Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

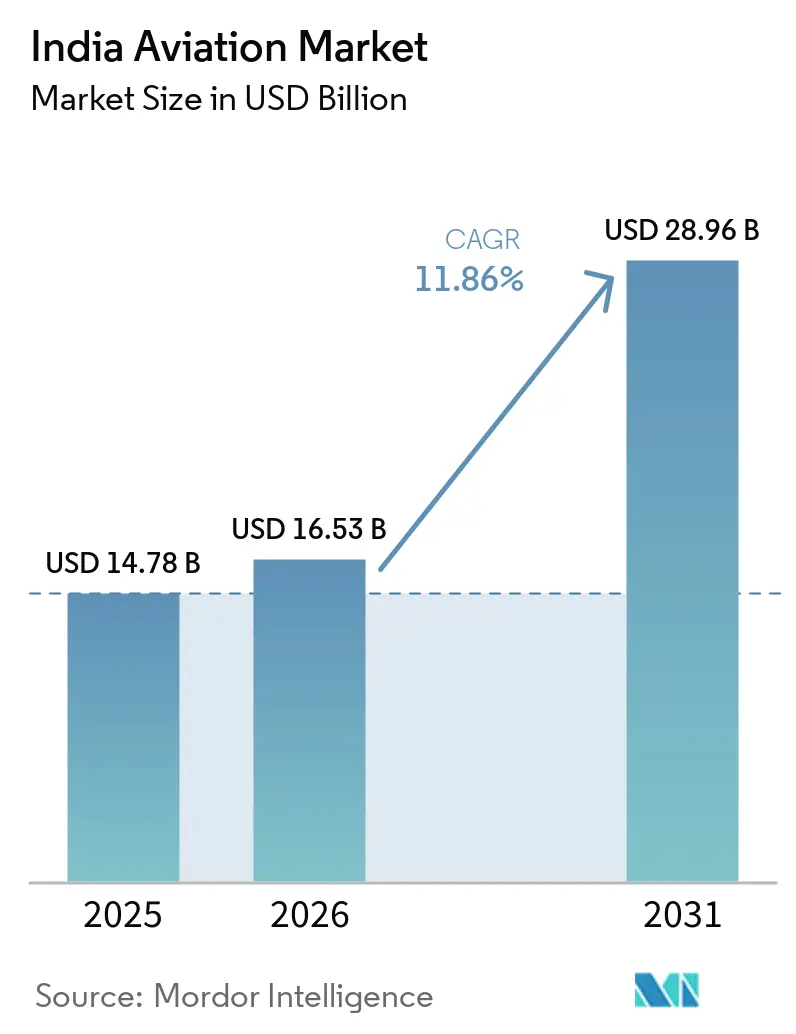

| Base Year Market Size (2025) | USD 14.78 Billion |

| Market Size (2026) | USD 16.53 Billion |

| Market Size (2031) | USD 28.96 Billion |

| Growth Rate (2026 - 2031) | 11.86% CAGR |

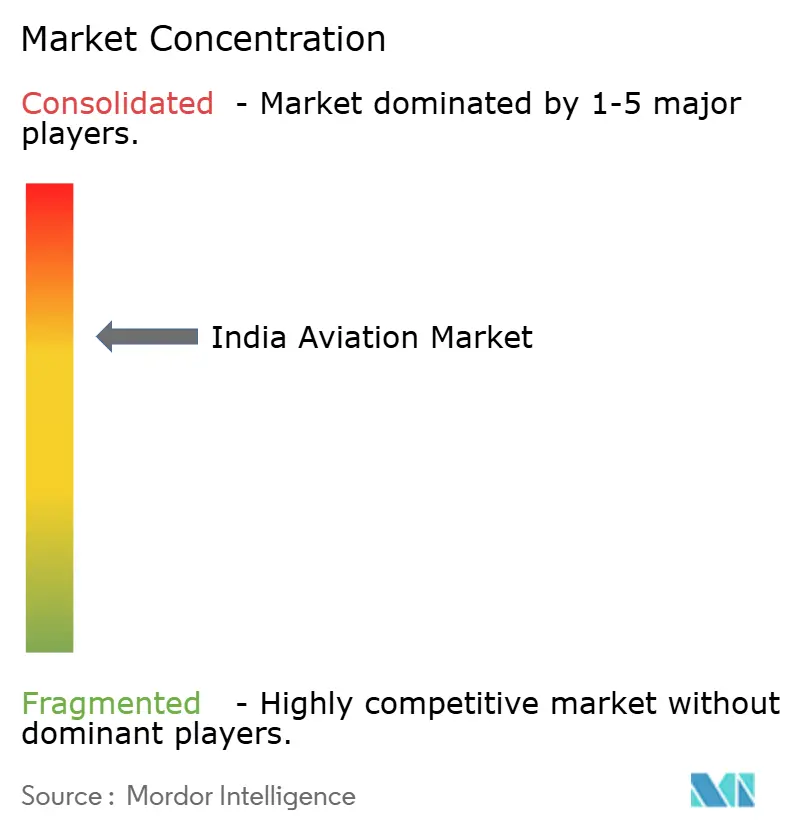

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Aviation Market Analysis by Mordor Intelligence

The India Aviation market size is expected to grow from USD 14.78 billion in 2025 to USD 16.53 billion in 2026 and is forecast to reach USD 28.96 billion by 2031 at 11.86% CAGR over 2026-2031. Domestic traffic has almost regained its pre-pandemic momentum, and policy support through the UDAN regional connectivity scheme keeps new routes commercially viable. The intensification of fleet modernization by leading airlines, higher defense outlays, and a widening e-commerce footprint in Tier 2 and Tier 3 cities reinforces demand for aircraft, engines, and air cargo infrastructure. However, fuel-price swings, infrastructure gaps at smaller airports, and shortages of flight crews and maintenance engineers act as counterweights to growth. The India Aviation market benefits from synchronized public spending, private capital, and latent travel demand, creating a compelling medium-term outlook.

Key Report Takeaways

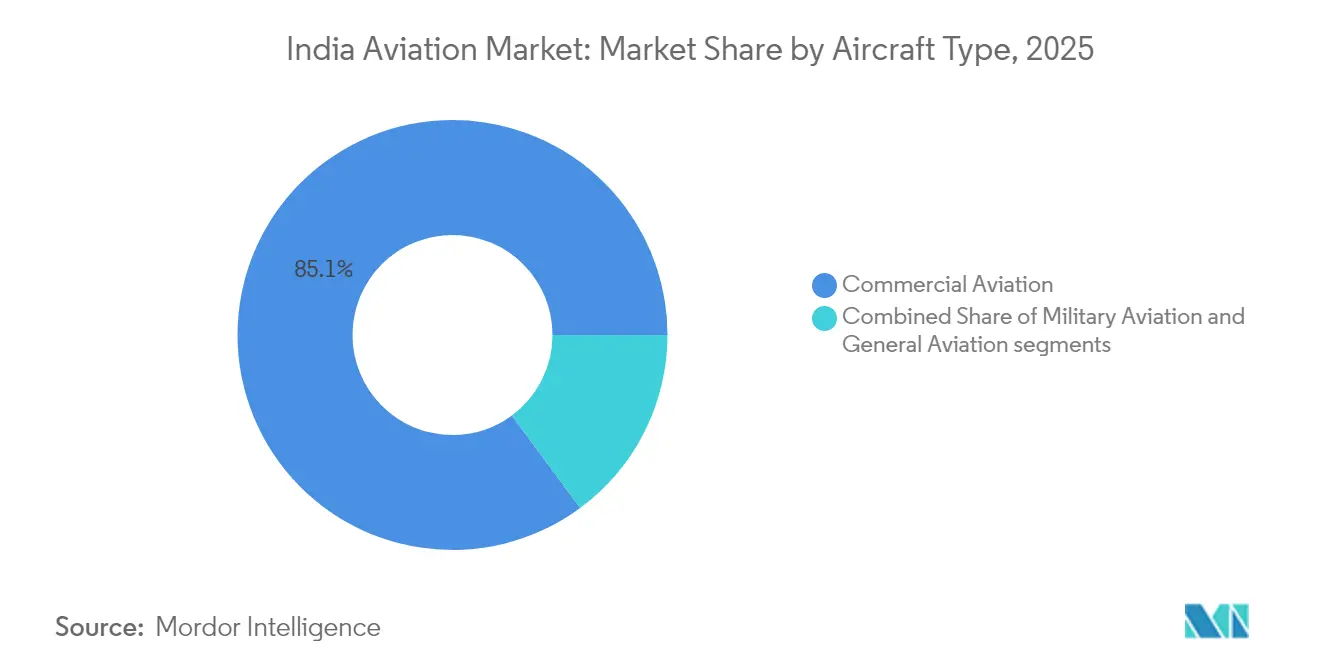

- By aircraft type, commercial aviation held 85.12% of the India Aviation market share in 2025, while military aviation is growing the fastest at a 13.92% CAGR through 2031.

- By propulsion technology, turbofan engines dominated the Indian aviation market with 70.65% of the market size in 2025; electric-and-hybrid systems are the fastest-growing group at a 14.73% CAGR.

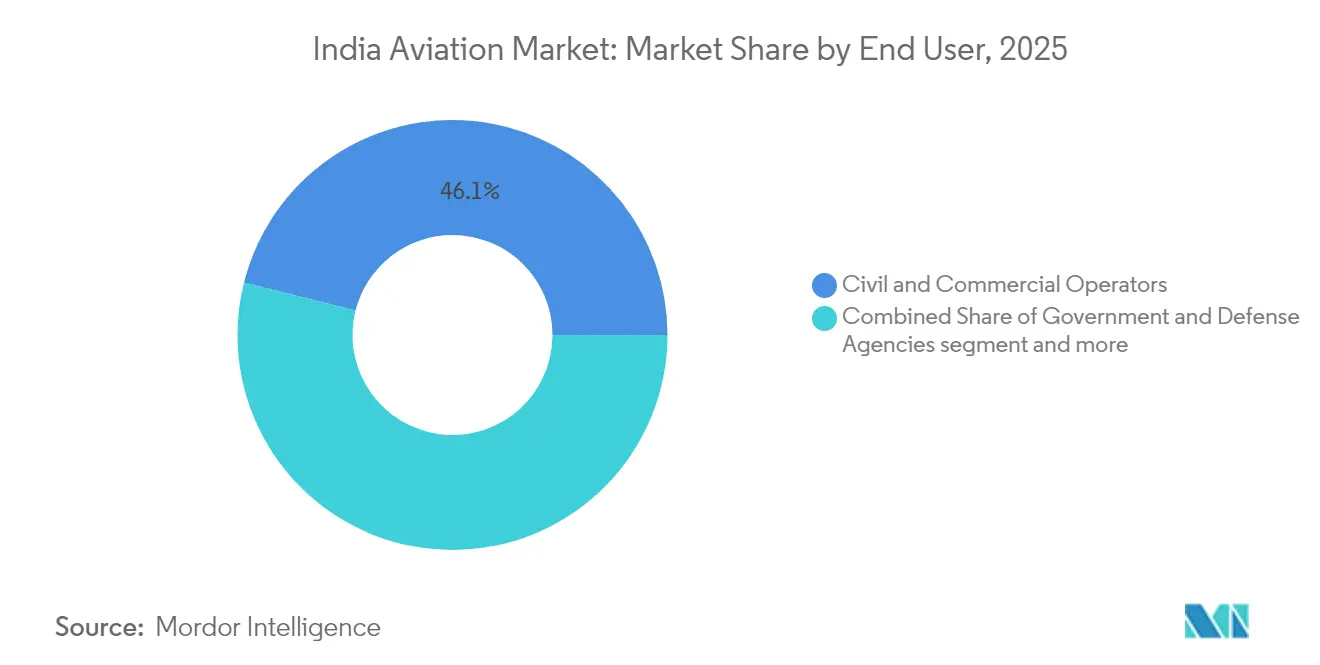

- By end user, civil and commercial operators accounted for 46.08% of the India Aviation market size in 2025, whereas government and defense agencies delivered the highest 13.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Aviation Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-COVID passenger rebound and airport capacity expansion | +3.2% | Mumbai, Delhi, Bengaluru, Hyderabad | Medium term (2-4 years) |

| India’s FY27 target of over 220 operational airports | +2.8% | Tier-2 and Tier-3 cities nationwide | Long term (≥ 4 years) |

| Increase in defense capital outlay driving military aircraft orders | +2.1% | Bengaluru, Hyderabad, Nashik manufacturing hubs | Long term (≥ 4 years) |

| Growing express cargo demand from e-commerce in Tier-2 and Tier-3 cities | +1.9% | Uttar Pradesh, Bihar, Rajasthan, Madhya Pradesh | Medium term (2-4 years) |

| Tax incentives supporting indigenous avionics research and development | +1.2% | Aerospace clusters of Karnataka, Tamil Nadu, Maharashtra | Long term (≥ 4 years) |

| SAF blending mandate from 2027 catalyzing new aviation fuel supply chains | +0.8% | Major airports in Delhi, Mumbai, Bengaluru | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-COVID passenger rebound and airport capacity expansion

Domestic passenger traffic increased to 164 million in 2024, representing 95% of the 2019 level, while international recovery reached 87%.[1]Directorate General of Civil Aviation, “Traffic Statistics – 2024,” dgca.gov.in The number of operational airports doubled from 74 in 2014 to 148 by 2024, easing slot congestion at Delhi, Mumbai, and Bengaluru. Capacity additions, such as Navi Mumbai International Airport and the enlargement of Delhi Terminal 1, have increased available slots by 35% since 2022, supporting a projected 300 million passengers by 2030.[2]Airports Authority of India, “Annual Report 2024,” aai.aero These steps address historical choke points and redistribute traffic across a broader airport network, aligning runway, terminal, and air traffic control investments with latent demand. Accelerated certification of new airports under UDAN further tightens the link between infrastructure rollout and traffic recovery, ensuring that the India Aviation market maintains momentum even as yields normalize.

India’s FY27 target of over 220 operational airports

Seventy-two new airports are at various stages of construction as of 2024, bringing the planned total to more than 220 by FY27. Greenfield sites in Jewar, Dholera, and Bhogapuram complement brownfield upgrades, raising national capacity while bringing aviation access to 1 billion Indians. Dedicated cargo hubs are integrated into the rollout, directly responding to a 15% annual growth in cargo. UDAN 5.0 added 25 fresh routes and 19 helicopter links during 2024, underscoring the government’s campus-to-capital connectivity model.[3] Press Information Bureau, “UDAN 5.0 Launch,” pib.gov.in The program aligns with the Make-in-India initiative by establishing new maintenance bases and parts-manufacturing clusters near emerging airports, thereby deepening supply-chain roots in underserved geographies.

Increase in defense capital outlay driving military aircraft orders

Defense capital expenditure reached INR 1.72 lakh crore (USD 20.6 billion) for FY25, with roughly one-quarter allocated to aviation projects. Procurement plans encompass 114 multi-role fighters, 57 carrier-based jets, and 123 naval helicopters, ensuring consistent demand through 2030. Hindustan Aeronautics Limited booked its largest-ever order backlog in 2024, spanning Tejas Mk1A fighters and Prachand light helicopters. Local-content rules that require 50% indigenous sourcing lift ancillary manufacturing, tooling, and composite-material suppliers. Defense procurement thus multiplies output beyond frontline aircraft to encompass avionics, engines, and maintenance ecosystems—vital inputs supporting growth in the Indian Aviation Market.

Growing express cargo demand from e-commerce in Tier-2 and Tier-3 cities

E-commerce penetration in smaller cities reached 35% in 2024, driving express air-cargo volumes up by 23% annually. Operators such as Blue Dart and Delhivery lifted freighter utilization to 78%, aided by night-parking approvals and slot relaxations. Regional airports in Coimbatore, Indore, and Bhubaneswar logged a 40% rise in cargo throughput, validating the thesis that air freight addresses the last-mile limitations of road logistics. Airlines view cargo as a hedge against passenger revenue cyclicality, prompting fleet conversions of aging narrowbodies. Government grants for cargo-terminal infrastructure under UDAN Cargo supplement private investment, accelerating multimodal connectivity across emerging consumption centers in the Indian Aviation Market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent volatility in aviation turbine fuel (ATF) prices and limited hedging options | –2.1% | Nationwide; highest pressure on smaller airlines | Short term (≤ 2 years) |

| Infrastructure bottlenecks at Tier-3 airports affecting logistics efficiency | –1.8% | Nationwide; acute gaps in regional and cargo operations | Long term (≥ 4 years) |

| Shortage of skilled pilots and aircraft maintenance engineers despite training initiatives | –1.4% | Remote cities across all regions | Medium term (2-4 years) |

| Rupee depreciation posing risks to dollar-denominated aircraft lease agreements | –1.2% | Nationwide; affects all carriers with international lease deals | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent volatility in aviation turbine fuel prices and limited hedging options

Aviation turbine fuel accounted for 35-40% of airline operating costs in 2024 and experienced intra-year price swings of 45%. State-level VAT differentials ranging from 1% to 30% further distort cost structures. Indian carriers hedge only 15% of their fuel needs, compared to 60–80% for global peers, a gap attributed to the absence of sophisticated derivatives in local markets. The cost spike forced fare surcharges, reduced capacity deployment by cash-strapped carriers, and increased break-even load factors. Without a functional jet-fuel futures market, airlines will continue to absorb volatility or pass it on to travelers, tempering the expansion of the India Aviation market’s profit pool over the near term.

Infrastructure bottlenecks at Tier-3 airports affecting logistics efficiency

Many Tier-3 airports operate single runways, possess limited cargo bays, and lack modern navigation aids, restricting aircraft types and nighttime operations. Forty percent are located more than 50 km from the nearest city center, diluting convenience gains from air travel and dampening load factors. UDAN route expansion sometimes outpaced ground-handling and passenger-amenity upgrades, leading to sub-optimal utilization of new connections. Weather-related diversions remain frequent because smaller airports still await installation of Category I landing systems. The resulting operational inefficiencies inflate costs for regional carriers and slow traffic diffusion away from congested metro hubs. This structural drag impedes balanced development of the India Aviation market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Aircraft Type: Commercial Dominance with Military Momentum

Commercial aviation accounted for 85.12% of the Indian aviation market size in 2025, driven by the expansion of full-service and low-cost carriers, which increased their fleets and frequencies. IndiGo’s order book and Air India’s post-merger fleet of 470+ aircraft underline narrowbody leadership, while widebodies gain traction for long-haul routes at an 10.85% CAGR. Military aviation, although smaller, expands at a rate, with the fastest growth at a 13.92% CAGR, fueled by domestic fighter programs and helicopter procurement under Atmanirbhar Bharat.

The breadth of the commercial segment aids cabin interiors, ground-support equipment, and digital services suppliers, creating a multiplier effect within the Indian aviation market. General aviation holding an 8.62% share, saw business jet registrations rise 35% in 2024, reflecting corporate India’s focus on time-efficient mobility. Military-segment acceleration broadens the industrial base, drawing private firms into tier-1 and tier-2 supply roles under offset obligations. Collectively, diversified aircraft demand procurement helps absorb manufacturing investments, stabilizing production volumes across market cycles.

By Propulsion Technology: Turbofan Scale Meets Alternative-Fuel Experimentation

Turbofan engines represented 70.65% of the Indian aviation market share in 2025, their dominance anchored in medium- and long-haul operations, where fuel efficiency and range remain paramount.The Indian aviation market size for turbofans is projected to rise at an 11.42% CAGR alongside the growth of narrowbody and widebody fleets. Turboprops, with 18.72% share, serve regional routes created under UDAN, especially where short runways favor their performance envelope.

Electric and hybrid systems offer the steepest trajectory, with a 14.73% CAGR, albeit from a small base. Government incentives and startup innovation encourage experimental platforms for training and short-haul commuter missions. Rolls-Royce, Safran, and Pratt & Whitney’s active partnerships with local MROs enhance engine-maintenance ecosystems, lowering total-cost-of-ownership barriers for operators. The development of SAF-compatible engine upgrades aligns propulsion innovation with national sustainability mandates, ensuring that the Indian aviation market evolves in lockstep with global decarbonization trends.

By End User: Civil Operators Lead, Defense Users Accelerate

Civil and commercial operators controlled 46.08% of the India Aviation market size in 2025, encompassing scheduled airlines, charter services, and dedicated freighters. Scheduled carriers dominate domestic seat capacity, while cargo specialists grow yield per kilogram in response to e-commerce demand spikes. Business aviation owners, corporates, and high-net-worth individuals held a 30.88% share, aided by fractional ownership and aircraft management models that lower entry barriers.

Government and defense agencies post the quickest 13.12% CAGR, reflecting elevated capital budgets for air-power modernization. Coast Guard and paramilitary aviation programs add multirole helicopters and surveillance aircraft, extending demand beyond the Air Force and Navy. The civil-military customer mix diversifies cash flows for OEMs and local suppliers, smoothing revenue cycles and encouraging technology spillovers. Balanced end-user growth, therefore, injects resilience into the Indian Aviation market, shielding it from single-segment shocks.

Geography Analysis

Metro hubs continue to anchor air traffic, yet regional airports are gaining ground as connectivity broadens and cities expand into rural areas. The northern region, led by Delhi’s Indira Gandhi International Airport, captured 31.45% of passenger traffic and 34% of freight in 2025. Western India, including Mumbai and Pune, contributed a 27.62% share, secured by financial services, travel, and pharmaceutical exports. Southern India shows the most substantial upside at a 13.76% CAGR, driven by Bengaluru’s technology corridor, Hyderabad’s aerospace cluster, and Chennai’s auto-component hub.

Tier-1 cities, including Delhi, Mumbai, Bengaluru, Chennai, Kolkata, and Hyderabad, accounted for 68% of passenger traffic in 2024, down from 78% in 2019, highlighting the success of regional connectivity. Cargo flow follows a different map: Delhi and Mumbai process 45% of international freight, whereas Chennai and Bengaluru lead in automobile and electronics exports, respectively.

International connectivity remains heavy in the Middle East, accounting for 35% of outbound modernization passengers, reflecting labor migration and transit linkages. Southeast Asia accounts for 22%, energized by tourism and electronics supply chain ties, while Europe holds 18% due to business travel and diaspora. Smaller achieve progressively higher ICAO Category I status by earning Category I status through the implementation of higher landing systems and advanced air traffic management upgrades under phased modernization plans. Collectively, geographic diversification distributes economic gains, lowers congestion risk, and embeds aviation more deeply into regional development strategies, reinforcing long-term growth for the Indian aviation market.

Competitive Landscape

Aircraft manufacturing and airline operations exhibit moderate concentration, with Airbus SE and The Boeing Company supplying approximately 85% of commercial aircraft, which command price and delivery slot premiums. Hindustan Aeronautics Limited retains 60% of indigenous military production and leads local systems integration, while private firms such as Tata Advanced Systems scale composite aerostructures. On the airline side, IndiGo holds 57% domestic share, leveraging cost discipline and high utilization. Air India’s ongoing merger with Vistara creates a challenger with substantial widebody orders and a USD 70 billion fleet modernization plan.

Strategic tie-ups proliferate: Tata Boeing Aerospace rolls out Apache fuselages in Hyderabad, and the Airbus-Tata consortium is preparing to assemble the C-295 transport aircraft at Vadodara. Engine OEMs deepen their presence via in-country MRO sites, illustrated by Rolls-Royce’s Trent-engine service center in Bengaluru, which created 500 skilled jobs in 2024. Airport privatization adds a fresh competitive layer, with GMR and Adani vying to deliver superior passenger experiences through biometric boarding and digital retail platforms.

White-space opportunities lie in regional aviation, cargo freighter conversions, and third-party maintenance. DGCA’s updated Civil Aviation Requirements accommodate experimental aircraft types, facilitating orderly yet agile innovation. Overall, the India Aviation market rewards players who blend cost efficiency with technological agility and eco-friendly credentials.

India Aviation Industry Leaders

Airbus SE

Hindustan Aeronautics Limited (HAL)

The Boeing Company

Dassault Aviation

Lockheed Martin Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: India signed a deal worth INR 623.70 billion (USD 7.03 billion) with state-owned Hindustan Aeronautics Ltd (HAL) to purchase domestically manufactured fighter aircraft as part of its military modernization program.

- September 2025: The Ministry of Defence (MoD) finalized a contract with Hindustan Aeronautics Limited (HAL) for 97 Tejas Mark-1A light combat aircraft for the Indian Air Force. The procurement comprises 68 fighter jets and 29 twin-seater aircraft, including associated equipment. The delivery schedule spans six years, starting from 2027-28.

- June 2023: Air India, the Tata Group-owned global airline, finalized purchase agreements for 470 aircraft from Airbus and Boeing for its USD 70 billion fleet expansion program.

India Aviation Market Report Scope

Commercial Aviation, General Aviation, Military Aviation are covered as segments by Aircraft Type.By Aircraft Type

| Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | ||

| Freighter | ||

| General Aviation | Business Jets | Large Jet |

| Mid-Size Jet | ||

| Light Jet | ||

| Helicopters | ||

| Others | ||

| Military Aviation | Fixed-Wing Aircraft | Multi-Role Aircraft |

| Training Aircraft | ||

| Transport Aircraft | ||

| Others | ||

| Rotorcraft | Multi-Mission Helicopter | |

| Transport Helicopter | ||

| Training | ||

By Propulsion Technology

| Turboprop |

| Turbofan |

| Piston Engine |

| Turboshaft |

| Others |

By End User

| Business and General Aviation Operators |

| Civil and Commercial Operators |

| Government and Defense Agencies |

| By Aircraft Type | Commercial Aviation | Passenger Aircraft | Narrowbody Aircraft |

| Widebody Aircraft | |||

| Freighter | |||

| General Aviation | Business Jets | Large Jet | |

| Mid-Size Jet | |||

| Light Jet | |||

| Helicopters | |||

| Others | |||

| Military Aviation | Fixed-Wing Aircraft | Multi-Role Aircraft | |

| Training Aircraft | |||

| Transport Aircraft | |||

| Others | |||

| Rotorcraft | Multi-Mission Helicopter | ||

| Transport Helicopter | |||

| Training | |||

| By Propulsion Technology | Turboprop | ||

| Turbofan | |||

| Piston Engine | |||

| Turboshaft | |||

| Others | |||

| By End User | Business and General Aviation Operators | ||

| Civil and Commercial Operators | |||

| Government and Defense Agencies | |||

Market Definition

- Aircraft Type - All the aircraft related to commercial, military and general aviation have been included in this study

- Sub-Aircraft Type - Fixed-Wing passenger aircraft, freighter aircraft, business jets, piston fixed-wing aircraft, military fixed-wing aircraft, and rotorcraft are included under this study.

- Body Type - Body type includes all types of aircraft segmented based on application/size/capacity/role.

| Keyword | Definition |

|---|---|

| IATA | IATA stands for the International Air Transport Association, a trade organization composed of airlines around the world that has an influence over the commercial aspects of flight. |

| ICAO | ICAO stands for International Civil Aviation Organization, a specialized agency of the United Nations that supports aviation and navigation around the globe. |

| Air Operator Certificate (AOC) | A certificate granted by a National Aviation Authority permitting the conduct of commercial flying activities. |

| Certificate Of Airworthiness (CoA) | A Certificate Of Airworthiness (CoA) is issued for an aircraft by the civil aviation authority in the state in which the aircraft is registered. |

| Gross Domestic Product (GDP) | Gross domestic product (GDP) is a monetary measure of the market value of all the final goods and services produced in a specific time period by countries. |

| RPK (Revenue Passenger Kilometres) | The RPK of an airline is the sum of the products obtained by multiplying the number of revenue passengers carried on each flight stage by the stage distance - it is the total number of kilometers traveled by all revenue passengers. |

| Load Factor | The load factor is a metric used in the airline industry that measures the percentage of available seating capacity that has been filled with passengers. |

| Original Equipment Manufacturer (OEM) | An original equipment manufacturer (OEM) traditionally is defined as a company whose goods are used as components in the products of another company, which then sells the finished item to users. |

| International Transportation Safety Association (ITSA) | International Transportation Safety Association (ITSA) is an international network of heads of independent safety investigation authorities (SIA). |

| Available Seats Kilometre (ASK) | This metric is calculated by multiplying Available Seats (AS) in one flight, defined above, multiplied by the distance flown. |

| Gross Weight | The fully-loaded weight of an aircraft, also known as “takeoff weight,” which includes the combined weight of passengers, cargo, and fuel. |

| Airworthiness | The ability of an aircraft, or other airborne equipment or system, to operate in flight and on the ground without significant hazard to aircrew, ground crew, passengers or to other third parties. |

| Airworthiness Standards | Detailed and comprehensive design and safety criteria applicable to the category of aeronautical product (aircraft, engine or propeller). |

| Fixed Base Operator (FBO) | A business or organization that operates at an airport. An FBO provides aircraft operating services like maintenance, fueling, flight training, charter services, hangaring, and parking. |

| High Net worth Individuals (HNWIs) | High Net worth Individuals (HNWIs) are individuals with over USD 1 million in liquid financial assets. |

| Ultra High Net worth Individuals (UHNWIs) | Ultra High Net worth Individuals (UHNWIs) are individuals with over USD 30 million in liquid financial assets. |

| Federal Aviation Administration (FAA) | The division of the Department of Transportation is concerned with aviation. It operates Air Traffic Control and regulates everything from aircraft manufacturing to pilot training to airport operations in the United States. |

| EASA (European Aviation Safety Agency) | The European Aviation Safety Agency is a European Union agency established in 2002 with the task of overseeing civil aviation safety and regulation. |

| Airborne Warning and Control System (AW&C) aircraft | Airborne Warning and Control System (AEW&C) aircraft is equipped with a powerful radar and on-board command and control center to direct the armed forces. |

| The North Atlantic Treaty Organization (NATO) | The North Atlantic Treaty Organization (NATO), also called the North Atlantic Alliance, is an intergovernmental military alliance between 30 member states – 28 European and two North American. |

| Joint Strike Fighter (JSF) | Joint Strike Fighter (JSF) is a development and acquisition program intended to replace a wide range of existing fighter, strike, and ground attack aircraft for the United States, the United Kingdom, Italy, Canada, Australia, the Netherlands, Denmark, Norway, and formerly Turkey. |

| Light Combat Aircraft (LCA) | A light combat aircraft (LCA) is a light, multirole jet/turboprop military aircraft, commonly derived from advanced trainer designs, designed for engaging in light combat. |

| Stockholm International Peace Research Institute (SIPRI) | Stockholm International Peace Research Institute (SIPRI) is an international institute that provides data, analysis, and recommendations for armed conflict, military expenditure, and arms trade as well as disarmament and arms control. |

| Maritime Patrol Aircraft (MPA) | A maritime patrol aircraft (MPA), also known as maritime reconnaissance aircraft is a fixed-wing aircraft designed to operate for long durations over water in maritime patrol roles, in particular, anti-submarine warfare (ASW), anti-ship warfare (AShW), and search and rescue (SAR). |

| Mach Number | The Mach number is defined as the ratio of true airspeed to the speed of sound at the altitude of a given aircraft. |

| Stealth Aircraft | Stealth is a Common term applied to low observable (LO) technology and doctrine, that makes an aircraft near invisible to radar, infrared or visual detection. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the historical and forecast years have been provided in revenue and volume terms. For sales conversion to volume, the average selling price (ASP) is kept constant throughout the forecast period for each country, and inflation is not a part of the pricing.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms