Agro-Rural Tourism Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

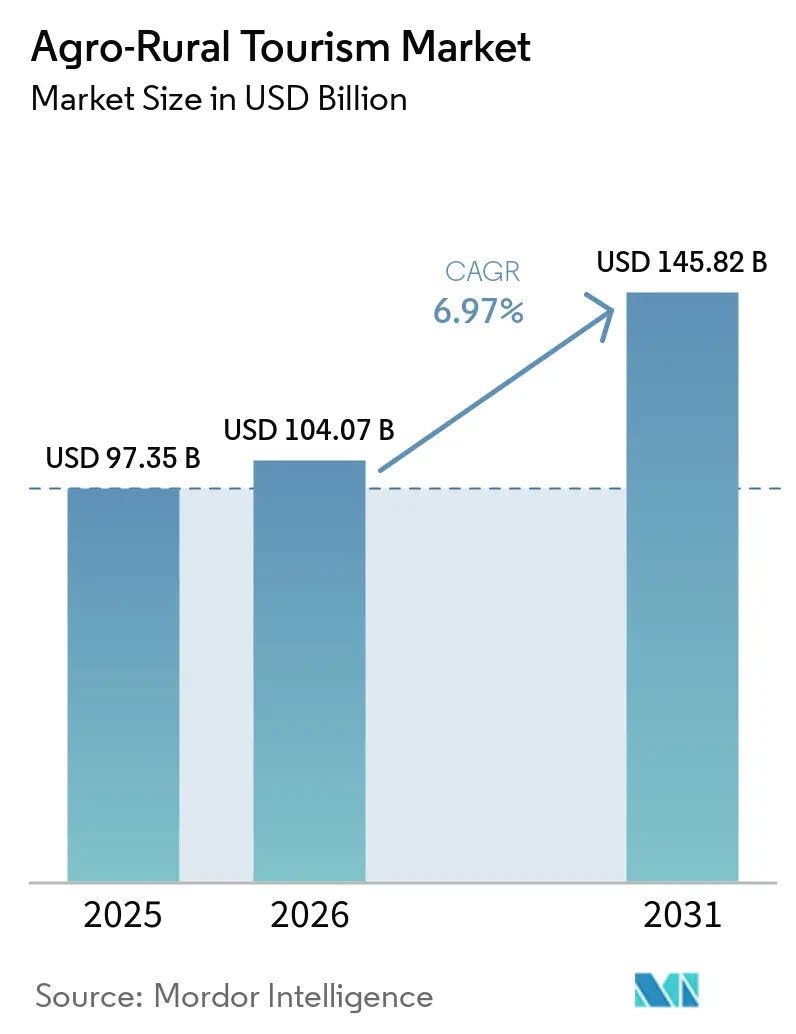

| Market Size (2026) | USD 104.07 Billion |

| Market Size (2031) | USD 145.82 Billion |

| Growth Rate (2026 - 2031) | 6.97% CAGR |

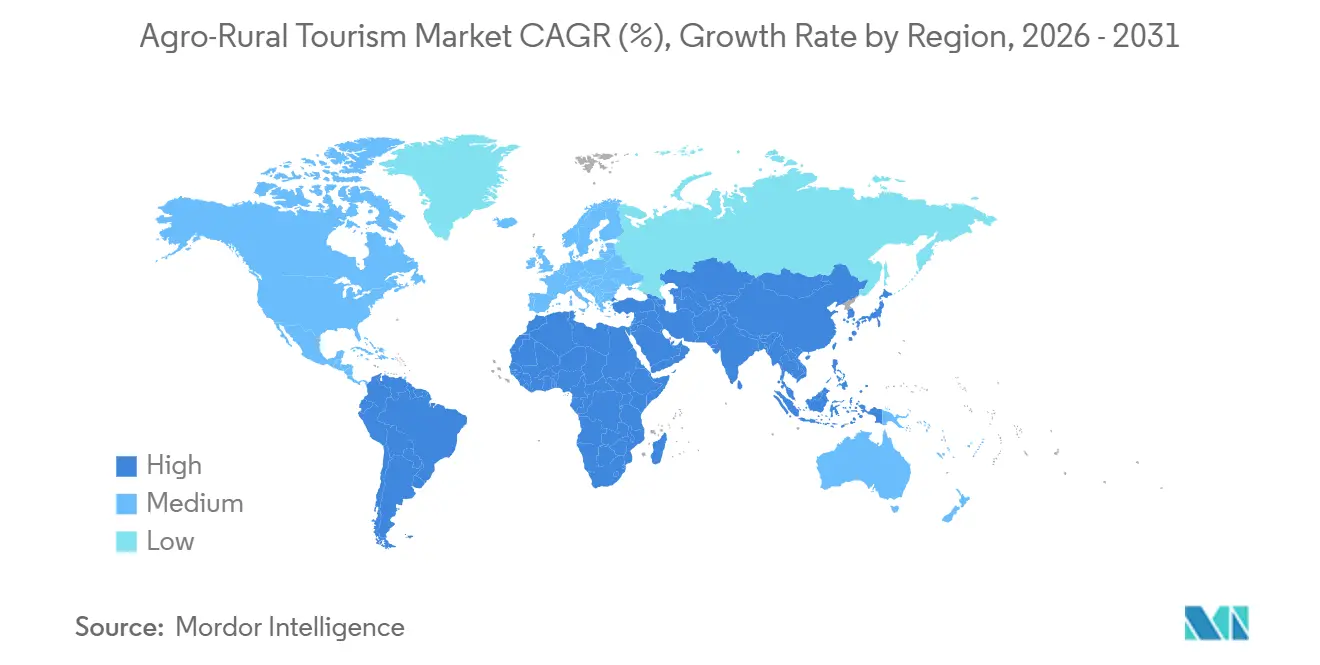

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

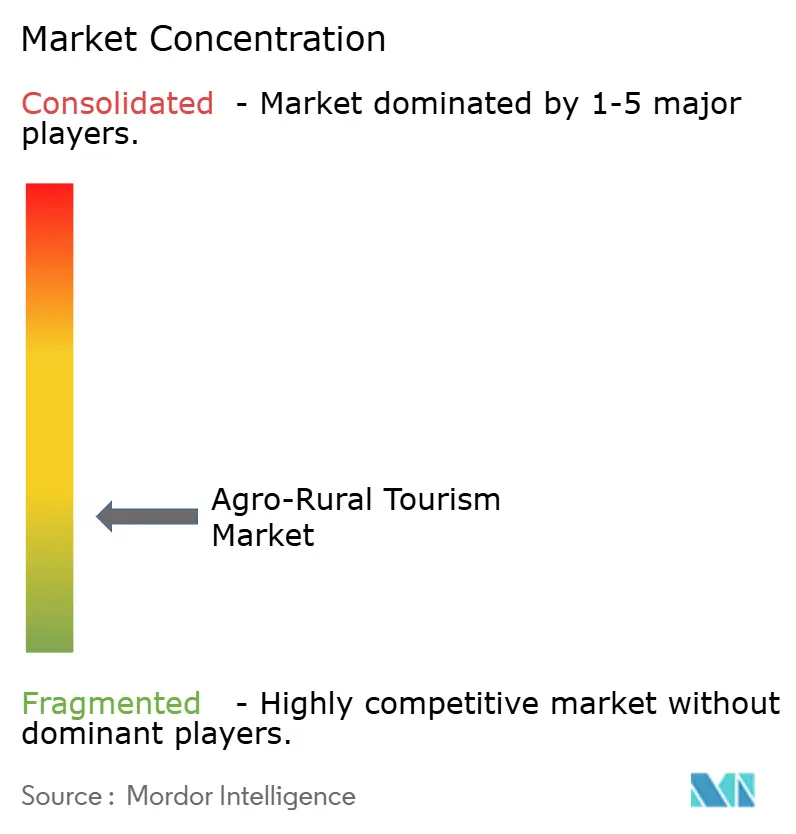

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Agro-Rural Tourism Market Analysis by Mordor Intelligence

The Agro-Rural Tourism Market was valued at USD 97.35 billion in 2025 and is estimated to grow from USD 104.07 billion in 2026 to reach a higher valuation by 2031, at a CAGR of 6.97% during the forecast period (2026–2031). Growth is driven by expanded rural programs in regions like Ireland, Scotland, and India, which are boosting demand for experience-focused rural travel. The shift from suppressed travel levels in 2020-2023 to immersive, farm-centered stays offers farm businesses opportunities to diversify income and manage commodity price fluctuations. Policy frameworks, such as the Philippines' 2026-2031 plan, are strengthening farmer incomes by linking accredited farms with institutional buyers. Digital booking platforms and community discovery channels are improving market access, while enhanced compliance and visitor safety standards in mature regions are fostering trust among families and international travelers, further supporting the market's expansion.

Key Report Takeaways

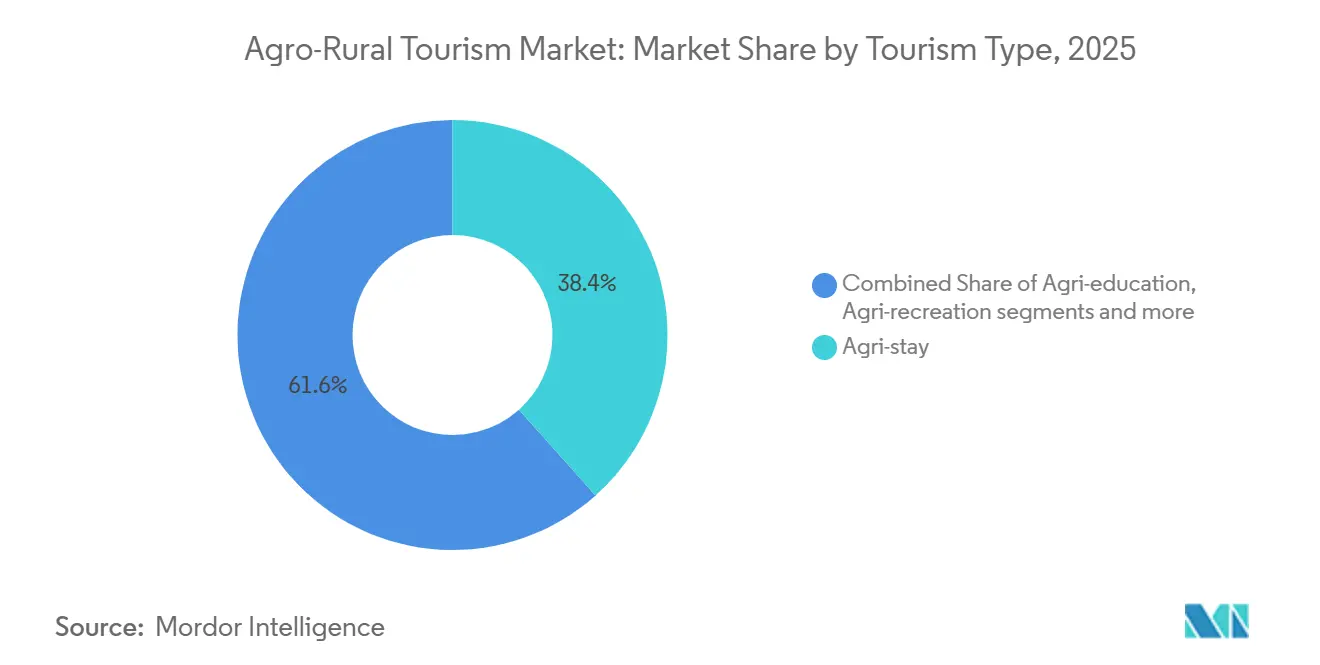

- By tourist type, agri-stay (farm accommodation) held the largest share of the Agro-Rural Tourism market in 2025 at 38.42%, while others (agri-volunteer, agri-wellness, etc.) are projected to post the fastest 2026–2031 growth at an 8.94% CAGR.

- By booking channel, direct bookings (farm website/phone) accounted for 44.15% of the Agro-Rural Tourism market share in 2025, while social-media and community platforms are projected to record the highest growth at a 9.97% CAGR through 2031.

- By travelers type, domestic tourists held the largest share of the Agro-Rural Tourism market in 2025 at 73.65%, and are also projected to grow at a 7.04% CAGR through 2031.

- By revenue source, accommodation accounted for 32.75% of the Agro-Rural Tourism market share in 2025, while retail (farm shop, crafts) is projected to expand at an 8.45% CAGR through 2031.

- By geography, Europe captured 32.50% of the Agro-Rural Tourism market share in 2025, while Asia-Pacific is projected to grow the fastest at an 8.92% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Agro-Rural Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising preference for immersive and experience-led travel | 1.9% | Global, with early concentration in Northern Europe, Japan and the United States coastal states | Medium term (2-4 years) |

| Increasing policy support for rural tourism through government subsidy programs | 1.5% | Asia-Pacific core (India, Philippines, China), spillover to Middle East and Africa (Saudi Arabia, Oman) | Long term (≥ 4 years) |

| Growing need for income diversification among farming communities | 1.3% | North America & European Union (farm income stress zones), expanding to Latin America | Short term (≤ 2 years) |

| Rapid expansion of digital booking platforms for short-duration rural stays | 1.2% | Global, led by North America and Western Europe, accelerating in Asia-Pacific urban corridors | Short term (≤ 2 years) |

| Increasing consumer inclination toward sustainable and carbon-conscious travel experiences | 1.0% | Northern Europe, Scandinavia, Pacific Northwest United States, New Zealand, spill to urban Asia-Pacific | Medium term (2-4 years) |

| Emergence of rural locations as attractive hubs for remote workers and long-stay travelers | 0.9% | Europe (Spain, Portugal, Italy), Asia-Pacific (Indonesia, Thailand), Americas (Mexico, Costa Rica) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising preference for immersive and experience-led travel

Participatory farm experiences that combine education, local food, and nature are gaining popularity, with activities like guided harvests, tastings, and producer workshops drawing families and school groups to accredited farms during peak periods. Structured tastings and educational farm programs have become standard in leading European regions, while Saudi Arabia focuses on hands-on produce picking and farm education to ensure year-round engagement under its national diversification strategy[1]La Voce della Ristorazione, “Agriturismo Italia 2026,” lavocedellaristorazione.it. Public programs are integrating farms into procurement networks for hotels and cruise operators, creating steady demand for accredited sites. To attract remote professionals, operators are offering packages that combine nature, wellness, and flexible work amenities, catering to those seeking quiet rural settings with reliable connectivity for extended stays during off-peak periods[2]Lower Marsh Farm, “Work From Home Away – Escape to Lower Marsh Farm for a Remote Working Retreat,” lowermarshfarm.com.

Increasing policy support for rural tourism through government subsidy programs

Targeted incentives are reducing entry barriers and operating costs for farm-based stays and experiences by supporting rural operators through investment schemes, grants, and subsidies. Programs like Scotland's initiative and sector census highlight increased business numbers, strong visitor turnout, and opportunities for capital inflows beyond traditional accommodation. Ireland promotes agri-food tourism with capped grants for developing tasting rooms, trails, and visitor facilities aligned with national standards. In India, Maharashtra and Arunachal Pradesh combine subsidies, concessional tariffs, and certifications to lower costs while ensuring sustainability and safety. Additionally, infrastructure projects, such as Ireland's Outdoor Recreation Infrastructure Scheme, enhance rural visitor flows by connecting farms to walking and cycling networks.

Growing need for income diversification among farming communities

The adoption of on-farm tourism in North America has increased as producers seek countercyclical revenue streams amid weak commodity cycles and declining farm incomes. Many operators now offer stays, tours, or pick-your-own experiences, repurposing underutilized spaces into cabins, trailers, or event venues to stabilize cash flow and offset rising input costs. In Sri Lanka, farmers show significant interest in agritourism due to unstable incomes and underemployment, aiming to generate additional earnings, create jobs, and engage communities. Gulf projects integrate lodging with value-added processing, allowing producers to capture margins across the value chain. Young entrepreneurs are revitalizing rural areas with guesthouses and farm-centric businesses, fostering ecosystems around nature, food, and culture.

Rapid expansion of digital booking platforms for short-duration rural stays

Farmstay listings in North America are expanding faster than general accommodations in the short-term rental market, driven by discovery tools that highlight unique stays and user-generated reviews emphasizing authentic rural experiences. Aggregators like Harvest Hosts streamline RV and farm-based networks by integrating Escapees RV Club, enhancing campground visibility, and offering members a unified directory of farms, wineries, breweries, and campgrounds under one membership. In Europe, direct sales dominate agritourism, but platforms like Farmtravel.com are growing with multilingual interfaces and tools that centralize traffic while allowing farms to control bookings. In Southeast Asia, digital channels drive agro-experience discovery, though limited coordination among stakeholders hinders structured itinerary development and conversion rates.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inadequate Infrastructure And Accessibility Challenges In Rural Regions | -1.1% | Asia-Pacific, Sub-Saharan Africa, Andean Latin America | Long term (≥ 4 years) |

| Strong Seasonality Impacting Occupancy Rates And Revenue Stability | -0.8% | Europe, temperate North America, Southern Hemisphere Asia-Pacific | Medium term (2-4 years) |

| Stringent Biosecurity And Agricultural Compliance Requirements | -0.6% | Australia, New Zealand, European Union, North America | Short term (≤ 2 years) |

| Persistent Concerns Around Health, Hygiene, And Animal-Human Interaction Risks | -0.5% | Global, with heightened sensitivity in United Kingdom and Canada | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Inadequate infrastructure and accessibility challenges in rural regions

Aging rail and road networks in Europe hinder rural access, as station closures and delayed upgrades reduce mass-transit options to agritourism areas, increasing reliance on private vehicles and limiting inclusive visitation. In India, poor accommodation availability, inadequate road quality, and limited access to electricity and internet are significant barriers, rated as severe by operators, and reducing demand for higher-value international bookings. Sri Lankan surveys show most agritourism sites lack proper roads and visitor facilities, creating a revenue-capital cycle that delays improvements. In the United States, essential infrastructure requirements and the distance to emergency care raise financial and safety challenges for small farms, underscoring the need for clear hygiene and safety measures [3]Vermont Agency of Agriculture, “Ensuring Visitor Safety on Your Farm,” agriculture.vermont.gov.

Strong seasonality impacting occupancy rates and revenue stability

Analyses in Eastern Europe highlight that agritourism growth often leads to significant seasonal fluctuations, increasing pressure on local services during peak months while leaving capacity underutilized in off-peak periods. In Italy, contrasting holiday peaks in spring and winter lows have driven operators to adopt strategies such as off-peak incentives and bundled experiences to boost occupancy beyond weekend surges. In the United States, stabilized park visitation patterns post-pandemic have shifted operator focus to predictable, repeat demand. Studies from Italy and Poland show agritourism contributes minimally to farm income, limiting reinvestment, while year-round regulatory compliance in some United States regions raises fixed costs, tightening margins for small operators[4]National Ag Law Center, “Vermont Agritourism,” nationalaglawcenter.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Tourism Type: Hands-On Experiences Outpace Passive Lodging

The agri-stay (farm accommodation) segment accounted for 38.42% of the Agro-Rural Tourism market, driven by demand for immersive rural lodging experiences that combine accommodation with food, wine, cultural heritage, and educational farm activities. This segment benefits from established rural tourism ecosystems in mature destinations, where farms are integrated into hospitality networks offering structured packages. These packages attract domestic and international travelers seeking short-stay, nature-connected experiences near urban centers. Seasonal travel patterns, weekend tourism flows, and repeat visits tied to festivals, harvest cycles, and curated farm-to-table experiences contribute to high occupancy rates, enhancing revenue stability and reinforcing the segment's leadership.

The "Others" segment, including agri-volunteer programs, agri-wellness retreats, and similar offerings, is projected to grow at a CAGR of 8.94% through 2031. Growth is driven by demand for non-traditional rural engagement formats such as farm volunteering, experiential workshops, yoga retreats, and nature-based therapy activities that emphasize mental well-being and skill-based participation. Consumer preference for meaningful travel experiences encourages farms to diversify offerings, enabling deeper visitor engagement through hands-on agricultural activities such as harvesting, animal care, and sustainable farming education. Wellness-oriented agritourism is gaining popularity as travelers associate rural environments with stress reduction, healthier lifestyles, and digital detox opportunities. Policy support for rural development, integration of farms into local tourism circuits, and collaboration with educational institutions boost weekday demand and utilization rates. Seasonal and event-driven programming enhances revenue concentration, allowing operators to optimize pricing and invest in off-peak innovations. These factors are transforming the agro-rural tourism market into a more experience-driven, diversified, and high-value ecosystem.

By Booking Channel: Social Media Gains While Direct Stays Dominant

Many farm owners prioritize commission-free sales and maintain relationships with repeat guests, leading to direct bookings accounting for 44.15% of transactions in 2025. In Europe, agritourism transactions largely occur directly, though digital discovery driven by local food, wine, and nature experiences is growing, with bookings often made via phone or farm websites. Social media and community platforms are forecast to grow at a 9.97% CAGR through 2031, supported by visual discovery tools and peer networks that highlight authenticity and uncover lesser-known farms. Specialist platforms enable farms to manage reservations independently with listing scalability and white-label tools, avoiding high OTA commissions and preserving profitability. Integrated ecosystems now combine membership options, campground searches, and farm host services, simplifying trip planning and expanding the rural tourism customer base. General OTAs focus on tours and tastings rather than accommodations, leaving room for specialist platforms or direct channels to maintain market share in room bookings and extended-stay packages. Social discovery integrations with RV ownership, route planning, and host networks continue to benefit the agro-rural tourism market, with partnerships enhancing inventory and filtering options like vehicle length and access rules. Traditional agencies curate group itineraries for agricultural education and farm-to-table programs, appealing to international travelers seeking multi-farm routes and consistent standards. A digital divide persists in emerging markets, where limited online presence hinders structured bookings. Over time, unified membership platforms, direct farm booking engines, and niche discovery portals are expected to coexist, emphasizing authenticity and direct relationships while leveraging platform-enabled reach.

By Travelers Type: Domestic Volume, International Growth

Domestic travelers accounted for 44.15% of the Agro-Rural Tourism market in 2025, driven by the convenience of short-haul travel, familiarity with local destinations, and travel patterns aligned with weekends, holidays, and school schedules. This demand is supported by rising interest in nearby nature-based getaways, farm stays, and rural activities offering relaxation without long-distance travel. Factors such as increasing disposable incomes, improved connectivity, and curated rural tourism circuits further sustain participation in both developed and emerging markets. Domestic tourism is projected to grow at a 7.04% CAGR from 2026 to 2031, driven by government-led rural development programs, destination marketing, and infrastructure upgrades that encourage overnight stays. Structured farm experiences, including agricultural workshops, food and wine tastings, and wellness retreats, enhance the appeal of domestic travel. Digital platforms and social media are increasing the visibility of rural destinations, while flexible pricing and localized packages improve affordability. Domestic travelers provide stable, year-round occupancy for agro-rural operators, balancing seasonal fluctuations and supporting rural livelihoods. This segment remains critical in driving growth and fostering resilience within the Agro-Rural Tourism market.

Geography Analysis

Europe is projected to hold the largest regional share at 37.50% in 2025, driven by strong agritourism capacity, diverse food and wine offerings, and sustained domestic and intra-regional travel, which support high seasonal occupancy. Growth is reinforced by expansion of licensed tasting rooms, educational farms, and coordinated rural infrastructure, while Southern Europe and island regions are expanding faster than saturated northern markets, indicating supply rebalancing and destination diversification. Spain’s enotourism model and European Union-supported outdoor infrastructure further enhance rural accessibility and the integration of nature-based travel. Asia-Pacific is the fastest-growing region with a 10.51% CAGR through 2031, supported by policy-led rural tourism integration, subsidy programs, and structured farm tourism development in China, India, the Philippines, and Vietnam, where accreditation systems and supply-chain linkages are improving standards. North America shows a hybrid structure of fragmented operators and consolidating digital platforms, supported by state-level funding and RV-based membership ecosystems. The Middle East is developing integrated agritourism hubs combining farms, hospitality, and retail, while South Africa is expanding visibility through national platforms. Across regions, growth is shaped by safety standards, sustainability expectations, and digital discovery systems. The competitive landscape remains fragmented at operator level, while platforms increasingly consolidate discovery and bookings. Opportunities are emerging in underserved rural areas, digital coliving models, and midweek demand optimization, balancing local ownership with platform-led scalability.

Competitive Landscape

The agro-rural tourism market remains fragmented: the five largest brands collectively command only one-fourth of revenue, preserving a low consolidation barrier while encouraging hyper-local differentiation. Harvest Hosts leads platform-centric solutions, attracting RV travelers via subscription benefits and exclusive farm parking. Farm Stay United States and Farm Stay United Kingdom operate curated directories that vet quality and provide joint marketing campaigns for small holdings that lack individual advertising budgets. WWOOF International coordinates volunteer labor exchanges across 130 nations, leveraging non-cash value propositions to expand global reach. Agritours Canada packages multi-farm circuits geared toward international visitors, highlighting maple forests in Quebec and wheat fields in Saskatchewan.

Competition centers on authenticity, technological ease, and regulatory knowledge. Farms integrating user-friendly booking engines and live-chat support reduce friction, boosting conversions. Location-based AR games, evidenced by ScienceDirect research, raise visitor dwell time and average spend as travelers hunt virtual rewards among real crops. Operators with strong community ties secure local produce supply chains, ensuring food freshness and authenticity. Marketing collaborations with nearby microbreweries or cheesemakers produce bundled itineraries that leverage multi-brand storytelling. Large hospitality groups cautiously explore the space through minority stakes in established farm networks, suggesting a future where hybrid models combine corporate efficiencies with farm authenticity.

Strategic moves highlight a tilt toward data-centric expansion. Harvest Hosts’ July 2024 acquisition of Escapees RV Club unlocked a synergistic community and enriched data pools, enabling targeted promotions based on route histories. Regional tourism boards invest in capacity-building workshops to level technological competencies across operators, recognizing that digital literacy directly influences visitor satisfaction. Insurance firms craft bespoke policies for agri-tourism, using telematics to price risk dynamically based on event calendars and livestock density. Over the medium term, analytics-driven yield management may become a norm, allowing farms to adjust package prices based on weather forecasts and social-media sentiment.

Early movers in the inventory aggregation space, be it by region or theme, stand poised to forge robust and defensible brands. Yet, the scalability of these uniform models grapples with challenges posed by hyper-local heritage and linguistic diversity. The most adept aggregators honor local autonomy, offering communal resources such as marketing, booking platforms, and training, instead of imposing a stringent branding. This federated strategy resonates with travelers’ desires for genuine and diverse experiences, guaranteeing that growth amplifies, rather than diminishes, the distinct allure of the agro-rural tourism market.

Agro-Rural Tourism Industry Leaders

Feather Down Farms

Harvest Hosts

Farm Stay USA

WWOOF International

Farm Stay UK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Scotland’s Agritourism Growth Tracker reported USD 395.15 million (GBP 292.9 million) in sector value, 2.5 million visitors, and about 8,000 full-time equivalent jobs as of 2025, alongside a USD 1.34 million (GBP 1 million) investment scheme and plans to host the Global Agritourism Conference in Aberdeen.

- February 2026: The Philippines launched the Farm Tourism Strategic Action Plan 2026-2031 that expands accreditation, links farm sites to tourism circuits, and aligns enterprise development and market access with farmer income outcomes.

- July 2025: Omran Group detailed progress on Janaen Salalah, an agritourism project with an Integrated Tourism Complex license that allows foreign ownership and includes processing, education, recreation, and hospitality components aligned with Vision 2040.

- June 2025: Harvest Hosts and RV Trader announced a strategic partnership that connects RV specifications with compatible campsites and host locations, adding filters for length and hookups to unify planning, purchase, and trip execution across platforms.

Global Agro-Rural Tourism Market Report Scope

The scope of the Agro‑Rural Tourism Market covers all tourism activities centered on farm‑based stays, rural experiences, and countryside cultural engagement, including accommodation, recreation, education, events, wellness, and on‑farm retail. The study defines the market as tourism occurring within working farms and rural communities, excluding urban hospitality and non‑agricultural adventure tourism. It analyzes global market size, forecasts, drivers, restraints, regulations, technology trends, and competitive dynamics across tourism types, booking channels, traveler categories, revenue streams, and regions, providing a comprehensive view of growth patterns and structural opportunities within rural tourism ecosystems.

| Agri-stay (farm accommodation) |

| Agri-education (classes & tours) |

| Agri-recreation (outdoor activities) |

| Agri-events & festivals |

| Others (Agri-volunteer (WWOOF, farm work) Agri-wellness (yoga retreats, nature therapy)) |

| Direct (farm website / phone) |

| Online Travel Agencies (OTAs) |

| Traditional Travel Agencies |

| Social-media / community platforms |

| Domestic Tourists |

| International Tourists |

| Accommodation |

| Activities & Experiences |

| Food & Beverage |

| Retail (farm shop, crafts) |

| North America | Canada |

| United States | |

| Mexico | |

| South America | Brazil |

| Peru | |

| Chile | |

| Argentina | |

| Rest of South America | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| BENELUX | |

| NORDICS | |

| Rest of Europe | |

| Asia-Pacific | India |

| China | |

| Japan | |

| Australia | |

| South Korea | |

| South-East Asia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Tourism Type | Agri-stay (farm accommodation) | |

| Agri-education (classes & tours) | ||

| Agri-recreation (outdoor activities) | ||

| Agri-events & festivals | ||

| Others (Agri-volunteer (WWOOF, farm work) Agri-wellness (yoga retreats, nature therapy)) | ||

| By Booking Channel | Direct (farm website / phone) | |

| Online Travel Agencies (OTAs) | ||

| Traditional Travel Agencies | ||

| Social-media / community platforms | ||

| By Travelers Type | Domestic Tourists | |

| International Tourists | ||

| By Revenue Source | Accommodation | |

| Activities & Experiences | ||

| Food & Beverage | ||

| Retail (farm shop, crafts) | ||

| By Geography | North America | Canada |

| United States | ||

| Mexico | ||

| South America | Brazil | |

| Peru | ||

| Chile | ||

| Argentina | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| BENELUX | ||

| NORDICS | ||

| Rest of Europe | ||

| Asia-Pacific | India | |

| China | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the agro-rural tourism market?

The agro-rural tourism market size is USD 104.07 billion in 2026 and is forecast to reach USD 145.82 billion by 2031 at a 6.97% CAGR over 2026-2031.

Which region leads and which grows fastest in agro-rural tourism through 2031?

Europe leads with 32.50% in 2025, while Asia-Pacific is projected to be the fastest-growing at a 8.92% CAGR through 2031.

Which segments are the largest and the fastest-growing in this space?

Agri-stay leads by tourism type with 38.42% in 2025, while Others (Agri-volunteer, agri-wellness etc) is projected to grow fastest at 8.94% CAGR to 2031.

How are booking channels shifting in agro-rural tourism?

Direct bookings hold a 44.15% share in 2025, and social-media and community platforms are forecast to grow fastest at 9.97% CAGR to 2031.

What is the primary demand mix between domestic and international travelers?

Domestic tourists accounted for 73.65% of arrivals in 2025, also Domestic tourists are projected to grow at a 7.04% CAGR through 2031.

Which revenue streams are scaling fastest for farm operators?

Accommodation accounts for 32.75% of farm income in 2025, and Retail (farm shop, crafts) are growing fastest at an 8.45% CAGR through 2031.

Page last updated on: