Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

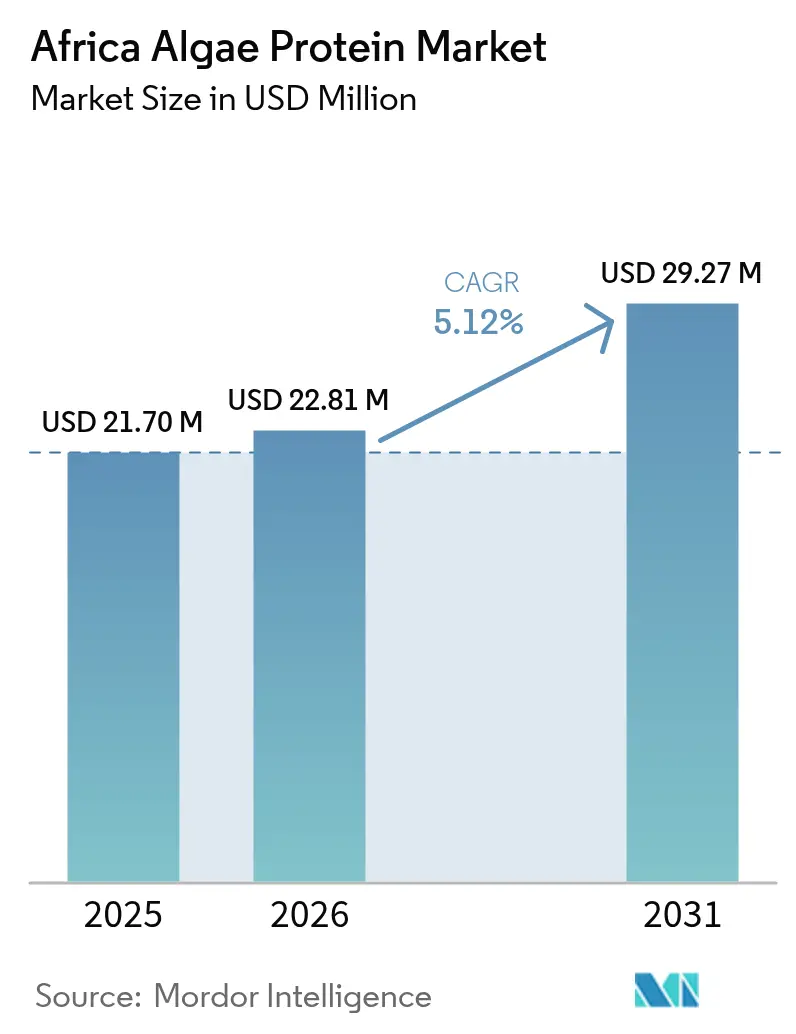

| Base Year Market Size (2025) | USD 21.70 Million |

| Market Size (2026) | USD 22.81 Million |

| Market Size (2031) | USD 29.27 Million |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

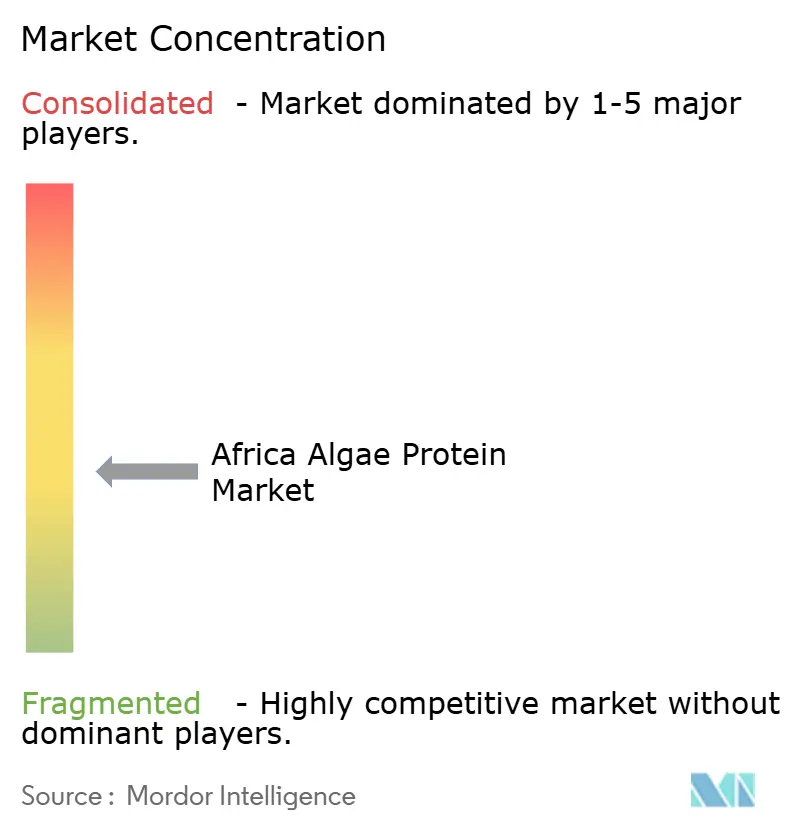

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Algae Protein Market Analysis by Mordor Intelligence

Africa algae protein market size in 2026 is estimated at USD 22.81 million, growing from 2025 value of USD 21.70 million with 2031 projections showing USD 29.27 million, growing at 5.12% CAGR over 2026-2031. Spirulina and chlorella are moving from niche supplements into aquaculture feed, school-feeding schemes, and cosmetic pigments, widening the customer base across the continent. South Africa dominates current output because its open-raceway farms sit next to ISO-certified extraction plants that funnel phycocyanin into global colorant supply chains. Nigeria is emerging fastest as tilapia and catfish farmers replace up to 30% of fishmeal with home-grown spirulina, trimming feed bills and lifting margins. Marine algae is winning new investment in Tanzania’s Zanzibar archipelago, where the World Bank-funded TASFAM program targets 200,000 metric tons of carrageenan-grade seaweed by 2030, unlocking protein co-products for feed and fertilizer. Regulatory alignment under the African Union’s new Food Safety Agency promises to streamline cross-border trade, yet fragmented in-country rules still cause export rejections, especially when heavy-metal limits diverge from Codex standards.

Key Report Takeaways

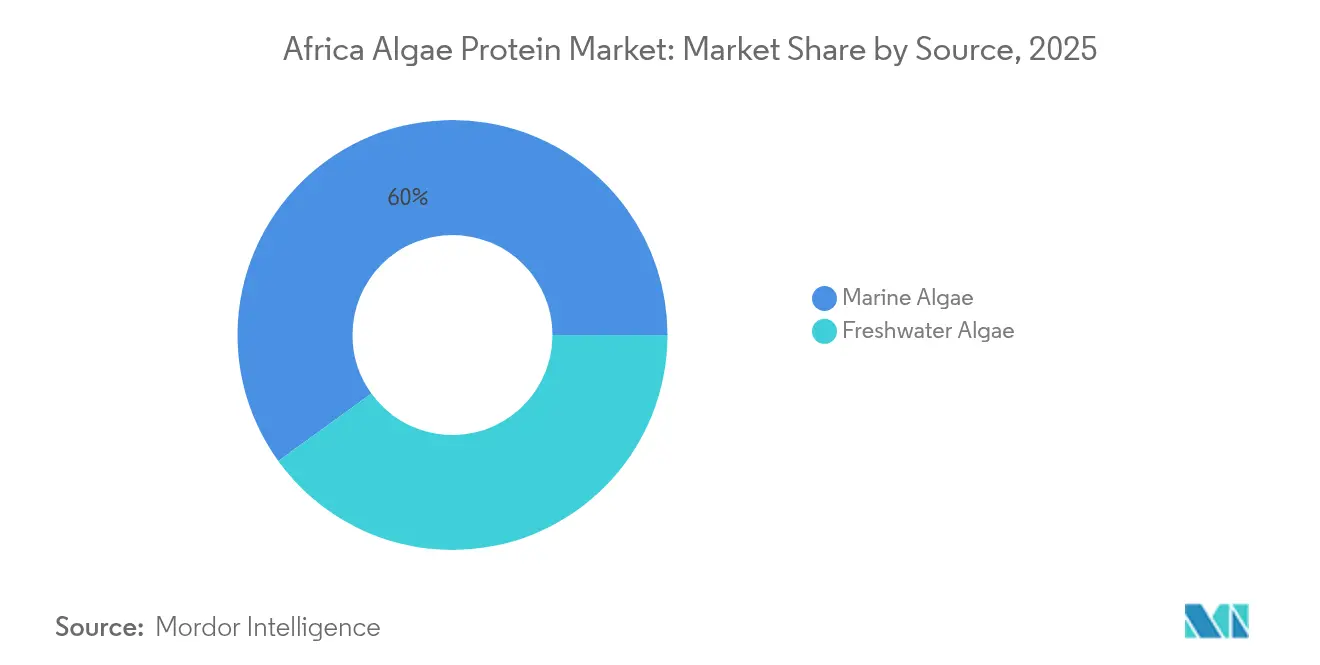

- By source, freshwater algae held 40.04% of 2025 revenue, while marine algae is forecast to post a 6.65% CAGR through 2031.

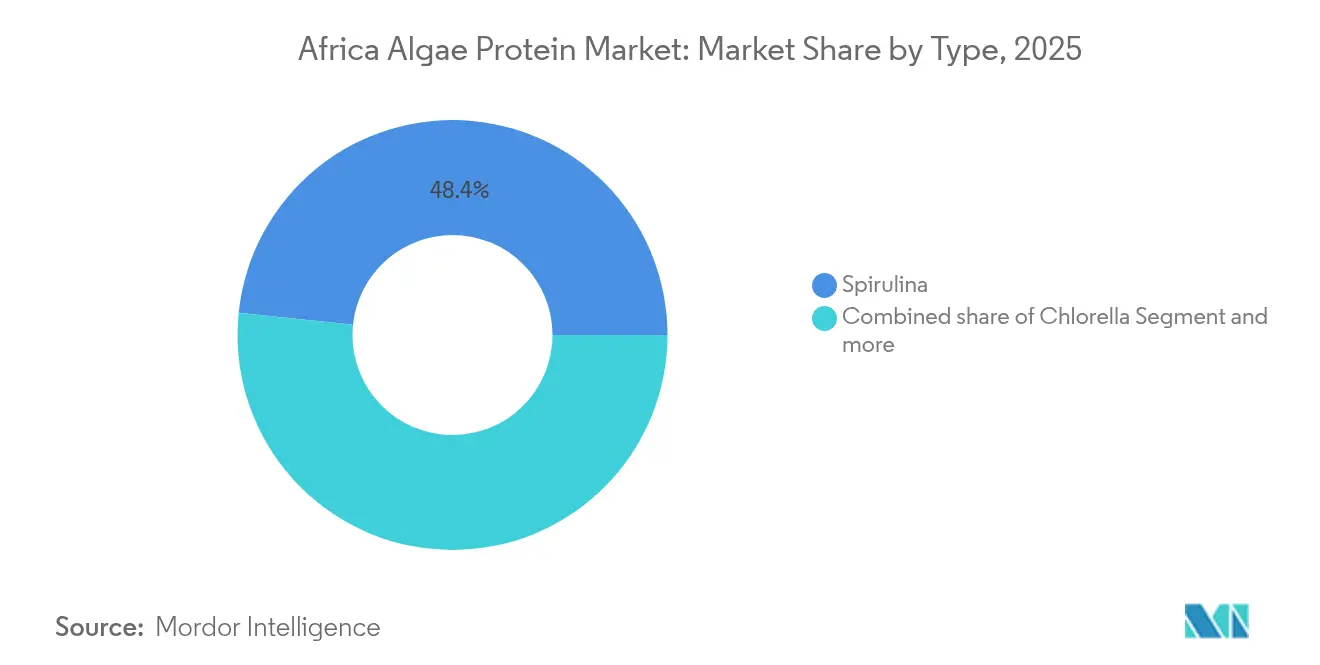

- By type, spirulina accounted for 48.35% of 2025 volume, whereas chlorella is projected to expand at a 6.03% CAGR through 2031.

- By application, food and beverages led with a 34.12% slice of 2025 demand, but supplements are on track for a 6.88% CAGR through 2031.

- By geography, South Africa captured 46.05% of the Africa algae protein market share in 2025, yet Nigeria is set to log the highest regional growth at 6.6% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Algae Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for algae protein in sports nutrition and dietary supplements | +1.2% | South Africa, Kenya, Nigeria (urban centers) | Medium term (2-4 years) |

| Growth in functional foods and beverages using clean-label ingredients | +0.9% | Global, with early adoption in South Africa and Kenya | Medium term (2-4 years) |

| Government and NGO malnutrition-relief programs adopting spirulina | +0.8% | Ethiopia, Uganda, Kenya, Tanzania, Ghana | Short term (≤ 2 years) |

| Adoption of algae protein in aquaculture and animal feed | +1.0% | Nigeria, Kenya, Tanzania (coastal aquaculture zones) | Short term (≤ 2 years) |

| Cosmetic-grade phycocyanin extraction capacity expansion in South Africa | +0.4% | South Africa, with exports to the EU and North America | Long term (≥ 4 years) |

| Focus on sustainability and environmental impact | +0.7% | Global, with regulatory influence in South Africa and Kenya | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for algae protein in sports nutrition and dietary supplements

In South Africa and Kenya, urban consumers are increasingly opting for plant-based protein powders, steering clear of soy allergens and being mindful of whey’s environmental impact. Spirulina and chlorella, boasting a bioavailability of over 80% and a complete amino-acid profile, are becoming favorites among formulators. These ingredients are particularly appealing to endurance athletes and gym enthusiasts who are willing to pay a premium for clean-label certifications. In 2024, Kenyan startup Nasaru Naturals, fresh off securing over USD 100,000 in seed funding, is now on the hunt for an additional USD 500,000 to scale up Lake Natron's spirulina cultivation. They've teamed up with Victory Farms to experiment with algae-fortified tilapia feed, which also serves as a supplement for human consumption. This innovative dual-use approach slashes production costs by 25% per kilogram, allowing them to compete directly with imported pea-protein isolates on price. Meanwhile, South African brands are revamping their pre-workout blends, infusing them with phycocyanin-rich spirulina extracts. By harnessing the antioxidant properties of this pigment, they're carving out a unique niche in a saturated market. With the African Union's Food Safety Agency, inaugurated in February 2025, providing much-needed regulatory clarity, the cross-border supplement trade is poised for a boost. This alignment on maximum residue limits for pesticides and heavy metals is set to streamline the process.

Growth in functional foods and beverages using clean-label ingredients

In South Africa, bakery and dairy-alternative producers are infusing spirulina powder into their offerings, including protein-enriched bread, pasta, and oat milk. This move aligns with a growing consumer preference for ingredient lists that are both recognizable and devoid of synthetic additives. In 2024, the FAO's Joint Expert Committee on Food Additives (JECFA) reaffirmed spirulina's Generally Recognized as Safe (GRAS) status[1]Source: FAO, “JECFA Monograph on Spirulina,” fao.org. This endorsement clears a significant hurdle for food processors aiming for Codex Alimentarius compliance. Meanwhile, in Nairobi and Johannesburg, health-conscious millennials are being targeted with green-juice blends and functional smoothies that capitalize on chlorella's rich chlorophyll content. Yet, formulators grapple with a challenge: the earthy flavor of spirulina necessitates the use of masking agents, like natural vanilla or cocoa, which inflate ingredient costs by 5% to 10%. In Ghana, Chale Spirulina commenced commercial production in January 2024 at its Kumasi facility. They're rolling out a pre-gelatinized spirulina flour, designed to disperse uniformly in dough, to local bakeries. This breakthrough not only resolves a long-standing palatability concern but also positions Chale Spirulina to tap into West Africa's burgeoning functional-food market, expected to see double-digit growth rates until 2030.

Government and NGO malnutrition-relief programs adopting spirulina

In 2024, Ethiopia's Spirulina Center, in collaboration with the United Nations World Food Programme, distributed over 50 metric tons of spirulina tablets to malnourished children and pregnant women. This initiative led to a notable 15% reduction in stunting rates within just six months. Meanwhile, Uganda's Spirumaisha project, backed by the Belgian Development Cooperation, successfully trained 200 smallholder farmers. These farmers learned to cultivate spirulina in cost-effective open-pond systems, achieving impressive yields of 8 grams per square meter daily, all without the use of chemical fertilizers. In Turkana County, Kenya's Ministry of Health initiated a 2024 pilot program, fortifying maize porridge with 5% spirulina powder. This effort aims to combat protein-energy malnutrition prevalent among pastoralist communities. The cost-effectiveness of these programs stems from spirulina's unique cultivation requirements: it doesn't need arable land and can thrive in brackish water, which is typically unsuitable for conventional crops. However, scaling up these initiatives presents logistical challenges. Spirulina boasts a mere 7-day shelf life post-harvest, underscoring the urgent need for on-site spray-drying infrastructure. Additionally, the African Union's Food Safety Agency is collaborating with member states to standardize microbiological standards for spirulina powder. These standards currently differ by country, complicating bulk procurement efforts by international NGOs.

Adoption of algae protein in aquaculture and animal feed

Nigerian farmers of catfish and tilapia are now substituting a significant portion of fishmeal in their feed formulations with locally sourced spirulina. This shift not only cuts costs but also ensures growth rates surpassing 1.2 grams per day. The economic viability of this substitution stems from spirulina's protein content, which exceeds 60% on a dry-weight basis. Additionally, the omega-3 fatty acids in spirulina enhance fillet quality, allowing it to fetch a 10% price premium in Lagos's wholesale markets. In Kibuyuni, Kenya's Blue Empowerment project, backed by the European Union, has melded seaweed cultivation with tilapia cages. Their findings reveal that algae-based feed can curtail nitrogen effluent by 25%, thereby reducing the risks of eutrophication in coastal lagoons. Meanwhile, Tanzania's Zanzibar archipelago is ramping up carrageenan-grade seaweed production. This initiative, under the World Bank's USD 200 million TASFAM project, aims for an ambitious target of 200,000 metric tons annually by 2030, with some set aside for aquaculture feed trials. Further bolstering the region's seaweed endeavors, the Zanzibar Seaweed Cluster Initiative (ZASCO) has established a carrageenan processing plant with a capacity of 1,500 metric tons per year. Management is also delving into the co-production of a protein-rich seaweed meal tailored for poultry and aquaculture. However, for these burgeoning initiatives to thrive, alignment with the African Union's Sanitary and Phytosanitary (SPS) framework will be paramount, ensuring smooth cross-border trade of algae-based feed ingredients.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High production cost | -0.6% | Nigeria, Kenya, Ghana (smallholder systems) | Short term (≤ 2 years) |

| Limited consumer awareness and palatability challenges | -0.5% | Rural areas across Africa | Medium term (2-4 years) |

| Contamination and quality control challenges | -0.4% | West Africa, East Africa (open-pond systems) | Short term (≤ 2 years) |

| Fragmented quality and regulatory standards are causing export rejections | -0.3% | Nigeria, Ghana, Kenya (export-oriented producers) | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High production cost

In sub-Saharan Africa, energy costs for spirulina cultivation are 30% to 50% higher than in Asia. This disparity arises from an unreliable grid and a dependence on diesel generators for tasks like paddle-wheel agitation and spray-drying. For instance, while Nigerian producers face electricity costs of USD 0.40 per kilogram of dried spirulina, their counterparts in India pay only USD 0.15. Such high energy expenses diminish Nigeria's competitiveness in the export market. Additionally, food-grade CO₂, essential for pH control in photobioreactors, is priced at USD 200 per metric ton in Nairobi. This is twice the European rate, a consequence of local industrial-gas suppliers not achieving economies of scale. Furthermore, many inoculum and nutrient inputs, including sodium bicarbonate and potassium nitrate, are imported, inflating operating costs by an additional 15% to 20%. To combat these challenges, Ghana's Chale Spirulina has teamed up with local salt producers, securing sodium bicarbonate below market rates and reducing input costs by 12%. Meanwhile, solar-powered drying systems are gaining traction as a cost-saving measure. Pilot projects in Kenya have showcased a 40% reduction in energy use. However, the initial investment of USD 75,000 for a 100-kilogram daily capacity is a significant hurdle for smallholders. While the African Development Bank's Climate Action Window offers concessional financing that could help scale up these initiatives, the average 18-month loan-approval timeline poses a challenge, stalling capacity expansions.

Limited consumer awareness and palatability challenges

In West and East Africa, rural populations often mistake spirulina for an industrial or pharmaceutical product, showing limited awareness of its potential as a food ingredient. The earthy, seaweed-like flavor of spirulina poses a challenge, as it's not well-received in traditional porridges and stews. In response, NGOs are experimenting with microencapsulation techniques to mask the taste while ensuring the nutrients remain bioavailable. Uganda's Spirumaisha project found that 35% of its beneficiaries stopped spirulina supplementation after just three months, primarily due to flavor issues. This highlights the urgent need for formulations that resonate with local tastes. Meanwhile, urban consumers in South Africa and Kenya, influenced by imported superfoods and wellness trends on social media, show a greater openness to spirulina. However, its retail price is three to five times that of soy protein isolate, which makes many hesitant. Efforts by the African Union's Food Safety Agency and national health ministries aim to promote algae consumption. Yet, with budget constraints, their outreach is predominantly urban, leaving rural areas largely unaddressed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Marine Algae Gains as Seaweed Infrastructure Scales

Marine algae are projected to grow at a 6.65% CAGR from 2026 to 2031, surpassing freshwater algae, which held a 40.04% market share in 2025. Tanzania's World Bank-backed TASFAM project is investing USD 200 million in Zanzibar's seaweed farming infrastructure, targeting 200,000 metric tons of carrageenan-grade production by 2030. The Zanzibar Seaweed Cluster Initiative operates a 1,500-metric-ton carrageenan plant and is exploring protein-rich seaweed meal for aquaculture feed, leveraging the archipelago's 1,600-kilometer coastline and farmer cooperatives. Kenya's Blue Empowerment project integrated seaweed cultivation with tilapia cages in Kibuyuni, reducing nitrogen effluent by 25% in coastal lagoons. While freshwater algae, led by spirulina, benefit from lower capital costs and year-round cultivation in landlocked countries like Ethiopia and Uganda, marine algae's co-product potential (carrageenan, protein, bioactive compounds) is attracting investors. Coastal BioTech secured USD 20 million in December 2024 to build a seaweed-to-biofertilizer plant in Zanzibar, converting processing waste into organic soil amendments.

Freshwater spirulina's dominance in 2024 stems from its role in malnutrition relief and phycocyanin extraction. Ethiopia's Spirulina Center distributed over 50 metric tons in 2024, reducing child stunting rates by 15% in six months. Uganda's Spirumaisha project trained 200 farmers to cultivate spirulina in low-cost open ponds, yielding 8 grams per square meter daily without chemical fertilizers. Marine algae's faster growth is driven by infrastructure investments and regulatory support. The African Union's Sanitary and Phytosanitary framework is prioritizing seaweed trade protocols to reduce export rejections affecting West African spirulina producers.

By Type: Chlorella Gains Ground in Elderly Nutrition

In 2025, Spirulina held a 48.35% market share, highlighting its role in malnutrition programs, aquaculture feed, and phycocyanin extraction for cosmetics. Chlorella is projected to grow at a 6.03% CAGR through 2031, driven by its higher protein density (60%-70% dry weight vs. spirulina's 55%-65%) and use in elderly and medical nutrition targeting sarcopenia and immune senescence. Over 70 companies produce Chlorella vulgaris globally, with Taiwan leading at 400 metric tons annually and Germany at 130-150 metric tons. African production is nascent, limited to pilot facilities in South Africa and Kenya. Mechanical or enzymatic processing enhances chlorella's digestibility and unlocks bioactive compounds like nucleotides and beta-glucans, supporting immune health in aging populations. South African brands are launching chlorella-based protein powders for the over-60 demographic, which is expected to grow 15% annually through 2030 due to urbanization and rising incomes.

Spirulina's dominance stems from its versatility and established supply chains. DIC Corporation and Sensient Technologies source African spirulina for LINABLUE phycocyanin, used in confectionery and beverages. Sun Chemical showcased this ingredient at the Institute of Food Technologists' FIRST 2024 trade show in Chicago. Ghana's Chale Spirulina introduced pre-gelatinized spirulina flour in January 2024, addressing dispersibility issues in bakery applications and targeting West African functional-food demand. The "Others" category, including Dunaliella salina and Haematococcus pluvialis, remains small due to high cultivation costs and low consumer awareness. However, Haematococcus, rich in astaxanthin, is gaining interest from South African cosmetic formulators seeking natural carotenoid alternatives. Regulatory clarity from the African Union's Food Safety Agency is crucial for chlorella adoption, as current standards focus on spirulina and lack specific microbiological limits for chlorella powder.

By Application: Supplements Outpace Food as Clean-Label Demand Surges

From 2026 to 2031, the supplements sector is projected to grow at a 6.88% CAGR, driven by urban consumers in South Africa and Kenya seeking soy-free, plant-based protein powders without synthetic additives. In 2025, the food and beverages segment held a 34.12% market share, supported by spirulina-infused bakery items and dairy substitutes, though palatability challenges limit rural adoption. Kenyan startup Nasaru Naturals is expanding spirulina cultivation at Lake Natron for sports-nutrition brands and partnering with Victory Farms to trial algae-enhanced tilapia feed, which doubles as a human supplement. This model cuts costs by 25% per kilogram, achieving price parity with imported pea-protein isolates. Sports and performance nutrition dominate the supplements segment, driven by gym-goers and endurance athletes prioritizing amino-acid profiles with over 80% bioavailability. Elderly and medical nutrition are emerging, with chlorella-based products addressing sarcopenia and immune support in aging populations.

In 2024, animal feed held a significant market share, as Nigerian catfish and tilapia farmers replaced up to 30% of fishmeal with spirulina, reducing costs while maintaining growth rates above 1.2 grams daily. Tanzania's Zanzibar archipelago is co-producing seaweed meal under the World Bank's TASFAM initiative, targeting 200,000 metric tons of carrageenan-grade seaweed by 2030, with a portion allocated for aquaculture feed trials. The food and beverage sector faces spirulina's earthy flavor, requiring masking agents like vanilla or cocoa, which increase ingredient costs by 5% to 10%. Chale Spirulina's pre-gelatinized flour resolves clumping in bakery dough, ensuring even distribution. While cosmetics and biofertilizers remain niche, they attract impact investors. Coastal BioTech's USD 20 million Zanzibar facility converts carrageenan byproducts into organic soil enhancers, sequestering 2 metric tons of CO₂-equivalent per hectare.

Geography Analysis

In 2025, South Africa held a 46.05% market share, supported by advanced cultivation infrastructure, pharmaceutical-grade processing facilities, and proximity to Cape Town's export terminals. A February 2025 analysis confirmed the economic viability of extracting cosmetic-grade C-phycocyanin at scales above 500 kilograms annually, with production costs of USD 80 per gram. Cosmetic-grade phycocyanin is replacing synthetic blue dyes in premium skincare serums. DIC Corporation and Sensient Technologies source South African spirulina for their LINABLUE and SUNFOODS portfolios. Limited ISO 22716-certified facilities constrain exports, but the African Union's Food Safety Agency is working to harmonize standards. South Africa's year-round sunlight enables open-raceway cultivation, cutting energy costs by 20%.

Nigeria is projected to grow at a 6.6% CAGR through 2031, driven by aquaculture operators replacing fishmeal with spirulina, reducing feed costs by up to 30% for tilapia and catfish. Farmers in Lagos and Ogun states report that spirulina-fortified feed improves fillet quality. However, reliance on diesel generators due to unreliable electricity doubles energy costs compared to India. Kenya is emerging as a sports-nutrition hub, with Nasaru Naturals scaling Lake Natron spirulina cultivation and partnering with Victory Farms to trial algae-fortified tilapia feed. Kenya's Blue Empowerment project integrated seaweed cultivation with tilapia farming, reducing nitrogen effluent by 25%.

Tanzania's Zanzibar archipelago is scaling carrageenan-grade seaweed production under the World Bank's USD 200 million TASFAM project, targeting 200,000 metric tons annually by 2030. The Zanzibar Seaweed Cluster Initiative operates a 1,500-metric-ton carrageenan plant and is exploring protein-rich seaweed meal for aquaculture feed. Coastal BioTech secured USD 20 million in December 2024 to build a seaweed-to-biofertilizer plant, converting carrageenan waste into organic soil amendments that sequester 2 metric tons of CO₂-equivalent per hectare. Ghana's market is growing, with Chale Spirulina launching commercial production in January 2024 at its Kumasi facility, targeting bakeries with pre-gelatinized spirulina flour. The company partnered with KITA to train farmers and scale production for West African functional-food demand. Elsewhere in Africa, Ethiopia, Uganda, Zimbabwe, and Morocco focus on malnutrition-relief programs. Ethiopia's Spirulina Center distributed over 50 metric tons in 2024, reducing child stunting rates by 15%. Zimbabwe established its first spirulina microfarm in April 2024 at Gwebi Agricultural College to train smallholders and support local food fortification.

Competitive Landscape

In the Africa algae protein market, which exhibits moderate concentration, regional specialists like SAFi Spirulina, Chale Spirulina, and Nasaru Naturals compete alongside global players such as DIC Corporation, Sensient Technologies, and Parry Nutraceuticals. These global companies source African-grown spirulina primarily for phycocyanin extraction and natural-color portfolios. However, fragmentation persists in West and East Africa, where smallholder producers rely on open-pond systems with limited quality-control infrastructure. This has led to a 25% increase in export rejections in 2024 due to heavy-metal and microbial contamination. Strategic initiatives are focusing on vertical integration and co-product development. For instance, Coastal BioTech announced a USD 20 million seaweed-to-biofertilizer plant in Zanzibar, which converts carrageenan processing waste into organic soil amendments, reducing production costs by 15%. Additionally, white-space opportunities exist in chlorella cultivation for elderly nutrition, cosmetic-grade phycocyanin extraction in Kenya and Tanzania, and marine seaweed protein isolates for aquaculture feed. Nasaru Naturals, an emerging disruptor, secured over USD 100,000 in seed funding in 2024 to scale Lake Natron spirulina cultivation and partnered with Victory Farms to trial algae-fortified tilapia feed, which also serves as a human supplement.

Technology adoption is increasingly distinguishing market leaders from laggards. Parry Nutraceuticals re-entered the European Union market in October 2024 with organic spirulina processed using its proprietary Tuymai filtration system, which removes heavy metals and microbial contaminants to meet European Pharmacopoeia standards. Chale Spirulina has addressed dispersibility issues in bakery applications by introducing pre-gelatinized flour, ensuring even distribution in dough without clumping. Meanwhile, the African Union established the Africa Food Safety Agency in February 2025 to harmonize microbiological and heavy-metal standards. This initiative is expected to reduce export rejections and facilitate cross-border trade of algae-based ingredients. However, ISO 22000 certification remains a significant barrier for smallholders, costing between USD 15,000 and USD 25,000 annually, yet it is essential for accessing premium export markets.

Players investing in advanced technologies, such as closed photobioreactor systems and pharmaceutical-grade processing, are well-positioned to capture the lucrative cosmetic-grade phycocyanin segment. This segment commands prices ranging from USD 200 to USD 400 per gram in European and North American markets. Coastal BioTech’s circular-economy model and Nasaru Naturals’ innovative partnerships highlight the potential for cost reduction and product diversification in the region. As the market evolves, companies that prioritize quality control, technological advancements, and compliance with international standards will likely gain a competitive edge in the Africa algae protein market.

Africa Algae Protein Industry Leaders

ALGO-RITME

Live Spirulina SA

Soaring Free Superfoods

SAFi Spirulina

Biodelta Neutraceuticals

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nasaru Naturals, a Kenyan spirulina producer, announced it is seeking USD 500,000 in funding to scale Lake Natron cultivation and expand its partnership with Victory Farms to trial algae-fortified tilapia feed that doubles as a co-product for human supplements. The company secured over USD 100,000 in seed funding in 2024 and is targeting sports-nutrition brands in Nairobi and Johannesburg.

- December 2024: Coastal BioTech secured USD 20 million to build a seaweed-to-biofertilizer plant in Zanzibar, Tanzania, converting carrageenan processing waste into organic soil amendments that sequester 2 metric tons of CO₂-equivalent per hectare. The facility is expected to commence operations in late 2025, targeting East African horticulture and aquaculture markets.

- April 2024: E2G FOOD, The Cares Organization, and Zimbabwe's National Food Corporation established the country's first spirulina microfarm at Gwebi Agricultural College in Harare. The facility targets smallholder training and local food fortification, with plans to distribute spirulina tablets to malnourished children in rural districts.

Africa Algae Protein Market Report Scope

The Africa Algae Protein Market is segmented by Type into Spirulina, Chlorella, and Other Types. The market is segmented by Application into Food & Beverages, Dietary Supplements, Pharmaceuticals, and Others. The report is also segmented by geography.

Source

| Freshwater Algae | Marine Algae | |

| Type | Spirulina | |

| Chlorella | ||

| Others | ||

| Application | Food and Beverages | Bakery |

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| Others | ||

| Supplements | Sport/Performance Nutrition | |

| Elderly Nutrition and Medical Nutrition | ||

| Animal Feed | ||

| Other Applications | ||

By Geography

| Nigeria |

| South Africa |

| Kenya |

| Tanzania |

| Ghana |

| Rest of Africa |

| Source | Freshwater Algae | Marine Algae | |

| Type | Spirulina | ||

| Chlorella | |||

| Others | |||

| Application | Food and Beverages | Bakery | |

| Dairy and Dairy Alternative Products | |||

| Meat/Poultry/Seafood and Meat Alternative Products | |||

| Others | |||

| Supplements | Sport/Performance Nutrition | ||

| Elderly Nutrition and Medical Nutrition | |||

| Animal Feed | |||

| Other Applications | |||

| By Geography | Nigeria | ||

| South Africa | |||

| Kenya | |||

| Tanzania | |||

| Ghana | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large will the Africa algae protein market be by 2031?

The market is projected to reach USD 29.27 million by 2031, expanding at a 5.12% CAGR between 2026 and 2031.

Which country leads in current output?

South Africa leads with 46.05% of 2025 revenue thanks to ISO-certified extraction plants and reliable export logistics.

What segment is growing fastest?

Supplements, especially sports-nutrition powders, are forecast to post a 6.88% CAGR through 2031.

Why are marine algae investments rising?

Programs such as Tanzania’s TASFAM fund large-scale seaweed farms that provide carrageenan, protein meal, and biofertilizer co-products, boosting investor appeal.

What limits small producers today?

High energy costs, fragmented regulations, and the USD 15,000-25,000 annual cost of ISO 22000 certification restrict smallholder export access.

How does algae protein support sustainability goals?

Spirulina emits 90% less carbon than beef protein and uses saline water, aligning with corporate emissions-reduction targets and African Union climate strategies.

Page last updated on: