Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

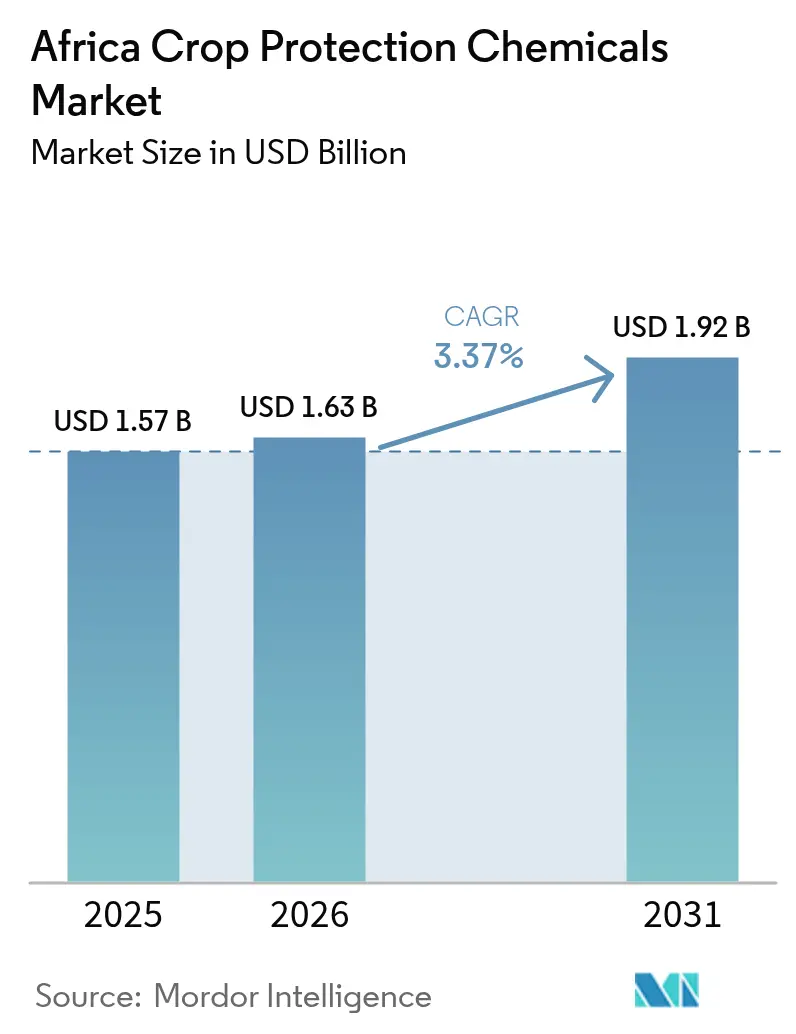

| Base Year Market Size (2025) | USD 1.57 Billion |

| Market Size (2026) | USD 1.63 Billion |

| Market Size (2031) | USD 1.92 Billion |

| Growth Rate (2026 - 2031) | 3.37% CAGR |

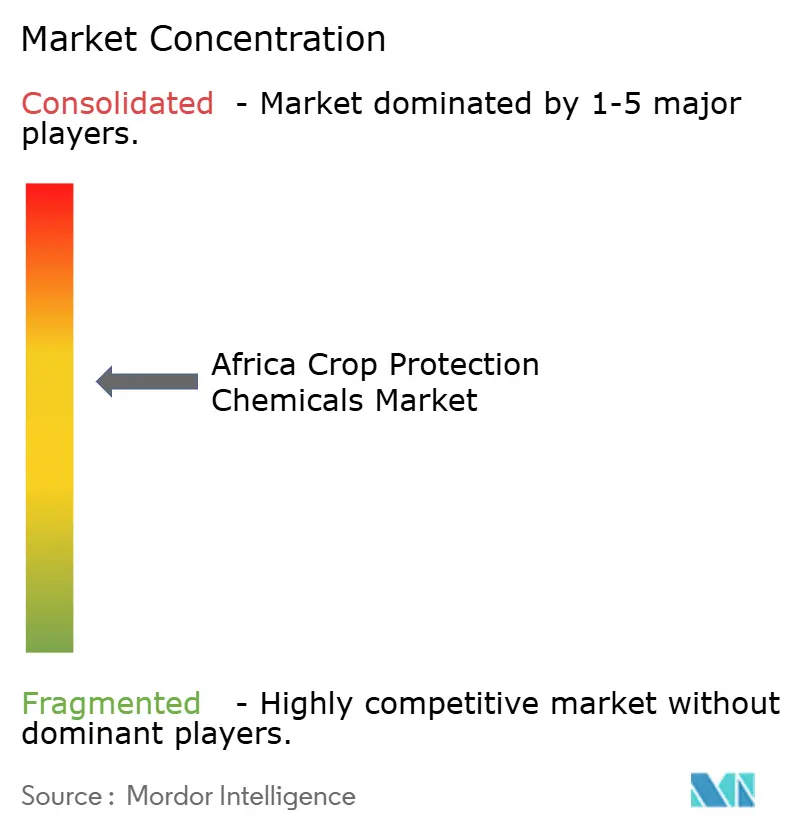

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Crop Protection Chemicals Market Analysis by Mordor Intelligence

The Africa crop protection chemicals market size is anticipated to increase from USD 1.57 billion in 2025 to USD 1.63 billion in 2026 and reach USD 1.92 billion by 2031, growing at a CAGR of 3.37% over 2026-2031. Demand continues to pivot around climate-driven pest outbreaks, subsidy-backed input programs, and the steady march of herbicide-tolerant seed technologies. Commercial estates in Southern and Eastern Africa are expanding spray schedules to protect high-value maize and soybean acreages, while horticulture exporters shift toward premium, low-residue actives that comply with tightened European Union (EU) standards. Counterfeit proliferation and Red Sea freight volatility are eroding distributor margins, placing a premium on traceable supply chains and local formulation capacity. Multinational suppliers are accelerating digital-advisory rollouts that connect credit, weather intelligence, and agronomy, nudging smallholders toward timely, label-compliant applications.

Key Report Takeaways

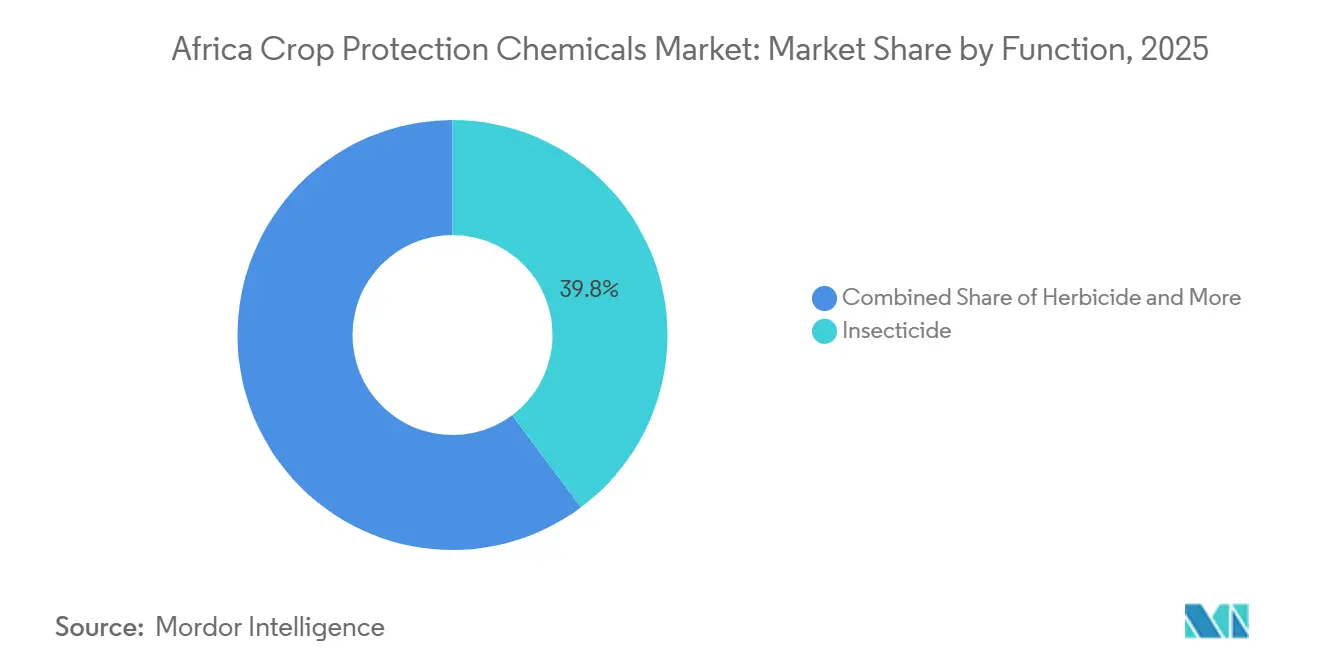

- By Function, insecticides led with 39.8% of the Africa crop protection chemicals market share in 2025, and herbicides exhibit the fastest 3.7% CAGR during 2026-2031.

- By Application mode, foliar products captured 50.7% of the Africa crop protection chemicals market size in 2025, while soil treatment advanced at the fastest 3.7% CAGR from 2026-2031.

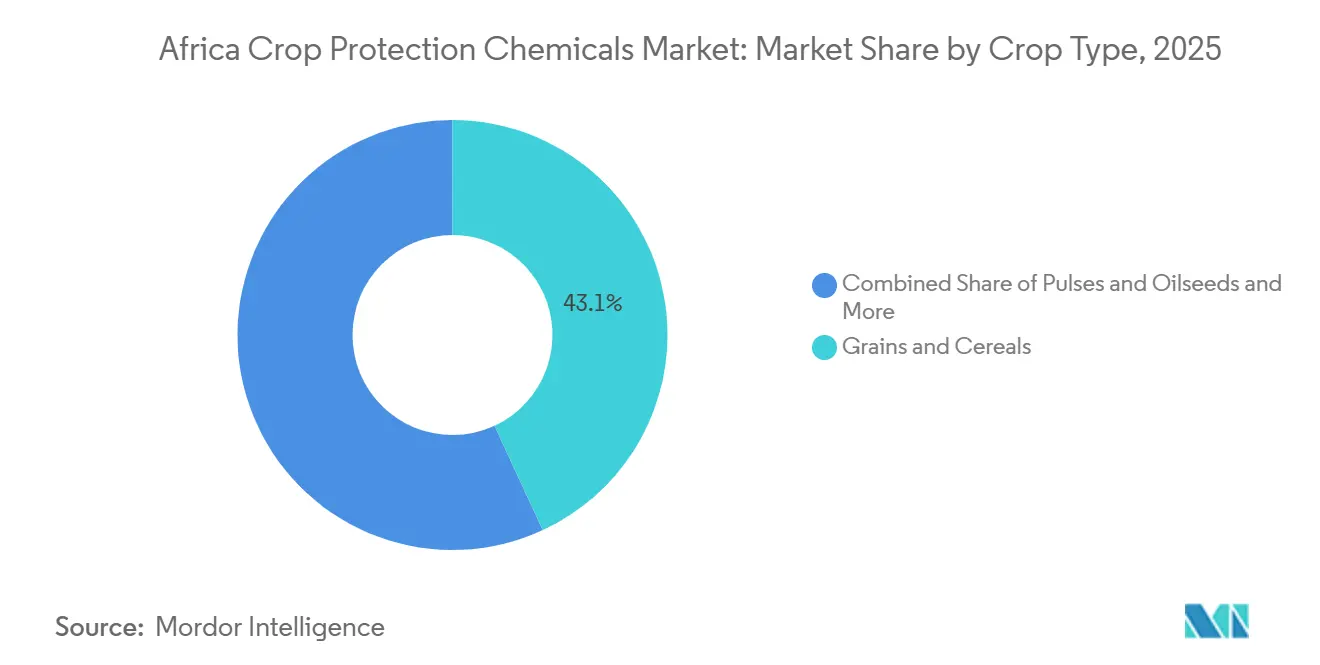

- By Crop type, grains and cereals held a 43.1% share of the Africa crop protection chemicals market in 2025, while pulses and oilseeds are expanding at the fastest 3.5% CAGR during 2026-2031.

- By Geography, South Africa accounted for a 13.6% share of the Africa crop protection chemicals market in 2025 and is forecast to post the fastest 5.1% CAGR from 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Crop Protection Chemicals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating pest pressure from climate-change-driven outbreaks | +0.8% | East and West Africa hot spots | Medium term (2-4 years) |

| Government input-subsidy programs boosting pesticide use | +0.6% | Nigeria, Kenya, Ghana, and Ethiopia | Short term (≤ 2 years) |

| Rapid adoption of herbicide-tolerant crop varieties | +0.5% | South Africa, Nigeria, and Kenya | Medium term (2-4 years) |

| Expansion of commercial farming clusters | +0.7% | Southern Africa and Ethiopian-Kenyan corridors | Long term (≥ 4 years) |

| EU maximum residue limit (MRL) revisions moving exporters to premium actives | +0.4% | South Africa, Kenya, and Ghana | Short term (≤ 2 years) |

| Mobile agro-fintech platforms easing liquidity barriers | +0.3% | Nigeria, Kenya, and Ghana | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Escalating Pest Pressure from Climate-Change-Driven Outbreaks

Rising temperatures and irregular rainfall patterns are extending insect breeding periods and enabling invasive species to spread into new agro-ecological zones. According to the Food and Agriculture Organization (FAO), fall armyworm infestations were reported in 44 countries in 2024, with Kenya experiencing maize yield losses of 10-30% in areas lacking effective control measures[1]Source: Food and Agriculture Organization, “Fall Armyworm Monitoring and Early Warning System,” fao.org. In 2021, desert locust swarms destroyed over 25,000 hectares in Ethiopia, leading to the extensive use of organophosphate and pyrethroid products. Farmers have responded by increasing the frequency of foliar sprays and utilizing premium systemic insecticides. Climate models predicting a temperature rise of 1.5-2 °C suggest that pest reproduction rates could increase by 10-25%, sustaining high demand for insecticides through 2031.

Government Input-Subsidy Programs Boosting Pesticide Use

Voucher-based schemes in Nigeria, Kenya, Tanzania, and Ghana subsidize a portion of pesticide costs for key staple crops. Voucher and e-wallet payments lower credit risk, spur distributor expansion, and stimulate early-season stocking. Fiscal constraints and donor dependency create start-stop purchasing patterns, yet still inject sizable short-term demand spikes. In Nigeria, subsidies covered a significant share of pesticide expenses for rice and maize. In Kenya, a portion of agricultural input funding was allocated to pesticides. Despite challenges such as delays and inconsistent coverage, participating farmers tend to prefer registered pesticide brands, reducing informal trade in the targeted districts. Suppliers that pre-register products within government procurement lists secure preferential access to these large-volume channels.

Rapid Adoption of Herbicide-Tolerant Crop Varieties

The approval of TELA maize and genetically modified cowpea, which offer drought tolerance (DT) and stem borer protection, is driving increased interest in herbicide-tolerant (HT) traits[2]Source: Corteva Agriscience, “Herbicide-Tolerant Maize Adoption in South Africa,” corteva.com. In South Africa, over 85% of maize cultivation involves genetically modified (GM) varieties, incorporating both insect-resistant (Bt) and herbicide-tolerant (HT) traits. Kenya is progressing toward adopting genetically modified (GMO) herbicide-tolerant (HT) and insect-resistant maize to enhance average yields, which stood at approximately 18.5 bags (90 kg) per hectare in 2024. HT crops reallocate budgets from insecticides to herbicides, particularly glyphosate and new stacked-mode formulations designed to manage resistant weed biotypes. Fragmented biotechnology regulations necessitate that suppliers implement country-specific stewardship programs and coexistence guidelines. Seed companies are partnering with agrochemical firms to provide seed-and-spray packages that ensure compatibility with trait-specific herbicides.

Expansion of Commercial Farming Clusters

Mechanized estates have improved procurement processes and facilitated the use of multi-mode chemistries. Private equity and development finance institutions have supported large-scale row-crop projects in Zambia, Tanzania, Mozambique, and Ethiopia. In South Africa, commercial farms accounted for a notable share of national crop protection expenditure, despite occupying a smaller proportion of planted land. Zambia has attracted agricultural investments, leading to the establishment of estates equipped with center-pivot irrigation systems that utilize soil-applied herbicides. Tanzania's growth corridor initiative has developed commercial clusters, driving demand for bundled agronomy services and credit-linked supply chains. Cluster-based logistics have consolidated demand into hub stores, reducing distribution costs for suppliers. Land tenure reforms in Kenya and Ghana have further encouraged consolidation, although intermittent political uncertainty can delay land transactions. Precision agriculture service providers have partnered with input firms to offer bundled solutions, including scouting drones, decision dashboards, and variable-rate prescriptions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent regional bans on high-toxicity actives | -0.5% | Kenya and South Africa | Short term (≤ 2 years) |

| Accelerating pest and weed resistance | -0.4% | Intensive zones continent-wide | Medium term (2-4 years) |

| Proliferation of counterfeit pesticides | -0.6% | Nigeria, Kenya, and Ghana | Short term (≤ 2 years) |

| Red Sea and Suez shipping volatility inflating costs | -0.3% | All import-dependent nations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Regional Bans on High-Toxicity Actives

In 2024, South Africa implemented measures to prohibit several active ingredients in agricultural remedies, focusing on phasing out pesticides containing carcinogenic, mutagenic, or reprotoxic (CMR) substances. This included re-registration requirements for these products and encouraging registrants to adopt lower-toxicity molecules. In the same year, Kenya’s Agriculture and Food Authority confiscated illegal agrochemicals valued at Kenya Shilling (KES) 3.4 million (USD 26,000). South Africa’s regulatory body now mandates expanded environmental assessments, extending new registration timelines by up to 18 months. Additionally, the Economic Community of West African States (ECOWAS) introduced a pesticide harmonization draft aimed at phasing out over 30 active ingredients. Reformulation efforts have increased research costs by USD 2-5 million per molecule, leading to reduced portfolios, particularly for small molecules targeting niche pests, which discourages smaller generic firms. These portfolio gaps are further exacerbated as growers shift to more expensive alternatives, negatively impacting near-term sales.

Accelerating Pest and Weed Resistance

The Insecticide Resistance Action Committee reported high pyrethroid resistance in fall armyworm populations across multiple countries. Glyphosate-resistant palmer amaranth in South African fields significantly reduced efficacy. Therefore, growers are required to rotate modes of action and use residual herbicides, increasing both costs and operational complexity. Without coordinated stewardship efforts, resistance may surpass the pace of new product development, potentially impacting the Africa crop protection chemicals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Function: Insecticides Lead, Herbicides Accelerate

In 2025, insecticides secured 39.8% of the Africa crop protection chemicals market share, driven by fall armyworm, locust, and stem-borer outbreaks across staples and vegetables. The Africa crop protection chemicals market size for insecticides is projected to rise steadily but cede relative share as genetically modified insect-resistant crops diffuse. Herbicides are projected to register the fastest CAGR of 3.7% from 2026-2031, reflecting widespread uptake of herbicide-tolerant seeds and a push to curb escalating rural wages. Fungicides and nematicides serve targeted niches in wheat, potatoes, and floriculture, where disease pressure and export standards justify premium spend. Molluscicides remain minor outside Egypt’s rice fields, yet high-humidity vegetable belts offer pockets of growth as farmers seek season-long snail protection.

Labor scarcity is a significant factor driving the adoption of chemical weed control. Manual weeding is considerably more expensive compared to herbicide programs, making herbicides the preferred economic choice. The adoption of pre-emergence herbicides has significantly reduced weed-related yield losses in key regions. Insecticide volumes remain stable despite rising resistance, with certain classes gaining market share. Suppliers respond with combo packs that integrate pre-emergence herbicides. Investment in digital scouting platforms enables threshold-based insecticide applications, aligning with stewardship guidelines. These factors collectively support the steady growth of the Africa crop protection chemicals market.

By Application Mode: Foliar Dominates, Soil Treatment Gains Traction

Foliar products captured a 50.7% market share in 2025, favored for in-season flexibility across insecticides, fungicides, and desiccants. Revenue generated through foliar applications will grow moderately, with new wettable granule and ultra-low-volume formulations reducing water needs. Soil treatments expand at a fastest 3.7% CAGR from 2026-2031 as estates adopt pre-plant herbicides and nematicides to protect high-value row crops. Seed treatment adoption gains momentum where certified seed systems mature, offering in-seed pest protection that lowers labor and environmental exposure. Fumigation and chemigation remain specialty practices tied to high-value potatoes, tobacco, and irrigated cereals.

Investment in chemigation systems, though limited to irrigated estates, is climbing due to water-use efficiency mandates. Conservation agriculture systems in Southern Africa extensively utilize residual herbicides in no-till maize farming. In South Africa’s potato belt, root-knot nematode outbreaks have driven increased demand for granular nematicides. The seed treatment segment is anticipated to grow significantly as domestic coaters expand operations. Additionally, infrastructure investments, such as center-pivot chemigation rigs, could enable new delivery methods, further diversifying the crop protection chemicals market in Africa.

By Crop Type: Grains and Cereals Anchor, Pulses and Oilseeds Rise

Grains and cereals delivered 43.1% market share of 2025 revenues, reflecting maize and wheat dominance in Southern and East Africa. Pulse and oilseed fields register a fastest 3.5% CAGR from 2026-2031 as soybeans and sunflowers expand in Zambia and South Africa under government-backed diversification schemes. Commercial crops such as cotton and sugarcane absorb concentrated insecticide and herbicide volumes, while fruits and vegetables prioritize low-residue actives to meet export tolerances. Turf and ornamental usage, though small, benefits from urban landscaping budgets in Lagos, Nairobi, and Johannesburg.

Zambia plans to expand soybean cultivation, which is anticipated to increase the demand for pre-emergence herbicides. In South Africa, most soybean farmers are adopting combined herbicide and pod-borer management programs. These developments demonstrate how changes in crop composition influence the volume and value dynamics of the crop protection chemicals market in Africa.

Geography Analysis

South Africa commanded 13.6% of market share in 2025 and exhibited the fastest growing CAGR of 5.1% from 2026-2031, fueled by large estates integrating precision agronomy, seed technology, and multi-mode pesticide programs. Rigorous registration frameworks limit counterfeit penetration yet prolong new-product approvals, prompting multinationals to invest in local data to speed dossiers. South Africa presents a mature, technology-intensive ecosystem with precision agriculture penetration above 30% among commercial farmers. South Africa is anticipated to grow as citrus and grape exporters adopt ultra-low-dose systemic fungicides to secure European Union market access. Domestic manufacturers operate toll formulation plants that supply neighboring countries, leveraging the Southern African Development Community duty framework.

North Africa is driven by Egypt’s irrigated vegetable production and Morocco’s focus on tomatoes and citrus for export. Investments in reducing residue breaches and expanding premium insecticide sales supported growth in the region. Algeria’s reliance on subsidized fungicides and herbicides in its wheat belt faced challenges from water scarcity, potentially limiting long-term growth. West Africa followed, with Nigeria’s smallholder maize and rice systems dominating the market, though counterfeit products in informal distribution channels hindered premium adoption. Ghana and Côte d’Ivoire maintained steady demand through cocoa board distribution systems.

East Africa contributed significantly, with Kenya’s horticulture and Tanzania’s maize production benefiting from subsidies and digital credit channels. Central Africa’s market share was driven by cocoa production in Cameroon and subsistence farming in the Democratic Republic of the Congo, though political instability and infrastructure gaps constrained growth. Despite these challenges, NGO-led pest-alert programs in Central Africa may create future opportunities. Together, these regional trends supported the overall growth of the Africa crop protection chemicals market in 2025.

Competitive Landscape

Top players Bayer AG, Syngenta Group, BASF SE, Corteva Agriscience, and FMC Corporation jointly held a significant share of 2025 revenue, reflecting moderate concentration that leaves strategic openings for other key players, including United Phosphorus Limited (UPL), Nufarm, and Sumitomo Chemical. Companies like Syngenta, Bayer, and Corteva leverage extensive dealer networks, crop advisory services, and credit programs to maintain strong relationships with commercial estates and export-oriented growers. Meanwhile, UPL and Nufarm focus on off-patent active ingredients, smaller packaging options, and flexible credit terms to cater to price-sensitive smallholder farmers.

Technological innovations are a key differentiator for multinational firms. Adama and Rotam are expanding their presence in West Africa by combining competitive pricing for generics with season-based repayment plans. Bayer’s Climate FieldView supports variable-rate herbicide application, enhancing customer retention. Syngenta’s Cropwise platform utilizes satellite imagery and artificial intelligence pest models, securing service contracts with estates. BASF SE has filed fungicide patents targeting cereal pathogens in Africa, indicating plans for premium product launches[3]Source: BASF SE, “Patent Database: Fungicide Innovations for African Cereals,” basf.com.

Mobile fintech partnerships are reshaping last-mile access to crop protection products. Corteva Agriscience collaborates with Digifarm in Kenya to offer bundled input loans, while Bayer’s FarmRise expansion in Nigeria has connected farmers to mobile storefronts that integrate pesticide, seed, and fertilizer purchases. The rise of direct-to-farmer e-commerce is compressing agro-dealer margins, compelling market players to balance traditional and digital distribution channels. As freight disruptions and regulatory restrictions continue to influence product portfolios, agile supply chains and data-driven advisory models are anticipated to play a critical role in determining market share dynamics within the Africa crop protection chemicals market.

Africa Crop Protection Chemicals Industry Leaders

BASF SE

Bayer AG

Corteva Agriscience

FMC Corporation

Syngenta Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: BASF SE South Africa has introduced a new fungicide called Revytek, designed to improve maize disease management. The product offers effective control of major fungal pathogens, enabling farmers to enhance crop health and yields.

- September 2024: BASF SE introduced Cimegra SC, an insecticide designed to combat fall armyworm, a significant pest affecting maize crops. The product incorporates a new active ingredient that ensures effective and durable protection while minimizing the risk of resistance development.

- April 2024: Syngenta Group unveiled Pergado Ultra, a new fungicide innovation for disease control in crops. It offers enhanced protection against downy mildew and other fungal diseases, aiming to improve crop yields and resilience in Africa.

Africa Crop Protection Chemicals Market Report Scope

Crop protection chemicals, also referred to as pesticides or agrochemicals, are substances formulated to prevent, control, or eliminate pests, diseases, and weeds that pose a threat to crops. These chemicals, which include herbicides, insecticides, and fungicides, are applied to plants or soil to improve agricultural productivity and safeguard crop quality and yield.

The Africa Crop Protection Chemicals Market report provides a comprehensive analysis across multiple segments. By function, the market covers fungicides, herbicides, insecticides, nematicides, and molluscicides. Based on the application mode, it evaluates chemigation, foliar spray, fumigation, seed treatment, and soil treatment methods. In terms of crop type, the study includes commercial crops, fruits and vegetables, grains and cereals, pulses and oilseeds, and turf and ornamental plants. Geographically, the assessment spans South Africa, Egypt, Kenya, and the Rest of Africa. Market size and forecasts are presented in value (USD) and volume (metric tons).

By Function

| Fungicide |

| Herbicide |

| Insecticide |

| Molluscicide |

| Nematicide |

By Application Mode

| Chemigation |

| Foliar |

| Fumigation |

| Seed Treatment |

| Soil Treatment |

By Crop Type

| Commercial Crops |

| Fruits and Vegetables |

| Grains and Cereals |

| Pulses and Oilseeds |

| Turf and Ornamental |

By Country

| South Africa |

| Egypt |

| Kenya |

| Rest of Africa |

| By Function | Fungicide |

| Herbicide | |

| Insecticide | |

| Molluscicide | |

| Nematicide | |

| By Application Mode | Chemigation |

| Foliar | |

| Fumigation | |

| Seed Treatment | |

| Soil Treatment | |

| By Crop Type | Commercial Crops |

| Fruits and Vegetables | |

| Grains and Cereals | |

| Pulses and Oilseeds | |

| Turf and Ornamental | |

| By Country | South Africa |

| Egypt | |

| Kenya | |

| Rest of Africa |

Market Definition

- Function - Crop Protection Chemicals are apllied to control or prevent pests, including insects, fungi, weeds, nematodes, and mollusks, from damaging the crop and to protect the crop yield.

- Application Mode - Foliar, Seed Treatment, Soil Treatment, Chemigation, and Fumigation are the different type of application modes through which crop protection chemicals are applied to the crops.

- Crop Type - This represents the consumption of crop protection chemicals by Cereals, Pulses, Oilseeds, Fruits, Vegetables, Turf, and Ornamental crops.

| Keyword | Definition |

|---|---|

| IWM | Integrated weed management (IWM) is an approach to incorporate multiple weed control techniques throughout the growing season to give producers the best opportunity to control problematic weeds. |

| Host | Hosts are the plants that form relationships with beneficial microorganisms and help them colonize. |

| Pathogen | A disease-causing organism. |

| Herbigation | Herbigation is an effective method of applying herbicides through irrigation systems. |

| Maximum residue levels (MRL) | Maximum Residue Limit (MRL) is the maximum allowed limit of pesticide residue in food or feed obtained from plants and animals. |

| IoT | The Internet of Things (IoT) is a network of interconnected devices that connect and exchange data with other IoT devices and the cloud. |

| Herbicide-tolerant varieties (HTVs) | Herbicide-tolerant varieties are plant species that have been genetically engineered to be resistant to herbicides used on crops. |

| Chemigation | Chemigation is a method of applying pesticides to crops through an irrigation system. |

| Crop Protection | Crop protection is a method of protecting crop yields from different pests, including insects, weeds, plant diseases, and others that cause damage to agricultural crops. |

| Seed Treatment | Seed treatment helps to disinfect seeds or seedlings from seed-borne or soil-borne pests. Crop protection chemicals, such as fungicides, insecticides, or nematicides, are commonly used for seed treatment. |

| Fumigation | Fumigation is the application of crop protection chemicals in gaseous form to control pests. |

| Bait | A bait is a food or other material used to lure a pest and kill it through various methods, including poisoning. |

| Contact Fungicide | Contact pesticides prevent crop contamination and combat fungal pathogens. They act on pests (fungi) only when they come in contact with the pests. |

| Systemic Fungicide | A systemic fungicide is a compound taken up by a plant and then translocated within the plant, thus protecting the plant from attack by pathogens. |

| Mass Drug Administration (MDA) | Mass drug administration is the strategy to control or eliminate many neglected tropical diseases. |

| Mollusks | Mollusks are pests that feed on crops, causing crop damage and yield loss. Mollusks include octopi, squid, snails, and slugs. |

| Pre-emergence Herbicide | Preemergence herbicides are a form of chemical weed control that prevents germinated weed seedlings from becoming established. |

| Post-emergence Herbicide | Postemergence herbicides are applied to the agricultural field to control weeds after emergence (germination) of seeds or seedlings. |

| Active Ingredients | Active ingredients are the chemicals in pesticide products that kill, control, or repel pests. |

| United States Department of Agriculture (USDA) | The Department of Agriculture provides leadership on food, agriculture, natural resources, and related issues. |

| Weed Science Society of America (WSSA) | The WSSA, a non-profit professional society, promotes research, education, and extension outreach activities related to weeds. |

| Suspension concentrate | Suspension concentrate (SC) is one of the formulations of crop protection chemicals with solid active ingredients dispersed in water. |

| Wettable powder | A wettable powder (WP) is a powder formulation that forms a suspension when mixed with water prior to spraying. |

| Emulsifiable concentrate | Emulsifiable concentrate (EC) is a concentrated liquid formulation of pesticide that needs to be diluted with water to create a spray solution. |

| Plant-parasitic nematodes | Parasitic Nematodes feed on the roots of crops, causing damage to the roots. These damages allow for easy plant infestation by soil-borne pathogens, which results in crop or yield loss. |

| Australian Weeds Strategy (AWS) | The Australian Weeds Strategy, owned by the Environment and Invasives Committee, provides national guidance on weed management. |

| Weed Science Society of Japan (WSSJ) | WSSJ aims to contribute to the prevention of weed damage and the utilization of weed value by providing the chance for research presentation and information exchange. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms