Market Overview

| Study Period | 2021 - 2031 |

|---|---|

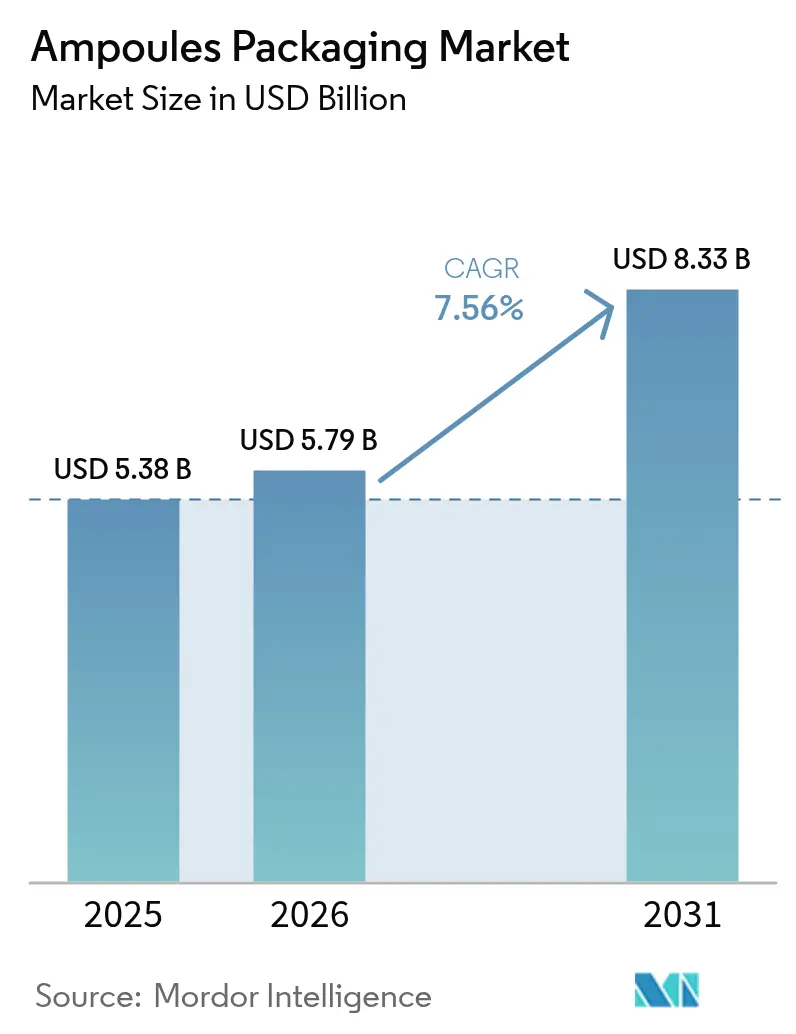

| Market Size (2026) | USD 5.79 Billion |

| Market Size (2031) | USD 8.33 Billion |

| Growth Rate (2026 - 2031) | 7.56% CAGR |

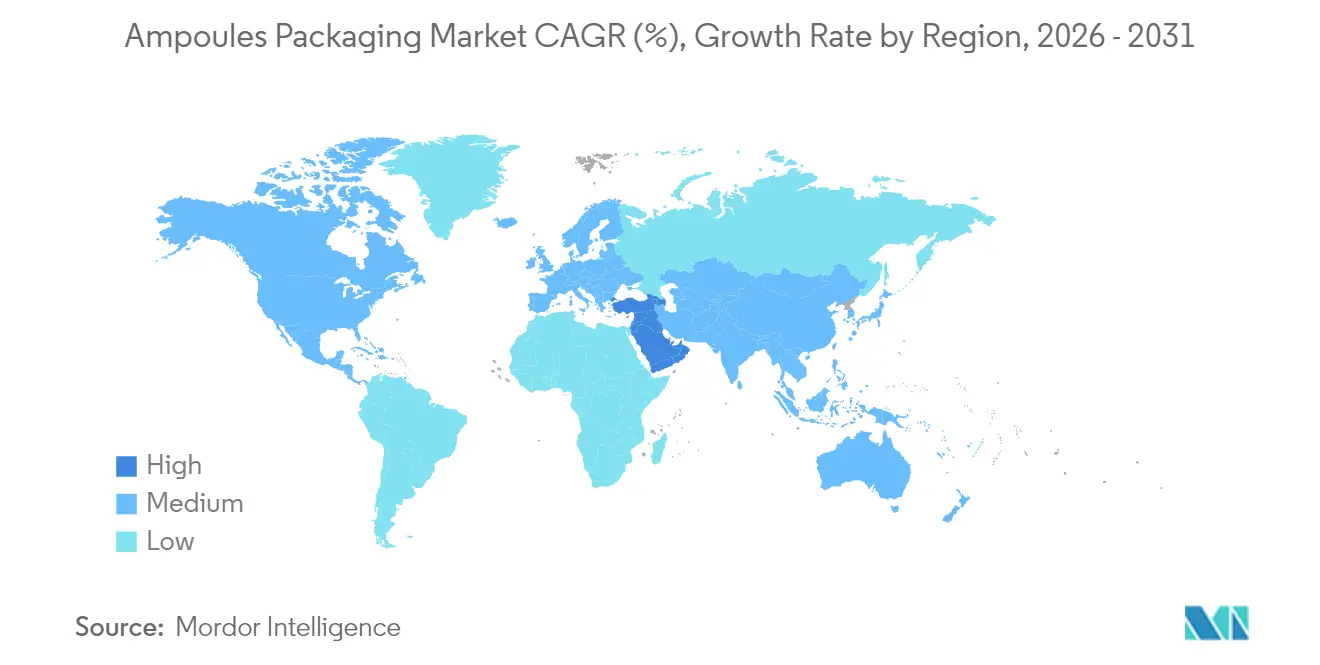

| Fastest Growing Market | Middle East |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Ampoules Packaging Market Analysis by Mordor Intelligence

ampoules packaging market size in 2026 is estimated at USD 5.79 billion, growing from 2025 value of USD 5.38 billion with 2031 projections showing USD 8.33 billion, growing at 7.56% CAGR over 2026-2031. Expansion is anchored in the pharmaceutical sector’s pivot toward single-dose injectable formats, propelled by biologics growth and global regulations that prioritize tamper-evident, serialised containers.[1]U.S. Food and Drug Administration, “Drug Supply Chain Security Act Overview,” fda.gov Glass ampoules currently dominate because they combine chemical inertness with established regulatory acceptance, yet plastic formats are scaling quickly as blow-fill-seal (BFS) platforms prove their sterility and cost benefits. Asia-Pacific leads demand after China and South Korea approved new botulinum toxin indications in 2024, while AI-enabled visual inspection lines accelerate quality-assurance gains for high-volume producers. Competitive intensity remains moderate: leading suppliers differentiate on break-system design, traceability features and sustainability programs instead of unit price, cushioning margins even as energy-related costs fluctuate.[2]SCHOTT Pharma, “One-Point-Cut Break System Factsheet,” schott.com

Key Report Takeaways

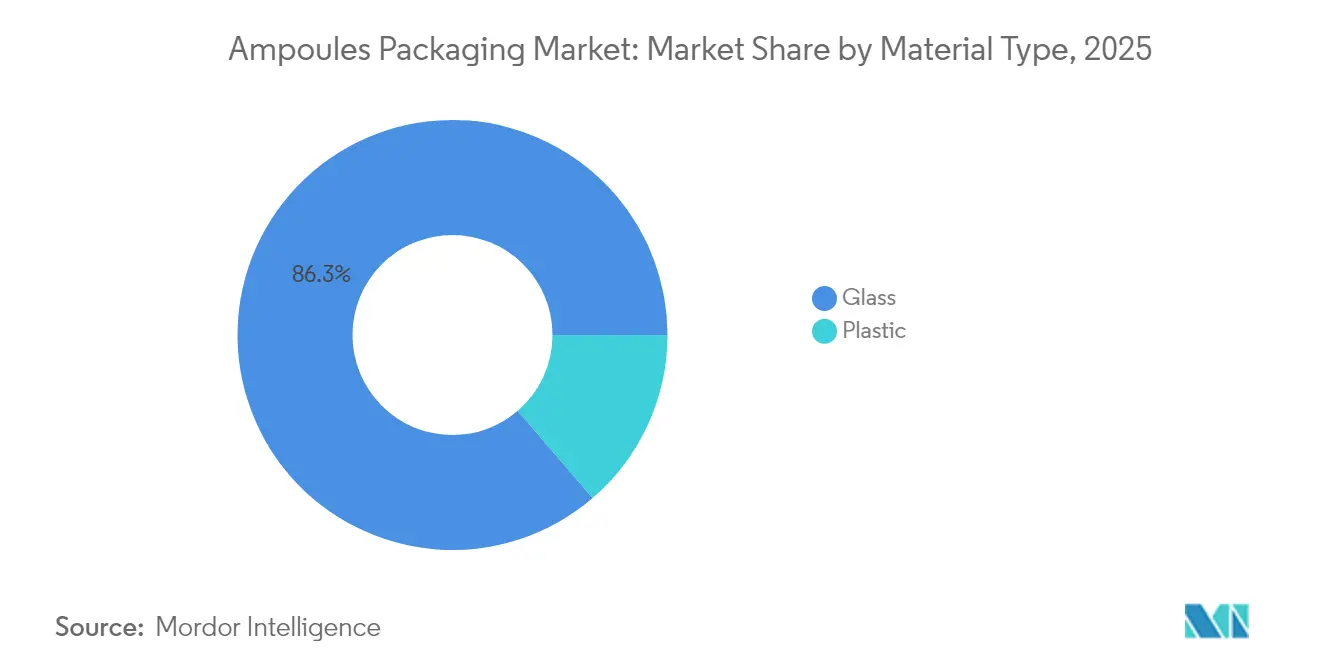

- By material type, glass held 86.30% of ampoules packaging market share in 2025, whereas plastic alternatives are forecast to expand at a 9.65% CAGR through 2031.

- By ampoule type, straight-stem designs led with 62.20% revenue share in 2025, while easy-open systems are advancing at a 9.05% CAGR to 2031.

- By capacity, the ≤2 mL segment commanded 42.60% share of the ampoules packaging market size in 2025; the 6–10 mL range is projected to grow at 8.6% CAGR.

- By end-user industry, pharmaceuticals contributed 90.70% of 2025 revenue, whereas personal care and cosmetics are expanding at 9.22% CAGR through 2031.

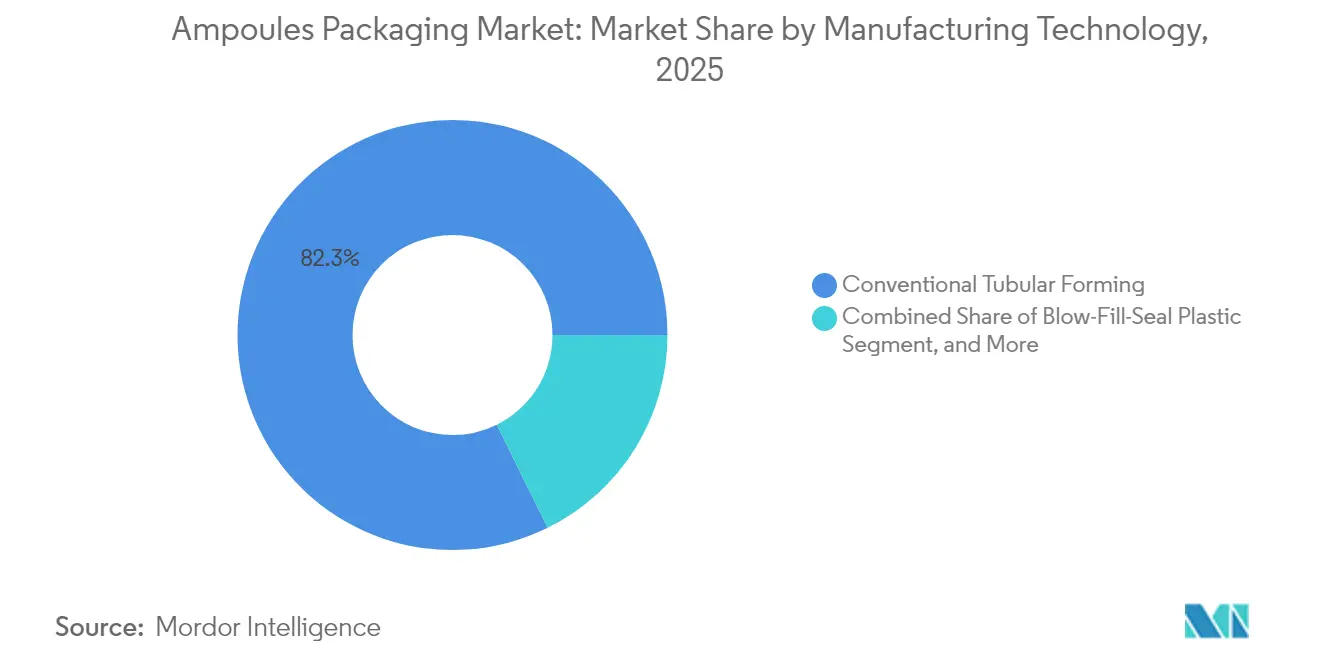

- By manufacturing technology, conventional tubular forming accounted for 82.30% share in 2025, but BFS is the fastest-growing method at 9.92% CAGR.

- By geography, Asia-Pacific captured 39.40% share in 2025; the Middle East is expected to post the quickest growth at 8.90% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ampoules Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Demand for tamper-evident pharma packs | +1.2% | Global, with EU and North America leading regulatory adoption | Medium term (2-4 years) |

| Recyclability and circular value of Type-I glass | +0.8% | Europe and North America, expanding to APAC | Long term (≥ 4 years) |

| Regulatory push on injectable traceability | +1.5% | Global, with US DSCSA and EU FMD driving implementation | Short term (≤ 2 years) |

| Biologics CDMO shift toward single-dose ampoules | +1.8% | North America and Europe, with APAC capacity expansion | Medium term (2-4 years) |

| AI-enabled zero-defect visual inspection lines | +0.9% | Global, with early adoption in developed markets | Medium term (2-4 years) |

| Rise of injectable aesthetics in APAC | +1.1% | APAC core, with spillover to Middle East and Latin America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Demand for Tamper-Evident Pharmaceutical Packs

Drug manufacturers are investing heavily in visible tamper-evidence to satisfy FDA 21 CFR 211.132 and EU Falsified Medicines Directive requirements, steering ampoule specifications toward break-ring and score-line technologies that produce unmistakable indicators of interference. SCHOTT Pharma’s One-Point-Cut system captured 62% of the global break-system sub-market by 2024, demonstrating how patient-safety features have moved from premium to standard expectation. Tamper-evidence also lowers liability risk for high-value biologics because compromised integrity directly threatens therapeutic efficacy. Hospitals increasingly cite simplified authenticity checks as a procurement criterion, encouraging suppliers to prioritise robust break designs. The resulting shift tightens qualification windows for alternative materials, reinforcing glass dominance in critical-care formulations.

Recyclability and Circular Value of Type-I Glass

Sustainability mandates push stakeholders to prefer containers that can re-enter production loops without downgrading quality. Type-I borosilicate satisfies this need: a 2024 closed-loop pilot by SCHOTT Pharma, Corplex and Takeda trimmed greenhouse-gas emissions by 50% versus virgin glass while meeting USP <660> chemical resistance benchmarks. European regulators now tie procurement incentives to recyclability scores, encouraging local health systems to favour glass derived from cullet streams. SGS audits confirm recycled Type-I maintains identical hydrolytic stability, so pharmaceutical‐quality thresholds remain intact. As brand owners target Scope 3 decarbonisation, ampoule producers that guarantee traceable recycled content secure supply-agreement advantages. These developments extend to Asia-Pacific as multinationals transplant EU ESG criteria into regional tender processes.

Regulatory Push on Injectable Traceability

The final phase of the US Drug Supply Chain Security Act requires every prescription drug package to carry unique, serialised identifiers by November 2025, mirroring EU-FMD provisions already enforced since 2019. Ampoule suppliers now embed 2D barcodes or machine-readable laser marks during forming, shifting traceability from secondary labels to the primary container. Stevanato Group’s glass-integrated coding solution supports plants running 400 ampoules per minute without compromising sterility, enabling end-to-end electronic pedigree capture.[3]Stevanato Group, “FY 2024 Results Presentation,” stevanatogroup.com Pharmaceutical customers gain real-time visibility that reduces diversion risk and sharpens demand planning. Capital expenditure rises initially, but manufacturers recoup costs via lower recall exposure and optimised inventory turns.

Biologics CDMO Shift Toward Single-Dose Ampoules

Contract development and manufacturing organisations (CDMOs) are expanding fill-finish suites specifically for single-dose ampoules as biologic APIs multiply. Samsung Biologics will surpass 784,000 L of capacity in 2025, while Lonza and Fujifilm Diosynth accelerate parallel expansions to attract monoclonal antibody programs. Single-dose, glass Type-I ampoules mitigate cross-contamination risk and simplify shelf-life studies for unstable proteins. CDMOs prefer standardised formats that serve multiple clients; hence demand is shifting from custom vials to platform ampoules capable of fast line changeovers. This dynamic raises long-term machinery utilisation and incentivises suppliers to co-locate tubing, forming and inspection assets near biologics clusters in North America and Europe.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Prefilled syringes cannibalising volumes | -1.4% | Global, with strongest impact in North America and Europe | Medium term (2-4 years) |

| Post-use sharps and chemical waste burden | -0.6% | Global, with stricter regulations in developed markets | Long term (≥ 4 years) |

| Tubing supply volatility from low-carbon furnaces | -0.8% | Europe and North America, with supply chain dependencies | Short term (≤ 2 years) |

| Glass delamination recall risk | -0.7% | Global, with heightened regulatory scrutiny | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Prefilled Syringes Cannibalising Volumes

Retail-oriented biologics and self-administered therapies are migrating to ready-to-inject syringes that offer dosing accuracy and patient convenience. Stevanato Group’s 15% surge in syringe revenue in 2024 coincided with a 34% slump in vial sales, exemplifying format substitution pressure. Syringes carry superior margins, prompting producers to reallocate furnace hours away from ampoules. The shift is accelerated by blockbuster GLP-1 agonists, where self-injection adherence drives payer preference. Nevertheless, ampoules remain vital for drugs sensitive to silicone oil or tungsten residue associated with syringe stoppers. The segmented demand profile obliges ampoule suppliers to target niche, stability-critical molecules and invest in marketing that highlights glass purity advantages.

Tubing Supply Volatility from Low-Carbon Furnaces

European glassmakers are rebuilding legacy furnaces to meet a 25% CO₂-reduction target by 2030, but switch-over periods tighten tubing availability. O-I Glass’s USD 150 million revamp of its Alloa plant temporarily removed 80,000 t of annual capacity, raising spot prices by up to 40% in 2024. Energy-price spikes linked to natural-gas markets further squeeze margins. Pharmaceutical buyers locked into qualified glass sources face costly revalidation should shortages persist. Although SGD Pharma’s hydrogen-assisted furnace pilot shows promise, capital intensity and skilled-labour gaps hinder rapid replication. These constraints motivate larger buyers to forward-contract tubing volumes and consider dual-sourcing strategies despite qualification overhead.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Glass Dominance Faces Plastic Innovation

Glass maintained an 86.30% share of the ampoules packaging market in 2025, reflecting entrenched regulatory confidence and unmatched chemical durability. Plastic formats, however, are logging a 9.65% CAGR through 2031, powered by BFS lines that cut sterility validation steps and shrink labor outlays. Within glass, Type-I borosilicate remains the default for biologics, oncology drugs and highly reactive compounds. Corning’s Valor composition eliminates delamination while retaining hydrolytic class I properties, widening glass’s applicability to high-stress cold-chain environments.

Manufacturers adopt divergent business models: SCHOTT Pharma derived 55% of 2024 revenue from high-value glass offerings that command premium pricing, whereas polymer specialists chase volume in vaccines and generics. Supply-chain simplicity strengthens plastic economics because containers form, fill and seal in one pass, reducing secondary packaging needs. Still, the ampoules packaging market size for glass‐based solutions stood at USD 4.64 billion in 2025, dwarfing plastic’s USD 739.4 million contribution. The trajectory indicates coexistence rather than displacement, hinging on therapeutic risk tolerance, required shelf-life and sustainability calculus.

By Ampoule Type: Easy-Open Systems Drive Innovation

Straight-stem ampoules led with 62.20% of ampoules packaging market share in 2025, but user-friendly formats such as One-Point-Cut (OPC), score-ring and color-breakring designs are rising at 9.05% CAGR. Healthcare providers increasingly rank reduced needlestick injuries and breakage complaints as procurement criteria, making easy-open options indispensable for nursing and at-home care settings. In parallel, funnel-type ampoules retain relevance for viscous or suspension formulations where wider necks enable efficient filling.

Easy-open uptake is also fueled by self-administration trends in vaccines and aesthetics. SCHOTT Pharma’s easyOPC design cuts opening force variability by 60%, thereby decreasing spillage risk during dose preparation. As break-system patents expire, mid-tier producers can emulate these features, intensifying price competition in lower-margin therapeutic classes. Nonetheless, premium biologics continue to favor proprietary break technologies that guarantee sterility and traceability, reinforcing margin resilience for innovation leaders. The ampoules packaging market size for easy-open variants is projected to surpass USD 2.33 billion by 2031, supported by differentiating ergonomic value.

By Capacity: Mid-Range Volumes Capture Growth

Ampoules ≤2 mL captured 42.60% of 2025 revenue thanks to biologics requiring single-dose administration. Capacity selection reflects a trade-off between waste minimisation and dosing flexibility: multi-dose hospital settings are driving 8.6% CAGR in the 6–10 mL band because larger fills reduce administration time per patient round. The 3–5 mL range remains the default for routine antibiotics and analgesics, balancing production cost and dosing convenience.

Manufacturing economics diverge accordingly. Small capacities permit higher cavity counts per cycle, leading to lower per-unit energy usage, whereas mid-range sizes optimise furnace throughput. For injectable aesthetics, clinics prefer 1 mL glass ampoules to ensure product freshness, reinforcing the profile of single-use packages in Asia-Pacific. Conversely, chemotherapy protocols often adopt 10 mL fills to match infusion bag volumes, illustrating capacity’s dependence on clinical workflow. Ampoules packaging market share within each band could swing further if waste-charge regulations incentivise smaller or larger fills.

By Manufacturing Technology: Automation Drives Transformation

Conventional tubular forming lines held an 82.30% share in 2025 but BFS installations are expanding at 9.92% CAGR, driven by integrated forming-fill-seal productivity and reduced contamination risk. BFS eliminates separate washing, depyrogenation and sterilisation stages, enabling sub-10-minute format changeovers that suit multi-product CDMO facilities. Laser-scoring advances further reduce break-defect rates, crucial for high-value APIs where a single hairline crack can trigger batch rejection.

Automation yields data-rich environments: Antares Vision’s AI-Go module retrofits legacy cameras to deep-learning classifiers that flag micro-defects invisible to rule-based systems. Adoption is fastest in North America and the EU where labor shortages and quality-by-design frameworks elevate ROI for high-capex upgrades. Ampoules packaging market size associated with BFS lines is expected to cross USD 1.08 billion by 2031 as vaccine producers and ophthalmic drug makers transition away from open-container fills.

By End-User Industry: Cosmetics Segment Accelerates

Pharmaceutical applications contributed 90.70% of 2025 sales, but injectable aesthetics in personal care are expanding at 9.22% CAGR through 2031. China’s middle-class consumers maintained or raised spending on botulinum toxin and dermal fillers during 2024 economic slowdowns, creating robust incremental demand for pharma-grade containers in non-therapeutic settings. Regulatory authorities treat these products as medical devices, so packaging specifications mirror pharmaceutical standards, sustaining the market’s value proposition.

Cosmetics buyers emphasise premium appearance, driving adoption of clear glass with ceramic printing rather than ink labels. For OEMs, the cost threshold remains secondary to brand perception, allowing ampoule suppliers to preserve margins. Meanwhile, hospital pharmacy outsourcing in Europe anchors demand as compounding rules tighten, ensuring a floor for pharmaceutical volumes even under syringe substitution pressure. The ampoules packaging market size for cosmetics is poised to reach USD 625.7 million by 2031, small but strategic for diversification.

Geography Analysis

Asia-Pacific controlled 39.40% of global revenue in 2025, buoyed by capacity expansions across China, India and South Korea as governments localise injectable drug supply chains. China’s biopharmaceutical output hit CNY 565.3 billion (USD 78.4 billion) in 2024 and could eclipse CNY 1.4 trillion (USD 194 billion) by 2029, sustaining demand for ampoules despite sporadic API export restrictions tied to the 2024 Anti-Espionage Law. South Korea’s aesthetics cluster in Gangnam fuels consistent small-volume glass orders, while India’s “Make in India” incentives support BFS capacity additions for vaccines. Concurrently, ASEAN members court CDMOs by offering tax holidays and streamlined GMP approvals, amplifying regional competitiveness.

North America’s growth is steadier, underpinned by biologics commercialisation pipelines and DSCSA compliance deadlines that require serialised primary containers. The United States drives high-value orders for Type-I glass and AI-enabled inspection lines that satisfy USP <1790> recommendations for parenteral visual inspection. Canada works to align with US traceability norms, spurring suppliers to provide bilingual packaging and GS1-compatible codes. Notably, herbicide litigation and supply-chain shocks have encouraged drug makers to dual-source ampoules from Mexico, broadening North American intra-regional trade.

Europe remains a value-rich but mature territory where sustainability and circular-economy targets dictate purchasing. The revised EU Packaging and Packaging Waste Regulation obliges recyclability scores above 70% by 2030, elevating demand for closed-loop Type-I glass streams. German hospitals formed a buying consortium in 2024 that gives 5-year contracts to vendors meeting ≥50% cullet content, signalling future procurement norms. Meanwhile, energy-price volatility tied to gas supply cuts heightened concern over furnace downtime, prompting some firms to stockpile borosilicate tubing. Yet EU Recovery Funds earmarked for life-science infrastructure will subsidise next-generation inspection gear, partially offsetting cost fears.

The Middle East recorded the highest regional CAGR at 8.90% through 2031 as Saudi Arabia and the UAE channel public-health budgets into local manufacturing. Riyadh’s Vision 2030 pharmaceutical programme co-funds sterile injectables plants, creating greenfield demand for BFS and tubular lines. Gulf Cooperation Council tender rules prioritize cost-effectiveness, positioning Indian and European mid-tier firms to capture share. However, limited skilled labour necessitates technology-transfer partnerships that intertwine equipment supply with long-term service contracts.

Latin America’s uptake is hindered by macroeconomic instability, yet Brazil’s ANVISA pushes serialization that mirrors EU-FMD requirements, opening opportunities for traceability-enabled ampoules. Africa remains nascent outside Egypt’s vaccine complex; nonetheless, the African Union’s 2040 target for 60% local vaccine manufacturing may catalyse BFS investments later in the forecast horizon.

Competitive Landscape

The market is moderately consolidated: SCHOTT Pharma, Gerresheimer and Stevanato Group occupy the quality-premium niche, while SGD Pharma and regional contenders focus on mid-tier offerings. SCHOTT Pharma posted EUR 899 million (USD 974 million) revenue in 2024, delivering a 27.8% EBITDA margin by emphasising high-value break-systems and traceability features. Gerresheimer’s glass division saw a 2.6% organic decline amid destocking, prompting a strategic pivot toward plastic containment solutions after acquiring Bormioli Pharma in 2025. Stevanato Group attained EUR 1.104 billion (USD 1.20 billion) turnover by increasing its mix of high-value solutions to 38%, highlighting the profitability advantage of technologically differentiated products.

Competitive strategy tilts toward vertical integration and digital upgrades. Manufacturers deploy AI-assisted inspection suites to guarantee near-zero defect levels, thus qualifying for biologics fill-finish contracts where batch failures are costly. Patent activity rose sharply in 2024, centring on laser-scored break lines and embedded data matrix coding, underscoring technology as the key moat. Sustainability credentials also drive tender wins: closed-loop glass trials and furnace electrification commitments differentiate suppliers when European buyers apply ESG scoring.

M&A remains a growth lever. Gerresheimer’s Bormioli Pharma takeover broadens plastic capability and increases leverage with global pharma accounts. Amcor’s planned all-stock merger with Berry Global, announced November 2024, would create a diversified packaging giant with a deeper pharmaceutical footprint. Novo Holdings’ USD 16.5 billion purchase of Catalent aims to relieve biologics capacity bottlenecks, indirectly benefitting ampoule suppliers tied to Catalent’s fill-finish network. Regional players court joint ventures that secure tubing supply or open BFS technology access, signalling ongoing consolidation as barriers to quality compliance rise.

Ampoules Packaging Industry Leaders

-

Gerresheimer AG

-

James Alexander Corporation

-

Schott Pharma AG and Co. KGaA

-

Essco Glass Pvt. Ltd.

-

Stevanato Group S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gerresheimer finalised the acquisition of Bormioli Pharma, enhancing its plastics portfolio and enabling high-value integrated solutions across glass and polymer formats.

- May 2025: Syntegon introduced Pharmatag 2025, a filling platform optimised for high-efficiency liquid packaging, including rapid-change ampoule modules that cut line clearance time by 30%.

- February 2025: Novo Holdings closed its USD 16.5 billion Catalent acquisition, aiming to relieve fill-finish bottlenecks for weight-loss drugs and accelerate packaging innovations, including advanced ampoules.

- November 2024: Amcor disclosed plans to acquire Berry Global via an all-stock transaction, creating a diversified entity with amplified reach in pharmaceutical primary packaging.

Global Ampoules Packaging Market Report Scope

An ampoule is a small, sealed glass or plastic bottle that is used to contain and preserve a sample, usually a solid or liquid. Ampoule packaging is being used in the pharmaceutical, personal care, and cosmetic industries. Ampoule packaging is mostly used to protect liquid or solution from air and contaminants. The study tracks the demand for ampoules that are being used in different end-user industries and the revenue generated by the players operating in the market.

The ampoule packaging market is segmented by material (glass and plastic), end-user industry (pharmaceutical, personal care, and cosmetic, other end-user industries), and geography ( North America (United States and Canada), Europe (United Kingdom, Germany, France, Italy, Spain, and Rest of Europe), Asia-Pacific ( China, India, Japan, South Korea, Australia and New Zealand, and Rest of Asia-Pacific), Latin America ( Brazil, Mexico, and Rest of Latin America), Middle East and Africa ( Saudi Arabia, Egypt, United Arab Emirates, South Africa, and Rest of Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Material Type

| Glass |

| Plastic |

By Ampoule Type

| Straight-stem |

| Funnel-type |

| Closed (Form D) |

| Easy-Open (OPC, Score-Ring, CBR) |

By Capacity (mL)

| ≤2 mL |

| 3–5 mL |

| 6–10 mL |

| >10 mL |

By Manufacturing Technology

| Conventional Tubular Forming |

| Blow-Fill-Seal Plastic |

| Advanced Laser Scoring |

By End-user Industry

| Pharmaceutical |

| Personal Care and Cosmetics |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Rest of Middle East | |

| Africa | South Africa |

| Nigeria | |

| Rest of Africa |

| By Material Type | Glass | |

| Plastic | ||

| By Ampoule Type | Straight-stem | |

| Funnel-type | ||

| Closed (Form D) | ||

| Easy-Open (OPC, Score-Ring, CBR) | ||

| By Capacity (mL) | ≤2 mL | |

| 3–5 mL | ||

| 6–10 mL | ||

| >10 mL | ||

| By Manufacturing Technology | Conventional Tubular Forming | |

| Blow-Fill-Seal Plastic | ||

| Advanced Laser Scoring | ||

| By End-user Industry | Pharmaceutical | |

| Personal Care and Cosmetics | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current size of the ampoules packaging market?

The ampoules packaging market size reached USD 5.79 billion in 2026 and is forecast to hit USD 8.33 billion by 2031.

Which material dominates ampoule production?

Glass dominates with an 86.30% revenue share in 2025, thanks to its chemical inertness and entrenched regulatory acceptance.

Why is blow-fill-seal technology gaining popularity?

Blow-fill-seal integrates container formation, filling and sealing in one sterile step, lowering contamination risk and supporting a 9.92% CAGR within the ampoules packaging market.

How do traceability regulations affect ampoule design?

Global mandates such as the US DSCSA require unique identifiers on every prescription drug package, prompting manufacturers to laser-mark or barcode ampoules for end-to-end supply-chain visibility.

Which region is growing fastest?

The Middle East leads growth at a projected 8.90% CAGR through 2031, propelled by healthcare infrastructure investments in Saudi Arabia and the UAE.

Are prefilled syringes a threat to ampoules?

Yes; in North America and Europe, prefilled syringes are siphoning volumes, exerting an estimated -1.4% impact on the ampoules packaging market CAGR, although ampoules retain niches where glass purity is essential.

Page last updated on: