Asia-Pacific Algae Protein Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

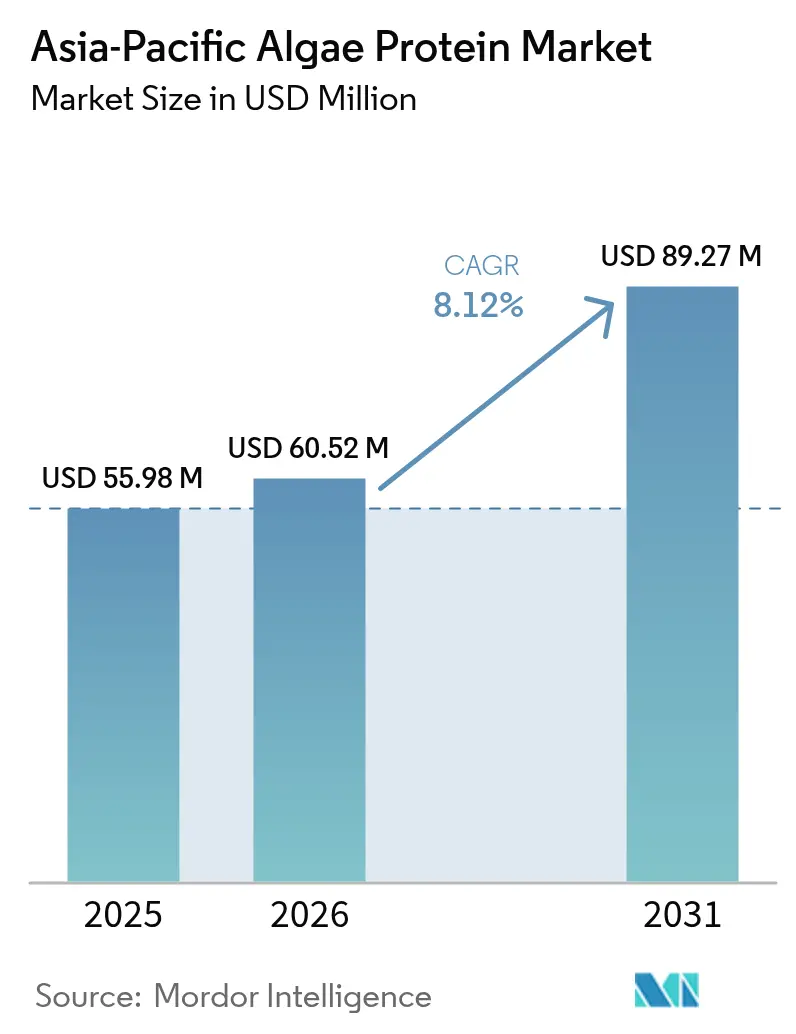

| Base Year Market Size (2025) | USD 55.98 Million |

| Market Size (2026) | USD 60.52 Million |

| Market Size (2031) | USD 89.27 Million |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Algae Protein Market Analysis by Mordor Intelligence

The Asia-Pacific algae protein market size in 2026 is estimated at USD 60.52 million, growing from 2025 value of USD 55.98 million with 2031 projections showing USD 89.27 million, growing at 8.12% CAGR over 2026-2031. This substantial growth is attributed to several key factors, including the increasing protein shortages across the region, which have heightened the demand for alternative protein sources. Government approvals have also played a pivotal role by expediting the use of microalgae ingredients, while the aquaculture industry is progressively transitioning from traditional wild-catch fishmeal to sustainable algal omega-3 oils. Regulatory frameworks in countries such as China, India, and Singapore have become more transparent, effectively reducing entry barriers for new players in the market. Additionally, advancements in technology, such as hybrid fermentation-photosynthesis processes, have significantly reduced energy costs by up to 50%, making production more efficient. Although the competitive intensity in the market remains moderate due to the economic advantages of regional production clusters, the establishment of capital-intensive facilities in locations like California and Singapore has raised the standards for water and energy usage. Furthermore, the market is witnessing increased demand driven by the rising number of functional food product launches, a growing focus on elderly nutrition, and the adoption of algae protein in cost-sensitive livestock feed applications. These factors collectively underscore the strong growth potential of the algae protein market in the Asia-Pacific region.

Key Report Takeaways

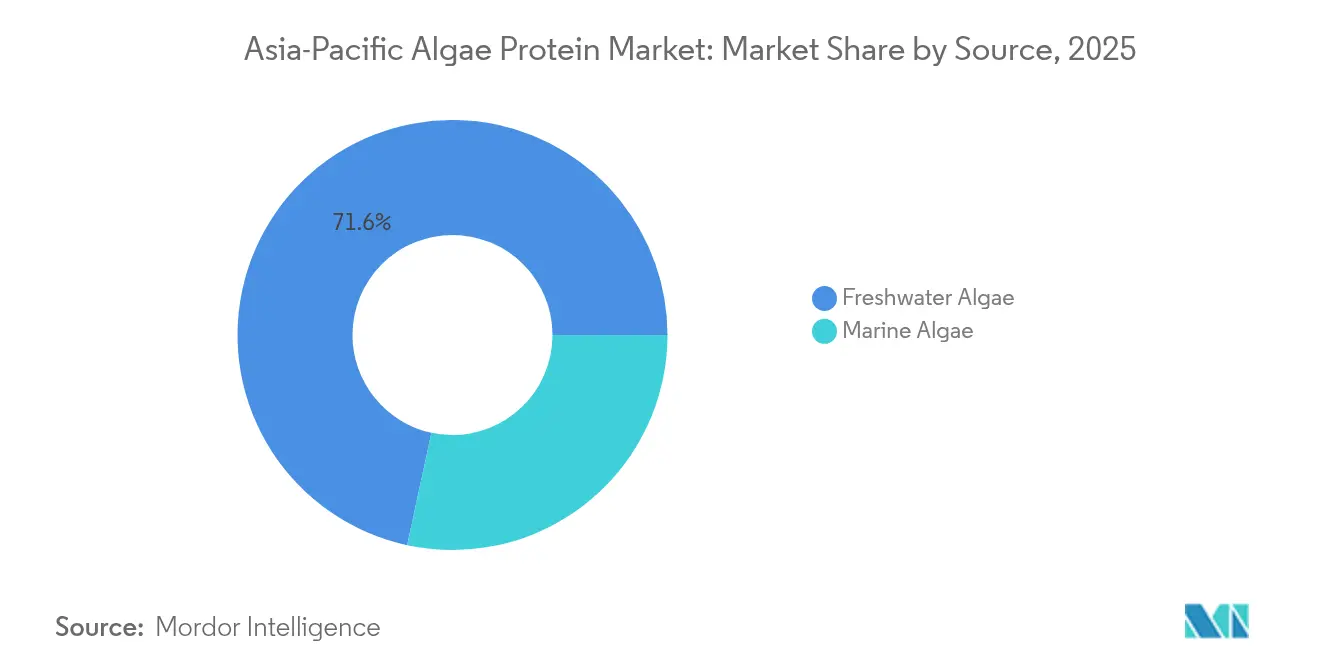

- By source, freshwater algae commanded 71.62% of the algae protein market share in 2025, whereas marine algae is forecast to grow at an 8.74% CAGR to 2031.

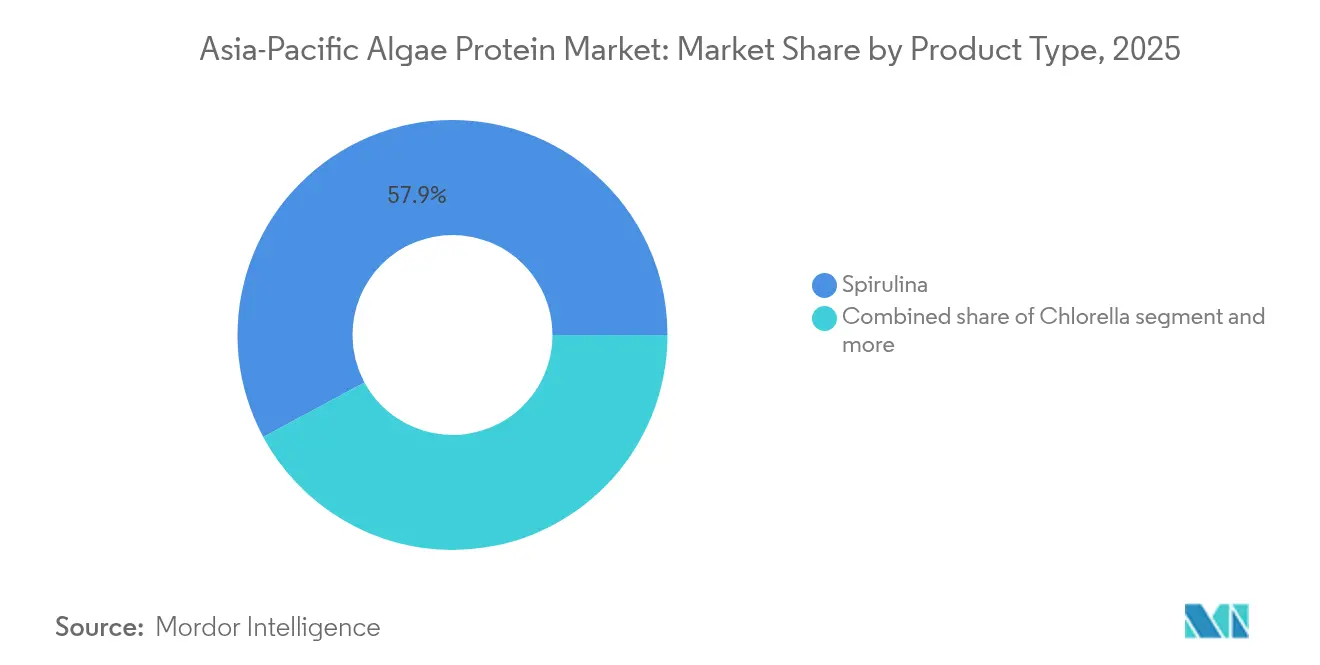

- By product type, spirulina led with 57.86% revenue share in 2025; chlorella is projected to expand at a 8.87% CAGR through 2031.

- By application, supplements captured 47.15% of revenue in 2025, while animal feed is advancing at an 8.53% CAGR to 2031.

- By geography, China held 34.05% of demand in 2025; India is expected to post the fastest growth at a 9.41% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Algae Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for alternative protein sources | +2.1% | China, India, Singapore, Thailand | Medium term (2-4 years) |

| Increasing consumer awareness of algae's nutritional benefits | +1.5% | Japan, South Korea, Australia, New Zealand | Short term (≤ 2 years) |

| Growing demand from dietary supplements | +1.8% | China, India, Japan, South Korea | Short term (≤ 2 years) |

| Easy availability of raw material | +1.2% | Indonesia, Thailand, China, India | Long term (≥ 4 years) |

| Increasing popularity of algae fortified products | +1.0% | Singapore, Japan, Australia, urban China | Medium term (2-4 years) |

| Government initiative towards algae farming | +1.4% | Singapore, India, Indonesia, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing demand for alternative protein sources

The algae protein market in the Asia-Pacific region is experiencing significant growth, driven by increasing demand for alternative proteins such as spirulina and chlorella in animal feed. These alternatives are progressively replacing traditional sources like soy and fishmeal, addressing sustainability challenges in aquaculture and livestock sectors. The adoption of spirulina in animal feed is accelerating at a rapid pace in the region, supported by substantial investments in large-scale cultivation and expedited regulatory approvals for eco-friendly feeds. As protein consumption per capita rises, domestic production of soy and peas in Asia-Pacific is unable to keep up, resulting in a growing protein deficit. This has created a structural demand for ingredients that do not depend on arable land. Algae, cultivated in photobioreactors or open ponds, eliminates the need for arable land and can be grown on marginal coastal or desert terrains. This geographic adaptability appeals to governments focused on enhancing food sovereignty. Additionally, China's decision to include microalgae in its 14th Five-Year Plan for bio-manufacturing highlights its efforts to reduce reliance on imported soy for animal feed.

Increasing consumer awareness of algae's nutritional benefits

In Japan and South Korea, where an aging population drives the demand for functional foods, clinical evidence highlighting the immune-boosting and antioxidant properties of spirulina and chlorella has shifted from niche wellness discussions to mainstream dietary recommendations. The World Bank indicates that in 2024, 30% of Japan's population will be aged 65 and older[1]Source: World Bank, "Population ages 65 and above", worldbank.org. These older consumers increasingly turn to algae proteins, such as spirulina and chlorella, attracted by their rich profiles of amino acids, antioxidants, omega-3 fatty acids, vitamins, and minerals. These nutrients are recognized for supporting muscle maintenance, joint health, immunity, and providing anti-aging benefits. In 2024, Japan's Ministry of Health, Labour and Welfare classified chlorella as a "Food with Function Claims." This classification permits manufacturers to market its immune-support benefits without prior approval, expediting product launches by 6 to 9 months. However, this awareness is uneven: urban consumers in Tokyo, Seoul, and Sydney are willing to pay premium prices for organic spirulina tablets, while rural consumers in India and Indonesia, being more price-sensitive, prefer fortified staples over standalone supplements. This disparity segments the market into distinct tiers based on willingness to pay.

Growing demand from dietary supplements

Brands are increasingly incorporating algae into their offerings, not only for its high protein content but also for its bioactive pigments, such as phycocyanin, which are promoted as natural performance enhancers. This shift in the sports-nutrition segment toward plant-based proteins has created significant opportunities for algae-based products. At the same time, the elderly nutrition sector is emerging as another area of growth. Sarcopenia, a condition that affects muscle mass and strength in individuals over 65, is particularly prevalent among Asians. Clinical trials have demonstrated that algae-derived amino acids are more effective than whey protein in improving muscle retention, especially among lactose-intolerant populations, a demographic that is notably large in China and Southeast Asia. Regulatory developments are further driving this trend. In 2024, India's Food Safety and Standards Authority of India (FSSAI) approved algal protein powder, removing previous compliance barriers. This approval has enabled brands to transition from grey-market channels to legitimate distribution networks, including pharmacies and e-commerce platforms, thereby expanding their reach and accessibility.

Easy availability of raw material

Asia-Pacific is a leading region in the global production of seaweed and microalgae biomass. This production concentration helps the region avoid the raw-material shortages faced by processors in Europe and North America. In 2024, China achieved a cultured algae production volume of 3.04 million metric tons, according to its Ministry of Agriculture and Rural Affairs[2]Source: Ministry of Agriculture and Rural Affairs, "China fishing industry statistical bulletin 2024", moa.gov.cn. The region's established infrastructure enables capacity expansions with shorter lead times and lower capital expenditures compared to greenfield projects in other regions. Freshwater algae such as spirulina and chlorella are cultivated in controlled environments across China, India, Japan, and Southeast Asia. At the same time, coastal nations utilize natural seaweed harvests, reducing reliance on imports and ensuring supply chain stability. Government-supported initiatives, including China's focus on biotech processing and India's efforts in biodiversity utilization, capitalize on existing infrastructure and GRAS/FDA approvals to improve accessibility. Reflecting this commitment, the Indian government, as reported by the Press Information Bureau, has allocated INR 640 crore for seaweed cultivation from 2020 to 2025[3]Source: Press Information Bureau, "Seaweed: A Nutritional Powerhouse From The Ocean", pib.gov.in.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs | -1.8% | Japan, South Korea, Australia, Singapore | Medium term (2-4 years) |

| High availability of alternative protein sources | -1.2% | China, India, Thailand, Indonesia | Short term (≤ 2 years) |

| Technological challenges in improving protein yield and purity | -0.9% | Global, concentrated in new entrants | Long term (≥ 4 years) |

| Stringent regulatory approvals for novel food ingredients and health claims | -0.7% | Japan, South Korea, Australia, New Zealand | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production costs

Algae protein remains 2-3 times more expensive than soy or pea isolates, primarily due to the significant capital expenditure and energy consumption required for photobioreactor operations. In closed photobioreactor systems, energy costs represent 30-40% of total operating expenses. Although solar energy integration offers a potential solution to reduce these costs, regions such as Thailand and Indonesia face challenges due to monsoon seasons, which result in inconsistent sunlight availability. This forces producers to rely on grid power as a backup, thereby diminishing the cost-saving advantages of solar energy. Additionally, in high-wage markets like Japan and Australia, the labor-intensive nature of harvesting and dewatering processes further drives up production costs. The adoption of automation in these regions has been slow, as the biological variability of algae cultures complicates the implementation of standardized automated systems. These factors collectively contribute to the higher cost of algae protein compared to alternative protein sources.

High availability of alternative protein sources

In the Asia-Pacific region, soy and pea proteins dominate food formulations due to their numerous advantages. These proteins benefit from well-established supply chains, neutral flavor profiles that do not interfere with the taste of final products, and significantly lower costs, approximately 60-70% less than algae-based alternatives. Consequently, microalgae remain limited to premium or functional product segments. The differentiation of algae lies in its unique attributes, such as omega-3 fatty acids, pigments, and bioactive co-products. However, these benefits primarily attract supplement consumers who are willing to pay higher prices, rather than cost-sensitive food manufacturers who prioritize affordability when sourcing bulk proteins for applications like bakery products or meat analogs. For instance, in 2024, Thailand's poultry sector conducted trials using spirulina as a replacement for soy in animal feed. Despite its potential, the sector reverted to conventional feed after determining that spirulina increased costs by 12% without delivering proportional improvements in productivity.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Algae Gains on Aquaculture Omega-3 Demand

Marine algae are projected to grow at a rate of 8.74% from 2026 to 2031, surpassing the growth of freshwater algae, which accounted for a significant 71.62% market share in 2025. This growth is primarily driven by the aquaculture industry's transition away from wild-caught fishmeal, leading to increased demand for algal omega-3 oils. In 2024, Indonesia's seaweed development initiatives focus on cultivating Gracilaria and Eucheuma for carrageenan and protein co-extraction. By leveraging its 40% share of global seaweed production, Indonesia aims to enhance downstream value rather than relying on raw biomass exports. Freshwater algae, dominated by spirulina and chlorella, continue to hold a strong position in dietary supplements and food fortification due to established GRAS approvals and consumer trust. However, they face margin pressures as generic producers from China and India flood the market with bulk powders priced below USD 10 per kilogram.

Regulatory developments are increasingly favoring marine species in specific applications. In 2024, China's National Health Commission approved Nannochloropsis oil, creating opportunities for marine microalgae in functional foods. Conversely, freshwater species have not received comparable recent approvals. Freshwater cultivation benefits from lower salinity-management costs and compatibility with inland aquaculture systems. For example, Thailand's shrimp-spirulina co-production system has effectively reduced water-treatment expenses. Marine algae, with their higher iodine and trace-mineral content, appeal to functional-food formulators. However, these attributes also raise allergenicity concerns, complicating novel-food approvals in regions like Australia and South Korea, where regulators apply stricter scrutiny to marine-derived ingredients compared to freshwater alternatives.

By Product Type: Chlorella's Extraction Edge Narrows Spirulina's Lead

In 2025, spirulina led the market with a significant 57.86% share. However, chlorella is projected to grow at a robust rate of 8.87% through 2031. This contrasting growth trajectory stems from chlorella's superior protein extraction efficiency, particularly when processed using pulsed-electric-field technology. This advanced method effectively disrupts chlorella's rigid cell wall without causing thermal degradation, preserving its nutritional integrity. Furthermore, chlorella's growth factor (CGF), a unique nucleotide-peptide complex, commands a 30-40% price premium in Japan's elderly-nutrition market. Clinical studies have demonstrated CGF's role in immune modulation, a benefit that sets chlorella apart. Despite spirulina's higher overall protein content, it cannot replicate this specific functional advantage, giving chlorella a competitive edge in targeted applications.

Other algae species, including Nannochloropsis, Tetraselmis, and Haematococcus, currently hold a smaller market share but are experiencing growth as niche applications gain traction. For example, Haematococcus-derived astaxanthin, marketed by companies such as Cyanotech and Algatech, is increasingly utilized in aquaculture feed and sports supplements due to its high-value antioxidant properties. Spirulina's established GRAS status and strong consumer recognition continue to reinforce its dominance in the dietary supplement market. However, chlorella's distinct functional benefits, coupled with its processing advantages, position it as a strong contender to capture additional demand. Food manufacturers seeking clean-label protein sources with added health benefits are likely to drive this incremental growth for chlorella.

By Application: Animal Feed Outpaces Supplements on Cost-Sensitive Demand

In 2025, supplements contributed 47.15% of application revenue, driven by their premium pricing in segments such as sports nutrition and elderly health. However, the animal feed segment is anticipated to grow at a compound annual growth rate (CAGR) of 8.53% through 2031. This growth is attributed to cost-conscious livestock and aquaculture producers increasingly replacing imported soy with domestically cultivated algae. Veramaris' USD 200 million algal-oil facility, which became operational in June 2024, plays a pivotal role in this shift. The facility supplies omega-3 concentrates to salmon and shrimp farms, addressing the rising demand from producers aiming to mitigate risks associated with microplastic contamination and the supply-chain uncertainties tied to wild-catch sources.

Although supplements are experiencing slower growth due to market saturation in Japan and South Korea, where spirulina and chlorella have already achieved significant penetration among health-conscious adults, there remains an opportunity for geographic expansion into emerging markets such as Southeast Asia and India. On the other hand, elderly nutrition is emerging as a key growth area. Sarcopenia, a condition that affects muscle mass and strength, is prevalent among Asians aged 65 and older. Clinical trials have demonstrated that algae-derived amino acids are more effective than whey protein in improving muscle retention, particularly among lactose-intolerant populations. This demographic trend is especially relevant in regions like China and Southeast Asia. In the animal feed sector, the cost sensitivity of producers limits algae usage to high-value applications, such as aquaculture and premium pet food, where the benefits of omega-3 enrichment and pigmentation justify the higher costs. Meanwhile, the use of algae in poultry and swine feed remains largely in the experimental stage.

Geography Analysis

In 2025, China holds a significant 34.05% share of the market, driven by its cost-effective spirulina cultivation. This cultivation is concentrated in Hainan province, where abundant year-round sunlight and brackish water help lower production costs. China's National Health Commission approved Nannochloropsis oil in 2024, creating opportunities for marine microalgae in functional foods. However, commercialization faces challenges due to limited production capacity and higher extraction costs compared to spirulina. Fresh spirulina is now being promoted in beverages and desserts through enclosed photobioreactors, appealing to Gen-Z consumers who see its green color as a natural food dye rather than a flaw. Despite this, China struggles with quality perception issues, as international buyers often associate Chinese algae with contamination risks. Premium producers are addressing this concern by obtaining third-party certifications such as USDA Organic and ISO 22000.

From 2026 to 2031, India is projected to grow at a robust 9.41%, the fastest rate in the region. This growth is driven by FSSAI's 2024 approval of algal protein powder for Reliance, which removed a regulatory barrier. This approval has legitimized the product and enabled its distribution through pharmacy and e-commerce channels, moving it out of the grey market. India's advantage lies in its dual regulatory framework: algal ingredients with traditional use bypass the novel-food classification, while state-level subsidies reduce capital expenditures. This combination creates a market entry timeline that is 6-9 months faster than in Japan or South Korea. Startups like Seagrass Tech are leveraging this advantage to launch localized products ahead of multinational competitors. However, maintaining consistent quality remains a challenge due to fragmented cultivation practices.

Japan, Thailand, Indonesia, and Singapore are at the forefront of policy innovation, implementing measures that enhance the competitiveness of their algae protein markets. These countries are adopting strategies such as blue-carbon credits, aquaculture integration, and hybrid facilities to reduce production costs. Despite higher labor expenses in the region, these policy measures help offset costs and ensure that production remains competitive. By fostering such innovations, these nations are successfully anchoring regional production within the algae protein market and maintaining their relevance in the global landscape.

Competitive Landscape

In the Asia-Pacific algae protein market, top players such as DIC Corporation, Parry Nutraceuticals, Corbion NV, Cyanotech Corporation, and Far East Bio Tech Co. Ltd. collectively hold a significant share. Despite this, the market remains fragmented due to production economics that favor regional clusters over global consolidation. Smaller entrants, including Brevel, are capitalizing on hybrid fermentation-photosynthesis techniques, which enable them to reduce energy costs by 50%. This innovative process presents a challenge for established players with legacy photobioreactor investments, as adopting such advancements could result in substantial stranded-asset write-offs, making it difficult for them to compete on cost efficiency.

Food-ingredient applications present a significant growth opportunity, as algae's current penetration in categories such as bakery, dairy alternatives, and meat analogs remains below 5%. This limited adoption is primarily due to challenges related to flavor and color, which can be addressed through sensory innovations like deodorization and microencapsulation. The market is predominantly led by Chinese players, driven by the country's high production capacity for algae-based ingredients. To strengthen their market position, key players are actively engaging in acquisitions and mergers, aiming to expand their geographical presence and grow their customer base.

Disruptors on the rise include precision-fermentation startups. These companies sidestep photosynthesis, instead producing algae proteins in bioreactors using sugar feedstocks. This method holds the promise of achieving cost parity with soy by 2027. However, it grapples with regulatory uncertainties in many Asia-Pacific markets, where novel-food frameworks are still trying to define fermentation outputs. Patent activity has surged, particularly in extraction technologies like pulsed-electric-field and enzyme-assisted hydrolysis, doubling since 2024. This uptick underscores the industry's focus on yield improvement as a key competitive edge. For export-oriented producers, obtaining ISO 22000 and FSSC 22000 certifications has become essential. International buyers now prioritize traceability and contamination controls, standards that open-pond systems often struggle to meet. Strategic approaches vary: while multinationals chase geographic diversification and a broader co-product portfolio, regional players adopt a different tactic. They often launch in markets like India or China, where regulatory approvals are swifter, and once they've built brand equity, they pivot to exporting to premium markets.

Asia-Pacific Algae Protein Industry Leaders

-

Corbion NV

-

Cyanotech Corporation

-

Parry Nutraceuticals

-

Far East Bio Tech Co. Ltd.

-

DIC Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Corbion has received regulatory approvals in China to introduce its algae-based omega-3 DHA solutions. These solutions are designed to cater to both the human and animal nutrition markets, marking a significant step for Corbion in expanding its presence in the Chinese market.

- December 2024: LO Carbon Solutions, in partnership with the Kerala University of Fisheries and Ocean Studies (KUFOS), has unveiled India's inaugural micro-algae-based liquid tree. This groundbreaking prototype aims to transform urban air quality management, seamlessly blending biotechnology with innovative design.

Asia-Pacific Algae Protein Market Report Scope

| Freshwater Algae |

| Marine Algae |

| Spirulina |

| Chlorella |

| Others |

| Food and Beverages | Bakery |

| Dairy and Dairy Alternative Products | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| Others | |

| Supplements | Sport/Performance Nutrition |

| Elderly Nutrition and Medical Nutrition | |

| Animal Feed | |

| Others |

| China |

| Japan |

| India |

| Thailand |

| Singapore |

| Indonesia |

| South Korea |

| Australia |

| New Zealand |

| Rest of Asia-Pacific |

| By Source | Freshwater Algae | |

| Marine Algae | ||

| By Product Type | Spirulina | |

| Chlorella | ||

| Others | ||

| By Application | Food and Beverages | Bakery |

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| Others | ||

| Supplements | Sport/Performance Nutrition | |

| Elderly Nutrition and Medical Nutrition | ||

| Animal Feed | ||

| Others | ||

| By Country | China | |

| Japan | ||

| India | ||

| Thailand | ||

| Singapore | ||

| Indonesia | ||

| South Korea | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

Key Questions Answered in the Report

What is the current value of the Asia-Pacific algae protein market?

The algae protein market size stands at USD 60.52 million in 2026.

How fast is the market expected to grow?

It is forecast to register an 8.12% CAGR, reaching USD 89.27 million by 2031.

Which segment is growing the fastest?

Marine algae is expanding at an 8.74% CAGR, driven by aquaculture demand for omega-3 oils.

Why is India considered the most promising country?

India combines a 9.41% forecast CAGR, streamlined FSSAI approvals, and 30% capital subsidies that accelerate photobioreactor deployment.

Page last updated on: