Aluminum Composite Panel (ACP) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

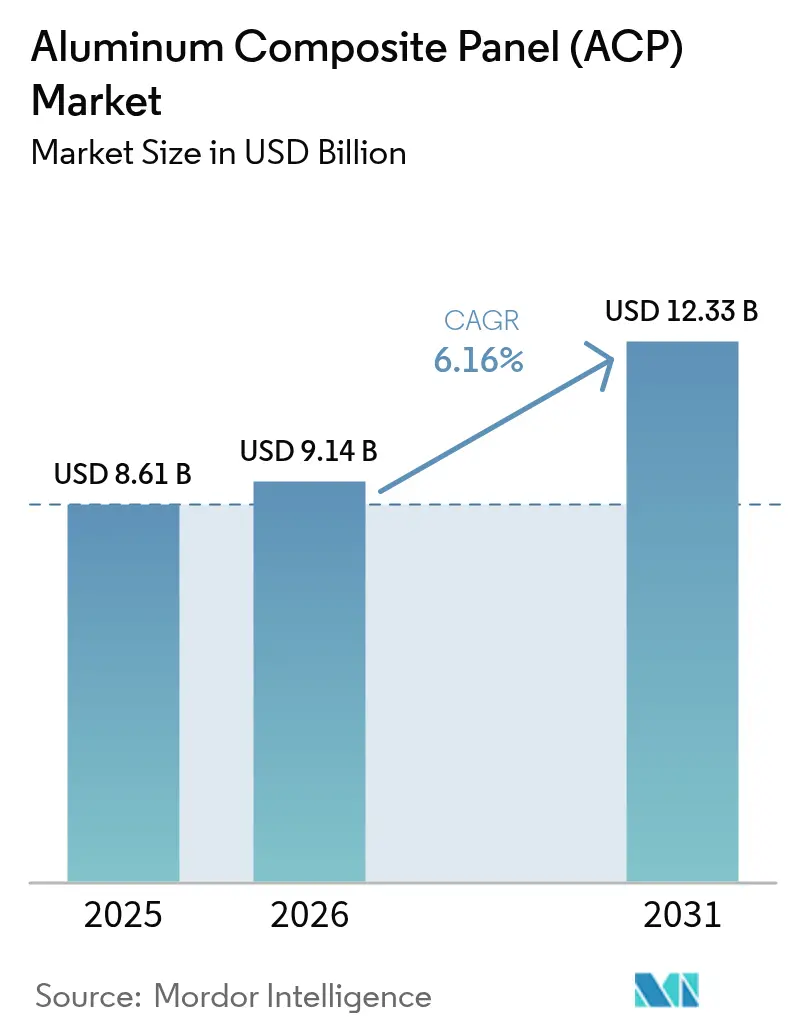

| Market Size (2026) | USD 9.14 Billion |

| Market Size (2031) | USD 12.33 Billion |

| Growth Rate (2026 - 2031) | 6.16% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aluminum Composite Panel (ACP) Market Analysis by Mordor Intelligence

Aluminum Composite Panel Market size in 2026 is estimated at USD 9.14 billion, growing from 2025 value of USD 8.61 billion with 2031 projections showing USD 12.33 billion, growing at 6.2% CAGR over 2026-2031. Robust demand for lightweight façades, tightening global fire-safety codes, and expanding modular construction pipelines underpin this growth trajectory. Competitive pricing from Asia-based manufacturers keeps upfront costs attractive, while PVDF-coated variants extend façade life cycles and lower lifetime maintenance spending. Weight-reduction imperatives in rail, marine, and commercial vehicle segments open fresh avenues beyond buildings. Meanwhile, volatility in primary aluminum prices and emerging substitute cladding materials temper near-term margin expansion across the aluminum composite panel market.

Key Report Takeaways

- By top coating, PVDF-coated panels captured 65.20% of the aluminum composite panel market share in 2025.

- By application, interior decoration accounted for 17.80% share of the aluminum composite panel market size in 2025, while hoarding signage is projected to expand at a 6.92% CAGR to 2031.

- By end-user industry, building & construction held 53.40% of revenue in 2025, whereas transportation is forecast to rise at a 6.32% CAGR through 2031.

- By geography, Asia Pacific led with 37.80% revenue share in 2025 and is advancing at a 6.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aluminum Composite Panel (ACP) Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of PVDF-coated ACPs for long-life facades | +1.8% | Global, with early adoption in North America & EU | Medium term (2-4 years) |

| Rising demand for lightweight panels in building & transport sectors | +1.5% | APAC core, spill-over to North America | Long term (≥ 4 years) |

| Expansion of digital-printing hoardings & signage applications | +1.2% | Global, concentrated in urban centers | Short term (≤ 2 years) |

| Tightening global fire-safety codes boosting A2/mineral-core ACP uptake | +1.0% | North America & EU, expanding to APAC | Medium term (2-4 years) |

| Off-site modular façade fabrication accelerating ACP panelization demand | +0.8% | Global, led by developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of PVDF-Coated ACPs for Long-Life Facades

PVDF technology commands 65.89% coating share and is rising at a 6.70% CAGR as its fluoropolymer layer delivers ultraviolet resistance, color retention, and 20–25-year service life[1]PRANCE Building Material, “PVDF Coating Performance Data Sheet,” prancebuilding.com. Owners view the premium as life-cycle value, because mid-life recoating is unnecessary. PVDF formulations also exhibit limited toxic fume evolution under fire load, a key attribute for code compliance in North America and Europe. Consequently, public infrastructure, airports, and Grade-A commercial towers increasingly specify PVDF as a performance baseline. Suppliers able to mass-produce uniform PVDF finishes capture higher margins and build durable specification relationships with architects.

Rising Demand for Lightweight Panels in Building & Transport Sectors

Aluminum composite panels reduce structural load by 30–50% in rail carriages versus conventional steel, boosting operating efficiency and passenger capacity. Building owners likewise favor lighter cladding to ease seismic design constraints and shorten installation cycles. Adoption accelerates in electric buses and ferries, where every kilogram saved extends battery range or payload. These cross-industry weight benefits underpin steady penetration into rolling-stock, marine superstructure, and refrigerated trailer skins, cementing medium-term upside for the aluminum composite panel market.

Expansion of Digital-Printing Hoardings & Signage Applications

Direct-to-panel UV, latex, and solvent inks unlock vivid, graffiti-resistant graphics without vinyl lamination, cutting turnaround times for construction hoardings and retail signage. Urban advertisers value single-panel customisation coupled with outdoor durability. The hoarding segment therefore posts the fastest 7.21% CAGR, adding incremental square-meter volume and introducing smaller print shops to the aluminum composite panel market.

Tightening Global Fire-Safety Codes Boosting A2/Mineral-Core Uptake

Post-fire inquiries in several countries have triggered bans on polyethylene-core cladding for high-rise retrofits. The 2024 International Building Code revision mandates limited-combustible façades for specific occupancy classes. Australia’s New South Wales imposed a ban on panels containing >30% polyethylene in 2018[2]Fair Trading NSW, “Building Products (Safety) Amendment Regulation 2018,” fairtrading.nsw.gov.au . Manufacturers are rapidly converting lines to mineral-filled A2 cores to retain specification access, temporarily tightening supply and elevating price points.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Availability of lower-cost cladding alternatives | -1.2% | Global, particularly in price-sensitive markets | Short term (≤ 2 years) |

| Volatile aluminum price trends squeezing converter margins | -0.9% | Global, with acute impact in manufacturing hubs | Medium term (2-4 years) |

| Regulatory bans on PE-core ACPs in high-rise retrofits | -0.6% | North America & EU, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Availability of Lower-Cost Cladding Alternatives

Fiber cement, high-pressure laminates, and engineered wood panels replicate many visual effects at lower material cost. In residential mid-rise projects with modest fire requirements, contractors often select these substitutes, forcing ACP suppliers to lean on lifecycle advantages and faster installation to preserve share. Emerging-market builders, operating on thin margins, amplify this pressure by demanding aggressive price concessions.

Volatile Aluminum Price Trends Squeezing Converter Margins

Primary aluminum averaged USD 2,600 per ton in early 2025 amid 120-USD intra-year swings tied to Chinese production policy and geopolitical risk. Metal content accounts for 60–70% of composite panel cost, leaving converters exposed when fixed-price contracts collide with spot spikes. Many now employ rigorous hedging programs or escalate clauses, yet persistent volatility still compresses margins relative to substitutes with stable input profiles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Top Coating: PVDF Maintains Premium Lead

PVDF-coated products held 65.20% revenue in 2025, the largest slice of the aluminum composite panel market. Superior ultraviolet stability extends service life to 25 years, trimming whole-life façade expenditure. That durability attracts commercial skyscrapers and coastal infrastructure where harsh sun, salt, and temperature swings accelerate aging. Fire-safety regulations further consolidate PVDF’s position because the coating withstands higher ignition temperatures while emitting lower smoke density. As mineral-core substrates become the high-rise standard, PVDF’s compatibility sustains premium price realisation of 20-30% over polyester rivals.

Margins thus expand when projects specify PVDF, rewarding converters that invest in high-capacity coil-coating lines and tight colour-match control. Simultaneously, budget-focused residential builds still rely on polyester coatings, keeping a value tier alive within the aluminum composite panel market. That two-tier structure allows firms to segment offerings by performance need and regional purchasing power, maximising total addressable demand without cannibalising flagship PVDF sales.

By Application: Interior Decor Leads While Hoarding Outpaces

Interior decoration represented 17.80% of the aluminum composite panel market size in 2025 thanks to hotels, hospitals, and shopping malls adopting easy-to-shape panels for lobbies and feature walls. Non-directional metallic finishes and anti-bacterial films further lift adoption in healthcare interiors. Meanwhile, the hoarding segment is forecast at 6.92% CAGR as developers print vivid branding onto site fences using direct-to-panel UV inks. Rapid replacement cycles amplify square-meter consumption despite low per-panel thickness.

Cladding still dominates volume but yields share slowly to specialty niches where bespoke textures or acoustic backing layers differentiate offers. Railways specify composite liners for station halls, while column cladding and beam wraps hide structural steel on industrial projects. These sub-niches diversify revenue streams and cushion cyclical downturns in core new-build construction.

By End-User Industry: Construction Remains Core, Transportation Gains Speed

Building & construction retained 53.40% of 2025 demand as energy-efficient envelopes and striking façades remain centre stage in modern architecture. Tall towers in seismic zones benefit from the panel’s light weight, enabling thinner foundations and smaller structural sections. At the same time, transportation is rising fastest at 6.32% CAGR as metros, intercity rail, and electric buses substitute heavier metals with composites to save fuel or extend battery range.

Marine cabin fit-outs, truck sidewalls, and refrigerated trailer skins represent additional growth paths. Aerospace and specialty industrial housings add incremental tonnage where temperature control or clean-room compliance is critical. Collectively, these moves broaden the aluminum composite panel market beyond its historic façades stronghold.

Geography Analysis

Asia Pacific led the aluminum composite panel market with a 37.80% share in 2025 and is advancing at a 6.65% CAGR to 2031. China hosts over 4,127 manufacturers offering more than 41,000 product variants priced between USD 7-20 per m², enabling scale economics that underpin both domestic megaprojects and export supply. Indian demand climbs in tandem with its USD 11.28 billion aluminum extrusions sector, expanding 7.6% annually as government drives affordable housing and metro rail rollouts. Southeast Asian urbanisation adds further uplift, and the region’s competitive cost base positions it as the global price setter for the aluminum composite panel market.

North America ranks second, defined by stringent fire-safety codes that reward suppliers certified to ASTM E-84 and NFPA 285 assemblies. The 2024 International Building Code revision reinforces mineral-core adoption and sustains margin premiums for compliant products. Modular hotel chains such as the Hilton Garden Inn in San Jose illustrate how panelised ACP sections speed fit-out times while meeting Class A flame-spread limits. Regional mills, including Century Aluminum’s expanded U.S. smelter, partially offset import reliance and dampen tariff uncertainty.

Europe follows with a sustainability lens, spotlighting decarbonised smelting and end-of-life recyclability. Novelis lifted recycled content from 33% to 63% across its aluminium portfolio, reinforcing the alloy’s circular credentials and supporting architects striving for green-building certification. Ongoing post-Grenfell fire reforms accelerate mineral-core mandates, prompting rapid line upgrades among European converters. South America plus the Middle East & Africa trail in volume but display above-trend growth where infrastructure buildout intersects with rising safety standards. The UAE’s hospitality pipeline, for instance, leverages ACP-clad modular rooms to cut project delivery schedules by months. Nonetheless, limited installer expertise and high capital costs slow wider penetration, keeping these regions in a developmental stage of the aluminum composite panel market.

Mordor Intelligence provides coverage of the aluminum composite panel (acp) market across other key regional markets, including Europe, each with their regulatory frameworks and demand patterns.

Competitive Landscape

The aluminum composite panel market is moderately fragmented: high-volume Chinese plants coexist with specialised Western players focused on code-driven niches. Top Chinese producers exploit labour and scale advantages, marketing polyester-coated panels at double-digit million square-meter capacity to price-sensitive customers. Conversely, North American and European incumbents prioritise mineral-core innovation, PVDF line-width upgrades, and cradle-to-cradle certification to secure premium institutional contracts.

Technology investment is the primary battleground. 3A Composites’ ALUCOBOND A2 non-combustible panel and ultra-thin 1.2 mm HYLITE polypropylene-core sheet illustrate how proprietary chemistry raises entry barriers. Digital-printing-ready surfaces and antimicrobial clear coats form ancillary differentiation layers, allowing suppliers to upsell value-added variants. Aluminum price gyrations inject earnings risk, so leading firms embed metal hedges or adopt index-linked contract clauses to preserve gross margins during volatile cycles.

Aluminum Composite Panel (ACP) Industry Leaders

3A Composites GmbH

Alubond USA

Alucoil (Grupo Aliberico)

Arconic Inc.

Mitsubishi Chemical Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Viva, a prominent aluminium composite panel (ACP) manufacturer, has launched the country's first A2 Fire Retardant Core production facility. This advanced facility sets new standards in fire safety, innovation, and international compliance within the ACP industry.

- October 2024: The Bureau of Indian Standards (BIS) has extended the deadline for mandatory certification under IS 17682: 2021 for Aluminium Composite Panels (ACP) to March 22, 2025. This standard specifies requirements for flat ACPs used in external applications like façades, curtain walls, and canopies, as well as internal uses such as partitions and ceilings. It also includes fire-retardant ACPs and various property applications.

Global Aluminum Composite Panel (ACP) Market Report Scope

An aluminum composite panel (ACP) is a flat panel crafted out of two aluminum alloy sheets bonded with a non-aluminum core to form a composite. It is used as cladding or facade material in buildings, insulation, and signage. The aluminum composite panel (ACP) market is segmented by top coating, application, end-user industry, and geography. By top coating, the market is segmented into PE, PVDF, and other top coatings. By application, the market is segmented into interior decoration, hoarding, insulation, cladding, railway carriers, column cover and beam wrap, and other applications. By end-user industry, the market is segmented by building and construction, transportation, and other end-user industries. The report also covers the market sizes and forecasts for the aluminum composite panel (ACP) market in 15 countries across the major regions. For each segment, market sizing and forecasts have been done based on revenue (USD million).

| PE (Polyester) |

| PVDF (Polyvinylidene Fluoride) |

| Other Coatings |

| Interior Decoration |

| Hoarding |

| Insulation |

| Cladding |

| Railway Carrier |

| Column Cover and Beam Wrap |

| Other Applications |

| Building and Construction |

| Transportation (Rail, Bus, Trailer, Marine) |

| Other End-User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Top Coating | PE (Polyester) | |

| PVDF (Polyvinylidene Fluoride) | ||

| Other Coatings | ||

| By Application | Interior Decoration | |

| Hoarding | ||

| Insulation | ||

| Cladding | ||

| Railway Carrier | ||

| Column Cover and Beam Wrap | ||

| Other Applications | ||

| By End-User Industry | Building and Construction | |

| Transportation (Rail, Bus, Trailer, Marine) | ||

| Other End-User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current Aluminum Composite Panel (ACP) Market size?

The aluminum composite panel market size is USD 9.14 billion in 2026.

How fast is the aluminum composite panel market expected to grow?

The market is projected to expand at a 6.16% CAGR from 2026 to 2031.

Which region leads global demand for aluminum composite panels?

Asia Pacific holds the largest share at 37.80% in 2025 and is also the fastest-growing region.

Why are PVDF-coated panels preferred for high-end façades?

PVDF coatings offer 20-25-year color stability, superior UV resistance, and enhanced fire performance, providing lower life-cycle costs.

Page last updated on: