EPA-Focused Algae Omega-3 Ingredients Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

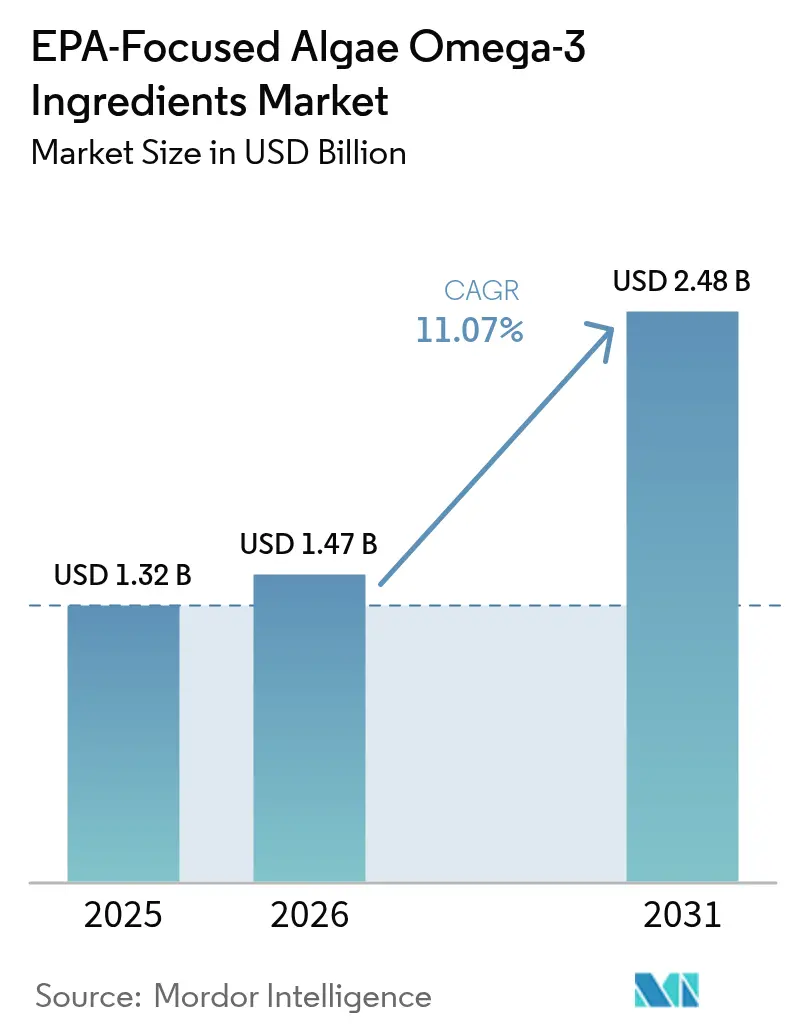

| Market Size (2026) | USD 1.47 Billion |

| Market Size (2031) | USD 2.48 Billion |

| Growth Rate (2026 - 2031) | 11.07% CAGR |

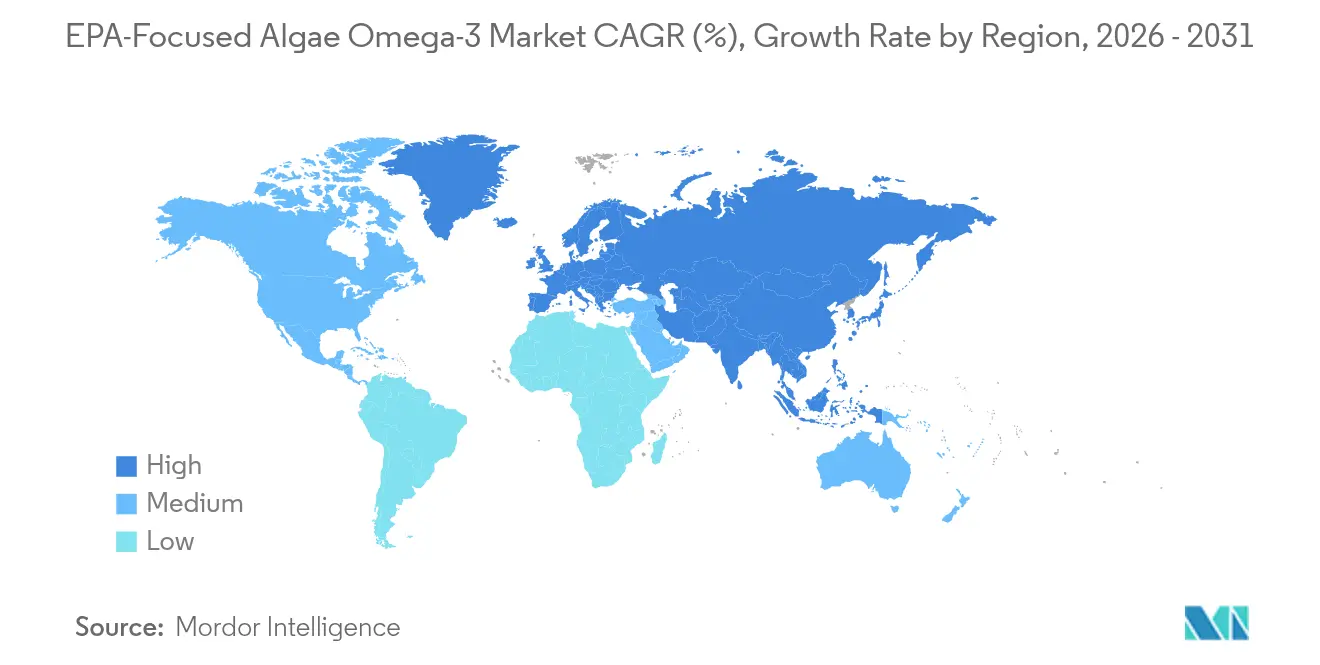

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

EPA-Focused Algae Omega-3 Ingredients Market Analysis by Mordor Intelligence

The EPA-Focused Algae Omega-3 Ingredients market size is expected to grow from USD 1.32 billion in 2025 to USD 1.47 billion in 2026 and is forecast to reach USD 2.48 billion by 2031 at 11.07% CAGR over 2026-2031. The growing clinical validation of eicosapentaenoic acid (EPA) for cardiovascular risk reduction, regulatory endorsements that favor contaminant-free algal oils, and rising consumer preference for plant-based nutrition are accelerating the adoption of EPA across supplements, functional foods, and aquaculture feeds. Premium pricing for EPA-only formulations, coupled with scale efficiencies at vertically integrated fermenters, underpins attractive margins even as energy costs fluctuate. Market leaders leverage proprietary strains to enhance lipid productivity, while regional entrants explore photosynthetic cultivation to circumvent electricity-intensive heterotrophic processes. Technology convergence around strain engineering, waste-heat recovery, and co-location with sugar or glycerol sources continues to narrow cost gaps with fish oil, expanding addressable demand in emerging economies.

Key Report Takeaways

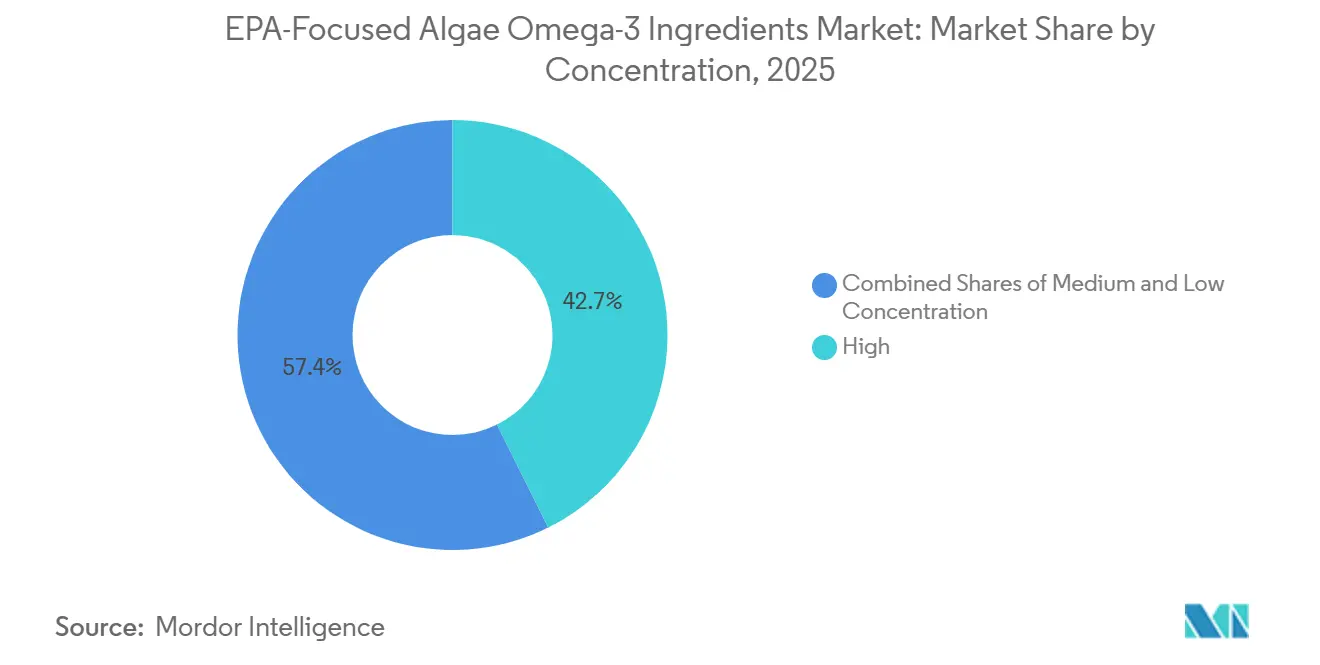

- By concentration, high-purity (>70% EPA) products controlled 42.65% of the EPA-focused algae omega-3 ingredients market share in 2025, whereas medium-concentration (40-69% EPA) offerings are growing fastest at a 12.63% CAGR to 2031.

- By form, triglyceride-structured EPA captured 51.60% of 2025 revenue and is on track for a 12.42% CAGR through 2031.

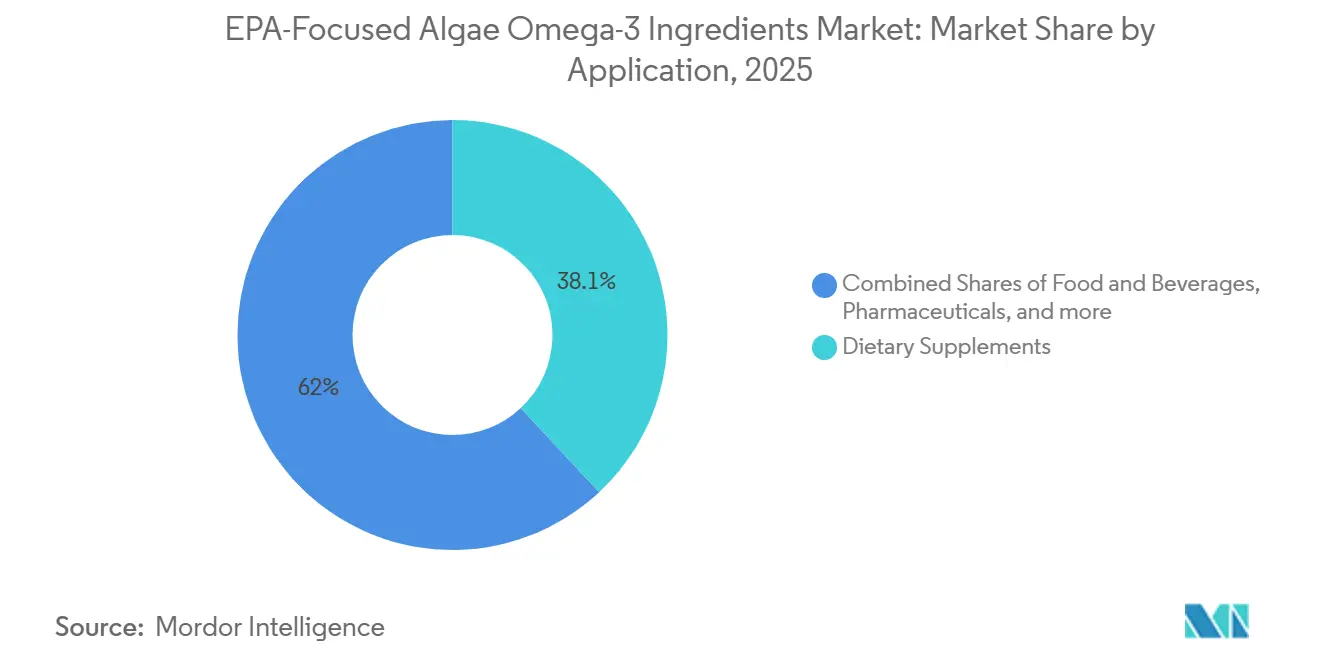

- By application, dietary supplements led with 38.05% of 2025 sales, yet food and beverage usage is expanding at 12.72% annually to 2031.

- By geography, North America held 35.95% of 2025 revenue, while the Asia Pacific region records the strongest 12.34% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global EPA-Focused Algae Omega-3 Ingredients Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging health awareness boosts demand for EPA in heart health and cognitive support | +2.8% | Global, with strongest uptake in North America and Europe | Medium term (2-4 years) |

| Vegan and plant-based diet trends favor algae-derived EPA | +2.5% | North America, Europe, APAC urban centers | Long term (≥ 4 years) |

| Increasing applications in infant formulas and functional foods | +2.2% | Europe, Asia Pacific, North America | Medium term (2-4 years) |

| Regulatory approvals and government initiatives promote algae omega-3 | +1.8% | Global, led by EU and U.S. FDA frameworks | Short term (≤ 2 years) |

| Innovation in high-purity, contaminant-free algal strains | +1.5% | Global, with R&D hubs in Netherlands, U.S., China | Long term (≥ 4 years) |

| Adoption in precision aquaculture feed formulations | +1.7% | Asia Pacific, Europe, South America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Health Awareness Boosts Demand for EPA in Heart Health and Cognitive Support

Cardiovascular disease continues to be the leading cause of mortality worldwide. The REDUCE-IT trial showed that a daily intake of 4 grams of icosapent ethyl reduced major adverse cardiac events by 25% in statin-treated patients, raising EPA from a general wellness ingredient to a targeted therapeutic option. This clinical validation prompted the American Heart Association to revise its 2024 guidelines, recommending EPA-rich supplementation for individuals with triglyceride levels above 150 milligrams per deciliter, a condition affecting approximately 25% of U.S. adults[1]Source: American Heart Association, “Omega-3 Scientific Statement 2024,” heart.org. Algae-derived EPA serves as a contaminant-free alternative to fish oil, which the Environmental Protection Agency has flagged for methylmercury accumulation in predatory species like tuna and swordfish. Furthermore, emerging research on EPA's role in neuroinflammation suggests it may help slow cognitive decline in early-stage Alzheimer's patients by modulating microglial activation, a mechanism distinct from DHA's structural role in neuronal membranes. In Japan, the Consumer Affairs Agency approved a "Foods with Function Claims" label for algae-derived EPA products designed to support memory retention in adults over 60. This regulatory milestone has enabled the distribution of these products through convenience-store chains in Tokyo and Osaka.

Vegan and Plant-Based Diet Trends Favor Algae-Derived EPA

The global shift toward plant-based diets has underscored a structural disconnect between consumer preferences and traditional omega-3 sources. Fish-oil production reduces forage stocks, such as Peruvian anchoveta, and increases bycatch mortality. Algae EPA, which meets vegan certification standards from The Vegan Society, attracts flexitarian consumers who focus on environmental concerns rather than ethical issues. In 2024, sales of plant-based protein products in the United States rose by 27%, with prominent brands like Ripple Foods and Oatly incorporating algae omega-3 into their beverages to address nutritional deficiencies caused by reduced seafood intake. Corbion's AlgaPrime DHA, initially designed for aquaculture, has also gained popularity among vegan supplement brands promoting "ocean-friendly" EPA capsules. These capsules command a 15-20% price premium over traditional fish-oil softgels in European retail markets. Life-cycle assessments reveal that algae fermentation generates 63% lower greenhouse gas emissions per kilogram of omega-3 compared to wild-catch fisheries, aligning with corporate buyers' Scope 3 carbon-reduction objectives. Younger consumers, particularly those aged 25 to 40, show a greater willingness to pay for sustainability-certified ingredients. This behavior indicates that the vegan-EPA segment is poised to grow faster than fish-oil alternatives as Millennial and Gen-Z groups reach their peak earning years.

Increasing Applications in Infant Formulas and Functional Foods

Manufacturers of infant formula are facing increasing regulatory requirements to replicate the fatty-acid profile of human breast milk, which contains both EPA and DHA in ratios typically ranging from 1:3 to 1:5, depending on maternal diet. The European Food Safety Authority's (EFSA) 2024 update to infant formula guidelines allows the inclusion of algae-derived EPA at concentrations up to 0.5% of total fatty acids, provided the source organism is either Schizochytrium or Crypthecodinium, and contaminant testing confirms heavy metal levels below 0.01 parts per million[2]Source: European Food Safety Authority. "Novel Foods Authorisation."efsa.europa.eu. In the United States, manufacturers operating under FDA GRAS (Generally Recognized as Safe) notices have begun reformulating stage-2 formulas for infants aged 6 to 12 months, incorporating algae-derived EPA to support visual and cognitive development during the critical myelination phase. In addition to infant nutrition, functional food applications for algae-derived EPA are expanding into products such as fortified yogurt, granola bars, and ready-to-drink smoothies. The neutral taste profile and oxidative stability of algae EPA enable manufacturers to include 50-100 milligrams per serving without the off-flavors associated with earlier fish-oil formulations. For example, Danone's 2024 launch of an EPA-fortified probiotic yogurt in France utilized Schizochytrium oil to support gut-brain axis claims. This dual-benefit positioning led to an 18% higher repeat-purchase rate compared to standard probiotic SKUs.

Regulatory Approvals and Government Initiatives Promote Algae Omega-3

Government endorsements and streamlined approval pathways are driving algae EPA's evolution from a niche ingredient to a mainstream input. In 2024, China's National Medical Products Administration updated its health-food registration guidelines, recognizing algae-derived omega-3 as an approved functional component. This update reduced the approval timeline from 24 to 12 months and removed the requirement for domestic clinical trials if applicants provide safety dossiers from EFSA or FDA. In the UK, the Food Standards Agency issued a positive safety assessment for high-EPA algae oils in 2024. This approval enables their inclusion in meal-replacement shakes and sports-nutrition powders, which can now be distributed through National Health Service-approved channels. In the U.S., the FDA permits a qualified health claim associating omega-3 with a reduced risk of coronary heart disease, applicable to algae EPA[3]Source: U.S. Food and Drug Administration. "Qualified Health Claims for Omega-3 Fatty Acids." fda.gov. However, labels must state that the claim is based on "supportive but not conclusive research." These regulatory developments simplify market entry for new brands and lower compliance costs for multinational companies reformulating their products. This shift increasingly positions algae EPA as a preferred alternative to fish oil, particularly in regions with stringent contaminant testing.

Restraint Impact Analysis*

| Restraints | (~)% Impact on CAGR Forecasts | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production costs from fermentation processes | -1.8% | Global, most acute in regions with high energy costs (Europe, Japan) | Medium term (2-4 years) |

| Technical challenges in achieving high EPA yields | -1.2% | Global, affecting all heterotrophic fermentation operations | Long term (≥ 4 years) |

| Supply chain dependencies on controlled fermentation | -0.9% | Global, with vulnerabilities in glucose and nitrogen supply | Short term (≤ 2 years) |

| Environmental concerns over energy-intensive production | -1.1% | Europe, North America (carbon-tax jurisdictions) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Production Costs from Fermentation Processes

Producing 10,000 metric tons of EPA from microalgae requires substantial investment. Facilities demand over USD 150 million due to the need for pharmaceutical-grade glucose, sterile bioreactors, and stringent temperature controls. Once operational, energy consumption becomes a major cost driver, reaching 8-12 kilowatt-hours per kilogram of crude algae oil. In 2024, European producers faced significant challenges when natural gas prices spiked to approximately USD 127 per megawatt-hour following pipeline disruptions. This increase forced some producers to halt operations and rely on lower-cost Asian suppliers for finished oils. Labor costs further strain budgets, as skilled bioprocess engineers and quality-assurance personnel contribute 15-20% to total expenses. Western producers are particularly affected, competing with Chinese and Indian fermentation plants where wages are 40-60% lower. Additionally, achieving economies of scale remains difficult for facilities producing less than 5,000 metric tons annually. This limitation has led to market consolidation, favoring vertically integrated giants capable of distributing fixed costs across multiple product lines.

Technical Challenges in Achieving High EPA Yields

Wild-type strains of Schizochytrium and Nannochloropsis synthesize DHA and EPA alongside other lipids, such as palmitic and oleic acids. In typical fermentations, this restricts EPA content to 10-15% of the total lipid yield. Researchers have enhanced desaturase and elongase enzyme activity through metabolic engineering, achieving laboratory yields of 25% EPA in Yarrowia lipolytica. However, scaling these results to industrial levels presents challenges, including plasmid loss, culture contamination, and reduced biomass productivity. Downstream purification processes, such as molecular distillation and chromatography, increase production costs by 30-40%. Additionally, each purification step results in a 5-10% yield loss, diminishing the economic advantages of high-EPA strains. Although photosynthetic cultivation of Nannochloropsis in open ponds is energy-efficient, it faces issues like seasonal variability, contamination from competing algae species, and EPA levels that rarely exceed 3% of dry weight, making it unsuitable for pharmaceutical-grade applications. The technical limit on EPA yield per fermenter run further constrains throughput, forcing producers to either invest in additional bioreactor capacity or accept lower margins on medium-purity products.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Concentration: Premium Purity Commands Cardiovascular Segment

In 2025, high-concentration EPA formulations, containing 70% or more EPA by weight, accounted for 42.65% of the market share, primarily due to their use in pharmaceutical applications. These applications require icosapent ethyl prescriptions to meet FDA monograph standards, which demand 96% purity. Medium-concentration products, with 40-69% EPA, are growing at an annual rate of 12.63% through 2031. This growth is driven by functional-food manufacturers who balance bioavailability with ingredient costs. These manufacturers incorporate 50-60% EPA oils into fortified beverages and snack bars, targeting general wellness rather than disease management. In contrast, low-concentration offerings, with less than 40% EPA, are used in aquaculture feed and pet nutrition. In these segments, the cost per kilogram of omega-3 is prioritized over absolute purity, allowing for the co-extraction of DHA and other fatty acids. Ingredient suppliers are shifting their focus to medium concentrations, recognizing that while food and beverage brands cannot absorb the 40-50% price premium of pharmaceutical-grade purification, they still require EPA levels sufficient to support health claims on packaging.

Regulatory compliance significantly impacts concentration choices. For example, the European Union's Novel Food framework permits algae oils with up to 450 milligrams of EPA per daily serving in dietary supplements without requiring additional safety data. However, higher doses necessitate clinical-trial approval. Similarly, Japan's Ministry of Health, Labour and Welfare limits EPA to 600 milligrams per day for over-the-counter products, with higher amounts requiring prescription oversight. To address these requirements, Veramaris and DSM-Firmenich have invested in modular purification lines. These systems can adjust concentration targets within a single production run, enabling them to serve pharmaceutical, supplement, and food clients from the same fermentation batch while managing demand fluctuations across various end-use segments. Additionally, emerging strain-engineering efforts aim to produce 80% EPA directly in the fermenter. This innovation eliminates the need for costly distillation processes and reduces the price gap between medium and high concentrations.

By Form: Triglyceride Structure Mirrors Human Milk

In 2025, triglyceride-form EPA contributed 51.60% of the market revenue, with a projected growth rate of 12.42% through 2031. This growth is driven by its superior bioavailability and structural similarity to human breast milk, where omega-3 fatty acids are located at the sn-2 position of the glycerol backbone. Clinical studies reveal that triglyceride EPA achieves 50% higher plasma incorporation compared to ethyl-ester formulations when consumed with a low-fat meal. This characteristic is particularly significant for infant-formula applications, where fat content is strictly regulated. Ethyl-ester EPA, which held a 32.25% market share in 2025, remains the leading form in pharmaceutical products due to its ability to deliver higher EPA content per capsule, typically 1,000 milligrams versus 600-700 milligrams for triglycerides, and its adherence to USP (United States Pharmacopeia) monograph standards for prescription omega-3 drugs. Phospholipid-form EPA, derived from polar lipid fractions of specific algae species, accounted for the remaining 16.15% of the market. Its growing use in cognitive-health supplements is supported by evidence that phosphatidylcholine-bound EPA crosses the blood-brain barrier more effectively than free fatty acids.

In 2025, the European Food Safety Authority issued an opinion on algae-oil safety, noting that triglyceride forms exhibit lower oxidation rates during storage. This characteristic extends their shelf life to 24 months, compared to 18 months for ethyl esters under similar packaging conditions. Corbion's AlgaPrime product line utilizes enzymatic re-esterification to convert ethyl-ester intermediates back into triglycerides. While this process increases production costs by USD 2-3 per kilogram, it enables premium pricing in European infant-formula tenders, where procurement specifications require the triglyceride form. However, phospholipid EPA faces limitations due to its low natural abundance in most algae strains, typically 5-8% of total lipids. This scarcity necessitates selective extraction, driving costs above USD 200 per kilogram and restricting its use to high-margin nootropic supplements sold directly to consumers. Efforts to enhance phospholipid synthesis are underway, with research institutions in the Netherlands and Australia investigating genetic modifications of Nannochloropsis. Pilot-scale trials are anticipated in 2026.

By Application: Supplements Lead, Food Accelerates

In 2025, dietary supplements constituted 38.05% of the demand, driven by well-established distribution networks such as health-food retailers, e-commerce platforms, and pharmacy chains, which prominently feature omega-3 softgels. Food and beverage applications, expanding at an annual growth rate of 12.72%, are the fastest-growing among all end uses. Plant-based protein brands are incorporating algae EPA into ready-to-drink shakes, fortified oat milk, and functional snack bars, capitalizing on cognitive-health and cardiovascular-wellness claims, as highlighted by Innova Market Insights. Infant-formula manufacturers represent a high-value niche in the food sector, with EPA prices reaching USD 180-220 per kilogram. This premium pricing reflects compliance with stringent European and U.S. regulations on contaminant levels and fatty-acid ratios. Pharmaceutical applications, particularly prescription icosapent ethyl for severe hypertriglyceridemia, yield the highest profit margins but face volume constraints. These limitations stem from the requirement for 96% EPA purity and adherence to Good Manufacturing Practice regulations mandated by the FDA and the European Medicines Agency.

Animal-feed applications, especially in salmon and shrimp aquaculture, accounted for 17.65% of the 2025 volume and are growing at a rate of 11.28%. Producers aim to reduce dependence on wild-catch fishmeal and fish oil, which have experienced price volatility exceeding 30% year-over-year due to El Niño-related declines in anchovy stocks off the coast of Peru, as reported by the FAO Fisheries Report. In 2024, Veramaris demonstrated through trials that replacing 50% of fish oil in salmon feed with algae EPA maintained fillet omega-3 content above 2 grams per 100 grams while improving feed-conversion ratios from 1.25 to 1.15. This enhancement translates to cost savings of USD 0.08-0.12 per kilogram of harvested fish. Shrimp hatcheries in Thailand and Vietnam are adopting algae EPA to enhance larval survival rates, which can drop below 40% when fishmeal is contaminated with Vibrio bacteria. Algae oils eliminate this pathogen risk, increasing survival rates to 65-70% in controlled trials. Additionally, regulatory frameworks in the European Union now permit "fed with algae omega-3" labeling on farmed salmon packaging. This labeling provides a marketing advantage and supports premium pricing in sustainability-focused retail markets.

Geography Analysis

In 2025, North America captured a 35.95% market share, driven by the U.S.'s USD 8 billion dietary-supplement industry. The regulatory framework in the U.S., under the Dietary Supplement Health and Education Act, allows omega-3 products to make structure-function claims without requiring pre-market FDA approval. The American Heart Association's 2024 recommendation of EPA supplementation for individuals with elevated triglycerides has boosted both prescription and OTC demand. Additionally, the U.S. Department of Agriculture's 2025-2030 Dietary Guidelines identified algae-derived omega-3 as a viable seafood alternative for those avoiding animal products. In Canada, the Natural and Non-prescription Health Products Directorate approved several algae-EPA products for cardiovascular claims in 2024, enabling distribution through national pharmacy chains like Shoppers Drug Mart. In Mexico, the growing middle class and a 35% prevalence of metabolic syndrome among adults over 40 are driving demand for omega-3 supplements. However, import tariffs on finished products exceeding 15% present an opportunity to develop domestic fermentation capacity.

Asia Pacific is projected to grow at an annual rate of 12.34% through 2031, making it the fastest-growing region. This growth is largely fueled by China's National Health Awareness Campaign, which emphasized omega-3 consumption for urban populations and allocated CNY 2 billion (USD 280 million) for public education on cardiovascular disease prevention. In Japan, where 28% of the population is over 65, demand for cognitive-health supplements is rising. The Consumer Affairs Agency's 2024 approval of "Foods with Function Claims" labels for algae EPA, targeting memory retention has expanded distribution through convenience stores in cities such as Tokyo, Osaka, and Nagoya. India's dietary-supplement market grew by 22% in 2024, with algae EPA gaining popularity as a vegetarian-friendly option in a country where 30-40% of the population adheres to lacto-vegetarian diets for cultural or religious reasons. In Australia, the Therapeutic Goods Administration includes algae omega-3 in its complementary-medicines registry. Local brands like Melrose Health have introduced algae-EPA softgels aimed at fitness enthusiasts and plant-based consumers. In South Korea, the Ministry of Food and Drug Safety approved algae EPA for use in infant formula in 2024, prompting domestic manufacturers to reformulate their premium product lines.

Europe accounted for 24.10% of 2025 revenue, with Germany, the U.K., and France leading consumption due to high consumer awareness of omega-3 benefits and strict contaminant regulations that favor algae over fish oil. The European Food Safety Authority's updated Novel Food approvals for Schizochytrium oils have streamlined market entry, reducing time-to-market from 18 months to 9 months for products with established safety. Following Brexit, the U.K. established a separate regulatory pathway, allowing the Food Standards Agency to issue approvals. In 2024, the agency published positive safety assessments for high-EPA algae oils, permitting their use in meal-replacement shakes distributed through National Health Service channels. Spain and Italy are emerging as growth markets for algae EPA in functional foods, with Mediterranean diet followers increasingly adopting fortified olive oils and yogurt as convenient delivery formats. South America and the Middle East-Africa regions, which together represented 8.20% of 2025 demand, remain underpenetrated. However, Brazil's regulatory agency ANVISA approved algae omega-3 for dietary supplements in 2024, and Saudi Arabia's Food and Drug Authority is reviewing applications for infant formula. These developments could drive double-digit growth in these regions by 2027.

Competitive Landscape

The EPA-focused algae omega-3 ingredients market scores high in concentration as DSM-Firmenich, Corbion, and BASF collectively own fermentation IP, strain libraries, and large-scale purification. Veramaris’ Nebraska plant exceeds 15,000 tons annual capacity and delivered 30 % faster salmon weight gain in 2024 trials, winning multi-year contracts with Mowi and SalMar. Corbion reported a 22 % EBITDA margin on algae ingredients by piggybacking on lactic-acid infrastructure, while BASF bundles EPA with vitamins and carotenoids for one-stop procurement.

Strategically, leaders integrate backward into strain engineering and forward into turnkey formulations. Veramaris now sells pre-blended feed concentrates, and Corbion supplies ready-to-use infant-formula bases. Regional tariffs of 20-25 % on finished supplements leave white space for local fermenters in Brazil and South Africa. Patent activity in 2024 centered on CRISPR-editing Yarrowia and Schizochytrium to hit 30 % fermenter-level EPA, a breakthrough that could disrupt purification economics. Smaller firms like Fermentalg and BioProcess Algae target pharmaceutical niches where margins offset scale disadvantages, though their limited tonnage keeps them outside mainstream feed and food channels.

Emerging photosynthetic projects in desert climates aim to couple abundant sunlight with low land cost, but contamination control and yield variability have hindered commercialization. Horizontal alliances, such as Corbion-Bunge’s plan to use biodiesel glycerol waste, signal new cost-sharing tactics likely to influence future competitive dynamics across the EPA-focused algae omega-3 ingredients market.

EPA-Focused Algae Omega-3 Ingredients Industry Leaders

-

Omega Protein Corporation

-

The Archer Daniels Midland Company

-

DSM-Firmenich

-

Corbion N.V.

-

BASF SE

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: GC Rieber VivoMega, a Norwegian omega-3 specialist, has introduced Algae 1060 TG Premium, a highly concentrated algae oil delivering both EPA and DHA in triglyceride form for superior absorption and formulation flexibility.

- July 2025: Corbion has obtained multiple regulatory approvals from China's General Administration of Customs (GACC) for its AlgaPrime DHA and AlgaVia DHA brands, enabling market entry in human and animal nutrition segments.

- October 2024: DSM-Firmenich expanded its life's omega-3 nutraceutical portfolio with the launch of life's DHA B54-0100. The functional ingredient, which was launched worldwide following the announcement, became the company's most potent DHA oil to date. According to DSM, Life's DHA B54-0100 delivered 545mg of DHA and 80mg of EPA per serving — providing users with 620mg of omega-3s in one serving. Through this highly concentrated oil, dietary supplement makers could create smaller and more cost-effective capsules with high bioactivity.

Global EPA-Focused Algae Omega-3 Ingredients Market Report Scope

The EPA-focused algae Omega-3 ingredient market has been segmented by concentration into high concentration, medium concentration, and low concentration; by form into triglycerides and phospholipids. and ethyl esters; and by application into food and beverage, dietary supplements, pharmaceuticals, and animal feed. The market is segmented by geography into North America, Europe, Asia-Pacific, South America, and Middle-East, and Africa. The market sizing has been done in value terms in USD for all the abovementioned segments.

| High Concentration |

| Medium Concentration |

| Low Concentration |

| Triglycerides |

| Ethyl Esters |

| Phospholipids |

| Food and Beverages | Functional Food and Beverages |

| Infant Formulas | |

| Others | |

| Dietary Supplements | |

| Pharmaceuticals | |

| Animal Feed |

| North America | United States |

| Mexico | |

| Canada | |

| Rest of North America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Netherlands | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Concentration | High Concentration | |

| Medium Concentration | ||

| Low Concentration | ||

| By Form | Triglycerides | |

| Ethyl Esters | ||

| Phospholipids | ||

| By Application | Food and Beverages | Functional Food and Beverages |

| Infant Formulas | ||

| Others | ||

| Dietary Supplements | ||

| Pharmaceuticals | ||

| Animal Feed | ||

| By Geography | North America | United States |

| Mexico | ||

| Canada | ||

| Rest of North America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Netherlands | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the EPA-Focused Algae Omega-3 Ingredients Market in 2026?

The EPA-Focused Algae Omega-3 Ingredients Market size is USD 1.47 billion in 2026.

What CAGR is forecast for EPA-Focused Algae Omega-3 Ingredients Market from 2026 to 2031?

A compound annual growth rate of 11.07% is projected over 2026-2031.

Which concentration segment is expanding fastest?

Medium-concentration (40-69% EPA) oils are rising at a 12.63% CAGR, driven by functional-food demand.

Which geographic region is growing quickest?

Asia Pacific leads with a 12.34% CAGR owing to public-health campaigns and aging populations.

Page last updated on: