Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 75.92 Billion |

| Market Size (2026) | USD 79.81 Billion |

| Market Size (2031) | USD 102.43 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Africa Foodservice Market Analysis by Mordor Intelligence

The African foodservice market size is expected to grow from USD 75.92 billion in 2025 to USD 79.81 billion in 2026 and is forecast to reach USD 102.43 billion by 2031 at 5.12% CAGR over 2026-2031. The African foodservice market is expanding rapidly, driven by urbanization, a youthful population, and technological advancements. Urban migration and busier lifestyles are increasing demand for convenient dining options like Quick-Service Restaurants (QSRs) and Cloud Kitchens. As of 2024, Africa's urbanization rate was nearly 45.5%, according to the World Bank[1]Source: World Bank, "Urbanization rate in Africa", data.worldbank.org. Rising disposable incomes among the growing middle class further enable frequent dining out and access to diverse, quality meals. Technological adoption, including smartphones and food delivery apps, is transforming the market. For example, in January 2025, KFC introduced a WhatsApp ordering system in South Africa to reduce data costs and improve accessibility. The rise of cloud kitchens, highlighted by the Cloud Kitchen Convention in April 2025, reflects the industry's shift toward efficiency. Changing consumer preferences for healthier, high-quality options are driving menu innovation, such as Food Service India's Ramadan-special Haleem Grain Base launched in March 2025. Additionally, growth in tourism and hospitality supports the market, with international brands like McDonald's and local players such as Famous Brands Limited and Vida e Caffè expanding to capitalize on this evolving landscape.

Key Report Takeaways

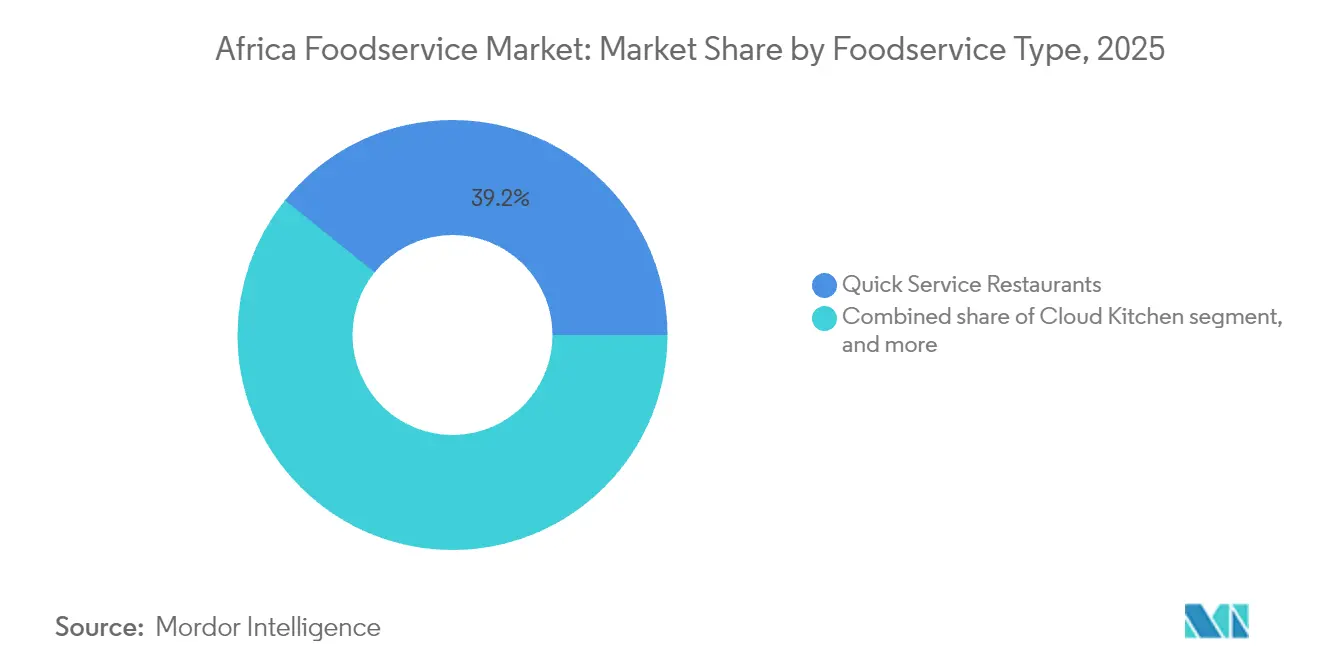

- By foodservice type, quick-service restaurants held a 39.22% revenue share of the African foodservice market in 2025, while cloud kitchens are expected to advance at a 7.42% CAGR through 2031.

- By outlet format, independent operators led the Africa foodservice market with 68.30% of the market share in 2025; chained outlets, on the other hand, recorded the fastest growth at an 7.73% CAGR from 2026 to 2031.

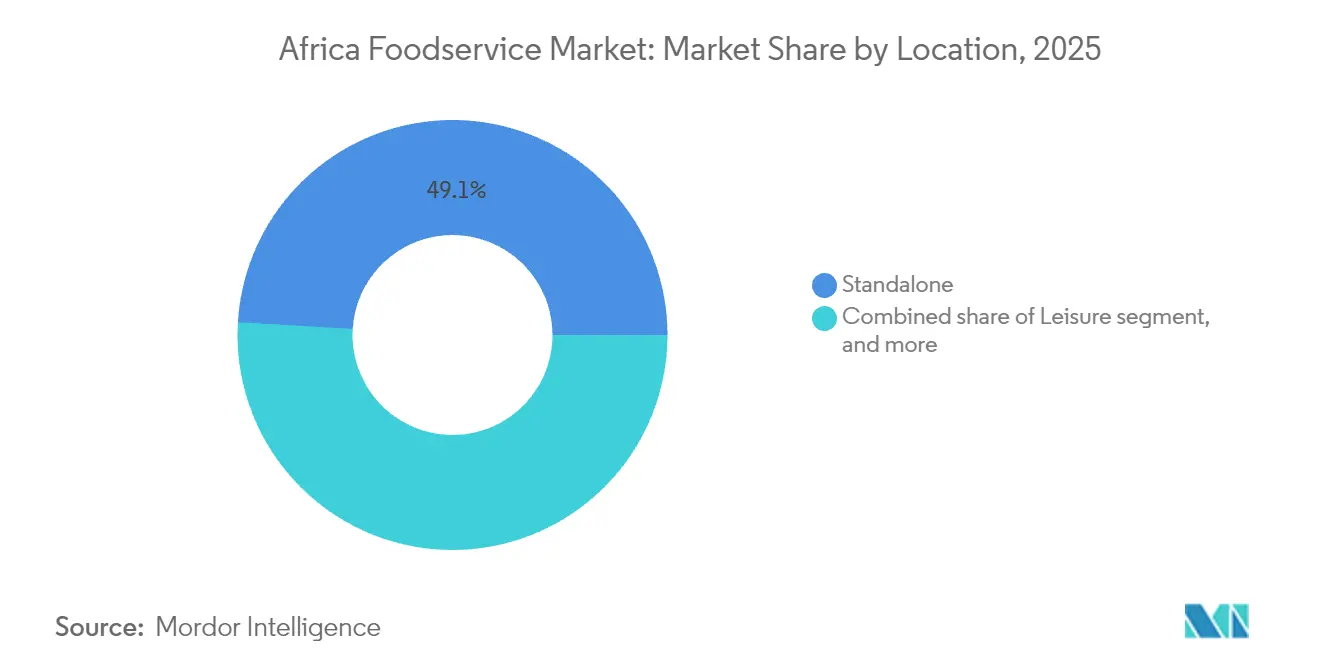

- By location, standalone sites accounted for 49.05% of the Africa foodservice market size in 2025, whereas leisure-anchored outlets are projected to expand at a 5.86% CAGR by 2031.

- By service type, dine-in represented 75.95% of 2025 transactions, but delivery is forecast to log a 7.05% CAGR through 2031.

- By geography, South Africa led the African foodservice market with 32.40% in 2025; Nigeria posted the fastest expansion at a 6.45% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Africa Foodservice Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urban middle-class expansion and rising disposable income | +1.8% | Nigeria, Kenya, Ghana, Ethiopia; spillover to Côte d'Ivoire, Tanzania | Long term (≥ 4 years) |

| Proliferation of mobile ordering and delivery platforms is accelerating off-premise sales | +1.5% | Nigeria (Lagos, Abuja), South Africa (Johannesburg, Cape Town), Kenya (Nairobi), Ghana (Accra) | Medium term (2-4 years) |

| Expansion of malls and formal retail anchors, creating foodservice space | +0.9% | South Africa, Nigeria, Kenya; early gains in Accra, Kigali, Dar es Salaam | Medium term (2-4 years) |

| AfCFTA-enabled intra-African supply-chain integration is lowering sourcing costs | +0.7% | Global (pan-African corridors), with early adoption in the East African Community and ECOWAS zones | Long term (≥ 4 years) |

| Surge in cold-chain investment improving perishables distribution reach | +0.8% | Nigeria, Kenya, South Africa, Ethiopia; secondary gains in Ghana, Rwanda | Medium term (2-4 years) |

| Renewable-energy-powered kitchens mitigating load-shedding risk | +0.5% | South Africa (Gauteng, Western Cape), Nigeria (Lagos, Abuja), Kenya (Nairobi) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid urban middle-class expansion and rising disposable income

Rapid urban middle-class expansion and the corresponding rise in disposable income are primary catalysts for the African foodservice market's growth, altering consumption patterns across the continent. As more people move to urban centers, faster-paced lifestyles increase reliance on convenient dining solutions like Quick-Service Restaurants (QSRs) and online delivery services. This shift coincides with a growing middle class allocating more discretionary income to leisure dining and diverse culinary experiences. The OECD-FAO Agricultural Outlook 2024-2033 highlights how urbanization drives food system transformation and demand for processed, diverse food items globally, including in Africa. Private sector entities are adapting with innovations; for instance, McDonald's increasingly uses app-based pickup systems to reduce reliance on third-party platforms and address demands for convenience and efficiency. These examples illustrate the link between rising spending power and the boom in accessible, varied foodservice options.

Proliferation of mobile ordering and delivery platforms accelerating off-premise sales

Mobile ordering and delivery platforms are rapidly transforming the African foodservice market, capitalizing on widespread smartphone use and a growing demand for convenience. As urban consumers increasingly turn to digital ordering, dining habits are shifting from traditional dine-in experiences to delivery and takeaway services. For example, the Global System for Mobile Communications Association projected a 50% mobile penetration rate in Sub-Saharan Africa by 2025[2]Source: Global System for Mobile Communications Association, "The Mobile Economy: Sub-Saharan Africa", gsma.com. Additionally, the industry's growth has been fueled by strategic partnerships between restaurants and aggregators, with major players such as Jumia Foods, Uber Eats, Bolt Foods, and Glovo leading the charge in key markets like Nigeria, Kenya, and South Africa.

Expansion of malls and formal retail anchors creating foodservice space

The expansion of malls and formal retail anchors is creating essential, structured foodservice spaces, thereby accelerating the growth of the African foodservice market by catering to the modern urban consumer's demand for convenience and integrated lifestyle experiences. These developments provide high-footfall, controlled environments that are attractive to both international chains seeking standardized operations and local brands aiming to scale within organized settings. Specific instances illustrate this expansion: Pret A Manger (UK-based grab-and-go brand) entered the South African market in February 2025 via a licensing deal with Millat Group, opening its first store in Johannesburg and planning further outlets in major cities within mall and high-street locations, leveraging the existing formal retail infrastructure. Furthermore, the overall trend of companies like Famous Brands Limited (which owns Mugg & Bean, Steers, Debonairs Pizza, etc.) continuing to diversify their portfolios and expand their presence within these formal retail and leisure locations underscores how mall expansion directly translates into structured growth opportunities for the foodservice sector across the continent.

AfCFTA-enabled intra-African supply-chain integration lowering sourcing costs

The integration of intra-African supply chains enabled by the African Continental Free Trade Area (AfCFTA) is set to lower sourcing costs, driving growth in the foodservice market by reducing tariffs and non-tariff barriers that have historically made intra-continental trade more expensive than external imports. The AfCFTA aims to eliminate 90% of tariffs and harmonize customs policies, fostering regional value chains in the agri-food sector, where previous intra-African tariffs averaged 18%. The OECD-FAO Agricultural Outlook 2024-2033 projects that such trade liberalization will boost regional agri-food trade, increase household incomes, and enhance purchasing power for diverse food options. While implementation faces challenges, recent developments highlight progress: Afreximbank reported in 2024 that intra-African trade rose to USD 220.3 billion, reflecting stronger regional economic linkages. The expansion of the Pan-African Payment and Settlement System (PAPSS) through 2024-2025 is also critical, reducing transaction costs and foreign exchange risks for cross-border trade. These financial improvements, along with private sector initiatives like the Worldwide Brewing Alliance's commitment to sourcing more local raw materials, are creating a more efficient supply chain landscape that benefits the African foodservice market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented informal sector complicating food-safety compliance | -0.6% | Nigeria, Ghana, Kenya, Ethiopia; concentrated in peri-urban zones | Long term (≥ 4 years) |

| High food inflation is eroding consumer purchasing power | -1.2% | Nigeria, Ghana, Kenya, Ethiopia; acute in import-dependent markets | Short term (≤ 2 years) |

| Persistent power outages and energy-price volatility | -0.9% | South Africa (Gauteng, KwaZulu-Natal), Nigeria (Lagos, Abuja), Ghana (Accra) | Medium term (2-4 years) |

| Talent shortages in digital logistics and food-safety technology | -0.4% | Nigeria, Kenya, South Africa; spillover to Ghana, Rwanda | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented informal sector complicating food-safety compliance

The fragmented and large-scale nature of Africa's informal foodservice sector restrains market growth by complicating food-safety compliance and deterring consumers seeking formal hygiene assurances. This sector, which dominates food market demand in sub-Saharan Africa, operates outside formal regulatory frameworks due to high business turnover, vendor mobility, and lack of infrastructure like potable water and waste disposal. These conditions lead to inconsistent food safety knowledge and practices, contributing to a high burden of foodborne illnesses. Government and association sources highlight these challenges; for instance, a 2025 NIH study on Namibian informal markets found moderate food safety knowledge but poor practices, such as inadequate temperature control. Similarly, a 2024 PMC analysis of South Africa's food safety framework noted the “complexity and fragmentation of the regulatory landscape,” complicating enforcement. Initiatives like the EU-funded FS4Africa project, launched in January 2024, aim to address issues like microbial contamination and weak traceability. However, persistent safety concerns and regulatory ambiguity limit consumer trust and hinder formal foodservice operators from establishing uniform safety standards across the market.

High food inflation eroding consumer purchasing power

High food inflation significantly restrains the African foodservice market by eroding consumer purchasing power, forcing households to prioritize essential food items over discretionary spending like dining out or ordering delivery. In many African nations, food items dominate the consumer price index (CPI), meaning rapid cost increases disproportionately impact household budgets. This economic pressure drives consumers to trade down to cheaper alternatives, reduce dining frequency, or revert to home cooking, suppressing sales and revenue for formal foodservice operators (QSRs, FSRs, Cafes/Bars). Government and association sources highlight this issue; the World Bank’s April 2025 Africa Pulse report identifies food price inflation as a key short-term challenge to economic stability and poverty reduction, with several countries facing double-digit food inflation rates that hinder non-essential sectors like commercial foodservice. Countries like Nigeria and South Africa experienced severe food price surges due to currency devaluation, infrastructure challenges, and global supply chain disruptions. Nigeria's food inflation rate reached nearly 40% in early 2025, according to the National Bureau of Statistics (NBS)[3]Source: National Bureau of Statistics, "CPI and Inflation Report June 2024", nigerianstat.gov.ng. In South Africa, the Bureau for Economic Research (BER) and local industry bodies reported in 2024 that restaurant and fast-food price inflation often exceeded the general CPI for food at home, forcing operators to balance passing costs onto consumers (risking lost business) and absorbing costs (eroding margins). These trends show that high food inflation creates an environment where affordability becomes a primary concern, limiting the market's growth potential despite demographic drivers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Foodservice Type: Cloud Kitchens Redefine Capital Efficiency

Cloud kitchens are forecast to expand at a 7.42% CAGR from 2026 to 2031, the fastest growth among foodservice types, as operators exploit delivery aggregators to test menu concepts without committing to high-street leases that can consume 15% to 20% of revenue in tier-1 cities. Quick-Service Restaurants held 39.22% of the market in 2025, anchored by international chains such as KFC, McDonald's, and Domino's, that benefit from global supply-chain scale and marketing budgets that local competitors cannot match. Full-Service Restaurants, spanning Asian, European, Middle Eastern, and North American cuisines, are growing steadily as urban professionals seek experiential dining, yet their capital intensity and labor costs limit scalability compared to quick-service formats. Cafes and Bars, including specialist coffee shops and juice bars, are carving niches in mall food courts and office districts, where foot traffic justifies premium pricing for artisanal beverages.

Yum! Brands opened approximately 2,900 KFC restaurants globally in 2024, with Africa representing a priority growth corridor where same-store sales grew 15% in fiscal 2023, driven by value-meal promotions and mobile-ordering integration, according to the Yum! Brands Annual Report 2024. McDonald's plans to reach 50,000 restaurants worldwide by 2027, with Africa and the Middle East targeted for 300 to 400 new openings, emphasizing drive-thru formats that reduce dine-in labor costs and accelerate order throughput, according to the McDonald's Corporation Annual Report 2024. Cloud kitchens in Lagos and Nairobi are leveraging platforms like Chowdeck and Glovo to operate multiple virtual brands, burgers, sushi, and salads from a single kitchen, a strategy that amortizes fixed costs across diverse revenue streams and hedges against single-cuisine demand volatility. Bakeries and ice-cream parlors within the quick-service segment are benefiting from impulse-purchase dynamics, particularly in malls where families allocate discretionary spending to treats rather than full meals, a behavioral pattern that persists even during inflationary cycles.

By Outlet: Chained Formats Gain Share Through Standardization

Chained outlets are projected to grow at an 7.73% CAGR from 2026 to 2031, surpassing the growth of independent outlets, which hold a 68.30% market share in 2025. Chains benefit from standardized operating procedures, centralized procurement, and digital loyalty programs, which independents struggle to replicate. Independent outlets dominate numerically due to lower capital and regulatory requirements, but their fragmentation weakens supplier bargaining power and exposes them to input-cost shocks, eroding margins. Spur Corporation, with 726 restaurants in 15 countries, opened 21 South African and 12 international outlets in the first half of fiscal 2025, targeting secondary cities with lower competition and lease rates 30% to 40% below Johannesburg or Cape Town, as per Spur Corporation's Interim Results 2025. Famous Brands closed 47 underperforming outlets in the first half of 2024, including 14 Steers, 11 Fishaways, and 5 Debonairs, to focus on high-traffic locations and delivery-optimized formats, according to Famous Brands' Interim Results 2024.

Restaurant Brands International acquired Carrols Restaurant Group, a 1,017-unit Burger King franchisee, for USD 1 billion in May 2024, signaling a shift toward ownership in high-growth markets where operational control justifies capital investment. In South Africa, Nando's, with approximately 300 outlets and a ZAR 28 billion (USD 1.5 billion) brand value, secures prime mall locations ahead of smaller competitors. Independent operators are forming buying cooperatives to negotiate bulk discounts on essentials like cooking oil, flour, and packaging, narrowing but not eliminating the cost gap with chains. Digital ordering is another challenge; chains invest in proprietary apps and CRM systems to track customer preferences and automate promotions, while independents rely on third-party aggregators that charge 20% to 30% commissions and control customer relationships, a disadvantage that compounds over time.

By Location: Leisure Anchors Capture Experiential Spending

Leisure-based outlets, anchored in malls, entertainment complexes, and mixed-use developments, are projected to grow at a 5.86% CAGR from 2026 to 2031, as developers allocate 25% to 30% of gross leasable area to foodservice to boost foot traffic and extend dwell times. Standalone outlets held 49.05% of the market share in 2025, benefiting from lower rent and operational flexibility, though they lack the captive traffic generated by malls and travel hubs. Lodging-based foodservice, concentrated in hotels and resorts, is recovering from pandemic disruptions but remains limited by occupancy rates in markets like Nigeria and Kenya. Retail-anchored outlets, embedded in supermarkets and department stores, are growing as grocers experiment with in-store dining to compete with e-commerce and justify physical store visits. Travel-based outlets, located in airports and bus terminals, command premium pricing due to captive demand but face regulatory challenges around lease terms and revenue-sharing agreements with transport authorities.

South Africa's mall development pipeline includes eight new centers scheduled to open between 2025 and 2027, adding 120,000 square meters of retail space, primarily in Gauteng and the Western Cape. According to the South African Property Owners Association, foodservice tenants have pre-leased 30% of the available units. Kenya's Two Rivers Mall in Nairobi, which opened additional phases in 2024, allocated 15,000 square meters to restaurants and cafes, attracting international franchises such as KFC, Subway, and Domino's, alongside local concepts like Java House and Artcaffe. Nigeria's Jabi Lake Mall in Abuja and Ikeja City Mall in Lagos are undergoing expansions that will add 50 foodservice units by 2026, targeting middle-income families who view mall visits as weekend entertainment rather than purely transactional shopping trips. Standalone outlets in peri-urban areas are leveraging lower rents, ranging from approximately USD 8 to USD 12 per square meter, compared to USD 25 to USD 40 in malls, to offer larger seating areas and parking. This value proposition appeals to families and groups who prioritize space and affordability over mall amenities.

By Service Type: Delivery Gains as Congestion Monetizes Convenience

Delivery service is forecast to grow at a 7.05% CAGR from 2026 to 2031, driven by smartphone penetration, which reached 52% in Sub-Saharan Africa in 2024, and delivery platforms subsidizing rider wages to build network density. Dine-in service accounted for 75.95% of transactions in 2025, reflecting cultural preferences for communal eating and the experiential value of restaurant ambiance. However, its share is declining as urban congestion and time scarcity shift demand toward off-premise formats. Takeaway service appeals to price-conscious consumers who avoid delivery fees but lack time for dine-in meals, a segment quick-service chains target with drive-thru lanes and mobile-order-ahead systems. Chowdeck's expansion into Ghana in May 2025, following its NGN 30 billion (USD 20 million) in gross merchandise value during 2024, highlights how delivery platforms are replicating Lagos playbooks in secondary markets with nascent competition.

Glovo's exit from Ghana in May 2024, citing profitability pressures, underscores the unit economics challenge for delivery aggregators in markets where average order values remain below USD 10 and rider wages consume 40% to 50% of gross transaction value Bloomberg. Prosus, which operates food-delivery assets across Africa, reported 15% year-on-year growth in its food-delivery segment in fiscal 2024. However, the division remains unprofitable as it prioritizes market-share gains over margin expansion, according to the Prosus Annual Report 2024. Restaurants are responding by launching proprietary delivery fleets to bypass aggregator commissions; Food Concepts operates its own riders in Lagos and Abuja, reducing per-order costs by 18% and retaining customer data to inform menu development and promotional targeting. Dine-in operators are upgrading ambiance with live music, chef's tables, and Instagram-worthy interiors to justify premium pricing and differentiate from delivery-optimized competitors. This strategy works in affluent neighborhoods but struggles in price-sensitive markets where value outweighs experience.

Geography Analysis

South Africa held 32.40% of the Africa foodservice market in 2025, supported by a mature quick-service infrastructure, per-capita GDP of USD 6,500, and urbanization rates above 67%. However, the market faces challenges from Eskom's Stage 6 load-shedding, which has increased energy costs, and food inflation that, although moderating to 4.7% in September 2024, remains high for staples such as maize and cooking oil. Famous Brands closed 47 underperforming outlets in early 2024, while Spur Corporation opened 21 restaurants, focusing on secondary cities with lower lease rates. Renewable energy adoption is on the rise, with Famous Brands installing solar arrays at 12 outlets, reducing grid dependence by 60% and saving ZAR 45,000 (approximately USD 2,500) per site monthly. The Johannesburg Stock Exchange-listed foodservice sector is consolidating, with Bidcorp signaling readiness for acquisitions in fragmented markets.

Nigeria is projected to grow at a 6.45% CAGR from 2026 to 2031, driven by Lagos and Abuja's combined population of over 35 million and delivery platforms offering time-saving convenience. Despite food inflation of 34.8% in October 2024, quick-service chains are launching affordable combo meals to retain customers. Food Concepts is expected to expand to over 240 stores by 2025, including an outlet at Lagos Murtala Muhammed Airport. Chowdeck surpassed NGN 30 billion (USD 20 million) in gross merchandise value in 2024 and raised USD 2.5 million to expand its rider network. Frequent power-grid collapses in 2024 are pushing operators to invest in inverter systems and solar panels, favoring chains over independents. The federal government’s partnership with private firms to install solar-powered cold-storage hubs is improving perishables distribution, benefiting quick-service chains.

Kenya, Ghana, and Ethiopia are experiencing similar trends driven by urbanization, mobile-money adoption, and infrastructure investment. Kenya's electricity tariffs rose by 23% in 2024, increasing utility costs for restaurants, yet Nairobi's workforce continues to drive demand for lunch deliveries. The Nairobi-Mombasa corridor added 2,500 refrigerated trucks in 2024, reducing transit times for perishables and enabling restaurants in Nairobi to offer coastal seafood. Ghana's 28% cedi depreciation in 2024 inflated import costs, forcing quick-service chains to use local alternatives, which risks damaging brand loyalty. Chowdeck expanded into Ghana in May 2025, targeting the middle-income neighborhoods of Accra. Ethiopia's diaspora remittances reached USD 5.1 billion in 2024, boosting spending in Addis Ababa, where international fast-food brands are opening flagship stores. The Rest of Africa segment, including markets such as Senegal and Tanzania, remains fragmented but is attracting franchisors seeking first-mover advantages. Spur Corporation opened 12 international outlets in early fiscal 2025, including locations in Mauritius, Zambia, and Botswana.

Competitive Landscape

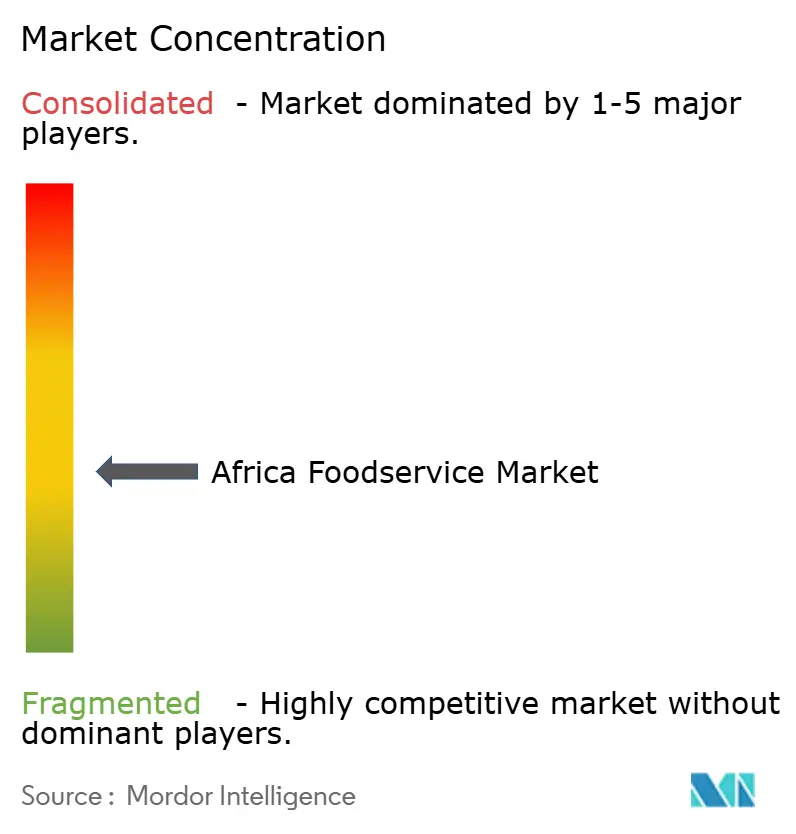

The Africa foodservice market is fragmented, with international chains like Yum! Brands, McDonald's, and Restaurant Brands International hold significant market shares. Regional players such as Famous Brands, Spur Corporation, and Nando's dominate outlet numbers but generate lower revenue due to smaller average ticket sizes. Competition is intensifying as chains implement standardized operations, centralized procurement, and digital loyalty programs, which independent operators struggle to match. Delivery aggregators like Chowdeck and Glovo are disrupting traditional dine-in traffic by capturing transaction data that informs menu development and promotions. Opportunities exist in tier-2 and tier-3 cities, where lease rates are lower and competition is less intense. However, challenges such as unreliable power, fragmented cold chains, and limited digital payment penetration complicate operations and delay profitability. Cloud kitchens and local quick-service chains like Food Concepts are emerging as disruptors, leveraging cost efficiencies and hyperlocal knowledge to compete effectively with international franchises.

Technology is transforming the competitive landscape. Yum! Brands' Byte platform processed over USD 30 billion in digital sales globally in 2024, integrating mobile ordering, loyalty rewards, and predictive analytics to optimize labor and inventory. McDonald's loyalty program reached 175 million active users across 60 markets in 2024, driving a 12% to 15% increase in visit frequency among enrolled customers through personalized promotions. Restaurant Brands International's USD 1 billion acquisition of Carrols Restaurant Group in May 2024 highlights a shift toward owning operations in high-growth markets, a strategy that increases capital requirements but enhances operational control and margin capture. These advancements are setting new benchmarks for efficiency and customer engagement in the foodservice market.

Regulatory compliance is becoming a key differentiator in the market. Formal operators invest in HACCP certifications, traceability systems, and staff training to meet food safety standards enforced by bodies like Nigeria's NAFDAC and South Africa's Department of Health. These investments create reputational advantages for chains targeting middle-income and affluent consumers who prioritize hygiene and brand trust. Informal vendors, while avoiding these costs, lack the credibility to compete effectively in these segments. As the market evolves, adherence to regulatory standards and the ability to build consumer trust will play a critical role in shaping competitive dynamics across Africa's foodservice landscape.

Africa Foodservice Industry Leaders

-

Famous Brands Limited

-

Yum! Brands Inc.

-

McDonald’s Corporation

-

Restaurant Brands International

-

Nando’s Group Holdings

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Chowdeck made its debut in Ghana, marking its first venture beyond Nigeria. The platform is zeroing in on the middle-income neighborhoods of Accra, bolstering its presence with a fleet of riders and collaborations with local eateries. This expansion comes on the heels of Chowdeck achieving a milestone of over NGN 30 billion (USD 20 million) in gross merchandise value in 2024. Notably, Chowdeck's strategy mirrors its successful playbook from Lagos, stepping into a market vacated by Glovo in May 2024, which cited profitability challenges as its reason for exit.

- February 2025: Restaurant Brands International completed its acquisition of Burger King China, adding 1,200 outlets to its portfolio and signaling a strategy to own rather than franchise in high-growth markets. The deal follows RBI's June 2024 acquisition of Popeyes Louisiana Kitchen China (PLK China), which added 400 restaurants, and its May 2024 purchase of Carrols Restaurant Group, a 1,017-unit Burger King franchisee in the United States.

- August 2024: Glovo launched in-app advertising in Nigeria, enabling restaurants to promote menu items and limited-time offers directly within the platform. The feature monetizes Glovo's user base without increasing delivery commissions, a strategic pivot following the company's exit from Ghana in May 2024 due to profitability pressures.

Africa Foodservice Market Report Scope

By Foodservice Type

| Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | ||

| Juice/Smoothie/Desserts Bars | ||

| Specialist Coffee and Tea Shops | ||

| Cloud Kitchen | ||

| Full Service Restaurants | By Cuisine | Asian |

| European | ||

| Latin American | ||

| Middle Eastern | ||

| North American | ||

| Other FSR Cuisines | ||

| Quick Service Restaurants | By Cuisine | Bakeries |

| Burger | ||

| Ice Cream | ||

| Meat-based Cuisines | ||

| Pizza | ||

| Other QSR Cuisines |

By Outlet

| Chained Outlets |

| Independent Outlets |

By Location

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

By Service Type

| Dine-In |

| Takeaway |

| Delivery |

By Geography

| Nigeria |

| Ghana |

| Ethiopia |

| Kenya |

| South Africa |

| Rest of Africa |

| By Foodservice Type | Cafes and Bars | By Cuisine | Bars and Pubs |

| Cafes | |||

| Juice/Smoothie/Desserts Bars | |||

| Specialist Coffee and Tea Shops | |||

| Cloud Kitchen | |||

| Full Service Restaurants | By Cuisine | Asian | |

| European | |||

| Latin American | |||

| Middle Eastern | |||

| North American | |||

| Other FSR Cuisines | |||

| Quick Service Restaurants | By Cuisine | Bakeries | |

| Burger | |||

| Ice Cream | |||

| Meat-based Cuisines | |||

| Pizza | |||

| Other QSR Cuisines | |||

| By Outlet | Chained Outlets | ||

| Independent Outlets | |||

| By Location | Leisure | ||

| Lodging | |||

| Retail | |||

| Standalone | |||

| Travel | |||

| By Service Type | Dine-In | ||

| Takeaway | |||

| Delivery | |||

| By Geography | Nigeria | ||

| Ghana | |||

| Ethiopia | |||

| Kenya | |||

| South Africa | |||

| Rest of Africa | |||

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms