Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 4.42 Billion |

| Market Size (2026) | USD 4.91 Billion |

| Market Size (2031) | USD 8.31 Billion |

| Growth Rate (2026 - 2031) | 11.08% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Tourism Market Analysis by Mordor Intelligence

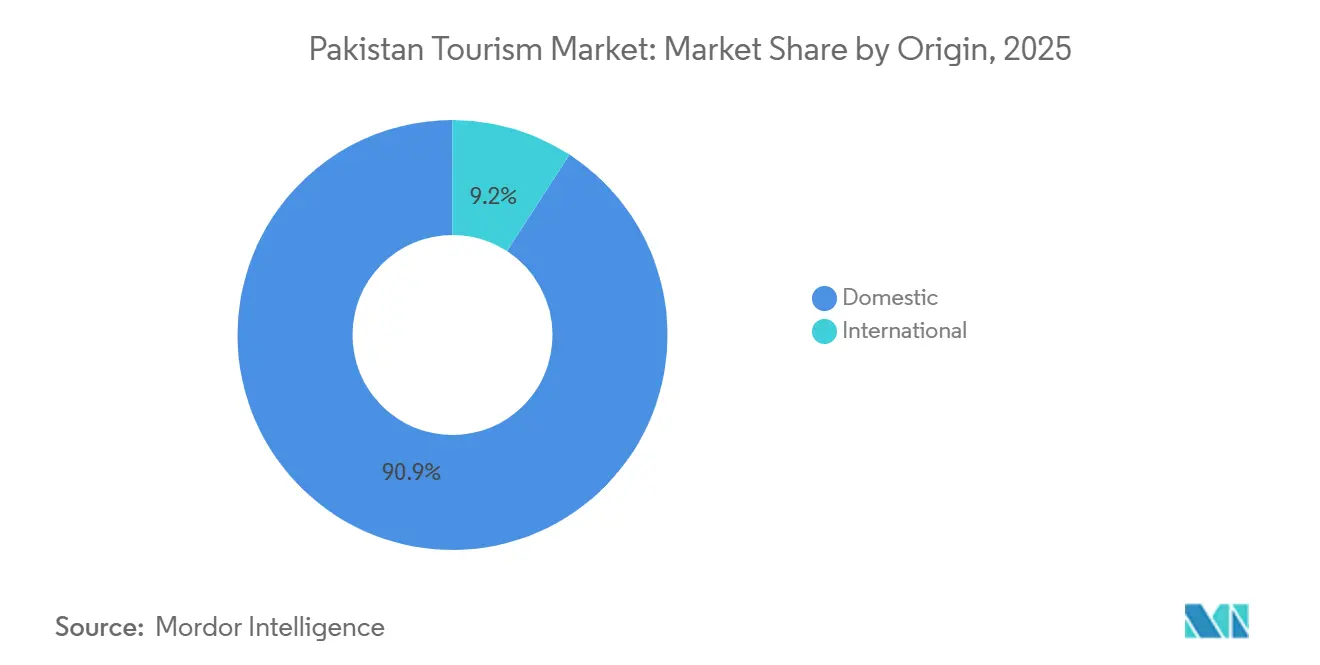

The Pakistan tourism market size is USD 4.91 billion in 2026 and is forecast to reach USD 8.31 billion by 2031 at an 11.08% CAGR, supported by policy actions and infrastructure development that improve accessibility and reduce travel friction. Pakistan's reintroduction of an online visa system for 192 countries has eased entry for leisure, religious, and family travelers, boosting inbound traffic to gateway cities and northern highlands. In February 2026, the federal cabinet restructured the Pakistan Tourism Development Corporation to enhance national branding and coordination. The New Gwadar International Airport, inaugurated in October 2024, and Karakoram Highway upgrades have improved access to Gilgit-Baltistan, enabling multi-destination circuits. A weaker rupee in 2025 increased price competitiveness for dollar-based visitors despite higher costs for local suppliers. Domestic travelers accounted for 90.85% of activity in 2025, while international travel is projected to grow at a 12.05% CAGR through 2031. Expanding tier-1 hotels beyond major cities is essential to reduce capacity constraints and attract higher-yield segments.

Key Report Takeaways

- By origin, domestic travelers held 90.85% of the Pakistan Tourism Market in 2025, while international arrivals are projected to grow at a 12.05% CAGR through 2031.

- By type, Travel Services led with 55.35% of the Pakistan Tourism Market in 2025, while Accommodation Services are expected to expand at a 14.05% CAGR through 2031.

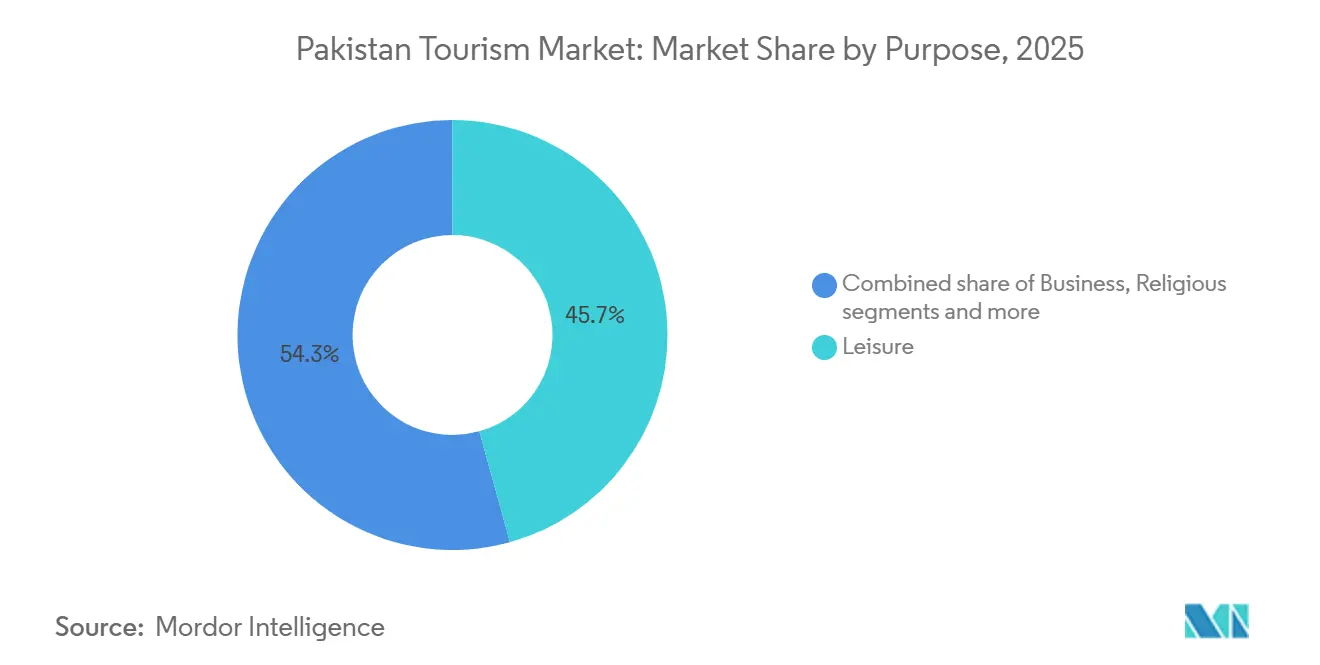

- By purpose, Leisure Travel accounted for 45.70% of the Pakistan Tourism Market in 2025, while MICE is forecast to post the highest growth with a 15.02% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Pakistan Tourism Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inbound travel is rebounding strongly following the rollout of e‑visas | +1.8% | Global, strongest in GCC, UK, North America | Short term (≤ 2 years) |

| A government‑led “Explore Pakistan” branding campaign is elevating the country’s global tourism profile | +1.2% | Global, with early gains in diaspora markets | Medium term (2-4 years) |

| USD 10 billion in CPEC‑linked infrastructure upgrades is transforming connectivity and accessibility | +2.1% | National, concentrated in Gilgit-Baltistan, Balochistan, KP | Long term (≥ 4 years) |

| Outbound trips by the Pakistani diaspora for VFR (visiting friends and relatives) are surging | +1.6% | Global, concentrated in North America, Europe, GCC | Short term (≤ 2 years) |

| Digital booking adoption among Gen‑Z travelers is accelerating market penetration | +1.4% | National, urban centers Karachi, Lahore, Islamabad | Medium term (2-4 years) |

| Opening of previously restricted valleys is fueling growth in adventure tourism | +0.9% | National, Gilgit-Baltistan, Hunza, Swat, Chitral | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inbound travel is rebounding strongly following the rollout of e‑visas

Pakistan expanded its online visa services to 192 countries, simplifying travel planning for leisure and religious tourists and reducing uncertainties that previously hindered short-notice trips. The shift to a unified digital platform with clear categories and eligibility eased documentation for tour operators, benefiting the tourism market reliant on consistent entry rules during peak seasons. Sikh pilgrim visits to holy sites increased significantly in late 2024 and early 2025, reflecting steady demand beyond summer. Improved visa processes attract both returning diaspora and first-time visitors, enabling new offerings like family heritage tours in Punjab and faith-based city trips in Lahore and Nankana Sahib. Government mobility initiatives and Gulf hub airline schedules boost multi-country itineraries, helping Pakistan capture longer stays and higher spending per trip[1]Travel Buddy, “Pakistan Online Visa Expansion for 192 Countries & Tourism Investment,” Travel Buddy, travel-buddy.ai.

A government‑led “Explore Pakistan” branding campaign is elevating the country’s global tourism profile

The federal government repositioned the Pakistan Tourism Development Corporation (PTDC) to focus on policy support and national tourism branding, aiming to unify messaging across heritage, adventure, and faith tourism. The Pakistan tourism market benefits from directives prioritizing climate-conscious infrastructure and hotel upgrades in northern regions where demand exceeds capacity. PTDC operates a multilingual portal that catalogs attractions, offers travel guidance, and helps diaspora travelers plan trips combining family time with cultural and mountain excursions. The National Tourism Coordination Board and public entities organize efforts into themes like branding, adventure tourism, religious tourism, and investment facilitation, converting them into products and events. Partnerships with consumer tech brands enhance digital storytelling, reshaping Pakistan’s image for younger global audiences and increasing travel interest in key diaspora markets[2]Lahore Chamber of Commerce & Industry (LCCI), “Govt Approves PTDC Restructuring Plan to Boost Tourism Branding,” LCCI, lcci.pk.

USD 10 billion in CPEC‑linked infrastructure upgrades is transforming connectivity and accessibility

Airport and highway upgrades under the China-Pakistan Economic Corridor are reshaping access patterns. The New Gwadar International Airport is expected to open in October 2024, while ongoing work on the Karakoram Highway is improving coastal and northern routes. The Dassu-Sazin section of the highway, set for completion by 2026, will reduce travel times to Gilgit-Baltistan, enabling multi-stop tourism circuits with reliable logistics. Rail modernization through ML-1 aims to enhance connectivity along the Karachi-Peshawar corridor, supporting business travel and group tours once implementation begins. The first phase of CPEC projects established credibility in energy and transport, while the second phase focuses on industrial and human capital, benefiting tourism services, employment, and training. These developments are unlocking previously inaccessible destinations, diversifying visitor activities, and integrating local communities into digital homestay and guiding platforms[3]CPEC Info, “China to Invest Up to $10bn in Pakistan as New Deals Signal Surge in FDI,” CPEC Info, cpecinfo.com.

Digital booking adoption among Gen‑Z travelers is accelerating market penetration

Mobile wallets saw strong adoption by mid-2025, while e-commerce spending on travel apps grew steadily. This shift highlights a preference for mobile-first discovery, ticketing, and last-minute changes, catering to domestic multi-city trips and flexible weekend getaways. Hotels integrating real-time inventory with online channels achieved higher occupancy and improved yield management, emphasizing digital capabilities as key performance drivers in Pakistan's tourism market. A Lahore study revealed strong interest in travel apps combining maps, bookings, and navigation, supporting efforts to consolidate services into a single mobile interface. Provincial sales tax incentives for digital payments, including card and wallet transactions, reduced tax rates, and encouraged traceable, cashless operations. The Federal Board of Revenue’s real-time reporting and digital invoice mandates formalized online transactions, improving data visibility and control for businesses scaling in Pakistan's tourism market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility of the currency against the USD is pushing package prices higher | -1.9% | National, with spillover to international operator margins | Short term (≤ 2 years) |

| Security concerns in certain provinces are discouraging tourist confidence | -1.2% | National, primarily Balochistan, southern KP | Medium term (2-4 years) |

| Insufficient Tier‑1 hotel capacity outside major metro hubs is limiting accommodation options | -0.8% | National, multi-destination tour circuits affected | Medium term (2-4 years) |

| A complicated tax framework on tourism services is increasing compliance burdens | -0.6% | National, provincial variation creates compliance costs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatility of the currency against the USD is pushing package prices higher

An exchange rate shock from 2024 to 2025 increased local-currency costs for imported fuel, fittings, and food items, raising operating expenses and prompting quarterly supplier renegotiations, especially for smaller operators with limited hedging options. By 2025, foreign exchange reserves improved, and inflation eased from 2024 peaks, though service imports, including travel-related items, rose in early FY2025, limiting short-term discounting. The Asian Development Bank reported inflation moderation and rupee stabilization in 2025, aiding planning for Pakistan's tourism market in 2026. An October 2025 agreement between the IFC and the State Bank improved currency risk management in local lending, supporting capital expenditures during exchange-rate stress. A weaker rupee increased purchasing power for inbound visitors spending in hard currency, partially offsetting forex challenges for suppliers and operators in the tourism sector.

Security concerns in certain provinces are discouraging tourist confidence

Travel advisories restricting non-essential travel in parts of Balochistan and southern Khyber Pakhtunkhwa limit the audience for leisure products, pushing operators to focus on safer corridors. Northern areas report increased mountaineering interest but face road-safety issues due to infrastructure gaps, emphasizing the need for guardrails, roadside outposts, and reliable cellular coverage. Policymakers highlight tourism’s role in job creation and cultural diplomacy, encouraging safety investments to boost operator confidence in Pakistan's tourism market. Gilgit-Baltistan’s tourism portal provides updated destination details, aiding itinerary planning and adherence to seasonal advisories. Improved infrastructure and faster response times on mountain roads could attract more family travelers and group tours seeking scenic routes with dependable safety measures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Origin: Diaspora Remittances Power Inbound Revival

Domestic tourists accounted for 90.85% of Pakistan's tourism market share in 2025, driven by population size, airfare costs, and visa challenges that favored local trips over international travel. International arrivals are projected to grow at a 12.05% CAGR through 2031, supported by e-visa access and airport upgrades. These changes are expected to attract first-time and repeat diaspora visitors, who often combine family visits with leisure trips. Road improvements, including the Karakoram Highway, enhance connectivity from Islamabad to northern valleys, enabling multi-stop itineraries. Stable Gulf route schedules and group offers align with diaspora travel patterns, strengthening international demand and reducing seasonality in the market.

Domestic travelers remain the primary drivers of occupancy and transport use year-round, while diaspora visitors boost yields during peak holiday periods. Remittance inflows from Saudi Arabia, the United Arab Emirates (UAE), the United Kingdom (UK), and the United States of America (USA) align with diaspora visitor origins and support retail spending during VFR trips. Religious tourism, such as Sikh pilgrimages to Nankana Sahib and the Kartarpur Corridor, provides a counter-seasonal boost, supporting year-round operations. Clear compliance under the FBR framework reduces friction for operators managing mixed clientele. Transparent visa processes and stable routes are expected to increase repeat visits and extend the average stay for inbound travelers balancing family and leisure activities[4]Riaz Haq, “Improved Security and New Infrastructure Boost Pakistan Tourism,” Riaz Haq, riazhaq.com.

By Type: Hotels Chase Capacity Gap as Digital Bookings Surge

Travel Services held 55.35% of Pakistan's tourism market in 2025, driven by airlines, tour operators, and ground handlers shaping demand and itineraries. Accommodation Services are expected to grow at a 14.05% CAGR through 2031, addressing limited tier-1 capacity in Islamabad and northern destinations where peak-season occupancies restrict multi-destination packaging. Islamabad faces a 4,000-room shortfall, with limited five-star hotels meeting nightly demand exceeding 8,000 rooms, creating opportunities for global and regional brands. New properties near Islamabad International Airport and business districts aim to stabilize mid-week occupancies through MICE and corporate demand. Aligning hotel pipelines with airport connectivity and road upgrades is critical for expanding access to secondary destinations.

Airline fleet expansions, including Fly Jinnah’s new aircraft and routes, are increasing seat capacity on domestic and Gulf sectors, supporting leisure and VFR trips. The national carrier’s privatization in December 2025 and fleet expansion plan are expected to enhance competitiveness in trunk and long-haul routes, enabling group rates and hotel partnerships. Online travel agencies are boosting direct-to-consumer planning with localized products and integrated payments, improving pricing transparency. Adoption of property management systems and point-of-sale platforms supports real-time inventory control and revenue management. Lower digital payment tax rates encourage formalization, scaling online channels in Accommodation and Travel Services.

By Purpose: MICE Conference Halls Sprout as VFR Spending Lifts Retail

Leisure Travel accounted for 45.70% of Pakistan's tourism market share in 2025, driven by improved road access and the opening of scenic northern valleys with summer appeal. The MICE segment is projected to grow at a 15.02% CAGR through 2031, supported by large venues in Karachi and new convention infrastructure in Lahore, which stabilizes mid-week demand. Visiting Friends and Relatives trips contribute to retail spending in cities, aided by worker remittances that combine shopping with cultural excursions. The Kartarpur Corridor facilitates daily Sikh pilgrim visits to the Gurdwara Darbar Sahib, ensuring consistent faith-based travel. Airlines and hotels now offer meeting packages paired with short leisure trips, addressing the demand for blended business and leisure travel.

Improved northern road connectivity supports community-based homestays on verified platforms, offering affordable, culturally immersive lodging that complements tier-1 hotels and benefits local suppliers. Domestic and inbound operators promote MICE services at trade shows, capturing events requiring reliable logistics. Streamlined pilgrim visas and faster processing could boost faith-based tourism from nearby markets, stabilizing demand. Rising outbound travel reflects growing digital readiness, which OTAs and airlines can leverage through co-marketing with diaspora communities if entry processes remain smooth. Standardized invoicing and real-time reporting under the FBR regime encourage formal MICE providers to scale, ensuring consistent service delivery in Pakistan's tourism industry.

Geography Analysis

The Karachi, Lahore, and Islamabad triangle holds a significant share of hotel room capacity and serves as the main gateway for trips to northern regions. Improved safety and roadside infrastructure are expected to boost international tourism to northern areas like Gilgit-Baltistan, Hunza, Swat, and Kaghan. CPEC-led roadworks have reduced travel times to mountain destinations, enabling multi-stop itineraries and wider spending distribution. Serena Hotels’ expansions in Hunza and Sost reflect confidence in the northern corridor, with green certification goals supporting sustainable development. The Karakoram Highway alternative section, set for completion by 2026, will enhance access, route reliability, and seasonal operations. Expanded rescue and safety services are likely to attract more family travelers to scenic valleys previously seen as adventure-only destinations.

Khyber Pakhtunkhwa’s Buddhist trail and UNESCO-listed sites add cultural depth to northern itineraries, appealing to Asian markets for study tours and meditation retreats, which help balance demand during off-peak months. Sindh benefits from Karachi Expo Centre’s capacity expansion, driving business and exhibition-related hotel demand. Punjab’s Sikh heritage sites and the Kartarpur Corridor sustain year-round faith-based travel, strengthening the tourism market’s resilience. Coordinated efforts on site maintenance, signage, and digital content can enhance short heritage circuits from Lahore and Faisalabad, combining shrines, museums, and culinary experiences.

Balochistan focuses on coastal and logistics development around Gwadar, with the international airport opening in October 2024 expected to improve access and support gradual tourism growth along the Makran coast. Azad Jammu and Kashmir’s adventure and religious sites could attract more private investment in lifts and lodging as regulatory clarity and road access improve, extending visitor stays. Provincial sales tax differences across Punjab, Sindh, and Khyber Pakhtunkhwa create compliance challenges, but digital payment-linked reductions may lower rates and encourage formal channels. Collaboration between provincial tourism departments and PTDC on standards and content can diversify destinations and reduce pressure on peak-season hotspots.

Competitive Landscape

The Pakistan tourism market is fragmented, with small and mid-sized operators serving domestic travelers outside major metropolitan areas. Hospitality groups and airlines focus on scaling operations to enhance reliability and distribution. Pakistan Services Limited’s 2025 shareholding restructuring provided financial flexibility for investments in new sites, branding, and technology, improving productivity and consistency in high-demand circuits. The privatization of the national carrier in December 2025 initiated fleet expansion and service upgrades, reducing bottlenecks on key routes essential for leisure and MICE (Meetings, Incentives, Conferences, and Exhibitions) travel. Private carriers’ fleet growth and increased frequencies strengthen connectivity, support group travel, and reduce risks for event planners. Northern expansions by hotel brands diversify offerings beyond summer seasons, ensuring year-round cash flows.

Digital differentiation drives growth as online travel agencies localize content, payments, and language to align with consumer preferences, boosting conversion rates for domestic and outbound segments. International hotel chains expand through management and franchise agreements, increasing visibility for mid-scale and upscale properties that balance corporate and leisure demand. Regional brands’ projects cater to diverse positioning and pricing, supporting city-based MICE demand and leisure corridors while reducing seasonality. Developer-led initiatives and branded residences accelerate openings in high-demand submarkets and offer extended stay options for work and family visits.

Technology adoption strengthens operations, with tier-1 hotels using cloud-native property management systems integrated with POS and channel management tools for real-time pricing and allocation. New carriers like Air Karachi aim to fill frequency gaps in domestic and regional routes, enabling dynamic scheduling during peak leisure and VFR (Visiting Friends and Relatives) seasons. Payment innovations, such as Alipay+ integration, expand acceptance in retail and attractions, supporting Asian visitor segments and integrating SMEs into the digital economy. Homestay platforms in iconic valleys offer culturally immersive alternatives, easing pressure on tier-1 hotels during peak months. Compliance with tax and invoicing regulations supports formal growth and reduces risks for multi-province operators.

Pakistan Tourism Industry Leaders

Pakistan International Airlines (PIA)

Airblue

SereneAir

Hashoo Group (Pearl-Continental & Marriott Pakistan)

Serena Hotels

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: The Cabinet Committee on State-Owned Enterprises approved restructuring PTDC to establish a focused center of excellence for policy support, coordination, and national tourism branding.

- February 2026: Shiji Group implemented its cloud-native Daylight PMS at Pearl Continental Hotel Rawalpindi, marking the first deployment of its kind in Pakistan. The hotel plans to adopt Infrasys POS next for its food and beverage operations.

- February 2026: The National Highway Authority awarded a contract under its Road Maintenance Account to upgrade the Dassu-Sazin section of the KKH. This project aims to improve safety, reduce travel time on N-35, and strengthen connectivity between Pakistan and China.

- January 2026: Pakistan has extended its online visa services to 192 countries, enhancing tourism and investment opportunities by simplifying the e-visa process for international visitors.

Pakistan Tourism Market Report Scope

Pakistan's tourism industry includes inbound, outbound, and domestic travel, along with accommodation and hospitality services nationwide. The market is segmented by origin (domestic, international), type (accommodation, travel services), and purpose (leisure, business, VFR, religious, MICE, other travel). The report highlights drivers like e-visas, branding campaigns, CPEC infrastructure, diaspora VFR trips, Gen-Z digital bookings, and adventure tourism growth. Restraints include currency volatility, security issues, limited Tier-1 hotel capacity, and complex tax systems. It examines regulations, technology, supply chains, and competition using Porter’s Five Forces. The study provides market size forecasts (USD), company profiles, strategies, and opportunities like ecotourism and digital tourist-card systems.

By Origin

| Domestic |

| International |

By Type

| Accommodation Services |

| Travel Services |

By Purpose

| Leisure |

| Business |

| Visiting Friends & Relatives (VFR) |

| Religious |

| Meetings-Incentives-Conferences-Exhibitions (MICE) |

| Other Purposes |

| By Origin | Domestic |

| International | |

| By Type | Accommodation Services |

| Travel Services | |

| By Purpose | Leisure |

| Business | |

| Visiting Friends & Relatives (VFR) | |

| Religious | |

| Meetings-Incentives-Conferences-Exhibitions (MICE) | |

| Other Purposes |

Key Questions Answered in the Report

What is the current size and growth outlook for the Pakistan tourism market?

The Pakistan tourism market size is USD 4.91 billion in 2026 and is forecast to reach USD 8.31 billion by 2031 at an 11.08% CAGR, supported by visa facilitation and corridor-driven infrastructure upgrades.

Which segments lead demand and which are growing fastest in Pakistan’s tourism?

Travel Services led with 55.35% share in 2025, while Accommodation Services are projected to grow fastest at 14.05% CAGR to 2031, and MICE is the fastest-growing purpose segment at 15.02% CAGR.

How will the e-visa changes affect inbound travel to Pakistan?

The 2026 expansion of the online visa system to 192 countries lowers entry barriers and improves planning certainty, which supports more inbound trips and higher conversion among diaspora and first-time visitors.

What regions in Pakistan are set to benefit most from tourism over the next few years?

Northern areas, including Gilgit-Baltistan, Hunza, Swat, and Kaghan, should gain from shorter travel times along the Karakoram Highway and new hotel openings that make multi-stop itineraries more practical.

How is the competitive landscape evolving in Pakistan’s tourism?

The market remains fragmented, yet privatization of the national carrier, new entrants like Air Karachi, and cloud-native hotel technology deployments signal a shift toward scale, reliability, and digital integration.

What are the top risks to watch in Pakistan’s tourism over 2026–2031?

Currency volatility and lingering travel advisories in select provinces are key risks, while hotel capacity gaps outside major metros and compliance complexity add operational pressure for multi-region operators.

Page last updated on: