Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

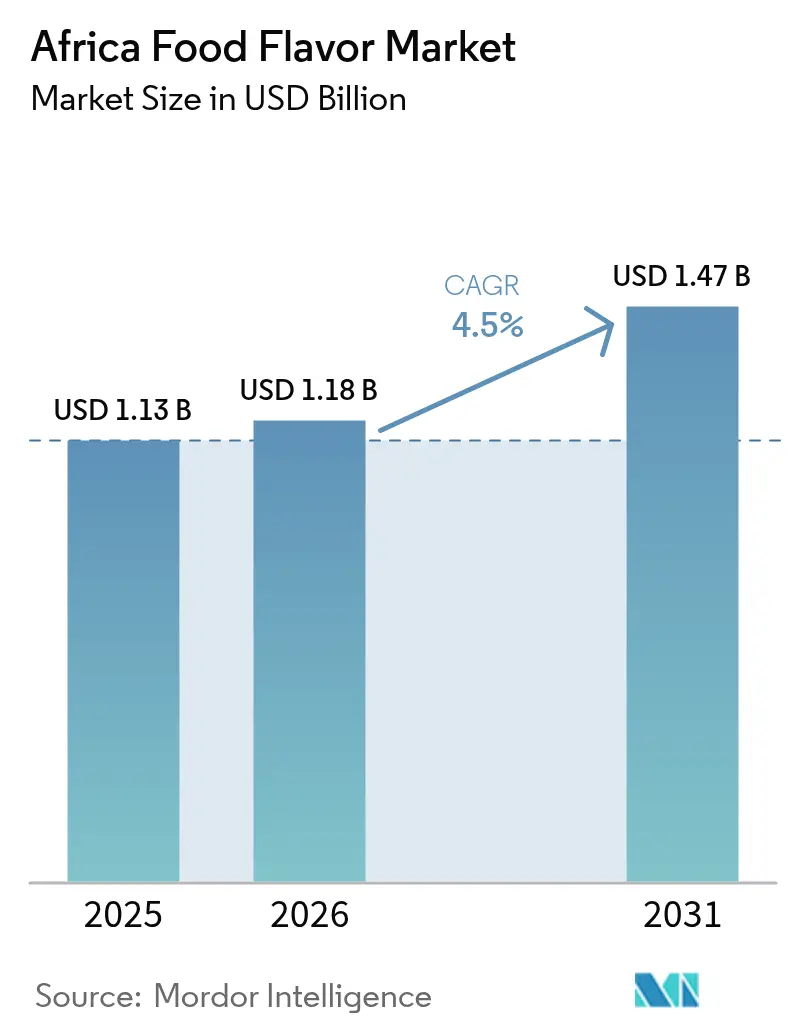

| Base Year Market Size (2025) | USD 1.13 Billion |

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.47 Billion |

| Growth Rate (2026 - 2031) | 4.50% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Africa Food Flavor Market Analysis by Mordor Intelligence

The Africa food flavor market size was valued at USD 1.13 billion in 2025 and estimated to grow from USD 1.18 billion in 2026 to reach USD 1.47 billion by 2031, at a CAGR of 4.50% during the forecast period (2026-2031). This growth is fueled by the continent's burgeoning food-processing sector, increasing urban incomes, and a notable shift towards convenience meals that utilize specialized flavor systems. The market is expanding, driven by a rising appetite for natural clean-label ingredients, a surge in ready-to-drink (RTD) beverages, and heightened consumer interest in international cuisines. While cost-sensitive manufacturers often resort to synthetic options as a buffer against currency fluctuations, a strong marketing push around wellness is driving a swift uptick in demand for natural extracts. The competitive landscape is moderately intense, with multinationals forging deeper local partnerships and regional players capitalizing on niche opportunities in major cities.

Key Report Takeaways

- By type, synthetic flavors led with 70.88% of the Africa food flavor market share in 2025, whereas natural flavors are forecast to advance at a 6.48% CAGR to 2031.

- By form, liquid variants held 66.95% of the Africa food flavor market size in 2025, while powder formats are projected to rise at a 5.47% CAGR through 2031.

- By application, beverages captured a 43.29% share of the Africa food flavor market size in 2025, and the same segment is expected to expand at a 5.78% CAGR through 2031.

- By geography, South Africa accounted for 48.10% of revenue in 2025, whereas Egypt is poised for the fastest climb at a 5.29% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Market Trends and Insights

Drivers Impact Analysis of Africa Food Flavor Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for natural clean-label flavors | +1.2% | Global, with strongest adoption in South Africa and Kenya | Medium term (2-4 years) |

| Growth of packaged and convenience-food sector | +0.8% | Nigeria, Egypt, South Africa core markets | Short term (≤ 2 years) |

| Expansion of flavored RTD beverages and energy drinks | +1.0% | Nigeria leads, spill-over to Kenya and Ghana | Short term (≤ 2 years) |

| Consumer preference for international and ethnic cuisines | +0.6% | Urban centers across South Africa, Nigeria, Kenya | Medium term (2-4 years) |

| Sustainability and upcycled ingredients in flavor manufacturing | +0.4% | South Africa and Kenya early adopters | Long term (≥ 4 years) |

| Flavor innovation in alcoholic beverages and RTD cocktails | +0.5% | South Africa, Nigeria, Kenya mature markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Natural Clean-Label Flavors

Across Africa's urban markets, consumers are increasingly demanding natural flavor solutions, driven by a heightened awareness of ingredient transparency. This shift mirrors a broader trend towards health consciousness, prompting manufacturers to reformulate products in line with clean-label expectations. Symrise, underscoring the industry's commitment, highlights its strategic investment in sourcing natural raw materials, boasting a 95% sustainability rate for its strategic biological materials[1]Source: Symrise AG, “Sustainability Report 2025,” symrise.com. This trend is especially pronounced in South Africa's established retail landscape, where consumers are not only scrutinizing ingredient lists but also gravitating towards products that resonate with wellness ideals.

Consumer Preference for International and Ethnic Cuisines

Food-service outlets in Johannesburg and Lagos now serve up Korean barbecue, Mexican tacos, and Thai curries, introducing diners to flavors like chili, lemongrass, and chipotle. In response, packaged-food brands are rolling out fusion crisps, spicy mayonnaise, and ramen seasonings, all tailored to local taste preferences. This trend is bolstering the African food flavor market, as each new fusion SKU demands custom formulation and sensory testing. Givaudan reports that its culinary centers in South Africa are conducting co-creation workshops, where chefs and technologists fine-tune spice intensity to suit West African tastes. This collaboration results in an expanded SKU count, boosting volumes for both natural and synthetic flavor bases.

Sustainability and Upcycled Ingredients in Flavor Manufacturing

Processors are reducing their carbon footprints by replacing petrochemical solvents with bio-fermented carriers derived from sugarcane bagasse. Upcycled fruit pulp is being transformed into citrus terpenes, which not only reduce raw material costs but also provide marketable eco-claims. Kenyan start-ups, like Green Juju, are turning pineapple cores into flavor precursors, securing premium contracts with beverage companies. As European importers increasingly demand lifecycle data, African suppliers are now monitoring Scope 3 emissions to ensure consistent trade flows. While circular-economy sourcing offers promise for supply security, its current modest volumes lead to only an incremental impact on Africa's food flavor market.

Flavor Innovation in Alcoholic Beverages and RTD Cocktails

In Cape Town and Lagos, craft distillers unveil canned gin-tonics and rum punches infused with trendy botanicals like rooibos, baobab, and hibiscus. These new offerings utilize micro-dose flavor systems, ensuring the spirits' core identity remains intact. With premiumization trends emphasizing transparency in ABV labeling, off-notes become more pronounced, broadening the demand for high-purity extracts. Heineken's acquisition of Distell in South Africa has paved the way for flavored beers to find new distribution channels, amplifying the demand for tropical esters and citrus peel oils. In response to rising alcohol taxes, brands are shifting focus to lower-ABV spritzers, prioritizing fruity flavor profiles over ethanol potency, thus ensuring continued growth in flavor demand.

Restraints Impact Analysis of Africa Food Flavor Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented cold-chain and logistics infrastructure | -0.7% | Nigeria, Kenya, Rest of Africa most affected | Long term (≥ 4 years) |

| Volatile currency and import-dependence for key inputs | -0.9% | Nigeria, Ghana, Kenya primary impact zones | Short term (≤ 2 years) |

| Changing regulatory landscape | -0.3% | Continental scope with varying national implementation | Medium term (2-4 years) |

| Counterfeit and low-quality flavor products | -0.4% | Nigeria, Kenya, Rest of Africa concentrated risk | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Cold-Chain and Logistics Infrastructure

Infrastructure limitations hinder market growth in Nigeria, where inadequate cold storage and transportation networks lead to increased spoilage rates and restrict product distribution. The ColdHubs initiative in Nigeria, with its 58 cold rooms preventing the loss of 13,800 kg of food, showcases innovative solutions but underscores the significant infrastructure gaps. This fragmentation is especially detrimental to natural flavor ingredients, which need temperature-controlled storage and transport. As a result, manufacturers are often compelled to turn to synthetic alternatives or bear the brunt of elevated costs for specialized logistics.

Volatile Currency and Import-Dependence for Key Inputs

Flavor manufacturers grapple with rising costs due to currency instability. A stark example is the Nigerian naira's plunge from 430 NGN/USD to 1,700 NGN/USD between October 2022 and 2024, highlighting regional currency pressures, as reported by MIT Sloan[2]Source: MIT Sloan, “Currency Conundrums: Volatile African Exchange Rates and What Can Be Done,” mitsloan.mit.edu. These challenges are intensified by the manufacturers' reliance on imported specialized flavor ingredients, leading to unpredictable input costs. Such volatility complicates pricing strategies and margin management. Further underscoring the continent-wide nature of this issue, Ghana's cedi saw a 54% drop in 2022, while Kenya's currency depreciated by 15% in 2023.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Africa Food Flavor Market Segment Analysis

By Type:

Synthetic Dominance Amid Natural GrowthIn 2025, synthetic flavors command a dominant 70.88% market share, thanks to their cost advantages and reliable supply chains, even in unpredictable economic climates. While natural flavors hold a smaller slice of the market, they are the fastest-growing segment, expanding at a 6.48% CAGR through 2031, driven by a surge in consumer health awareness and a preference for clean labels. Nature-identical flavoring finds a niche, balancing cost-effectiveness with a nod to consumers' desire for natural-sounding ingredients.

The synthetic segment's stronghold is anchored in price stability and reliable availability. These factors are paramount for manufacturers, especially in currency-volatile regions where import costs can swing widely. While natural flavors grapple with supply chain hurdles, they are reaping rewards from premiumization trends. This is especially evident in South Africa's established market, where consumers are willing to pay a premium for perceived health advantages. Moreover, as regulatory bodies like NAFDAC in Nigeria and SAHPRA in South Africa tighten their scrutiny on flavor additives, it could hasten the industry's pivot towards natural alternatives, especially as compliance standards evolve

By Application:

Beverages Lead Market ExpansionIn 2025, the beverages segment not only leads with a commanding market share of 43.29% but also boasts the highest growth rate at 5.78% CAGR. This surge is fueled by a booming demand for energy drinks and innovative ready-to-drink (RTD) cocktails. Following closely, the dairy segment reaps benefits from urbanization and increasing disposable incomes, bolstering the consumption of premium dairy products. While the bakery and confectionery sectors enjoy steady growth, savory snacks are emerging as a high-potential category, reflecting shifting consumption patterns.

As African consumers warm up to processed meat products, meat applications show promise, albeit still trailing behind traditional categories. The beverages segment's dominance underscores a shift in consumption trends, with energy drinks, as highlighted by Kerry Group, set to expand at a robust 10.06% CAGR across the continent. Meanwhile, other applications like sauces and seasonings are riding the wave of international cuisine popularity, further propelled by the growth of quick-service restaurant chains in major African cities.

By Form:

Liquid Formats Dominate ProcessingIn 2025, liquid flavors command a dominant 66.95% share of the market, underscoring their adaptability in beverage applications and their seamless integration into large-scale manufacturing. While currently holding a smaller share, powder formats are on a rapid ascent, boasting a 5.47% CAGR growth rate projected through 2031. This surge is attributed to their shelf-stability benefits and lower transportation costs. Meanwhile, other variants, such as encapsulated and spray-dried forms, cater to niche applications, leveraging advantages like controlled release and extended shelf life.

The liquid segment's stronghold mirrors the beverage category's market leadership. Liquid flavors not only meld effortlessly into drink formulations but also ensure precise dosing. On the other hand, powder formats are gaining momentum in regions grappling with infrastructure hurdles. Their benefits include the elimination of cold-chain dependencies and a marked reduction in spoilage risks during transit. With an eye on the future, Symrise is making strategic moves. Their foray into spray-drying technologies and plant protein applications positions them at the forefront of the powder format boom. Moreover, their emphasis on energy-efficient processing methods underscores a commitment to addressing sustainability challenges.

Geography Analysis

South Africa Food Flavor Market

In 2025, South Africa commands a dominant 48.10% market share, capitalizing on its robust food processing infrastructure and the regulatory oversight of SAHPRA. The nation's well-established retail sector is witnessing a trend towards premiumization, as consumers increasingly opt for and are willing to pay a premium for natural and organic flavor solutions. Illustrating this industrial momentum, Tiger Brands has invested R300 million in a new peanut butter manufacturing facility. Furthermore, the government is signaling a strategic emphasis on value-added agricultural processing, evidenced by its backing of the essential oils industry through specialized sector reports.

Africa Food Flavor Market

Nigeria, despite grappling with infrastructure hurdles, is emerging as a high-growth market. This surge is fueled by significant foreign investments, notably JBS's USD 2.5 billion and Flour Mills Nigeria's USD 1 billion expansions. With a population of 250 million, Nigeria boasts a vast demand potential. NAFDAC's stringent measures against counterfeit products, highlighted by the seizure of N20.5 billion in fake drugs and adulterated tomato paste at Onne Port, underscore the agency's commitment to upholding food safety standards. However, the naira's steep plunge from 430 to 1,700 per USD between 2022 and 2024 has posed challenges, compelling manufacturers to rethink their supply chain strategies. Egypt is on track to be the fastest-growing market, projecting a 5.29% CAGR through 2031. This growth is largely attributed to government initiatives bolstering processed food exports. Egypt's prime location offers a gateway to both Middle Eastern and European markets. Coupled with urbanization and increasing disposable incomes, domestic demand is on the rise. Meanwhile, Kenya, despite facing economic challenges, is witnessing steady growth. The government's emphasis on agricultural value addition is paving the way for flavor companies to forge local sourcing partnerships. Across the Rest of Africa, markets are on diverse growth paths. Ghana is expanding its cocoa processing, Ethiopia is enhancing its coffee value chain, and each market presents distinct opportunities for flavor ingredient applications.

Competitive Landscape

In the Africa food flavor market, moderate consolidation is evident. Givaudan achieved a 20.9% like-for-like growth in the SAMEA territory by integrating global R&D with sensory panels based in Johannesburg. DSM-Firmenich, capitalizing on merger synergies, is bundling taste, texture, and nutrition solutions, thereby strengthening its relationships with producers in the dairy and baked-goods sectors. Kerry, leveraging insights from its Taste and Nutrition network, is co-designing beverage concepts that resonate with the continent’s burgeoning energy-drink market. While established players utilize their scale for consistent supply and adept regulatory navigation, local specialists like Teubes are carving out niches by using indigenous botanicals to craft bourbon-vanilla analogs.

Technology adoption is reshaping competitive dynamics. IFF is investing USD 70 million in a Cedar Rapids line, producing TAURA fruit pieces and advancing digital twin modeling for enhanced process efficiency[4]Source: NAFDAC, “Guidelines for Registration of Food Additives 2024,” nafdac.gov.ng. Even though this U.S.-based plant primarily serves African snack exporters seeking natural fruit inclusions. Symrise is infusing artificial intelligence into its flavor creation process, accelerating formulation cycles and reducing trial batches by 20%. Meanwhile, regional start-ups like AfroFlavor Labs are leveraging machine learning to tailor chili intensity to specific country palates, underscoring a grassroots embrace of technology.

Currency fluctuations are squeezing gross margins, prompting strategic hedging maneuvers. Multinational firms are entering into multi-year contracts for vanilla and citrus, pegged to stable currencies, while local players are securing forward purchases in dollars. Sustainability credentials have become pivotal in tender evaluations; suppliers failing to substantiate their Scope 3 footprints face potential exclusion from retailer assessments. As technology, sourcing strategies, and compliance agility intertwine, they will shape the hierarchy in the African food flavor market.

Africa Food Flavor Industry Leaders

Koninklijke DSM NV

Kerry Group PLC

Teubes oils out of Africa

Givaudan

Corbion Purac

- *Disclaimer: Major Players sorted in no particular order

Africa Food Flavor Market Companies Covered in this Report

- Givaudan

- DSM-Firmenich

- Kerry Group

- Symrise

- IFF

- Sensient Technologies

- Archer Daniels Midland

- BASF

- Corbion

- Takasago

- Teubes (South Africa)

- FlavourCraft (Kenya)

- Treatt

- Olam Food Ingredients

- AfroFlavor Labs (Nigeria)

- Mane SA

- Robertet

- Manifatture Arditi

- Sensient South Africa

- Flavorchem (Africa)

Recent Industry Developments in Africa Food Flavor Market

- June 2025: International Flavors & Fragrances (IFF) participated in the Africa Food Show in Cape Town, South Africa. The company hosted expert sessions on food and beverage innovation, focusing on consumer trends in Africa.

- March 2025: Namibia implemented the Livestock and Livestock Products Amendment Act, designating dairy products, poultry, and related items as controlled products requiring import/export permits from the Livestock and Livestock Products Board, affecting food ingredient trade flows in the southern African region.

Africa Food Flavor Market Report Scope

The Africa food flavor market is segmented by type and application. Based on type, the market is segmented into the natural flavor, synthetic flavor, and nature-identical flavor. By application, the market is segmented into bakery, beverages, confectionery, dairy products, snacks, and other applications. This report also provides a regional analysis of the market studied.

Segmentation Overview

By Type

| Natural Flavor |

| Synthetic Flavor |

| Nature Identical Flavoring |

By Application

| Dairy |

| Bakery |

| Confectionery |

| Savory Snack |

| Meat |

| Beverages |

| Others |

By Form

| Powder |

| Liquid |

| Others |

By Geography

| South Africa |

| Nigeria |

| Kenya |

| Egypt |

| Rest of Africa |

| By Type | Natural Flavor |

| Synthetic Flavor | |

| Nature Identical Flavoring | |

| By Application | Dairy |

| Bakery | |

| Confectionery | |

| Savory Snack | |

| Meat | |

| Beverages | |

| Others | |

| By Form | Powder |

| Liquid | |

| Others | |

| By Geography | South Africa |

| Nigeria | |

| Kenya | |

| Egypt | |

| Rest of Africa |

Key Questions Answered in the Report

How large will the Africa food flavor market be by 2031?

It is projected to reach USD 1,471.52 million by 2031, growing at a 4.50% CAGR from 2026.

Which segment grows fastest within African flavor applications?

Beverages post the highest forecast CAGR at 5.78%, fueled by energy drinks and RTD cocktails.

Why do synthetic flavors still dominate African demand?

They offer stable pricing and reliable supply chains, critical advantages in countries with volatile exchange rates.

Which country is the fastest-growing market?

Egypt is expected to expand at a 5.29% CAGR due to export-focused food processing and supportive policies.

Page last updated on: