030, advancing at a 5.8% CAGR. Adoption is rising because veterinarians now rely on tailored sedation protocols that support complex minimally invasive surgery, advanced imaging, and behavioral care. Combination α2-agonist products that cut cardiovascular risk, growing pet-insurance enrollment that lowers out-of-pocket costs, and sustained growth in conservation projects that depend on chemical immobilization all underpin demand. At the same time, escalating regulatory scrutiny of xylazine diversion and persistent shortages of board-certified veterinary anesthesiologists introduce operational hurdles that suppliers must navigate. Across regions, technological innovation, public-health concerns, and shifting pet-owner expectations intersect to define both opportunities and compliance obligations for participants in the animal sedative market.

Key Report Takeaways

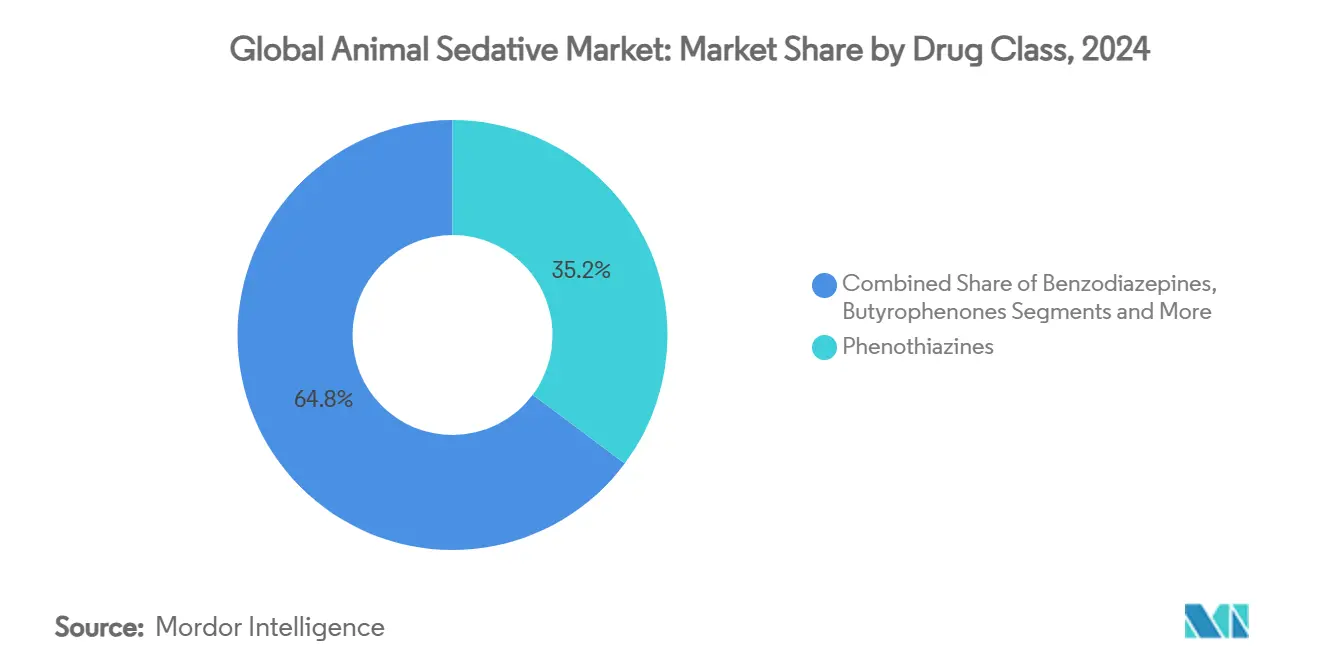

- By drug class, phenothiazines led with 35.2% of animal sedative market share in 2024, while α2-agonists are forecast to expand at a 9.8% CAGR to 2030.

- By application, surgical procedures held 42.8% of 2024 revenue; behavior and noise-anxiety management is projected to grow the fastest at 10.5% CAGR through 2030.

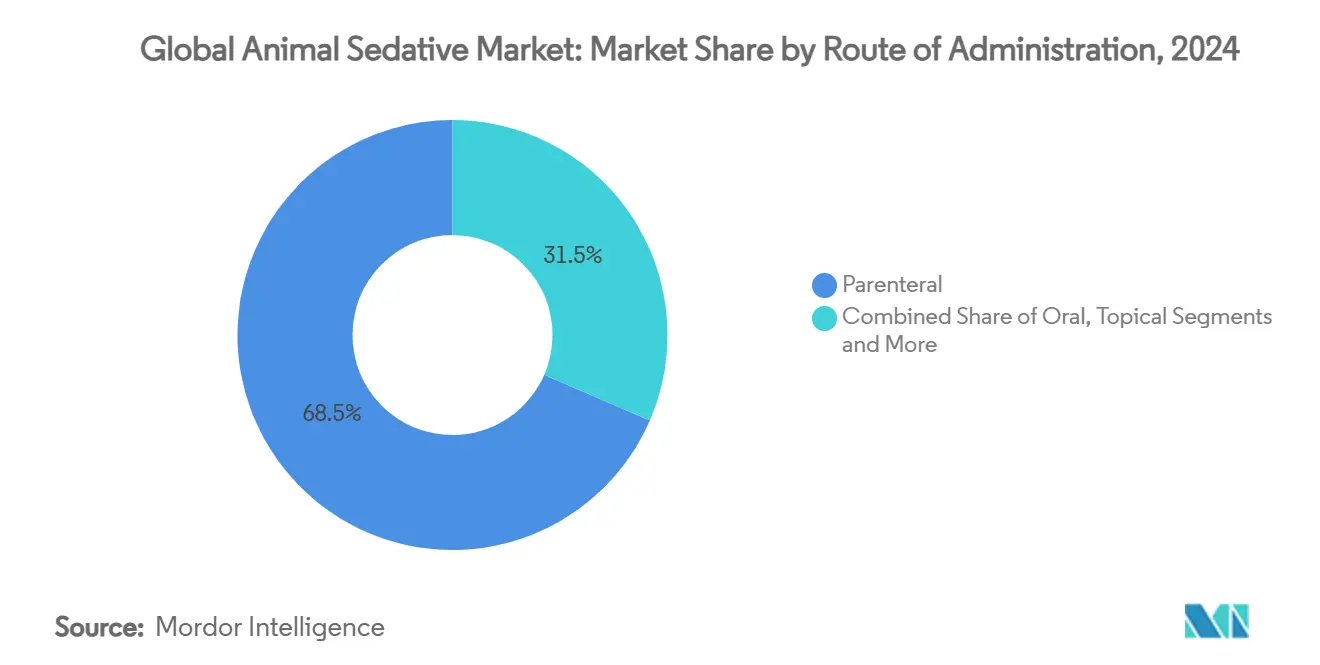

- By route of administration, parenteral products captured 68.5% revenue in 2024, yet transmucosal delivery is set to record the highest 11.2% CAGR during the period.

- By animal type, companion animals commanded 51.2% of 2024 revenue and are advancing at an 8.9% CAGR through 2030.

- By geography, North America accounted for 40.3% of 2024 sales; Asia Pacific is poised for the quickest 9.4% CAGR to 2030.

Global Animal Sedative Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDA approvals of novel α2 combination sedatives | +1.20% | Global, early uptake in North America and EU | Medium term (2-4 years) |

| Growing minimally-invasive companion-animal procedures | +0.90% | North America and EU core, spreading to APAC | Long term (≥ 4 years) |

| Rising pet-insurance coverage | +0.70% | North America and EU, expanding in APAC cities | Medium term (2-4 years) |

| Increased R&D spending on advanced veterinary anesthesia | +0.60% | Global, focused in developed markets | Long term (≥ 4 years) |

| Wildlife relocation projects requiring chemical immobilization | +0.30% | Conservation hotspots worldwide | Short term (≤ 2 years) |

| Sustainability push for low-carbon anesthetic protocols | +0.20% | EU and North America, global diffusion | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in FDA Approvals Of Novel Α2 Combination Sedatives

The FDA’s recent fast-track approach for veterinary α2-agonist combinations is reshaping sedation practice. Zenalpha, cleared in December 2024, combines medetomidine with vatinoxan to maintain central sedation while blocking peripheral receptors, reducing bradycardia and hypotension risks. PropofolVet Multidose, approved in November 2024, adds formulary competition in injectables and signals regulators’ willingness to expand choice in anesthesia.[1]U.S. Food and Drug Administration, “PropofolVet Multidose Approval,” fda.gov Together, these clearances illustrate a shift toward precision sedation, prompting developers to prioritize customizable, reversible formulations that minimize systemic stress yet support efficient workflow.

Expansion of Companion-Animal Minimally Invasive Procedures

Endoscopy, laparoscopy, and advanced imaging now feature routinely in companion-animal medicine, each demanding reliable sedation to prevent motion artifacts and maintain analgesia. Guidelines from the American Animal Hospital Association classify anesthesia-free dentistry as unacceptable, making standardized sedation mandatory for oral care.[2]DVM360 Editorial Staff, “Anesthesia‐Free Dentistry Standards,” aaha.org Teaching hospitals in Japan report more sedative prescriptions supporting imaging and biopsy protocols, reflecting owners’ willingness to pay when insurance covers advanced diagnostics. Short-acting drugs with rapid reversal dominate in this outpatient-focused environment, driving interest in new α2-agonist combinations and transmucosal options.

Rising Pet-Insurance Coverage Boosting Spend on Sedation

Pet-insurance enrollment already exceeds 30% in many urban U.S. markets, lowering economic barriers to elective or preventive procedures that require sedation. Feline-specific solutions such as Bonqat, which addresses transport anxiety, help close the gap between dog and cat clinic visits. Higher traffic in clinics lifts procedure volumes, which, in turn, encourages manufacturers to launch cost-efficient multi-dose products and invest in training resources for general practitioners.

Growing R&D Investment in Advanced Veterinary Anesthesia

Market leaders allocate larger R&D budgets to new molecules, delivery systems, and reversal agents. Zoetis alone has introduced more than 2,000 products in the past decade, while Boehringer Ingelheim added specialized vaccine technology through the acquisition of Saiba Animal Health. Patent filings show that the industry focuses on buccal, sublingual, and intranasal routes that improve compliance and reduce stress. This confirms that product differentiation now lies in formulation science rather than simply new active ingredients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adverse cardiovascular and neurologic events | -0.80% | Worldwide, heightened oversight in developed markets | Medium term (2-4 years) |

| Stringent multi-agency regulatory timelines | -0.60% | Global, most acute in North America and EU | Long term (≥ 4 years) |

| Recreational diversion of xylazine tightening controls | -0.50% | North America core, extending to EU | Short term (≤ 2 years) |

| Shortage of certified veterinary anesthesiologists | -0.40% | Worldwide, acute in developed markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Adverse Cardiovascular & Neurologic Events of Sedatives

FDA pharmacovigilance data list 1,910 dexmedetomidine-linked adverse events between 2004 and 2023, including bradycardia, hypotension, and rare neurologic complications such as diabetes insipidus.[3]Frontiers in Pharmacology, “Dexmedetomidine Adverse Events,” frontiersin.org Prolonged hypotension after acepromazine and respiratory depression with α2-agonists require intensive monitoring, limiting adoption in clinics without advanced equipment. Emerging combination products aim to mitigate these effects, but safety concerns still curb expansion in resource-constrained markets.

Recreational Diversion of Xylazine Driving Tighter Controls

Xylazine now appears in illicit drug samples across 49 U.S. states, prompting the Combating Illicit Xylazine Act that proposes Schedule III status while safeguarding veterinary use. Legislative uncertainty adds compliance costs, complicates interstate logistics, and could disrupt supply for large-animal and wildlife sectors that rely on xylazine for reliable immobilization.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Drug Class: a2-Agonists Gain On Phenothiazine Incumbency

Phenothiazines held a 35.2% share of the global animal sedative market in 2024, owing to decades of routine use. However, α2-agonists are projected to record the fastest 9.8% CAGR amid rising demand for concurrent analgesia and reversibility. The animal sedative market size for α2-agonists is expected to expand notably in small-animal practices where medetomidine combinations offer shorter recovery and cardiovascular stability. Benzodiazepines fill stress-reduction niches for feline transport, while dissociatives and butyrophenones remain staples for exotic species. Opioids continue as adjuncts, but regulatory complexity keeps their growth muted. Future gains hinge on combination products that address phenothiazine hypotension and α2 cardiovascular suppression.

Advances in receptor-selective pairing, such as medetomidine plus vatinoxan, showcase how focused pharmacology can shift market preference. These innovations compete against injectable phenothiazines on safety profiles rather than cost alone. Cannabinoid research and neuro-steroid compounds sit in the pipeline, signaling a potential re-ordering of drug-class rankings over the forecast horizon as intellectual property barriers expire and new molecules debut.

By Application: Behavioral Use Accelerates Beyond the Surgical Core

Surgery generated 42.8% of 2024 revenue and remains indispensable, yet behavioral and noise-anxiety sedation is rising at a 10.5% CAGR. The animal sedative market size for behavioral indications is widening because veterinarians now advocate stress-free visits as a standard of care. Dental procedures, enhanced by the AAHA stance against anesthesia-free cleaning, continue to underpin surgical volume. Diagnostic imaging also benefits, as motion-free scans demand deep, controlled sedation.

Noise-phobia, travel stress, and owner-requested calm for at-home grooming are new revenue streams. Bonqat’s pregabalin formula exemplifies products designed expressly for behavioral use, offering oral administration that eliminates clinic injection anxiety. Transport and wildlife relocation segments likewise depend on predictable onset and quick reversal, and remote darting technology extends adoption outside traditional clinical walls.

By Route of Administration: Transmucosal Delivery Disrupts Injectable Tradition

Parenteral solutions still generated 68.5% of 2024 revenue, reflecting their reliability. However, transmucosal and topical systems are forecast to grow 11.2% annually as clinics prioritize patient comfort. The animal sedative market share for parenteral products will erode modestly but remain dominant through 2030 because complex surgery and emergency care still favor intravenous or intramuscular control.

Oral gels such as detomidine for horses reach procedure success rates of 76% compared with 7% on placebo, revealing the clinical appetite for stress-free routes. Sublingual and intranasal devices are under patent review, promising better absorption and owner-administered options. Injectable suppliers answer by launching multi-dose preservatives and smaller-gauge pre-filled syringes to reduce pain and waste.

By Animal Type: Companion Animals Continue to Lead Adoption

Companion animals held 51.2% revenue share in 2024 and will expand at an 8.9% CAGR. Canine cases dominate volume, but feline growth is newly energized by anxiety-focused oral solutions. Livestock uptake is steady yet tempered by drug-residue rules, while equine demand centers on convenient oral sedatives that fit performance testing frameworks. Wildlife and zoo programs, although niche, influence formulation R&D through calls for high-potency, low-volume injectables. Constrained veterinary infrastructure in emerging economies limits advanced anesthetic monitoring, yet this gap also drives interest in extended-release protocols that cut repeat dosing.

By Formulation Type: Injectables Retain Primacy in a Diversifying Mix

Injectables remain preferred for their rapid onset and controlled depth, highlighted by FDA clearance of PropofolVet Multidose in 2024. Oral tablets and capsules handle pre-visit stress management, whereas gels and pastes hold niches in equine and exotic care. Research into liposome-encapsulated sedatives suggests impending longer-acting injectables that also lower systemic exposure. Transdermal patches and temperature-responsive hydrogels are early-stage but illustrate how convenience and safety will frame competitive differentiation.

By End-user: Veterinary Hospitals Shape Clinical Innovation Uptake

Comprehensive monitoring capabilities at veterinary hospitals make them the first to adopt new combination products and device-enabled delivery. Clinics generate the bulk of doses across routine services, favoring dependable, budget-sensitive lines. Academic institutes validate off-label protocols and document safety data that influence label expansion. Zoos and wildlife centers co-develop dartable formulations and reversal agents to support conservation missions. Tele-veterinary expansion and mobile practices are emerging channels; both require portable, easy-to-reconcile sedation kits, creating a crossover market between hospital-grade and field-ready products.

Geography Analysis

North America contributed 40.3% of 2024 revenue thanks to sophisticated referral hospitals, high pet-insurance adoption, and an FDA framework that expedites veterinary-drug approvals. The United States drives most demand, with Canada supplementing through robust livestock and wildlife programs, while Mexico rounds out regional growth through rising small-animal care standards. Regulatory focus on xylazine diversion adds compliance burdens but also fuels demand for safer α2 alternatives. The animal sedative market size for North America will keep expanding as insurers cover more elective procedures, yet competition intensifies due to generics such as PropofolVet Multidose.

APAC is the fastest-growing geography at a 9.4% CAGR. China’s Ministry of Agriculture approval pathway, though stringent, favors established manufacturers, giving multinationals an edge. Japan shows mature demand, characterized by complex prescription patterns that mirror U.S. trends. India’s pharmacovigilance initiatives elevate safety benchmarks and accelerate premium product uptake in urban centers. Varying veterinary-specialist availability across the region limits deep sedation adoption, yet rapid urbanization and disposable-income growth offset these constraints.

Europe benefits from strong welfare legislation and eco-conscious buyers who prefer low-carbon TIVA protocols over volatile inhalants. Germany and the United Kingdom anchor demand via large companion-animal populations and advanced veterinary curricula, while France and Italy contribute through mixed livestock and pet sectors. Stringent EMA and local regulations raise barriers for entrants but reward suppliers that meet high safety and environmental standards. South America and the Middle East & Africa remain emerging, with livestock management and growing pet ownership driving baseline demand, though uneven infrastructure may slow uptake of advanced anesthetic monitoring.

Competitive Landscape

Market concentration is moderate: a cluster of multinational firms controls the broadest portfolios, yet niche innovators compete through formulation science. Zoetis tops revenue tables with USD 8.5 billion in 2025 animal-health sales, highlighting new offerings such as Bonqat and monoclonal antibodies that complement sedation protocols. Boehringer Ingelheim posted EUR 4.7 billion (USD 5.5 billion) in 2025 animal-health revenue and strengthened its pipeline via the Saiba Animal Health acquisition that adds virus-like-particle vaccines requiring dependable anesthesia during administration. Dechra leverages Zenalpha to differentiate in the reversible-sedation segment, while Parnell positions generics like PropofolVet Multidose to win on cost.

Patents covering transmucosal devices, sustained-release injectables, and dual-chamber syringes illustrate how technology serves as a market-entry moat for emerging players. Tightening xylazine controls favors companies with compliance infrastructure and validated supply chains.

Shortage of certified anesthesiologists motivates suppliers to fund residency programs and simplify protocols, thereby expanding the practitioner base that can employ advanced sedatives safely. Strategic alliances with veterinary schools and professional associations accelerate field adoption and underpin brand trust.

Global Animal Sedative Industry Leaders

Elanco

Ceva

Merck & Co. Inc.

Dechra Pharmaceuticals PLC

Zoetis Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Dechra won FDA approval for Otiserene (marbofloxacin, terbinafine, dexamethasone) single-dose otic suspension for canine otitis externa.

- April 2025: Zoetis updated U.S. Librela labeling after analysis of more than 1 million treated dogs and 25 million doses worldwide.

- March 2025: Zoetis reported Librela matched meloxicam for pain relief in canine osteoarthritis while posting fewer adverse events across a 101-dog study.

- February 2025: AVMA reintroduced the Combating Illicit Xylazine Act, targeting Schedule III status for xylazine while preserving veterinary exemptions.

- December 2024: FDA cleared Zenalpha (medetomidine + vatinoxan) for canine sedation, delivering onset in 14 minutes and recovery in 38 minutes with reduced cardiovascular impact.

Global Animal Sedative Market Report Scope

As per the report's scope, animal sedatives are drugs used on animals to reduce irritability and excitement. They are CNS depressants that interact with brain activities and decelerate them. They are injected before any medical procedure on animals. The Animal Sedative Market is Segmented by Drug Class (Phenothiazines, Benzodiazepines, alpha-2 adrenergic Receptor Agonists, Butyrophenones, and Other Drug Classes), Application (Surgical, Diagnosis, and Clinical Research Studies), Route of Administration (Oral and Parenteral), Animal Type (Small and Large), and Geography (North America, Europe, Asia Pacific, and Rest of the World). The report offers the value (in USD million) for the above segments.

| Phenothiazines |

| Benzodiazepines |

| ?2-Adrenergic Receptor Agonists |

| Butyrophenones |

| Dissociative Agents |

| Neuro-steroid Anesthetics |

| Opioids (Sedative adjuncts) |

| Other Classes |

| Parenteral |

| Oral |

| Transmucosal / Topical |

| Inhalational |

| Injectable Solutions |

| Tablets & Capsules |

| Gels / Pastes |

| Transdermal Patches |

| Companion Animals | Dogs |

| Cats | |

| Livestock | Cattle |

| Swine | |

| Others | |

| Equine | |

| Wildlife & Exotics |

| Surgical |

| Diagnostic Imaging & Dentistry |

| Clinical Research Studies |

| Behaviour / Noise-Anxiety Management |

| Transport & Handling |

| Veterinary Hospitals |

| Veterinary Clinics |

| Academic & Research Institutes |

| Zoos & Wildlife Centers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Drug Class | Phenothiazines | |

| Benzodiazepines | ||

| ?2-Adrenergic Receptor Agonists | ||

| Butyrophenones | ||

| Dissociative Agents | ||

| Neuro-steroid Anesthetics | ||

| Opioids (Sedative adjuncts) | ||

| Other Classes | ||

| By Route of Administration | Parenteral | |

| Oral | ||

| Transmucosal / Topical | ||

| Inhalational | ||

| By Formulation Type | Injectable Solutions | |

| Tablets & Capsules | ||

| Gels / Pastes | ||

| Transdermal Patches | ||

| By Animal Type | Companion Animals | Dogs |

| Cats | ||

| Livestock | Cattle | |

| Swine | ||

| Others | ||

| Equine | ||

| Wildlife & Exotics | ||

| By Application | Surgical | |

| Diagnostic Imaging & Dentistry | ||

| Clinical Research Studies | ||

| Behaviour / Noise-Anxiety Management | ||

| Transport & Handling | ||

| By End-user | Veterinary Hospitals | |

| Veterinary Clinics | ||

| Academic & Research Institutes | ||

| Zoos & Wildlife Centers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current value of the animal sedative market?

The animal sedative market stands at USD 239.27 million in 2025 and is forecast to reach USD 317.18 million by 2030 at a 5.8% CAGR.

Which drug class is growing the fastest?

Α2-agonists show the quickest expansion, posting a 9.8% CAGR through 2030 due to new combination products that lower cardiovascular risk.

Why is behavioral sedation gaining importance?

Owner demand for stress-free clinic visits and products like pregabalin oral solutions is driving a 10.5% CAGR in behavior and noise-anxiety applications.

How are regulatory changes around xylazine affecting the market?

Proposed Schedule III classification in the United States increases compliance burdens and may shift demand to alternative sedatives that retain efficacy without similar diversion risk.

Which region offers the strongest growth outlook?

Asia Pacific leads with a 9.4% CAGR thanks to rising pet ownership, improving veterinary infrastructure, and regulatory pathways that increasingly recognize advanced formulations.

Page last updated on: