Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

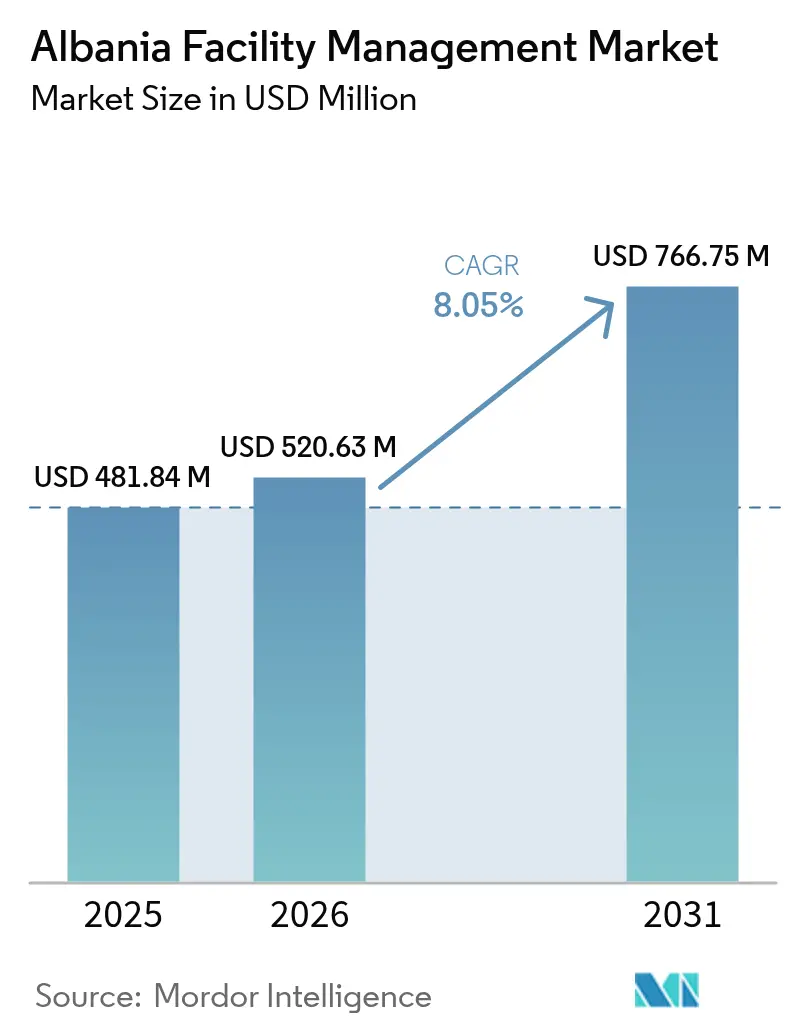

| Base Year Market Size (2025) | USD 481.84 Million |

| Market Size (2026) | USD 520.63 Million |

| Market Size (2031) | USD 766.75 Million |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Albania Facility Management Market Analysis by Mordor Intelligence

The Albania facility management market size is expected to grow from USD 481.84 million in 2025 to USD 520.63 million in 2026 and is forecast to reach USD 766.75 million by 2031 at 8.05% CAGR over 2026-2031. This Albania facility management market size outlook reflects rapid real-estate expansion, the 2026 roll-out of national energy-performance standards, and growing reliance on outsourced service providers.[1]European Bank for Reconstruction and Development, “Albania Country Strategy,” ebrd.com Robust EU pre-accession financing, tighter building regulations, and technology adoption are aligning to shift building owners toward performance-based contracts that couple predictive maintenance with guaranteed energy savings. International hotel chains entering Tirana and the coastal corridor are setting new service benchmarks that cascade across commercial, institutional, and industrial properties. Technical skills shortages have magnified the cost advantages of outsourcing, while municipal infrastructure upgrades tied to EU funds are expanding the scope of professional facilities oversight. Together, these drivers are repositioning the Albania facility management market from reactive maintenance to data-driven asset stewardship.

Key Report Takeaways

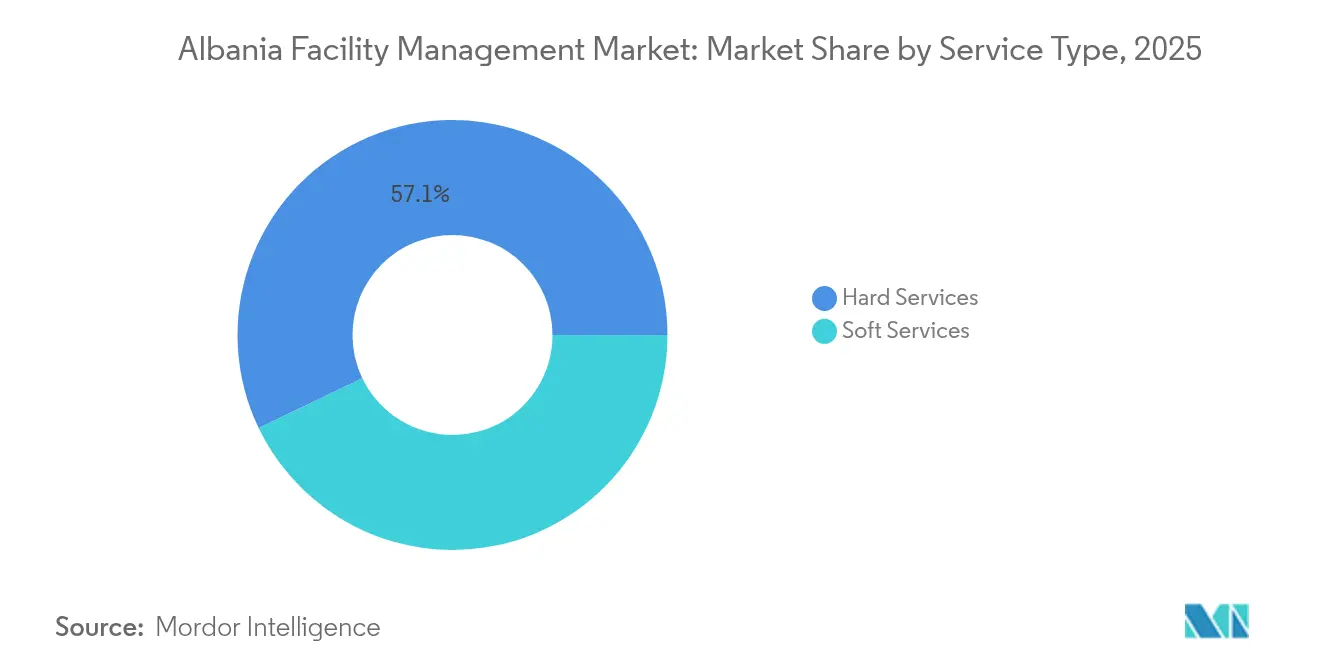

- By service type, hard services led with 57.12% of the Albania facility management market share in 2025.

- By offering type, outsourced models held 64.22% of the Albania facility management market size in 2025 and carry the fastest projected 9.12% CAGR through 2031.

- By end-user industry, commercial facilities accounted for 38.45% of Albania's facility management market share in 2025, while institutional and public infrastructure is set to expand at an 8.55% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Albania Facility Management Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Technological advancements in building management systems | +1.8% | National, with early gains in Tirana, Durrës, Vlorë | Medium term (2-4 years) |

| Growth of the real estate sector | +2.1% | Coastal areas and the Tirana metropolitan region | Short term (≤ 2 years) |

| Increasing emphasis on green-building practices | +1.4% | National, driven by EU compliance requirements | Long term (≥ 4 years) |

| Macroeconomic indicators supporting FM demand | +1.2% | National, with spillover effects to regional centers | Medium term (2-4 years) |

| EU-funded energy-efficiency retrofit programs boosting FM outsourcing | +1.6% | National, prioritizing public buildings and infrastructure | Long term (≥ 4 years) |

| Expansion of flexible workspace and hybrid office models is increasing the FM scope | +0.9% | Urban centers, particularly Tirana and Durrës | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Technological Advancements in Building Management Systems

Albania’s facility owners are embedding smart meters, sensors, and analytics platforms to cut energy losses and extend asset life. National utility OSHEE has deployed 53,000 smart meters, demonstrating that real-time data can reduce technical losses and improve billing accuracy. With mandatory building-energy performance rules taking effect in 2026, automation will shift from an optional upgrade to a baseline compliance requirement. New hotel projects such as Hyatt Regency Tirana are specifying integrated HVAC, lighting, and security controls, raising expectations across the Albanian facility management market. Pilot projects in Tirana schools show that indoor-environment sensors can enhance comfort while lowering energy use. Vendors that pair digital platforms with on-site delivery are positioned to secure multi-year, performance-based contracts throughout the Albania facility management market.

Growth of the Real-Estate Sector

Gross fixed capital formation rose in 2024, feeding a pipeline of mixed-use towers, logistics hubs, and coastal resorts. Landmark developments such as the 50-storey Bond Tower merge retail, office, and hospitality functions, multiplying the service categories required per site. Higher property-tax assessments introduced in 2025 encourage owners to outsource facilities to specialists who can generate measurable cost savings. International investors are therefore accelerating demand for professional oversight, maintaining the upward trajectory of the Albania facility management market.

Increasing Emphasis on Green-Building Practices

Although hydropower accounts for 98% of national electricity, seasonal variability prompts building owners to adopt low-carbon technologies and demand-response software. Public-school retrofits achieved energy-use reductions of 40% when moving toward near-zero-energy standards. EU-aligned codes now require transparent tracking of resource consumption, pushing facilities teams toward integrated waste and energy reporting. EU-supported circular-economy funding of EUR 87 million for solid-waste infrastructure extends facility scopes to recycling optimisation. These regulations and incentives are embedding sustainability into every service contract within the Albanian facility management market.

EU-Funded Energy-Efficiency Retrofit Programmes Boosting FM Outsourcing

The EU accession framework adopted in 2024 unlocked multilateral capital for public-asset refurbishment. Albania’s Energy Efficiency Agency couples retrofit financing with multi-year performance contracts to guarantee savings. A fiscal plan to reduce public debt while raising capital expenditure makes outsourced facilities management attractive for municipalities under budget pressure. Projects such as Community Infrastructure Support in Durrës include long-term FM obligations alongside reconstruction funding. These arrangements push public bodies to rely on specialist operators, broadening the outsourced segment of the Albania facility management market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Labour-market constraints and skills shortage | -1.9% | National, with acute impact in rural areas | Short term (≤ 2 years) |

| Infrastructure gaps and regional disparities | -1.2% | Rural and secondary urban centers | Medium term (2-4 years) |

| Fragmented regulatory compliance is deterring foreign FM entrants | -0.8% | National, affecting international market entry | Long term (≥ 4 years) |

| Limited adoption of digital FM platforms among SME property owners | -0.7% | National, concentrated in smaller municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Labour-Market Constraints and Skills Shortage

Only 60.9% of working-age Albanians hold a job, and many lack certificates in HVAC, automation, or energy management. Emigration drains technical talent, prompting 74% of companies to consider hiring foreign workers. Vocational pathways rarely include predictive-maintenance curricula, and upskilling initiatives will need time to close the gap. Rising wage premiums and recruitment delays place upward price pressure on the Albania facility management market.

Infrastructure Gaps and Regional Disparities

Waste-collection services cover 70% of the population, limiting integrated FM outside main cities. Broadband and digital-payment gaps hinder cloud-based work-order systems in inland municipalities. Road upgrades such as the Building Resilient Bridges programme are improving access, but mountainous terrain maintains high travel times and costs.[2]World Bank Group, “Building Resilient Bridges Program,” worldbank.org Until these disparities narrow, the growth of the Albania facility management market beyond the coastal and capital regions will be gradual.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Hard Services Lead Infrastructure Modernization

Hard services generated USD 275.23 million in 2025, equal to 57.12% of overall revenue in the Albania facility management market. Ageing mechanical, electrical, and plumbing systems require upgrades before the 2026 energy-performance mandate. International hotel brands demand strict uptime and lifecycle cost management, driving adoption of variable-speed drives and high-efficiency chillers. Soft services, though smaller in share, are on track for a 9.35% CAGR as hygiene, workplace wellness, and flexible staffing become standard. Over the forecast horizon, soft services will capture a larger slice of the Albania facility management market, yet capital-intensive hard work will remain essential for code compliance.

Facilities managers increasingly bundle asset management with real-time analytics, moving from scheduled maintenance to predictive models. Cleaning, security, and catering are evolving into experience-oriented offerings, especially in mixed-use towers. This two-speed pattern allows providers to cross-sell, deepening wallet share within the Albania facility management market.

By Offering Type: Outsourcing Dominates Market Evolution

Outsourced contracts represented 64.22% of revenue in 2025 and will advance at a 9.12% CAGR through 2031, the highest growth among delivery models. International hotel chains and mixed-use developers prefer integrated providers that deliver single-invoice accountability. In-house management persists in defence and justice facilities where security protocols demand direct control, yet even ministries are carving out cleaning and landscaping to external specialists. Bundled FM models that exploit volume discounts on energy and consumables are spreading across Grade-A offices. The Albania facility management market is therefore mirroring European practice: owners focus on core real-estate strategy while vendors assume technical risk.

Third-party providers also benefit from a transparent business-registration reform that cuts company formation time to one day, making it easier to enter and scale. Technology platforms that unify work orders, compliance logs, and tenant feedback further cement outsourcing’s comparative advantage.

By End-User Industry: Commercial Leads While Institutional Accelerates

Commercial premises accounted for 38.45% of revenue in 2025, anchored in Tirana’s central business district where Class-A offices and retail destinations cluster. Technology firms and shared-service centres favour long-term agreements that guarantee uptime and cybersecurity-grade access control. Institutional and public infrastructure facilities are the fastest-growing end-user, advancing at an 8.55% CAGR as EU-funded retrofits require lifetime performance monitoring. Education and healthcare upgrades drive infection-control cleaning and IoT-based air-quality checks unfamiliar to traditional custodial teams.

Retail-warehouse hybrids along the Durrës-Vlorë corridor need seasonal staffing, prompting providers to design flexible workforce pools. Industrial facilities in energy and light manufacturing are emerging as growth niches as investors capitalise on competitive labour costs and renewable-energy availability. This diversity reinforces resilience across the Albania facility management market.

Geography Analysis

Tirana generates more than half of the national FM revenue, reflecting its concentration of embassies, mixed-use towers, and Grade-A offices that require 24/7 technical cover. Apartment prices in the capital climbed 16.9% year on year in 2024, incentivising owners to invest in professional upkeep. Integrated contracts featuring energy analytics and tenant-experience apps have become the norm, making Tirana a test bed for advanced services within the Albanian facility management market.

The coastal cities of Durrës, Vlorë, and Sarandë form the fastest-growing cluster as tourist arrivals topped 10 million in 2024. Resorts, marinas, and seasonal retail strips need scalable labour and mobile equipment fleets. Road and tunnel projects are shrinking travel times, enabling Tirana-based operators to run satellite teams along the coast. Seasonal demand fluctuations oblige providers to fine-tune staffing levels, yet opportunities for value-added services remain robust in the Albania facility management market.

Interior regions lag due to sparse infrastructure and smaller property footprints. However, programmes such as Building Resilient Bridges and KfW-backed solid-waste systems inject more than USD 100 million into secondary municipalities. As broadband and e-governance spread, cloud-based FM platforms will allow remote supervision, gradually unlocking efficiencies nationwide.

Competitive Landscape

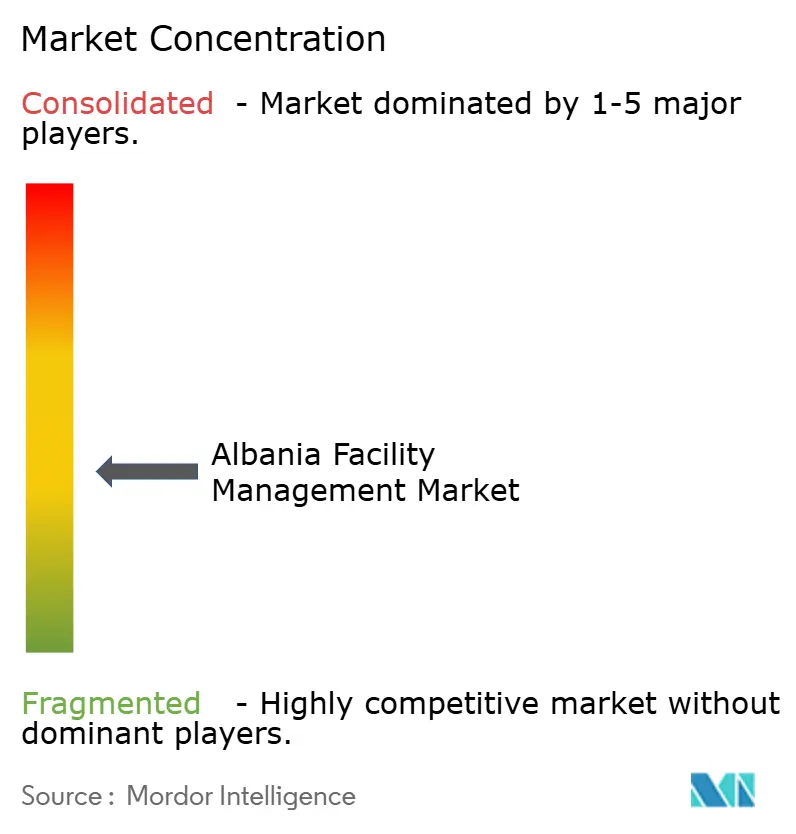

The Albania facility management market features moderate concentration: the five largest providers control a prominent share of revenue. Global firms such as Colliers supply advisory and benchmarking services, often pairing with local licensees for execution. Diversey Holdings offers hygiene chemicals and training, making it a preferred partner for hotels aiming at international cleanliness protocols.

Domestic leader ACREM manages more than 800,000 m² of commercial property and leverages strong local networks to win municipal contracts.[4]ACREM, “Property Services Leadership,” acrem.al BMF Grup is scaling integrated packages that blend robotics, smart-meter analytics, and fire-safety audits, backed by 25 years of MEP expertise. Competitive edge is migrating toward vendors that invest in workforce certification and digital dashboards, prerequisites for EU-funded projects that demand audit-ready records.

Consolidation is expected as single-service firms grapple with rising compliance costs and talent shortages. Strategic alliances that combine foreign technology with local staffing are emerging as the favoured route to national coverage. Providers able to bundle energy-performance guarantees with traditional hard and soft services stand to capture premium margins across the Albania facility management market.

Albania Facility Management Industry Leaders

Globe William International

Mott Mcdonald

Diversey Holdings Ltd

AlbStar Sh.a.

Colliers

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Plans for a USD 1.4 billion resort on Sazan Island advanced, signalling the largest single FM opportunity to date in Albania.

- February 2025: The Economic Reform Programme 2025-2027 is committed to higher capital expenditure while lowering public debt, widening outsourcing prospects for public infrastructure.

- January 2025: Property revaluation started in 14 municipalities, cutting capital-gains tax for sellers from 15% to 5% and boosting transaction volumes that spur follow-on FM demand.

- November 2024: Hyatt confirmed 70% Balkan expansion for its Regency brand, including flagship properties in Tirana and Palase that will need world-class facility operations.

Albania Facility Management Market Report Scope

The Albania facility management market is segmented by service type (hard services [asset management, MEP and HVAC services, fire systems and safety, and other hard FM services] and soft services [office support and security, cleaning services, catering services, and other soft FM services]), offering type (in-house and outsourced [single FM, bundled FM, and integrated FM]), and by end-user (commercial, hospitality, institutional & public infrastructure, healthcare, industrial & process sector, and others). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

By Service Type

| Hard Services | Asset Management |

| MEP and HVAC Services | |

| Fire Systems and Safety | |

| Other Hard FM Services | |

| Soft Services | Office Support and Security |

| Cleaning Services | |

| Catering Services | |

| Other Soft FM Services |

By Offering Type

| In-house | |

| Outsourced | Single FM |

| Bundled FM | |

| Integrated FM |

By End-user Industry

| Commercial (IT and Telecom, Retail and Warehouses, etc.) |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) |

| Institutional and Public Infrastructure (Govt, Education, Transportation) |

| Healthcare (Public and Private Facilities) |

| Industrial and Process (Manufacturing, Energy, Mining) |

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) |

| By Service Type | Hard Services | Asset Management |

| MEP and HVAC Services | ||

| Fire Systems and Safety | ||

| Other Hard FM Services | ||

| Soft Services | Office Support and Security | |

| Cleaning Services | ||

| Catering Services | ||

| Other Soft FM Services | ||

| By Offering Type | In-house | |

| Outsourced | Single FM | |

| Bundled FM | ||

| Integrated FM | ||

| By End-user Industry | Commercial (IT and Telecom, Retail and Warehouses, etc.) | |

| Hospitality (Hotels, Eateries, Large-scale Restaurants) | ||

| Institutional and Public Infrastructure (Govt, Education, Transportation) | ||

| Healthcare (Public and Private Facilities) | ||

| Industrial and Process (Manufacturing, Energy, Mining) | ||

| Other End-user Industries (Multi-housing, Entertainment, Sports and Leisure) | ||

Key Questions Answered in the Report

What is the current value of the Albania facility management market?

The Albania facility management market size is USD 520.63 million in 2026 and is projected to grow to USD 766.75 million by 2031.

Which service category dominates revenue?

Hard services hold 57.12% of revenue because ageing mechanical, electrical, and plumbing systems require extensive upgrades.

Why is outsourcing expanding faster than in-house delivery?

Outsourced providers offer trained personnel, compliance guarantees, and technology platforms, driving a 9.12% CAGR for outsourced contracts through 2031.

Which end-user segment is advancing most quickly?

Institutional and public infrastructure facilities are growing at an 8.55% CAGR due to EU-funded retrofits that demand lifetime performance monitoring.

How will the 2026 energy-performance mandate affect demand?

Mandatory performance standards will increase uptake of IoT-enabled monitoring, predictive maintenance, and specialist energy-management services across the Albania facility management market.

Where are the highest geographic growth prospects?

The coastal corridor from Durrës to Vlorë is expanding fastest, spurred by tourism projects and infrastructure upgrades that require year-round facility oversight.

Page last updated on: