Adipic Acid Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

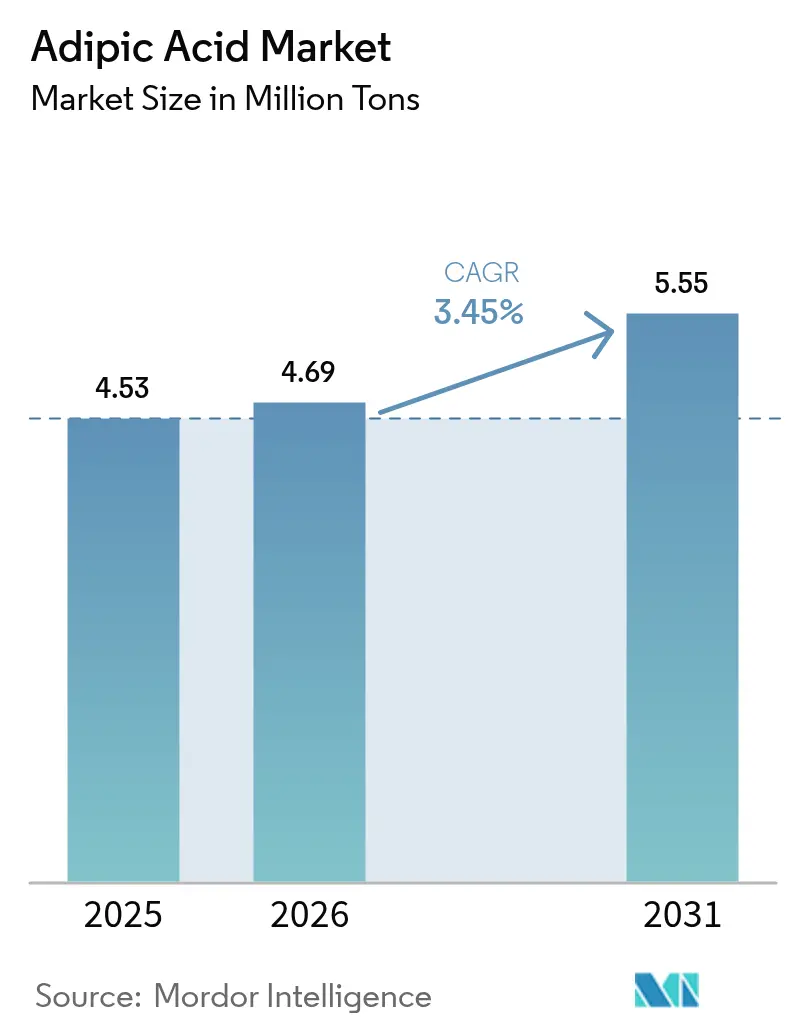

| Market Volume (2026) | 4.69 Million tons |

| Market Volume (2031) | 5.55 Million tons |

| Growth Rate (2026 - 2031) | 3.45% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Adipic Acid Market Analysis by Mordor Intelligence

The Adipic Acid market size is expected to grow from 4.53 million tons in 2025 to 4.69 million tons in 2026 and is forecast to reach 5.55 million tons by 2031 at 3.45% CAGR over 2026-2031. Emission regulations, automotive light-weighting, and the appeal of bio-fermentation pathways are the pivotal forces shaping this trajectory. Asia-Pacific remains the production and consumption epicenter, while North America and Europe advance low-emission technologies that can meet tightening policy targets. Disruptive strides in fermentation are narrowing cost gaps with nitric-acid oxidation, and strategic capital flows into integrated nylon 66 capacity signal confidence in downstream demand. Feedstock volatility and scale-up risks temper optimism, yet regulatory tailwinds and end-market diversification keep the adipic acid market on a clear growth path.

Key Report Takeaways

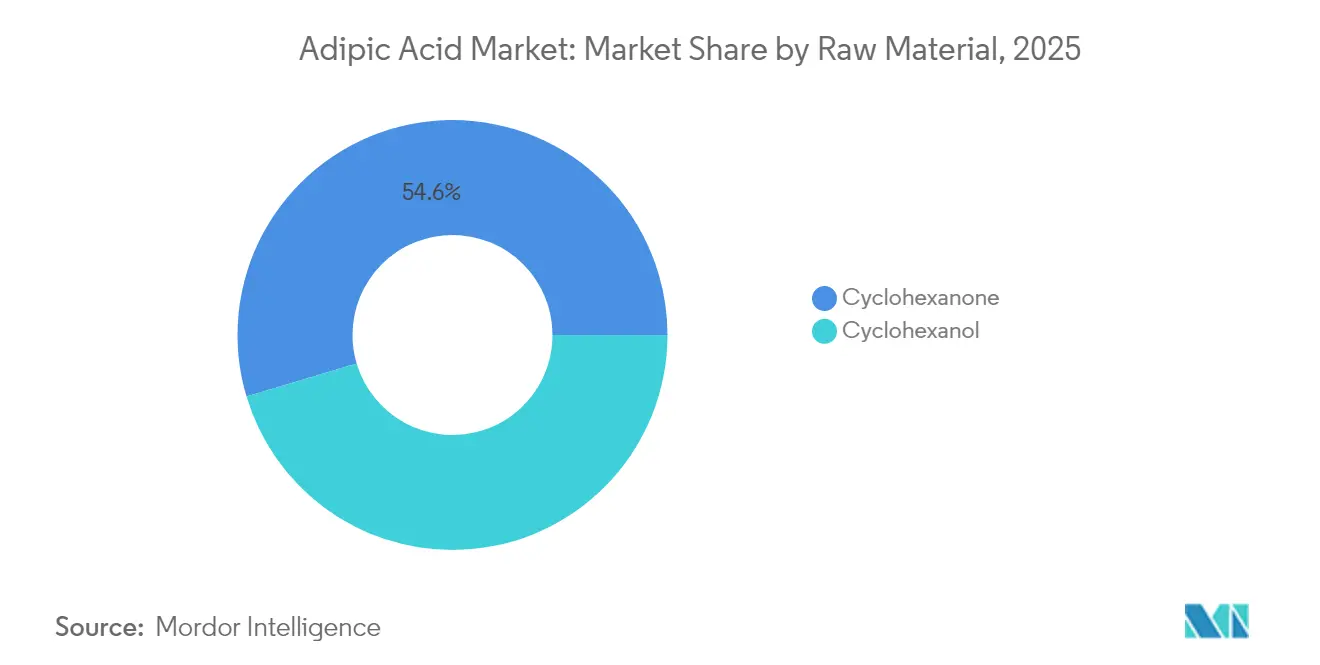

- By raw material, cyclohexanone led with 54.62% of adipic acid market share in 2025, while cyclohexanol is projected to register the fastest 4.78% CAGR through 2031.

- By production process, nitric-acid oxidation accounted for 90.98% of adipic acid market share in 2025; bio-fermentation is set to advance at a 4.82% CAGR over 2026-2031.

- By end product, nylon 66 fibers held 35.22% share of the adipic acid market size in 2025, whereas polyurethanes are tracking the highest 5.26% CAGR to 2031.

- By application, plasticizers accounted for 28.66% of adipic acid market share in 2025, while food additives is projected to register the fastest 4.61% CAGR through 2031.

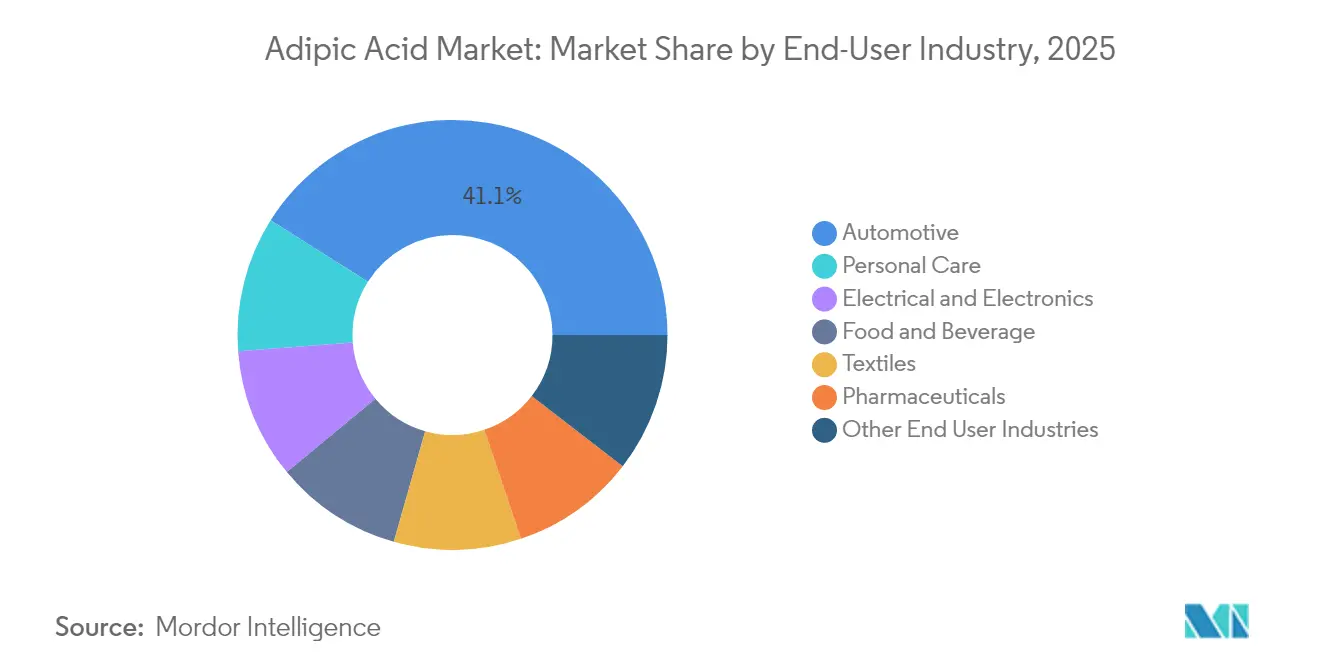

- By end-user industry, the automotive sector retained 41.05% adipic acid market share in 2025, yet personal care leads growth with a 4.63% CAGR forecast.

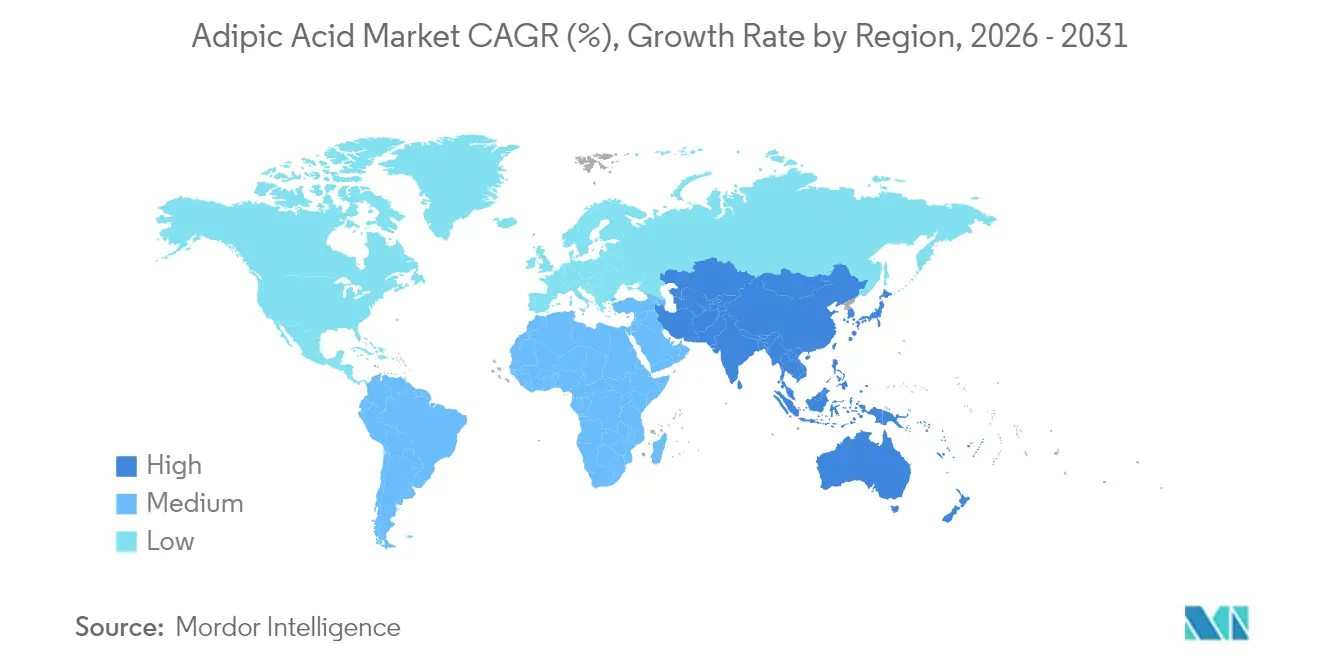

- By geography, Asia-Pacific dominated with 46.88% share in 2025 and is poised to expand at 4.98% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Adipic Acid Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand for Nylon 66 in e-mobility lightweight parts | +0.80% | Asia-Pacific and North America | Medium term (2-4 years) |

| Shift from metal to plastics in EV battery casings | +0.60% | China and North America | Medium term (2-4 years) |

| Growth of energy-efficient construction foams | +0.50% | North America and Europe | Long term (≥ 4 years) |

| Expansion of textile filament capacity | +0.40% | Asia-Pacific and South America | Short term (≤ 2 years) |

| Emergence of bio-based adipic acid for compostable films | +0.30% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Demand for Nylon 66 in E-Mobility Lightweight Parts

Electric vehicle manufacturers are embracing nylon 66 to reduce vehicle mass and extend driving range, which elevates consumption of adipic acid-based intermediates. INVISTA’s project to double Shanghai nylon 66 output to 400,000 tons places production close to adiponitrile feedstock, lowering logistics costs and shortening supply chains. BASF’s 260,000-ton hexamethylenediamine unit in France expands regional self-sufficiency for critical monomers[1]BASF, “BASF Builds World-Scale Hexamethylenediamine Plant in France,” basf.com . Battery thermal-management and structural modules rely on nylon 66 for heat resistance that metals cannot offer at comparable weight. Recent unplanned outages at adiponitrile plants in China highlighted supply vulnerability and prompted producers to integrate upstream operations for risk mitigation.

Shift from Metal to Plastics in EV Battery Casings

Automakers are converting metal battery covers to polymer solutions that combine weight savings with enhanced design flexibility. Polyurethane foams derived from adipic acid now insulate casings while dissipating heat, and Covestro’s ISCC+ certified raw materials illustrate the industry’s sustainability pivot. United States automotive producers consumed 142 million lb of polyurethane coatings in 2023, a scale that underscores the near-term revenue upside for adipic acid suppliers. Complex geometries are achievable through plastics, enabling streamlined battery pack architectures. Premium pricing for high-performance polymers offsets higher raw-material costs and encourages capacity additions that stabilize the adipic acid market.

Growth of Energy-Efficient Construction Foams

Tighter building-code mandates across North America and Europe are pushing demand for rigid and spray polyurethane foams that require adipic acid-derived polyols. High R-values, flame retardancy, and sound-damping dampening position these foams as multi-functional solutions for net-zero buildings. Bio-based pathways employing vegetable oils and lignin attract green-building certification points. Multifunctionality, including electromagnetic interference shielding, widens the application envelope to smart-home infrastructure. Global insulation retrofits, especially under European Renovation Wave programs, sustain long-term volume growth for the adipic acid market.

Expansion of Textile Filament Capacity

Asian producers are scaling nylon fibers for technical textiles that demand abrasion resistance and moisture management. Research on biobased PA56 reveals up to 50% lower fossil resource needs relative to conventional nylons. Wool/PA56 blends show promise in automotive interiors where comfort and durability converge. Controlled copolymer crystallization tailors mechanical properties for high-end performance wear. Hyosung’s USD 1 billion Vietnam project for biobased 1,4-butanediol underpins fiber diversification strategies. Heightened textile innovation diversifies the downstream base for the adipic acid market and shields producers from automotive cyclicality.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in cyclohexanone feedstock prices | -0.70% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Scale-up challenges for bio-fermentation pathways | -0.40% | North America and Europe | Medium term (2-4 years) |

| Geopolitical risk to nitric-acid supply chains | -0.30% | Trade-dependent regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Cyclohexanone Feedstock Prices

Cyclohexanone accounts for roughly two-thirds of conversion costs; hence, price swings rapidly compress margins. Limited upstream diversification means unplanned outages or geopolitical shocks ripple through the value chain. Rising logistics and energy costs further destabilize total production economics, complicating long-term contracts. Vertical integration or alternative feedstocks such as bio-aromatics are gaining attention as resilience strategies. However, securing capital for upstream acquisitions is challenging when feedstock cycles remain unpredictable.

Scale-Up Challenges for Bio-Fermentation Pathways

While laboratory titers of cis,cis-muconic acid have reached 47.2 g/L, productivity declines markedly when processes scale beyond 150 L. Economic models projecting an adipic acid price of USD 2.60 kg hinge on ideal yields, which may not be met in early commercial plants. Microbial tolerance to high acid concentrations remains a central bottleneck, requiring strain engineering to reach 50-100 g/L thresholds. Historical bankruptcies such as BioAmber amplify investor caution, and regulatory reviews add timeline uncertainty. These hurdles slow but do not halt the transition toward bio-routes in the adipic acid market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Raw Material: Cyclohexanone Dominance Faces Bio-Based Disruption

Cyclohexanone controlled 54.62% adipic acid market share in 2025, confirming its entrenched role in nitric-acid oxidation. The adipic acid market size tied to cyclohexanone represents roughly half of global output, reinforcing the importance of stable supply chains. Cyclohexanol, however, is rising at 4.78% CAGR as producers deploy greener oxidation catalysts that slash nitrous oxide emissions. Catalyst designs featuring hydrogen peroxide achieve 92.3% conversion and 29.4% selectivity to adipic acid, reflecting substantial efficiency gains. Faradaic-efficient electrocatalysis that co-generates hydrogen gas at 93% efficiency presents an additional revenue stream and aligns with decarbonization targets.

Bio-aromatic concepts that valorize lignin can remove crude-derived intermediates from the chain altogether. Engineered Pseudomonas putida strains deliver 2.5 g/L adipic acid from lignin fragments and point toward future integration of biorefinery side-streams. Lifecycle assessments suggest a 58% CO2 reduction and 23% lower energy demand versus petrochemical routes, positioning such pathways as compliance tools under evolving carbon-pricing regimes. Although volumes remain small, successful commercialization could redraw raw-material economics within the adipic acid market.

By Production Process: Nitric-Acid Oxidation Maintains Control Despite Environmental Pressure

Nitric-acid oxidation constituted 90.98% of the adipic acid market in 2025 due to mature technology and sunk capital. The adipic acid market size linked to this process benefits from economies of scale but endures scrutiny over nitrous oxide emissions. Texas regulations limit NOx to 2.5 lb per ton, illustrating regional compliance burdens.

Bio-fermentation, despite holding only 4.82% CAGR momentum, is gathering commercial trials that run on glucose and xylose. When carbon costs are internalized, economic parity edges closer, particularly in regions with renewable-energy surpluses. Co-location with corn-ethanol plants can secure feedstock and utilities, further compressing variable cost. The competitive narrative hinges on whether fermentation can achieve the scale needed to drop fixed costs below incumbent asset levels.

By End Product: Polyurethanes Accelerate Past Traditional Nylon Applications

Nylon 66 fibers held 35.22% of 2025 sales, serving automotive, electronics, and industrial threads where tensile integrity is vital. Yet, polyurethanes are advancing at 5.26% CAGR as construction, refrigeration, and seating applications widen. Commercial builders favor high-density rigid foams with flame retardant and electromagnetic interference shielding, while auto OEMs exploit flexible foams for seating comfort. Mexico, a significant consumer of polyurethane globally, is driving the segment's growth.

Bio-based polyurethane trials using vegetable oils enable drop-in performance with improved carbon footprints. Demonstrated recyclability via chemical depolymerization furthers their circular credentials. Adipate plasticizers remain a niche but profitable offshoot for lubricant and coating applications. The larger product mix expands addressable markets, cushioning demand swings in any single downstream sector.

By Application: Food Additives Emerge as Unexpected Growth Driver

Plasticizers dominated with a 28.66% share in 2025, reinforcing the role of adipate esters in flexible PVC goods. Food additives, however, are gaining at a 4.61% CAGR as clean-label requirements spur the adoption of adipic acid as an acidulant in powdered beverages and desserts. WHO risk assessments confirm safe daily intake, removing regulatory barriers for formulators.

In coatings, adipic acid confers corrosion resistance and heat endurance valued in automotive and industrial finishes. Unsaturated polyester resins and synthetic lubricants contribute steady niche demand anchored by specialised performance needs. The diverse application portfolio broadens revenue channels for participants in the adipic acid market, aligning with resilience strategies that mitigate cyclic exposure.

By End-User Industry: Personal Care Accelerates Beyond Automotive Dominance

Automotive applications retained 41.05% of the 2025 volume on the back of e-mobility adoption and metal-to-plastic substitutions. Yet personal care is the fastest-growing end user with a 4.63% CAGR, propelled by consumer interest in sustainable formulations. Adipic acid esters provide emolliency and pH balance in skincare and hair products, and formulators value the ingredient’s low irritation profile.

Electrical and electronics lean on nylon 66’s insulation prowess, while textiles leverage performance fibers for functional apparel. Pharmaceuticals continue as a stable outlet for adipic acid in API synthesis. The broadened industry spread reduces sensitivity to any single macroeconomic cycle and underlines the strategic depth of the adipic acid market.

Geography Analysis

Asia-Pacific held 46.88% of global volume in 2025 and drives the fastest 4.98% CAGR as China scales capacity and India channels petrochemical investment into Gujarat corridors. Rapid adoption of catalytic destruction units has started to narrow the carbon gap between Chinese and Western producers. North America remains a stronghold for food-grade and high-purity grades of adipic acid. Ascend Performance Materials and AdvanSix operate fully integrated chains that benefit from shale-gas economics and strict U.S. emission controls, which favor producers with demonstrated compliance records. Fermentation pilots clustered in the Midwest leverage corn feedstock and renewable electricity from wind corridors. Europe’s policy focus on circularity is driving capital toward integrated assets that couple downstream resin plants with upstream monomers to minimize logistics emissions. BASF’s French hexamethylenediamine investment exemplifies a hub model that embeds sustainability into supply architecture. South America and the Middle East & Africa show emerging interest through infrastructure build-outs, yet political and economic volatility create hurdles that could delay large-scale investments. Together these dynamics illustrate a regionally stratified complexion that continues to shape global supply patterns in the adipic acid market.

Competitive Landscape

The adipic acid market shows moderate concentration with BASF, Ascend Performance Materials, and INVISTA accounting for a sizable installed capacity share. BASF’s decision to close Ludwigshafen adipic acid operations by end-2025 signals realignment toward higher-margin units and modern plants with lower emissions. INVISTA’s expanded Shanghai nylon 66 complex ties monomer and polymer production under one roof, harvesting economies of scope. Ascend capitalizes on feedstock integration to navigate cyclohexanone price volatility.

Bio-based challengers are partnering with established firms and fermentation tollers to commercialize organisms engineered for adipic acid production. Cost-curve parity depends on scaling above 50,000 t per year, a threshold that current pilot projects target before 2030. Intellectual-property filings reveal aggressive research into electrocatalytic oxidation catalysts and high-tolerance microbial strains, with patent races intensifying across China, the United States, and Europe.

Consolidation is underway as Lone Star Funds moves to acquire RadiciGroup’s specialty chemicals branch, signaling that private equity sees untapped synergies in a market transitioning toward higher specialty volumes. Market participants increasingly benchmark environmental performance in tender processes, so early adopters of low-emission technologies gain bidding advantages. Competitive intensity will likely hinge on the execution of scalable, cost-effective decarbonization strategies rather than capacity alone.

Adipic Acid Industry Leaders

BASF SE

Ascend Performance Materials

INVISTA

AdvanSix Inc.

Radici Partecipazioni SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2024: BASF has announced plans to discontinue adipic acid production at its Ludwigshafen site by the end of 2025. This decision aligns with a strategic review to enhance competitiveness amid changing market dynamics.

- November 2024: Toray Industries, Inc. and PTT Global Chemical Public Company Limited (GC) signed an MoU to explore the mass production of bio-based adipic acid from non-edible biomass. They aim for commercial production in Thailand and Japan by 2030 if viable.

Global Adipic Acid Market Report Scope

Adipic acid is a white, crystalline compound primarily used to produce nylon 6,6. It also creates polyurethanes as a reactant to form plasticizers, lubricant components, and polyester polyols. The adipic acid market is segmented by raw material, end product, application, end-user industry, and geography. By raw material, the market is segmented into cyclohexanol and cyclohexanone. By end product, the market is segmented into nylon 66 fibers, nylon 66 engineering resins, polyurethanes, adipate esters, and other end products. By application, the market is segmented into plasticizers, unsaturated polyester resins, wet paper resins, coatings, synthetic lubricants, food additives, and other applications. By end-user industry, the market is segmented into automotive, electrical and electronics, textiles, food and beverage, personal care, pharmaceuticals, and other end-user industries. The report also covers the market size and forecasts for the market in 15 countries across the globe. For each segment, the market sizing and forecasts have been done based on volume (kilotons).

| Cyclohexanol |

| Cyclohexanone |

| Nitric-acid Oxidation |

| Bio-fermentation |

| Nylon 66 Fibers |

| Nylon 66 Engineering Resins |

| Polyurethanes |

| Adipate Esters |

| Other End Products |

| Plasticizers |

| Unsaturated Polyester Resins |

| Wet Paper Resins |

| Coatings |

| Synthetic Lubricants |

| Food Additives |

| Other Applications |

| Automotive |

| Electrical and Electronics |

| Textiles |

| Food and Beverage |

| Personal Care |

| Pharmaceuticals |

| Other End User Industries |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Raw Material | Cyclohexanol | |

| Cyclohexanone | ||

| By Production Process | Nitric-acid Oxidation | |

| Bio-fermentation | ||

| By End Product | Nylon 66 Fibers | |

| Nylon 66 Engineering Resins | ||

| Polyurethanes | ||

| Adipate Esters | ||

| Other End Products | ||

| By Application | Plasticizers | |

| Unsaturated Polyester Resins | ||

| Wet Paper Resins | ||

| Coatings | ||

| Synthetic Lubricants | ||

| Food Additives | ||

| Other Applications | ||

| By End-user Industry | Automotive | |

| Electrical and Electronics | ||

| Textiles | ||

| Food and Beverage | ||

| Personal Care | ||

| Pharmaceuticals | ||

| Other End User Industries | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the adipic acid market?

The adipic acid market reached 4.69 million tons in 2026 and is projected to grow to 5.55 million tons by 2031.

Which region dominates the adipic acid market?

Asia-Pacific leads with 46.88% share and also posts the fastest 4.98% CAGR through 2031.

Why are polyurethanes the fastest-growing end product?

Rising demand for high-performance insulation and automotive interior foams is pushing polyurethane consumption at a 5.26% CAGR.

How are bio-fermentation routes impacting market dynamics?

Fermentation technologies growing at 4.82% CAGR promise lower emissions and comparable costs, challenging nitric-acid oxidation’s dominance.

What are the main restraints to market growth?

Cyclohexanone price volatility and technical scale-up challenges in bio-fermentation remain the key hurdles.

Page last updated on: