Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

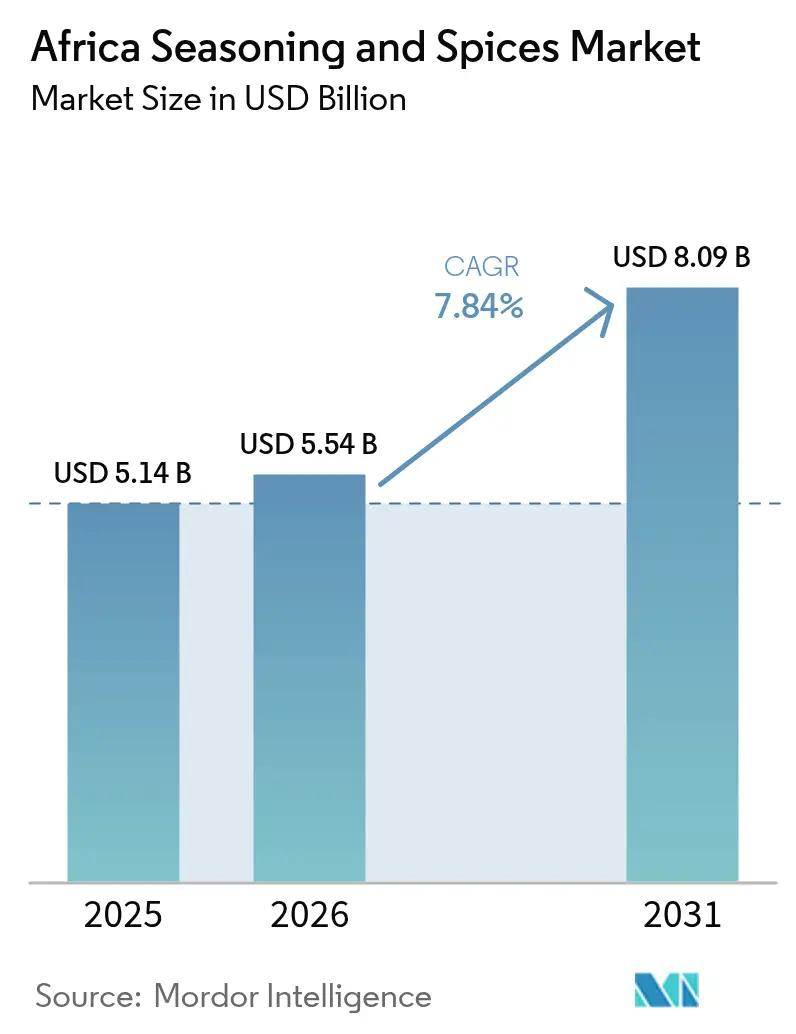

| Base Year Market Size (2025) | USD 5.14 Billion |

| Market Size (2026) | USD 5.54 Billion |

| Market Size (2031) | USD 8.09 Billion |

| Growth Rate (2026 - 2031) | 7.84% CAGR |

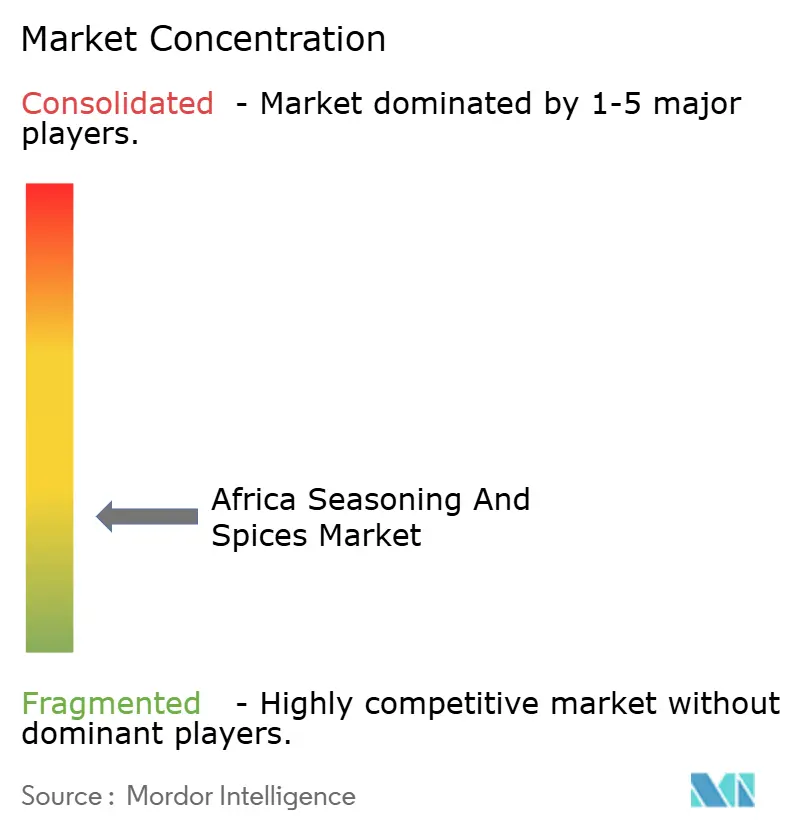

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Seasoning And Spices Market Analysis by Mordor Intelligence

The African seasonings and spices market size is expected to grow from USD 5.14 billion in 2025 to USD 5.54 billion in 2026 and is forecast to reach USD 8.09 billion by 2031 at 7.84% CAGR over 2026-2031. This outlook reflects how rapid urbanization, expanding food-processing capacity, and higher disposable incomes are reshaping daily diets and lifting per-capita consumption across the region. Quick-service restaurant roll-outs, stronger modern retail penetration, and product innovation anchored in indigenous flavor profiles are widening growth runways for the African spices and seasonings market, while climate-related supply shocks and logistics bottlenecks remain watch points. Multinational flavor houses are localizing production to meet just-in-time demand, and regional specialists are leveraging deep cultural knowledge to serve micro-markets with differentiated blends. Collectively, these forces validate the long-term potential of the Africana spices and seasonings market as a cornerstone of the continent’s emergent packaged-food ecosystem.

Key Report Takeaways

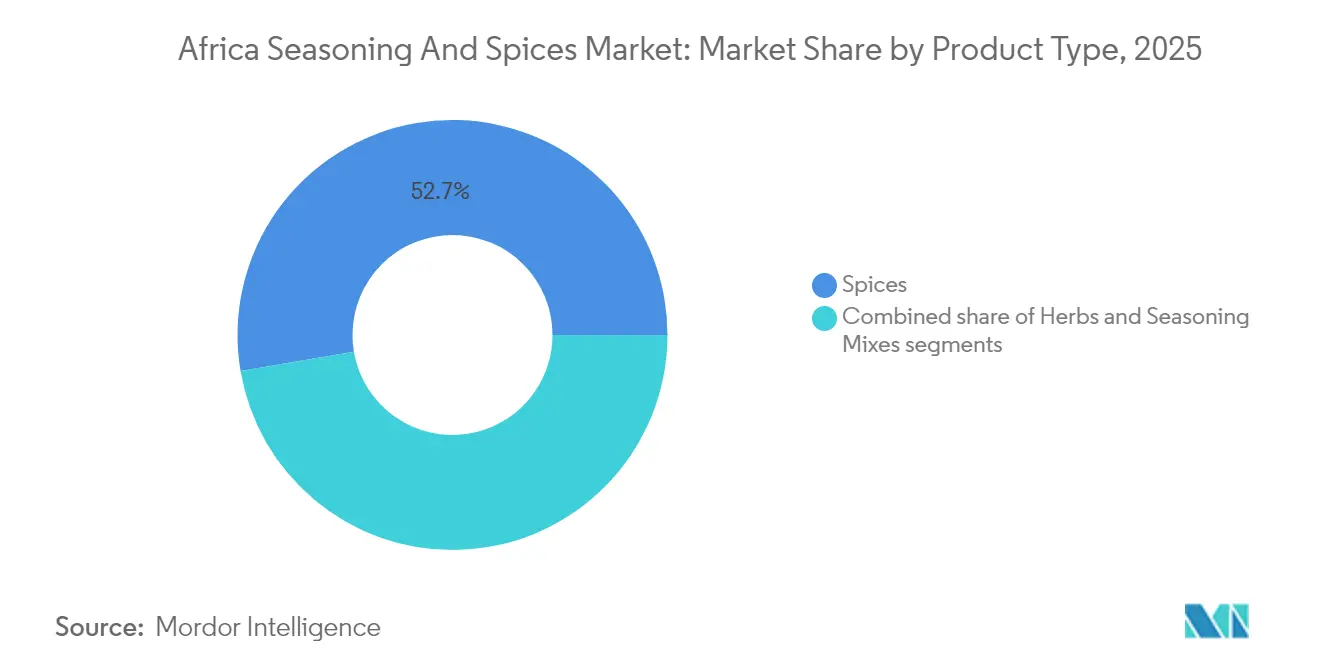

- By product type, spices dominated with 52.68% of the African spices and seasonings market share in 2025, while herbs are projected to post the fastest 9.12% CAGR through 2031.

- By form, ground and powder products captured 62.85% revenue share in 2025; whole spices are set to advance at a 9.35% CAGR over the same horizon.

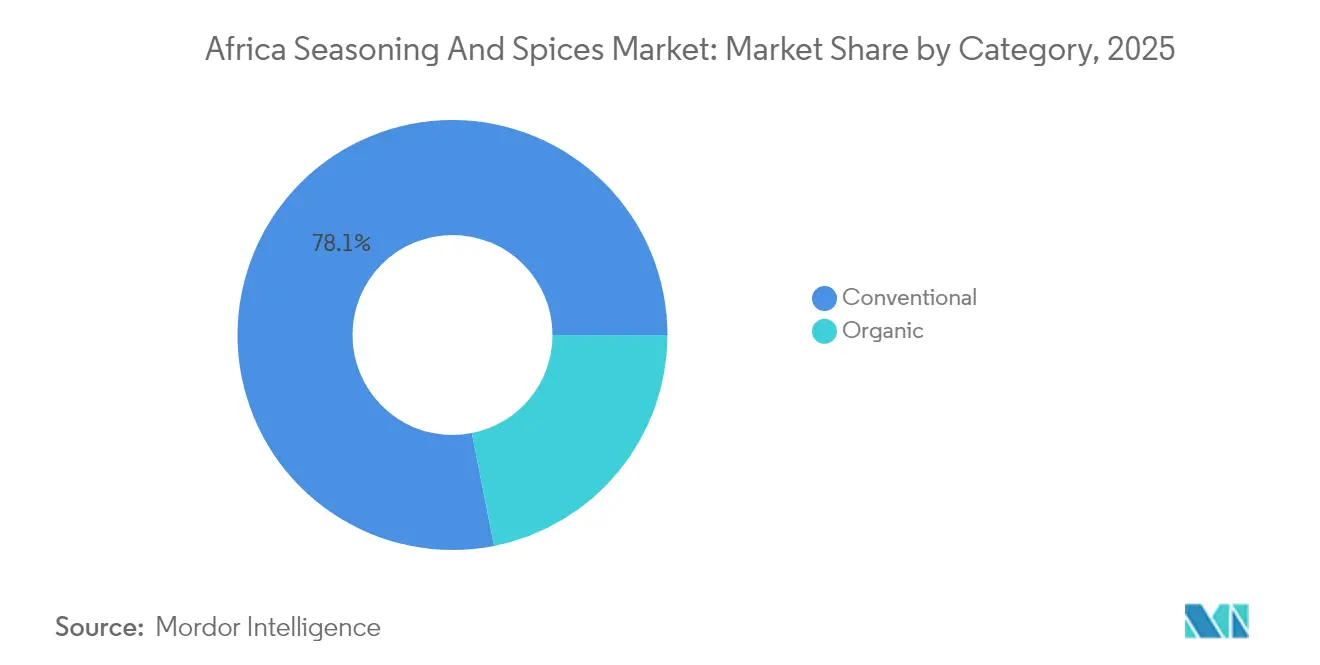

- By category, conventional offerings held 78.10% of the African spices and seasonings market size in 2025, yet organic lines are forecast to grow at a 9.62% CAGR to 2031.

- By end use, food processing accounted for 65.25% of 2025 demand, while retail channels are expanding at a 9.48% CAGR as modern trade networks deepen.

- By geography, Nigeria led with a 21.55% share in 2025, and Ethiopia is poised for the fastest 8.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Africa Seasoning And Spices Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for convenient processed foods | +2.1% | Nigeria, South Africa, Kenya, Ghana | Medium term (2-4 years) |

| Preference for natural and clean-label seasonings | +1.8% | South Africa, Morocco, Egypt, urban centers | Long term (≥ 4 years) |

| Growth in quick service restaurants and foodservice chain boost demand | +1.6% | Nigeria, South Africa, Kenya, urban markets | Short term (≤ 2 years) |

| Ethnic and cross-cultural culinary exploration | +1.2% | Global export markets, urban African centers | Medium term (2-4 years) |

| Innovation in flavor profiles and development of exotic/local spice blends | +0.9% | Morocco, Ethiopia, South Africa, Nigeria | Long term (≥ 4 years) |

| Government value-addition programs for spice crops | +0.7% | Ethiopia, Nigeria, Rwanda, Tanzania | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising demand for convenient processed foods

The seasoning and spices market demonstrates significant growth potential, driven by urbanization trends and an expanding workforce of 529.4 million people in 2024 in Africa (International Labour Organization), which are transforming food consumption patterns through increased demand for processed convenience foods [1]Source: International Labour Organization, "Statistics on Employment", ilostat.ilo.org. The growing urban and semi-urban workforce requires quick meal solutions, driving food processing companies to source standardized, shelf-stable spices and seasoning mixes for consistent mass production. Ghana's increased imports of food processing ingredients demonstrate the gap between domestic production capacity and market demand, creating opportunities for seasoning suppliers who can provide industrial quantities and custom blends. This shift extends beyond cities, as expanding retail networks enable rural populations to access packaged foods, increasing demand for familiar-tasting seasoning mixes. Food processors are developing local production facilities to reduce import reliance, sustaining demand for bulk spices and seasoning blends. Africa currently processes less than 25% of its food production (Partners in Food Solutions), indicating significant growth potential in value-added processing that requires industrial seasonings. Established companies like Kerry Group and Olam operate in Africa's market, supporting local supply chains and developing products that meet consumer demands for convenience and quality in the seasoning and spices segment. The combination of urbanization, workforce expansion, and developing retail infrastructure continues to drive growth in Africa's seasoning and spices market.

Preference for natural and clean-label seasonings

The increasing demand for ingredient transparency is significantly influencing product formulation strategies in various markets, particularly in urban areas where health-conscious consumers drive the growth of premium segments. Expanding South Africa's organic products market demonstrates a regional transition toward natural and minimally processed food ingredients. This shift enables premium pricing through clean-label positioning, supported by transparent sourcing and origin information. Multinational food companies are reformulating their products to comply with clean-label requirements, increasing the demand for natural spice extracts and organic-certified seasonings as alternatives to synthetic flavor enhancers. This development coincides with global flavor trends, as traditional spices such as berbere and ras el hanout receive international recognition for their natural complexity. The shift toward natural and clean-label seasonings combines health considerations with sustainability values, prompting companies like Givaudan and Kerry Group to invest in natural flavor technologies for both regional and global markets. This consumer preference transformation is reshaping the market through enhanced ingredient transparency, product authenticity, and natural formulations, contributing to market growth and premium product development.

Growth in quick service restaurants and foodservice chain boost demand

The expansion of quick service restaurants (QSRs) is driving demand for standardized seasoning solutions that deliver consistent flavor experiences across multiple locations. Galito's piri-piri growth in South Africa demonstrates how regional QSR chains use distinctive spice profiles to establish brand identity while maintaining operational efficiency through standardized seasoning systems. The QSR sector's growth is supported by increasing disposable incomes and changing lifestyle patterns that favor dining out and food delivery, particularly among urban millennials and working professionals. KFC's presence of over 1,400 outlets by 2024 highlights the significant scale of QSR penetration in the region [2]Source: KFC Corporation, "Our Company - Where We Dish It Up", global.kfc.com. Seasoning suppliers must provide technical expertise in product development, ensure supply chain reliability, and develop cost-effective formulations that preserve profit margins while delivering authentic flavors. This demand includes local restaurant concepts expanding across cities, creating opportunities for regional spice suppliers to develop seasoning blends suited to local preferences. The expanding QSR presence complements overall foodservice growth, enhanced by digital ordering and delivery platforms, meeting consumer demand for quick, flavorful meals. These trends increase the consumption of bulk ingredients and custom blends essential for QSR and foodservice chain operations.

Ethnic and cross-cultural culinary exploration

The market demonstrates robust growth potential driven by increasing global recognition of traditional spice blends and seasonings, as food manufacturers incorporate these flavors into their product lines. According to Spices, Inc.'s 2025 Flavor Report, African spices are a leading trend, with increased consumer interest in traditional blends such as berbere, chakalaka, and mitmita, which provide complex flavor profiles. This trend enables producers to serve both domestic markets seeking traditional flavors and international markets interested in new taste experiences. Urban centers demonstrate significant cross-cultural culinary fusion, where diverse communities demand varied spice profiles, expanding opportunities for specialty importers and local producers with diverse ingredient portfolios. In the foodservice sector, chefs integrate traditional spice techniques into modern dishes, increasing demand for premium, traceable spice ingredients that enable innovation while maintaining authenticity. The increasing global and regional appreciation strengthens the market by expanding export opportunities and fostering local culinary innovation, establishing these spices as an important component in the global flavor market.

Restraints Impact Analysis of Africa Seasoning And Spices Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fluctuating raw material prices, especially due to climate and weather impacts | -1.4% | West Africa, East Africa, drought-prone regions | Short term (≤ 2 years) |

| Informal and fragmented market structure, impacting quality traceability | -0.9% | Nigeria, Ghana, Kenya, smallholder regions | Medium term (2-4 years) |

| Inconsistent supply chains and infrastructure challenges for distribution | -0.8% | Rural Africa, landlocked countries, remote regions | Medium term (2-4 years) |

| Issues with quality control and authenticity for small-scale producers | -0.6% | Ethiopia, Kenya, Ghana, smallholder farming areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Fluctuating raw material prices, especially due to climate and weather impacts

Climate variability is driving unprecedented volatility in agricultural production, disrupting traditional growing seasons and impacting the quality consistency critical for the seasoning and spices market. In Nigeria, irregular rainfall and temperature fluctuations threaten chili pepper yields and capsaicin levels, compelling processors to diversify sourcing regions to meet product standards. Madagascar’s vanilla production, though outside the core spices category, exemplifies how climate impacts can ripple across aromatic crops, influencing broader supply chains. West African ginger farmers face similar challenges from water stress and soil degradation, forcing adaptation in cultivation practices to sustain quality and yield. These fluctuations increase raw material price instability, exerting margin pressure on food processors and seasoning manufacturers, who often must resort to reformulating products to balance cost control with quality. This balancing act risks inconsistencies in product flavor and consumer acceptance, presenting ongoing challenges for established companies like Kerry Group that operate across the African seasoning market. The dynamic underscores the urgency for climate-resilient agricultural strategies and supply chain innovations to maintain the growth and reliability of Africa’s seasoning and spices sector in an increasingly volatile environment.

Informal and fragmented market structure, impacting quality traceability

Informal trading channels remain prevalent across spice markets, significantly undermining efforts to ensure quality traceability and limiting producers' access to premium export markets and the formal food processing sector. For instance, in Kenya’s spice industry, smallholder producers without GlobalGAP certification struggle to meet international quality and traceability standards. Fragmented production systems face persistent issues such as inadequate post-harvest handling, poor storage, and insufficient documentation, all of which are critical for maintaining consistent product quality and complying with food safety regulations. These inefficiencies disrupt supply chains, making it challenging for buyers to secure reliable sourcing with consistent quality, thereby restricting market access for small-scale producers. Furthermore, the informal market structure delays the adoption of advanced technologies and knowledge transfer, both essential for improving production efficiency and product standards. These challenges perpetuate cycles of low productivity and constrain the overall growth potential of the seasoning and spices sector in Africa. Addressing these constraints through formalization and enhanced support for small producers is crucial to unlocking the market’s full potential and advancing quality standards.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Africa Seasoning And Spices Market Segment Analysis

By Product Type:

Spices Drive Volume While Herbs Accelerate GrowthIn 2025, spices hold a commanding 52.68% market share, highlighting their critical role in culinary traditions and food processing applications across the continent. Traditional spices such as pepper, turmeric, and cinnamon continue to experience strong demand from both local consumers and food manufacturers, who utilize these ingredients for their flavor and preservation properties. Herbs are emerging as the fastest-growing segment, with a projected 9.12% CAGR through 2031. This growth is driven by increasing consumer sophistication and a rising preference for complex flavor profiles that integrate traditional African herbs with international seasoning concepts. Salt and salt substitutes remain essential for preservation and flavor enhancement, particularly in food processing, where sodium reduction initiatives are creating opportunities for innovative salt substitute formulations.

The herbs category is benefiting from the growing recognition of traditional African medicinal and culinary herbs like moringa and baobab, which are gaining traction in both domestic and export markets due to their nutritional properties and unique flavor contributions. Seasoning mixes represent a strategic growth opportunity, addressing the demand for convenient solutions that deliver consistent flavor profiles without requiring extensive ingredient knowledge or preparation time. Innovation in flavor profiles is particularly evident in the herbs segment, where producers are developing proprietary blends that combine traditional African herbs with international flavor trends to create differentiated products for premium market segments. The InnoFoodAfrica project's work on underutilized African crops demonstrates how traditional ingredients can be processed into modern food applications, supporting growth in the herbs and specialty seasonings categories.

By Form:

Ground Products Dominate as Whole Spices Gain Premium TractionGround and powder forms dominate the market in 2025, holding a 62.85% share. This trend reflects consumer preferences for convenience and the food processing industry's demand for standardized ingredients that seamlessly integrate into manufacturing. Ground products lead due to their versatility in both household cooking and industrial applications, where consistent particle size and flavor release are critical for maintaining product quality. Meanwhile, whole spices are projected to grow at a 9.35% CAGR through 2031, driven by premium market segments that emphasize authenticity, freshness, and the ability to customize grinding and flavor intensity for specific culinary needs.

Urban consumers, equipped with grinding tools and access to premium retail channels, are becoming increasingly discerning. They are recognizing the flavor quality differences between freshly ground and pre-ground products. Additionally, formats such as crushed, flakes, and paste cater to specialized applications in foodservice and ethnic cuisine, where texture and flavor nuances are essential. Food processing companies are increasingly requesting customized grinding specifications to optimize flavor release and shelf stability for their products. This shift creates opportunities for suppliers who can provide technical expertise and flexible processing capabilities. Moreover, the growing trend of artisanal and craft food products supports the whole spice market, where visual appeal and perceived authenticity play significant roles in premium branding strategies.

By Category:

Conventional Dominance Faces Organic ChallengeConventional products hold a significant 78.10% share of the market in 2025, driven by established supply chains, competitive pricing, and widespread availability across retail and foodservice sectors. This segment effectively addresses the needs of price-sensitive consumers and large-scale food processors, focusing on cost efficiency and supply reliability. In contrast, organic products are experiencing strong growth, with a 9.62% CAGR projected through 2031. This growth is attributed to increasing demand from health-conscious urban consumers and export markets, where organic certification enables premium pricing and compliance with stringent import standards.

International demand, particularly from European buyers, is a key driver for the organic segment. These buyers prioritize sustainable sourcing and adherence to environmental regulations, such as the EU's deforestation rules set to take effect in 2025. South Africa's expanding organic market highlights the potential for premium positioning when supported by effective certification systems and consumer education initiatives. Additionally, organic certification is enhancing agricultural practices and improving supply chain traceability, which raises overall market quality standards, including for conventional products. The certification process also creates entry barriers, reducing competition and allowing producers who meet regulatory requirements to secure premium pricing.

By End Use:

Food Processing Leads While Retail Channels AccelerateFood processing applications account for 65.25% of the market share in 2025, highlighting their critical role in driving demand for bulk spices and seasoning ingredients. Food manufacturers prioritize consistent quality, competitive pricing, and reliable supply chains to support production planning and inventory management for both domestic and export-oriented products. The processing segment benefits from ongoing industrialization trends and government initiatives, such as Nigeria's Special Agro-Industrial Processing Zones program, which aims to enhance local value-added manufacturing capabilities. Within food processing, bakery and confectionery applications lead in volume, while meat and seafood processing generate demand for specialized seasoning blends that improve flavor and extend shelf life.

Retail channels are projected to grow at a 9.48% CAGR through 2031, driven by the expansion of modern trade formats and increasing consumer purchasing power in urban markets. Supermarkets and hypermarkets are becoming vital distribution channels, offering broader product assortments and quality assurance that attract middle-class consumers seeking branded spice products. Online retail stores represent a growing opportunity, particularly for specialty and premium products that benefit from detailed product information and customer reviews, which influence purchase decisions. The retail segment's growth reflects evolving consumer preferences for branded products and convenience shopping, creating opportunities for suppliers to leverage attractive packaging, strategic brand positioning, and partnerships with modern retail formats.

Geography Analysis

Nigeria Seasoning And Spices Market

Nigeria's market dominance is driven by its large population, expanding food processing infrastructure, and strategic investments in agricultural value chains that cater to both domestic consumption and regional exports. In 2025, the country holds a 21.55% market share, reflecting consistent demand growth fueled by urbanization and rising disposable incomes, which have encouraged the adoption of premium products across diverse consumer segments. Government initiatives supporting ginger production and processing highlight a commitment to agricultural value addition. However, inefficiencies in the supply chain and informal market structures continue to impede quality standardization. Security challenges in agricultural regions further threaten supply chain stability, necessitating diversified sourcing strategies and investments in rural infrastructure to sustain production growth.

Ethiopia Seasoning And Spices Market

Ethiopia's projected 8.32% CAGR through 2031 positions it as the fastest-growing market in the region. This growth is supported by government initiatives aimed at increasing spice exports, with ambitious targets that could reshape the country's agricultural export profile. Ethiopia's traditional expertise in producing berbere and other indigenous spice blends provides a competitive advantage in international markets, where authentic Ethiopian flavors command premium pricing and benefit from differentiated positioning strategies. The country's focus on agricultural value addition aligns with broader economic objectives, including export diversification and rural income growth through improved farming and processing practices. While power supply issues and infrastructure limitations have constrained food processing expansion, ongoing investments in industrial zones and utility infrastructure are systematically addressing these challenges.

Africa Seasoning And Spices Market

South Africa, Morocco, Kenya, and Ghana present diverse growth opportunities, each leveraging unique competitive advantages and market strategies to capture specific segments within the broader regional market. South Africa's expansion in the organic products segment highlights the potential for premium positioning, supported by certification systems and consumer education initiatives that emphasize quality and health benefits. Morocco's expertise in the spice trade and its strategic geographic location create export opportunities to European and Middle Eastern markets. Kenya's focus on quality certification and GlobalGAP compliance addresses barriers to international market access. Ghana's growth in food processing ingredient imports in 2023 reflects an expanding manufacturing base and increasing demand for value-added ingredients to support local production. The implementation of AfCFTA across 37 participating countries by October 2024 offers tariff reduction opportunities, fostering intra-African trade growth and regional supply chain integration .

Competitive Landscape

Fragmented competition in the market creates opportunities for both multinational corporations and regional specialists to secure market share through tailored strategies. Major players like McCormick, Kerry Group, and Givaudan are making significant investments in regional production and technical expertise centers. For instance, Kerry Group's April 2025 inauguration of its inaugural taste manufacturing facility in Rwanda. This move underscores a trend of merging global capabilities with insights into local markets, aiming to efficiently cater to East African food and beverage producers. Such a localized strategy not only streamlines supply chain costs and complexities but also fosters the development of products attuned to regional palates.

Regional players, armed with a profound grasp of local flavor inclinations, robust distribution networks, and inherent cost benefits, adeptly navigate price-sensitive segments. By delivering authentic flavor profiles deeply intertwined with local cultures, these companies cultivate brand loyalty. This expertise not only sets them apart in a competitive landscape but also allows them to cater to the diverse culinary traditions across Africa. Their swift adaptability and cultural alignment bolster their position in a market that's becoming more discerning about quality, even as it remains sensitive to price.

There's a wealth of untapped potential in areas like organic certification, traceability systems, and enhanced processing capabilities. These can cater to both premium domestic consumers and export markets that demand high-quality standards. While the uptake of digital traceability and quality management systems has been modest, it signals a ripe opportunity for tech-savvy entrants. Moreover, niche players are adopting vertical integration strategies, allowing them to harness value at various supply chain stages while staying agile to consumer preferences. In essence, the fragmented landscape of the market fosters a vibrant competitive arena, where diverse players can flourish by harnessing technology, innovation, and localized expertise.

Africa Seasoning And Spices Industry Leaders

-

McCormick & Company Inc.

-

Freddy Hirsch Group

-

Kerry Group Plc

-

Givaudan S.A.

-

Olam Group

- *Disclaimer: Major Players sorted in no particular order

Africa Seasoning And Spices Market Companies Covered in this Report

- McCormick & Company Inc.

- Kerry Group Plc

- Givaudan S.A.

- Freddy Hirsch Group

- Deli-Spices (Pty) Ltd

- Natpro Spicenet (Pty) Ltd

- Olam Group

- Exim International (Pty) Ltd

- Golden Spices

- Cape Spice Company

- MANE SA

- Robertsons

- Organic Spices Inc

- Tiger Foods Limited

- Sensient Technologies Corporation

- Griffith Foods

- JayNana Foods Limited

- Rhodes Food Group

- Uto Spices and Marinades Ltd

- Mr Spices

Recent Industry Developments in Africa Seasoning And Spices Market

- April 2025: Kerry Group inaugurated its first taste manufacturing facility in Rwanda, East Africa, to support local food and beverage producers. This investment was a key step in Kerry's plan to channel EUR 1 billion into emerging markets, demonstrating its commitment to driving growth and sustainability in the global food sector. Additionally, this facility reflected Kerry's strategy of establishing manufacturing and research hubs near Africa's high-growth markets.

- November 2024: GBfoods launched its signature chicken seasoning, introducing a distinctive blend of flavors to Nigerian kitchens. This seasoning cube combines over eighty meticulously selected local spices and herbs, each chosen to reflect the essence of being "full of nature" and "full of flavor," a quality highly valued by consumers.

- September 2024: Nigerian startup Mamae Foods, recognized for its diverse spice offerings, secured a USD 100,000 investment from Eastside Ventures/Ghost Partners Fund, a local impact investor. Mamae Foods’ product portfolio included Jollof Rice Spice Mix, Pepper Soup Spice Mix, Masala Curry, Native Spice Blend, and an All-Purpose Spice Mix. With a focus on locally sourced ingredients, the company planned to utilize this investment for product extensions and to increase its manufacturing capacity to 20 tonnes daily.

Africa Seasoning And Spices Market Report Scope

Spices and seasonings are widely used to add flavor, aroma, color, and taste to food & beverages and sometimes as preservatives or antibacterial agents. Manufacturers use these attributes of spices and seasonings to improve their product quality and taste and increase their shelf life.

The African seasoning and spices market is segmented by product type and application. Based on product type, the market has been segmented into salt and salt substitutes, herbs, and spices. Furthermore, herbs are segmented into thyme, basil, oregano, parsley, and other herbs. Likewise, spices are further segmented into pepper, cardamom, cinnamon, clove, nutmeg, and other spices. By application, the market has been segmented into bakery and confectionery, soup, meat and seafood, sauce, salad, dressings, savory snacks, and other applications.

For each segment, the market sizing and forecasts have been done based on value (in USD million).

Segmentation Overview

By Product Type

| Salt and Salt Substitutes | |

| Herbs | Thyme |

| Basil | |

| Oregano | |

| Parsley | |

| Other Herbs | |

| Spices | Pepper |

| Cardamom | |

| Cinnamon | |

| Clove | |

| Nutmeg | |

| Turmeric | |

| Other Spices | |

| Seasoning Mixes |

By Form

| Whole |

| Ground/Powder |

| Others (crushed, flakes, paste, etc.) |

By Category

| Conventional |

| Organic |

By End Use

| Food Processing | Bakery and Confectionery |

| Soups, Noodles and Pasta | |

| Meat and Seafood | |

| Sauces, Salads and Dressings | |

| Savory Snacks | |

| Other Applications | |

| Foodservice/HoReCa | |

| Retail | Supermarkets/Hypermarkets |

| Convenience Stores | |

| Online Retail Stores | |

| Other Distribution Channel |

By Country

| South Africa |

| Nigeria |

| Egypt |

| Morocco |

| Kenya |

| Ethiopia |

| Ghana |

| Rest of Africa |

| By Product Type | Salt and Salt Substitutes | |

| Herbs | Thyme | |

| Basil | ||

| Oregano | ||

| Parsley | ||

| Other Herbs | ||

| Spices | Pepper | |

| Cardamom | ||

| Cinnamon | ||

| Clove | ||

| Nutmeg | ||

| Turmeric | ||

| Other Spices | ||

| Seasoning Mixes | ||

| By Form | Whole | |

| Ground/Powder | ||

| Others (crushed, flakes, paste, etc.) | ||

| By Category | Conventional | |

| Organic | ||

| By End Use | Food Processing | Bakery and Confectionery |

| Soups, Noodles and Pasta | ||

| Meat and Seafood | ||

| Sauces, Salads and Dressings | ||

| Savory Snacks | ||

| Other Applications | ||

| Foodservice/HoReCa | ||

| Retail | Supermarkets/Hypermarkets | |

| Convenience Stores | ||

| Online Retail Stores | ||

| Other Distribution Channel | ||

| By Country | South Africa | |

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Kenya | ||

| Ethiopia | ||

| Ghana | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the current value of the Africa spices and seasonings market?

The market is valued at USD 5.54 billion in 2026.

How fast is demand for organic seasonings growing across Africa?

Certified-organic products are forecast to register a 9.62% CAGR through 2031.

Which country leads regional consumption?

Nigeria holds 21.55% of 2025 regional revenue.

Which product segment is expanding the quickest?

Herbs are pacing a 9.12% CAGR to 2031.

Page last updated on: