Ethiopia Agriculture Market Analysis by Mordor Intelligence

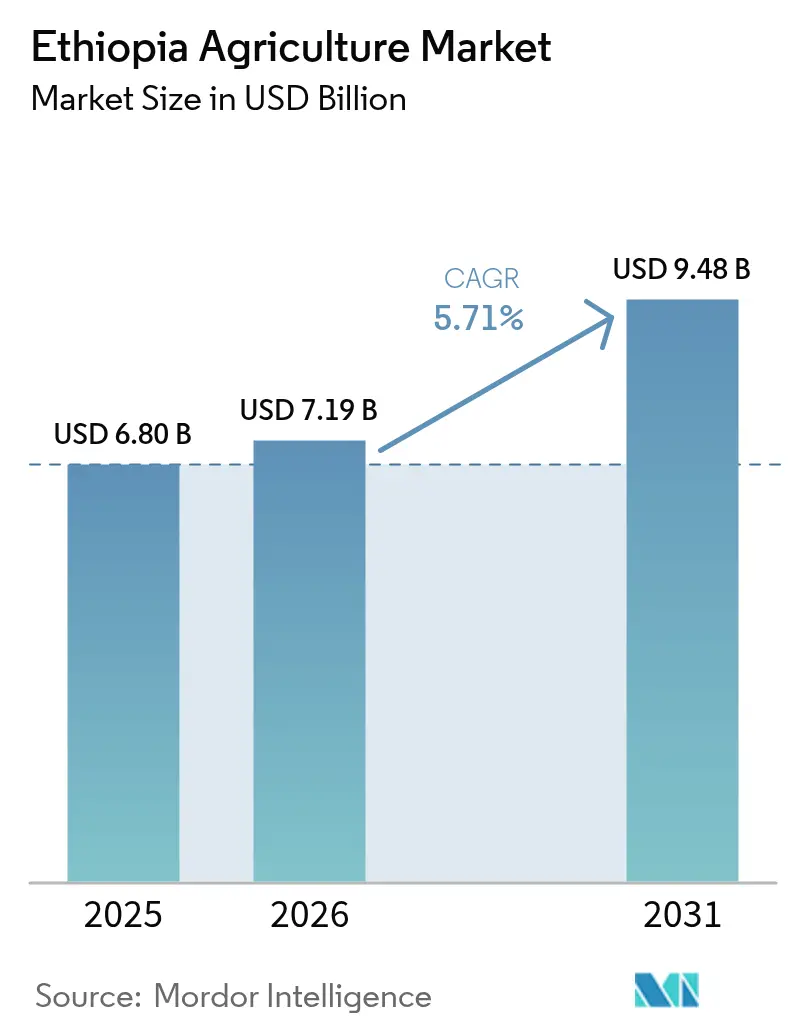

The Ethiopia agriculture market size was valued at USD 6.80 billion in 2025 and estimated to grow from USD 7.19 billion in 2026 to reach USD 9.48 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031). Rising cereal demand from a population expanding at 2.5% annually, swift irrigation buildouts in lowland belts, and duty-free Gulf access for fresh produce are combining to accelerate revenue growth. Fertilizers still account for the largest slice of spending, yet mechanization programs are closing the equipment gap by subsidizing tractor leases and combine harvesters. Digital trading on the Ethiopian Commodity Exchange is compressing bid-ask spreads, lifting farm-gate returns and injecting transparency into the Ethiopia agriculture market. Government-led soil fertility and seed-multiplication initiatives, together with solar-powered cold-storage deployment, are beginning to ease the twin constraints of nutrient exhaustion and post-harvest spoilage.

Key Report Takeaways

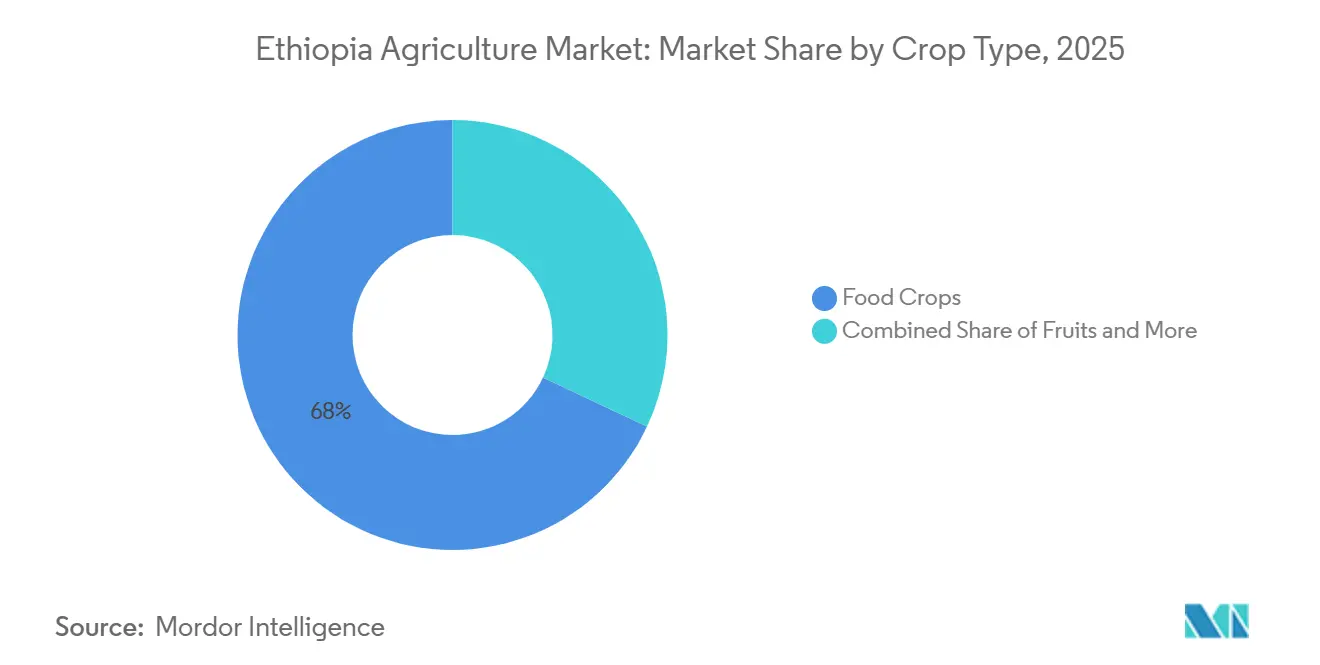

- By crop type, food crops were the largest segment, holding 68% of the Ethiopia agriculture market share in 2025, while fruits are the fastest-growing segment, forecast to record a 9.2% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Ethiopia Agriculture Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising domestic demand for staple cereals | +2.4% | National, with acute pressure in urban centers and deficit zones in Tigray, Afar | Short term (≤2 years) |

| Expanding irrigation infrastructure projects | +1.8% | Somali, Afar, lowland Southern Nations, Nationalities, and Peoples (SNNP), and eastern Oromia | Medium term (2-4 years) |

| The government and donors focus on the agriculture corridors | +1.5% | National, with early gains in Southern Nations, Nationalities, and Peoples (SNNP), Oromia, and Amhara corridor zones | Long term (≥4 years) |

| Digitalization of Ethiopian commodity exchange | +1.1% | National, with the highest adoption in Oromia, Amhara, and Southern Nations, Nationalities, and Peoples (SNNP) coffee and grain zones | Medium term (2-4 years) |

| Solar-powered cold-storage micro-grids in rural hubs | +0.9% | Southern Nations, Nationalities, and Peoples (SNNP), Oromia, and Amhara horticulture zones | Medium term (2-4 years) |

| New agro-export protocols with Saudi Arabia and the United Arab Emirates | +1.0% | National, with a concentration in the Southern Nations, Nationalities, and Peoples (SNNP) fruit zones and the Somali livestock areas | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Domestic Demand for Staple Cereals

Population growth, urbanization, and changing consumption patterns are driving a significant increase in domestic demand for staple cereals such as teff, maize, and wheat in Ethiopia. With a population exceeding 120 million, ensuring food security remains a national priority, leading to efforts to expand cultivation and improve productivity. Urban centers such as Addis Ababa and other regional cities are experiencing stronger demand, encouraging farmers to intensify cereal production. This growing demand is driving the adoption of agricultural inputs, such as fertilizers and improved seeds, and prompting government interventions to address yield gaps. Cereal consumption is outpacing production. In 2024, Ethiopia's total wheat grain equivalent imports reached 1.7 million metric tons, an increase of nearly 80% from 2023, according to the United States Department of Agriculture[1]Source: USDA Foreign Agricultural Service, “Grain and Feed Annual – Ethiopia,” usda.gov.

Expanding Irrigation Infrastructure Projects

Irrigation expansion is transforming Ethiopia's traditionally rain-fed agricultural system into a more resilient and sustainable production model. Investments in small- and medium-scale irrigation in regions such as Afar, Somali, and eastern Oromia are mitigating the impacts of erratic rainfall and drought cycles. Irrigation facilitates increased cropping intensity, enables multiple annual harvests, and supports the cultivation of high-value crops such as horticulture and cotton. Transitioning from rain-fed agriculture to controlled irrigation reduces climate-related risks and stabilizes multi-season planting. Smallholder irrigation schemes demonstrate notable technical efficiency, highlighting opportunities for improved water management and increased private sector involvement. The spatial expansion of irrigation remains the largest physical investment driver in Ethiopia agriculture market.

Government and Donor Focus on Agriculture Corridors

Strategic agricultural corridor development focuses on enhancing productivity, logistics, and market access in high-potential areas within Oromia, Amhara, and Southern Nations, Nationalities, and Peoples (SNNP). Investments in these corridors integrate extension services, infrastructure, and agro-processing facilities to minimize post-harvest losses and promote commercialization. This strategy strengthens value chains and improves farm-gate price realization. Cluster farming has doubled yields when combined with mechanical plowing, highlighting the economic benefits of adopting machinery. Smallholder access to equipment remains a challenge. Government initiatives, such as import tax waivers and concessional loans, are supporting scalability. Increased mechanization improves harvested-area efficiency, contributing to higher output in Ethiopia agricultural market.

New Agro-Export Protocols with Saudi Arabia and United Arab Emirates

Bilateral trade agreements and phytosanitary protocols with Gulf countries are creating new export opportunities for Ethiopian livestock and horticulture. Enhanced export compliance mechanisms are improving market access and increasing foreign exchange earnings. The Somali region and Southern Nations, Nationalities, and Peoples (SNNP) fruit zones are notably benefiting from stronger trade ties with Gulf nations. In 2024, Ethiopia secured duty-free market access for fruits, vegetables, and livestock products to Saudi Arabia and the United Arab Emirates, unlocking export opportunities valued at USD 180 million annually. This development is diversifying Ethiopia's export base beyond coffee, which constituted 32% of agricultural exports in 2024[2]Source: Ministry of Trade and Regional Integration, “Export Protocols,”mot.gov.et.

Restraints Impact Analysis*

| Restraint | (~) %Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low land productivity and soil degradation | -1.6% | National, most severe in Oromia, Amhara, and Southern Nations, Nationalities, and Peoples (SNNP), continuous cropping zones | Short term (≤2 years) |

| Inadequate access to affordable finance | -1.3% | National, with acute constraints in Somali, Afar, and remote Amhara districts | Medium term (2-4 years) |

| Fall Armyworm outbreaks in highland maize zones | -0.8% | Amhara, Oromia, and Southern Nations, Nationalities, and Peoples (SNNP) highland maize belts | Short term (≤2 years) |

| Fragmented landholdings limit mechanization scale | -0.7% | National, with the highest fragmentation in Amhara and Southern Nations, Nationalities, and Peoples (SNNP) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Low Land Productivity and Soil Degradation

Ethiopia's agricultural productivity faces challenges due to soil erosion, nutrient depletion, and limited fertilizer use. Continuous cropping without sufficient nutrient replenishment has led to a decline in soil organic carbon levels, particularly in key production regions such as Oromia and Amhara. This has resulted in reduced yields per hectare and constrained income growth. According to FAOSTAT, average cereal yields were 2.6 metric tons per hectare in 2024, a decrease from 2.7 metric tons per hectare in 2025, with cropland experiencing significant nutrient loss[3]Source: Food and Agriculture Organization, “FAOSTAT – Crops and Livestock Products,” fao.org. Soil acidity and erosion in the highlands further degrade nutrient availability, while limited adoption of liming practices exacerbates fertility issues. Although the Green Legacy Initiative has planted billions of tree seedlings to enhance soil structure, the implementation of conservation agriculture remains inconsistent.

Inadequate Access to Affordable Finance

Smallholder farmers encounter credit constraints due to high collateral demands and the limited reach of rural banking services. The lack of affordable financing prevents these farmers from investing in essential resources such as irrigation systems, mechanization, and improved seeds, thereby hindering modernization and productivity growth. Additionally, the concentration of credit among a small group of borrowers worsens the issue, as large enterprises dominate loan allocations, leaving smallholder farmers with restricted access to formal financial services. While digital wallets such as Telebirr cater to numerous subscribers and have the potential to facilitate microloans, their integration with formal banking systems remains limited. This scarcity of capital impedes the adoption of mechanization and irrigation, constraining the growth of the Ethiopian agriculture market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Crop Type: Food Crops Anchor Market Stability

Food crops were largest segment, held 68% of the Ethiopia agriculture market share in 2025. Cereals such as teff, wheat, maize, and sorghum occupy a significant portion of cultivated land in Ethiopia, reflecting their importance to the country's food security and rural livelihoods. Pulses, including chickpeas, lentils, and faba beans, also contribute substantially to crop value. Maize, Ethiopia's highest-yielding cereal nationwide, is expanding in lowland areas through irrigation. Sorghum and millet remain essential in the Somali and Afar regions, where their drought tolerance is prioritized over yield potential. Pulses, particularly chickpeas and kidney beans, are primarily exported to India, Pakistan, and Turkey. Growth in this segment is constrained by volatile international prices and quality-related disputes.

Fruits are fastest growing segment, forecast to record 9.2% CAGR through 2031, shifting the Ethiopia agriculture market share toward high-value horticulture. Avocado are among the fastest-growing exported fruits, particularly from the Oromia region, one of Ethiopia's largest agricultural areas. Shipments are primarily directed to Europe and the Middle East. Strawberries and other fresh fruits have been exported to markets such as Saudi Arabia, reflecting activity beyond traditional regional markets. Traditional fruits, including bananas, mangoes, citrus fruits (oranges and lemons), papayas, guavas, and avocados, are extensively cultivated and serve as the foundation for both local consumption and export opportunities.

Geography Analysis

Oromia contributes significantly to national agricultural output by focusing on seasonal cultivation, supported by fertilizer and improved seed distribution. The region employs cluster mechanized maize farming, which strengthens its dominance in grain production and enhances its position in the Ethiopian agriculture market. Additionally, coffee, fruit, and sorghum enterprises benefit from Oromia's diverse agro-climatic conditions, while relative security in the region attracts private investment in storage and processing facilities.

Despite ongoing security challenges, the Amhara region remains a key national sorghum supplier and maintains a strong agricultural research network. Microfinance programs that integrate credit with training have improved entrepreneurial outcomes for rural producers, highlighting the role of financial inclusion in bolstering regional contributions to the Ethiopian agriculture market. The resilience of agricultural output in the region will depend on continued infrastructure rebuilding efforts.

The Somali and Other regions, which include Somali, Afar, and emerging zones in Tigray, are projected to experience the fastest growth among all geographies. This growth is driven by the expansion of irrigation systems and the adoption of drought-tolerant cultivars suited to lowland conditions. The government's lowland development strategy, which emphasizes irrigation and climate-adapted crops, supports this rapid growth by diversifying livelihoods and reducing vulnerability to drought-induced food insecurity.

Competitive Landscape

Ethiopia's agriculture market involves various stakeholders, including producers, importers, and exporters. Leading players in seed production and distribution include Belayneh Kindie Group, Ethio Agri-CEFT, and ACOS Ethiopia. In the export segment, international traders such as Louis Dreyfus Company and Olam International dominate coffee and oilseed exports. These companies provide pre-harvest financing and technical support in exchange for committed supply agreements at predetermined prices. Vertical integration is gaining traction as a competitive strategy, with horticulture exporters include Jittu Horticulture PLC and Agriberries, investing in farming operations. These companies secure consistent quality and volumes by owning or leasing land for avocado, mango, and vegetable production.

Opportunities exist for new entrants capable of deploying large-scale mechanization. For instance, commercial farms in Oromia's Bale zone have achieved high wheat yields. Additionally, agribusinesses that can aggregate smallholder output and bypass intermediary traders, who often capture a significant share of farm-gate value, stand to benefit. Strategic partnerships between domestic producers and international buyers are also emerging. For example, Olam International is piloting regenerative agriculture programs in coffee-growing regions, enabling farmers to earn carbon-credit revenues per hectare.

Technology adoption in Ethiopia's agriculture sector is accelerating. Precision agriculture platforms such as FarmDrive and AgroCenta are providing smallholders with digital extension services, weather forecasts, and market linkages. Cooperatives are also playing a disruptive role. For instance, the Wondo Genet Producers Cooperative aggregates output from 4,800 members and negotiates directly with processors, bypassing intermediary traders and improving farmer margins. The Ethiopian Standards Agency enforces quality standards for export crops. These include coffee grading, sesame moisture content, and pulse size specifications. Exporters are required to obtain certificates of conformity before shipment, ensuring compliance with these standards.

Recent Industry Developments

- June 2025: Ethiopia's Ministry of Agriculture and Precision Development (PxD) signed a USD 3 million agreement to establish a Project Management Unit (PMU) to implement the country's Digital Agriculture Roadmap. The Bill and Melinda Gates Foundation funded the two-year project to increase digital technology adoption across Ethiopia's agricultural value chain.

- February 2025: Ethiopia's National Variety Release Committee approved three TELA maize hybrids, which are genetically engineered to be insect-resistant and drought-tolerant. These varieties, which represent Ethiopia's first commercial biotech food crop, can increase yields by up to 60%. The hybrids will be provided to smallholder farmers without royalty fees.

- November 2024: Ethiopia initiated its first refrigerated vegetable export to Europe, shipping 12 metric tons of Sugar Snap and Mangetout peas to the Netherlands through Djibouti. This development, spearheaded by Ethio Vegfru, establishes a refrigerated logistics corridor for sea freight, strengthening Ethiopia's position in the international fruit and vegetable market.

Ethiopia Agriculture Market Report Scope

Agriculture in Ethiopia involves the production of various food crops, such as fruits and vegetable crops. The Ethiopia Agriculture Market Report is Segmented by Crop Type (Food Crops, and more). The Report Includes Production Analysis (Volume), Consumption Analysis (Value and Volume), Import Analysis (Value and Volume), Export Analysis (Value and Volume), Wholesale Price Trend Analysis and Forecast, List of Key Players, and More. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

By Crop Type

| Food Crops | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | |

| Key Supplying Markets | |||

| Export Market Analysis | Export Value and Volume | ||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Fruits | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Vegetables | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| Plantation Crops (Coffee, Tea, etc.) | Production Analysis | Production Volume | |

| Area Harvested and Yield | |||

| Consumption Analysis (Value and Volume) | |||

| Import Value and Volume | |||

| Key Supplying Markets | |||

| Export Value and Volume | |||

| Key Destination Markets | |||

| Wholesale Price Trend Analysis and Forecast | |||

| Seasonality Analysis | |||

| By Crop Type | Food Crops | Production Analysis | Production Volume | |

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Trade Analysis (Value and Volume) | Import Market Analysis | Import Value and Volume | ||

| Key Supplying Markets | ||||

| Export Market Analysis | Export Value and Volume | |||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Fruits | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Vegetables | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

| Plantation Crops (Coffee, Tea, etc.) | Production Analysis | Production Volume | ||

| Area Harvested and Yield | ||||

| Consumption Analysis (Value and Volume) | ||||

| Import Value and Volume | ||||

| Key Supplying Markets | ||||

| Export Value and Volume | ||||

| Key Destination Markets | ||||

| Wholesale Price Trend Analysis and Forecast | ||||

| Seasonality Analysis | ||||

Key Questions Answered in the Report

What is the Ethiopia agriculture market projected to be worth by 2031?

The Ethiopia agriculture market was valued at USD 6.80 billion in 2025 and estimated to grow from USD 7.19 billion in 2026 to reach USD 9.48 billion by 2031, at a CAGR of 5.71% during the forecast period (2026-2031).

Which crop category is expanding fastest?

Fruits lead growth at a 9.2% CAGR, fueled by corridor investments and Gulf market access.

Why is irrigation pivotal for Ethiopia's farm output?

New schemes allow two annual crop cycles and raise land productivity by up to 120% in lowland zones.

How does digital trading benefit growers?

Electronic exchange trading trims bid-ask spreads to 3.2% and boosts farm-gate prices by about USD 8 per quintal.

Page last updated on: